UAE MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

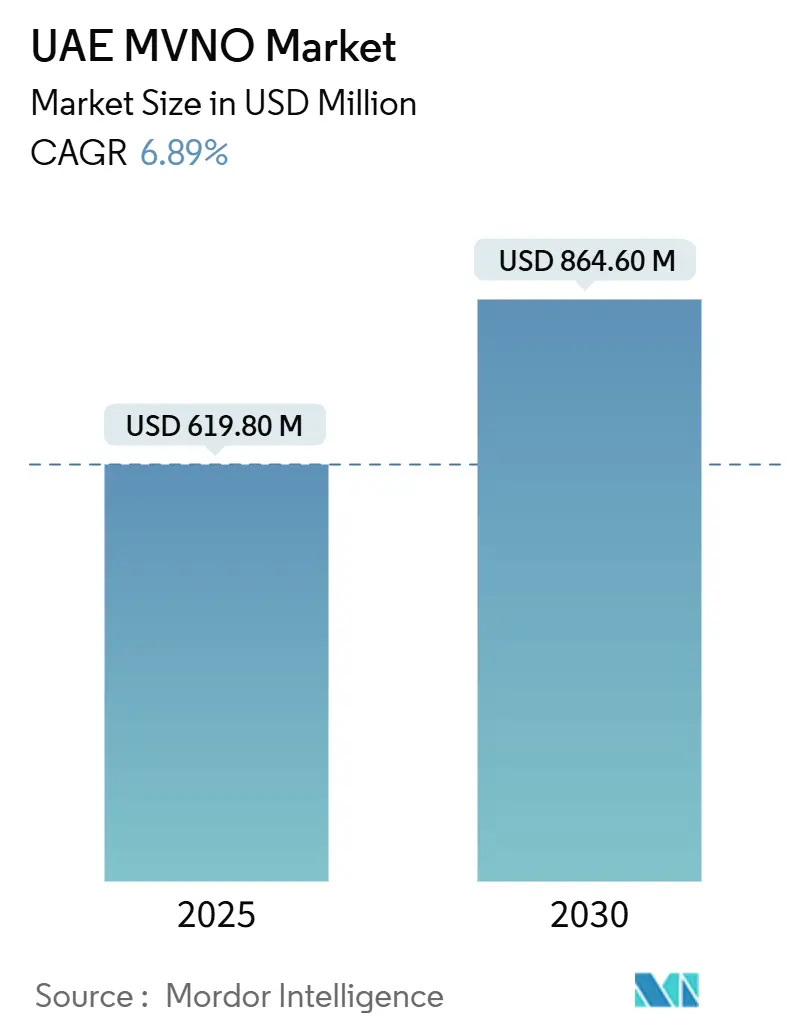

| Market Size (2025) | USD 619.80 Million |

| Market Size (2030) | USD 864.60 Million |

| Growth Rate (2025 - 2030) | 6.89% CAGR |

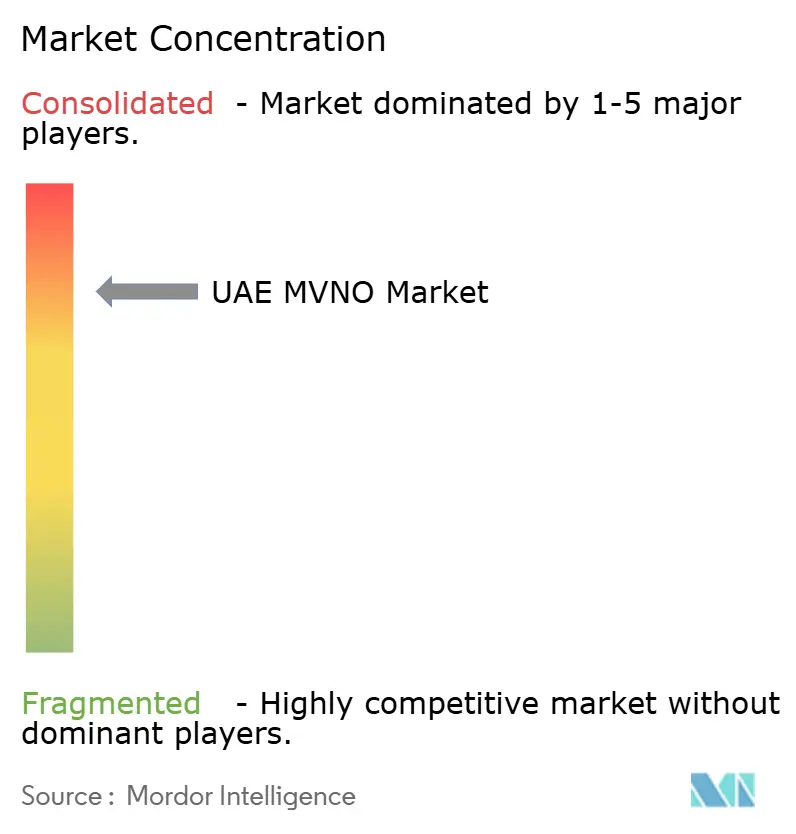

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE MVNO Market Analysis by Mordor Intelligence

The UAE MVNO Market size is estimated at USD 619.80 million in 2025, and is expected to reach USD 864.60 million by 2030, at a CAGR of 6.89% during the forecast period (2025-2030). In terms of market size, the market is expected to grow from 0.77 million subscriber in 2025 to 1.07 million subscriber by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

Strong 5G coverage, network-slicing readiness, and rapid smart-device adoption let virtual operators pivot from basic resale toward full-service models that bundle IoT, eSIM tourism, and fintech features. On-premise deployments still dominate because local data-residency rules favor in-country processing, yet cloud-native MVNO cores are scaling fastest as operators chase lower capex and quicker service launches. Rising enterprise digitization, sustained expatriate inflows, and government licensing reforms are widening the addressable base, while compliance costs and wholesale price rigidity remain notable frictions. Overall, the UAE MVNO market is moving from a volume-driven voice resale play to a service-quality race centered on differentiated customer experiences and vertical expertise.

Key Report Takeaways

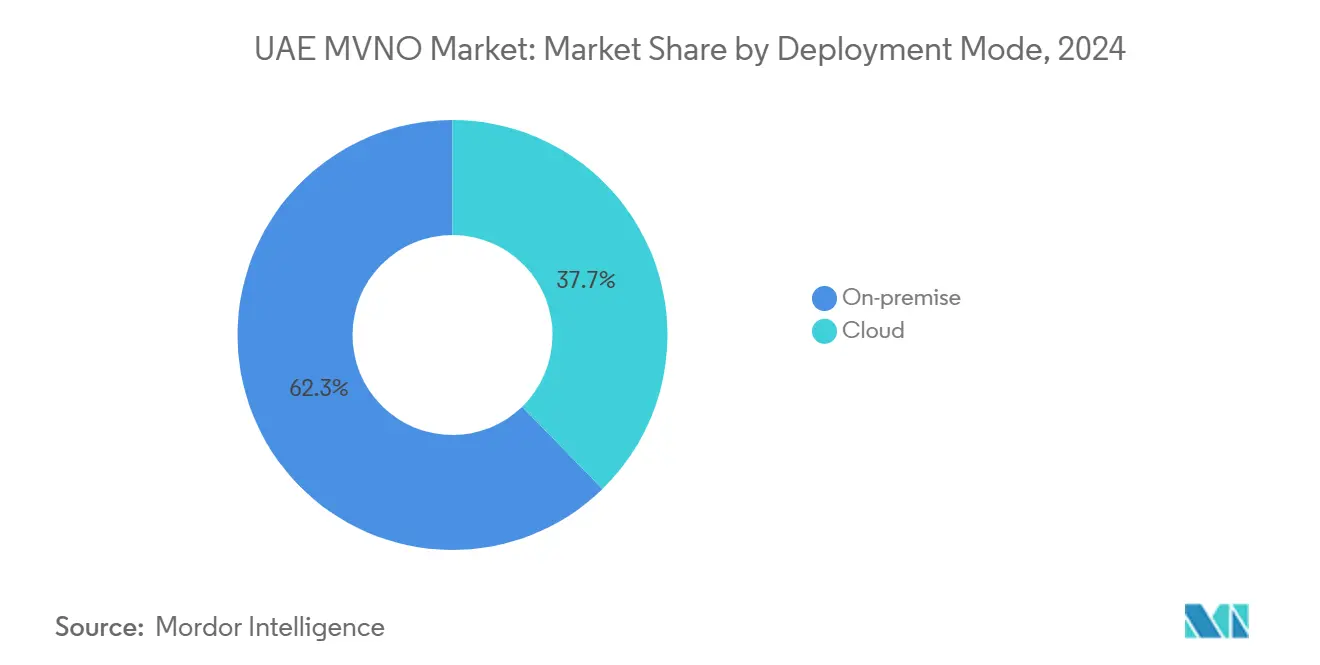

- By deployment model, on-premise infrastructure led with 62.28% UAE MVNO market share in 2024; cloud-based solutions are forecast to expand at a 19.86% CAGR to 2030.

- By operational mode, resellers and light configurations held 55.68% share of the UAE MVNO market size in 2024, while full MVNOs record the strongest projected CAGR at 13.79% through 2030.

- By subscriber type, consumer connections accounted for 74.65% share of the UAE MVNO market size in 2024 and IoT subscriptions are advancing at a 19.86% CAGR through 2030.

- By application, discount services controlled 40.67% UAE MVNO market share in 2024; business-oriented offerings are set for a 15.56% CAGR out to 2030.

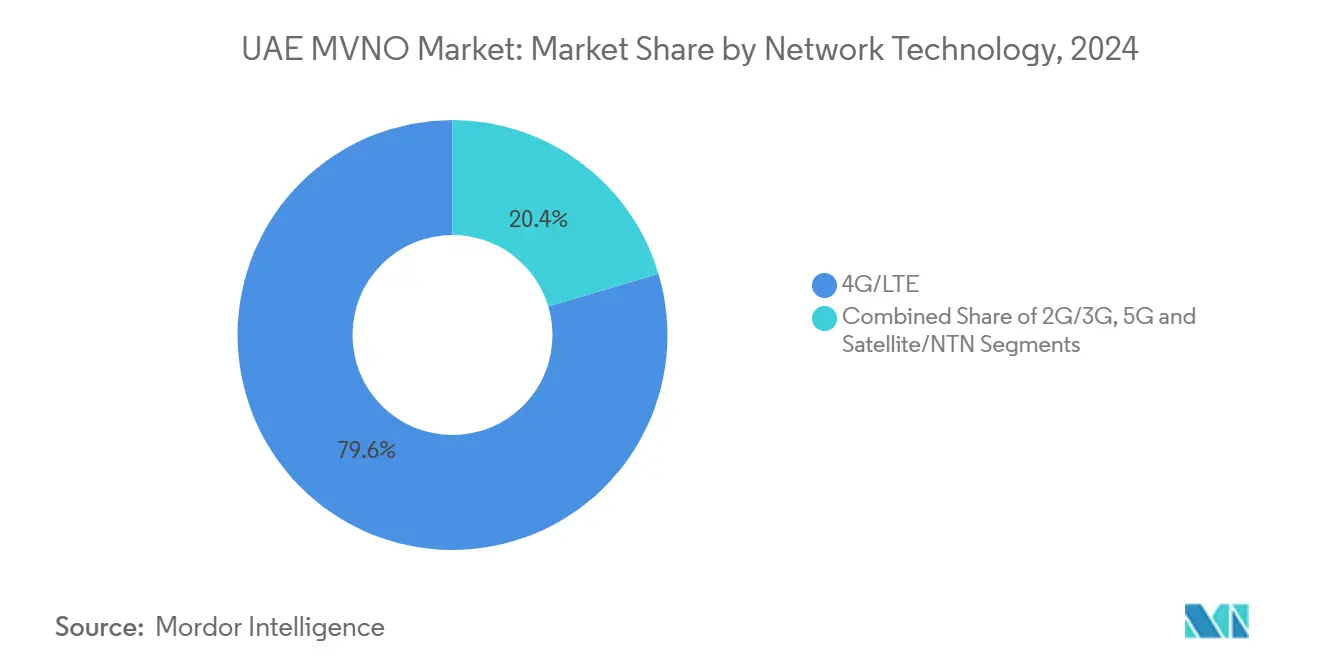

- By network technology, 4G/LTE secured 79.59% share of the UAE MVNO market size in 2024, whereas 5G services are projected to surge at a 33.72% CAGR by 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TDRA licensing reforms | +1.8% | UAE nationwide | Medium term (2-4 years) |

| High smartphone penetration | +1.2% | Dubai & Abu Dhabi | Short term (≤ 2 years) |

| 5G network-slicing wholesale models | +2.1% | Major emirates | Medium term (2-4 years) |

| Expanding expatriate base | +0.9% | Dubai, Sharjah, Abu Dhabi | Long term (≥ 4 years) |

| Tourism-focused eSIM bundles | +0.6% | Tourism hubs | Short term (≤ 2 years) |

| Free-zone IoT corridors | +0.3% | ADNOC, DEWA, KEZAD zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government push for increased competition through TDRA’s MVNO licensing reforms

The Telecommunications and Digital Government Regulatory Authority (TDRA) modernized licensing in 2025, requiring nondiscriminatory wholesale access and codifying network-slicing as an approved resource-sharing method. Newcomers now negotiate clearer service-level terms, gain visibility via TDRA’s public coverage maps, and secure spectrum-agnostic access that removes significant historical hurdles. These rule changes shorten time-to-launch for niche IoT and roaming specialists, provide legal certainty for investors, and expand wholesale bargaining power that was previously held almost exclusively by the duopoly. [1]Telecommunications and Digital Government Regulatory Authority, “Regulatory Framework for MVNOs 2025,” tdra.gov.ae.

High mobile-broadband and smartphone penetration enabling differentiated service plays

Median mobile download speeds reach 451 Mbps, ranking second globally and giving MVNOs confidence to innovate at the application layer rather than invest in network upgrades. Multi-SIM usage surpasses 1.9 active lines per capita, letting consumers adopt a secondary line for specific value-added bundles. Premium handset penetration above 60% supports eSIM uptake, AI-powered support apps, and device-linked fintech, all areas where nimble MVNOs can compete effectively against slower legacy billing systems.

5G network-slicing wholesale models reducing entry barriers for virtual operators

Cloud-native 5G cores rolled out by e& and du expose dynamic slices with guaranteed latency and throughput. March 2025 saw e& partner with Mavenir to automate slice provisioning, confirming wholesale readiness for MVNOs that need enterprise-grade SLAs. Dedicated slices mean virtual operators can serve autonomous transport, industrial robotics, and low-latency gaming without the performance compromises that historically accompanied shared-capacity models. [2]Mavenir, “e& UAE selects Mavenir for cloud-native 5G core,” thefastmode.com

Growing expatriate population demanding affordable international voice and data bundles

Expatriates form 83.5% of residents and routinely communicate across borders, creating perennial demand for tailored voice minutes, data passes, and roaming-lite plans. Conventional bundles from host MNOs often miss cultural nuances, allowing expatriate-focused MVNOs to specialize in language-specific support, time-zone-aware customer service, and prepaid pricing that aligns with home-country norms. Uptake of such offerings drives stable customer acquisition through word-of-mouth within migrant communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Incumbent MNO dominance limiting wholesale pricing flexibility | -1.4% | UAE nationwide | Medium term (2-4 years) |

| Stringent national cyber-security and lawful intercept compliance costs | -0.8% | High on smaller MVNOs | Short term (≤ 2 years) |

| Restricted access to NTN/satellite bandwidth | -0.3% | Remote coverage zones | Long term (≥ 4 years) |

| Online KYC/eKYC verification delays | -0.4% | Digital-first MVNOs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Incumbent MNO dominance limiting wholesale pricing flexibility

e& and du still own every radio-access network in the country, giving them leverage to set minimum traffic commitments and multi-year revenue-share clauses that raise MVNO breakeven thresholds. Retail-wholesale conflict also emerges: each wholesale discount erodes the incumbents’ own postpaid ARPU, incentivizing them to protect margin by curbing headline rate cuts. Smaller MVNOs thus face slim room for price-led disruption, compelling them to focus on niche features rather than aggressive tariff wars.[3]“Etisalat and du Financial Results 2024,” Arab News, arabnews.com

Stringent national cyber-security and lawful-intercept compliance costs

TDRA’s Information Assurance mandates obligate every licensee—not only host networks—to maintain threat-monitoring, incident-response, and lawful-intercept hooks. Building those layers inside a lean MVNO IT stack requires specialist talent and constant audits, turning regulatory adherence into a disproportionately heavy fixed cost. For newcomers lacking scale, compliance outlays can approach core-platform licensing costs, limiting the pool of capital available for marketing and service innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Local control dominates, cloud scales fastest

On-premise configurations captured 62.28% of the UAE MVNO market share in 2024 as both corporate customers and regulators favored domestic data processing for security and sovereignty. Maintaining in-house infrastructure lets virtual operators assure latency-sensitive enterprise apps and align with Information Assurance directives that discourage offshore traffic paths. Nevertheless, capital intensity and slower feature rollouts weigh on profitability.

Cloud deployments, growing at 19.86% CAGR, are reshaping cost curves by shifting spend from hardware to subscription OPEX. Public-cloud MVNE platforms deliver automated provisioning, analytics, and orchestration that shorten service-launch cycles, an essential edge in the UAE MVNO market where consumer tastes pivot quickly around seasonal travel or viral app trends. Hybrid set-ups—local packet gateways married to cloud-hosted BSS—are emerging among scale-up operators balancing compliance and agility.

By Operational Mode: Full MVNOs ascend amid reseller weight

Reseller and light variants collectively held 55.68% share of the UAE MVNO market size in 2024, proving the gateway model remains attractive for brands testing demand before deep technical investment. Yet service-operator and full MVNO constructs are scaling at 13.79% CAGR as players seek richer margins through ownership of core elements such as HLR/HSS, PCRF, and real-time charging.

Full MVNO independence boosts negotiating power when sourcing bulk capacity and unlocks differentiated offers—think dedicated IoT APNs or low-latency gaming slices—difficult to deliver through pure resale. Upgrading, however, demands network-engineering talent, local datacenter space, and separate regulatory audits, creating a two-speed market in which cash-rich challengers widen their moat while thin-cap stack-light brands stay price takers.

By Subscriber Type: Consumers rule, IoT accelerates

Residential users constituted 74.65% of 2024 subscriptions, driven by expatriate-oriented language packs, family bundles, and value-driven prepaid lines that supplement a postpaid SIM from an incumbent. Marketing spend therefore still skews toward mass social-media outreach and retail kiosk tie-ins at airports.

IoT connections, although a modest base, are expanding at 19.86% CAGR, boosted by national smart-city pilots, metering rollouts, and industrial robotics inside free zones. MVNOs equipped with device-management portals and API toolkits can monetize vast sensor fleets whose ARPU is low but connection longevity is high, smoothing revenue volatility that typifies prepaid consumer portfolios. This dynamic exemplifies the UAE MVNO industry’s pivot toward balanced consumer–enterprise revenue mixes.

By Application: Discount legacy bulk, business drives premium

Discount offers grabbed 40.67% UAE MVNO market share in 2024, testifying to price sensitivity among blue-collar expatriates who remit savings and demand frictionless international top-ups. These plans optimize cost via lower wholesale QoS tiers and bulk minute/data pools negotiated annually.

Business-grade packages are on track for 15.56% CAGR as SMEs and corporates migrate from legacy PBX and VPN solutions to mobile-first UCaaS, split billing, and compliance-ready data plans. Such offers often integrate Microsoft Teams voice or secure APN segmentation, commanding premium ARPU that offsets smaller subscriber bases. With 98% UAE enterprise cloud adoption slated by 2026, MVNOs able to bundle security, MDM, and 5G slices will gain share in this lucrative niche.

By Network Technology: LTE rules income, 5G sparks innovation

LTE held 79.59% share of the UAE MVNO market size in 2024; its coverage breadth and mature tariffs make it the workhorse for everyday voice and mobile broadband. MVNOs lean on LTE for predictable wholesale rates, ensuring stable gross-margin planning.

5G, posting a 33.72% CAGR, is less about mass coverage and more about new revenue verticals. Industrial AR, telemedicine, and live 4K multi-camera event streaming rely on 5G’s low latency and slice isolation. March 2025’s Space42-Viasat pact to co-create 5G NTN illustrates how satellite backhaul will extend these slices beyond terrestrial footprints, letting MVNOs court maritime and aviation clients without building separate roaming deals.

By Distribution Channel: Digital-first edges ahead

Digital-only channels amassed 45.09% share in 2024 and should climb further at 12.5% CAGR as UAE PASS and biometrics streamline eKYC. App-centric onboarding halves acquisition cost, supports instant eSIM activation, and powers self-service upsell flows—features that resonate with tech-savvy residents.

Brick-and-mortar remains relevant for device financing, SIM swaps, and high-touch corporate contracts, but overhead is rising. MVNOs are therefore refashioning stores into experience hubs showcasing VR demos or IoT dashboards rather than operating them as pure retail points. This omnichannel recalibration aligns with consumer expectations shaped by the UAE’s broader e-commerce boom, reinforcing the strategic weight of digital property.

Geography Analysis

Dubai and Abu Dhabi collectively generate more than 70% of MVNO revenues, reflecting dense expatriate clusters, tourism inflows surpassing 15 million visitors, and enterprise headquarters concentration. In these emirates, 5G mid-band coverage exceeds 98%, giving virtual operators blanket capacity for high-bandwidth propositions such as unlimited UHD streaming passes and real-time cloud-gaming bundles. The same urban density, however, intensifies competition, prompting providers to differentiate via localized Arabic and South-Asian language customer care and partnerships with ride-hailing apps for on-the-go top-ups.

Northern emirates—including Sharjah and Ras Al Khaimah—deliver cost-sensitive subscriber pools with above-average prepaid churn. MVNOs emphasizing micro-recharge denominations, zero-fee mobile-remittance corridors, and community-store agent networks achieve stronger footholds here. Network-slicing will let them maintain uniform service quality even where backhaul density is lower, proving essential for IoT corridor projects in industrial free zones.

Looking outward, UAE-based operators eye neighboring GCC states for regional roaming extensions. Virgin Mobile’s 2025 Kuwait launch signals a blueprint: leverage UAE core infra, negotiate country-specific IMSIs, and market pan-GCC eSIM roaming packs. Obstacles include divergent spectrum policies and foreign-ownership caps, yet technical parity across 5G SA cores eases interconnect. Success in exporting the UAE MVNO market playbook could unlock multi-country scale benefits, further solidifying domestic operators’ bargaining stance with wholesale partners.

Competitive Landscape

A structural duopoly defines the wholesale supply side: e& posted AED 59.2 billion revenue in 2024 with 15 million domestic lines, while du served 8.2 million mobile subscribers, ensuring both possess scale to dictate wholesale terms. Their strategies embrace MVNO enablement as a hedge against price-erosion in core segments. Example: e& supplies differentiated slices to Virgin Mobile UAE under a revenue-share pact that aligns virtual-operator expansion with host-network utilization growth.

Virgin Mobile UAE’s app-only model and 4.6/5 satisfaction score demonstrate digital experience as a critical moat. Beyond ONE’s 2024 acquisition of FRiENDi Mobile consolidated 4 million customers under one holding, leveraging shared MVNE resources to accelerate product rollouts. Lebara remains the archetype for diaspora-focused plays, refining bundled international minutes and supporting a multilingual call-center to keep churn below 2% monthly.

White-space opportunities persist in vertical IoT, maritime, and oil-field connectivity where incumbent MNOs lack bespoke service layers. New entrants are courting ADNOC and DEWA projects with private-slice offers guaranteeing sub-20 ms latency and on-premise data anchoring. Regulatory clarity on spectrum leasing inside industrial zones further encourages MVNO proposals that were unviable under legacy frameworks. The gradual shift from retail-subscriber acquisition toward ecosystem partnerships reflects the ongoing sophistication of the UAE MVNO market.

UAE MVNO Industry Leaders

Virgin Mobile UAE

Friendi Group

Swyp

Lebara Mobile UAE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Space42 and Viasat partner on a global 5G Non-Terrestrial Network for direct-to-device satellite service.

- March 2025: Mavenir and e& UAE begin multi-year cloud-native 4G/5G core deployment focusing on AI-driven orchestration.

- January 2025: TDRA introduces Service Coverage Interactive Maps for public transparency.

- November 2024: Beyond ONE launches Virgin Connect eSIM roaming across 140+ countries

UAE MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large will mobile virtual network revenues be in the UAE by 2030?

The sector is forecast to reach USD 864.6 million by 2030, reflecting a 6.89% CAGR from 2025.

Which subscriber segment is expanding fastest in UAE MVNO services?

IoT connections are set to grow at 19.86% CAGR on the back of smart-city projects and industrial automation.

What share of UAE MVNO traffic still rides on LTE rather than 5G?

LTE carried 79.59% of virtual-network traffic in 2024, though 5G volumes are accelerating quickly.

Why are compliance costs a challenge for smaller virtual operators?

TDRA Information Assurance rules require each MVNO to run independent security monitoring and lawful-intercept systems, raising fixed overhead.

Which distribution model now captures the largest share of new SIM activations?

Digital-only onboarding leads with 45.09% of activations and is scaling at 12.5% CAGR due to UAE PASS-based eKYC.

Which emirate generates the highest MVNO revenue?

Dubai tops the list thanks to dense expatriate populations, tourist arrivals, and near-universal 5G mid-band coverage.

Page last updated on: