Thailand Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

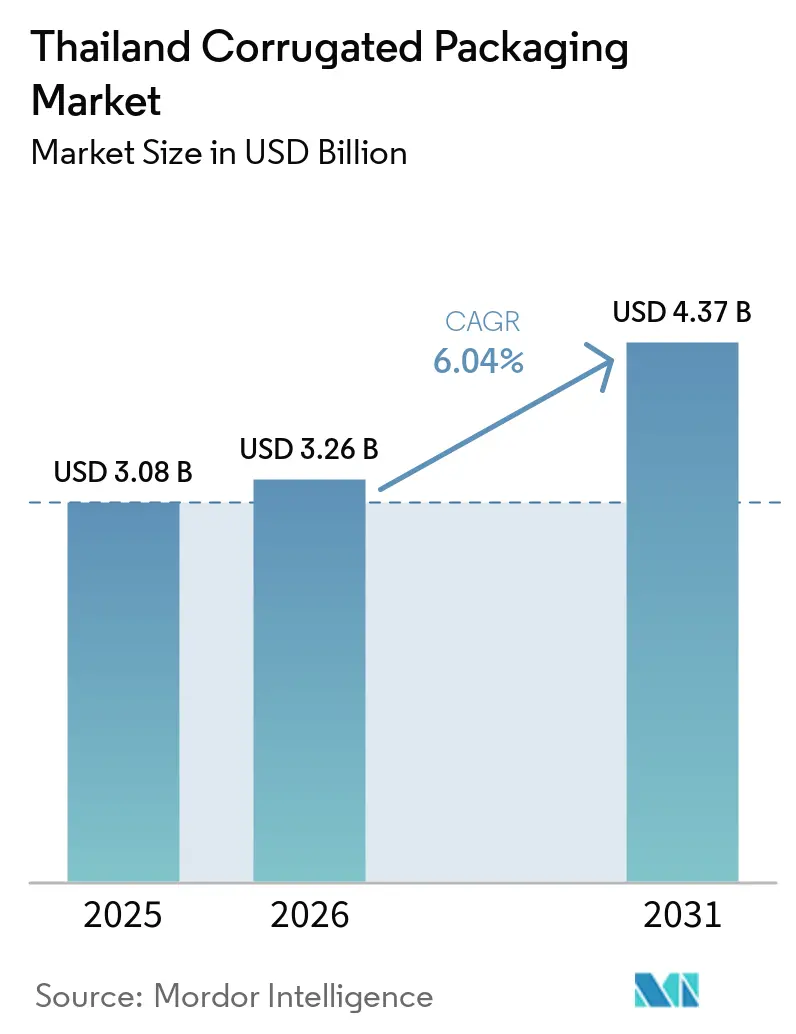

| Base Year Market Size (2025) | USD 3.08 Billion |

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Corrugated Packaging Market Analysis by Mordor Intelligence

The Thailand corrugated packaging market size was valued at USD 3.08 billion in 2025 and estimated to grow from USD 3.26 billion in 2026 to reach USD 4.37 billion by 2031, at a CAGR of 6.04% during the forecast period (2026-2031). Expanding e-commerce parcel volumes, sustained processed-food exports, and brand demand for high-color retail displays are reinforcing steady structural growth. Investment incentives from the Board of Investment have lowered conversion costs for automation and digital printing, while January 2026 packaging-waste rules mandate recyclable or reusable formats, accelerating the move toward recycled linerboard. Capacity additions by integrated producers are reshaping supply dynamics, yet energy price volatility and recycled-pulp import disruptions into China keep input costs unpredictable. Mid-tier converters respond by widening supplier bases and adopting time-of-use electricity contracts, preserving competitiveness across domestic and export cartons.

Key Report Takeaways

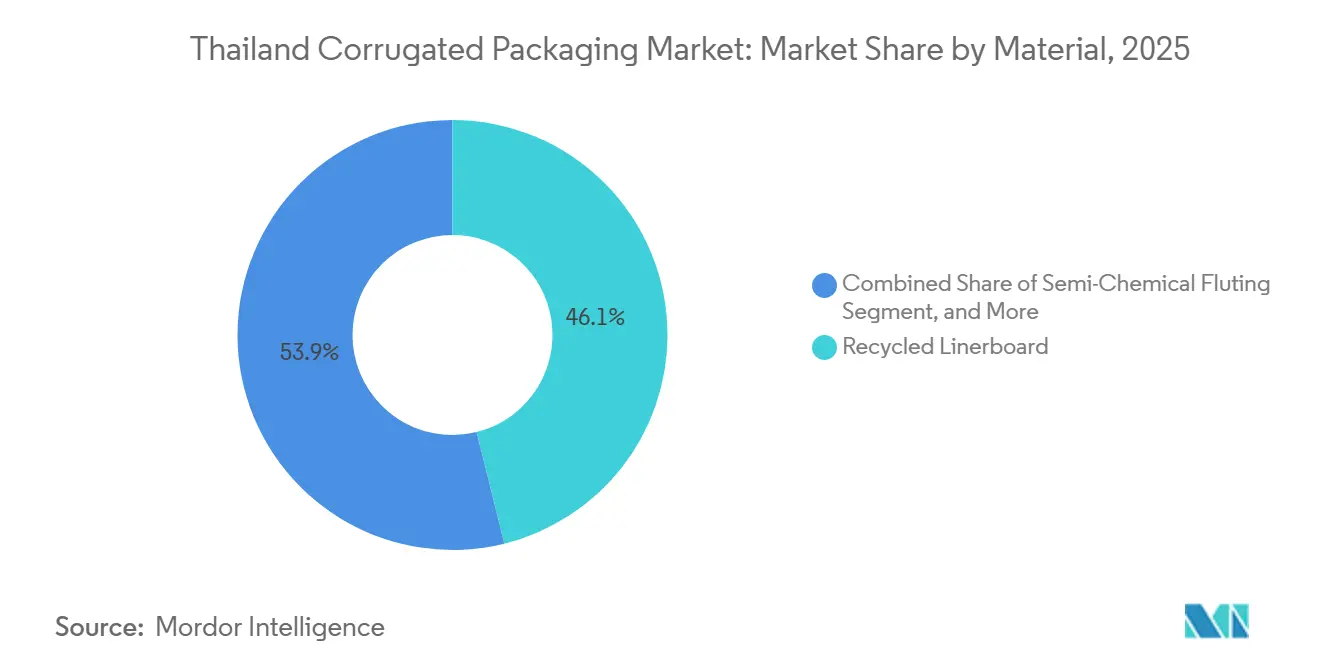

- By material, recycled linerboard captured 46.12% of the Thailand corrugated packaging market share in 2025.

- By flute type, the Thailand corrugated packaging market size for the E flute segment is forecast to advance at a 7.99% CAGR through 2031.

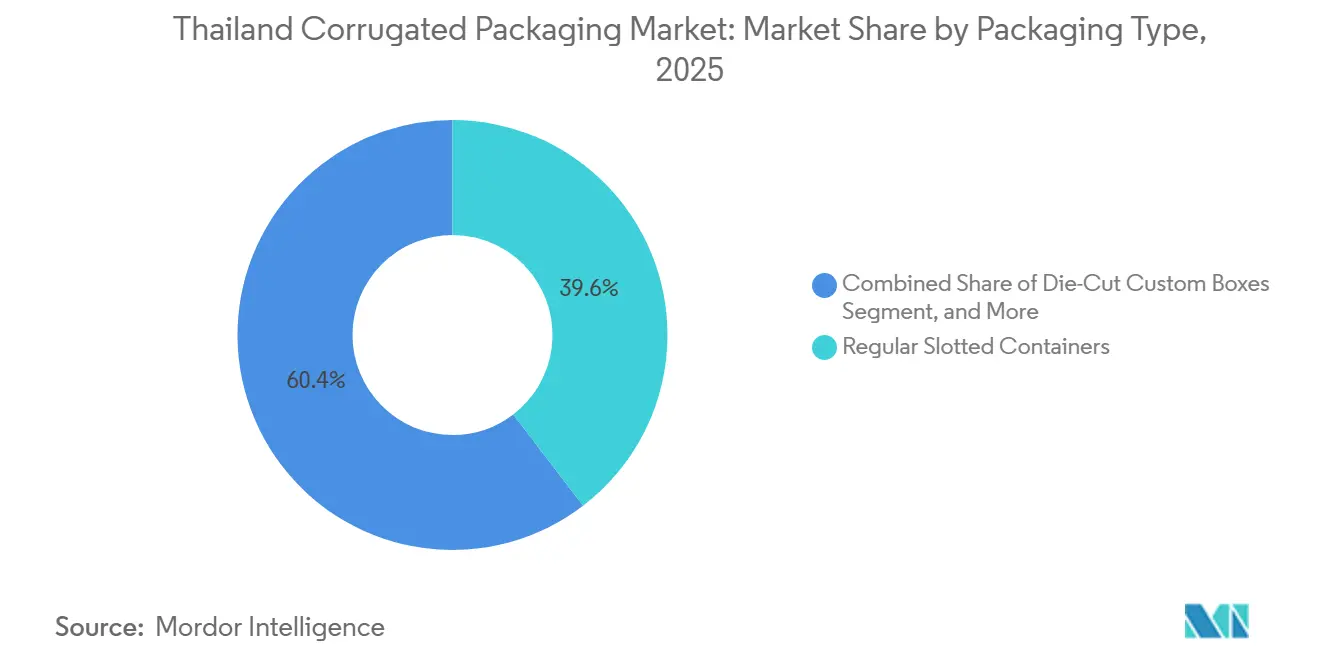

- By packaging type, regular slotted containers captured 39.61% of the Thailand corrugated packaging market share in 2025.

- By wall type, the Thailand corrugated packaging market size for the triple-wall boards segment is forecast to advance at a 7.84% CAGR through 2031.

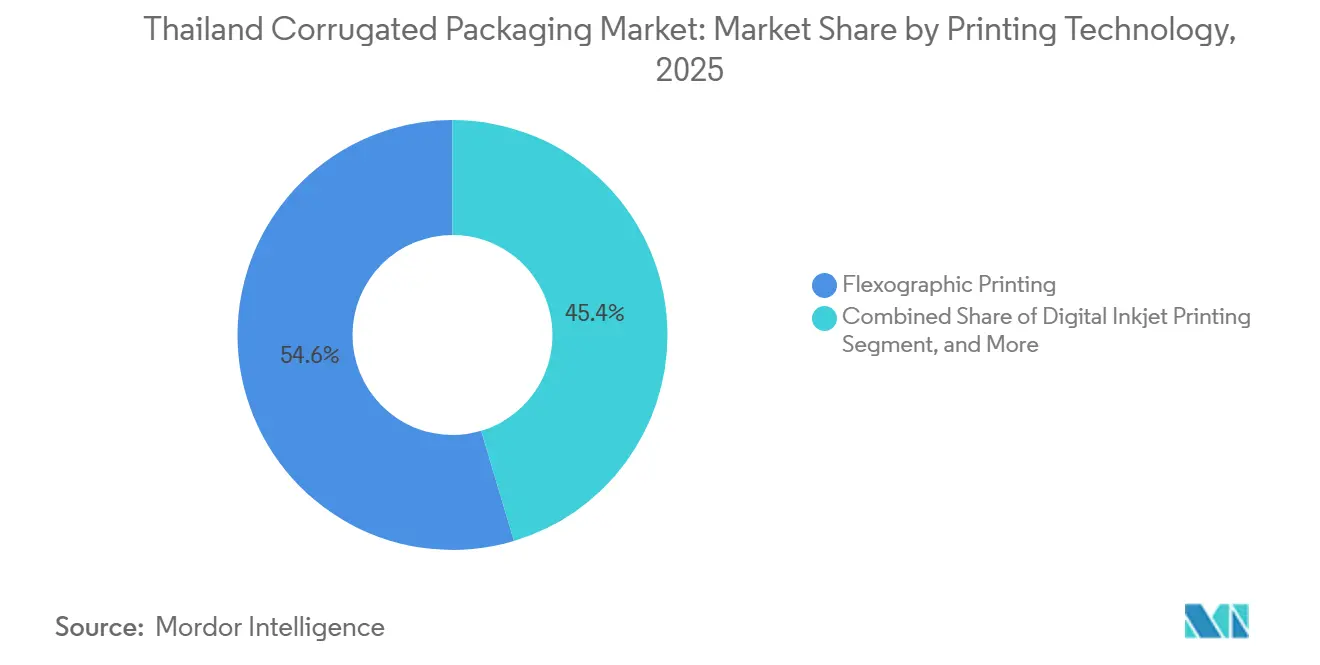

- By printing technology, flexographic printing captured 54.62% of the Thailand corrugated packaging market share in 2025.

- By end-user industry, the Thailand corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Expansion Accelerating Parcel Volumes | +1.80% | National, concentrated in Bangkok Metropolitan Region and Eastern Economic Corridor | Short term (≤ 2 years) |

| Thailand BOI Incentives for Sustainable Packaging Manufacturing | +1.20% | National, preferential zones in Eastern Economic Corridor | Medium term (2-4 years) |

| Rapid Growth in Processed-Food Exports | +1.40% | National, export-oriented clusters in Eastern and Central regions | Medium term (2-4 years) |

| Shift Toward Lightweight Recycled Linerboard | +0.90% | National | Long term (≥ 4 years) |

| Retail Adoption of High-Color Digital Print Displays | +0.60% | National, early uptake in Bangkok and major retail hubs | Short term (≤ 2 years) |

| ASEAN Cross-Border Trade Growth via RCEP | +0.70% | National, spillover to ASEAN partners | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Expansion Accelerating Parcel Volumes

Thailand’s online spending is set to rise from USD 26 billion in 2024 to USD 60 billion by 2030, giving the Thailand corrugated packaging market direct exposure to a fast-growing parcel stream.[1]Sasathorn Phaspinyo, “Thailand's Logistics Hub Drives Innovation And Cross-Border Trade,” FedEx China, fedex.com TikTok Shop alone has tripled its gross merchandise value year-over-year, spurring merchants to demand right-sized corrugated mailers that move smoothly through automated sortation.[2]Growth HQ Editorial Team, “TikTok Shops Southeast Asia Takeover: Key Logistics Insights,” Growth HQ, growthhq.io Same-day delivery rollouts by major platforms rely on fulfillment centers that now integrate robotics in 75% of large Thai operations, lifting unit velocities and corrugated-box turnover. Lazada’s new facility in the Eastern Economic Corridor cut packing lead time from around two hours to 14 minutes, illustrating how automation multiplies carton demand. Converters able to supply tamper-evident, auto-locking designs gain preferred-vendor status with marketplaces that benchmark damage-free delivery rates.

Thailand BOI Incentives for Sustainable Packaging Manufacturing

The Board of Investment classifies smart, active, and intelligent packaging as promoted activities, granting up to an eight-year corporate tax holiday and full machinery-duty exemptions. Foreign investors also secure land-ownership rights, encouraging multinationals to site converting plants near deep-water ports.[3]Bangkok Post Staff, “BOI Adds Smart Packaging,” Bangkok Post, bangkokpost.com Corrugators that install Industry 4.0 production lines qualify for an extra three-year 50-100% tax reduction.[4]Thailand Board of Investment, “BOI Investment Promotion Privileges,” thailand.go.th SCG Packaging earmarked THB 10,000 million (USD 265 million) for 2026 to expand automated lines and implement artificial-intelligence quality control, expecting annual savings of THB 600 million (USD 18.2 million). Incentives shorten payback periods on high-speed digital presses and energy-efficient corrugators, lifting sector productivity.

Rapid Growth in Processed-Food Exports

Durian output is projected to reach 1.89 million tonnes in 2026, up 21% year-on-year, and most shipments are in ventilated corrugated cartons engineered for long-haul transport to China. Cassava pellet exports worth USD 3.13 billion now reach Middle Eastern feed buyers, prompting the need for humidity-barrier liners. Chicken-meat export earnings of USD 4.31 billion demand hygienic, frozen-grade boxes that maintain integrity at -18 °C or below. The government’s “Thailand, The Land of Tropical Fruits” campaign pushes brand-specific packaging for diversified markets, multiplying small-lot print jobs. These developments widen the specification range that the Thailand corrugated packaging market must serve, from breathable produce crates to moisture-resistant cases.

Shift Toward Lightweight Recycled Linerboard

SCG Packaging recycled 3.8 million tonnes of recovered paper in 2024, meeting 97% of its packaging-paper fiber needs. Import sourcing from Europe, the United States, and Japan fills quality gaps, while acquisitions in the Netherlands and the United States secure high-grade old corrugated containers. Panjapol Pulp Industry’s FSC-certified mills now integrate solar power and bark dryer technology to halve daily coal consumption. Lightweight linerboard lets shippers cut basis weight without losing edge-crush resistance, lowering freight costs as container rates stay volatile. Global brands that track Scope 3 emissions increasingly specify recycled content, reinforcing long-run demand for this grade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Recycled Paper Supply | -1.10% | National, exposed to China import policy and global RCP flows | Short term (≤ 2 years) |

| Rising Energy Costs for Corrugators | -0.80% | National, higher impact on grid-reliant plants | Short term (≤ 2 years) |

| Capacity Overbuild in Bangkok Region | -0.40% | Bangkok Metropolitan Region and neighboring provinces | Medium term (2-4 years) |

| Increasing Use of Reusable Plastic Crates | -0.30% | National, notably in produce and beverage channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Recycled Paper Supply

China’s October 2025 rule capping impurities in recycled dry pulp at 0.5% led to 3,000-4,000 Thai containers held at Chinese ports, straining cash flows and plunging prices for a two-month window. Thailand ships up to 3 million tonnes of dry pulp to China annually, so a lower import ceiling may squeeze smaller processors unable to upgrade sorting lines. Price swings have already shown a 21% volume drop in February 2025 despite a 1.3% price uptick. Converters are hedging risk by installing AI-enabled quality-inspection systems and diversifying fiber imports, yet input-cost uncertainty weighs on long-term contracts.

Rising Energy Costs for Corrugators

Industrial electricity exceeds THB 4.5 (USD 0.13) per kWh during weekday peaks, falling to roughly THB 2.6 (USD 0.07) off-peak, while the quarterly Fuel Adjustment Charge mirrors global natural-gas trends. Energy can account for 12% of box-making costs, and a Trang Cannery case study showed that per-unit electricity use rose nearly 50% as line utilization fell. Rooftop solar, biomass boilers, and time-of-use tariffs cut power bills 10-15%, but smaller converters lack capital for such retrofits. When pulp prices rise in tandem with power surcharges, margin compression deepens, slowing machinery upgrades across the Thailand corrugated packaging industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Linerboard Gains Long-Term Leadership

Recycled linerboard held 46.12% share of the Thailand corrugated packaging market size in 2025, and its 7.31% CAGR to 2031 reflects regulatory pushes for full recyclability. Converters are downgrading basis weights, yet edge-crush strength is maintained via improved fiber mixing and starch formulations. Vertical integration by leading mills secures feedstock, buffering clients against global spikes in recovered-paper prices. Virgin Kraft still serves export loads needing high burst strength, while semi-chemical fluting balances cost and strength in multi-wall builds. Special moisture-barrier coatings remain niche but vital for durian or cassava cargoes that undergo moisture cycling in humid holds.

The Thailand corrugated packaging market benefits from BOI incentives that offset capital costs for recycled-paper processing lines, allowing mid-tier firms to match integrated giants on sustainability claims. Remote sensors now track board moisture and compressive strength in real time, helping brands verify recycled content without sacrificing performance. As 2030 recyclability targets near, demand for mono-material structures grows, anchoring recycled linerboard’s expansion trajectory.

By Flute Type: E Flute Rises on Shelf-Ready Appeal

B flute accounted for 37.85% of revenue share in 2025, continuing to dominate shipping cartons where cushioning and stacking strength are essential. E flute’s 7.99% forecast CAGR stems from its slim caliper and fine flute pitch, which doubles shelf facings without enlarging footprints. Retailers prefer E flute displays because high-resolution graphics print directly onto the board, eliminating separate liners. Rising digital press penetration enables cost-effective short runs, enabling seasonal promotions.

The Thailand corrugated packaging market responds with precision-cutting lines that bring E flute speed closer to B flute throughput, trimming labor and scrap rates. High-performance adhesives stabilize the thinner profile, and converters now laminate thin micro flutes into tri-wall configurations for electronics exports. As omnichannel brands seek unified ship-and-shelf packs, E flute’s graphic clarity and space efficiency make it the primary upgrade path from traditional profiles.

By Packaging Type: Point-of-Purchase Displays Accelerate

Regular slotted containers covered 39.61% of 2025 revenue, anchoring industrial and export logistics. Yet point-of-purchase displays will post an 8.36% CAGR, driven by modern trade outlets replacing polypropylene boards with recyclable corrugated standees. Lightweight pallet displays roll directly to aisles, cutting restocking labor. Digital-inkjet presses personalize artwork for each campaign, reducing the inventory of slow-moving SKUs.

The Thailand corrugated packaging market favors die-cut designs that self-lock without tape, simplifying store setups and meeting chain-wide assembly standards. E flute and F flute variants enhance print fidelity, while water-based inks meet food-contact limits for snack or beverage promotions. Converters offering structural-design services secure higher margins as brand owners shift more trade-marketing spend into experiential retail.

By Wall Type: Triple-Wall Strengthens Export Protection

Single-wall boxes retained 50.84% share in 2025 because e-commerce fulfillment scales easily with lightweight stock. Triple-wall boards, forecast at 7.84% CAGR, secure heavy parts, automotive assemblies, and industrial machinery bound for global customers. Triple-wall meets U.S. federal shipping standards while reducing crate weight compared to plywood, boosting container utilization.

Thai specialist plants near Laem Chabang port integrate heavy-duty corrugators with inline die-cutters to fabricate oversized shippers for SUVs and agricultural equipment bound for North America. The Thailand corrugated packaging industry also deploys triple-wall configurations for airfreight of high-value electronics, where every kilogram shaved reduces charges. Double-wall remains the middle-ground option for appliances and beverage multipacks.

By Printing Technology: Digital Inkjet Crosses the Adoption Tipping Point

Flexographic printing commanded 54.62% share in 2025, thanks to low ink prices on high-coverage jobs. Digital inkjet’s 7.32% CAGR stems from its ability to cost-effectively run variable graphics without plates, making it ideal for e-commerce unboxing themes. Hybrid presses pair flexo flood-coats with single-pass inkjet detail, lowering digital ink consumption by up to 80%.

Kento modular hybrids allow converters to start with one flexo and one inkjet deck, scaling later as order depth widens. Water-washable photopolymer plates cut VOC emissions, aligning with BOI green-manufacturing metrics. Automation features like automatic pre-register, and LED-UV curing shrink makeready in minutes, raising overall equipment effectiveness across the Thailand corrugated packaging market.

By End-User Industry: E-Commerce Fulfillment Centers Outpace All Segments

Processed foods accounted for 27.91% of revenue in 2025, reflecting Thailand’s consistent role as a global supplier of protein and fruit. Fastest growth comes from e-commerce fulfillment centers at an 8.21% CAGR, fueled by social-commerce bursts and last-mile upgrades. Corrugated packagers now design auto-mailer systems that right-size each box on-the-fly, cutting void fill and dimensional-weight fees.

Fresh-produce shippers specify vented trays for durian and mango, while beverage brands adopt multi-depth blanks to secure PET bottles. Electronics exporters, who saw a 67% year-over-year surge in January 2026 shipments, require anti-static inserts and high edge-crush cartons. This evolutionary mix keeps the Thailand corrugated packaging industry closely linked to downstream manufacturing and digital-commerce trends.

Geography Analysis

Central Thailand, anchored by the Bangkok Metropolitan Region, accounts for the largest share of Thailand's corrugated packaging market, underpinned by dense consumer bases and proximity to industrial estates. High e-commerce penetration in Bangkok is accelerating parcel volumes, reinforcing demand for single-wall cartons. Eastern Seaboard provinces such as Chonburi and Rayong, positioned within the Eastern Economic Corridor, contribute robustly through automotive and electronics exports that favor triple-wall and heavy-duty solutions. The corridor’s port connectivity shortens delivery cycles, supporting regional printers that produce time-sensitive promotional displays.

Northern and Northeastern regions see steady growth as processed-food clusters around Chiang Mai and Khon Kaen expand, boosting durian, longan, and cassava exports. Ventilated produce cartons and moisture-resistant shipping cases command steady runs in these areas. Government-backed rail links to China under the Pan-Asia Railway initiative are expected to divert some sea freight, prompting converters to design cartons compatible with intermodal handling. Western Myanmar border trade further lifts corrugated demand for agricultural goods transiting Mae Sot.

Southern Thailand, dominated by seafood and rubber exports, relies on humidity-tolerant kraft and poly-coated liners. Rubber-glove manufacturers shipping to the United States and Europe require dust-free packaging that preserves sterility, adding niche volumes for high-specification cartons. Island tourism boosts local consumption of packaged beverages, prompting seasonal spikes in beverage carriers. Across all regions, the Thailand corrugated packaging market remains resilient by aligning structural designs with diverse climatic and logistical needs.

Competitive Landscape

SCG Packaging Public Company Limited leads the Thailand corrugated packaging market, accounting for 44% of its consolidated sales in the country and operating 0.92 million tonnes per year of fiber-packaging capacity. The December 2025 acquisition of PT Prokemas Adhikari Kreasi for IDR 467 billion (USD 981 million) added 144,000 tonnes of Indonesian capacity, fortifying a regional hub strategy. Thai Containers Group, the 70-30 joint venture between SCG and Rengo, continues to install high-speed digital presses, enabling six-color single-pass output at 10,000 boards per hour.

Mid-tier challengers focus on heavy-duty niches. Union and Oji Interpack fabricate triple-wall AAA-grade products near Samut Sakhon to serve automotive suppliers. Tri-Wall Thailand operates corrugating and fabricating plants near Laem Chabang port, synchronizing with Japanese equipment exporters seeking lightweight alternatives to wood crates. Market entry barriers have eased due to BOI incentives, yet raw-material integration and logistics networks keep scale players ahead.

Strategic moves revolve around vertical fiber sourcing, automation, and sustainability branding. SCG’s 99 recycling centers across ASEAN enhance security for recovered paper, while digital-print investments enable micro-runs for personalized campaigns. Smaller converters differentiate through design studios that co-create retail displays. Global buyers audit Thai plants for FSC certification and carbon footprint data, elevating compliance as a competitive lever in Thailand's corrugated packaging industry.

Thailand Corrugated Packaging Industry Leaders

SCG Packaging Public Company Limited

Oji Holdings Corporation

Rengo Co., Ltd.

Smurfit Westrock plc

Mondi Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Taokaenoi Food and Marketing, SCG Chemicals, and Dow Thailand initiated a circular packaging project converting multilayer snack-film waste into food-grade resin for new pouches, targeting commercial launch by end-2026.

- February 2026: ALPLA opened a 24,000 m² integrated plant in Chachoengsao, Thailand, adding injection molding and development facilities that complement its PET and HDPE recycling joint venture.

- December 2025: SCG Packaging completed the USD 981 million acquisition of PT Prokemas Adhikari Kreasi, gaining 144,000 tonnes annual corrugated capacity in West Java.

- October 2025: Rengo’s Thai Containers Group agreed to acquire 60% of Indonesian converter PT Prokemas Adhikari Kreasi, increasing Rengo’s Indonesian factory count to 12.

Thailand Corrugated Packaging Market Report Scope

The Thailand Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Thailand Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current value of the Thailand corrugated packaging market and its projected size by 2031?

The market stands at USD 3.26 billion in 2026 and is projected to reach USD 4.37 billion by 2031 at a 6.04% CAGR.

How are Thailand's BOI incentives shaping investments in corrugated packaging plants?

Up to eight-year tax holidays and duty-free machinery imports reduce payback periods for automated corrugators and digital presses, spurring domestic and foreign capacity additions.

Which material segment is growing fastest within Thailand's corrugated packaging sector?

Recycled linerboard is advancing at a 7.31% CAGR as regulators and brand owners prioritize full recyclability.

Why is digital inkjet printing gaining traction among Thai corrugated converters?

Single-pass inkjet enables cost-effective short runs and variable graphics, ideal for e-commerce promotions, while hybrid presses cut ink usage and makeready time.

How do China's import policies affect Thai recycled-paper exporters?

Tight impurity thresholds and full-container inspections create shipment delays, price volatility, and force smaller processors to upgrade quality-control systems or exit the trade.

Which end-user sector offers the strongest growth opportunity to corrugated suppliers?

E-commerce fulfillment centers, spurred by social-commerce platforms and same-day delivery expectations, are forecast to grow at an 8.21% CAGR through 2031.

Page last updated on: