Greece MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

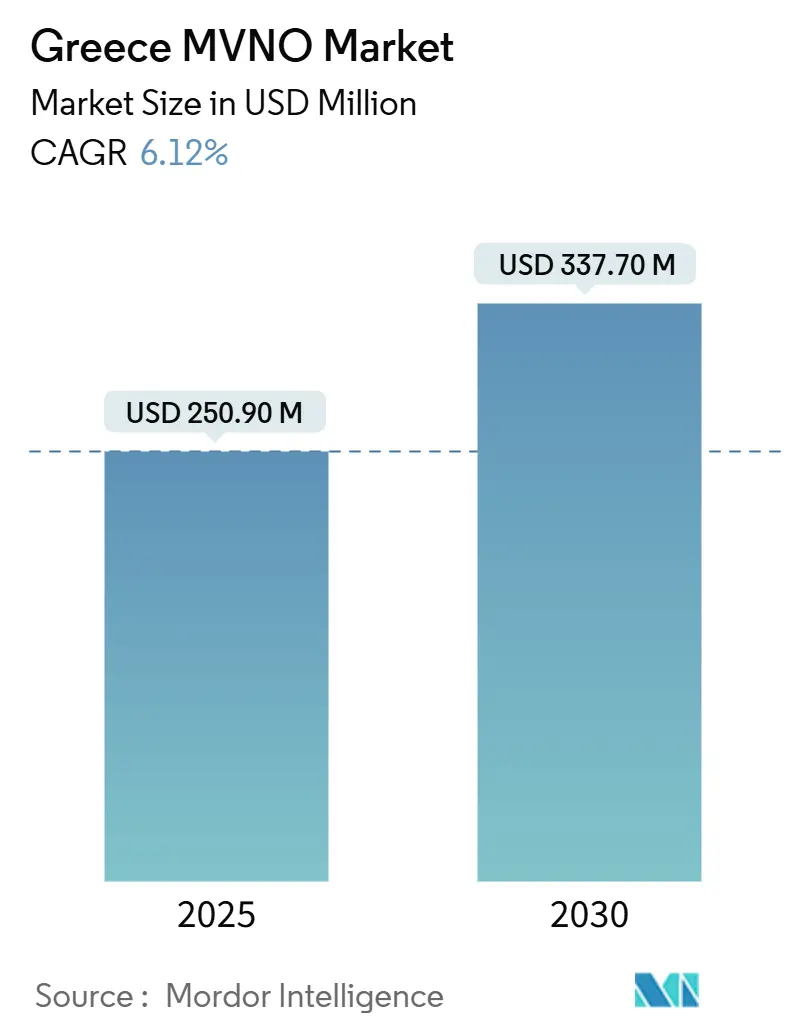

| Base Year Market Size (2025) | USD 250.90 Million |

| Market Size (2025) | USD 250.90 Million |

| Market Size (2030) | USD 337.70 Million |

| Growth Rate (2025 - 2030) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece MVNO Market Analysis by Mordor Intelligence

The Greece MVNO Market size is estimated at USD 250.90 million in 2025, and is expected to reach USD 337.70 million by 2030, at a CAGR of 6.12% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 570.90 thousand subscriber in 2025 to 747.20 thousand subscriber by 2030, at a CAGR of 5.53% during the forecast period (2025-2030).

That growth reflects steady liberalization under EU wholesale‐access rules, the arrival of a fourth network operator in March 2025, and continuing infrastructure investments led by Deutsche Telekom. Cloud-native platforms already dominate deployments, 5G speeds now rank among Europe’s fastest, and digital-only distribution channels capture more than half of new SIM activations. Competitive pressure has intensified as prepaid promotions narrow the historic pricing gap with the rest of Europe, while tourism recovery and digital-nomad visas create seasonal yet high-value demand pockets. At the same time, margin compression from regulated roaming rates and unregulated wholesale fees encourages MVNOs to focus on operational efficiency and service differentiation rather than price alone.

Key Report Takeaways

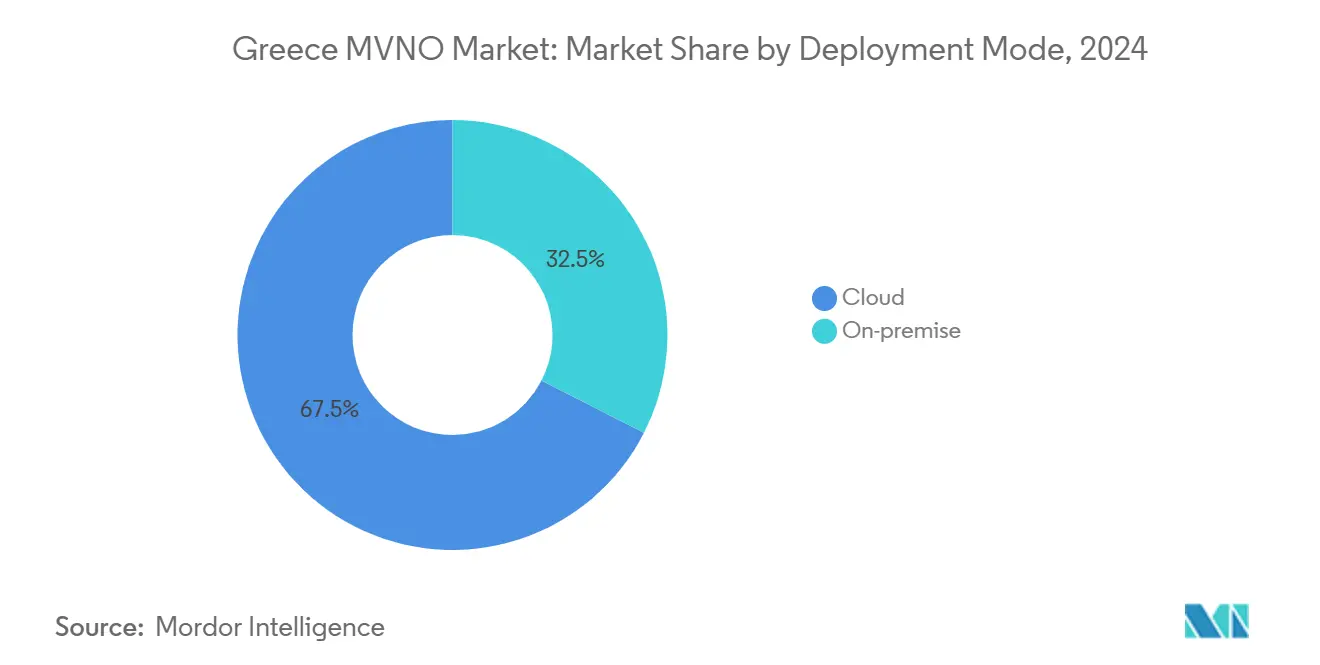

- By deployment model, cloud infrastructure captured 67.48% revenue share in 2024; on-premise solutions are projected to expand at a 10.72% CAGR to 2030.

- By operational mode, reseller/light/brand formats held 72.72% of the Greece MVNO market share in 2024, while full MVNOs recorded the fastest projected CAGR at 29.77% through 2030.

- By subscriber type, consumer lines accounted for 89.41% of the Greece MVNO market size in 2024; IoT-specific subscriptions are forecast to grow at a 36.52% CAGR between 2025-2030.

- By application, discount services led with 49.81% share of the Greece MVNO market size in 2024 and cellular M2M connections are advancing at a 19.00% CAGR through 2030.

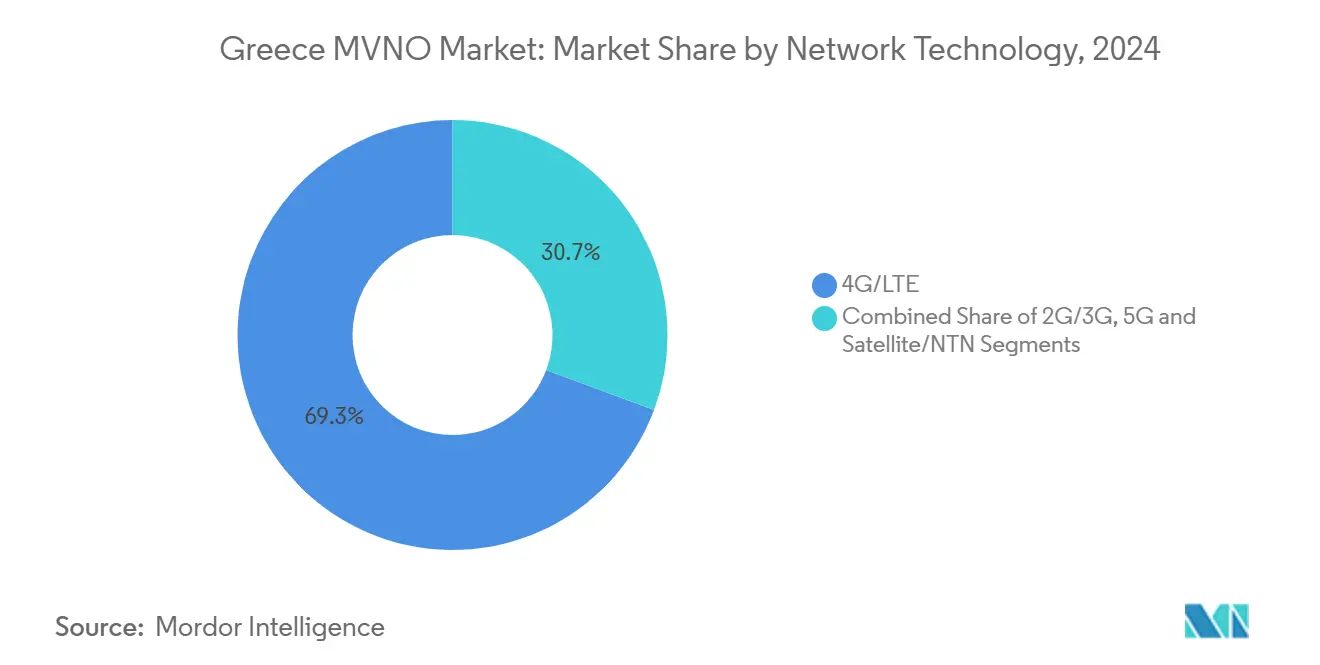

- By network technology, 4G/LTE commanded 69.33% share in 2024; 5G services are projected to expand at a 27.30% CAGR through 2030.

- By distribution channel, digital-only onboarding captured 53.13% revenue share in 2024; third-party wholesale channels are growing at a 10.35% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Greece MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-mandated wholesale access | +1.2% | EU-wide, Greece implementation | Medium term (2-4 years) |

| Price-sensitive youth prepaid demand | +0.8% | Athens, Thessaloniki | Short term (≤ 2 years) |

| 5G & eSIM support digital-only MVNOs | +1.5% | National, urban first | Medium term (2-4 years) |

| Tourism recovery lifts data-only SIM sales | +0.9% | Islands, tourist hubs | Short term (≤ 2 years) |

| Digital-nomad visa lengthens data demand | +0.6% | Athens, Thessaloniki, islands | Long term (≥ 4 years) |

| Maritime/logistics IoT connectivity | +0.4% | Piraeus, Thessaloniki ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Mandated Wholesale Access Keeps Entry Barriers Low

Mandatory access obligations under the European Electronic Communications Code guarantee new entrants the ability to lease radio capacity from incumbent networks without discriminatory terms. [1]European Commission, “Wholesale Access Obligations Under the EECC,” ec.europa.eu Greece’s regulator EETT supplements the mandate with regular tariff benchmarking to curb excessive pricing. The framework encouraged Orizon to start commercial service as an MVNO in 2025 ahead of its own RAN rollout, adding sustainable pressure on the big-3 MNOs. Academic studies conclude that such obligations have not deterred infrastructure investment by host networks, countering long-standing operator concerns. [2]Springer-Verlag, K. Buhk et al., “MVNO Profitability Under Different Access Fee Models,” springer.comFor MVNOs, predictable access terms reduce capital requirements, shorten time-to-market, and support long-term planning, underpinning the Greece MVNO market expansion.

5G and eSIM Adoption Enables Lean, Digital-Only Operations

COSMOTE’s standalone 5G network regularly delivers median downlink speeds above 547.5 Mbps, covering more than 60% of the population by mid-2025. Layered on that footprint, eSIM activation lets MVNOs provision service instantly through mobile apps, removing physical distribution costs. Network slicing allows virtual operators to sell low-latency or high-bandwidth tiers without deploying their own core, while cloud billing platforms scale usage dynamically. These efficiencies translate into lighter cost structures and faster subscriber acquisition, particularly in tourist and IoT niches. As a result, digital-only brands account for over half of new SIMs and drive the Greece MVNO market’s shift from pure price play to service-led competition.

Surge in Inbound Tourism Boosts Short-Term Data Volumes

International arrivals rebounded sharply in 2025, with passenger throughput at Athens International Airport surpassing pre-2020 levels by June. Non-EU visitors cannot exploit “roam-like-at-home” pricing, so they gravitate to local data-only bundles offered by MVNOs at rates from USD 3 to USD 126 depending on duration. eSIM storefronts embedded in travel booking apps push real-time offers upon landing, lowering acquisition cost while increasing average daily usage. Seasonal spikes allow operators to monetize spare network capacity without long-term spectrum commitments. Consequently, data-first tourist plans account for a growing share of prepaid gross additions and reinforce the Greece MVNO market’s diversification beyond domestic consumers.

Digital-Nomad Visa Extends Long-Stay Data Demand

Since its launch, Greece’s digital-nomad visa has issued more than 12,000 permits to remote professionals who typically consume 35-45 GB of data monthly, well above the national average. [3]MDPI, A. Alexandridis, “Maritime Communications Market Trends 2024,” mdpi.com Those users value continuous, high-quality connectivity for work and lifestyle applications and are willing to pay premiums for flexible plans that bundle device insurance, cloud storage, or local banking perks. MVNOs exploit this opportunity by offering subscription tiers with multi-country roaming, dedicated customer support, and optional IoT add-ons for smart accommodation. Long-tenure profiles boost lifetime value and moderate the volatility inherent in tourist flows, adding a stable growth pillar to the Greece MVNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale access fees | -1.8% | National | Short term (≤ 2 years) |

| “Roam-like-at-home” regulation cuts ARPU | -1.1% | EU-wide | Medium term (2-4 years) |

| Scarcity of local MVNE platforms | -0.7% | National | Long term (≥ 4 years) |

| Strong brand loyalty to incumbents | -0.9% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Wholesale Access Fees Compress Margins

Lease rates charged by the big-3 MNOs remain outside direct price regulation, enabling them to preserve a comfortable spread over MVNO retail tariffs. With adjusted EBITDA margins above 40%, host networks can afford aggressive retail promotions that squeeze MVNO pricing headroom. Academic cost-volume models show that full MVNOs need at least 250,000 active lines to break even under current fee structures. These economics push smaller brands to laser-focus on niche audiences or adopt ultra-lean cloud operations. Unless the newly-entered fourth operator pursues a disruptive wholesale strategy, high access fees will continue to cap profitability, tempering the Greece MVNO market’s near-term upside.

EU “Roam-Like-at-Home” Rules Erode Prepaid Revenue

Since mid-2022, all EU residents pay domestic rates when traveling within the bloc, eliminating the premium once associated with international data passes. For Greek MVNOs that historically attracted diaspora and expatriate users through cheap roaming, the regulation has clipped prepaid ARPU by an estimated 11 % year on year. Operators must now craft alternative value propositions—content bundles, OTT partnerships, or vertical IoT solutions—to replace lost roaming income. While the rule enhances consumer welfare and stimulates overall data consumption, it also compresses the revenue mix and prolongs payback periods on customer acquisition spending within the Greece MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Agility

Cloud-hosted cores accounted for 67.48% of the Greece MVNO market in 2024, and that portion is projected to climb in line with a 10.72% CAGR through 2030. Such setups eliminate heavy upfront outlays for switching and billing nodes, enabling entrants to pivot rapidly toward new customer segments. The Greece MVNO market size for cloud-based platforms thus outpaces the on-premise cohort, which still serves security-conscious enterprises and regulated IoT implementations.

Migration to hyperscale data centers also positions MVNOs to integrate AI chatbots, dynamic pricing engines, and real-time analytics without custom hardware. These capabilities shorten issue-resolution cycles and lift NPS scores, reinforcing brand equity. Meanwhile, sovereign-cloud requirements in finance and public sector niches ensure a continued, though slower-growing, role for localized deployments.

By Operational Mode: Full MVNOs Take Control

Reseller/light formats captured 72.72% of 2024 revenue, yet full MVNOs are forecast to grow at 29.77% annually, reflecting the appetite for autonomy over SIM provisioning, BSS stacks, and customer data. Control of the IMS core lets providers craft VoWiFi, private APN, or slice-based offers that are impossible under wholesale branding agreements. The Greece MVNO market share for full operators should therefore expand noticeably as digital-only challengers scale.

Ownership of back-office functions also unlocks margin upside by negotiating multi-host wholesale deals and steering traffic to the lowest-cost network in real time. However, greater capex and regulatory burden elevate break-even thresholds, meaning only brands with clear vertical focus or large distribution ecosystems will migrate fully.

By Subscriber Type: IoT Accelerates Beyond Consumer Dominance

While consumer lines still represented 89.41% of active SIMs in 2024, IoT connections are set to grow 36.52% per year, propelled by Greece’s 17.4% share of global shipping tonnage. Connected-vessel monitoring, livestock tracking, and smart-grid meters add millions of low-ARPU but low-churn devices. Consequently, the Greece MVNO market size for IoT is forecast to overtake small-enterprise voice by 2029.

Enterprise data lines remain attractive given ARPU levels two to three times higher than prepaid consumer, yet growth is steadier at single digits. MVNOs able to bundle analytics dashboards and SLA-backed connectivity will court logistics, retail, and healthcare clients who prize uptime over raw price.

By Application: M2M Surges Past Discount Voice

Discount voice and data packages held 49.81% share of the Greece MVNO market size in 2024 as users sought relief from historically high incumbent tariffs. Nonetheless, cellular M2M solutions are marching ahead at a 19.00% CAGR, underpinned by smart-port pilots in Piraeus and predictive-maintenance rollouts across maritime fleets. The Greece MVNO market share for M2M remains modest but expands steadily as device counts multiply.

Business application bundles—ranging from pooled data for field teams to secure APN services—provide sticky revenue albeit at lower growth rates. Emerging categories like connected-tourism wearables and micro-mobility trackers illustrate how MVNOs convert network slices into differentiated offers rather than pure megabyte packages.

By Network Technology: 5G Reshapes the Competitive Playbook

4G/LTE still accounted for 69.33% of active lines in 2024, yet 5G subscriptions are growing at a 27.30% CAGR. With COSMOTE’s SA core live and both Vodafone and Nova accelerating NSA coverage, wholesale access to 100 MHz of mid-band spectrum lets MVNOs deliver fiber-like speeds. The Greece MVNO market size attributable to 5G therefore broadens beyond urban early adopters into enterprise fixed-wireless and media streaming user bases.

Legacy 2G/3G networks survive chiefly for low-power M2M sensors, while non-terrestrial networks gain traction for blue-water shipping routes. Hybrid SIMs that roam seamlessly between terrestrial 5G and L-band satellite links exemplify the innovation frontier.

By Distribution Channel: Digital Onboarding Becomes the Norm

Online journeys captured 53.13% of 2024 gross additions as ID-verification APIs and eSIM QR codes compressed sign-up time below five minutes. In parallel, the Greece MVNO market is witnessing a 10.35% CAGR in third-party channels, with grocery and energy retailers cross-selling connectivity. Physical stores remain relevant for handset financing and elderly segments uncomfortable with app-only service.

Partnerships with travel aggregators and neo-banks extend reach beyond national borders, while embedded-connectivity offers in IoT hardware add “connectivity as a feature” revenue streams. As KYC regulation evolves toward full digital equivalence, the share of in-app activations is set to exceed 70% before 2030.

Geography Analysis

The domestic Greece MVNO market anchors regional revenue, benefiting from favorable EU policy, improving spectrum efficiency, and Deutsche Telekom’s USD 3.26 billion (EUR 3 billion) capex pledge through 2027. Athens and Thessaloniki concentrate more than 55% of active SIMs, propelled by student populations and enterprise headquarters. Island clusters generate outsized prepaid demand during peak tourism season, allowing MVNOs to monetize dynamic capacity without year-round spectrum costs.

Cross-border EU dynamics influence wholesale terms and roaming traffic. Although the broader European MVNO landscape is maturing, Greece’s historically high retail prices leave room for challenger brands to undercut incumbents while maintaining margin. Regulation harmonizes technical entry requirements, easing future expansion for Greek MVNOs into neighboring Balkan markets.

Global connectivity flows center on maritime corridors where Greek-flagged vessels traverse Suez-to-Rotterdam routes. MVNOs partnering with LEO satellite constellations can bundle shore-to-ship and intra-EU roaming, capturing value that extends Greece MVNO market capabilities into a de-facto international footprint.

Competitive Landscape

The Greece MVNO market hosts a moderately concentrated roster led by Lycamobile, CU, What’s Up, and F2G, collectively controlling slightly more than half of active SIMs. Orizon’s 2025 entry, backed by an existing energy customer base, injects fresh wholesale demand and the promise of bundled utility-telco packages that may unsettle incumbents.

Strategic emphasis is shifting from price-only competition toward vertical specialization. Lycamobile pursues diaspora communities with multi-country bundles, while What’s Up leans on COSMOTE’s 5G slices to offer low-latency gaming add-ons. Newer entrants collaborate with fintechs and travel platforms to blend connectivity with payments and loyalty rewards, raising switching costs.

Wholesale hosts exploit their radio leadership to upsell premium access tiers; COSMOTE positions its standalone architecture as a wholesale differentiator, and Vodafone promotes carrier-grade APIs for IoT MVNOs. Regulatory vigilance by EETT curbs exclusionary tactics, yet sustained margin gaps encourage MVNOs to adopt ultra-lean cost models and focus on under-served niches.

Greece MVNO Industry Leaders

Lycamobile Greece

F2G (Nova/Wind)

Frog Mobile

Taza Mobile

Inter Telecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Orizon launched commercial mobile service as Greece’s fourth operator, starting as a Vodafone-hosted MVNO and targeting 200,000 bundled energy subscribers.

- February 2025: Deutsche Telekom confirmed EUR 3 billion investment for Greece through 2027, prioritizing 5G expansion and fiber backhaul.

- January 2025: EETT began tariff benchmarking with Tarifica to assess wholesale fairness versus five EU peers.

- December 2024: COSMOTE recorded Europe’s fastest 5G median speed at 547.52 Mbps with 60% population coverage.

Greece MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the MVNO opportunity in Greece by 2030?

Total revenue is projected to reach USD 337.7 million by 2030, up from USD 250.9 million in 2025.

Which subscriber segment is growing fastest for Greek MVNOs?

IoT connections are expanding at a 36.52% CAGR through 2030, outpacing consumer and enterprise lines.

What is the primary barrier to profitability for new MVNO entrants in Greece?

Unregulated wholesale access fees charged by the three incumbent MNOs compress margins and raise break-even thresholds.

How does 5G network slicing benefit virtual operators?

It lets MVNOs sell differentiated low-latency or high-bandwidth tiers without deploying their own core network, reducing capital needs while improving service variety.

Why are tourism and digital-nomad visas important to Greek mobile providers?

Seasonal tourists and long-stay remote workers drive high-value data demand, allowing MVNOs to monetize spare capacity with flexible eSIM-based plans.

What is the expected impact of EU roaming rules on prepaid revenues?

“Roam-like-at-home” pricing has cut prepaid ARPU by roughly 11%, forcing operators to seek new value-added services to offset lost roaming income.

Page last updated on: