Footwear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

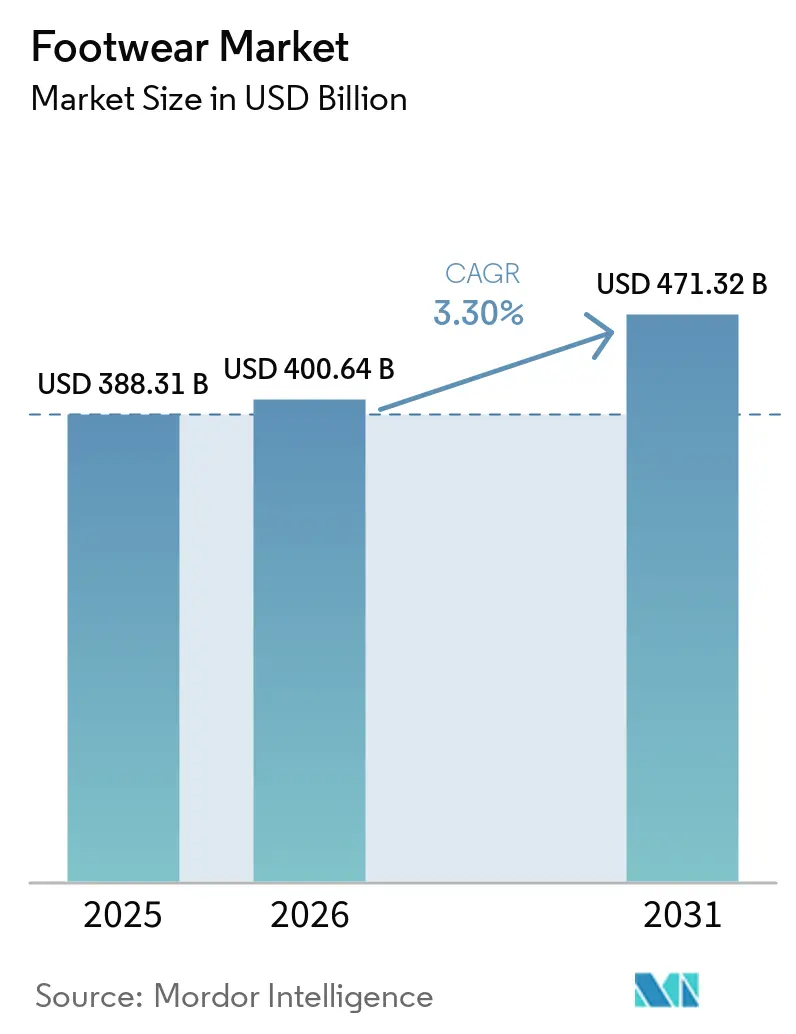

| Market Size (2026) | USD 400.64 Billion |

| Market Size (2031) | USD 471.32 Billion |

| Growth Rate (2026 - 2031) | 3.30% CAGR |

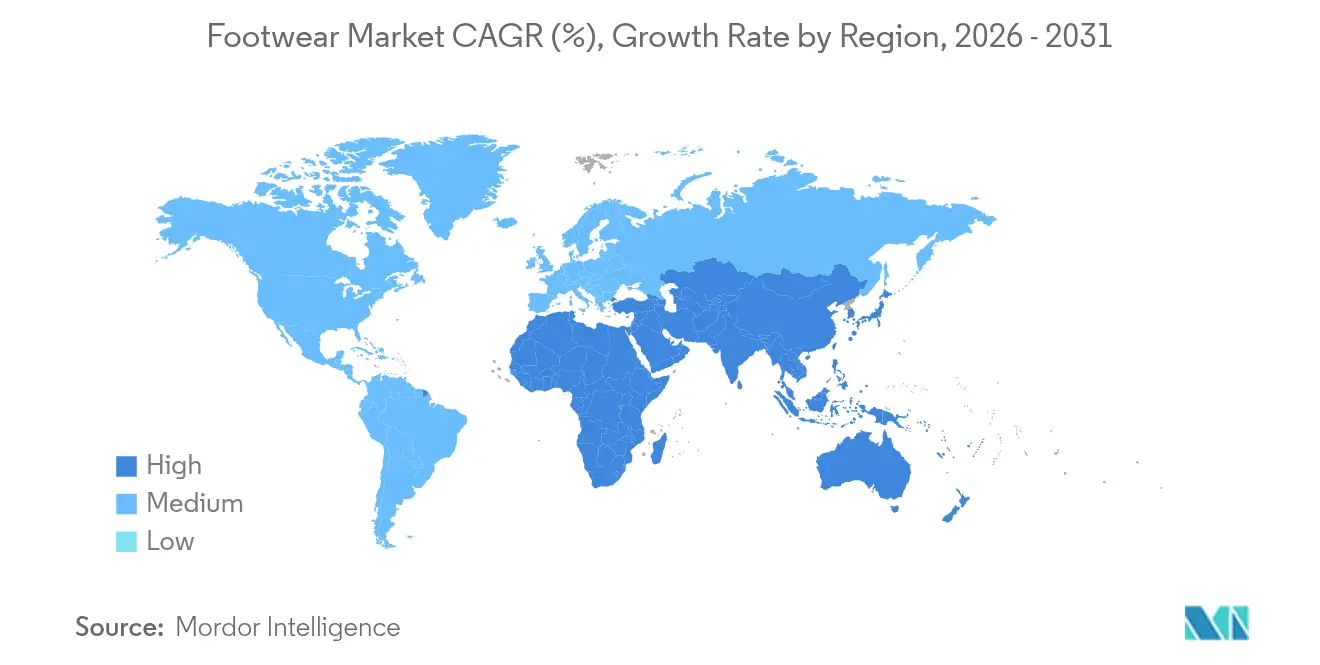

| Fastest Growing Market | South America |

| Largest Market | North America |

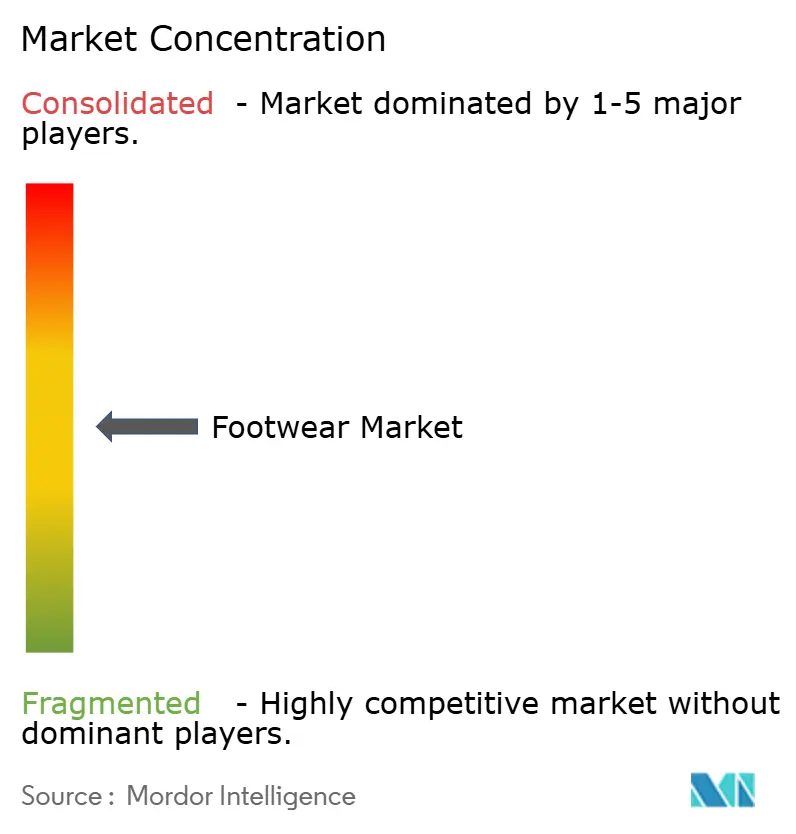

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Footwear Market Analysis by Mordor Intelligence

The footwear market size was valued at USD 388.31 billion in 2025 and estimated to grow from USD 400.64 billion in 2026 to reach USD 471.32 billion by 2031, at a CAGR of 3.30% during the forecast period (2026-2031). As the sector adapts to the rising trend of athleisure, embraces sustainability mandates, and witnesses the ascent of direct-to-consumer (D2C) brands, it continues to expand steadily. The growing popularity of athleisure reflects changing consumer preferences for versatile and comfortable apparel, while sustainability mandates are driving innovation in materials and production processes. The rise of D2C brands is reshaping traditional retail models by enabling brands to establish direct relationships with consumers, enhancing customer experience and loyalty. While Asia-Pacific stands as a hub for both production and consumption, global design and supply-chain strategies are being influenced by regulatory shifts, notably the EU’s Ecodesign for Sustainable Products Regulation (ESPR), which aims to improve product sustainability and reduce environmental impact[1]Source: European Commission, "New EU rules for measuring environmental impact of clothes and shoes", environment.ec.europa.euacross the footwear industry. The landscape is further complicated by consolidation efforts from financial sponsors and retailers, as companies seek to strengthen their market positions through mergers and acquisitions. Heightened competition due to fluctuating material prices is pressuring profit margins, while the emergence of new revenue streams through increased digital engagement, such as e-commerce and social media platforms, is creating opportunities for growth and innovation in the footwear market.

Key Report Takeaways

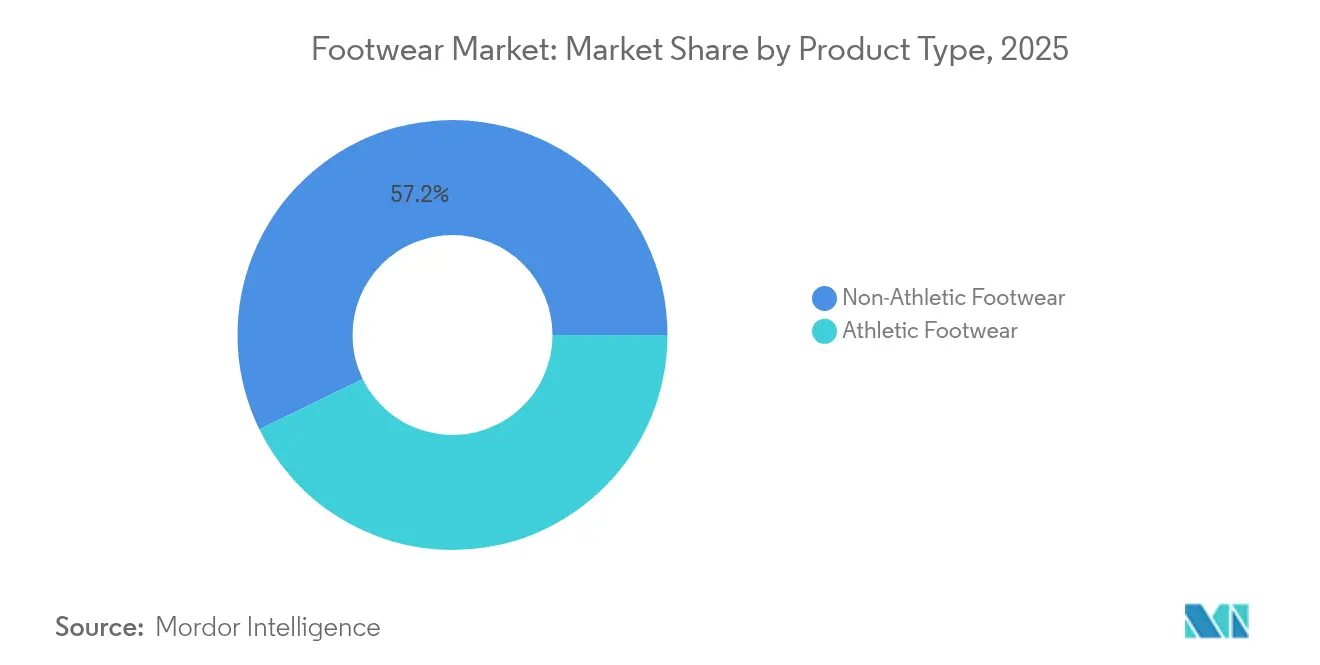

- By product type, non-athletic footwear held 57.23% of the footwear market share in 2025, while athletic footwear is projected to register the fastest 4.67% CAGR over 2026-2031.

- By gender, women accounted for 48.74% of 2025 sales, and the kids segment is set to expand at a 4.55% CAGR through 2031.

- By category, the mass segment dominated with 87.36% revenue in 2025, whereas premium offerings are expected to grow at a 4.49% CAGR in the same horizon.

- By distribution channel, specialty stores accounted for 57.56% of sales in 2025, and online retail is forecasted to post a 5.38% CAGR through 2031.

- By region, North America represented 31.26% of 2025 demand, while the South America region is poised for a 4.83% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Footwear Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for athleisure footwear | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Aggressive marketing and influencer ties | +0.8% | Global urban centers | Short term (≤ 2 years) |

| Rise of sustainable and bio-based materials | +0.6% | Europe, North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth of D2C digital-native brands | +0.9% | Developed markets worldwide | Medium term (2-4 years) |

| Mass adoption of smart and connected shoes | +0.4% | North America, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of resale and sneakerhead culture | +0.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging demand for athleisure footwear

Athleisure is increasingly merging the realms of sports and casual wear, becoming a staple in daily wardrobes and driving robust sales, even in established markets. In 2024, Adidas experienced a 17% surge in footwear sales, primarily driven by performance-oriented designs. Modern brands are integrating lightweight foams and energy-return plates into their lifestyle designs, allowing a single piece to seamlessly transition from the gym to the office and social events. This blending is not only drawing market share away from conventional fashion brands but also compelling luxury names to introduce sport-themed collections. The growing popularity of athleisure has also led to significant shifts in consumer preferences, with a heightened demand for products that combine functionality, comfort, and style. In response, retailers are reshaping their offerings throughout the footwear industry, dedicating more space to running-centric sneakers and adaptable trainers, while also investing in marketing strategies that highlight the versatility and performance of these products in the footwear market.

Aggressive marketing and influencer collaborations

Brand discovery in social commerce is increasingly leaning on genuine creator partnerships, driving swift conversions, particularly with Gen Z. These partnerships enable brands to connect with their target audience on a more personal level, fostering trust, loyalty, and deeper engagement. Micro-influencers, offering niche credibility, achieve this at a fraction of the cost of traditional media, allowing challenger brands to scale swiftly and compete effectively in the market. Their ability to resonate with specific communities makes them a valuable asset for brands aiming to establish a strong foothold. Today's success is tied to constant content updates and clear disclosures; audiences swiftly lose interest if collaborations seem rehearsed or inauthentic. To address this shift, traditional players are bolstering their in-house studios, investing in content creation capabilities, and experimenting with live-stream shopping pilots to maintain their relevance and adapt to the evolving consumer behavior in the footwear industry. These strategies aim to bridge the gap between traditional approaches and the dynamic demands of social commerce.

Rise of sustainable and bio-based materials

With the ESPR banning the destruction of unsold stock and mandating digital product passports for traceability, sustainability has evolved from a mere positioning tactic to a crucial licensing requirement[2]Source: European Union Law, "establishing a framework for the setting of ecodesign requirements for sustainable products, amending Directive (EU) 2020/1828 and Regulation (EU) 2023/1542 and repealing Directive 2009/125/EC", eur-lex.europa.eu. These measures aim to enhance transparency and accountability across the supply chain, ensuring that products meet stringent environmental standards. In 2025, suppliers like Dow rolled out bio-circular resin portfolios, offering brands a commercial-scale alternative to traditional petroleum-based inputs. These bio-circular resins are derived from renewable sources, reducing dependency on fossil fuels and lowering the overall carbon footprint of production processes. Brands quick to adopt these changes not only command premium price points but also bolster their brand equity by aligning with consumer demand for sustainable practices. In contrast, those lagging grapple with compliance costs, potential fines, and reputational damage that could erode customer trust. Principles of circular design, such as fully recyclable midsoles and refillable footbeds, are transitioning from pilot projects to mainstream launches, first in Europe and soon across the globe. These innovations not only reduce waste but also promote a closed-loop system, where materials are reused and recycled, contributing to a more sustainable future within the footwear industry.

Growth of D2C digital-native footwear brands

Pure-play D2C entrants leverage real-time data to fine-tune products and pricing, reclaiming margins once surrendered to wholesalers. However, escalating customer-acquisition costs and a saturated online marketplace have driven a shift towards an omnichannel approach. The next-generation brands that thrive today strike a balance between their own storefronts and retail partnerships. By integrating physical and digital channels, these brands enhance customer experiences, offering seamless shopping journeys that cater to diverse consumer preferences. This strategy not only reduces fulfillment costs but also broadens their reach, all while maintaining a consistent brand voice. Furthermore, retail partnerships allow brands to tap into established customer bases and benefit from the operational expertise of their partners. As a result, this hybrid approach is elevating service expectations throughout the footwear market, compelling competitors to innovate and adapt across the footwear industry to the evolving landscape. The shift also highlights the growing importance of agility and adaptability in meeting consumer demands across multiple touchpoints in the footwear market.

Restraints Impact Analysis of Footwear Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extensive availability of counterfeit goods | -0.7% | Asia-Pacific, MEA, global online channels | Medium term (2-4 years) |

| Volatile raw-material prices and disruptions | -0.9% | Manufacturing hubs worldwide | Short term (≤ 2 years) |

| ESG scrutiny on labor practices | -0.4% | Asian manufacturing nations | Long term (≥ 4 years) |

| Anti-plastic legislation on synthetics | -0.3% | Europe, North America, spreading globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extensive availability of counterfeit products

Illicit shoes, worth a staggering USD 467 billion, flood the global e-commerce landscape, undermining trust and diverting sales from legitimate sources. The intricate web of supply chains makes tracing the origin of these products a challenge, as counterfeiters exploit gaps in transparency and oversight to distribute fake goods. These counterfeit operations often involve multiple intermediaries, making it even harder to pinpoint their source. Marketplace algorithms, despite advancements, struggle to distinguish between genuine items and high-quality counterfeits, allowing these products to proliferate unchecked. Birkenstock's recent court-mandated inspections of factories in India underscore the costly enforcement challenges that genuine rights-holders encounter, as they are forced to invest heavily in legal actions, factory audits, and monitoring measures to protect their intellectual property. These enforcement efforts often require collaboration with local authorities and legal systems, further increasing the complexity and cost. As brands ramp up their spending on protection measures, this not only drains resources from research and development but also escalates operating costs throughout the footwear industry, ultimately impacting profitability, innovation, and the ability to compete in an increasingly saturated market.

Volatile raw-material prices and supply-chain disruptions

Geopolitical tensions and extreme weather fluctuations are causing price swings in rubber, ethylene-vinyl acetate, and cotton, thereby compressing gross margins. These price fluctuations are driven by supply chain disruptions, trade restrictions, and unpredictable climatic conditions, which directly impact raw material availability and costs. With over 50% of its footwear sourced from Vietnam, Nike finds itself vulnerable to potential tariff hikes and port slowdowns, which could delay shipments and increase operational costs. The company's multistage production process—sourcing uppers from Indonesia, midsoles from China, and assembly in Vietnam—heightens the risk of disruptions, as any bottleneck in one stage can cascade through the entire supply chain. While brands are hastening the near-shoring of certain SKUs and diversifying their supplier bases to mitigate these risks, the lengthy process of capacity build-out, which involves significant investment and time, leaves them exposed to short-term vulnerabilities within the footwear industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Footwear Market Segment Analysis

By Product Type:

Athletic Momentum AcceleratesIn 2025, non-athletic footwear dominated the market, capturing 57.23% of total sales revenue. Sneakers, merging trendy designs with comfort-driven technology, have become a staple for many consumers. Boots, a seasonal favorite, benefit from changing weather and cultural trends. Meanwhile, flip-flops find their niche among budget-conscious beachgoers. Innovations like advanced cushioning and knit uppers, once exclusive to performance footwear, have blurred the lines between casual and athletic shoes. Leading brands, recognizing this shift, are blending casual and athletic lines, ensuring their offerings resonate with consumers throughout the week. This fusion of styles and technologies solidifies non-athletic footwear's position as a market frontrunner, celebrated for its adaptability and wide-ranging appeal in the footwear industry.

Athletic footwear is now the industry's fastest-growing segment, projected to achieve a CAGR of 4.67% through 2031, outpacing its non-athletic counterparts. Continuous innovations, such as smart midsoles and bio-based foams, are redefining comfort and performance, allowing brands to command premium prices. Running shoes, riding the wave of the wellness trend and increasing marathon participation, are striking a chord with health-conscious consumers. At the same time, outdoor trekking footwear is witnessing a surge in demand, spurred by a boom in adventure tourism, particularly in North America and Asia-Pacific. For instance, the Sports and Fitness Industry Association reported that approximately 247.1 million Americans engaged in sports and fitness activities in 2024. The distinction between athletic and lifestyle shoes is increasingly blurred, with elite sports features seamlessly integrating into mainstream designs, broadening market appeal. However, this rapid innovation pace is shortening product lifecycles, compelling brands to adopt agile inventory strategies in the footwear market to keep pace with consumer trends. This dynamic landscape not only fuels the sector's growth but also presents lucrative opportunities for brands that emphasize agility and innovation.

By End User:

Women Lead, Kids SurgeIn 2025, women's footwear dominates the market, raking in USD 180.51 billion and accounting for 48.74% of total sales. This dominance is fueled by a wide array of styles, from classic pumps to trendy athleisure, catering to diverse occasions and tastes. Such a broad selection not only entices frequent purchases but also sees consumers regularly updating their choices to align with fashion trends and seasonal shifts. Innovative features, like breathable fabrics and antimicrobial treatments, keep women's footwear lines fresh, addressing the growing demand for comfort, functionality, and health-conscious materials. The rising trend of unisex styles and sizing in women's collections signals a significant industry shift towards inclusivity, prioritizing style over traditional gender norms. Major brands are capitalizing on these trends, crafting collections for varied lifestyle archetypes, broadening their market reach, and refining their product lines. This comprehensive approach solidifies women's footwear as the industry's largest and most dynamic segment.

On the other hand, children's footwear is the segment to watch, with projections pointing to a robust 4.55% CAGR in the coming years. This surge is driven by heightened parental awareness of proper foot development and increased participation in school and sports, leading to more frequent replacements. Leading brands are seizing this opportunity, introducing adult-level innovations, like breathable knit materials and antimicrobial liners, to their youth and kids' lines. This strategy not only elevates average selling prices for smaller-sized shoes but also meets parental demands for functionality and health benefits. Consequently, children's footwear has evolved beyond basic styles and traditional school shoes, now embracing fashion-forward and athletic designs that resonate with adult and teen trends. The industry's shift towards inclusive, gender-neutral designs and shared size grids between kids and adults further underscores this convergence. With messaging increasingly focused on healthy lifestyles and active play, the children's footwear segment is set to continue its upward trajectory in the global footwear industry.

By Category:

Premium Rise Tests Mass ScaleIn 2025, the mass segment dominates the global footwear market, accounting for 87.36% of total revenue. This underscores the enduring appeal of affordability to the majority of consumers. Major manufacturers leverage economies of scale, allowing them to integrate comfort-enhancing technologies without straining price points. This strategy poses challenges for smaller competitors aiming for profitable margins. By adopting features like eco foams and recycled yarns, mass brands are narrowing the innovation divide with premium categories, ensuring their products match up in quality and sustainability. Such strides bolster their market position, assuring budget-conscious consumers that modern features don't have to come with a hefty price tag. Moreover, aggressive discounts and promotions amplify their allure to price-sensitive shoppers, who keenly seek savings. The mass segment's evolution underscores the paramount importance of delivering enhanced value, even at accessible price points, ensuring both volume sales and unwavering consumer loyalty in the footwear market.

Conversely, the premium footwear segment is set to expand at a robust 4.49% CAGR, outpacing the overall market. This growth is fueled by affluent consumers' increasing desire for exclusivity, brand heritage, and sustainable materials. Shoppers in this segment are becoming more discerning, valuing provenance and limited edition releases. They're often seen queuing up for exclusive capsule collections that vanish moments after their debut. High-end brands, particularly those collaborating with sports icons, are adeptly blending traditional craftsmanship with state-of-the-art performance technology. This fusion results in products that excel in both style and functionality. Such aspirational allure has polarized the market: while value-centric shoppers hunt for bargains, aspirational buyers willingly pay a premium for standout pieces and eco-friendly credentials. Mid-range brands, caught in this crossfire, face mounting pressure from both sides and must refine their brand narratives to maintain relevance. As luxury and premium brands intensify their focus on innovation, storytelling, and sustainability, they're not just setting new desirability benchmarks but also charting a consistent upward trajectory for the segment in the footwear industry. The premium segment's vigorous growth underscores the footwear market's valuation of not just function and affordability, but also emotional resonance and perceived prestige.

By Distribution Channel:

Omnichannel WinsIn 2025, specialty stores dominated the footwear retail scene, clinching 57.56% of total sales. Their lasting allure stems from expert fittings, attentive service, and a curated selection that resonates with discerning shoppers. To elevate the in-store experience, retailers are integrating advanced services like gait analysis and bespoke 3D-printed orthotics. These innovations not only help customers achieve the ideal fit but also cater to specific comfort and performance needs. Such tailored experiences cultivate trust and nurture long-term loyalty, setting specialty channels apart from generic mass retail. These unique services not only drive repeat visits but also boost spending, as consumers seek personalized advice and customization that online platforms can't offer. Consequently, specialty stores not only defend their market position but also broaden their lead, skillfully merging knowledgeable staff with cutting-edge technology. Their focus on expertise, personalization, and engagement solidifies the brick-and-mortar channel's pivotal role in premium and technical footwear sales.

On the other hand, within the footwear industry, online retail is swiftly rising as the leading channel for footwear sales, projected to grow at an impressive 5.38% CAGR in the upcoming years. The meteoric rise of e-commerce is anchored in its unparalleled convenience, boasting features like same-day delivery and AR-driven sizing tools that mitigate fit uncertainties and curtail return rates. Digital advancements also shine at checkout, with social media integrations facilitating impulse buys straight from livestreams, significantly expediting the journey from discovery to purchase. Brands are responding to the demand for a fluid shopping experience by embracing hybrid models like click-and-collect, allowing customers to order online and either try on or pick up their items in-store. This fusion of digital and physical interactions not only streamlines the purchasing process but also enhances brand engagement and provides valuable data insights in the footwear market. For families, subscription boxes offer a novel approach, delivering personalized footwear solutions for children’s evolving needs. The surge in online and omnichannel tactics underscores the importance of agility and customization in fostering customer loyalty and adapting to the dynamic landscape of the footwear industry.

Geography Analysis

North America Footwear Market

North America, accounting for 31.26% of global demand, stands as the largest footwear market. The region’s consumers are driving demand for sustainable and tech-integrated products, from carbon-neutral snowboard boots to Bluetooth-enabled running shoes, underscoring a willingness to pay premiums for innovation. At the same time, tariff pressures in Vietnam and rising labor costs are squeezing margins, prompting firms to diversify supply chains toward Mexico and Central America. Market consolidation is also reshaping retail dynamics, exemplified by Dick’s USD 2.4 billion acquisition of Foot Locker in 2025, which strengthens bargaining power with suppliers and redefines channel leverage in the footwear industry.

South America Footwear Market

South America is the fastest-growing market, projected at a 4.83% CAGR. Rising incomes, rapid urbanization, and expanding retail penetration are accelerating demand, particularly in affordable and mid-tier segments. Brands are leveraging cost advantages and favorable trade policies to scale presence across the region, though macroeconomic instability and currency fluctuations remain headwinds for premium imports, limiting the expansion of high-end categories within the footwear industry.

APAC and Europe Footwear Market

Asia-Pacific continues to function as the global manufacturing hub, with supply chains concentrated in China, Vietnam, and India ensuring efficiency through shorter production cycles and reduced lead times. Tamil Nadu in particular secured INR 17,550 crore (USD 2.1 billion) in non-leather investments from Nike, Puma, Crocs, and Adidas in 2024, expected to generate 230,000 jobs and reinforce the region’s strategic importance. Europe, meanwhile, is setting the global benchmark for sustainability through regulatory measures such as the ESPR, with companies in Germany and Scandinavia leading adoption of bio-based leather alternatives to meet consumer demand for eco-friendly products throughout the footwear industry. ghlighted by Dick’s strategic acquisition of Foot Locker for USD 2.4 billion in 2025. This consolidation is reshaping channel leverage, enabling retailers to strengthen their market position and negotiate better terms with suppliers.

Mordor Intelligence provides coverage of the footwear market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The footwear market showcases a moderate concentration. While giants like Nike, Adidas, Skechers, Puma, and New Balance lead the pack, their collective dominance still paves the way for specialized newcomers. A notable sign of this evolving landscape is 3G Capital's USD 9.4 billion bid for Skechers in 2025, highlighting private equity's keen interest in harnessing operational efficiencies. Meanwhile, midsize players like On, Hoka, and Veja are carving out their niches, drawing loyal customers with their focus on performance and sustainability, and gradually encroaching on the territory of established brands.

In this competitive arena, technology investments are pivotal. Nike's flagship "House of Innovation" stores in Europe boast RFID-enabled stock tracking, underscoring their tech-forward approach. Adidas, not to be outdone, has experimented with 3D-printed midsoles for customized damping. Sustainability is another key differentiator: Dow's 2025 portfolio of low-carbon resins positions them as frontrunners, granting them exclusive material access. Meanwhile, smaller brands, facing challenges with premium materials, are pivoting towards unique styles or localized supply chains.

The dynamics of channel power are shifting. Brands are rapidly establishing direct-to-consumer (D2C) storefronts, aiming to harness valuable data and boost profit margins. Yet, traditional wholesale channels remain vital for expanding geographic reach. In response, retailers are introducing their own sneaker labels and exclusive collaborations, striving to maintain foot traffic. Furthermore, resale platforms, once on the fringes, are now playing a significant role in shaping pricing perceptions and product release strategies in the footwear industry, marking a new competitive dimension in the footwear landscape.

Footwear Industry Leaders

-

Nike Inc.

-

Adidas AG

-

Puma SE

-

Skechers USA, Inc.

-

VF Corporation

- *Disclaimer: Major Players sorted in no particular order

Footwear Market Companies Covered in this Report

- Nike, Inc.

- Adidas AG

- Puma SE

- VF Corporation

- Skechers USA, Inc.

- ASICS Corporation

- Under Armour, Inc.

- New Balance Athletics, Inc.

- Deckers Outdoor Corp.

- Anta Sports Products Ltd.

- Li-Ning Company Ltd.

- ABC Mart

- Kering SA (Gucci)

- Wolverine World Wide, Inc.

- Fila Holdings Corp.

- LVMH Moet Hennessy Louis Vuitton SE (Louis Vuitton)

- Brooks Sports, Inc.

- Bata India

- Columbia Sportswear Company

- Crocs Inc

Recent Industry Developments in Footwear Market

- June 2025: Reebok has unveiled its latest addition, the Reebok FloatZig 2 running shoe. This new model boasts SuperFloat+ nitrogen-injected foam and a revamped Zig Tech midsole, promising a springier and more stable experience. The brand asserts that these enhancements boost energy return and stability, making it ideal for daily training.

- June 2025: Pair-ie-tales has debuted its women's footwear brand in India. The shoes, crafted for comfort, feature the Cloud Comfort™ sole system - a triple-layered innovation tailored for everyday wear. This system is designed to provide enhanced cushioning, support, and durability, ensuring a comfortable experience for users throughout the day.

- June 2025: Nike, in collaboration with NorBlack NorWhite, unveiled a fresh women's footwear line. The new collection boasts four distinct sneaker silhouettes: the Nike Air Max Craze, Motiva, Pegasus 41, and the Calm slide. This partnership highlights Nike's commitment to blending innovative design with cultural influences, offering a unique and stylish range tailored for women.

- May 2025: Skechers USA Inc has unveiled the Skechers Aero Tempo, a performance-driven shoe emphasizing lightweight design and responsive cushioning. This new addition to its product portfolio is specifically engineered for runners who prioritize speed and agility, offering enhanced comfort and support to optimize their performance. The Aero Tempo reflects Skechers' commitment to innovation in athletic footwear, combining advanced materials and cutting-edge design to meet the demands of competitive and recreational runners alike.

Global Footwear Market Report Scope

Footwear is a protective covering for the feet, such as shoes, sandals, and other types. These products protect the feet from hurting the feet and help in easing day-to-day physical activities.

The scope of the global footwear market includes type, end user, distribution channel, and geography. Based on type, the market is segmented into athletic footwear and non-athletic footwear. The athletic footwear segment includes running shoes, sports shoes, trekking/hiking shoes, and other athletic footwear types. The non-athletic footwear segment includes boots, flip-flops/slippers, sneakers, and other non-athletic footwear. Further segmentation is done based on end users, which includes men, women, and kids. The segmentation based on the distribution channel includes offline retail stores and online retail stores. The report outlines the insights of all the global regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

Segmentation Overview

| Athletic Footwear | Running Shoes |

| Sports Shoes | |

| Trekking/Hiking Shoes | |

| Other Athletic Footwear | |

| Non-Athletic Footwear | Boots |

| Flip-Flops/Slippers | |

| Sneakers | |

| Other Non-Athletic Footwear |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Athletic Footwear | Running Shoes |

| Sports Shoes | ||

| Trekking/Hiking Shoes | ||

| Other Athletic Footwear | ||

| Non-Athletic Footwear | Boots | |

| Flip-Flops/Slippers | ||

| Sneakers | ||

| Other Non-Athletic Footwear | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global footwear market?

The footwear market size reached USD 400.64 billion in 2026 and is projected to hit USD 471.32 billion by 2031.

Which region leads global footwear demand?

North America leads global footwear demand with 31.26% share, driven by strong consumer appetite for sustainable, premium, and tech-integrated products.

Which product category is growing fastest?

Athletic footwear is forecast to post the quickest 4.67% CAGR through 2031 due to continued athleisure adoption.

What drives premium footwear growth?

Consumers pay for limited editions, eco-friendly materials, and advanced cushioning, supporting a 4.49% CAGR in the premium segment.

Page last updated on: