Market Overview

| Study Period | 2021 - 2031 |

|---|---|

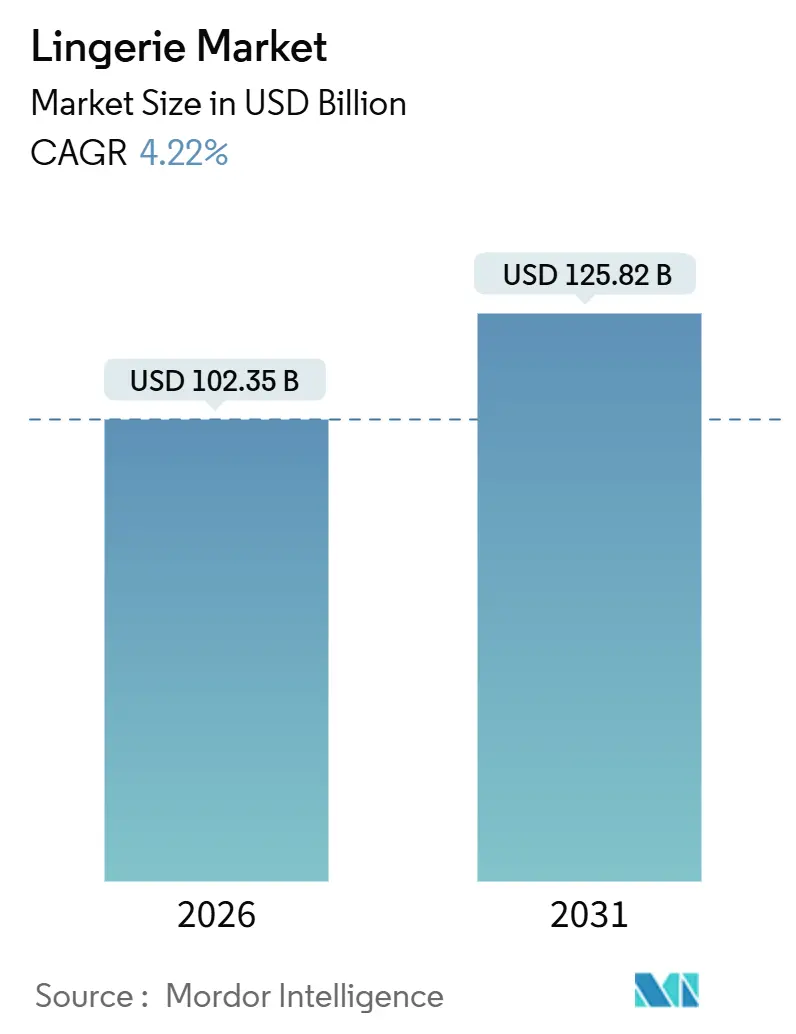

| Market Size (2026) | USD 102.35 Billion |

| Market Size (2031) | USD 125.82 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

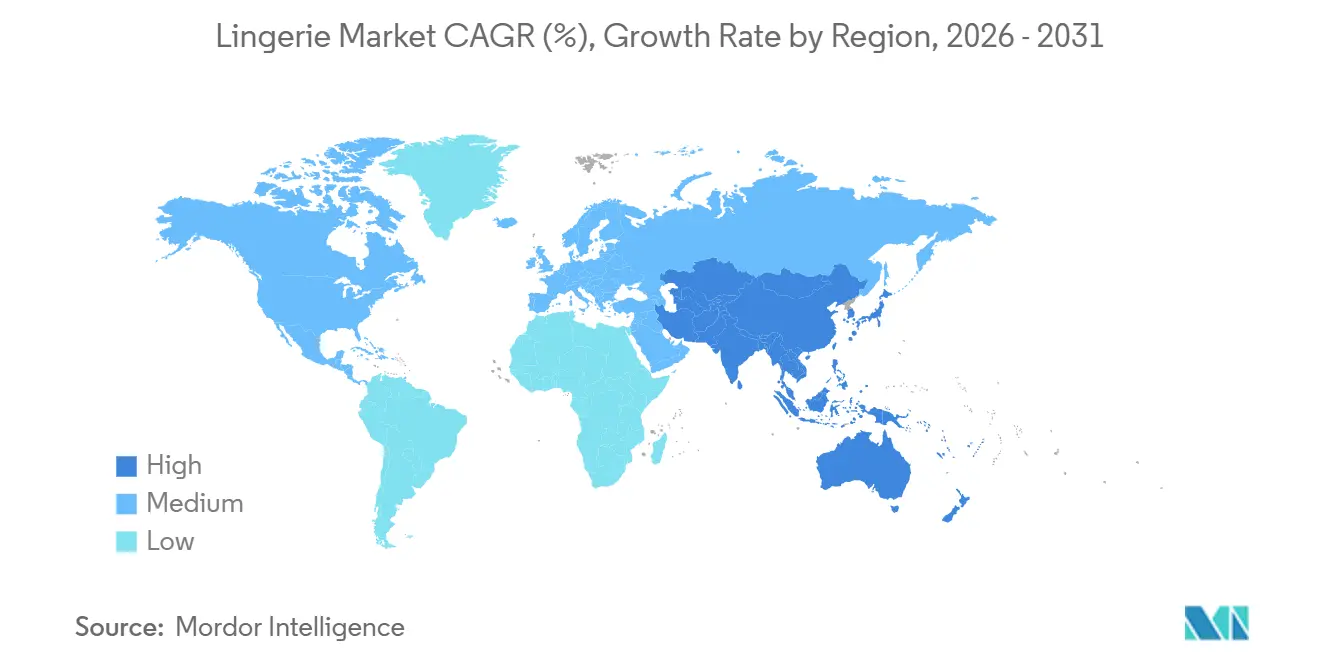

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

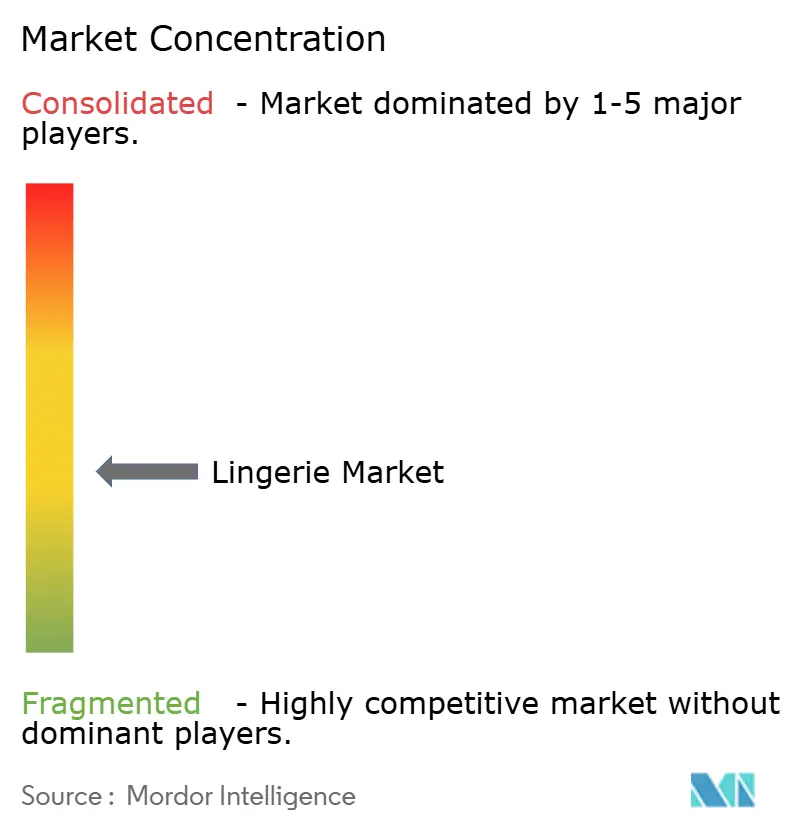

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lingerie Market Analysis by Mordor Intelligence

The lingerie market size is USD 102.35 billion in 2026 and is projected to reach USD 125.82 billion by 2031, reflecting a 4.22% CAGR. This growth is being driven by several key factors, including the ongoing trend of urbanization, the increasing participation of women in the workforce, and the rapid adoption of virtual fitting technologies. These elements are collectively propelling the lingerie market toward higher-margin digital sales channels. Brands are increasingly focusing on strategies such as offering extended sizing options, utilizing recyclable fibers, and leveraging data-driven product launches to meet evolving consumer demands. However, the market faces challenges, including fluctuations in raw material prices and the prevalence of counterfeit products, which are impacting overall profitability. The competitive landscape is undergoing a significant transformation, shifting away from traditional department-store aisles to omnichannel ecosystems. In these ecosystems, algorithm-driven fit recommendations and influencer-led storytelling are becoming critical factors in driving customer conversions. The Asia-Pacific region continues to be the epicenter of market growth, fueled by rising disposable incomes and changing consumer preferences. Meanwhile, North America and Europe are prioritizing sustainability initiatives, using eco-friendly practices and materials to justify premium pricing and appeal to environmentally conscious consumers.

Key Report Takeaways

- By product type, brassieres led with 58.36% revenue share in 2025; premium-priced brassieres are forecast to expand at a 9.62% CAGR through 2031.

- By material, synthetic blends commanded 45.41% of 2025 sales, yet recycled and bio-based fibers are positioned to grow at 9.36% annually to 2031.

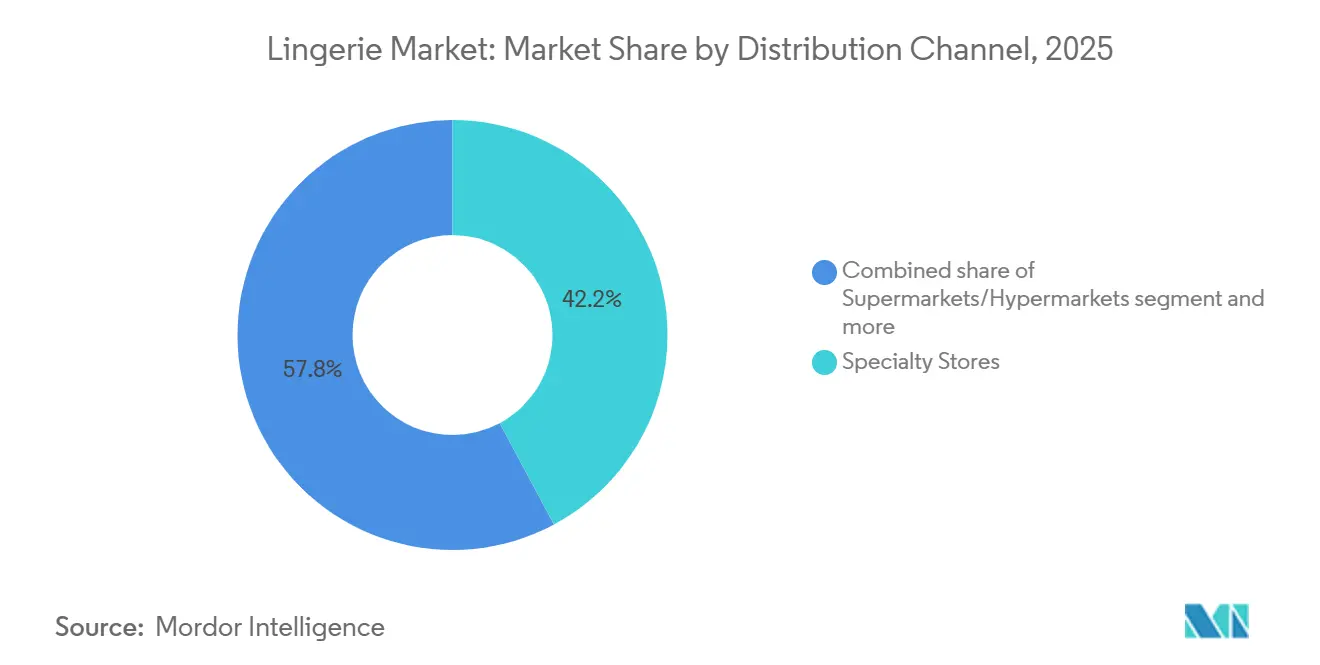

- By distribution channel, specialty stores held 42.17% of 2025 revenue, while online retail is set to advance at a 10.02% CAGR through 2031.

- By geography, Asia-Pacific accounted for 62.38% of 2025 turnover and is projected to post a 10.14% CAGR to 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lingerie Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising body positivity trends fuel demand for inclusive sizing and styles | +0.8% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Increasing disposable income supports premium and luxury lingerie purchases | +0.7% | Asia-Pacific core (China, India, Southeast Asia), spillover to Middle East | Short term (≤ 2 years) |

| Celebrity endorsements and social media marketing enhance brand visibility | +0.6% | Global, particularly North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Technological innovations like virtual fitting rooms improve customer experience | +0.9% | North America, Europe, and Asia-Pacific metropolitan areas | Medium term (2-4 years) |

| Rising demand for sustainable and ethically made lingerie influences buying choices | +0.7% | Europe leads, followed by North America and urban Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce improves accessibility and product variety | +1.0% | Global, with accelerated growth in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising body positivity trends fuel demand for inclusive sizing and styles

Body-positive messaging has evolved from being a focus of social-media activism to becoming a practical reality within supply chains. This shift has driven brands to expand their size ranges and feature models who represent their actual customer base, moving away from traditional runway standards. In 2024, ThirdLove launched a 78-size matrix, utilizing machine-learning algorithms trained on 15 million fit profiles. This approach aims to identify the ideal cup-and-band combinations for underserved body types. Similarly, in 2025, Savage X Fenty expanded its size range to include 4XL. This move was paired with celebrity endorsements that helped normalize lingerie for individuals with fuller figures. These changes are pressuring established players to adapt by updating manufacturing processes and retraining retail staff, which incurs significant short-term costs that smaller brands often cannot manage. Additionally, this shift complicates inventory management, as brands must carry a broader range of sizes without a proportional increase in sales velocity. This dynamic increases working-capital demands and the risk of markdowns. Although regulatory influence in this area remains minimal, voluntary commitments to size diversity are becoming an industry norm, driven by consumer backlash against brands perceived as exclusionary.

Increasing disposable income supports premium and luxury lingerie purchases

The premium lingerie segment is experiencing growth, driven by increasing disposable incomes in emerging markets. According to the Office for National Statistics [1]Office for National Statistics, "Average Household Income", ons.gov.ukdata from 2024, the median household disposable income in the United Kingdom was GBP 43,500. Rising household incomes in Asia-Pacific and the Middle East are fueling increased demand for premium lingerie, contrasting with the luxury-spending fatigue seen in mature markets. Bank of America's 2025 consumer survey highlighted that affluent shoppers in China and India are prioritizing intimate apparel, considering it both a functional need and an aspirational purchase. To address this trend, brands are introducing tiered collections, including mass-market lines for higher sales volumes and exclusive limited-edition silk or lace pieces to achieve better margins. This approach helps brands attract aspirational first-time buyers while retaining repeat customers willing to upgrade. However, the strategy carries the risk of brand dilution if premium and mass-market products are displayed in the same retail spaces or promoted through the same marketing channels. The impact is particularly significant in urban areas, where disposable income growth surpasses inflation, creating high-margin demand pockets within predominantly price-sensitive markets.

Technological innovations like virtual fitting rooms improve customer experience

Virtual fitting technology is overcoming a long-standing obstacle in online lingerie sales: the difficulty of determining fit before purchase. In 2024, Fit:match introduced 3D body-scanning kiosks that quickly capture 150 measurements in less than 30 seconds, providing size recommendations with only a 2% margin of error compared to in-person fittings. In 2025, Google launched an AI-powered virtual try-on tool that overlays lingerie onto user-uploaded images, adjusting for unique body shapes, skin tones, and lighting conditions. Adore Me partnered with Veesual in early 2026 to bring augmented-reality fitting to its mobile app. These advancements simplify the online shopping experience and open up markets in regions with limited physical store access or cultural sensitivities around in-person fittings. Additionally, the technology generates proprietary data on body shape distributions, helping brands optimize inventory management and product design. While adoption is primarily concentrated in North America and Europe, due to high smartphone usage and robust broadband infrastructure, pilot projects are being tested in urban India and Southeast Asia.

Celebrity endorsements and social media marketing enhance brand visibility

In 2024, Victoria's Secret overhauled its marketing strategy, moving away from its discontinued Angels franchise. Instead, it launched campaigns featuring Gigi Hadid and Hailey Bieber, focusing on authenticity rather than fantasy. Similarly, in 2025, Rihanna's Savage X Fenty capitalized on Instagram and TikTok, generating an impressive 1.2 billion impressions. This social media traction converted into direct-to-consumer sales, avoiding the challenges of wholesale markdowns. The data highlights a clear trend: influencer posts on digital channels provide a lower cost per acquisition compared to traditional mediums like television or print. Additionally, real-time engagement metrics enable brands to adjust creative content within days instead of waiting for quarterly updates. However, heavy reliance on celebrity endorsements carries risks. A brand's equity can be significantly impacted by an endorser's personal reputation, and algorithm changes on social platforms can drastically reduce organic reach. Meanwhile, smaller brands without access to celebrity endorsements are leveraging micro-influencers. These influencers, while charging lower fees, achieve higher engagement rates within targeted niche communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality products dilute brand value and consumer trust | -0.5% | Global, with highest incidence in Asia-Pacific and online marketplaces | Medium term (2-4 years) |

| Intense competition from local and unbranded players pressures pricing | -0.6% | Asia-Pacific, Latin America, and Middle East and Africa | Short term (≤ 2 years) |

| Conservative cultural norms in some markets discourage open lingerie advertising | -0.3% | Middle East, South Asia, and select African markets | Long term (≥ 4 years) |

| Limited access to quality lingerie in tier-2 and tier-3 cities restricts potential demand | -0.4% | India, China, Southeast Asia, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-quality products dilute brand value and consumer trust

Counterfeit lingerie not only undermines brand equity but also poses safety risks. Fake products frequently utilize substandard materials, leading to skin irritations or inadequate support. This issue is especially pronounced in e-commerce, where visual checks are limited, and consumers often prioritize price over authenticity. In 2024, United States Customs and Border Protection reported seizing nearly USD 5 billion worth of counterfeit luxury items, including fashion and footwear products [2]United States Customs and Border Protection, "The Truth Behind Counterfeits", cbp.gov. The problem is exacerbated on online marketplaces, where third-party platforms frequently list counterfeit lingerie at discounted prices, undermining legitimate retailers. In response, brands are turning to blockchain authentication and QR-code traceability to fight counterfeits. However, these solutions come with added costs and necessitate consumer education. Furthermore, the rise of counterfeits muddles demand signals for brands, making it challenging to discern between genuine shifts in consumer preference and a move towards cheaper imitations. This confusion complicates inventory management and the development of new products.

Intense competition from local and unbranded players pressures pricing

Local and unbranded manufacturers in India, China, and Southeast Asia reduce prices by 30% to 40% compared to multinational brands. They achieve this by utilizing lower labor costs, limiting marketing expenses, and distributing directly through neighborhood retailers. In 2024, India's Zivame and Clovia expanded into tier-2 cities, offering cotton bras priced between INR 300 to INR 500 (USD 3.60 to USD 6.00), significantly lower than the INR 800 to INR 1,200 (USD 9.60 to USD 14.40) range of international brands. In 2025, local players in China captured 55% of the mass-market segment by adapting designs to regional preferences and maintaining faster inventory turnover than global competitors. This pricing strategy pressures multinationals to either introduce budget sub-brands or accept reduced margins, while also limiting their ability to pass on rising input costs to consumers. Furthermore, unbranded manufacturers benefit from regulatory loopholes, often bypassing safety tests and labor standards, which add costs for compliant firms and create an uneven competitive environment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brassieres Anchor Revenue While Innovation Diversifies Offerings

Brassieres accounted for 58.36% of the 2025 revenue and are projected to grow at a rate of 9.27% through 2031. This growth is driven by the introduction of expanded size ranges and the use of moisture-wicking fabrics, enhancing their appeal for activewear. In 2024 and 2025, wireless and bralette styles gained popularity as work-from-home trends persisted, with consumers favoring comfort over traditional structured support. Briefs, the second-largest category, capitalized on the athleisure trend. Seamless and high-waisted designs in briefs increasingly blurred the distinction between intimate apparel and outerwear. Other product categories, such as shapewear, camisoles, and sleepwear, hold a smaller market share but are attracting significant innovation. Efforts are particularly focused on sustainable materials and adaptive designs tailored for postpartum and mastectomy customers.

The shift toward inclusive sizing is significantly altering manufacturing dynamics and economics. Brands are now required to stock between 50 to 80 SKUs per style, a substantial increase from the historical range of 20 to 30 SKUs. This shift has led to higher inventory carrying costs and an elevated risk of markdowns if demand forecasts are inaccurate, posing challenges for inventory management and profitability. Despite limited regulatory influence, voluntary commitments to size diversity are becoming increasingly important in the competitive landscape. These commitments are now viewed as essential by consumers, who are more likely to penalize brands perceived as exclusionary. As a result, inclusive sizing has emerged as a critical factor for brands aiming to maintain relevance and competitiveness in the market.

By Price Range: Premium Segment Outpaces Mass Despite Luxury Headwinds

Mass-market lingerie accounted for 75.84% of the revenue in 2025, targeting price-sensitive consumers in emerging markets and budget-conscious shoppers in developed economies. At the same time, the premium segment is projected to grow at a rate of 9.62%. This growth is driven by affluent buyers who, despite a general slowdown in luxury spending, are choosing to "trade up." In both China and India, affluent shoppers increasingly perceive intimate apparel as both a necessity and an aspirational luxury. Premium brands are distinguishing themselves through strategies such as limited-edition fabrics, celebrity collaborations, and unique retail experiences. For instance, La Perla opened a flagship store in Dubai in 2024, featuring private fitting suites and champagne service, aimed at high-net-worth individuals willing to spend between USD 200 to USD 500 per piece.

The gap between mass and premium segments continues to widen. Brands are introducing tiered collections to appeal to both segments, but this approach risks brand dilution, particularly when premium and mass products share the same retail or marketing platforms. In 2025, Hanesbrands launched a premium sub-brand that highlighted organic cotton and lace and was priced higher than its core Hanes line. However, the brand struggled to establish its luxury credibility among consumers. Conversely, premium brands like Chantelle and Calida are exploring more accessible price points to sustain volume, though they face challenges with margin compression affecting profitability. The premium segment's resilience is attributed to its relatively lower price point compared to luxury handbags or jewelry, making it a more attainable entry into luxury for younger consumers who are building brand loyalty.

By Material: Recycled Fibers Disrupt Synthetic Dominance

In 2025, synthetic materials, nylon, polyester, and spandex, comprised 45.41% of sales due to their stretch, durability, and cost benefits. However, recycled and bio-based fibers are projected to grow at an annual rate of 9.36%, driven by sustainability mandates and increasing consumer activism. Organic Basics secured GOTS approval for its entire cotton supply chain in 2025, ensuring traceability from farm to finished garment and eliminating harmful dyes. Cotton remains a preferred choice for everyday essentials, particularly in warmer climates where its breathability is prioritized over the performance advantages of synthetics. Silk and satin cater to the luxury segment, appealing to occasion-based purchases and gifting, though their market share is restricted by price sensitivity and maintenance requirements.

The European Union is introducing the Ecodesign for Sustainable Products Regulation, expected to take effect in 2027. This regulation will require apparel brands to disclose carbon footprints and design products with recyclability in mind, accelerating the shift toward bio-based materials. However, the higher costs of sustainable materials limit their adoption in price-sensitive markets, forcing brands to manage margin compression. Furthermore, certifications add audit expenses and supply-chain complexities, which disadvantage smaller players and consolidate market share among larger firms with greater resources. To balance performance, sustainability, and cost, brands are exploring blended fabrics that combine recycled polyester with organic cotton. However, a lack of consumer awareness continues to hinder widespread acceptance.

By Distribution Channel: Specialty Stores Lead Market Share as E-commerce Growth Continues

In 2025, specialty stores represented 42.17% of sales, leveraging trained fitters and curated selections to meet the needs of customers who prefer in-person service. Meanwhile, online retail is expected to grow at a rate of 10.02%, fueled by virtual fitting tools and influencer marketing that simplify the remote shopping experience. In early 2026, Adore Me partnered with Veesual to integrate augmented-reality fitting into its mobile app, resulting in an 18 percentage point reduction in return rates within the first quarter. Supermarkets and hypermarkets appeal to budget-conscious shoppers seeking basic cotton styles, while other channels, such as direct sales and subscription boxes, cater to niche segments that prioritize convenience or curated offerings.

Omnichannel strategies are increasingly merging sales channels. In 2024, Victoria's Secret relaunched its e-commerce platform, incorporating AI-driven size recommendations and same-day delivery in metropolitan areas, successfully reclaiming customers who had shifted to digital-first competitors. However, the growth of e-commerce has intensified price competition, as consumers can quickly compare products across numerous brands, compressing profit margins and benefiting companies with superior logistics. In rural areas, last-mile delivery costs remain a significant challenge, while smaller players in cross-border e-commerce face obstacles such as tariffs and customs issues that hinder international expansion. This shift has also fragmented customer acquisition efforts: brands must now optimize for search algorithms, social media platforms, and influencer partnerships simultaneously, increasing both marketing complexity and costs.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 62.38% of the revenue share and is expected to grow at a rate of 10.14% through 2031. This growth is primarily driven by increasing middle-class incomes in China and India. Notably, tier-2 and tier-3 cities in these countries are emerging as key areas for new customer acquisitions. Furthermore, the rising participation of women in the workforce supports market growth. For example, data from India's Ministry of Statistics and Programme Implementation showed an increase in female labor force participation from 33.4% in April–June 2025 to 33.7% in July–September 2025 [3]Ministry of Statistics & Programme Implementation, "PERIODIC LABOUR FORCE SURVEY (PLFS)", pib.gov.in. Although logistics costs in China's lower-tier cities are higher than in coastal hubs, discouraging brands from offering full assortments, e-commerce platforms like Tmall and JD.com are addressing these challenges by providing subsidized shipping and virtual fitting tools. Japan's market, which matured earlier, is led by brands like Wacoal and Triumph. These companies focus on innovations catering to an aging population, with products such as wider bands and softer fabrics gaining traction in 2024 and 2025. Southeast Asia's market is fragmented: Indonesia and Thailand prefer locally priced brands, while Singapore and Malaysia's higher disposable incomes and exposure to Western fashion trends drive premium market penetration.

North America and Europe together contributed approximately 30% of the 2025 sales. However, both regions faced challenges from market saturation and shifting consumer preferences. In Europe, a growing emphasis on sustainability increased demand for Global Organic Textile Standard (GOTS)-certified organic cotton and recycled polyester. This trend is expected to accelerate with the European Union's Ecodesign for Sustainable Products Regulation, set to take effect in 2027, which will require carbon-footprint disclosures. Canada and Mexico displayed differing market dynamics: Canada followed United States trends, focusing on inclusive sizing and digital platforms, while Mexico's market remained divided between premium imports and local unbranded products.

Urban centers in South America, the Middle East, and Africa drove the remaining market share. Brazil's lingerie market benefited from a strong domestic manufacturing base and a cultural preference for bold designs. However, economic instability and currency depreciation constrained growth in the premium segment. The Middle East's luxury demand, supported by high incomes in Gulf Cooperation Council countries, faced challenges due to conservative cultural norms that limited advertising and product visibility. As a result, brands relied on word-of-mouth and influencer partnerships. South Africa's market reflected broader African trends: organized retail penetration remained low, and distribution challenges in smaller cities hindered brands from tapping into latent demand. Nevertheless, the adoption of mobile commerce provided an opportunity to reach underserved consumers.

Regulatory Landscape

Lingerie brands operate under broad consumer-product, chemical, labeling, and trade compliance regimes that vary by region, but expectations for safety and sustainability are tightening. In the European Union, the General Product Safety Regulation (GPSR) became fully applicable on 13 December 2024, raising safety and market-surveillance expectations for consumer goods including apparel sold into the single market.

Sustainability and chemical restrictions are becoming more operationally material for intimate apparel due to close-to-skin use and complex fiber blends. The European Commission adopted detailed rules under the Ecodesign for Sustainable Products Regulation (ESPR) in February 2026 that prohibit the destruction of unsold apparel, clothing accessories, and footwear, with the prohibition taking effect on 19 July 2026. This adds pressure to inventory planning and reverse logistics. PFAS restrictions are also advancing through national actions, including France implementing Decree No. 2025-1376 in January 2026 and Denmark setting a July 2026 effective date for a national prohibition on PFAS-containing apparel and footwear, pushing suppliers toward verified chemical management and alternative finishes.

Competitive Landscape

The lingerie market is moderately fragmented, which creates a competitive environment where established companies benefit from scale advantages, while niche innovations continue to emerge. This structure supports the coexistence of traditional and emerging players, fostering competition and ongoing product development. The ecosystem promotes innovation while ensuring stability through established distribution networks and strong brand recognition. The major players operating in the market are Jockey International Inc., Hanesbrands Inc., Victoria's Secret and Company, Triumph International, and PVH Corp.

Significant opportunities exist in underserved segments, including extended sizing, adaptive designs for differently-abled consumers, and sustainable product lines with transparent supply chains. Emerging companies focus on these segments by building brand identities around specific market gaps rather than directly competing with established players. As consumer preferences shift toward inclusivity and sustainability, these niche markets offer substantial growth potential. Companies targeting these areas often develop specialized expertise and loyal customer bases.

Three distinct strategies define the market landscape. Established brands are strengthening their positions by investing in omnichannel infrastructures and obtaining sustainability certifications. Direct-to-consumer brands, on the other hand, leverage customer data and rapidly iterate products to capitalize on niche opportunities. Fast-fashion retailers like Inditex's Oysho and Fast Retailing's Uniqlo utilize their supply-chain scale to deliver trend-driven lingerie at competitive prices, pressuring mid-tier competitors. White-space opportunities include adaptive designs for postpartum and mastectomy customers, age-inclusive products for older demographics, and circular business models encouraging garment returns for recycling. Patent filings in 2024 and 2025 highlight advancements in moisture-wicking fabrics, seamless construction techniques, and biodegradable elastics, reflecting an industry-wide shift toward performance and sustainability.

Lingerie Industry Leaders

-

Jockey International Inc.

-

Hansbrands Inc.

-

Triumph International

-

PVH Corp.

-

Victoria's Secret and Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Supply-chain control and manufacturing footprint diversification are active whitespace areas as brands and suppliers respond to fit complexity, sustainability disclosure, and trade volatility. In early 2026, Journelle moved toward vertical integration by acquiring its own manufacturing factory in Italy, signaling how specialty and premium players can tighten lead times, protect craftsmanship-led positioning, and reduce reliance on multi-tier sourcing for small-batch styles.

Materials circularity and lower-impact inputs are also becoming more commercial, supporting differentiated fibers and processing technology in lingerie. In May 2026, Lindex and BASF partnered to introduce loopamid, a textile-to-textile recycled polyamide, into selected lingerie styles by early 2027. Triumph International and MARC O'POLO also announced a partnership to introduce SUGARCUP bio-based material into the MARC O'POLO Bodywear collection, with a 2027 launch. Oniverse Group announced a EUR 30 million investment in Sri Lanka in February 2026 to build a high-tech bra component manufacturing plant, while Prym Intimates opened a new facility in Hung Yen, Vietnam in March 2026, supporting component availability and faster replenishment cycles for brands selling through omnichannel models.

Recent Industry Developments

- May 2026: Hanes (under Gildan Activewear Inc.) launched a collaborative activewear collection with FP Movement, signaling a cross-category strategy that could influence lingerie-adjacent basics and comfort-led innerwear purchasing. The deal expands cross-brand reach and informs omnichannel assortment planning for value-seeking consumers.

- March 2026: Prym Intimates opened a new facility in Hung Yen, Vietnam, expanding its component production footprint for hooks, fastenings, and closures. The new plant strengthens regional supply chain resilience and reduces replenishment lead times for omnichannel retailers.

- February 2026: Oniverse Group announced a EUR 30 million investment to build a high-tech bra component manufacturing plant in Sri Lanka, broadening high-value production capabilities in the region. The project creates capacity for premium and mid-market brands and supports diversification of supply sources.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue earned from lingerie products sold to end users through online and offline channels, measured in USD and tracked across major regions.

Scope exclusions: Swimwear, beachwear, and nightwear are excluded so the sizing stays focused on core intimate apparel purchases.

Segmentation Overview

-

By Product Type

- Brassiere

- Briefs

- Other Product Types

-

By Price Range

- Mass

- Premium

-

By Material

- Cotton

- Silk and Satin

- Synthetic (Nylon, Polyester, Spandex)

- Recycled and Bio-based Fibers

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by aligning the product scope and price points with public classifications, and then checking how demand indicators move across regions. We reference sources such as UN Comtrade for cross border apparel trade flows, the World Bank and IMF for consumer spending and macro indicators, the US Bureau of Labor Statistics for apparel price inflation signals, and Eurostat for household consumption and retail patterns across Europe.

To ground company level assumptions, we also review annual reports, earnings decks, and other investor communications, followed by category coverage from industry associations and reputed business press. When needed, we use paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export records to validate directionally consistent trends. The examples listed above are not exhaustive, and many other public sources were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test the demand story behind the numbers, especially where product mix, promotional intensity, and channel shift can move the value quickly. We spoke with manufacturers, distributors, retailers, and category specialists, and we also included viewpoints from merchandising and supply chain roles across APAC, EMEA, and the Americas to confirm assumptions that were unclear from desk research.

This input also helped reconcile differences in how stakeholders describe lingerie sets versus broader innerwear baskets when estimating realized pricing and online share.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 16% | APAC: 48% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 19% | Managers: 48% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where apparel and intimate-wear spending signals are converted into a lingerie demand pool through region-specific penetration and mix assumptions, and then translated into value using price and channel structure. To keep the totals realistic, we corroborate the outcome with selective bottom-up approximations, such as supplier and retailer roll-ups from a sampled set, and simple volume-by-average-selling-price checks for major product families.

Key inputs that shape the model include women population by age cohort, per-capita apparel spend movement, online share shift in innerwear purchases, inflation and promotion cycles that influence realized prices, and trade and production direction that signals supply availability. For forecasting, we lean on multivariate regression so the market can respond to changes in disposable income, price inflation, and channel mix, and then scenario checks are run to reflect faster or slower premiumization. Where direct volume indicators are missing, gaps are handled through proxy ratios that are validated in interviews, for example by keeping stable product-mix splits unless channel and pricing feedback clearly supports a change.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals like trade direction, price indexes, and region-level retail momentum so the final values do not drift away from what the industry is experiencing. If a variance looks too large, assumptions are revisited, and targeted follow-ups are done with the most relevant respondents before internal sign-off.

A multi-step review is followed so calculation logic, currency conversions, and growth rates are consistent across the time series. The report is refreshed annually, and interim updates are made when material events change pricing, demand, or channel structure. Before delivery, a final pass is completed so clients receive the most current view that can be traced back to clear drivers.

Mordor Intelligence's Lingerie Market Size Versus Other Published Estimates

Different publishers often show different lingerie market sizes because they do not always count the same products, they may use different price points, and they may update key assumptions on different schedules. In this category, even small choices on what counts as lingerie and how channel pricing is treated can create large value gaps.

The main gap comes from whether adjacent apparel categories are counted, where Mordor Intelligence treats lingerie as intimate apparel only and keeps swimwear, beachwear, and nightwear outside the calculation, and this scope choice typically pulls totals away from broader apparel-style estimates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 99.12 B (2025) | |

| Global Consultancy A | USD 98.71 B (2025) | Uses a different forecast frame and may blend historical and forecasted pricing for 2025, which can slightly lower the realized value versus a scope that applies current-year channel price structure. |

| Industry Publisher B | USD 95.20 B (2025) | Price-range splits and regional weights appear to lean more toward economy products and mass channels, which can compress the blended average selling price and reduce the total for the same year. |

The comparison shows that the spread is mainly explained by scope and pricing construction, rather than by a disagreement on demand direction. When product inclusion is kept tight and price and channel assumptions are checked against real market signals, the final number becomes easier to reconcile and repeat year after year.

Key Questions Answered in the Report

What is the current global value of the lingerie market?

The lingerie market size is USD 102.35 billion in 2026 and is on track to reach USD 125.82 billion by 2031.

Which region is growing fastest for intimate apparel sales?

Asia-Pacific leads growth, expected to post a 10.14% CAGR through 2031 on the back of rising middle-class incomes and accelerated e-commerce adoption.

How are brands reducing fit-related returns in online lingerie sales?

Companies deploy 3D body-scanning kiosks and augmented-reality try-on tools, cutting return rates by up to 18 percentage points.

Why are recycled fibers gaining share in lingerie manufacturing?

Regulatory pressure and consumer demand for traceability are driving a 9.36% annual growth in recycled and bio-based fabrics despite their 15%–25% price premium.

Page last updated on: