Streetwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 218.3 Billion |

| Market Size (2031) | USD 264.76 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

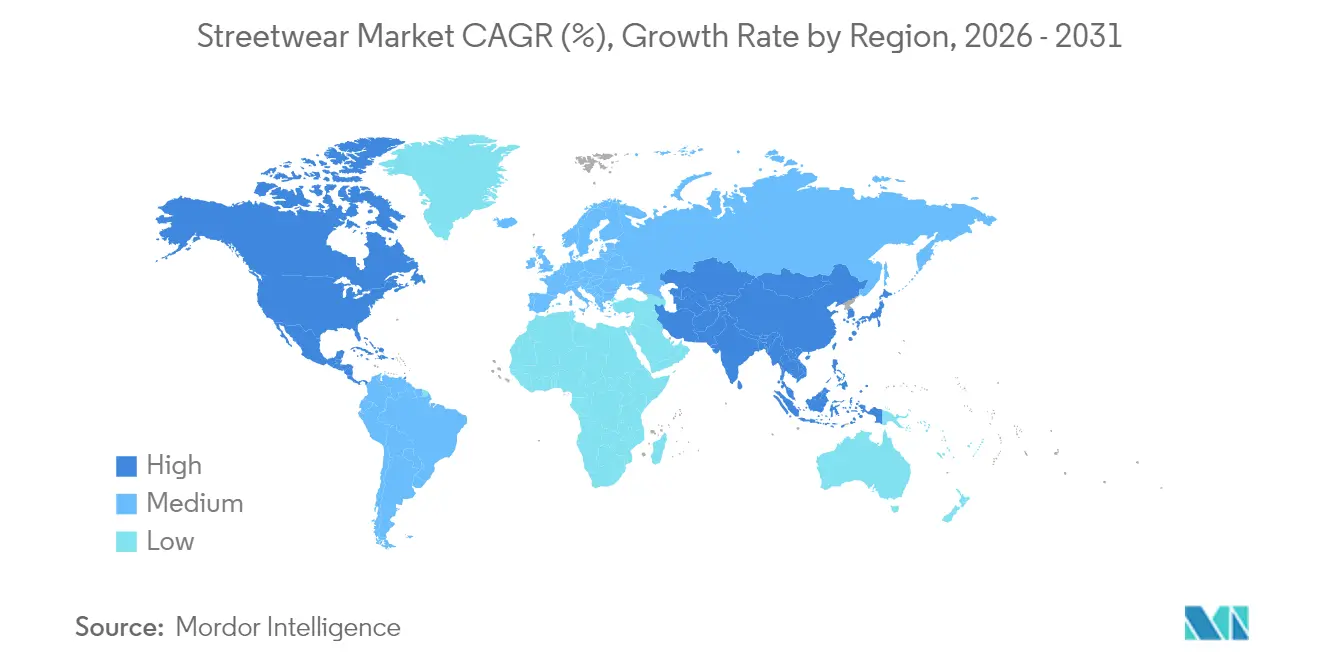

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Streetwear Market Analysis by Mordor Intelligence

streetwear market size in 2026 is estimated at USD 218.3 billion, growing from 2025 value of USD 210.03 billion with 2031 projections showing USD 264.76 billion, growing at 3.94% CAGR over 2026-2031. This steady expansion reflects rising Gen Z purchasing power, sustained digital adoption, and brand collaborations that keep the category culturally relevant. Majority of streetwear consumers are under 25, with this demographic prioritizing comfort (77.7%) and quality (67%) in their purchasing decisions. Asia-Pacific's manufacturing depth and e-commerce leadership position the region as both the largest and fastest-growing contributor, while supply-chain digitization helps brands balance limited-edition drops with consistent inventory flow. Furthermore, major brands like Nike, Inc., Adidas AG, and VF Corporation (Supreme) compete alongside specialized streetwear labels such as BAPE, Palace, and Stüssy, each leveraging distinct positioning strategies. The integration of social media platforms has transformed streetwear marketing, enabling brands to create viral product launches and maintain direct consumer engagement. Moreover, environmental consciousness among young consumers has pushed streetwear brands to incorporate sustainable materials and ethical manufacturing practices into their production processes. Thus, the convergence of youth culture, digital innovation, and sustainable practices continues to shape the streetwear market's evolution, suggesting sustained growth and adaptation to changing consumer preferences in the coming years.

Key Report Takeaways

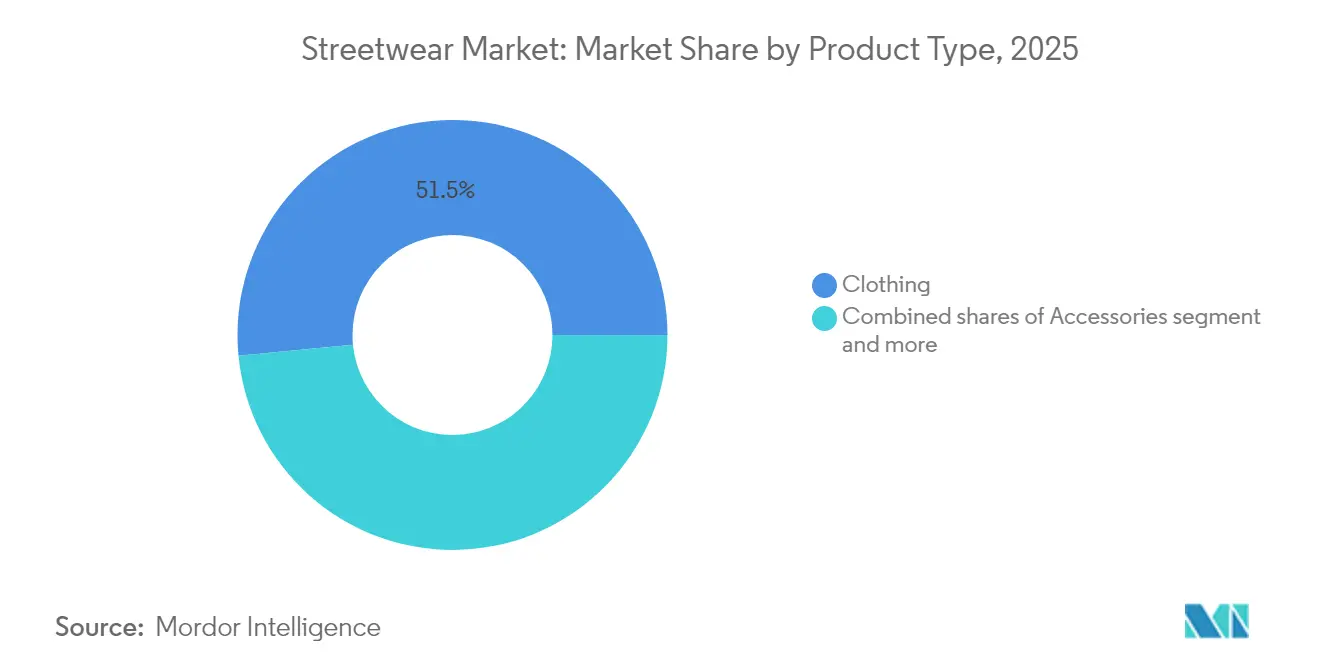

- By product type, clothing led with 51.54% revenue share in 2025; accessories are projected to expand at a 5.12% CAGR to 2031.

- By gender, male consumers held 57.38% of the 2025 streetwear market share, while unisex collections are advancing at a 4.26% CAGR through 2031.

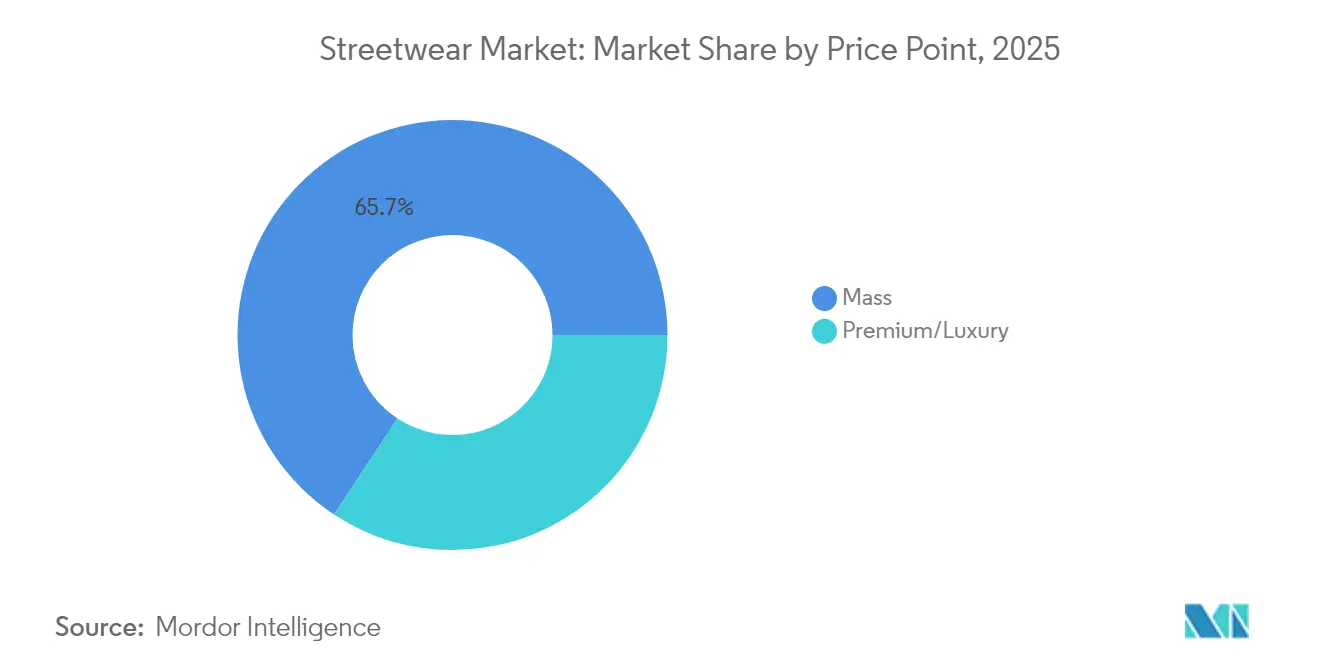

- By price point, the mass segment accounted for 65.72% of the 2025 streetwear market size; premium/luxury products are poised for 4.08% CAGR by 2031.

- By distribution channel, offline retail stores commanded 54.62% share in 2025, whereas online retail stores are growing at a 4.49% CAGR to 2031.

- By geography, Asia-Pacific captured 38.21% of 2025 revenue and is progressing at a 4.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Streetwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Youth culture and demographics | +1.2% | Global, with concentration in North America and Asia-Pacific | Long term (≥ 4 years) |

| Social media impact | +0.8% | Global, particularly strong in North America and Europe | Medium term (2-4 years) |

| Scarcity and exclusivity | +0.6% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Collaborations and partnerships | +0.5% | Global, with premium segments in developed markets | Short term (≤ 2 years) |

| Sustainability and ethical fashion | +0.4% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Digital and omnichannel engagement | +0.7% | Global, with e-commerce leadership in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Social Media Impact

Social media platforms function as the primary catalyst for streetwear trend propagation, with micro-influencers driving 53.6% of purchasing decisions among Gen Z consumers. Instagram's dominance in fashion discovery creates a direct pipeline from trend identification to purchase intent, fundamentally altering traditional marketing funnels. The platform's visual-first approach aligns perfectly with streetwear's aesthetic-driven culture, enabling brands to showcase products within lifestyle contexts rather than traditional retail environments. TikTok's algorithm-driven content distribution amplifies trend velocity, creating viral moments that can transform niche streetwear pieces into mainstream must-haves within days. This acceleration necessitates agile supply chain responses and inventory management strategies that traditional apparel companies struggle to implement. The democratization of fashion influence through social media also enables smaller streetwear brands to compete with established players through authentic storytelling and community building, disrupting traditional advertising spend hierarchies.

Scarcity and Exclusivity

The "drop culture" phenomenon transforms product scarcity from a supply constraint into a strategic marketing advantage, with brands deliberately limiting production to create urgency and desirability. This approach originated in Tokyo's streetwear scene with brands like GOODENOUGH and evolved into a mainstream strategy adopted by luxury fashion houses and major sneaker brands. The psychological impact of scarcity marketing drives immediate purchase decisions, with successful drops selling out within minutes and creating secondary market premiums that can exceed 200% of retail prices. Nike's strategic partnerships with Supreme exemplify this approach, where limited releases generate more brand value than traditional mass-market campaigns. The model's effectiveness stems from its ability to create community around exclusivity, transforming customers into brand advocates who actively promote upcoming releases. Furthermore, in July 2025, KFC celebrated National Fried Chicken Day on 6th July by partnering with streetwear brand ‘Market’ for a limited-edition merch collection including graphic t-shirts, hoodies, baseball hats, shorts, and more. In conclusion, drop culture has revolutionized modern marketing by transforming scarcity into a powerful tool for brand building, consumer engagement, and value creation.

Collaborations and Partnerships

Strategic collaborations between streetwear brands and luxury athleisure companies create new market categories while expanding consumer reach across demographic boundaries. For instance, in March 2025, Karl Kani and Culture Creators teamed up to launch the Creators Collection, a luxury athleisure brand designed to push creative and cultural boundaries. These partnerships leverage complementary brand strengths, with streetwear labels providing cultural authenticity while established companies contribute distribution networks and manufacturing capabilities. The collaboration model enables risk mitigation through shared investment and market testing, particularly valuable for entering new geographic markets or product categories. Recent examples include KITH's partnership with Disney, which successfully merged streetwear aesthetics with mainstream entertainment properties, demonstrating the model's versatility. Athletic brands increasingly partner with streetwear labels to access younger demographics, while luxury fashion houses collaborate with streetwear designers to inject contemporary relevance into traditional collections. For instance, Louis Vuitton, the epitome of luxury heritage, teamed up with Supreme, the rebellious New York streetwear brand. The collection featured LV monogrammed hoodies, skate decks, trunks, and leather accessories splashed with Supreme's bold red-and-white logo. Thus, the convergence of streetwear and mainstream fashion through strategic partnerships continues to reshape the market landscape, driving innovation and creating new opportunities for growth across the industry.

Sustainability and Ethical Fashion

The streetwear market is experiencing significant changes due to regulatory frameworks that mandate sustainable practices across the textile value chain. Regulators are increasingly mandating sustainable practices across the textile value chain, with the EU Strategy for Sustainable and Circular Textiles setting global compliance precedents. The strategy includes design requirements for durability, repairability, and recyclability, alongside mandatory recycled content specifications that will reshape production methodologies by 2030[1]Source: European Commission, "EU strategy for sustainable and circular textiles", environment.ec.europa.eu. Extended Producer Responsibility programs, implemented in Massachusetts (2025) and California, require brands to establish comprehensive recycling programs and assume end-of-life product responsibility. The Netherlands' Policy Programme for Circular Textile 2025-2030 demonstrates how government initiatives can accelerate industry transformation through specific targets and financial incentives[2]Source: Ministry of Infrastructure and Water Management, "Policy Programme for Circular Textile 2025-2030", government.nl. Brands holding sustainability certifications report sales increases up to 15%, indicating consumer willingness to pay premiums for environmentally responsible products. The regulatory momentum creates competitive advantages for early adopters while potentially disadvantaging companies that delay sustainability investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products | -0.9% | Global, particularly affecting premium segments | Medium term (2-4 years) |

| Rapid trend cycles | -0.6% | Global, with highest impact in fast fashion segments | Short term (≤ 2 years) |

| High production and retail costs | -0.8% | Global, with manufacturing concentration in Asia-Pacific | Medium term (2-4 years) |

| Supply chain disruptions | -0.7% | Global, with critical dependencies on Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products

The proliferation of counterfeit streetwear products through e-commerce platforms undermines brand value and consumer trust, with the U.S. Department of Homeland Security identifying rapid e-commerce growth as a primary facilitator of counterfeit trafficking [3]Source: U.S. Department of Homeland Security, "Combating Trafficking in Counterfeit and Pirated Goods", dhs.gov.Social media platforms inadvertently facilitate counterfeit distribution through targeted advertising and influencer partnerships that promote fake products to unsuspecting consumers. The challenge intensifies as counterfeiters adopt sophisticated manufacturing techniques and packaging that closely mimic authentic products, making detection increasingly difficult for consumers and enforcement agencies. Federal enforcement efforts have generally increased since 2001, but intellectual property enforcement remains a secondary priority for most agencies involved, limiting the effectiveness of anti-counterfeiting measures according to United States Government Accountability Office. The rise of e-commerce integration within social media platforms has created additional vulnerabilities, as counterfeiters exploit one-click purchasing features and direct messaging systems to reach potential buyers. This complex interplay between social media, e-commerce, and counterfeiting necessitates a more coordinated approach between platforms, regulatory bodies, and law enforcement agencies to effectively combat the proliferation of counterfeit goods.

Rapid Trend Cycles

The acceleration of fashion trend cycles through social media platforms creates unsustainable pressure on design teams and supply chains, forcing brands to prioritize speed over quality and innovation. TikTok's algorithm-driven content distribution can transform niche aesthetics into mainstream trends within days, leaving traditional design and production timelines obsolete. This velocity creates a paradox where brands must simultaneously maintain authenticity while rapidly adapting to trending aesthetics, often resulting in diluted brand identity and consumer confusion. The pressure to constantly produce new content and products increases operational costs while reducing profit margins, particularly affecting smaller streetwear brands with limited resources. Fast fashion competitors can replicate trending streetwear designs and bring them to market faster than original creators, undermining the value proposition of authentic streetwear brands. The trend acceleration also contributes to overconsumption and waste, contradicting the sustainability values that many streetwear consumers claim to prioritize, creating cognitive dissonance that may eventually impact purchasing behavior.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clothing Dominance Drives Accessories Innovation

Clothing maintains its leadership position with a 51.54% market share in 2025, reflecting its fundamental role in streetwear culture and self-expression. The clothing segment holds the largest share of the streetwear market as it represents the core element of streetwear culture. Streetwear items like graphic t-shirts, hoodies, and jackets appeal to diverse age groups and regions, making them the most accessible products in the market. However, accessories emerge as the fastest-growing segment with a 5.12% CAGR through 2031, driven by tech-integrated wearables and functional accessories that blur the lines between fashion and technology. Footwear represents the second-largest segment, with sustained growth driven by sneaker culture and limited-edition collaborations that create secondary market premiums.

Hats, bags, and traditional jewelry maintain steady demand through their role in completing streetwear aesthetics, while tech-integrated wearables falling on “others” represent the segment's future growth potential. The integration of digital technology into accessories creates new product categories, with smart jewelry and connected wearables gaining traction among tech-savvy consumers. Furthermore, the "Others" category, encompassing functional accessories and emerging product types, demonstrates the segment's innovation capacity and adaptability to changing consumer preferences. The accessories market demonstrates robust growth potential through both traditional items and technological innovation, with steady demand for classic streetwear accessories complemented by emerging opportunities in smart wearables and digital integration.

By Gender: Male Leadership Faces Unisex Disruption

Male consumers account for 57.38% of streetwear market share in 2025, reflecting the segment's historical roots in masculine-coded subcultures like skateboarding and hip-hop. However, unisex products represent the fastest-growing segment with a 4.26% CAGR through 2031, indicating a fundamental shift toward gender-neutral fashion that appeals to younger consumers' evolving identity concepts. This trend aligns with broader social movements toward gender inclusivity and challenges traditional fashion industry segmentation approaches. Female participation in streetwear culture continues expanding, driven by increased representation in traditionally male-dominated spaces and brands' recognition of women's purchasing power.

The unisex segment's growth reflects changing consumer preferences for versatile, inclusive products that transcend traditional gender boundaries. Brands increasingly design products with universal appeal, reducing inventory complexity while expanding potential customer bases. The introduction of Yoho! Girl magazine marked a turning point for female engagement in Chinese streetwear culture, demonstrating how targeted content can expand demographic reach. This gender evolution creates opportunities for brands to develop new product lines and marketing strategies that appeal to diverse consumer identities while maintaining authentic connections to streetwear's cultural foundations.

By Price Point: Mass Market Strength Enables Premium Growth

Mass market products dominate with a 65.72% share in 2025, reflecting streetwear's democratization and accessibility across income levels. This segment's strength enables brands to build customer bases and brand loyalty before introducing premium offerings. Premium and luxury streetwear segments grow at 4.08% CAGR through 2031, driven by consumers' willingness to pay higher prices for authenticity, exclusivity, and superior quality. The premium segment benefits from collaboration strategies and limited releases that create artificial scarcity and justify higher price points.

The mass market's dominance reflects streetwear's cultural accessibility and its role as a form of democratic fashion expression. However, the premium segment's faster growth indicates consumer sophistication and willingness to invest in quality pieces that serve as long-term wardrobe staples. Brands successfully navigate both segments by offering tiered product lines that maintain brand consistency while addressing different price sensitivities. The luxury streetwear segment particularly benefits from collaborations with high-end fashion houses and limited-edition releases that create collector value beyond functional utility.

By Distribution Channel: Offline Resilience Meets Online Acceleration

Offline retail stores maintain a 54.62% market share in 2025, demonstrating physical retail's continued relevance in streetwear culture where tactile experience and community building remain important. However, online retail stores represent the fastest-growing channel with a 4.49% CAGR through 2031, accelerated by digital-native consumers and enhanced e-commerce capabilities. The online channel's growth reflects improved logistics, virtual try-on technologies, and social media integration that recreates aspects of physical retail experience in digital environments.

Physical stores serve as cultural hubs and brand experience centers, particularly important for streetwear brands that emphasize community and authenticity. The offline channel's resilience stems from its ability to provide immediate gratification, social interaction, and product authentication that online channels struggle to replicate. However, successful brands increasingly adopt omnichannel strategies that integrate online and offline experiences, with digital platforms driving discovery and physical stores facilitating conversion.

Geography Analysis

Asia-Pacific's market dominance with a 38.21% share in 2025 reflects the region's unique combination of manufacturing capabilities, demographic advantages, and digital infrastructure development. The region's 4.33% CAGR through 2031 positions it as the primary growth engine for global streetwear expansion. China's role as both a major manufacturer and increasingly important consumer market creates synergies that benefit the entire regional ecosystem. The country's domestic platforms like Yoho!, demonstrate the potential for locally-developed streetwear ecosystems. Japan's influence on global streetwear culture continues through brands like A Bathing Ape (BAPE) and innovative retail concepts that blend physical and digital experiences. South Korea's K-pop cultural export amplifies streetwear adoption across the region and globally, creating cultural bridges that facilitate brand expansion.

North America maintains its position as the second-largest market, with established streetwear culture and high consumer spending power supporting both mass market and premium segment growth. The region's mature retail infrastructure and strong brand presence create competitive advantages for established players while presenting barriers for new entrants. Canada and Mexico benefit from USMCA (United States-Mexico-Canada Agreement) provisions that provide preferential access to the U.S. market, creating opportunities for regional supply chain optimization.

Europe demonstrates steady growth driven by sustainability initiatives and regulatory frameworks that favor established brands with compliance capabilities. The United Kingdom's post-Brexit trade relationships create new dynamics for brand distribution and manufacturing partnerships. Germany and France represent key markets with strong consumer spending power and established streetwear communities. The region's focus on sustainability aligns with younger consumers' values, creating opportunities for brands that successfully integrate environmental responsibility into their value propositions. However, the regulatory complexity and compliance costs may limit market entry for smaller international brands, potentially consolidating market share among established players with resources to navigate regulatory requirements.

Competitive Landscape

The streetwear market is moderately fragmented; the top tier of multinational athletic and lifestyle houses coexists with a long tail of culturally embedded independents. Nike, Inc., Adidas, and VF Corporation harness scale to secure prime materials and global distribution, yet they actively partner with niche creatives to preserve street-level relevance. Nike’s fiscal revenue of 2025 demonstrates the conglomerate’s capacity to weather cyclical downturns while funding R&D for new cushioning platforms. These companies are increasingly competing with both legacy luxury brands integrating streetwear aesthetics and digital-native startups that capitalize on social media trends and direct-to-consumer models.

The market is dynamic, with rapid trend cycles, frequent product drops, and a strong emphasis on exclusivity and community engagement. As streetwear continues to blend with mainstream and luxury fashion, the competitive environment is intensifying, pushing brands to innovate in design, marketing, and sustainability to capture and retain a diverse, global consumer base. Partnerships remain a dominant and effective competitive strategy for streetwear companies. For instance, in May 2025, Swiss athletic footwear company On partnered with Los Angeles streetwear brand PLEASURES and Austin-based running group The Loop to launch a new collection of footwear and apparel that combines performance features with street-style design elements.

Sustainability and innovation are becoming increasingly important as the streetwear market matures. Consumers are more conscious of environmental and ethical issues, prompting brands to adopt eco-friendly materials, transparent supply chains, and sustainable manufacturing processes. At the same time, technological advancements such as augmented reality (AR) try-ons, blockchain for authenticity verification, and smart fabrics are enhancing the consumer experience and product functionality. Companies that successfully integrate these elements while maintaining cultural relevance and exclusivity are positioned to thrive in a highly competitive landscape, driving the continued expansion of the streetwear market worldwide.

Streetwear Industry Leaders

-

Nike, Inc.

-

Addidas AG

-

PUMA SE

-

LVMH Moët Hennessy Louis Vuitton SE

-

VF Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Luxe streetwear company Summit Clothing launched a digital drive with agency PushON. The partnership saw the Manchester-based agency leading its paid media campaigns across Google and YouTube to expand the brand's online reach and improve return on ad spend.

- July 2025: Hot Wheels and B-Hype, the Dubai-born streetwear label, joined forces for an exclusive collaboration that reimagined speed and style through a fashion lens. The limited-edition Hot Wheels x B-Hype collection blended nostalgic design cues with street-level attitude and included exclusive apparel and Hot Wheels inspired pieces designed to resonate with die-hard collectors and a new generation of culture-makers.

- June 2025: Indian Motorcycle announced a first-of-its-kind brand apparel collaboration with renowned streetwear designer Jeremy Arviso. As an Indigenous streetwear designer, Arviso created designs inspired by his heritage. Past partnerships included the NFL, Nike, and the Phoenix Suns.

Global Streetwear Market Report Scope

Streetwear prioritizes comfort with loose, oversized fits and durable materials like cotton and denim. The streetwear market is segmented by product type, price point, and geography. By product type, the market is segmented into clothing, footwear, accessories, and others. By gender, the market is segmented into male, female, and unisex. By price point, the market is segmented into mass and premium/luxury. By distribution channel, the market is segmented into offline retail stores and online retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Clothing |

| Footwear |

| Accessories |

| Others |

| Male |

| Female |

| Unisex |

| Mass |

| Premium/Luxury |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Clothing | |

| Footwear | ||

| Accessories | ||

| Others | ||

| By Gender | Male | |

| Female | ||

| Unisex | ||

| By Price Point | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current streetwear market size?

The streetwear market size reached USD 218.3 billion in 2026 and is projected to rise to USD 264.76 billion by 2031 at a 3.94% CAGR.

Which region leads the streetwear market?

Asia-Pacific captured 38.21% of global revenue in 2025 and is also the fastest-growing region with a 4.33% CAGR through 2031.

What product category is growing fastest in streetwear?

Accessories are expanding at a 5.12% CAGR, driven by tech-integrated wearables and functional add-ons that complement core apparel collections.

What role does e-commerce play in streetwear growth?

Online channels are the fastest-growing distribution avenue, advancing at a 4.49% CAGR as mobile-first consumers seek frictionless checkout, live-streamed launches, and rapid delivery.

Page last updated on: