Sneakers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

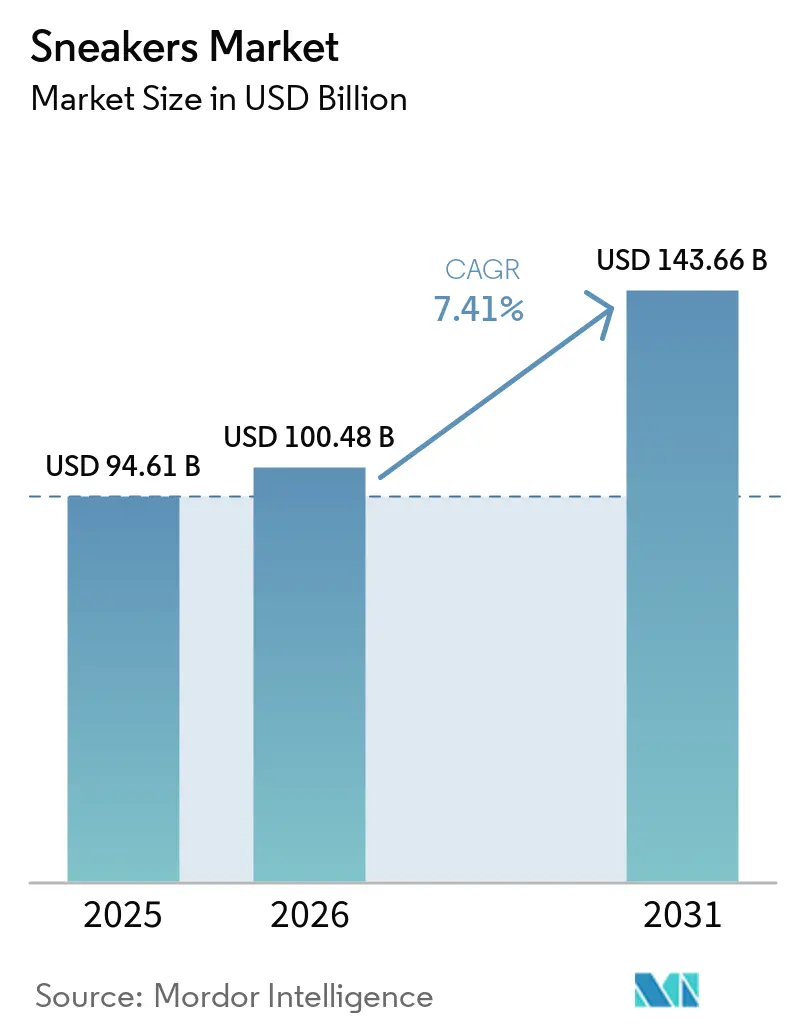

| Market Size (2026) | USD 100.48 Billion |

| Market Size (2031) | USD 143.66 Billion |

| Growth Rate (2026 - 2031) | 7.41% CAGR |

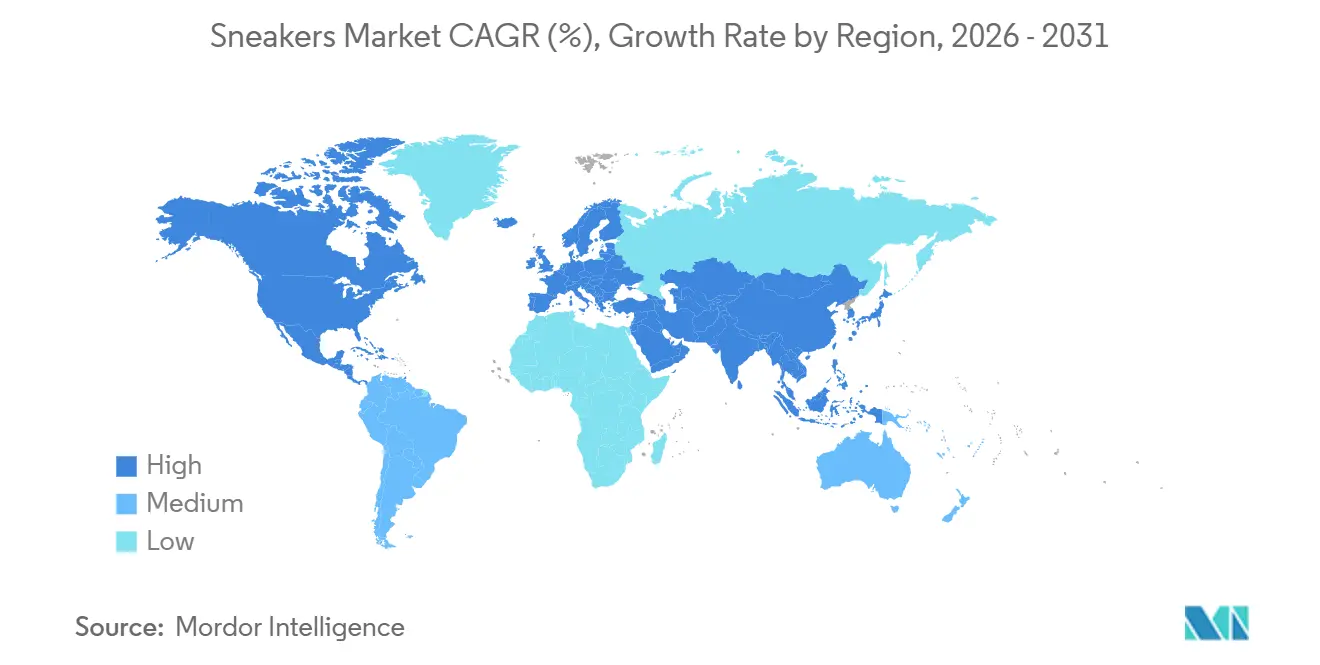

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sneakers Market Analysis by Mordor Intelligence

The sneakers market size is expected to grow from USD 94.61 billion in 2025 and USD 100.48 billion in 2026 to USD 143.66 billion by 2031, registering a CAGR of 7.41% between 2026 and 2031. Sneakers market expansion is being driven by the growing perception of sneakers as both functional gear and lifestyle statements, prompting brands to fuse technical performance with everyday design appeal. While performance footwear continues to account for a significant revenue share in the sneaker industry, lifestyle-oriented designs are witnessing faster uptake, reflecting consumer preference for multi-purpose use. The rise of digital-first purchasing behavior in the sneaker market, alongside simultaneous premiumization and demand for affordable options in emerging markets, is creating a dual-tier market structure. In the sneakers market, increasing health awareness and participation in fitness activities further reinforce steady demand growth across segments. Meanwhile, emerging players in the sneakers market are intensifying competition by leveraging sustainability narratives, community engagement, and direct-to-consumer strategies, gradually challenging established brands despite their scale and innovation advantages.

Key Report Takeaways

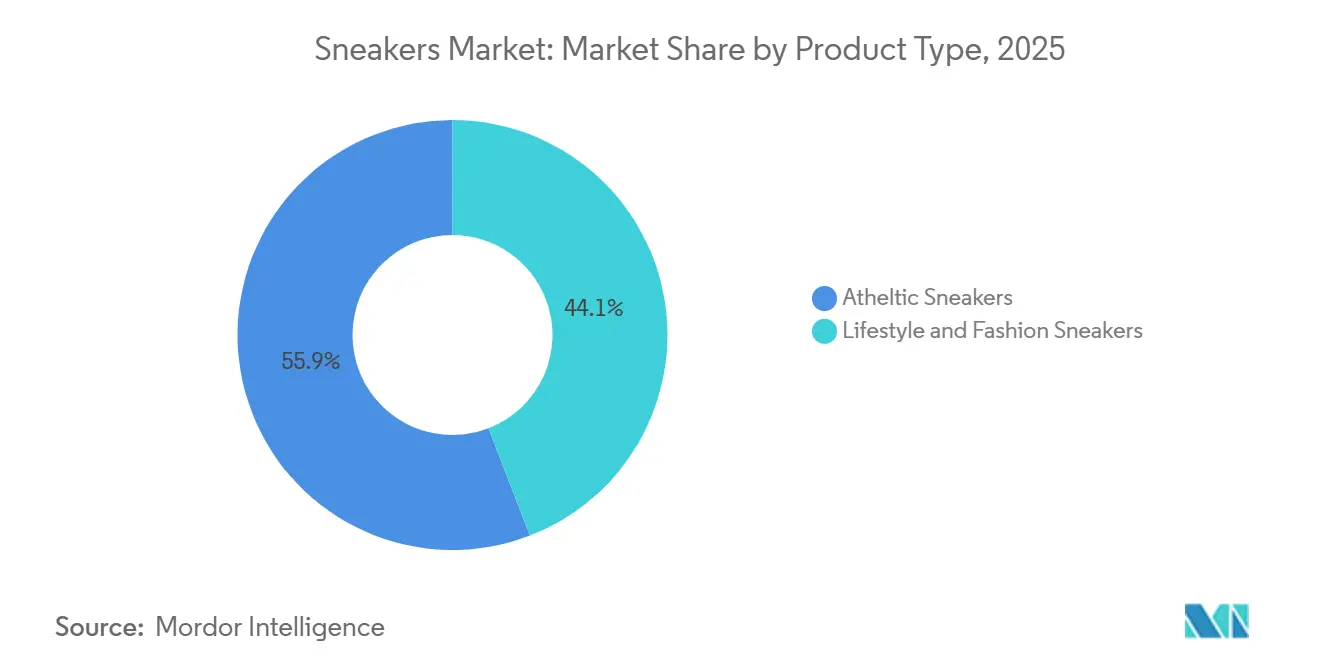

- By product type, athletic sneakers led with 55.87% of the market share in 2025, while lifestyle and fashion sneakers are forecast to expand at a 7.85% CAGR through 2031.

- By end user, men accounted for 53.45% of the market size in 2025, whereas the women’s segment is projected to advance at a 7.93% CAGR to 2031.

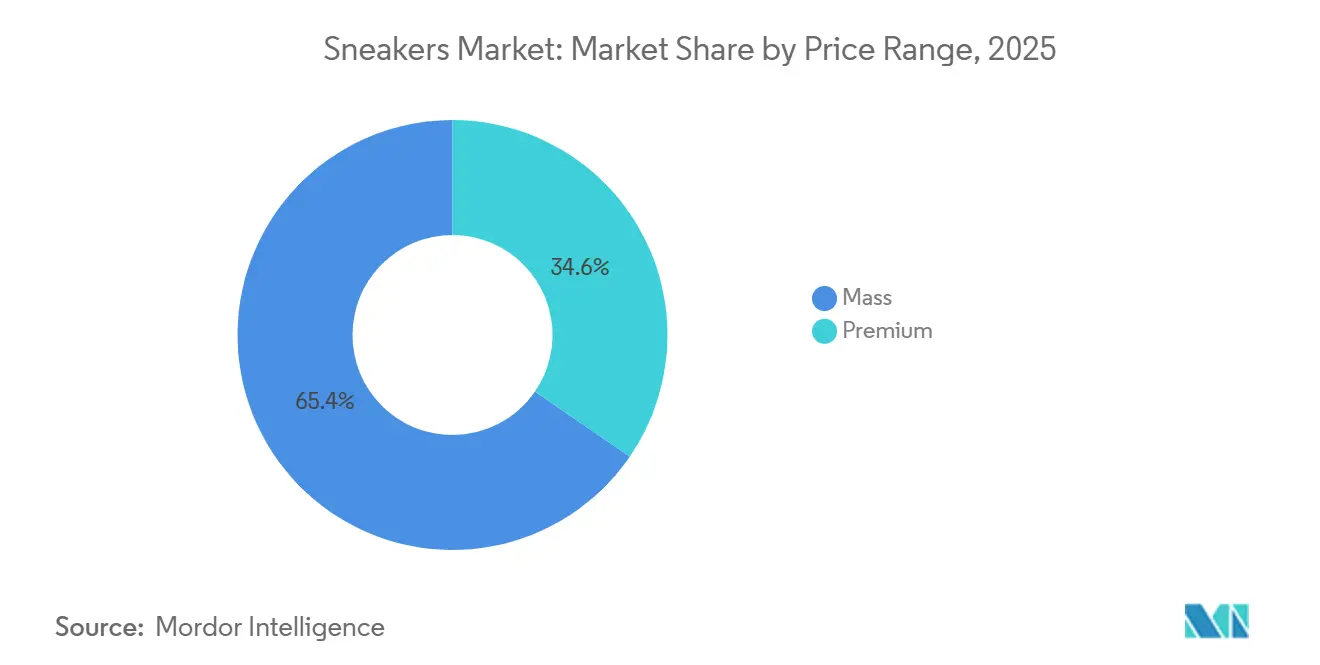

- By price range, mass products held 65.43% of the sneakers market size in 2025 and the premium tier is set to grow at 7.74% CAGR over 2026-2031.

- By distribution channel, specialty stores retained 36.35% revenue share in 2025 while online retail is expected to post an 8.22% CAGR to 2031.

- By geography, Asia-Pacific captured 32.28% of the sneakers market size in 2025 and is forecast to climb at an 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sneakers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing trends in athleisure and lifestyle-oriented fashion | +1.20% | Global, strongest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Escalating focus on health, wellness, and active lifestyles | +0.90% | Global, led by North America, Europe, affluent Asia-Pacific metros | Long term (≥ 4 years) |

| Increasing emphasis on sustainable and eco-conscious innovations | +0.80% | Europe and North America lead; emerging in Asia-Pacific cities | Long term (≥ 4 years) |

| Popularity of limited releases, brand collaborations, and hype-driven culture | +1.10% | Global, concentrated in North America, Europe, United Arab Emirates, China, Japan | Short term (≤ 2 years) |

| Expansion of digital platforms and e-commerce channels | +1.50% | Global, fastest in Asia-Pacific, Middle East, South America | Short term (≤ 2 years) |

| Rising demand for personalized and customizable products | +0.70% | North America and Europe lead; nascent in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing trends in athleisure and lifestyle-oriented fashion

Athleisure has transitioned from a niche trend to a central driver of growth in the global sneaker industry, with footwear increasingly designed to move seamlessly between workouts, workplaces, and social settings. Easing dress codes in the post-pandemic era has further accelerated this shift, as consumers prioritize versatility alongside style. Lifestyle-oriented sneaker categories are now expanding faster than purely performance-driven segments, reflecting demand for products that balance everyday wear with athletic functionality. Reflecting deeper wellness-oriented trends, Americans aged 15 and over spent an average of 5.5 hours per day on leisure and sports activities in 2024, marking a continued rise in active lifestyles [1]Source: United States Bureau of Labor Statistics, "American Time Use Survey Summary", bls.gov. Brands in the sneakers market are responding by integrating performance innovations such as advanced cushioning and lightweight materials with premium finishes and fashion-led aesthetics. At the same time, retro-inspired designs are gaining traction, driven by nostalgia among consumers with higher disposable incomes. The growing popularity of platform sneakers, particularly among women, highlights demand for comfort combined with style enhancement. Moving forward, companies must strike a balance between innovation, affordability, and multi-functional appeal to sustain growth across diverse consumer segments.

Escalating focus on health, wellness, and active lifestyles

The global sneaker market is increasingly shaped by casual fitness participants and wellness-focused consumers, rather than just professional athletes. A growing base of runners, walkers, and everyday users is expanding demand for footwear that prioritizes comfort, injury prevention, and durability over purely performance-driven features. According to the World Health Organization, 31% of adults do not meet recommended activity levels, projected to reach 35% by 2030, implying that nearly 69% of the population engages in some form of physical activity [2]Source: World Health Organization, "Physical Activity Factsheet", who.int. This broad participation in the sneakers market is encouraging brands to invest in advanced cushioning technologies and energy-return materials to enhance everyday movement. Recent product innovations highlight a strong focus on resilience and long-distance comfort, catering to users with consistent, moderate activity levels. The emergence of lifestyle-oriented sports and informal fitness routines is also driving demand for versatile sneakers that combine functionality with style. As a result, consumers are increasingly willing to pay premium prices for footwear that delivers tangible health and comfort benefits. Sustained growth in this segment will depend on how effectively brands balance technical innovation with real-world usability.

Increasing emphasis on sustainable and eco-conscious innovations

Sustainability is becoming a defining force in the sneakers industry, influencing everything from raw material sourcing to end-of-life product strategies. Consumers in Europe and North America are increasingly favoring brands that adopt recycled uppers, bio-based cushioning, and transparent supply chains. Leading players such as ASICS have introduced products like NEOTIDE with a significant share of recycled inputs, while Adidas has substantially shifted toward recycled polyester across its portfolio. This shift is strongly driven by Gen Z consumers, who actively evaluate brand sustainability claims and are willing to pay a premium for credible eco-friendly offerings. Companies are leveraging this trend through circular initiatives such as product take-back programs, lifecycle-based marketing, and lower-carbon distribution models. These strategies not only strengthen brand positioning but also help maintain sales volumes despite higher pricing. At the same time, innovations like bio-based materials and circular production systems are setting new industry benchmarks, though scalability remains a challenge due to cost pressures and uneven consumer adoption. As a result, brands must carefully align sustainability goals with performance expectations and affordability to drive widespread market acceptance.

Expansion of digital platforms and e-commerce channels

The sneakers market ecosystem is undergoing a major shift as digital channels reshape how products are designed, sold, and experienced. Online sales are projected to grow steadily, with smartphones already accounting for the majority of transactions. Brands are increasingly prioritizing direct-to-consumer platforms to retain higher margins while leveraging first-party data to inform product launches and consumer targeting. Leading players have demonstrated strong digital traction, with billions in revenue now generated through online channels. At the same time, resale platforms are structuring the secondary market, turning limited-edition sneakers into tradable assets with significant market value. Technologies such as AI-driven size recommendations and augmented reality try-ons are reducing return rates and enhancing purchase confidence. These advancements are pushing traditional retailers to evolve beyond transactional models toward immersive, experience-led store formats. Ultimately, competitive advantage will depend on integrating digital innovation with compelling, human-centric brand interactions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium product pricing limiting accessibility | -0.60% | Global, most acute in price-sensitive Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Short-lived fashion trends limiting long-term demand | -0.40% | Global, impacting lifestyle segment in North America and Europe | Short term (≤ 2 years) |

| Widespread counterfeit products undermining brand trust | -1.00% | Global, concentrated in Asia-Pacific, Middle East, online marketplaces | Short term (≤ 2 years) |

| Supply chain challenges disrupting product availability | -0.80% | Global, acute where sourcing depends on Vietnam, China, Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium product pricing limiting accessibility

In the sneakers market, economic pressures and shifting purchasing power are reshaping footwear demand, particularly in emerging markets where consumers are becoming increasingly value-conscious. High-end products remain inaccessible to a large share of buyers, driving many toward mid-tier or alternative options. While premiumization supports stronger margins, it also constrains volume growth and limits penetration across broader consumer segments. In response, brands are introducing more accessible premium offerings to attract aspirational consumers without diluting their core identity. However, maintaining brand equity amid rising price sensitivity remains a critical challenge, especially as promotional strategies risk conditioning consumers to expect discounts. Long-term success will depend on optimizing manufacturing processes, improving supply chain efficiencies, and adopting smarter value engineering to manage costs effectively. Additionally, brands must strengthen perceived value through durability, innovation, and design differentiation rather than relying solely on branding. Striking the right balance between exclusivity and accessibility will be key to sustaining growth in a constrained consumer environment.

Widespread counterfeit products undermining brand trust

Illicit replication of branded apparel and footwear continues to pose a serious challenge to the global fashion ecosystem, spanning garments, shoes, and leather accessories. Beyond direct revenue leakage, counterfeit products dilute brand equity, weaken consumer confidence, and raise concerns around product quality and safety. The rapid expansion of online marketplaces has further enabled organized counterfeit networks to scale and operate with greater sophistication. In 2024, the European Anti-Fraud Office, in coordination with customs authorities across Austria, Belgium, Germany, Italy, and partner non-EU nations, confiscated more than 1.8 million fake fashion products valued at approximately EUR 180 million [3]Source: European Anti-Fraud Office (OLAF), "OLAF leads major crackdown on counterfeit fashion smuggling across Europe", anti-fraud.ec.europa.eu. At the same time, verification and authentication platforms are increasingly detecting and intercepting counterfeit footwear in circulation across resale channels. This underscores the rising dependence on third-party authentication solutions to protect brand credibility and reinforce consumer confidence in the sneaker market. The challenge is intensified as counterfeit and genuine goods often originate from overlapping manufacturing hubs, limiting the effectiveness of visual verification. While technologies such as blockchain-based tagging and Radio Frequency Identification (RFID) offer traceability, they introduce additional cost pressures, making industry-wide adoption complex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Athletic Sneakers Retain the Core

Athletic sneakers remain the cornerstone of the sneakers market, accounting for 55.87% of total share in 2025, underscoring their continued importance in driving overall category performance. Their leadership is anchored in continuous advancements in cushioning systems, stability features, and high-performance materials that cater to both serious athletes and everyday users. Increasing participation in fitness activities, particularly running, is further reinforcing demand, while brands are elevating value perception through innovations focused on comfort and injury prevention. At the same time, the integration of performance technologies into mainstream designs is making athletic footwear more versatile, extending its relevance beyond purely sports-driven use cases.

In parallel, lifestyle and fashion sneakers are emerging as the fastest-growing segment, projected to expand at a CAGR of 7.85% through 2031, fueled by rising consumer preference for multi-functional footwear. Buyers are increasingly seeking designs that seamlessly transition from active settings to casual and social environments, driving the popularity of hybrid silhouettes. This has led brands to blend technical features with minimalist aesthetics, retro influences, and trend-driven elements to capture younger demographics. The growing overlap between performance and lifestyle categories is reshaping market dynamics, pushing companies to strike a balance between maintaining technical credibility and delivering strong visual appeal to sustain differentiation in an increasingly competitive landscape.

By End User: Women’s Sneaker Demand Accelerates

In 2025, the men’s category continues to lead the athletic sneaker market, accounting for 53.45% of total volume, underpinned by strong demand in performance-driven categories such as basketball and training. Despite this dominance, the market landscape is gradually evolving as brands rebalance their focus across demographics. The children’s segment remains stable, supported by consistent replacement cycles due to rapid foot growth and increasing parental emphasis on durability, comfort, and foot health. Features such as reinforced materials and appealing designs further strengthen demand in this category. As a result, companies are increasingly tailoring product portfolios and retail strategies to address distinct usage occasions and consumer expectations across age groups.

At the same time, the women’s segment is emerging as the fastest-growing, projected to expand at a CAGR of 7.93%, signaling a meaningful shift in consumer dynamics. This growth is driven by greater female participation in sports, rising demand for performance-equivalent products, and a shift away from legacy design approaches toward inclusive sizing and purpose-built innovation. Leading brands are strengthening their positioning through athlete partnerships, community engagement, and enhanced customization options that align with lifestyle and fashion preferences. While men continue to prioritize performance and brand legacy, women increasingly value a balance of comfort, aesthetics, and authenticity, prompting brands to refine research and development, marketing, and merchandising strategies to better capture this accelerating opportunity.

By Price Range: Premium Segment Fuels Margin Expansion

In 2025, the mass segment accounted for a commanding 65.43% share, driven by its strong appeal among price-sensitive consumers and its widespread availability across large retail formats. This segment continues to anchor overall market volumes by delivering dependable performance at accessible price points, making it the backbone of category penetration. However, operators in this space are increasingly navigating margin pressures due to heightened price transparency in online channels and the rapid proliferation of private labels replicating core designs. As a result, maintaining competitiveness now requires sharper cost efficiencies and clearer value positioning to sustain scale without eroding profitability.

In contrast, the premium segment is emerging as the primary engine of value expansion, projected to grow at a 7.74% CAGR through 2031. This growth is fueled by affluent buyers and sneaker enthusiasts who prioritize innovation, brand narrative, and exclusivity over price sensitivity. High-end offerings leverage advanced materials, performance credibility, and limited-edition drops to command strong pricing power and reinforce aspirational appeal. Additionally, evolving “affordable premium” pockets, such as mid-tier pricing bands in emerging markets, are creating new opportunities to bridge accessibility with aspiration. Going forward, premium players must carefully balance scarcity with scale, ensuring that brand equity remains intact while tapping into expanding consumer willingness to trade up.

By Distribution Channel: Online Retail Channels Gaining Momentum

Specialty retail formats continue to anchor sneaker distribution, accounting for 36.35% of total market share in 2025, driven by their ability to deliver expert guidance, personalized fittings, and access to exclusive or limited-edition drops. These stores create a high-touch environment that resonates with consumers who value authenticity and product knowledge before making a purchase. At the same time, supermarkets and hypermarkets cater to value-conscious buyers through wide accessibility and competitive pricing, often driving spontaneous purchases. Department stores and brand-owned outlets further complement the landscape by blending assortment variety with curated brand storytelling and controlled retail experiences.

On the other hand, online retail stores are emerging as the fastest-growing channel, expanding at a CAGR of 8.22% through 2031, fueled by the rapid shift toward mobile-first shopping and seamless digital engagement. Consumers increasingly rely on online platforms for discovery, comparison, and purchase, supported by improved sizing tools, flexible return policies, and personalized recommendations. The market is steadily evolving toward an integrated omnichannel ecosystem, where physical stores enhance brand immersion while digital platforms maximize convenience and data-driven engagement. As brands strengthen direct-to-consumer strategies and retailers explore experiential formats like pop-ups and customization hubs, the focus is shifting toward creating a unified and engaging consumer journey across all touchpoints.

Geography Analysis

Asia-Pacific stands as both the largest and fastest-expanding sneakers market, accounting for 32.28% of global revenue in 2025 and projected to grow at a robust 8.52% CAGR through 2031. This momentum is fueled by rising disposable incomes, rapid urbanization, and a large youth population that increasingly views sneakers as lifestyle and status symbols. Markets such as China, India, and Southeast Asia are witnessing strong traction, supported by a mix of global brands and competitive regional players offering value-driven innovation. Expansion into tier-2 and tier-3 cities, along with the rise of affordable-premium offerings, is further accelerating penetration. However, supply chain dependencies and geopolitical uncertainties continue to pose structural risks.

North America and Europe represent mature yet highly profitable markets, driven by premiumization, strong brand equity, and evolving consumer expectations. In these regions, sneakers are positioned at the intersection of performance, fashion, and identity, supported by influencer culture and a well-established resale ecosystem that amplifies exclusivity. Europe, in particular, is at the forefront of sustainability, with consumers actively demanding eco-friendly materials and transparent sourcing practices. While market saturation limits volume growth, continuous innovation, limited-edition launches, and sustainability-led differentiation are key levers for maintaining engagement and pricing power.

Emerging regions including the Middle East, South America, and Africa present significant long-term growth opportunities, albeit from a smaller base. The Middle East is rapidly developing into a high-value market, driven by affluent consumers and a growing appetite for exclusive sneaker drops and resale culture. Meanwhile, South America and Africa benefit from young, urbanizing populations with increasing interest in global fashion and sports trends. Despite challenges such as economic volatility, lower purchasing power, and underdeveloped retail infrastructure, brands can unlock growth through localized strategies, flexible pricing models, and improved distribution networks tailored to regional dynamics.

Competitive Landscape

The global sneakers market reflects a moderately concentrated structure, with the top players collectively accounting for a sizeable yet non-dominant share, leaving ample opportunity for emerging brands to build traction. While industry leaders such as Nike, Adidas, New Balance, Sketchers, and Puma, among others continue to anchor the market through brand equity and global distribution, their dominance is increasingly contested by agile challengers. Notably, Nike and its Jordan line command a disproportionate share of the resale ecosystem, highlighting the power of cultural relevance in sustaining premium pricing. At the same time, a growing share of industry profits is being captured by newer, design-driven players, indicating that speed, innovation, and niche appeal are becoming as critical as scale.

Competitive intensity is further shaped by the rise of performance-focused disruptors and strategic global investments. Brands like On and Hoka have successfully differentiated themselves through advanced cushioning technologies and a strong focus on the running community, attracting consumers seeking alternatives to legacy offerings. Meanwhile, strategic moves such as Anta’s investment in Puma signal a broader shift, where Asian players aim to combine domestic scale with international brand heritage to strengthen global positioning. This evolving mix of incumbents, challengers, and cross-border collaborations is redefining how competitive advantage is built and sustained in the sneakers landscape.

Technology and operating models are playing a pivotal role in transforming the sneaker industry dynamics. Leading brands are increasingly leveraging digital ecosystems, with initiatives such as Nike’s SNKRS platform enabling controlled product drops that enhance exclusivity while generating granular consumer insights. At the same time, platforms like StockX are reinforcing trust in the resale market through AI-driven authentication systems, safeguarding both consumers and brand value. Additionally, vertically integrated players such as New Balance are investing in localized manufacturing capabilities in the United States and United Kingdom, enabling faster response times and supply chain resilience. Looking ahead, the interplay of digital innovation, supply chain agility, and culturally resonant branding will define the next phase of growth in the global sneakers market.

Sneakers Industry Leaders

-

Nike Inc.

-

Adidas AG

-

Puma SE

-

New Balance Athletics Inc.

-

Skechers USA, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nike launched its Air Max Day 2026 lineup featuring new innovations like the Air Max Liquid alongside retro revivals such as special-edition Air Max 95s and classic silhouettes. The release underscores Nike’s strategy of blending advanced cushioning technology with nostalgic designs, supported by collaborations and refreshed colorways of iconic models.

- February 2026: Comet’s launch on Myntra reflects a strategic shift from a direct-to-consumer model toward marketplace-led scale, enabling broader consumer reach while maintaining brand positioning. This development underscores the evolution of India’s sneaker market toward culture-driven growth, where brand storytelling, community engagement, and experiential marketing play an increasingly critical role in shaping consumer demand.

- November 2025: Footasylum entered a strategic partnership with Mad Agency to expand distribution across Germany and Austria, marking a key step in its European growth strategy. The collaboration leverages Mad Agency’s regional expertise and retail network to build multi-brand, multi-channel presence in the DACH region and strengthen Footasylum’s international footprint.

Global Sneakers Market Report Scope

| Atheltic Sneakers |

| Lifestyle and Fashion Sneakers |

| Men |

| Women |

| Children |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Atheltic Sneakers | |

| Lifestyle and Fashion Sneakers | ||

| By End User | Men | |

| Women | ||

| Children | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and projected sneakers market size?

The sneakers market is valued at USD 100.48 billion in 2026 and is forecast to climb to USD 143.66 billion by 2031, reflecting a 7.41% CAGR.

Which product type leads the sneakers market share?

Athletic sneakers contributed 55.87% of 2025 revenue, maintaining leadership through continual technology upgrades.

Why is the women’s sneaker segment expanding faster than men’s?

Larger investments in women’s leagues and gender-specific product design are driving a 7.93% CAGR for footwear aimed at female athletes and lifestyle users.

Are premium sneakers outperforming mass options?

Yes, the premium tier is projected to expand at 7.74% CAGR despite commanding a smaller base than mass-market lines.

Page last updated on: