Europe Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 60.5 Billion |

| Market Size (2026) | USD 62.77 Billion |

| Market Size (2031) | USD 73.58 Billion |

| Growth Rate (2026 - 2031) | 3.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Corrugated Packaging Market Analysis by Mordor Intelligence

The Europe corrugated packaging market size is expected to increase from USD 60.50 billion in 2025 to USD 62.77 billion in 2026 and reach USD 73.58 billion by 2031, growing at a CAGR of 3.23% over 2026-2031. Demand patterns split along two distinct tracks. Recycled-content rules under the EU Packaging and Packaging Waste Regulation are forcing mills to lock in stable recovered-paper supply even as spot prices swing sharply. At the same time, e-commerce platforms and meal-kit providers are shifting specifications toward lighter, shelf-ready boxes that trim freight costs and accelerate retail throughput. Innovation-led niches such as digitally printed, custom die-cut formats are growing at nearly twice the aggregate pace, while legacy commodity grades face margin pressure from energy and feedstock volatility. Competitive dynamics are moderate, with the newly formed Smurfit Westrock holding a near-20% regional footprint, yet no firm controls pricing across all segments.

Key Report Takeaways

- By material type, the recycled linerboard segment captured 44.43% of the Europe corrugated packaging market share in 2025.

- By flute type, the Europe corrugated packaging market size for e flute is projected to grow at an 5.23% CAGR through 2031.

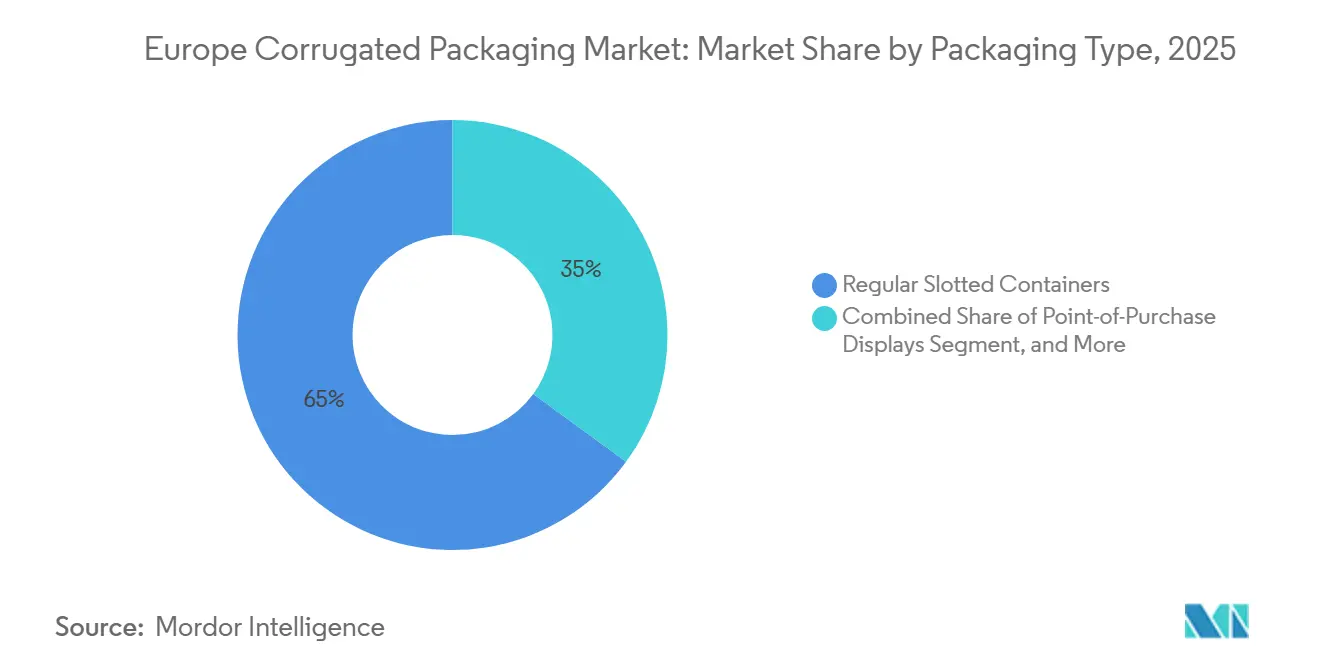

- By packaging type, the regular slotted containers segment captured 64.96% of the Europe corrugated packaging market share in 2025.

- By wall type, the Europe corrugated packaging market size for double-wall is projected to grow at an 5.56% CAGR through 2031.

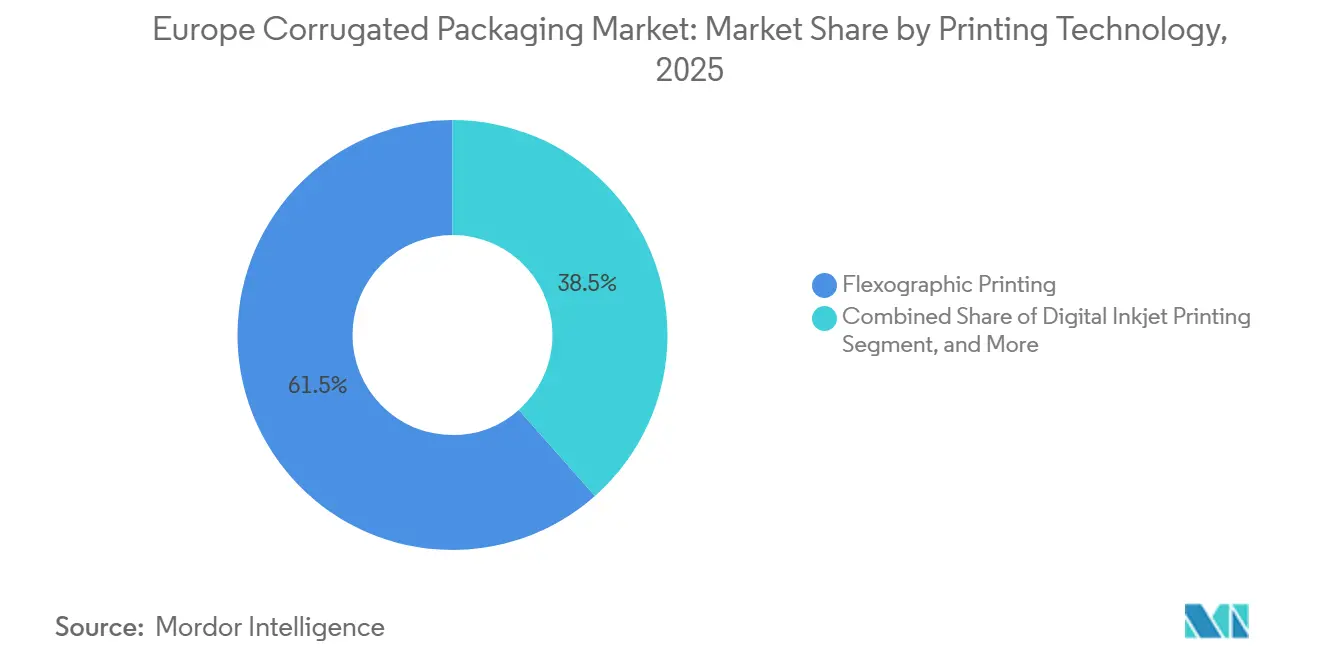

- By printing technology, the flexographic printing segment captured 61.53% of the Europe corrugated packaging market share in 2025.

- By end-user industry, the Europe corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.68% CAGR through 2031.

- By geography, the germany segment captured 24.63% of the Europe corrugated packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom Driving Demand for Lightweight Shipping Formats | +0.9% | Pan-European, strongest in Germany, France, United Kingdom, Benelux | Short term (≤ 2 years) |

| Shift Toward Plastic Substitution in FMCG Secondary Packaging | +0.7% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Mandatory Recycled-Content Targets Under EU Packaging and Packaging Waste Regulation | +0.6% | All EU member states | Long term (≥ 4 years) |

| Increasing Demand for Shelf-Ready Packaging in Retail Chains | +0.5% | Western Europe, expanding to Southern Europe | Medium term (2-4 years) |

| Automation of Corrugator Lines Enabling Shorter Lead-Times | +0.4% | Germany, France, Italy, Spain, Benelux | Long term (≥ 4 years) |

| Rapid Growth of Meal-Kit and Grocery Delivery Services | +0.3% | United Kingdom, Germany, France, Benelux, Nordic countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Demand for Lightweight Shipping Formats

Online retail platforms now specify lower-basis-weight boards that can withstand multiple automated sortation passes while reducing parcel freight costs. Amazon and Mondi released a 44-gram lighter mailer in 2025 that scales across millions of annual orders, saving thousands of tonnes of linerboard. Smurfit Westrock introduced a paper pallet wrap that substitutes plastic stretch film, widening corrugated’s role in unit-load stabilization. Lightweight profiles from BHS Corrugated lower grammage by 20 g/m² without sacrificing compression performance.[1]BHS Corrugated, “eCom Lightweight Profile,” bhs-world.com Cost, sustainability, and Scope 3 reporting pressures make this driver most acute in the three largest e-commerce markets.

Shift Toward Plastic Substitution in FMCG Secondary Packaging

Fast-moving consumer goods owners are eliminating shrink wrap, trays, and clamshells as they work toward compliance with the EU Single-Use Plastics Directive. DS Smith reported that it would replace more than 1.2 billion plastic packs with fiber-based designs by 2025. Klingele’s tie-up with Maistapack brought thermoformed fiber trays for fresh produce lines historically dominated by polystyrene. While demand lifts volume, Cepi cautioned in 2026 that accelerated substitution is draining recovered fibers to export markets, tightening domestic feedstock, and lifting input costs.

Mandatory Recycled-Content Targets Under EU Rules

The EU Packaging and Packaging Waste Regulation sets minimum recycled-content thresholds, a 50% ceiling on empty space, and digital product passport requirements. Compliance forces mills to invest in screening, de-inking, and barrier-coating innovations that reward vertically integrated groups with captive collection. Cepi warned in 2026 that recycled fiber outflows threaten supply, a tension likely to inflate costs for converters lacking closed-loop networks.

Increasing Demand for Shelf-Ready Packaging in Retail Chains

Supermarkets specify tear-strip, easy-open trays that move from truck to shelf with zero back-room labor. Smurfit Kappa’s ShelfSmart program increased sales by 13% for a snack brand by optimizing display visibility. The EU rule limiting empty space penalizes oversized cases, reinforcing exact-fit shelf-ready designs. Converters are expanding die-cutting and micro-perforation lines to satisfy these mandates across Germany, France, and the United Kingdom before cascading into Southern Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Costs Squeezing Mill Operating Margins | -0.5% | Italy, Spain, Germany, Nordic countries | Medium term (2-4 years) |

| Volatility in Old Corrugated Container Prices | -0.4% | Pan-European, acute in high recycled-linerboard users | Short term (≤ 2 years) |

| Competition From Reusable Plastic Crates in Fresh-Produce Logistics | -0.2% | Germany, France, Benelux, Nordic countries | Medium term (2-4 years) |

| Limited Corrugator Capacity Additions Due to Permitting Hurdles | -0.1% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Costs Squeezing Mill Operating Margins

Natural-gas prices jumped above EUR 68/MWh (USD 73/MWh) in March 2026, with Italy paying EUR 111/MWh (USD 119/MWh) because of its gas-heavy power mix. Stora Enso’s EUR 30 million (USD 32 million) Heinola upgrade cut emissions by 113,000 tCO₂ yet required multi-year capex. Energy shocks compress margins fastest at independent mills that lack hedging or CHP capacity, prompting temporary curtailments in Southern Europe.

Volatility In Old Corrugated Container Prices

Asian buyers pushed OCC prices up in December 2025, only for values to reverse weeks later. Mills that booked fiber at the peak could not immediately re-price finished boxes, eroding spreads. Cepi’s 2026 alert about OCC exports highlights the structural imbalance and foreshadows tighter contracts or vertical integration as converters seek feedstock security. This volatility disproportionately affects smaller converters lacking long-term supply contracts or vertical integration, widening the profitability gap between scale players and regional operators and potentially accelerating consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Sustains Leadership as Virgin Grades Rebound

Recycled linerboard owned 44.43% of Europe corrugated packaging market share in 2025. Widespread collection infrastructure and stable demand from grocery, beverage, and e-commerce channels anchor its dominance. Cepi’s preliminary 2024 data showed containerboard output rising 4.3% year-on-year, confirming supply resilience. Virgin Kraft Linerboard is projected to grow at 5.62% annually through 2031, as pharmaceuticals and premium foods require higher wet-strength and greater barrier-coating compatibility. Semi-chemical fluting gains relevance in triple-wall export cartons, where stiffness per gram outweighs cost. The European corrugated packaging market for virgin grades will expand as converters mitigate fiber-quality variability.

Competitive pricing gaps between recycled and virgin sheets have narrowed due to volatile OCC costs, reducing the automatic cost preference for recycled liners. Mayr-Melnhof flagged import pressure from Asia and extra Scandinavian capacity as forces weighing on recycled margins. Regulatory recycled-content mandates still tilt purchasing toward post-consumer fibers, yet brands may accept virgin inputs when functional barriers or food-contact rules complicate recycling pathways. The material mix, therefore, hinges on end-use performance more than price alone, a nuance that reshapes procurement within the European corrugated packaging market.

By Flute Type: Thin Profiles Capture Retail Display Budgets

B flute maintained 38.45% of overall volume in 2025, prized for its cushioning-to-weight balance. Brands are turning to E flute for direct-print retail-ready packs, propelling a 5.23% CAGR outlook through 2031. Digital white-ink launches eliminated historic print-quality gaps, making E flute viable for cosmetics and confectionery promotions. BHS Corrugated’s eCom profile is optimized for E and F flute runs, reducing paper usage while maintaining compression strength.

C flute and A flute support heavy goods but lose share where freight space, carbon targets, and shelf density matter more than maximum stacking strength. Regulatory empty-space limits further favor thinner flutes because oversized containers risk retailer penalties. As retailers standardize shelf-ready dimensions, converters extend microflute capability to guarantee strength in compact forms, sustaining momentum for thin profiles in the Europe corrugated packaging market size forecasts.

By Packaging Type: Custom Die-Cuts Monetize the Unboxing Moment

Regular slotted containers delivered 64.96% of segment revenue in 2025, due to automation compatibility and low unit cost. Direct-to-consumer brands, however, rate the social-media value of choreographed unboxing higher than marginal box price, driving die-cut custom formats toward a 5.45% CAGR. Flexographic inside-print, tear-away lids, and interior partitions reinforce product security and brand storytelling. The Europe corrugated packaging market size tied to die-cut boxes therefore rises faster than commodity grades.

Folding cartons produced on microflute cores blur lines with traditional solid board, extending corrugated into premium electronics and cosmetics. Point-of-purchase displays leverage digital inkjet for store-specific graphics, completing setup in hours without plate costs. Pallet boxes hold steady with industrial demand, but opportunities emerge for fiber-based pallet wraps that displace plastic film. Each niche reflects the growing willingness to pay for functional or aesthetic differentiation in the Europe corrugated packaging market.

By Wall Type: Triple-Wall Boards Protect Heavy Exports

Single-wall sheets represented 34.78% of 2025 sales, covering most grocery, apparel, and parcel traffic. Triple-wall structures are forecast to climb 5.56% annually as reshoring programs and machinery exports demand containers that withstand ocean bends and impacts. Automotive and industrial OEMs specify triple-wall bins that can be stripped and reused multiple cycles, diluting total cost over life. Single-face corrugated, used primarily for protective wrapping and void fill, is a niche segment yet is gaining traction as e-commerce operators seek alternatives to plastic bubble wrap and air pillows.

Double-wall boards balance cost and performance for appliances and furniture. Single-face liners replace bubble wrap as e-commerce operators seek curbside-recyclable void fill. Lightweighting breakthroughs enable some accounts to downgrade from double-wall to reinforced single-wall, trimming logistics emissions while meeting compression targets, a trend that reinforces efficiency goals within the Europe corrugated packaging market share landscape.

By Printing Technology: Digital Inkjet Moves From Niche To Mainstream

Flexographic presses retained 61.53% share in 2025 because large runs keep plate amortization low. Yet digital inkjet presses post a 5.78% CAGR to 2031 as SKUs proliferate and retailers request variable data for promotions and QR-code tracking. Saica’s order for HP PageWide C500 units underlines mainstream adoption. Mondi’s white-ink capability closes the color vibrancy gap on kraft liners, expanding the addressability of digital presses.[2]Mondi Group, “White Digital Print on E flute,” mondigroup.com

Litho-laminated sheets remain relevant for luxury spirits and fragrance packs, but inkjet speed gains are shrinking the crossover threshold. Screen and offset printing retreat to ultra-short or specialty work. As brands align with the EU’s recyclability guidance, single-step inkjet graphics avoid laminated films, supporting circularity objectives and sustaining growth momentum in the Europe corrugated packaging market.

By End-User Industry: E-Commerce Fulfillment Races Ahead Of Produce

Fresh food and produce accounted for 43.56% of demand in 2025, driven by entrenched use in refrigerated chains. Reusable plastic crates, however, cut damage 98% and are now pressure corrugated in berries, grapes, and leafy greens. Conversely, e-commerce fulfillment centers register the highest CAGR of 5.68% as same-day delivery and subscription services expand. Automation favors right-sized corrugated boxes over alternative substrates because paper fibers flow easily through recycling loops mandated by retailers.

Processed foods, beverages, and personal care products adopt shelf-ready cases to reduce labor and improve on-shelf presentation, sustaining mid-single-digit growth. Pharmaceuticals require tamper-evident, GDP-compliant packs that justify premium pricing. Industrial and automotive parts depend on triple-wall bulk bins. Collectively, these shifts diversify the Europe corrugated packaging market, cushioning cyclical downturns in any single vertical.

Geography Analysis

Germany generated 24.63% of regional revenue in 2025, supported by automotive and FMCG clusters that demand high-volume corrugated supply chains. Vertical integration, such as Klingele’s paper-mill network, affords just-in-time service advantages. Energy diversification tempers exposure to gas shocks compared with Southern peers. Cepi’s 2024 statistics confirmed Germany as the single largest contributor to the region’s containerboard output growth.

France, the United Kingdom, Italy, and Spain together form the next tier. French converters battle fragmentation, while British sellers tailor packs to stringent retailer scorecards. Italy bears the heaviest energy burden, paying EUR 111/MWh (USD 119/MWh) in March 2026 and prompting mills to accelerate renewable investments. Spain increased production to 5.863 billion m² in 2024, but flat revenue underscored weak pricing. Saica’s LIC Packaging stake illustrates cross-border deals aimed at Southern Europe’s growth pockets.[3]Saica Group, “LIC Packaging Acquisition,” saica.com

Benelux and Nordic markets, though smaller, outperform on growth as e-commerce penetration and sustainability mandates align. A new BHS corrugator in Belgium raised Lammerant’s productivity 20% in 2025, enabling same-week FMCG runs. Stora Enso’s Heinola upgrade combined capacity with a 113 ktCO₂ annual cut, signaling the Nordic model of low-carbon scaling. Eastern Europe, grouped under Rest of Europe, is slated for the fastest CAGR to 2031 as fresh-produce exports and near-shoring stimulate local corrugated demand.

Competitive Landscape

Europe corrugated packaging market competition remains moderate. The 2024 Smurfit Kappa-WestRock merger created a transatlantic leader with roughly 20% regional volume but lacked universal pricing sway. Mondi added 13 Schumacher plants in 2025, boosting density and proximity to just-in-time customers. Stora Enso balanced brownfield expansion and decarbonization with its Heinola project.

VPK Group raised its Ribble Packaging stake to 50% and purchased Open Imballaggi, signaling a preference for joint ventures that respect local ownership while expanding its footprint. Digital alliances are spreading: Saica bought HP presses, and HP signed a USD 50 million pact with ePac to expand inkjet reach across substrates.[4]HP Inc., “PageWide C500 Installation at Saica,” hp.com Smaller converters exploit short-run digital agility, yet rising capex needs for energy and sustainability upgrades tilt the field toward capital-strong players.

EU recycled-content mandates further favor integrated groups with captive collection, nudging the market toward measured consolidation without eliminating regional specialists. BHS Corrugated's Corruverse digital ecosystem and HP's PageWide digital presses are concentrated among large, multi-site operators, while smaller converters rely on flexographic printing and manual changeovers, widening the performance gap and potentially forcing exits or acquisitions.

Europe Corrugated Packaging Industry Leaders

Smurfit Westrock plc

Mondi plc

International Paper Company

Stora Enso Oyj

Klingele Papierwerke SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mayr-Melnhof Karton reported USD 4.27 billion equivalent revenue for 2025 and a USD 215 million adjusted operating profit, noting continued overcapacity in European cartonboard.

- February 2026: HP inked a USD 50 million agreement with ePac to extend digital printing across flexible substrates, paving the way for hybrid corrugated-flexible campaigns.

- February 2026: Cepi warned that accelerated paper substitution for plastics is drawing recycled fibers out of the EU and could jeopardize circular goals.

- September 2025: Mondi launched white digital printing on corrugated, unlocking premium graphics on kraft liners.

Europe Corrugated Packaging Market Report Scope

The Europe corrugated packaging market encompasses the production, distribution, and utilization of corrugated packaging materials across various industries. Corrugated packaging, known for its durability and recyclability, is widely used for shipping, storage, and other purposes. This market includes a range of products such as corrugated boxes, sheets, and trays, catering to sectors like food and beverage, pharmaceuticals, electronics, and others. The study focuses on analyzing market trends, growth drivers, challenges, and opportunities within the forecast period.

The Europe Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries), and Geography (Germany, France, United Kingdom, Italy, Spain, Benelux, Nordic Countries, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Benelux |

| Nordic Countries |

| Rest of Europe |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries | |

| By Geography | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Benelux | |

| Nordic Countries | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe corrugated packaging market by 2031?

Europe corrugated packaging is forecast to reach USD 73.58 billion by 2031, expanding at a 3.23% CAGR from 2026 to 2031.

Which geographic block is expected to add capacity fastest through 2031?

Southern and Eastern European countries are projected to post the quickest growth as fresh-produce exports and regional e-commerce fulfillment expand.

How are EU recycled-content rules influencing converter strategy?

Mills are investing in fiber-sorting, de-inking, and barrier-coating assets to satisfy minimum recycled-content thresholds, while vertically integrated players are locking in captive OCC streams to hedge price swings.

Why is digital inkjet printing gaining share in European corrugated?

Brand owners want variable-data graphics and rapid SKU changeovers without plate costs; new white-ink capabilities now deliver photo-quality results on kraft liners, widening the addressable range.

What segment shows the highest growth rate within end-use applications?

E-commerce fulfillment centers are projected to record a 5.68% CAGR to 2031, the fastest among all verticals, driven by same-day delivery and subscription-box demand.

How concentrated is the competitive landscape after recent consolidation?

Even after the Smurfit Westrock merger, the top five suppliers control just over 60% of regional volume, indicating a moderately concentrated field where mid-tier specialists still operate profitably.

Page last updated on: