Sandals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

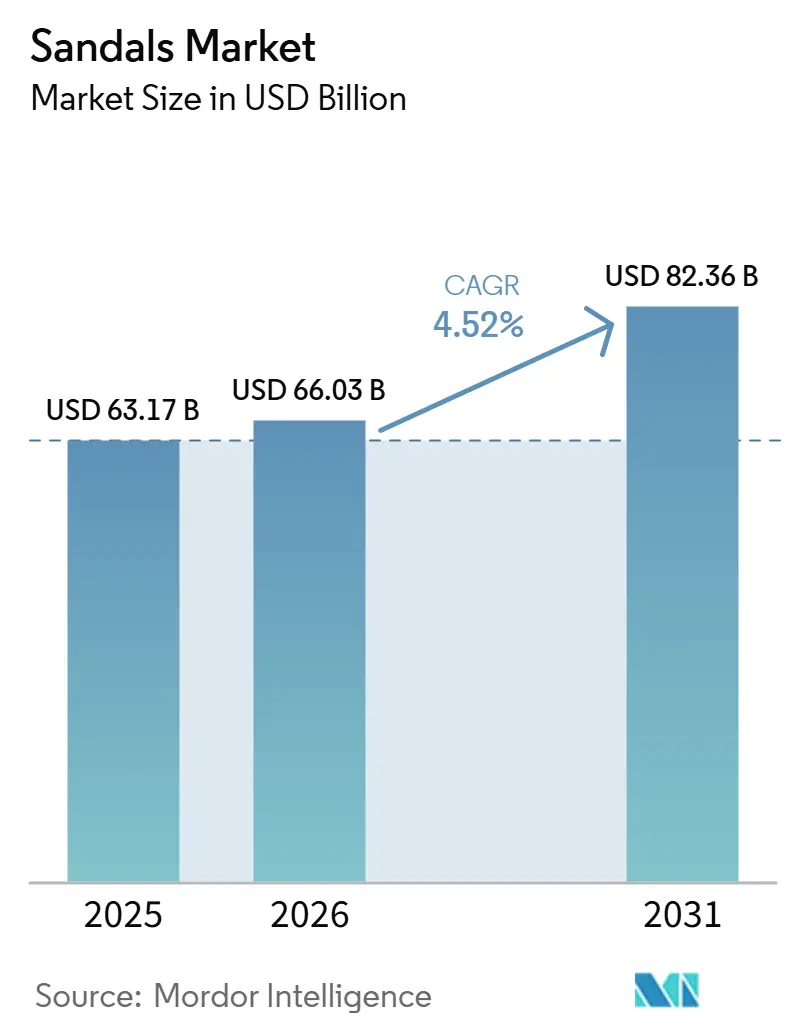

| Market Size (2026) | USD 66.03 Billion |

| Market Size (2031) | USD 82.36 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sandals Market Analysis by Mordor Intelligence

The sandals market size was valued at USD 63.17 billion in 2025 and estimated to grow from USD 66.03 billion in 2026 to reach USD 82.36 billion by 2031, at a CAGR of 4.52% during the forecast period (2026-2031). This trajectory reflects a structural shift in footwear consumption, driven by the casualization of workplace norms, increased awareness of foot health, and climate volatility, boosting demand for breathable, open-toe designs in tropical and temperate regions. Direct-to-consumer (DTC) models are disrupting the traditional dominance of brick-and-mortar formats, while tariff fluctuations are prompting brands to diversify sourcing away from China toward countries such as Vietnam, Cambodia, and India. In the Asia-Pacific region, India’s monsoon-driven consumption flip-flop and Indonesia’s year-round tropical climate anchor the market, while the Middle East and Africa are expected to see the fastest growth. Rising disposable incomes in countries such as Saudi Arabia, the United Arab Emirates, and Nigeria, combined with desert climates that make closed-toe footwear impractical, are driving this regional expansion. Additionally, regulatory changes, such as the European Union’s Ecodesign for Sustainable Products Regulation, are accelerating investments in bio-based materials and circular design, increasing compliance costs and raising barriers to entry.

Key Report Takeaways

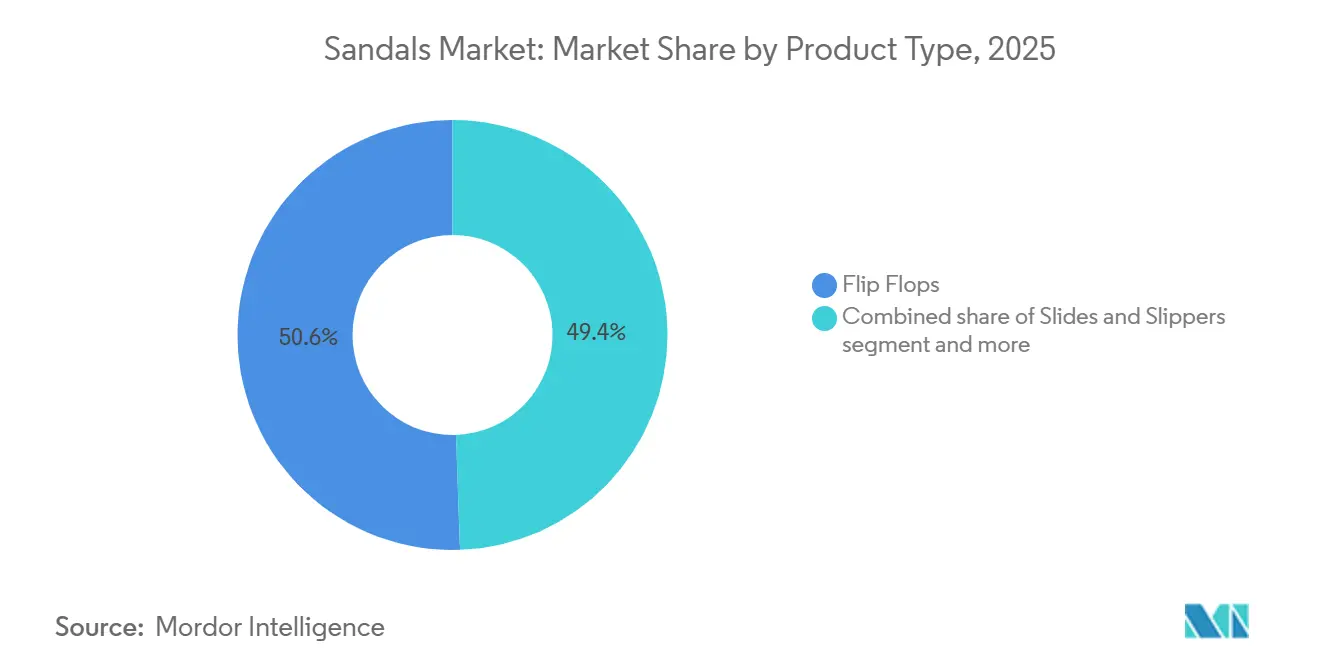

- By product type, flip flops led with 50.56% of the sandals market share in 2025, while slides and slippers are projected to expand at a 5.58% CAGR through 2031.

- By end user, women accounted for 52.13% of the value in 2025; men are forecast to grow fastest at a 5.72% CAGR over 2026-2031.

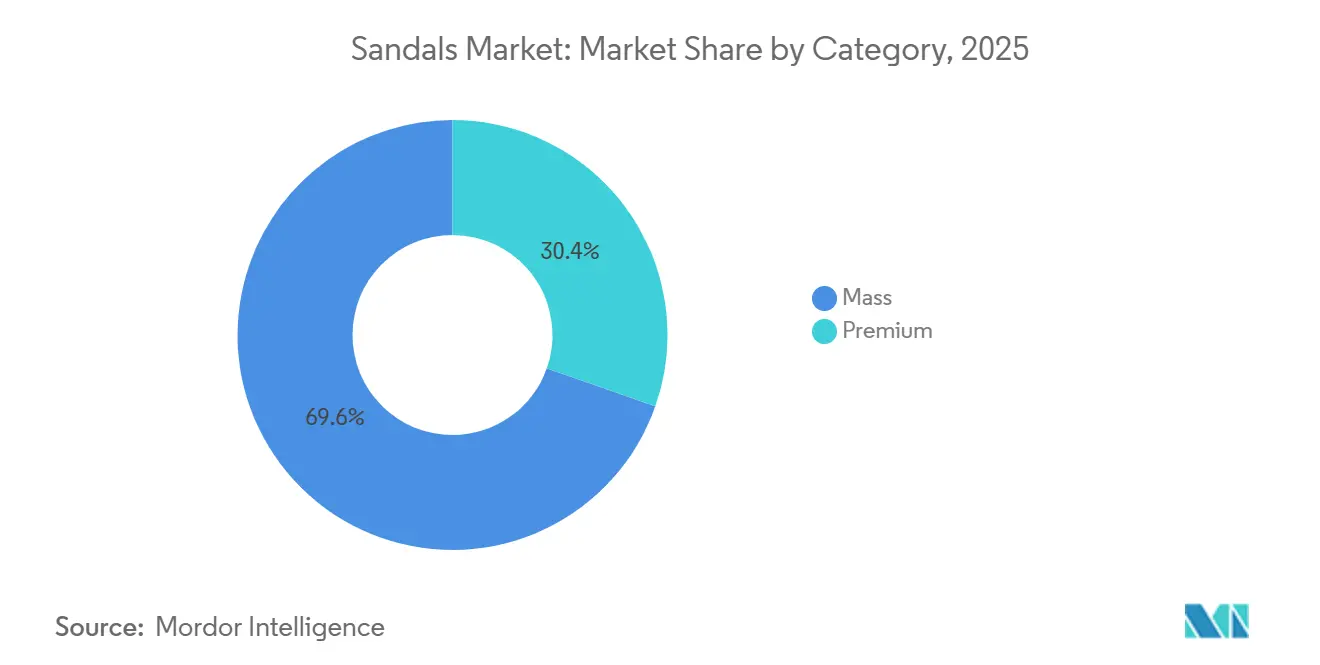

- By category, mass offerings held 69.62% of the 2025 sandals market share, but premium lines are set to increase at a 5.37% CAGR over 2026-2031.

- By distribution, offline retail accounted for 67.23% of 2025 spending, yet online channels are set to grow at a 5.46% CAGR through 2031.

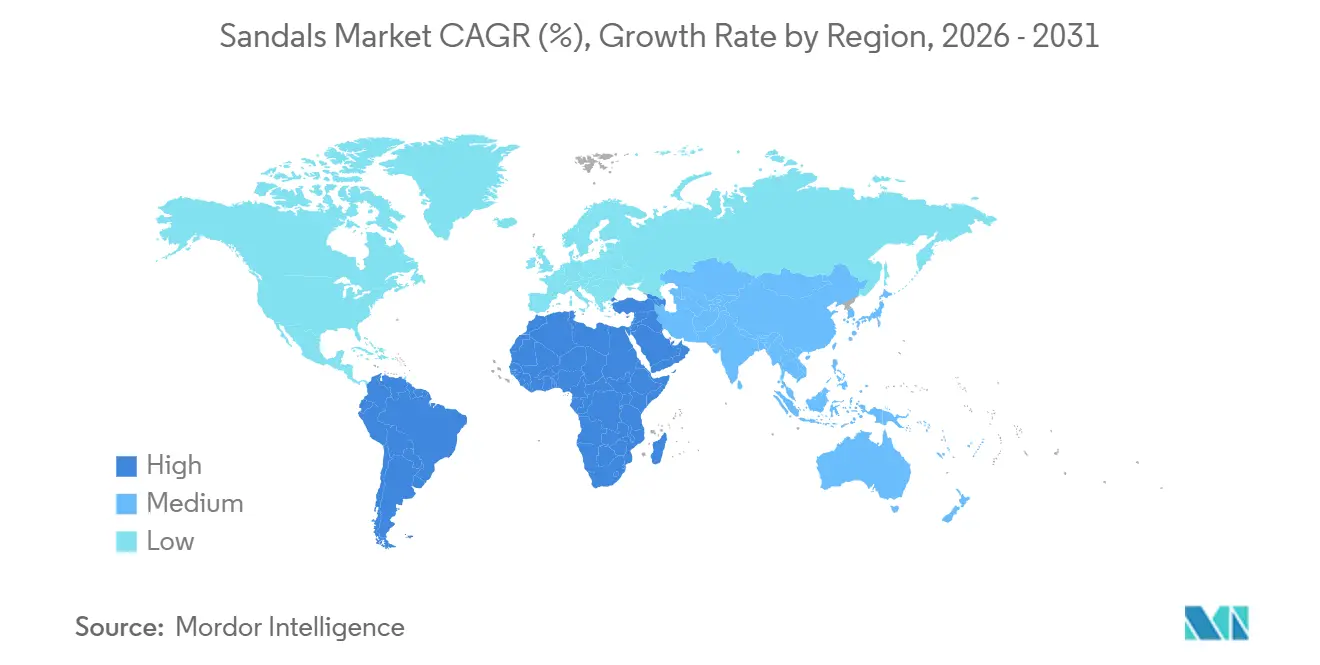

- By geography, Asia-Pacific commanded 37.58% of 2025 revenue; the Middle East and Africa are expected to post the fastest regional growth at a 6.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sandals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for comfortable, casual, and versatile footwear | +1.2% | Global, with early gains in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Surging demand for foot health and ergonomic support | +0.9% | Global, concentrated in aging demographics across North America, Europe, and Japan | Long term (≥ 4 years) |

| Athleisure and casualization of workplace dress codes | +0.8% | North America and Europe, spillover to corporate hubs in Asia-Pacific | Medium term (2-4 years) |

| Sustainable and eco-friendly materials innovation | +0.7% | Europe (regulatory-driven), North America (consumer-driven), emerging in Asia-Pacific | Long term (≥ 4 years) |

| Preference for breathable footwear in tropical climates | +0.6% | Asia-Pacific, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Growing outdoor recreation and travel-driven usage | +0.5% | Global, with peak demand in coastal and resort destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for comfortable, casual, and versatile footwear

The global demand for comfortable, casual, and versatile footwear is increasing, driven by the casualization of lifestyle and workplace attire. Hybrid work models have normalized comfort-oriented choices, positioning sandals as year-round essentials rather than seasonal footwear. This trend is particularly evident in North America and Europe, where evolving business-casual norms now permit open-toe footwear in non-hazardous office environments. Consumers are seeking footwear that transitions seamlessly across professional, social, and leisure settings, prompting brands to develop designs that integrate ergonomic functionality with refined aesthetics. Features such as modular footbeds, adjustable straps, and lightweight hybrid constructions reflect this shift, with products like Birkenstock’s “Arizona Soft Footbed” exemplifying the combination of comfort-focused engineering and versatile styling suitable for both office and casual use. Furthermore, the use of materials such as memory foam and bio-based soles aligns with the increasing consumer preference for sustainable comfort, driving the transformation of the global sandals market through adaptability, innovation, and eco-conscious design.

Surging demand for foot health and ergonomic support

Orthopedic and biomechanically engineered sandals are gaining traction as aging populations and sedentary lifestyles contribute to an increase in foot-related issues such as plantar fasciitis, flat feet, and joint pain. Brands like Oofos have capitalized on this trend with products such as the OOahh recovery slide, priced at USD 60, which uses proprietary OOfoam technology to absorb 37% more impact than standard EVA and reduce skeletal load rates by up to 88%, earning certification from the American Podiatric Medical Association (APMA). Additionally, foot orthoses integrated into sandals have been shown to significantly improve gait parameters and alleviate pain in individuals with flat feet, further validating the clinical efficacy of ergonomic designs. This growing body of evidence is driving increased recommendations from podiatrists and expanding insurance reimbursement eligibility in select markets. As a result, the market is broadening beyond wellness-focused consumers to include individuals with medically diagnosed foot conditions. Furthermore, advancements in materials and design, such as arch-support technologies and cushioned footbeds, are enabling brands to cater to a wider demographic seeking both comfort and therapeutic benefits.

Sustainable and eco-friendly materials innovation

Sustainable and eco-friendly materials innovation is becoming a critical growth driver in the sandals market, as both regulatory pressures and shifting consumer preferences demand environmentally responsible practices. The European Commission's Ecodesign for Sustainable Products Regulation prohibits the destruction of unsold textiles and footwear, compelling brands to design for durability, repairability, and end-of-life recovery [1]Source: European Commission, "New EU Rules to Stop Destruction of Unsold Clothes and Shoes," ec.europa.eu. This regulatory push is encouraging brands to adopt circular-economy principles and integrate sustainable materials into their supply chains. Initiatives like Fashion for Good's "The Next Stride" program are accelerating this transition by fostering collaboration between brands and material innovators to develop bio-based and recycled inputs. For instance, advancements in algae foam, mycelium leather, and chemical recycling technologies are enabling the production of eco-friendly soles and straps at a commercial scale. Additionally, partnerships such as Vivobarefoot's Circ collaboration are piloting closed-loop systems that reduce waste and carbon footprints. These innovations not only align with environmental goals but also resonate with eco-conscious consumers, who increasingly prioritize sustainability in their purchasing decisions.

Preference for breathable footwear in tropical climates

The demand for breathable footwear in tropical climates across Asia-Pacific, the Middle East, and Africa is driven by persistent heat and humidity, necessitating effective ventilation and moisture control. Sandals are particularly favored in these regions for their ability to reduce sweat buildup and lower the risk of fungal infections. Countries such as Indonesia, Thailand, and the Philippines exhibit consistently high year-round demand for flip-flops and open-toe designs suited to warm conditions. Rising disposable incomes are reshaping consumer preferences, with a noticeable shift from unbranded, basic options to branded, ergonomic designs, especially in emerging markets like Saudi Arabia, the United Arab Emirates, and Nigeria, where style, durability, and comfort are key considerations. To meet these evolving demands, brands are leveraging climate-responsive materials and foot health innovations, as exemplified by Havaianas’ breathable rubber flip-flops, which combine functionality with lifestyle appeal. Features such as improved airflow, quick-drying materials, and flexible soles further enhance the year-round relevance of sandals, making the tropical climate a critical growth driver in the global sandals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonality and weather-linked demand fluctuations | -0.3% | Temperate regions: North America, Europe, parts of Asia-Pacific | Short term (≤ 2 years) |

| Mandatory workplace safety regulations require closed footwear | -0.2% | Global | Long term (≥ 4 years) |

| Counterfeit and grey-market products eroding brand equity | -0.4% | Asia-Pacific (China, Vietnam, Indonesia, Philippines), Africa, Latin America | Medium term (2-4 years) |

| Environmental concerns regarding disposable footwear in fast fashion | -0.2% | Europe (regulatory-driven), North America (consumer activism), emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory workplace safety regulations require closed footwear

Mandatory workplace safety regulations present a significant challenge to the global sandals market by restricting their use in industrial and occupational environments. Industries such as manufacturing, construction, healthcare, and laboratories mandate closed-toe protective footwear to mitigate risks associated with impact, punctures, or chemical exposure. For example, the United States Occupational Safety and Health Administration's standard 29 CFR 1910.136 explicitly discourages open-toe footwear, establishing a regulatory framework adopted by many global markets [2]Source: Occupational Safety and Health Administration, "29 CFR 1910.136 Protective Footwear Standards," osha.gov. This limits the penetration of sandals in employment-intensive sectors where safety compliance is critical. The effect is particularly pronounced in emerging economies experiencing rapid manufacturing growth, where adherence to international safety standards is increasingly enforced. Furthermore, as automation and robotics reduce the reliance on human labor in hazardous roles, the remaining workforce is subject to stricter footwear compliance requirements. These regulatory constraints confine sandals primarily to casual, leisure, and lifestyle segments, allowing the market to grow in fashion and comfort categories while restricting expansion into professional and industrial applications.

Counterfeit and grey-market products eroding brand equity

Counterfeit and grey-market products continue to erode brand equity in the sandals market, particularly in regions like Asia-Pacific and Africa, where enforcement mechanisms struggle to keep pace with growing demand and the proliferation of cross-border e-commerce platforms. These platforms enable low-cost replicas to reach consumers rapidly, often bypassing regulatory scrutiny. For instance, enforcement authorities in the Philippines seized counterfeit Crocs and Nike sandals worth USD 3.8 million in 2025, while Vietnam confiscated over 7,000 counterfeit units within the first five months of the same year [3]Source: Philippine News Agency, "PHP 216 Million Counterfeit Footwear Seized," pna.gov.ph. Such activities not only dilute brand value but also erode consumer trust and loyalty, as counterfeit products often fail to meet the quality and safety standards of genuine brands. The grey market, where unauthorized distributors sell genuine products outside official channels, further complicates the issue by undercutting pricing strategies and disrupting authorized supply chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Slides Outpace Traditional Flip Flops

Flip flops accounted for 50.56% of the market value in 2025, driven by their affordability, widespread use in tropical climates, and deeply ingrained consumer preferences. Their lightweight design, ease of use, and versatility make them a staple for casual and outdoor activities, particularly in warm-weather regions. Flip flops are especially popular in markets like Asia-Pacific and Latin America, where they are considered essential footwear for daily use. However, this segment faces increasing margin pressures as mass-market retailers focus on high-volume sales rather than product differentiation. Despite these challenges, premium flip flops are emerging as a growing sub-segment, with brands like Havaianas and Reef introducing designs that incorporate sustainable materials, enhanced comfort features, and stylish aesthetics to appeal to environmentally conscious and fashion-forward consumers.

Slides and slippers are projected to grow at a 5.58% CAGR through 2031, fueled by advancements in athletic-recovery footwear and premium product positioning that support higher average selling prices. Slides, in particular, are evolving from basic casual footwear to versatile options that blend style, comfort, and performance. Athletic slides are gaining traction through collaborations that merge performance and lifestyle appeal. For instance, FootJoy partnered with Oofos in 2025 to introduce a co-branded recovery slide priced at USD 70. This product leverages Oofos' impact-absorption technology and FootJoy's established golf-apparel distribution network to target affluent, health-conscious consumers. Additionally, the demand for slippers has surged due to the rise in remote work and home-centric lifestyles, with consumers seeking comfortable yet stylish options for indoor use. Meanwhile, the "Others" segment, which includes gladiator sandals, espadrilles, and hybrid designs, is gaining momentum in premium channels.

By End-User: Men's Segment Narrows the Gender Gap

Women accounted for 52.13% of end-user demand in 2025, reflecting historical fashion norms and higher footwear ownership per capita. Women's sandals, while still dominant, are fragmenting into micro-segments such as gladiator styles, espadrille wedges, and minimalist slides, complicating inventory planning and diluting marketing efficiency. The growing emphasis on sustainability and comfort has led to increased demand for eco-friendly materials and ergonomic designs in women's sandals. Brands that can unify product lines under a single ergonomic or sustainability narrative, as Birkenstock has done, are capturing disproportionate share in both genders. Furthermore, premium brands are leveraging collaborations with fashion influencers and designers to create limited-edition collections, driving exclusivity and higher price points in the women's segment.

Men are advancing at 5.72% CAGR through 2031, the fastest of any demographic, as casualization erodes stigma around open-toe footwear in professional and social settings. Athletic slides from Nike, Adidas, and Puma, historically marketed to male athletes for post-game recovery, are now positioned as lifestyle essentials. The men's sandal market is witnessing a surge in demand for versatile designs that blend style and functionality, such as leather sandals with adjustable straps and hybrid models suitable for both casual and semi-formal occasions. Fashion trends are accelerating men's adoption. Leather sandals peak in search interest during late summer and early autumn, indicating that men are integrating open-toe footwear into transitional wardrobes rather than confining it to beach vacations. The children's segment, though smaller in absolute value, is benefiting from parents' willingness to invest in ergonomic designs that support healthy foot development, with APMA-certified sandals from Keen and Merrell gaining share in outdoor and specialty retail channels.

By Category: Premium Gains Ground on Scarcity and Clinical Validation

The mass segment commanded 69.62% of the market value in 2025. Mass-market players face margin compression from tariff volatility and counterfeit competition. Tariff headwinds are expected to cost Crocs USD 80 million annually in 2026, compressing operating margins and forcing the company to accelerate manufacturing shifts to Vietnam, Indonesia, and India. Flip flops, a key product in the mass segment, continue to dominate due to their affordability, lightweight design, and suitability for casual and outdoor activities. Their popularity is particularly strong in tropical and warm-weather regions, where they are a staple for daily wear. However, the segment faces challenges, including limited product differentiation and increased competition from counterfeit products. To counteract these pressures, brands are focusing on introducing eco-friendly materials and innovative designs to appeal to environmentally conscious consumers.

Premium offerings are climbing at a 5.37% CAGR through 2031, driven by scarcity positioning, clinical endorsements, and higher selling prices. Sandals are evolving into high-value products that combine style, comfort, and functionality. Premium sandals are gaining traction among consumers willing to pay a premium for ergonomic designs and sustainable materials. Brands like Havaianas and Reef are introducing collections with enhanced arch support, durable materials, and stylish aesthetics to cater to this demand. Additionally, premium slides and slippers are experiencing robust growth, supported by advancements in recovery footwear technology and collaborations with high-end fashion brands. These products are increasingly positioned as versatile options for both casual and semi-formal settings, appealing to a broader demographic. The rise of remote work and home-centric lifestyles has further boosted demand for premium slippers, as consumers prioritize comfort without compromising on style.

By Distribution Channel: Digital Grows Behind Fit Tech

Offline retail stores accounted for 67.23% of the distribution in 2025, driven by consumers' preference for physically evaluating fit, materials, and arch support before purchase. This segment remains vital for premium brands, as it enables them to offer immersive brand experiences and expert-fitting consultations that are difficult to replicate online. For instance, Birkenstock operates 97 mono-branded stores and plans to open 40 more by 2026, leveraging these outlets to drive full-price sales and strengthen brand loyalty. Similarly, Crocs, with its global network of approximately 2,600 mono-branded stores, plans to add 200 to 250 new locations in 2026. These stores are strategically positioned in high-traffic tourist destinations and suburban malls to capitalize on impulse purchases and enhance customer engagement.

On the other hand, online channels are growing at a CAGR of 5.46% through 2031, driven by technological advancements and shifting consumer behavior. Innovations such as computer-vision sizing tools, augmented-reality try-ons, and seamless return policies are reducing barriers to online shopping, making it a more attractive option for consumers. Additionally, the demand for personalization is rising, with consumers expecting curated recommendations based on gait analysis, previous purchases, and style preferences. Younger demographics, particularly Generation Z and Millennials, are also driving growth in this segment, these consumers increasingly consider resale value when making purchases, favoring durable, branded sandals that retain value in the secondary market over disposable, fast-fashion alternatives.

Geography Analysis

Asia-Pacific captured 37.58% of 2025 revenue, driven by India’s monsoon-driven flip-flop volumes and China’s rapid adoption of foam clogs. Crocs’ Chinese segment recorded a 30% year-on-year growth in Q4 2025, contributing approximately 8% to the company's total revenue. Similarly, Birkenstock achieved 34% constant-currency growth in Asia-Pacific in 2025, supported by the opening of flagship stores in Japan and South Korea. However, enforcement challenges persist, as evidenced by Vietnam's seizure of 7,000 counterfeit pairs in early 2025. The region's growth is further bolstered by rising urbanization, higher disposable incomes, and a growing preference for casual, comfortable footwear.

The Middle East and Africa are projected to achieve a 6.15% CAGR, the fastest regional growth rate, as rising disposable incomes in Gulf countries and Nigeria align with desert climates that favor open-toe footwear. Regulatory clarity and the establishment of tax-free retail zones in the United Arab Emirates have created an attractive environment for global brands to launch flagship stores, capitalizing on year-round demand. Additionally, the region's younger demographic and increasing fashion consciousness are driving demand for both affordable and premium sandal options.

North America and Europe are experiencing slower growth but are benefiting from trends such as premiumization and sustainability-focused legislation. The European Union's eco-design regulations are compelling brands to invest in durable, long-life components, enhancing the value proposition of German-made sandals. In North America, the growing emphasis on eco-friendly materials and ethical production practices is reshaping consumer preferences, with brands leveraging these trends to differentiate themselves in a competitive market. South America, led by Alpargatas, combines high volumes with low price points. However, trade-up behavior in countries like Chile and Peru is fostering the emergence of premium micro-niches.

Competitive Landscape

The sandals market is moderately concentrated, characterized by the presence of global leaders such as Crocs, Nike, Adidas, alongside regional specialists, private-label competitors, and digitally native disruptors. These players are capitalizing on emerging opportunities in recovery footwear, sustainable materials, and gender-specific ergonomics. Crocs operates 2,600 mono-brand stores and benefits from high-margin direct channels; however, sandals account for only 13% of its product mix, indicating significant growth potential. Birkenstock achieves a 31.8% adjusted EBITDA margin by limiting wholesale distribution and managing 97 owned stores, with plans to open 40 additional locations by 2026. Alpargatas maintains a strong domestic presence but has only recently achieved profitability in its international divisions, highlighting the challenges of transitioning low-cost flip-flops into premium markets.

Moreover, the market remains structurally fragmented with low concentration, as a considerable share of sales is distributed among numerous small and mid-sized brands operating in domestic or regional markets. Companies such as ECCO, Skechers, and Havaianas compete in distinct segments, including comfort, lifestyle, and casual fashion, underscoring segmentation-driven competition. This fragmentation intensifies price competition in the mass segment while enabling premium and luxury brands to sustain strong market positions through design and brand differentiation.

Competitive strategies are increasingly centered on innovation, sustainability, and channel expansion. Businesses are investing in eco-friendly materials, ergonomic designs, and direct-to-consumer (DTC) models. The expansion of e-commerce and DTC channels is lowering entry barriers, allowing emerging brands to scale rapidly and challenge established players. Simultaneously, incumbents are leveraging acquisitions and collaborations to strengthen their portfolios. As a result, the competitive landscape remains dynamic, driven by shifting consumer preferences for comfort, customization, and sustainability-focused differentiation.

Sandals Industry Leaders

-

Nike Inc.

-

Adidas AG

-

Skechers USA Inc.

-

Crocs Inc.

-

Deckers Outdoor Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bata India launched its campaign, "Everyday Essentials. Reinvented," focusing on open footwear, a key element in Indian wardrobes. The collection featured lightweight, supportive designs, including sandals, peep-toes, and adjustable styles, offering minimal, versatile, and long-lasting wearability.

- January 2026: ANTA Sports acquired a 29% stake in Puma SE for EUR 1.5 billion, marking the largest cross-border footwear investment by a Chinese company and positioning ANTA to leverage Puma's European distribution network and design expertise to accelerate its sandals and lifestyle categories.

- January 2026: Crocs Inc. launched the LEGO Brick Clog at a price of USD 149.99, which featured the brand's largest licensed Jibbitz assortment to date. The product generated significant social media engagement, resulting in pre-orders selling out within 48 hours. This demonstrated the revenue potential of intellectual property collaborations.

- March 2025: Footwear brand Catwalk opened an exclusive brand outlet in Lucknow to expand its physical retail presence in northern India. The store specialized in women's footwear and offered a selection of brightly colored handbags. It catered to various occasions with products like heeled sandals, court shoes, pumps, ankle boots, and sneakers.

Global Sandals Market Report Scope

The sandals market is segmented by product type, end-user, category, distribution channel, and geography. Based on product type, the market is segmented into flip flops, slides and slippers, and others. By end-user, the market is segmented into men, women, and children. By category, the market is segmented into mass and premium. By distribution channel, the market has been segmented into offline and online retail stores. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD).

| Flip Flops |

| Slides and Slippers |

| Others |

| Men |

| Women |

| Children |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Flip Flops | |

| Slides and Slippers | ||

| Others | ||

| By End-User | Men | |

| Women | ||

| Children | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global sandals revenue be by 2031?

Forecasts place the sandals market size at USD 82.36 billion in 2031, reflecting a 4.52% CAGR over 2026-2031.

Which region is expected to grow the fastest?

The Middle East and Africa is projected to post a 6.15% CAGR, outpacing all other regions thanks to rising incomes and desert climates favoring open-toe footwear.

What product style is gaining share most rapidly?

Slides and slippers lead growth at a 5.58% CAGR, driven by recovery-focused foam technologies and lifestyle positioning.

Why are premium sandals outpacing mass-market growth?

Scarcity strategies, clinical endorsements, and bio-based material innovation allow premium brands to sustain higher margins and a 5.37% CAGR through 2031.

Page last updated on: