Yoga Clothing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

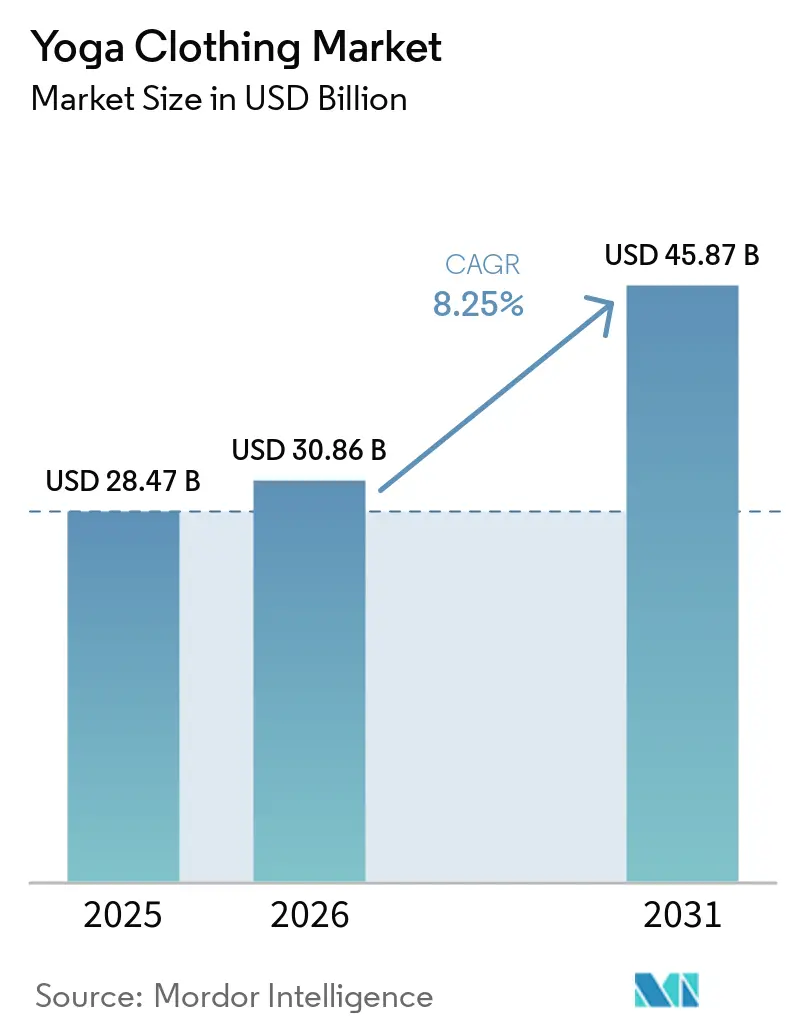

| Market Size (2026) | USD 30.86 Billion |

| Market Size (2031) | USD 45.87 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Yoga Clothing Market Analysis by Mordor Intelligence

The yoga clothing market size is expected to grow from USD 28.47 billion in 2025 to USD 30.86 billion in 2026 and is forecast to reach USD 45.87 billion by 2031 at a 8.25% CAGR over 2026-2031. The yoga clothing market is influenced by factors related to lifestyle, health, and fashion. Growing awareness of physical and mental well-being has increased yoga participation, driving demand for specialized apparel that offers comfort, flexibility, and performance. The athleisure trend has further blurred the distinction between activewear and casual wear, prompting consumers to use yoga clothing for both workouts and daily activities. Advances in fabric technology, including moisture-wicking, odor resistance, and the use of sustainable materials, have enhanced the appeal of these products. Social media, celebrity endorsements, and fitness influencers have also boosted brand visibility and consumer interest. Furthermore, the rise in female workforce participation, increased spending on wellness products, and the growth of e-commerce platforms with diverse product offerings have made yoga apparel more accessible and appealing to a wide range of consumers.

Key Report Takeaways

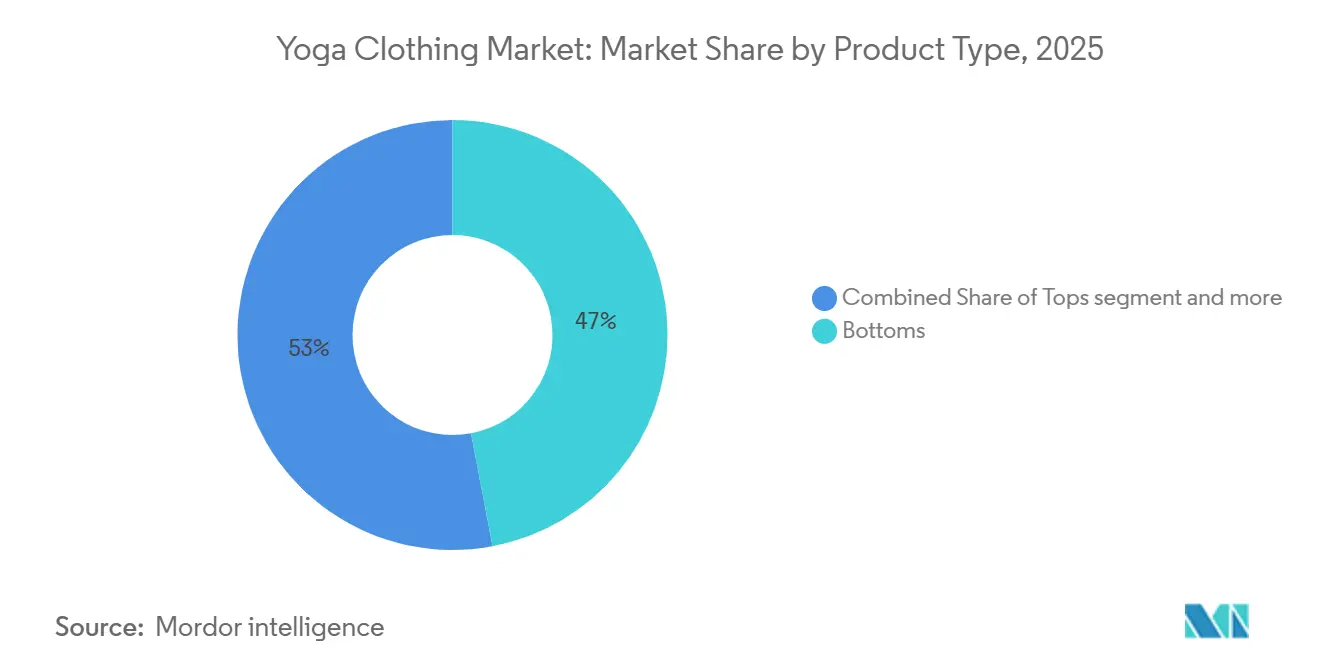

- By product type, bottoms commanded 47.03% of yoga clothing market share in 2025, while tops are projected to register an 8.95% CAGR from 2026-2031.

- By end user, female consumers held 59.30% share in 2025; the male segment is forecast to advance at an 8.84% CAGR through 2031.

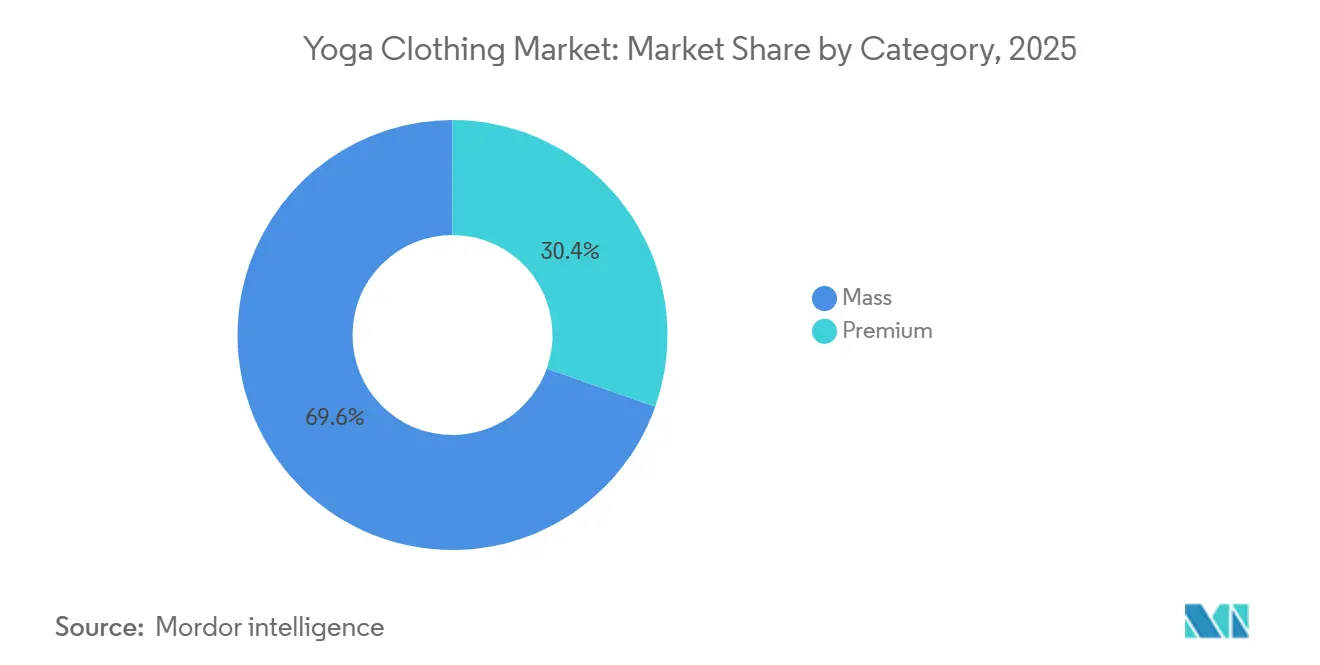

- By category, mass accounted for 69.58% share in 2025, yet premium is expected to expand at a 9.13% CAGR over 2026-2031.

- By distribution channel, offline retail stores secured 62.50% share in 2025, whereas online retail is projected to grow at a 9.36% CAGR to 2031.

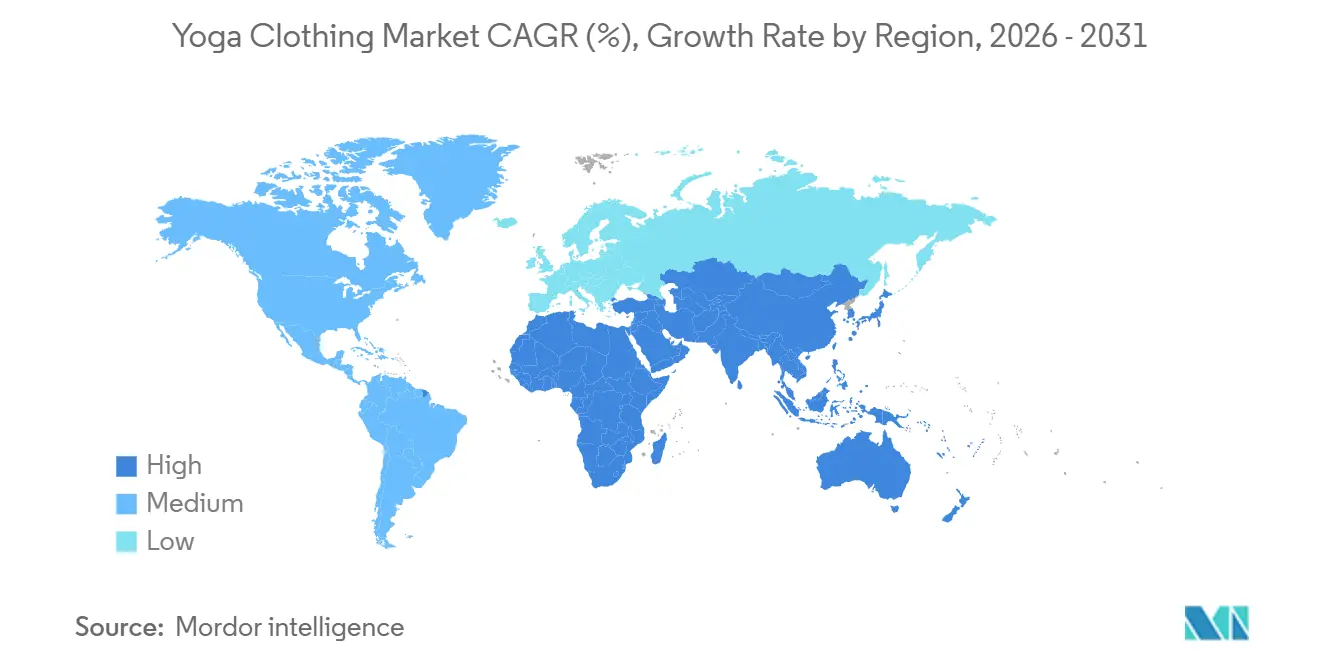

- Geographically, North America led with 32.23% share in 2025; Asia-Pacific is the fastest-growing region at a 9.61% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Yoga Clothing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of yoga as holistic wellness practice | +1.8% | Global, with highest penetration in North America, India, and urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of athleisure trend | +2.1% | Global, led by North America and Europe; accelerating in China and urban India | Long term (≥4 years) |

| Growing preference for functional and performance-oriented fabrics | +1.5% | North America, Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Innovation in sustainable and eco-friendly materials | +1.3% | Europe, North America, urban China; regulatory influence via Bluesign and GOTS certifications | Long term (≥4 years) |

| Influence of social media and fitness influencers | +1.0% | Global, with highest impact on Gen Z and Millennials across North America, Europe, and Asia-Pacific | Short term (≤2 years) |

| Increasing popularity of home-based fitness and digital yoga platforms | +0.9% | Global, accelerated by digital infrastructure in North America, Europe, and urban Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of yoga as holistic wellness practice

The increasing recognition of yoga as a holistic approach to physical fitness, mental well-being, and stress management is a significant driver of the global yoga clothing market. As consumers place greater emphasis on preventive healthcare and mindfulness-based routines, yoga has transitioned from a niche activity to a mainstream wellness practice. This shift has created a steady demand for specialized apparel designed to provide flexibility, comfort, and breathability. The trend is further supported by the rapid growth of yoga infrastructure. For example, according to the National Sporting Goods Association, nearly 7,500 new Pilates and yoga studios were registered in the United States in 2025, reflecting a notable rise in participation levels[1]Source: National Sporting Goods Association, "NSGA’s Annual Sports Participation Study Emphasizes Overall Growth," nsga.org. Additionally, government-led initiatives are accelerating adoption, particularly in emerging markets. In India, the government has promoted yoga and related practices through programs under Ayushman Bharat. The inclusion of AYUSH Health and Wellness Centres under the National AYUSH Mission involved a total expenditure of INR 3,399.35 crore between FY2019–20 and FY2023–24[2]Source: Press Information Bureau, "Cabinet approves inclusion of the AYUSH Health & Wellness Centres component of Ayushman Bharat in National AYUSH Mission," pib.gov.in. These policy-level efforts not only enhance awareness and accessibility of yoga but also sustain participation rates, driving consistent demand for yoga-specific clothing globally.

Expansion of athleisure trend

The global yoga clothing market is experiencing significant growth due to the rapid expansion of the athleisure trend, which has integrated activewear into everyday fashion. Consumers increasingly favor apparel that combines functionality, comfort, and style, enabling yoga clothing to transition from fitness settings to casual, travel, and even semi-formal environments. This trend has driven brands to create versatile products that offer both aesthetic appeal and performance features such as stretchability, breathability, and durability. Additionally, the influence of social media, celebrity endorsements, and evolving workplace dress codes prioritizing comfort has further established athleisure as a mainstream lifestyle choice. Consequently, yoga apparel has expanded beyond its traditional user base, appealing to a wider audience seeking stylish yet comfortable clothing, thereby driving substantial market growth.

Growing preference for functional and performance-oriented fabrics

The global yoga clothing market is experiencing growth due to a rising consumer preference for functional and performance-oriented fabrics that enhance comfort, durability, and workout efficiency. Yoga practitioners increasingly seek apparel that supports a wide range of movements and varying intensity levels, driving demand for advanced textiles with features such as moisture-wicking, four-way stretch, breathability, odor resistance, and temperature regulation. These fabric innovations not only enhance performance during yoga sessions but also ensure long-lasting wear and ease of maintenance, making them appealing to modern consumers. Additionally, heightened awareness of skin sensitivity and hygiene has led to the adoption of anti-microbial and hypoallergenic materials. This alignment of functionality and comfort continues to shape consumer purchasing decisions, contributing to the growth of the yoga clothing market.

Innovation in sustainable and eco-friendly materials

Innovation in sustainable and eco-friendly materials is becoming a significant factor in the global yoga clothing market, as environmentally conscious consumers increasingly prioritize products that reflect their values. Yoga, often associated with mindfulness and a connection to nature, has led buyers to favor apparel made from materials such as organic cotton, bamboo fibers, recycled polyester, and biodegradable fabrics. In response, brands are adopting low-impact dyeing processes, water-efficient manufacturing methods, and circular production models aimed at minimizing waste and reducing carbon emissions. Furthermore, transparency in sourcing and adherence to ethical labor practices have become essential considerations for consumers, encouraging companies to emphasize certifications and sustainability commitments. This focus on eco-conscious innovation not only helps differentiate products in a competitive market but also fosters brand loyalty, supporting sustained global demand for yoga clothing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product substitution by general activewear | -0.9% | Global, most acute in North America and Europe where Nike and Adidas hold strong brand equity | Medium term (2-4 years) |

| Counterfeit products and brand imitation | -0.6% | Global, with highest incidence in Asia-Pacific (China, Southeast Asia) and cross-border e-commerce | Long term (≥4 years) |

| Fit and sizing challenges across diverse body types | -0.4% | Global, particularly affecting mass-market penetration in North America, Europe, and urban Asia | Medium term (2-4 years) |

| Limited product differentiation across brands | -0.5% | Global, intensifying in mature markets (North America, Europe) as fast-fashion and private-label enter | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Product substitution by general activewear

The global yoga clothing market is constrained by the increasing substitution of yoga-specific apparel with general activewear, which provides similar functionality at often lower price points. Many consumers, particularly those who practice yoga casually or occasionally, prefer multipurpose activewear such as leggings, t-shirts, and sports bras. These items can be used across various fitness activities, reducing the demand for specialized yoga apparel. The widespread availability of affordable and stylish activewear from mass-market brands has further accelerated this trend. These products often feature comparable attributes, such as stretchability, moisture management, and comfort. Moreover, the versatility of general activewear for activities like gym workouts, running, and everyday wear makes it a practical option for budget-conscious consumers. This overlap in functionality and use cases diminishes the unique value proposition of dedicated yoga clothing, thereby limiting its potential for market growth.

Counterfeit products and brand imitation

The global yoga clothing market faces significant challenges due to the prevalence of counterfeit products and brand imitation, which negatively affect brand credibility and consumer trust. As demand for premium yoga apparel increases, counterfeit manufacturers are replicating popular designs, logos, and fabric claims, offering lower-cost alternatives that attract price-sensitive consumers. This practice not only diverts sales from authentic brands but also creates market confusion regarding product quality and performance standards. Counterfeit products often fail to meet the durability, comfort, and technical performance expected from genuine yoga clothing, potentially harming the overall perception of the category. The scale of this issue is evident from data provided by the United States Customs and Border Protection, which reported the seizure of approximately one million counterfeit clothing items in 2024. Apparel ranked as the third-largest category among all confiscated counterfeit goods[3]Source: United States Customs and Border Protection, "The Truth Behind Counterfeits," cbp.gov. These trends highlight the increasing difficulty for established brands in protecting intellectual property and maintaining consumer confidence, thereby limiting market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tops Accelerate as Hybrid-Use Gains Traction

Bottoms accounted for 47.03% of the market share in 2025, driven by their functionality, comfort, and versatility in both fitness and everyday use. Consumers prioritize features such as high stretchability, squat-proof fabrics, compression support, and moisture-wicking properties, which enhance performance during yoga and other physical activities. High-waisted designs, offering core support and body contouring, have gained significant popularity, particularly among female consumers seeking both comfort and aesthetic appeal. Furthermore, the use of advanced materials that ensure durability, breathability, and shape retention has bolstered product demand. The growing adoption of athleisure has positioned yoga bottoms as suitable for everyday wear, leading to increased repeat purchases and expanding their usage beyond workouts, thereby driving segment growth.

Tops are projected to grow at the fastest rate, with a CAGR of 8.95% through 2031, driven by increasing demand for comfort, breathability, and style in low- to medium-intensity workouts. Consumers are prioritizing lightweight and flexible fabrics that provide unrestricted movement while ensuring adequate support and ventilation. The emphasis on body positivity and personalized style has increased the demand for diverse fits, designs, and layering options, making yoga tops versatile for both exercise and casual wear. Furthermore, advancements in fabric technologies, including anti-odor properties, quick-drying materials, and seamless construction, enhance user experience and product differentiation. Fashion trends, social media, and fitness influencers also contribute to the growing demand, as consumers seek visually appealing and functional tops that meet both performance requirements and lifestyle preferences.

By End User: Male Segment Closes Gender Gap via Performance Narratives

Female consumers accounted for 59.30% of the market share in 2025, driven by higher participation in yoga and wellness activities, along with a strong focus on health, fitness, and self-care routines. Women increasingly prefer apparel that combines performance and style, resulting in high demand for products offering flexibility, moisture management, and body-contouring fits. The growing popularity of athleisure has further extended the use of yoga clothing beyond workouts, making it an integral part of everyday wardrobes. Additionally, frequent product innovations, such as high-waisted leggings, seamless designs, and supportive sports bras, cater to female preferences for comfort and aesthetics. Social media trends, celebrity endorsements, and fitness influencers significantly influence purchasing behavior, while the increasing availability of products on e-commerce platforms enhances accessibility and variety, collectively driving growth in this segment.

The male yoga apparel market is projected to grow at a CAGR of 8.84% through 2031, driven by the increasing adoption of yoga among men for fitness, flexibility training, and stress management. Growing awareness of yoga's physical and mental health benefits has led to higher investments in specialized apparel designed for performance and comfort. Products emphasizing breathability, durability, and freedom of movement, such as stretchable shorts, compression wear, and lightweight tops, are witnessing strong demand. Additionally, the trend toward functional fitness and cross-training has encouraged men to choose versatile yoga clothing suitable for various activities. The rising visibility of male fitness influencers and targeted marketing efforts by brands are also helping to challenge traditional stereotypes, thereby broadening the consumer base and supporting consistent growth in the male yoga apparel segment.

By Category: Premium Segment Leads Innovation Despite Mass Dominance

The mass category accounted for 69.58% of the market share in 2025, driven by factors such as affordability, accessibility, and the increasing participation of price-sensitive consumers in the fitness and wellness sector. As yoga gains broader acceptance, a significant number of beginners and casual practitioners opt for cost-effective apparel that provides basic comfort, flexibility, and durability. The growth of fast-fashion and value retail brands has enhanced the availability of yoga clothing through both offline and online channels, facilitating deeper market penetration in emerging and price-sensitive regions. Furthermore, the rising influence of athleisure has boosted demand for versatile, budget-friendly products suitable for both workouts and everyday use. Frequent product launches, discounts, and promotional activities also encourage repeat purchases, positioning mass-market yoga clothing as a key driver of volume growth.

The premium yoga clothing segment is projected to grow at a CAGR of 9.13% through 2031, driven by increasing consumer demand for high-quality, performance-oriented, and aesthetically appealing apparel that enhances the workout experience. Affluent and brand-conscious consumers are investing in yoga clothing featuring advanced fabric technologies, such as superior moisture management, four-way stretch, compression support, and enhanced durability. Additionally, premium brands focus on design innovation, superior fit, and exclusivity, catering to consumers seeking both functionality and style. The association of yoga with wellness, mindfulness, and lifestyle aspirations further boosts demand for premium products that align with personal values, including sustainability and ethical sourcing. Factors such as strong brand positioning, influencer partnerships, and immersive retail experiences also enhance perceived value, supporting growth in this segment.

By Distribution Channel: Online Retail Gains Share

Offline retail stores accounted for 62.50% of the market share in 2025, continuing to drive yoga clothing sales by providing a tactile and personalized shopping experience that remains important to many consumers, particularly for fit-sensitive apparel. Customers often prefer trying on products to evaluate comfort, stretch, size accuracy, and fabric quality before making a purchase, which is especially critical for performance wear such as yoga clothing. In-store assistance from sales staff, immediate product availability, and the ability to physically compare multiple styles further enhance consumer confidence in purchasing decisions. Additionally, branded outlets and specialty sports stores create immersive environments that align with lifestyle positioning, fostering stronger brand connections and loyalty. Seasonal discounts, in-store promotions, and visual merchandising also encourage impulse purchases, while yoga studios and fitness centers selling apparel directly contribute to localized demand.

Online retail stores are expected to grow at a CAGR of 9.36% through 2031, significantly driving yoga clothing sales. This growth is attributed to the convenience, extensive product variety, and competitive pricing offered by these platforms. Consumers benefit from the ability to explore multiple brands, compare product features, and access customer reviews, enabling informed purchasing decisions. The expansion of e-commerce platforms and direct-to-consumer brand websites has improved accessibility, particularly in areas with limited physical retail presence. Features such as easy return policies, size guides, and virtual try-on tools have addressed concerns related to fit and quality. Additionally, digital marketing strategies, influencer collaborations, and targeted advertisements on social media platforms enhance product visibility and consumer engagement. Promotions like frequent discounts, flash sales, and subscription-based offerings further incentivize online purchases, positioning this channel as a critical growth driver for the yoga clothing market.

Geography Analysis

In 2025, North America accounted for 32.23% of the market share, driven by a well-established fitness culture and high awareness of holistic wellness practices that emphasize both physical and mental health. The region benefits from a large base of regular yoga practitioners, supported by the widespread availability of studios, fitness centers, and wellness programs, which sustain consistent demand for specialized apparel. The strong presence of prominent activewear brands, including Lululemon Athletica and Nike, fosters innovation in fabric technology, design, and premium product offerings. Furthermore, the popularity of the athleisure trend has positioned yoga clothing as everyday wear, extending its use beyond workouts. High digital penetration, influencer-driven marketing strategies, and a robust e-commerce ecosystem enhance product visibility and accessibility, further driving market growth in the region.

Asia-Pacific is the fastest-growing region, with a CAGR of 9.61% projected through 2031. This growth is driven by increasing health consciousness, rising disposable incomes, and the adoption of fitness-oriented lifestyles among urban populations. The cultural significance of yoga in countries like India, coupled with government initiatives promoting traditional wellness practices, is fostering greater participation. Additionally, countries such as China and Japan are experiencing strong demand due to urbanization and the influence of Western fitness trends. The availability of affordable domestic brands alongside international players has improved access to yoga clothing across various income groups. Moreover, the rapid expansion of online retail platforms and mobile commerce, supported by social media engagement, is significantly contributing to sales growth and consumer awareness in the region.

In Europe, the demand for yoga clothing is driven by growing participation in yoga and fitness activities, coupled with a preference for sustainable and ethically produced apparel. In South America, increasing urbanization and the growth of middle-class populations are promoting active lifestyles, leading to higher demand for versatile and affordable yoga clothing. In the Middle East and Africa, market growth is supported by rising fitness awareness, the expansion of organized retail, and the growing popularity of boutique fitness studios, particularly in urban areas. Across these regions, global fashion trends, the entry of international brands, and improved access through e-commerce platforms are collectively fostering steady market growth.

Competitive Landscape

The global yoga clothing market is moderately fragmented, featuring a mix of dominant athleisure corporations, emerging premium challengers, and niche specialists emphasizing sustainability and performance. Established brands such as Lululemon Athletica, Nike, and Adidas maintain strong market presence through their brand equity, extensive distribution networks, and ongoing product innovation. Simultaneously, newer entrants like Vuori and Alo Yoga are gaining momentum by prioritizing superior fabric quality, fit, and lifestyle-oriented positioning, appealing to younger, digitally engaged consumers. Additionally, sustainability-focused brands such as Girlfriend Collective, Manduka, and prAna cater to environmentally conscious consumers by emphasizing transparent sourcing and eco-friendly materials. This diverse competitive structure fosters a dynamic marketplace where differentiation is driven by innovation, brand storytelling, and targeted consumer engagement.

Advancements in fabric technology and the rapid adoption of performance features across brands significantly influence competitive intensity. Proprietary material innovations such as specialized stretch fabrics, moisture management systems, and seamless construction initially provide differentiation but often become industry standards over time, diminishing long-term competitive advantages. Textile developers and manufacturers, including Teijin and Polartec, play a pivotal role in driving these advancements, contributing to continuous product evolution. Consequently, competition increasingly focuses on incremental improvements in comfort, durability, and versatility rather than groundbreaking innovations. Meanwhile, digital-first brands leverage direct-to-consumer models and online engagement to scale efficiently, intensifying competition with traditional retail-led approaches and reshaping customer acquisition and retention strategies.

Despite promising growth prospects, the market faces several challenges that constrain differentiation and profitability. The proliferation of counterfeit products poses a significant issue, with global illicit trade, undermining brand value and consumer trust. Additionally, the availability of lower-cost alternatives and private-label “dupes” from mass retailers erodes the pricing power of premium brands. The overlap between yoga clothing and general activewear further increases substitution risks. Large-scale players continue to dominate consumer spending in the athleisure segment, limiting the ability of yoga-specific brands to achieve full differentiation. Moreover, shorter product design cycles and the rapid replication of trends contribute to market commoditization, compelling companies to compete on pricing, branding, and customer experience rather than relying solely on product uniqueness.

Yoga Clothing Industry Leaders

-

Lululemon Athletica Inc.

-

Nike Inc.

-

Color Image Apparel Inc. (Alo Yoga)

-

Athleta (Gap Inc.)

-

Puma SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lululemon made its debut in India, unveiling its signature range of yoga pants, designed for both traditional yoga enthusiasts and those embracing urban wellness trends.

- June 2025: H&M Move, in celebration of International Day of Yoga, unveiled a limited women's collection, spotlighting stylish and functional yoga pants and coordinated sets, all crafted for comfort and flexibility.

- May 2025: Kooniez Pants, hailing from Los Angeles, introduced its handmade harem-style yoga pants, boasting features like a stretchy waistband, wide legs, adjustable hems, and deep pockets. Praised for their softness and breathability, these pants come in over 30 colors and cater to all body types.

- October 2024: Beyond Yoga, a prominent player in the activewear market, has unveiled a new pop-up store in New York. The store showcases the Spacedye collection, along with outerwear and a fresh fleece line, which features iyoga clothing and other activewear.

Global Yoga Clothing Market Report Scope

| Tops |

| Bottoms |

| One-piece and Sets |

| Accessories |

| Male |

| Female |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Tops | |

| Bottoms | ||

| One-piece and Sets | ||

| Accessories | ||

| By End User | Male | |

| Female | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the yoga clothing market?

The yoga clothing market size is USD 30.86 billion in 2026, with revenue forecast to hit USD 45.87 billion by 2031.

How fast is the yoga clothing market expected to grow?

The market is projected to register an 8.25% CAGR between 2026 and 2031, driven by expanding global yoga participation and athleisure adoption.

Which product segment leads the yoga clothing market?

Bottoms such as leggings and pants hold 47.03% of 2025 revenue, although tops record the highest growth pace at 8.95% CAGR.

Which region shows the fastest growth?

Asia-Pacific is the quickest-growing region with an 9.61% CAGR through 2031, propelled by surging demand in China, India, and Southeast Asia.

Page last updated on: