Leggings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

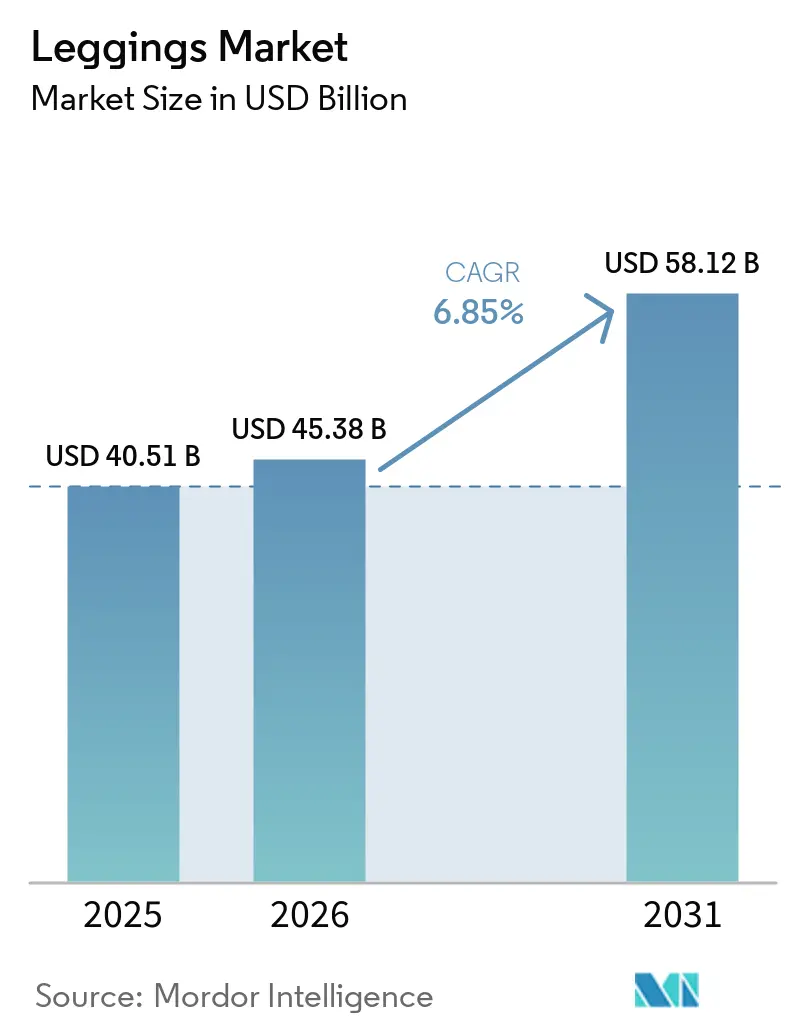

| Market Size (2026) | USD 45.38 Billion |

| Market Size (2031) | USD 58.12 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

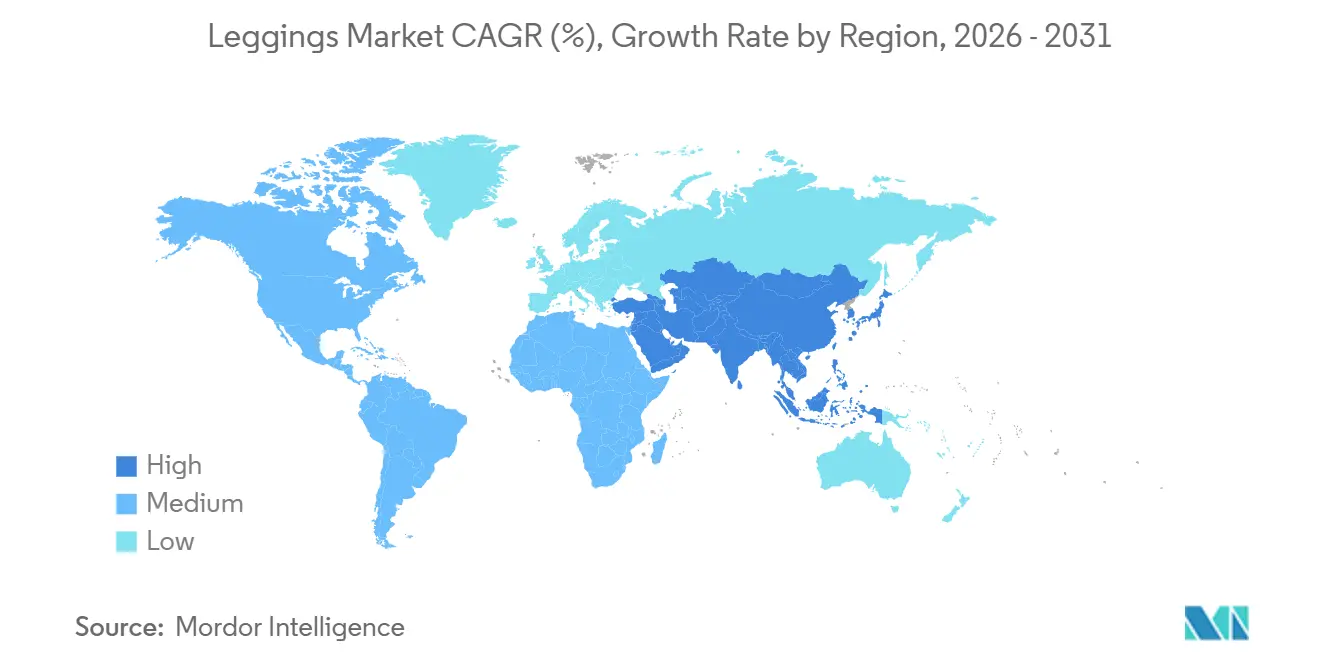

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Leggings Market Analysis by Mordor Intelligence

The leggings market size is expected to increase from USD 40.51 billion in 2025 to USD 45.38 billion in 2026 and reach USD 58.12 billion by 2031, growing at a CAGR of 6.85% over 2026-2031. The growth outlook reflects structural changes in day-to-day wardrobes as consumers gravitate toward garments that combine athletic performance with street-ready aesthetics. Heightened attention to personal wellness, continued hybrid work routines, and the normalization of moisture-wicking fabrics in offices and on travel corridors all underpin demand. Technical yarn innovations that improve stretch-recovery and recyclability are widening price bands, encouraging premium upselling while cutting waste. Alongside these factors, rising direct-to-consumer penetration is compressing time-to-market and elevating data-driven merchandising, allowing brands to serve micro-segments quickly.

Key Report Takeaways

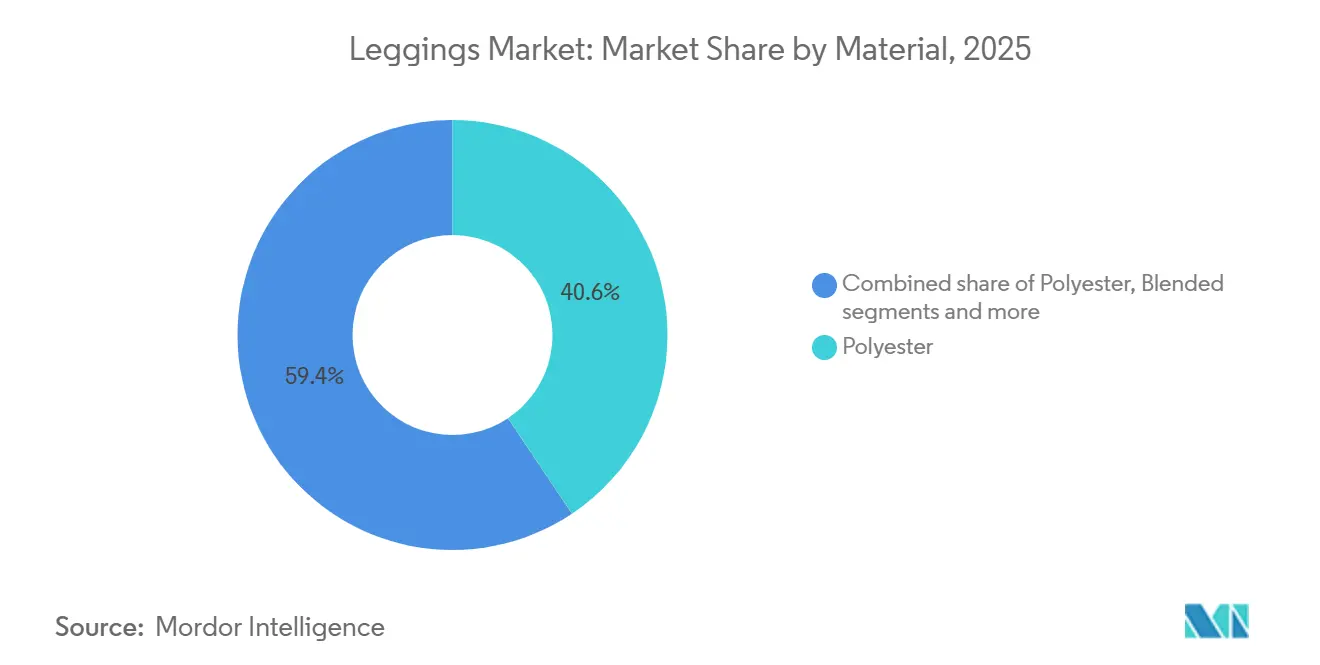

- By material, polyester secured 40.62% of the leggings market share in 2025, while blended fabrics are forecast to expand at a 7.54% CAGR through 2031.

- By end-user, women represented 70.26% of revenue in 2025; the men’s segment is projected to advance at an 8.21% CAGR over 2026-2031.

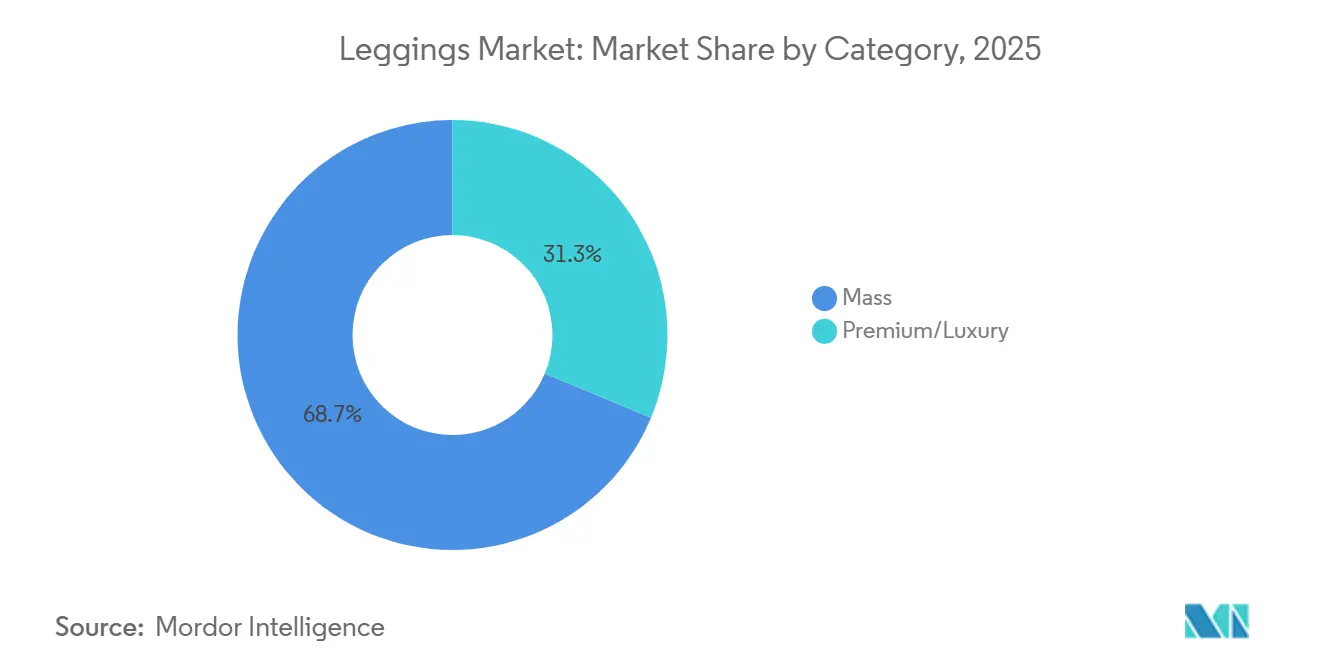

- By category, mass products accounted for 68.72% of the leggings market size in 2025, whereas premium lines are set to grow at a 7.65% CAGR to 2031.

- By distribution channel, specialty stores held 48.46% of revenue in 2025, yet online retail is predicted to post an 8.52% CAGR during the forecast horizon.

- By geography, North America captured 35.27% of the 2025 value, but Asia-Pacific is on track for the quickest regional climb at 7.95% a year to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Leggings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity Of Athleisure And Active Lifestyle Trends | +1.8% | Global, with strongest uptake in North America and urban Asia Pacific | Medium term (2-4 years) |

| Advancements In Fabric Technologies Enhancing Performance | +1.2% | Global; R&D concentrated in Japan, Germany, USA | Long term (≥4 years) |

| Increasing Consumer Preference For Comfort And Functionality | +1.0% | Global, particularly North America and Europe | Short term (≤2 years) |

| Rising Emphasis On Inclusivity And Size Diversity | +0.6% | North America and Europe; emerging in Latin America | Medium term (2-4 years) |

| Expansion Of Customization And Personalization Options | +0.5% | North America, Europe, urban China | Medium term (2-4 years) |

| Surging Demand For Sustainable And Eco-Friendly Materials | +1.4% | Europe (regulatory-driven), North America (consumer-driven), Asia Pacific (supply-chain driven) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Popularity of Athleisure and Active Lifestyle Trends

Athleisure has evolved from a niche category into a wardrobe staple, with consumers wearing performance fabrics to offices, social events, and travel. BCG research in 2024 found that younger cohorts prioritize versatility and comfort over occasion-specific dressing, a shift that persists even as return-to-office mandates increase. This behavioral change is compressing the distinction between gym wear and casual wear, enabling brands to command higher average selling prices by positioning products as multi-functional. Fast Retailing reported that Uniqlo's sweatshirts, sweatpants, and technical HEATTECH lines drove double-digit revenue growth in North America and Europe during the first half of fiscal 2026, underscoring demand for everyday performance fabrics. The wellness economy, valued at USD 1.5 trillion by McKinsey, is reinforcing leggings adoption as consumers link physical activity to mental health and productivity. Hybrid work schedules have also normalized athleisure in professional contexts, reducing the stigma of wearing moisture-wicking fabrics to video calls or client meetings.

Advancements in Fabric Technologies Enhancing Performance

Technical innovation in yarns and finishes is creating defensible product differentiation and margin expansion opportunities. Teijin Frontier introduced a recyclable stretch polyester yarn in 2024 that eliminates elastane while retaining recovery properties, addressing a critical barrier to textile-to-textile recycling. Under Armour partnered with Celanese to develop NEOLAST, an elastane alternative that reduces reliance on petrochemical-derived spandex and improves end-of-life recyclability. Enzymatic depolymerization is emerging as a scalable pathway for closed-loop nylon and polyester; Lululemon's 10-year offtake with Samsara Eco targets 20% of its fiber portfolio from enzymatically recycled sources by 2030, a volume commitment that signals confidence in commercial viability. PUMA's collaboration with RE&UP scales textile-to-textile recycling of polycotton and polyester-elastane blends, historically difficult feedstocks, into virgin-equivalent fibers, reducing dependence on bottle-derived rPET. These advances are shifting the cost curve for recycled inputs and enabling brands to meet European Union Digital Product Passport requirements, which mandate disclosure of recycled content and recyclability by 2027.

Increasing Consumer Preference for Comfort and Functionality

Comfort has overtaken aesthetics as the primary purchase driver, a trend that accelerated during pandemic lockdowns and has proven durable. UBS survey data from 2024 indicated that 68% of leggings buyers prioritize fit and fabric feel over brand name, a reversal from pre-2020 patterns when logo visibility drove purchase intent. This shift is pressuring brands to invest in ergonomic pattern-making and four-way stretch fabrics that accommodate a wider range of body movements. Fast Retailing's success with AIRism and HEATTECH, technical fabrics that regulate temperature and wick moisture, demonstrates that functional benefits can command premium pricing even in mass-market channels. Subscription models such as Fabletics, which reached 2.4 million VIP members by 2025, leverage comfort and fit consistency to reduce churn and increase lifetime value. The rise of "athflow", a hybrid of athleisure and loungewear, reflects consumer demand for garments that transition seamlessly from workout to rest, compressing the need for multiple wardrobe categories and increasing per-item wear frequency.

Rising Emphasis on Inclusivity and Size Diversity

Extended sizing and body-positive marketing are shifting from niche positioning to mainstream strategy as brands recognize that exclusionary size ranges limit addressable markets. BeyondBound launched leggings spanning XS to XXXL in 2025, while ICONI offers S to 4XL and Flurr extends to 8XL, signaling that technical performance fabrics are now engineered for a broader anthropometric spectrum [BeyondBound, ICONI, Flurr]. This expansion requires investment in grading algorithms, fit models, and inventory planning, but it unlocks revenue pools previously underserved by legacy brands. Inclusivity also encompasses adaptive design for consumers with mobility limitations, a segment that intersects with aging demographics in North America and Europe. The business case is compelling: brands that offer extended sizing report higher customer lifetime value due to reduced return rates and stronger brand loyalty. Regulatory momentum is building as well; the European Union's proposed Ecodesign for Sustainable Products Regulation includes provisions for durability and repairability that indirectly favor inclusive design by discouraging fast-fashion churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Prices Of Synthetic Fibers Impacting Costs | -1.2% | Global, with acute exposure in Asia Pacific manufacturing hubs | Short term (≤2 years) |

| Proliferation Of Counterfeit And Low-Quality Products | -0.8% | Global, concentrated in online marketplaces and emerging markets | Medium term (2-4 years) |

| Concerns Related To Fabric Durability And Quality | -0.6% | North America and Europe (consumer litigation risk); Asia Pacific (manufacturing quality control) | Medium term (2-4 years) |

| Intense Competition From Alternative Substitute Products | -0.9% | Global, strongest in North America and Europe where loungewear adoption is high | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fluctuating Prices of Synthetic Fibers Impacting Costs

Polyester and nylon prices are tightly correlated with crude oil and natural gas, exposing leggings brands to input-cost volatility that compresses gross margins when retail prices cannot adjust quickly. Reuters reported that geopolitical tensions in the Strait of Hormuz disrupted petrochemical feedstock flows in early 2025, spiking polyester prices by double digits and forcing brands to absorb costs or risk losing market share to competitors with better hedging strategies. Fast Retailing noted in its fiscal 2026 first-half results that weaker yen forward contracts increased the cost of sales, though the company offset this through improved discount control and operational efficiencies. The shift toward recycled polyester introduces new price dynamics; while recycled content reduces carbon footprint, it often trades at a premium to virgin fiber due to limited sorting and reprocessing infrastructure. Brands with long-term offtake agreements, such as Lululemon's 10-year commitment to Samsara Eco, are locking in supply to mitigate spot-market exposure, but smaller players lack the scale to negotiate similar terms.

Proliferation of Counterfeit and Low-Quality Products

Intellectual property violations pose persistent threats to brand integrity and consumer safety, with counterfeit apparel seizures reaching record levels that undermine legitimate market growth. U.S. Customs and Border Protection reported seizing over 1 million counterfeit apparel items in fiscal 2024, with wearing apparel accounting for USD 178,985,556 in manufacturer's suggested retail price value[1]Source: Asian Development Bank, “E-commerce Evolution IN Asia and the Pacific Opportunities and Challenges,” adb.org. Authentication technologies are being deployed to combat this; Quantum Base's Q-ID NFC cryptographic tags and Entrupy's AI-driven image recognition enable consumers and retailers to verify product authenticity at point-of-sale [Quantum Base, Entrupy]. Blockchain-based provenance tracking is also emerging, though adoption remains limited due to integration costs and the need for industry-wide standards. The proliferation of low-quality imitations on online marketplaces pressures legitimate brands to invest in brand protection, legal enforcement, and consumer education—costs that disproportionately burden smaller players. Premium brands are also exploring direct-to-consumer channels to bypass wholesale partners where counterfeit infiltration is harder to control.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Blended Fabrics Gain as Mono-Materials Hit Recycling Limits

Polyester held 40.62% of the material share in 2025, reflecting its cost advantage, moisture-wicking properties, and established supply chains. Blended fabrics, combining polyester with cotton, nylon, or elastane, are forecast to grow at 7.54% annually through 2031, the fastest rate among material segments. This acceleration stems from consumer preference for fabrics that balance performance and comfort; pure polyester can feel synthetic and trap odor, while blends soften hand-feel and improve breathability. Cotton leggings appeal to sustainability-conscious buyers seeking natural fibers, but their moisture retention and slower drying times limit adoption in high-intensity categories. The "Others" segment includes emerging materials such as Tencel, bamboo, and bio-based nylons, which remain niche due to higher costs and limited scale.

Teijin Frontier's launch of a recyclable stretch polyester yarn in 2024 addresses a critical barrier: elastane-blended fabrics are difficult to recycle because separation technologies are not yet commercially viable at scale. PUMA's collaboration with RE&UP to recycle polycotton and polyester-elastane blends into virgin-equivalent fibers signals that textile-to-textile pathways are maturing, though infrastructure investment remains concentrated in Europe and North America PUMA. Regulatory frameworks such as the European Union's Ecodesign for Sustainable Products Regulation, which mandates digital product passports by 2027, are pressuring brands to shift toward mono-materials or recyclable blends to meet minimum recycled-content thresholds Adidas Group. Cotton sourcing is also under scrutiny; PUMA reported that 99.5% of its cotton came from Better Cotton Initiative, organic, or recycled sources in 2024, reflecting industry-wide adoption of certification standards, according to PUMA Annual report 2025[2]Source: About PUMA, “E5 Resource Use and Circular Economy,” annual-report.puma.com.

By End-User: Men's Segment Outpaces as Athleisure Normalizes

Women accounted for 70.26% of leggings demand in 2025, a dominance rooted in decades of product innovation, celebrity endorsements, and retail prioritization. Men's leggings is expanding at 8.21% annually through 2031, the fastest end-user growth rate, driven by rising gym memberships, the normalization of athleisure in professional settings, and brand investments in men 's-specific fits and colorways. Kids' leggings benefits from school sports programs and parental willingness to invest in performance fabrics, though growth is tempered by shorter product lifecycles due to rapid size changes.

The men's acceleration reflects a behavioral shift. BCG research in 2024 found that younger male cohorts prioritize comfort and versatility over occasion-specific dressing, a pattern that mirrors the athleisure adoption curve among women a decade earlier. Fast Retailing reported strong demand for men's sweatshirts, sweatpants, and technical HEATTECH ranges in North America and Europe during the first half of fiscal 2026, underscoring that functional fabrics are gaining traction beyond traditional gym wear. Under Armour's "Pulse" regenerative sportswear capsule, launched in December 2025, targets environmentally conscious male consumers with plant-based, plastic-free designs and a composting program. Nike's emphasis on recovery and wellness, positioning leggings as essential to mental health and productivity, resonates with male consumers who historically viewed performance apparel as gym-specific.

By Category: Premium Gains as Sustainability Commands Price

Mass-market leggings represented 68.72% of sales in 2025, reflecting broad consumer access and price sensitivity in emerging markets. Premium and luxury leggings is growing at 7.65% annually through 2031, driven by affluent consumers willing to pay for technical innovation, sustainable materials, and brand storytelling. The premium segment benefits from direct-to-consumer models that bypass wholesale markdowns, subscription services that lock in recurring revenue, and collaborations with designers or athletes that create scarcity and social-media buzz.

Lululemon's 10-year offtake agreement with Samsara Eco for enzymatically recycled nylon and polyester, targeting 20% of its fiber portfolio by 2030, exemplifies how premium brands are investing in circular materials to justify higher price points. PUMA's achievement of 90% recycled or certified materials in 2024, one year ahead of schedule, demonstrates that sustainability commitments can differentiate premium offerings even as mass-market players lag due to cost constraints. Gap Inc.'s Victoria Beckham collaboration, launched in April 2026 as a 38-piece collection, illustrates how mass-market players are using designer partnerships to elevate brand perception and capture premium pricing. Subscription models such as Fabletics, which reached 2.4 million VIP members by 2025, blur the line between mass and premium by offering curated selections at mid-tier prices. The mass segment remains price-sensitive and vulnerable to counterfeit competition, particularly in online marketplaces where authentication is difficult.

By Distribution Channel: Online Retail Surges as DTC Models Scale

Specialty stores held 48.46% of the distribution share in 2025, benefiting from product expertise, fitting services, and the ability to showcase technical features through in-store demonstrations. Online retail is expanding at 8.52% annually through 2031, the fastest distribution growth rate, as brands invest in direct-to-consumer platforms, mobile commerce, and omnichannel fulfillment. Hypermarkets and supermarkets serve price-sensitive consumers seeking convenience, while "Others" includes department stores, factory outlets, and pop-up formats.

Adidas reported e-commerce revenue growth of 34% in the first quarter of 2025, driven by mobile optimization and personalized recommendations powered by customer data. Lululemon launched e-commerce in Mexico and opened 15 stores across North America, including 8 in Mexico, during fiscal 2026, illustrating how digital and physical channels reinforce each other. Uniqlo's RFID-enabled self-checkout, alterations, and Re. Uniqlo donation bins in new U.S. stores demonstrate how specialty retail is integrating services to compete with online convenience. Mobile commerce accounted for 55% of online leggings purchases in 2024, pressuring brands to optimize checkout flows and integrate social-media storefronts.

Geography Analysis

North America commanded 35.27% of leggings revenue in 2025, underpinned by high per-capita spending, mature athleisure adoption, and established specialty-retail infrastructure. Asia Pacific is forecast to grow at 7.95% annually through 2031, the fastest regional rate, as manufacturing shifts to India and Vietnam compresses lead times and landed costs while rising middle-class incomes in China and Southeast Asia expand the consumer base. Europe balances strong demand for sustainable products with regulatory frameworks such as the Ecodesign for Sustainable Products Regulation, which mandates digital product passports by 2027 and pressures brands to adopt traceable, recycled materials Adidas Group. South America and the Middle East & Africa remain smaller but are attracting investment as brands seek geographic diversification and tap into nascent fitness cultures.

Hong Fu's Rs 1,500 crore (approximately USD 180 million) facility in India, operational in January 2026 and employing 25,000 workers, signals that Nike and Adidas suppliers are reducing dependence on China and Vietnam to mitigate geopolitical and labor-cost risks[3]Source: Business Standard, “Uniqlo Aims to Make India Sourcing Hub,” business-standard.com. Uniqlo targets 30% local sourcing in India, up from 15-20%, while growing its domestic retail footprint to 18 stores and achieving 44% year-over-year revenue growth in fiscal 2026 Business Standard. Fast Retailing's Uniqlo brand reported double-digit revenue and profit growth in North America and Europe during the first half of fiscal 2026, driven by flagship-store openings in Chicago, San Francisco, and New York, as well as strong demand for HEATTECH and year-round sweatshirt ranges. PUMA opened a 1.2 million square-foot distribution center in Arizona in June 2024 and a 440,000 square-foot logistics facility in France in November 2025, investments that reduce delivery times and support omnichannel fulfillment.

Keppel Corporation and Fast Retailing signed a memorandum of understanding to explore retail real estate opportunities across Asia Pacific, with Uniqlo confirmed as a tenant in Hanoi's forthcoming largest shopping destination Retail News Asia. Brazil, Argentina, and Chile are seeing increased leggings adoption tied to urbanization and rising gym memberships, though economic volatility and currency fluctuations constrain purchasing power. The Middle East, particularly the United Arab Emirates and Saudi Arabia, is investing in sports infrastructure and wellness tourism, creating demand for premium leggings aligned with luxury retail ecosystems.

Competitive Landscape

The leggings market demonstrates moderate fragmentation, providing opportunities for both established athletic apparel leaders and emerging leggings brands to compete through distinct positioning strategies. Leading companies, such as Nike, Adidas, and Lululemon, capitalize on vertical integration, proprietary fabric innovations, and expansive global distribution networks to sustain their competitive edge. Meanwhile, newer brands focus on targeting niche segments, implementing direct-to-consumer business models, and utilizing advanced materials to gain market share.

Competition has intensified as traditional sportswear companies expand their presence in the athleisure segment, while fashion retailers introduce performance-focused leggings collections. The adoption of advanced technologies has become a key differentiator, with companies investing in smart fabrics, body scanning technologies for enhanced fit optimization, and sustainable manufacturing practices to appeal to environmentally conscious consumers.

Significant opportunities remain in areas such as inclusive sizing, customization technologies, and the use of sustainable materials, which address the needs of underserved consumer segments. Emerging disruptors are leveraging direct-to-consumer models and utilizing social media platforms to build brand recognition and engage with consumers, all while avoiding the high costs associated with traditional retail infrastructure.

Leggings Industry Leaders

Nike, Inc.

Adidas AG

Lululemon Athletica Inc.

Under Armour, Inc.

Puma SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CYSM Shapers launched a new product line, Curvy Leggings, designed for curvy body types. The stretch leggings accommodate various activities, from yoga to daily tasks, with users reporting satisfaction with the fit.

- June 2025: Buyco announces the launch of its VarsityLux collection for Fall '25, featuring wide-leg leggings and sportswear. The collection includes tailored wide-leg leggings designed with four-way stretch, breathable panels, and a leg-elongating silhouette that prioritizes comfort.

- May 2025: To commemorate the 10-year anniversary of its iconic Align leggings, Lululemon introduced the Align No Line, a seamless and innovative version of the original design. This launch highlights the brand's commitment to evolving its product offerings while maintaining the comfort and functionality that Align leggings are known for.

Global Leggings Market Report Scope

| Cotton |

| Polyester |

| Blended |

| Others |

| Women |

| Men |

| Kids |

| Mass |

| Premium/Luxury |

| Hypermarkets/Supermarkets |

| Specialty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Material | Cotton | |

| Polyester | ||

| Blended | ||

| Others | ||

| By End-User | Women | |

| Men | ||

| Kids | ||

| By Category | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the leggings market by 2031?

The leggings market is anticipated to reach USD 58.12 billion by 2031, expanding at a 6.85% CAGR from 2026 to 2031, according to Mordor Intelligence.

Which material category is forecast to grow fastest?

Blended fabrics are expected to record a 7.54% CAGR through 2031 as consumers favor comfort-stretch combinations and brands adopt recyclable blends.

How quickly is online retail growing within leggings?

Online retail channels are predicted to grow at an 8.52% CAGR to 2031, the fastest among distribution formats, driven by direct-to-consumer strategies.

Which region is likely to post the highest growth rate?

Asia-Pacific is set for a 7.95% CAGR through 2031, outpacing other regions as manufacturers shift capacity to India and Vietnam and middle-class spending rises.

Page last updated on: