Ireland MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

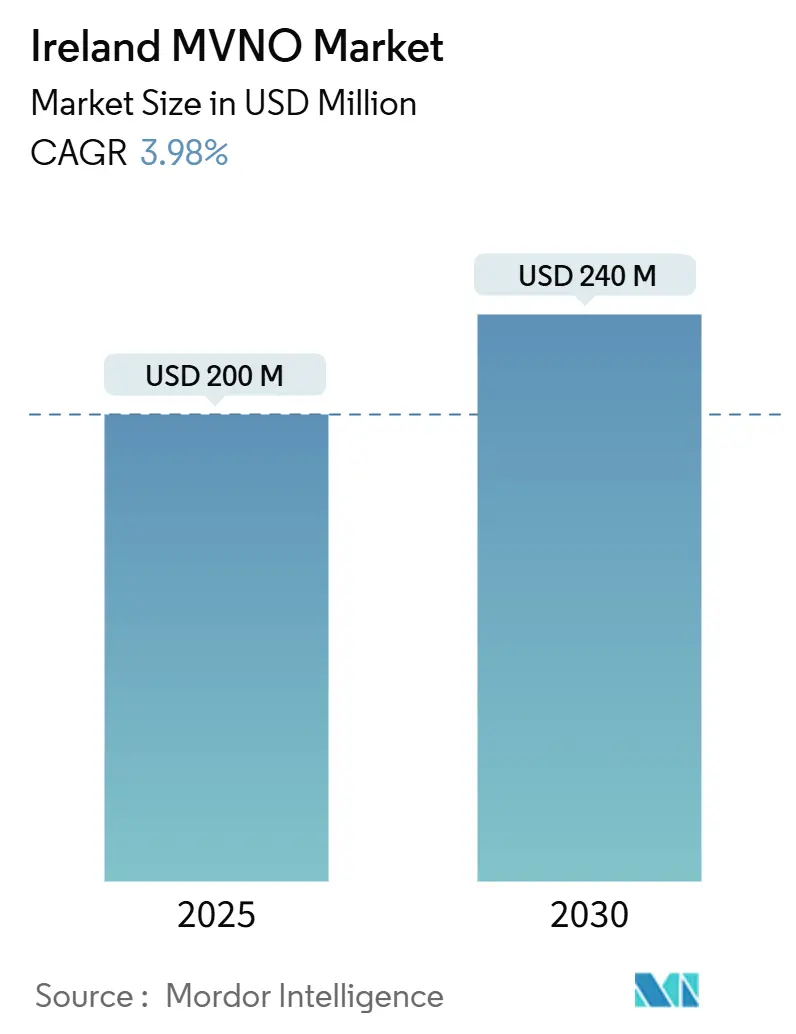

| Market Size (2025) | USD 200 Million |

| Market Size (2030) | USD 240 Million |

| Growth Rate (2025 - 2030) | 3.98% CAGR |

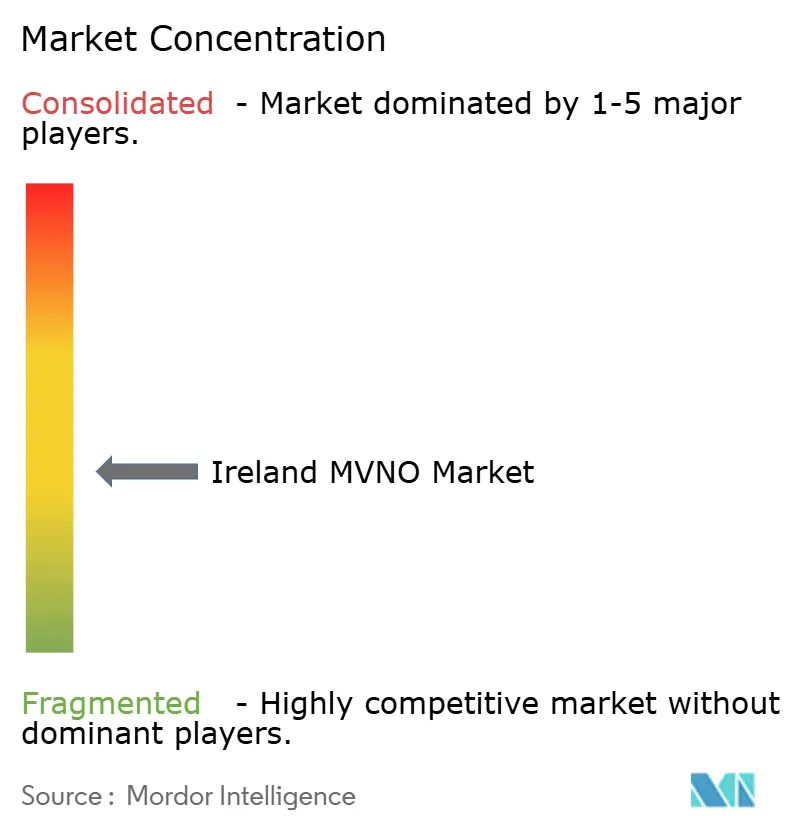

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland MVNO Market Analysis by Mordor Intelligence

The Ireland MVNO Market size is estimated at USD 200 million in 2025, and is expected to reach USD 240 million by 2030, at a CAGR of 3.98% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 1.29 million subscriber in 2025 to 1.54 million subscriber by 2030, at a CAGR of 3.55% during the forecast period (2025-2030).

The Ireland MVNO market is transitioning from rapid subscriber acquisition to disciplined profitability as price-led competition from digital-only sub-brands, stringent wholesale rules, and brisk 5G rollout reshape strategic priorities. Intensifying discount propositions, expanding capacity-based wholesale access, and an accelerating shift from voice-centric to data- and IoT-centric usage patterns have collectively compressed margins while broadening addressable use cases. With 4G/LTE still accounting for almost seven in ten connections, the Ireland MVNO market also faces a fast-moving 5G upgrade cycle that opens doors to network-slicing services for enterprise and public-sector IoT clients. Operators that combine cloud-native platforms with full-MVNO control are best positioned to scale new offerings quickly and offset consumer price erosion.

Key Report Takeaways

- By operational mode, Full MVNOs commanded 54.22% of the Ireland MVNO market share in 2024 and are tracking a 15.59% CAGR to 2030.

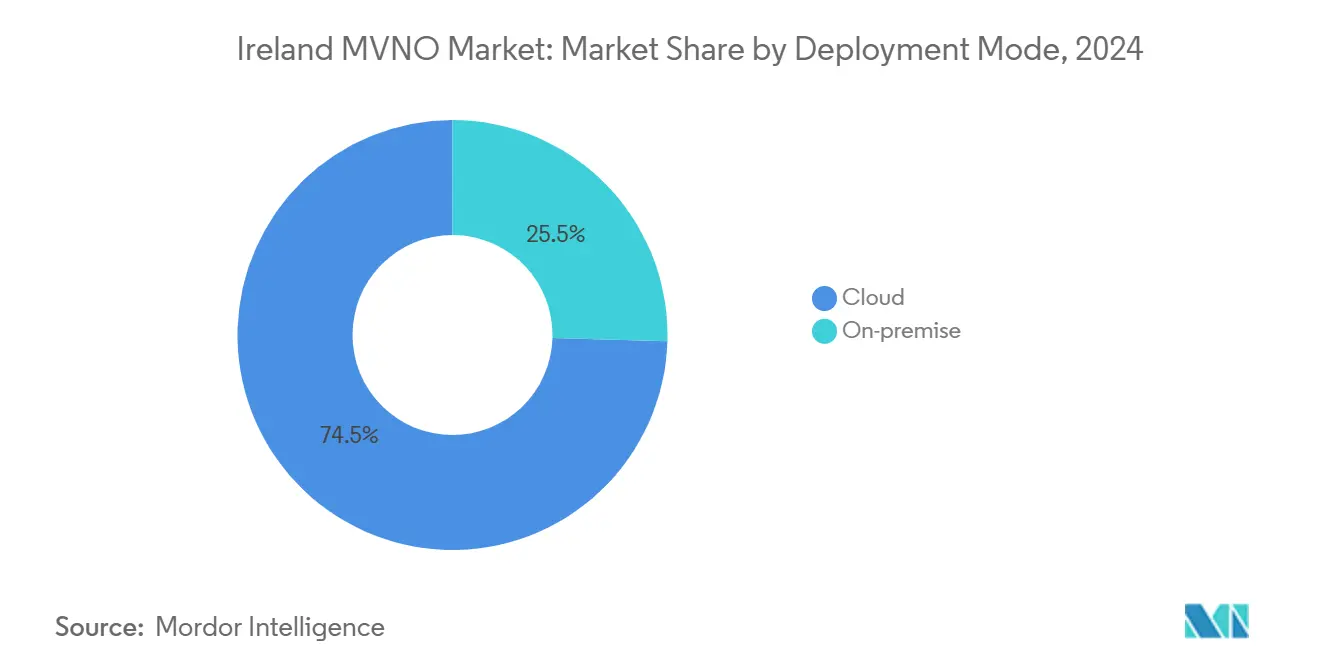

- By deployment model, cloud-based solutions captured 74.54% of the Ireland MVNO market size in 2024; on-premise infrastructure is expanding at a 7.30% CAGR through 2030.

- By subscriber type, the consumer segment held 76.06% revenue share in 2024, while IoT-specific connections are forecast to grow at an 18.00% CAGR.

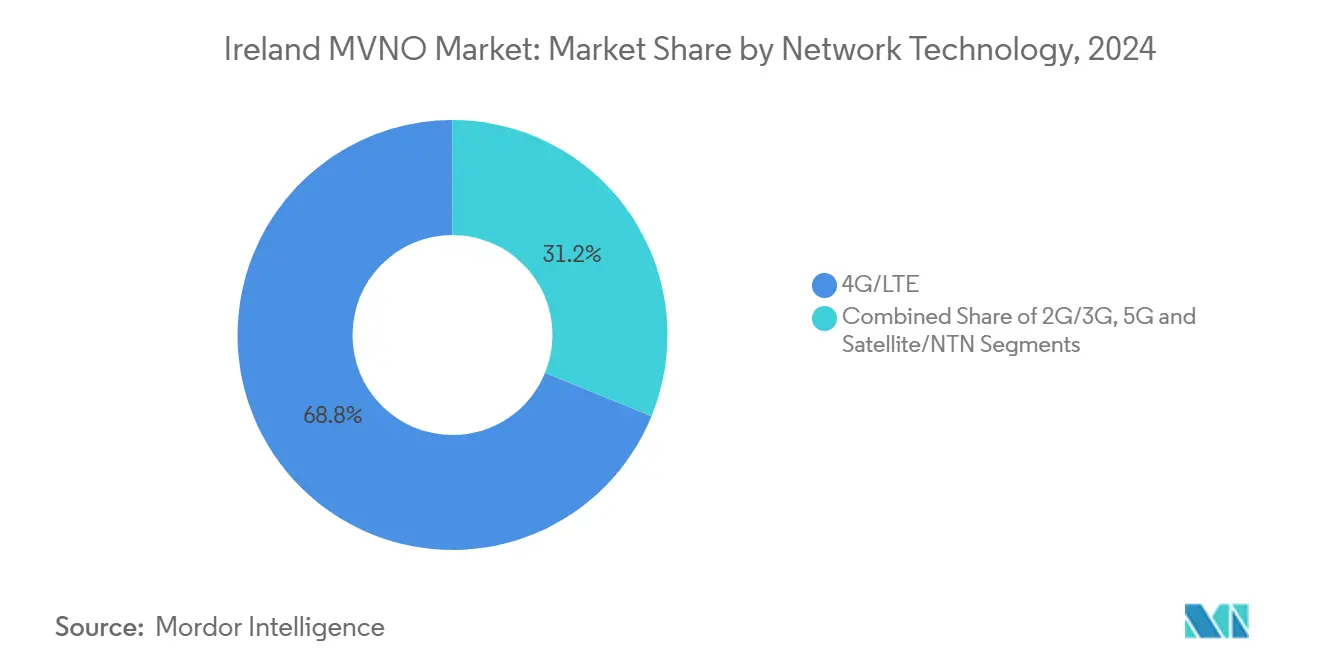

- By network technology, 4G/LTE dominated with 68.83% share of the Ireland MVNO market size in 2024; 5G lines are accelerating at a 24.90% CAGR to 2030.

- By distribution channel, online and digital-only sales reached 56.67% share in 2024 and are advancing at a 6.75% CAGR, reflecting a decisive shift toward direct-to-consumer onboarding.

Ireland MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price-based competition from digital-only discount sub-brands (GoMo, 48) | +0.8% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Expansion of capacity-based wholesale access mandated by ComReg (post-Three/O2 merger) | +1.2% | National | Medium term (2-4 years) |

| Surging demand for low-cost quad-play bundles (Sky, Virgin) | +0.6% | National, with early gains in Dublin, Cork | Medium term (2-4 years) |

| Accelerating enterprise and public-sector IoT connectivity demand (Cubic Telecom, Vodafone IoT) | +0.9% | National, enterprise hubs | Long term (≥ 4 years) |

| 5G network-slicing and private-network resale opportunities for full-MVNOs | +0.7% | National, industrial zones | Long term (≥ 4 years) |

| Post-Brexit roaming-fee arbitrage pulling UK visitors onto Irish prepaid SIMs | +0.3% | Border regions, tourist areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Price-Based Competition from Digital-Only Discount Sub-Brands

Digital-only propositions such as GoMo and 48 have dismantled traditional cost structures by forgoing physical retail, automating support, and piggybacking on parent-MNO radio layers. GoMo’s roaming tariff of EUR 0.03 per MB illustrates how vertically integrated MVNOs can undercut independents yet still retain margin through volume-linked wholesale deals. [1]GoMo, “EU Roaming Tariffs,” gomo.ie In response, smaller brands are pivoting toward niche-focused customer experience, tailored content bundles, or hyper-localized marketing where pure price wars are less decisive. Consumers have come to expect unlimited data packages priced below EUR 20 per month, raising the bar for baseline offers and forcing renewed focus on service differentiation, loyalty perks, and app-led self-care. The Ireland MVNO market therefore rewards brands that blend lean overhead with selective value-added services rather than blanket discounts.

Expansion of Capacity-Based Wholesale Access Mandated by ComReg

In its post-merger remedies for Three’s acquisition of O2, ComReg obliged MNOs to extend capacity-priced wholesale agreements that scale costs with actual usage rather than rigid flat fees. The rule change, in force through 2024 and expected to remain the template for future renewals, finally allows MVNOs to price unlimited data without incurring punitive overage costs or volume tier penalties. Early adopters, notably Virgin Mobile, have leveraged the policy to refresh all-data bundles and sharply grow net adds over 2024. The Ireland MVNO market benefits further as full-MVNOs gain negotiating leverage, enabling multi-network wholesale access, diversified fallback coverage, and stronger retail offers. The structure also lays groundwork for enterprise 5G network slicing, where bandwidth classes can be contracted on predictable cost curves.

Surging Demand for Low-Cost Quad-Play Bundles

Sky Mobile’s September 2024 entry signaled the rise of all-inclusive broadband-TV-voice-mobile bundles tailored to households already paying for premium content. [2]Independent News and Media, “Sky Mobile Eyes Quad-Play Upside,” independent.ie By cross-subsidizing mobile ARPU downwards to protect higher-margin pay-TV revenue, Sky and Virgin Media have tightened competitive screws on stand-alone MVNOs. Bundle penetration is heaviest in Dublin’s commuter belt and Cork’s tech corridors, where fibre penetration is high and multiscreen households prize seamless entertainment. Independent players now face a two-pronged challenge: either negotiate OTT or streaming tie-ups to match perceived bundle value, or double-down on specialized segments such as student SIMs, migrant calling packs, or digital-nomad data vaults. As the Ireland MVNO market matures, convergence economics favor firms that combine broadband pipes, premium content, and mobile data into a single bill.

Accelerating Enterprise and Public-Sector IoT Connectivity Demand

SoftBank’s EUR 473 million acquisition of Cubic Telecom underscored the strategic weight of specialized IoT MVNOs supplying automotive majors and multinational manufacturers. Rising deployment of connected vehicles, smart utilities, and municipal sensor grids boosts demand for multi-IMSI subscription management, zero-touch provisioning, and 5G Stand-Alone slices with deterministic latency. Public bodies tendering smart-city pilots increasingly stipulate local data residency and strict service-level guarantees, factors that full-MVNOs meet more readily than lightweight resellers. Over time, enterprise IoT’s higher ARPU and multi-year contract stickiness are expected to cushion the Ireland MVNO market against saturated consumer voice lines, while also fostering new wholesale constructs around API-based device orchestration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated mobile-subscriber penetration limiting organic growth | -0.9% | National | Short term (≤ 2 years) |

| High wholesale access fees and unfavorable data volume tiers for MVNOs | -1.1% | National | Medium term (2-4 years) |

| Cannibalisation by MNO controlled sub-brands (GoMo by Eir, 48/Clear by Three/Vodafone) | -0.7% | National, urban concentration | Short term (≤ 2 years) |

| Slow eSIM enablement and fragmented OTA provisioning standards | -0.4% | National, device-dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Saturated Mobile-Subscriber Penetration Limiting Organic Growth

Ireland’s active SIM penetration has exceeded 100% since 2024, meaning any incremental customer must be poached from a rival rather than newly created. This zero-sum reality heightens acquisition costs as cash-rich MNO sub-brands fight churn with rolling flash sales and heavily discounted introductory plans. Smaller MVNOs see payback periods lengthen and must allocate more budget to retention, loyalty rewards, and referral bonuses—raising overall cost-to-serve. With base voice and SMS usage flat, monetization pivots to upselling data allowances, premium roaming, or device financing. Yet these higher-value propositions often require scale economies and working-capital headroom not always available to niche entrants, dampening topline growth for the Ireland MVNO market.

High Wholesale Access Fees and Unfavourable Data Volume Tiers

Despite ComReg’s efforts, wholesale agreements still embed tier thresholds that penalize sub-scale MVNOs. Capacity bookings below certain gigabyte bands carry surcharges that elevate effective per-gig costs above those enjoyed by carrier-owned brands. Independent players attempting to mirror unlimited data offers thus face margin compression or must impose throttling clauses that dilute perceived value.[3]ComReg, “Retail Mobile Market Quarterly Report Q4-2024,” comreg.ie Complex roaming settlement rules further erode profit when serving data-hungry tourists, unless the MVNO negotiates multilateral roaming hubs—an administrative burden in itself. Unless cost curves fall faster, or shared-MVNE pooling gains traction, smaller brands risk stagnation, forcing strategic reviews, niche repositioning, or acquisition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud-hosted cores captured 74.54% of the Ireland MVNO market share in 2024. Operators leaning on public-cloud VNFs trimmed time-to-market for new tariffs by up to 40% and achieved opex reductions near 18%. The Ireland MVNO market size attributable to cloud deployments is projected to climb at a 7.30% CAGR, buoyed by elastic scaling during seasonal peaks and pay-per-use licensing that aligns cost with subscriber load.

On-premise cores persist among large enterprises and government agencies demanding isolated control planes, red-team audited security, or in-country data residency. However, their share of the Ireland MVNO market is forecast to erode as containerized micro-services, CI/CD pipelines, and infrastructure-as-code toolchains mature. Vodafone’s 2024 link-up with the Gigs platform illustrates how turnkey cloud stacks allow fintechs or device OEMs to spin up white-label mobile offers within weeks, lowering entry barriers and diversifying the MVNO ecosystem.

By Operational Mode: Full MVNOs Lead Through Infrastructure Control

Full MVNOs held 54.22% of revenues in 2024 and are extending that lead with a 15.59% CAGR, chiefly because owning the HLR/HSS, billing, and SIM provisioning unlocks flexible wholesale sourcing and richer service logic. Ireland MVNO market challengers such as Tesco Mobile employ multi-network fall-back, granular usage analytics, and custom loyalty programs that brand-light resellers cannot replicate.

Service-operator models still appeal to utility firms, retailers, or media houses that value branding over telecom wizardry, trading lower capex against dependency on host-MNO portals. Yet over the forecast horizon, the Ireland MVNO market anticipates a migration from simple resell agreements toward progressively deeper control levels, especially as 5G SA slices demand direct policy management and network exposure functions.

By Subscriber Type: Consumer Base Underpins IoT Upside

While consumer SIMs accounted for 76.06% of 2024 revenue, the IoT slice is the genuine outlier, expected to grow at an 18.00% CAGR. Much of today’s household growth revolves around family plan consolidation and streaming-driven data top-ups rather than new line activation. In contrast, industrial demand for embedded connectivity in machinery, smart meters, and connected cars adds lines at scale with predictable monthly payloads.

Enterprise accounts, though numerically smaller, drive healthy ARPU thanks to premium SLA surcharges, bespoke reporting, and field-service support. The Ireland MVNO market thus sees a dual mandate: sustain mass-market consumer value through simplified digital journeys while cultivating specialized IoT stacks—device-life-cycle consoles, eUICC management, and edge analytics—that lock in high-margin corporate spend.

By Application: M2M Connectivity Transforms Service Models

Discount voice-and-data bundles retained 41.14% share in 2024, but Cellular-M2M connections are accelerating at 18.44% CAGR as automotive platforms, asset trackers, and smart-grid nodes proliferate. The Ireland MVNO market size attached to M2M is set to quadruple by 2030 as connected-vehicle eCall mandates, cold-chain monitoring, and predictive-maintenance pilots scale nationwide.

Business-application SIMs for field-force tablets, PoS terminals, and SD-WAN back-up lines fill the mid-tier, yet procurement cycles remain lengthy and heavily service-level driven. Niche “other” uses—from emergency-service paging to maritime telemetry—deliver premium pricing but modest volumes. Across the mix, MVNOs strong in API orchestration, device-cloud connectors, and cybersecurity gain the inside track as M2M goes mainstream in the Ireland MVNO market.

By Network Technology: 5G Adoption Accelerates Infrastructure Investment

4G/LTE accounted for 68.83% of active lines in 2024, but 5G subscriptions are rocketing at 24.90% CAGR. Three Ireland’s 92% population coverage after a EUR 2 billion capex program, coupled with its five-year run as Ireland’s fastest network, cements the MNO as an attractive wholesale partner. The Ireland MVNO market size for 5G is forecast to overtake legacy 3G/2G by 2027, particularly as Vodafone sunsets 3G from October 2024.

Satellite and non-terrestrial networks, though nascent, emerge as complementary overlays for maritime, aviation, and rural use cases requiring ubiquitous reach. MVNO core vendors now bake NTN hooks into PCC and steering engines, signaling longer-term diversification beyond terrestrial radio.

By Distribution Channel: Digital-First Strategies Reduce Operational Costs

Digital-only distribution grabbed 56.67% share in 2024, underlining a consumer pivot to app-based onboarding and eSIM QR activation. Each remote sale shaves gross acquisition cost by an estimated EUR 12 versus full-service retail, giving digitally native brands pricing headroom. The Ireland MVNO market size derived from online sales is increasing at a 6.75% CAGR.

Still, brick-and-mortar shops remain essential for older demographics needing assisted setup or for handset financing prospects wanting physical device trials. Carrier sub-brand kiosks, such as Eir’s GoMo pop-ups, blend experiential marketing with tight OPEX control. Wholesale partnerships handle enterprise resale and M2M kit distribution where project-managed installs are critical. Over the horizon, universal eSIM enablement promises to slash SIM logistics further, though only 27% of 2024 handset shipments supported eSIM by default.

Geography Analysis

Ireland’s compact landmass and unified spectrum policy foster near-homogeneous service availability, placing nationwide footprint within reach of even mid-sized virtual operators under a single wholesale contract. Dublin and Cork generate the lion’s share of data traffic, with population density, office clusters, and 5G small-cell grids spurring ARPU-rich usage. Galway, Limerick, and Waterford collectively account for a growing minority of subscribers, riding tourism growth and university demand for flexible data packs.

Rural districts exhibit lower traffic per cell yet benefit from ComReg’s coverage obligations that require MNOs to extend LTE and 5G beyond profitable corridors. The Ireland MVNO market leverages infrastructure-sharing deals—involving over 6,000 towers now owned by Phoenix Tower International after its EUR 1 billion Cellnex buyout—to meet those mandates without crippling lease costs. Wholesale tower tenancy rates, while creeping upward, still undercut the capex burden of independent macro-builds. Seasonal surges blanket the west coast as foreign visitors flood the Wild Atlantic Way, spiking prepaid and short-duration eSIM demand.

Border counties occupy a special strategic niche. Post-Brexit re-imposition of UK roaming surcharges nudges mainland UK tourists toward Irish prepaid SIMs with EU-wide roaming, producing periodic traffic windfalls each holiday peak. The Ireland MVNO market therefore tunes marketing investment to festival calendars and ferry arrival patterns, stitching together a high-yield, visitor-centric sub-segment.

Enterprise and public-sector procurement concentrates in Dublin’s International Financial Services Centre and Cork’s growing pharma‐tech hub. MVNOs focusing on IoT and private 5G slices cluster local technical teams there, reinforcing a virtuous loop of regional specialization. Yet regulatory parity ensures that even in remote Donegal or Kerry, a new entrant can lawfully access nationwide RAN at industry-standard terms—flattening geographic barriers to competitive entry.

Competitive Landscape

The Ireland MVNO market hosts more than a dozen active brands, yet concentration remains moderate. Tesco Mobile leads at roughly 8% of cellular subscriptions, aided by full-core ownership, supermarket till-top-ups, and persistent loyalty campaigns. Virgin Mobile, Lebara, and Lyca Mobile form the second tier, each staking differentiated ground in quad-play bundles, international calling, or diaspora communities. A third tier consists of service-operators such as An Post Mobile, Clear Mobile, and the freshly launched Sky Mobile, the latter cross-selling to an existing TV base of 800,000 households.

Competition intensified in 2024 as GoMo and 48 rolled out sub-EUR 10 unlimited plans, forcing smaller independents into defensive retention. The resulting price deflation shrank blended ARPU by nearly 5% year on year, yet also widened the affordability window for light-data prepaid users. To preserve margin, leading MVNOs invested in AI-driven care chatbots, network analytics for proactive QoS, and big-data churn propensity models.

Strategically, cloud MVNE platforms such as Plintron and Gigs have lowered entry barriers for non-telecom brands—fintechs, wearables firms, or e-commerce specialists—to embed connectivity inside their service stack. Anticipated entrants include Revolut, which obtained an Irish e-money license in 2024 and is rumored to pilot eSIM travel data packs in 2025. With 5G SA slicing unlocking dedicated enterprise channels, ICT integrators and systems houses may soon field private-slice M-NOIs (mobile network operator of IoT) under wholesale access deals, likely prompting vertical consolidation or partnership models.

Ireland MVNO Industry Leaders

Tesco Mobile Ireland

GoMo

48

Virgin Mobile Ireland

Lycamobile Ireland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Three Ireland’s network ranked fastest nationwide for the fifth straight year, boasting 92% 5G population coverage after EUR 2 billion in upgrades.

- December 2024: UK CMA cleared the Vodafone–Three merger with behavioral remedies, potentially influencing cross-border wholesale and roaming rates.

- October 2024: ComReg confirmed the final switch-off schedule for Vodafone’s 3G network, directing MVNOs to migrate legacy devices.

- September 2024: Sky Mobile launched as Ireland’s eighth MVNO on Vodafone’s radio access, introducing aggressive quad-play incentives.

Ireland MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Ireland MVNO market in 2025?

The sector is valued at USD 200 million in 2025 and is projected to reach USD 240 million by 2030.

What CAGR is forecast for Ireland’s virtual network providers?

The market is expected to grow at 3.98% annually through 2030.

Which operational model is growing fastest?

Full MVNOs are expanding at 15.59% CAGR, outpacing other configurations.

Why are quad-play bundles important to Irish operators?

Bundles let providers offset low-margin mobile plans with higher-margin broadband and TV services, boosting customer lifetime value.

How will 5G influence MVNO opportunities?

5G Stand-Alone enables network slicing and private network resale, creating new enterprise IoT revenue streams for full-MVNOs.

What role does ComReg play in MVNO growth?

ComReg mandates capacity-based wholesale access and monitors fair pricing, allowing independents to launch competitive unlimited-data offers.

Page last updated on: