Football Shoes Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 29.41 Billion |

| Market Size (2030) | USD 38.34 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

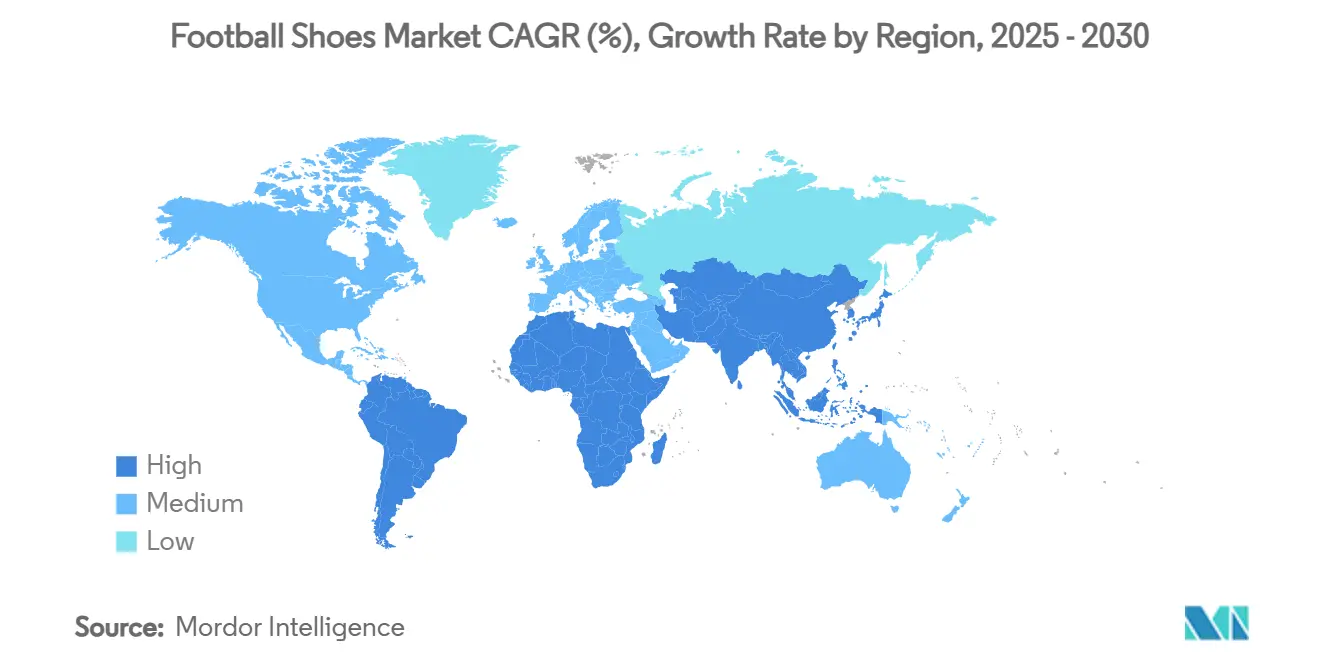

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Football Shoes Market Analysis by Mordor Intelligence

The global football shoes market size is valued at USD 29.41 billion in 2025 and is projected to reach USD 38.34 billion by 2030, expanding at a CAGR of 5.45% during the forecast period. The market is expanding as football gains wider traction across both amateur and professional levels. Rising investments in women’s leagues and the rapid urban development of sporting facilities are further fueling this growth. Cities globally are constructing artificial turf fields for year-round play, spurring demand for AG-specific shoes. Industry giants Nike and Adidas dominate with innovations like Flyknit uppers and Predator technology, while Puma carves a niche with its speed-centric Ultra series. New players are increasingly using online platforms to reach niche football communities and emerging consumer groups. While Europe boasts the largest market share, owing to its deep-rooted football culture, the Asia-Pacific region is witnessing the fastest growth, driven by grassroots programs and stadium developments in nations like China and India. The mass-market segment leads in sales, yet premium offerings are on the rise as athletes increasingly value performance, technology, and brand prestige. Additionally, the rise of e-sports and virtual football tournaments is also shaping consumer attitudes, as fans seek physical products linked to their favorite digital experiences.

Key Report Takeaways

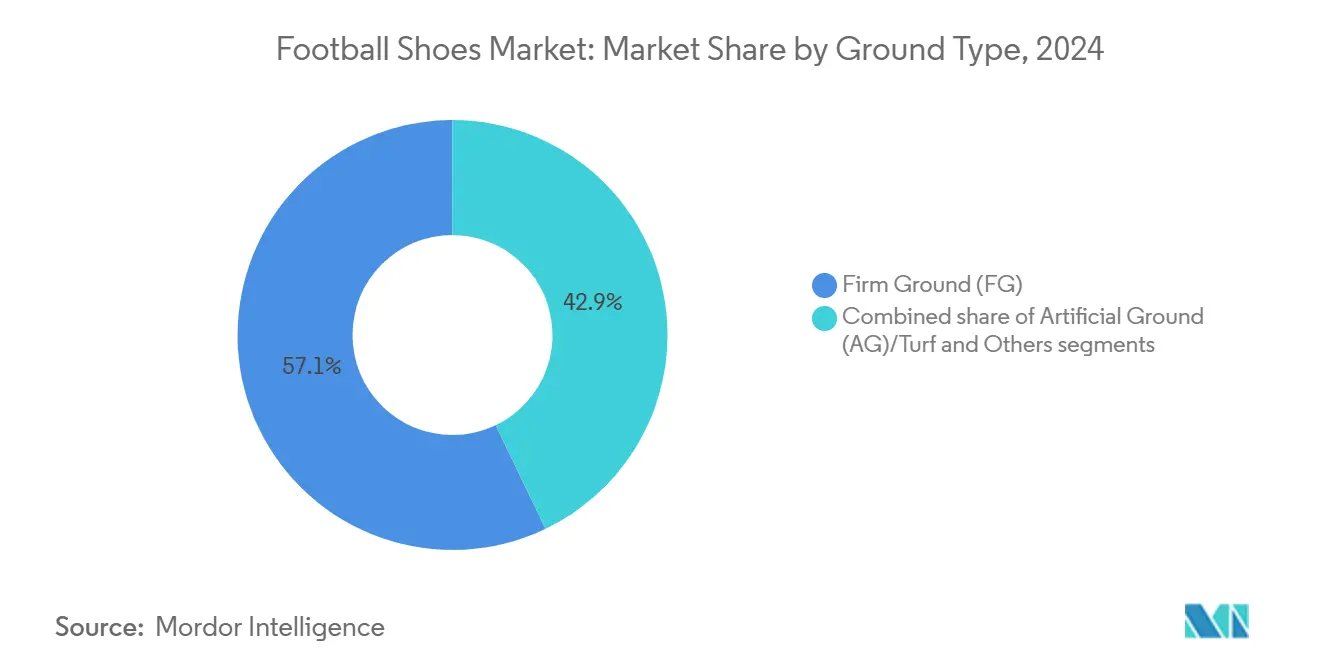

- By ground type, firm-ground models led with 57.12% of the football shoes market share in 2024, whereas artificial-ground variants are forecast to expand at an 8.40% CAGR to 2030.

- By end user, men held 62.18% of the football shoes market size in 2024, while the women’s segment is projected to grow at 7.86% CAGR through 2030.

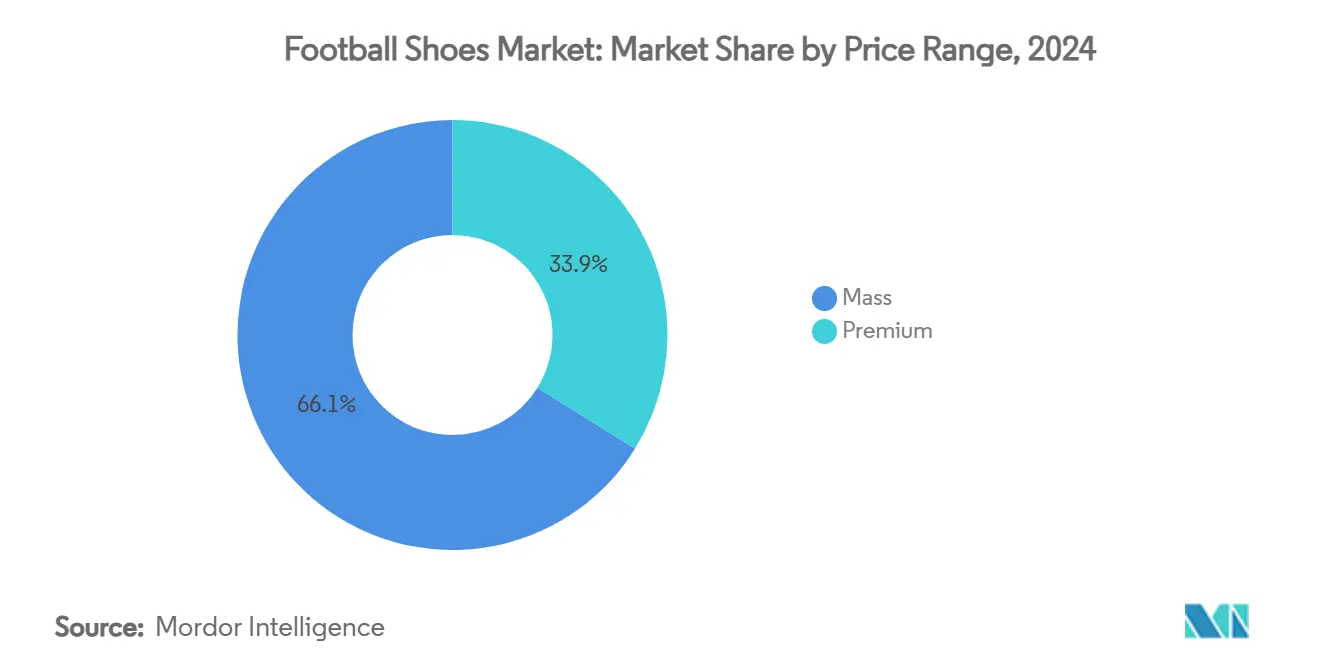

- By price range, the mass segment captured 69.45% of revenue in 2024; premium models, however, are poised for a 7.13% CAGR to 2030.

- By distribution channel, sports and athletic goods stores accounted for 41.65% revenue in 2024, whereas online retail stores are set to grow at 8.31% CAGR to 2030.

- By geography, Europe dominated with 40.87% revenue in 2024, yet Asia-Pacific is the fastest-growing region at 7.52% CAGR through 2030

Global Football Shoes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government and grassroots initiatives | +0.8% | Global (North America, Europe) | Medium term (2–4 years) |

| Growing women’s participation | +1.2% | Global (Europe, North America) | Long term (≥ 4 years) |

| Health and fitness awareness | +0.9% | Global (Asia-Pacific, North America) | Medium term (2–4 years) |

| Athlete endorsements and digital influence | +0.7% | Global (North America, Europe) | Short term (≤ 2 years) |

| Technological innovation | +1.1% | Global (North America, Europe) | Long term (≥ 4 years) |

| Urban street football culture | +0.6% | Global (Asia-Pacific cities) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government and Grassroots Initiatives Driving Football Participation

Government-backed initiatives are reshaping football participation, channeling investments into infrastructure and enhancing accessibility, particularly at the grassroots level. For example, the U.S. Soccer Forward Foundation has secured over USD 10 million to bolster low-cost youth programs in anticipation of the 2026 FIFA Men’s World Cup, with a clear aim: to foster inclusivity in underserved communities [1]Source: U.S. Soccer Federation, “Soccer Forward Foundation Launch,” ussoccer.com. Meanwhile, in the UK, the government is on a mission to double the number of top-tier community clubs by UEFA EURO 2028. In Wales, a EUR 4 million boost is being funneled into 64 grassroots projects, funding everything from new pitches to floodlights, all with an ambitious target of engaging 3.5 million more participants by 2030 [2]Source: Department for Culture, Media and Sport, “Grassroots Football Facilities Investment,” gov.uk. In addition, Germany has introduced a nationwide initiative to modernize training facilities, allocating EUR 25 million to improve access for youth players. Similarly, Australia is focusing on increasing female participation in football by launching a USD 15 million program aimed at building dedicated facilities for women and girls. Aligning these programs with major tournaments helps maximize visibility, capitalizing on the media buzz and public enthusiasm surrounding global events.

Growing Women's Participation in Football

Strategic investments in leagues, media coverage, and grassroots programs are propelling women's football into the commercial spotlight, paving long-term pathways for female athletes. National associations and governments are rallying behind the women's game. For instance, Football Australia noted a 16% uptick in female participation in 2024, a testament to the legacy of hosting the FIFA Women’s World Cup 2023 [3]Source: Football Australia, “National Participation Report 2024,” footballaustralia.com.au. The UK's Football Association is amplifying its "Let Girls Play" campaign, targeting equal football access for schoolgirls by 2024. Major events, like the 2024 Olympic Games, heightened visibility for female athletes, spurring engagement and sponsorship interest. The rise of professional leagues is creating visible female role models, inspiring greater participation and boosting demand for women’s football gear. In response, brands are broadening their women's collections, championing athlete-led marketing, and innovating sizes to cater to anatomical differences. Nike debuted the Phantom Luna, its inaugural women-led football boot, while Adidas rolls out gender-specific Predator and Copa series, fine-tuning fit, comfort, and traction for female athletes. With an increasing number of women shifting from casual to competitive play, the appetite for durable, high-performance footwear is set to surge.

Health and Fitness Awareness Boosting Football Activity

As consumers increasingly recognize the cardiovascular, social, and skill-development benefits of football, the sport is becoming a staple in fitness routines. The U.S. Soccer Federation champions football not just as a sport, but as a preventive health tool, highlighting its accessibility and community-building potential for America's 14.7 million players. Unlike solitary gym routines, football offers a social and mentally stimulating workout that appeals to both young and adult players. Urban environments are witnessing a surge in popularity for recreational formats, such as small-sided games and leagues like the Baller League, owing to their flexibility and reduced entry barriers. This evolving landscape is driving a steady demand for versatile football shoes, suitable for everything from turf to street courts, with features that boost agility, provide cushioning, and prevent injuries. Football's integration into wellness programs and community fitness events is broadening its appeal, elevating it from a mere sport to a lifestyle activity. Reinforcing this trend, the World Health Organization reports that 31% of adults currently fall short of recommended physical activity levels, with this proportion expected to increase to 35% by 2030 [4]Source: World Health Organization, “Global Physical Activity Trends,” who.int. This underscores the urgent need for engaging and accessible exercise forms, like football.

Athlete Endorsements and Digital Influence on Buyer Preferences

Professional athletes are reshaping market dynamics, merging their social media clout with collaborative product design, thereby boosting brand authenticity and deepening consumer engagement. Leading this transformation, brands like Nike and Adidas are bringing athletes into the heart of the creative process. For example, Addidas introduced a limited-edition F50 LY304 boot, crafted in collaboration with Lamine Yamal, the brand emphasized exclusivity and a compelling narrative. Meanwhile, Nike’s A.I.R. initiative integrates athlete insights with AI technology to develop customized prototypes for elite players such as Kylian Mbappé and Erling Haaland, further reinforcing the brand’s performance credibility. These collaborations go beyond traditional sponsorships athletes now act as cultural influencers, using their digital platforms to build stronger brand connections. This approach not only deepens emotional ties with fans but also enables brands to command premium prices, leveraging scarcity, innovation, and the cultural significance of their athlete partners. With the rising popularity of limited releases and exclusive behind-the-scenes content, co-created collections are emerging as pivotal tools for enhancing brand loyalty and carving out market distinction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High pricing of premium shoes | -0.9% | Global (price-sensitive markets) | Short term (≤ 2 years) |

| Competition from other sports | -0.4% | North America, Asia-Pacific | Medium term (2–4 years) |

| Counterfeit products | -0.6% | Global (Asia-Pacific focus) | Long term (≥ 4 years) |

| Raw-material price volatility | -0.7% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Products

Counterfeit football shoes not only pose legal challenges but also threaten brand integrity, erode consumer trust, and jeopardize athlete safety. Football shoes, a prime target in the sportswear counterfeiting arena, are increasingly falling prey to illicit manufacturers. High-grade replicas, crafted with alarming precision through sophisticated reverse-engineering, are flooding markets in hotspots like China, Turkey, and Hong Kong. The rise of e-commerce and small parcel deliveries has empowered counterfeiters, allowing them to sidestep customs and ship directly to consumers, complicating enforcement efforts. In a significant 2024 operation, the European Anti-Fraud Office (OLAF), in collaboration with customs agencies from Austria, Belgium, Germany, Italy, and several non-EU nations, confiscated over 1.8 million counterfeit fashion items, collectively valued at a staggering EUR 180 million. This extensive crackdown underscores the magnitude and tenacity of the counterfeiting issue, emphasizing the dual threat: the tarnishing of global brand credibility and the potential endangerment of consumers unwittingly purchasing subpar products.

Raw-material Price Volatility

Fluctuating prices of petroleum-based raw materials, notably ethylene and propylene oxide, crucial for football shoe midsoles and cushioning, are straining the football footwear market. These price swings inflate production costs, tightening margins for leading manufacturers and introducing planning uncertainties. Geopolitical events, like the U.S. ban on Xinjiang cotton, further complicate matters by disrupting the sourcing of textiles and synthetic blends for shoe uppers. This instability in the supply chain makes forecasting challenging and hinders consistent pricing across product lines. In light of these challenges, brands such as Adidas and Nike are pivoting towards bio-based foams and recycled materials. Initiatives like Nike’s "Move to Zero" and Adidas’ collaboration with Parley Ocean Plastic underscore this shift. However, these greener alternatives come with heightened research and development expenses and necessitate operational tweaks. While this transition is vital for future sustainability and regulatory alignment, it complicates raw material management in an already competitive and margin-sensitive football shoe market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ground Type: Artificial Surfaces Drive Technical Innovation

In 2024, firm ground (FG) football shoes command a dominant 57.12% market share,owing to their compatibility with natural grass and a long-standing consumer preference. Their prevalence is especially notable in Europe and South America, where amateur and professional leagues alike favor traditional grass fields. Leading brands, including Nike and Adidas, emphasize FG models in their flagship offerings. Notable examples include Nike's Phantom GX and Adidas' Predator Elite, both boasting advanced stud configurations and materials designed specifically for firm grass.

While artificial ground (AG) shoes currently occupy a smaller segment, they are witnessing the fastest growth, boasting a projected CAGR of 8.40% through 2030. This uptick is largely attributed to a global pivot towards synthetic turf installations in urban locales and educational institutions, valued for their durability and ability to support year-round play. In response, brands are rolling out AG-tailored versions of their bestsellers. Examples include Puma's Ultra Ultimate AG and Mizuno's Morelia Neo IV AG, both equipped with enhanced stud patterns and soleplate designs to boost traction and minimize injury risks on artificial surfaces.

By End User: Women's Segment Accelerates Market Expansion

In 2024, men's football shoes command a dominant 62.18% market share, underscoring the sport's historical male-centric demographics and deep-rooted male engagement, both professionally and recreationally. Major brands are doubling down on men's lines, with global icons like Kylian Mbappé sporting Nike's Mercurial and top male athletes endorsing Adidas' Predator Edge. This male dominance is bolstered by substantial sponsorship deals, robust viewership in men's leagues, and ingrained consumer preferences, especially in regions like Europe and South America.

Women's football shoes are on a rapid ascent, boasting a projected CAGR of 7.86% through 2030. This surge is fueled by heightened visibility of women's leagues, amplified media attention, and backing from government and association-led initiatives. Following the momentum of the FIFA Women’s World Cup 2023, Australia witnessed a 16% uptick in female participation in 2024. Brands are responding to this shift for example, Nike introduced the women-focused Phantom Luna, while Adidas launched customized versions of the Copa and Predator, designed to optimize fit and biomechanics for female athletes. The momentum is further amplified by professional female athletes, who not only serve as role models but also galvanize grassroots engagement and sway purchasing decisions among both youth and adults.

By Price Range: Premium Growth Outpaces Mass Market

In 2024, football shoe sales are dominated by the mass market segment, commanding a substantial 69.45% share. This dominance is largely attributed to volume sales, affordability, and widespread accessibility, catering to amateur players, school programs, and budget-conscious consumers. Brands respond with durable and functional models, meeting essential performance needs at competitive prices. Often, these mass-market offerings feature entry-level versions of flagship lines. For instance, Nike’s Vapor Club and Adidas’ Copa Pure 2 are tailored for casual players who prioritize value over advanced features.

Meanwhile, the premium football shoe segment is on a rapid ascent, eyeing a CAGR of 7.13% through 2030. An increasing appetite for performance-enhancing features, brand prestige, and exclusive designs fuels this surge. Innovations like Nike’s A.I.R. initiative and On’s LightSpray cushioning underscore how cutting-edge advancements elevate the value perception of premium models. Collaborations, such as Adidas’s limited-run F50 LY304 boots crafted with Lamine Yamal, spotlight the allure of exclusivity and athlete partnerships. Premium consumers actively invest in cutting-edge technology. Their strong brand loyalty fuels demand for these high-margin products and elevates their resale value, reinforcing the cultural stature of elite football footwear.

By Distribution Channel: Digital Transformation Accelerates Online Growth

In 2024, sports and athletic goods stores command a dominant 41.65% share of the football shoes market. This dominance is largely attributed to the in-store experience, enabling consumers to evaluate fit, comfort, and performance directly. These outlets are pivotal for both amateur and professional players, who seek expert advice and immediate access to products, particularly high-performance ones. Major brands, including Nike and Adidas, are bolstering this physical shopping experience by investing in flagship and specialty retail formats. They offer enhanced services such as gait analysis, product customization, and demonstrations led by athletes.

On the other hand, online retail is the fastest-growing distribution channel, boasting a CAGR of 8.31% projected through 2030. This surge is driven by the allure of digital shopping's convenience, a wider product range, and exclusive releases. E-commerce platforms are particularly resonating with the digitally savvy consumers in the Asia-Pacific region, who value speed, variety, and easy comparisons. These digital avenues empower brands to harness data for personalized experiences, AI-driven product suggestions, and robust loyalty initiatives, bolstering customer retention. The burgeoning trend of limited-edition football shoes and the rise of direct-to-consumer strategies underscore the significance of online platforms in accessing exclusive collections.

Geography Analysis

In 2024, Europe commands the football shoes market with a 40.87% share, bolstered by its entrenched football culture, established league systems, and robust infrastructure. Initiatives like the UK's ambition to double top-tier community clubs by UEFA EURO 2028 and Wales' EUR 4 million grassroots pitch investment are amplifying participation. Brands are benefiting from this heightened engagement. For example, Adidas has secured partnerships with 11 of the top 20 highest-earning football clubs for the 2025–2026 season, underscoring its stronghold in Europe's lucrative segment. With high merchandising revenues and unwavering consumer loyalty, Europe remains the prime arena for flagship product launches and brand-led innovations.

Asia-Pacific is emerging as the fastest-growing region, projected to expand at a 7.52% CAGR through 2030. This growth is fueled by rising incomes, urbanization, and a vast fan base, with ASEAN alone boasting over 300 million football enthusiasts. Owing to the legacy of the FIFA Women’s World Cup, Australia witnessed a 16% surge in women's football participation in 2024. Clubs like Norwich City are forging grassroots connections by partnering with local teams such as Chennaiyin FC in India. With a strong appetite for branded sportswear and active youth engagement, Asia-Pacific is solidifying its status as a pivotal growth hub for global players.

Other regions are also eyeing the football shoes market. North America is gearing up for the 2026 FIFA Men’s World Cup, with the U.S. Soccer Forward Foundation pouring over USD 10 million into expanding youth access. South America's fervent football passion ensures consistent demand, though economic challenges hinder the adoption of premium products. Meanwhile, the Middle East and Africa, with their burgeoning youth populations and infrastructure investments, are drawing interest.

Competitive Landscape

The market is highly consolidated, with major players including Nike, Adidas, and Puma dominating the football shoes market, leveraging robust distribution networks, athlete endorsements, and relentless product innovation. These industry giants secure their foothold through strategic partnerships with professional leagues and tournaments. Emerging brands are carving out space in niche segments, using direct-to-consumer models and innovative designs to compete. As brands for athlete collaborations and exclusive releases, competition in the market continues to intensify, underscoring the importance of visibility and brand loyalty.

In this space, technology has emerged as a key differentiator. Brands are investing heavily in advanced design and material innovation to enhance performance. For example, Nike’s A.I.R. project leverages athlete data to create customized prototypes, while on emphasizes lightweight engineering in its football-inspired footwear, highlighting the role of design in driving market appeal. Growth opportunities also remain in underdeveloped segments such as women’s football and footwear for artificial turf. Addressing this, Adidas introduced specialized models like the Predator Accuracy W.

As consumers become more environmentally conscious, sustainability emerges as a pivotal competitive edge.Brands are responding with innovation, as seen in Adidas’s use of Parley Ocean Plastic uppers and Nike’s commitment to sustainability through its Move to Zero initiative, both of which transform waste into high-performance footwear. These initiatives help reduce environmental impact while strengthening brand image, especially among younger consumers who prioritize ethical and sustainable products.

Football Shoes Industry Leaders

Nike, Inc.

Puma SE

Adidas AG

Mizuno Corporation

Under Armour, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nike launched the Hypervenom RGN football boot as part of its women's-focused innovation line, designed to deliver precision fit and traction. The boot featured a re-engineered soleplate and was released ahead of major women’s football tournaments to support elite female athletes.

- December 2024: Adidas released the limited-edition F50 LY304 signature boot for Lamine Yamal, with only 304 pairs produced. It is available in Laceless only; the F50 LY304 is engineered for speed. It features a thin, FIBERTOUCH upper with an adidas PRIMEKNIT collar for lockdown, and a SPRINTWEB 3D texture designed to help keep the ball close when across the pitch.

- November 2024: Nike reintroduced the Hypervenom RGN, a chrome edition of the Mercurial Vapor 1 RGN. These updated models showcase Nike’s enduring leadership in football performance innovation and its ongoing dedication to creating products that cater to the needs of today’s athletes. The Nike Hypervenom RGN is available on nike.com and at select retail stores.

Global Football Shoes Market Report Scope

| Firm Ground (FG) |

| Artificial Ground (AG)/Turf |

| Others |

| Men |

| Women |

| Kids/Children |

| Mass |

| Premium |

| Sports and Athletic Goods Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ground Type | Firm Ground (FG) | |

| Artificial Ground (AG)/Turf | ||

| Others | ||

| By End User | Men | |

| Women | ||

| Kids/Children | ||

| By Price Range | Mass | |

| Premium | ||

| By Distribution Channel | Sports and Athletic Goods Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current football shoes market size and growth outlook?

The football shoes market size is USD 29.41 billion in 2025 and is forecast to reach USD 38.34 billion by 2030 at a 5.45% CAGR.

Which region is growing fastest in the football shoes market?

Asia-Pacific posts the highest regional CAGR at 7.52% through 2030 due to rising disposable incomes, infrastructure spending, and grassroots programs.

How are women influencing football shoe demand?

Women’s participation is climbing 7.86% CAGR to 2030, creating demand for gender-specific fits, expanded size ranges, and marketing that resonates with female athletes.

What role do online channels play in football shoe sales?

Online retail is forecast to grow at 8.31% CAGR, propelled by convenience, extensive product choice, and advanced fit-visualization tools that reduce purchase hesitation.

Page last updated on: