Singapore MVNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

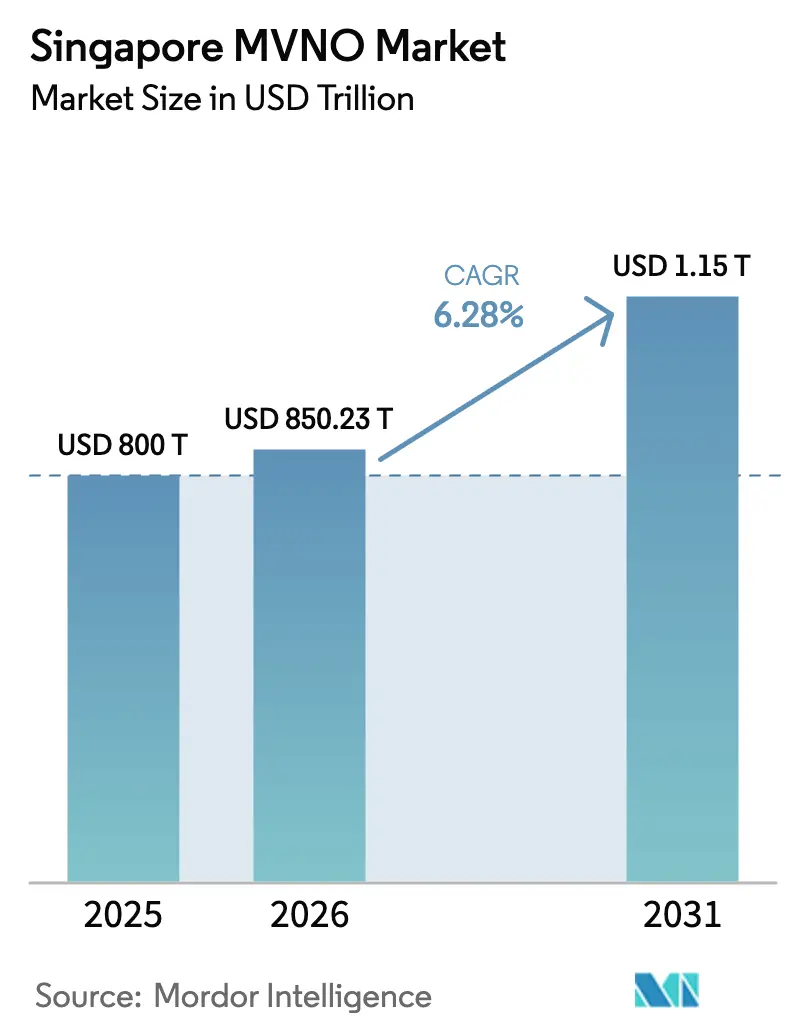

| Base Year Market Size (2025) | USD 800 Billion |

| Market Size (2026) | USD 850.23 Billion |

| Market Size (2031) | USD 1153.47 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore MVNO Market Analysis by Mordor Intelligence

The Singapore MVNO market size is expected to grow from USD 800 million in 2025 to USD 850.23 million in 2026 and is forecast to reach USD 1,153.47 million by 2031 at 6.28% CAGR over 2026-2031.

Intense competition among more than 10 virtual operators and four facilities-based incumbents has driven service innovation, kept data prices low, and encouraged rapid adoption of cloud-native operating models. Nationwide 5G standalone coverage, growing demand for IoT lines in smart-port and smart-city projects, and eSIM-based digital onboarding are widening enterprise revenue pools. At the same time, high wholesale access fees and stringent SIM-registration rules pressure margins, prompting operators to seek profitability through differentiation rather than price alone. Consolidation—most visibly Keppel’s divestment of M1’s telecom unit to Simba Telecom—illustrates the pivot toward scale efficiencies and integrated service portfolios.

Key Report Takeaways

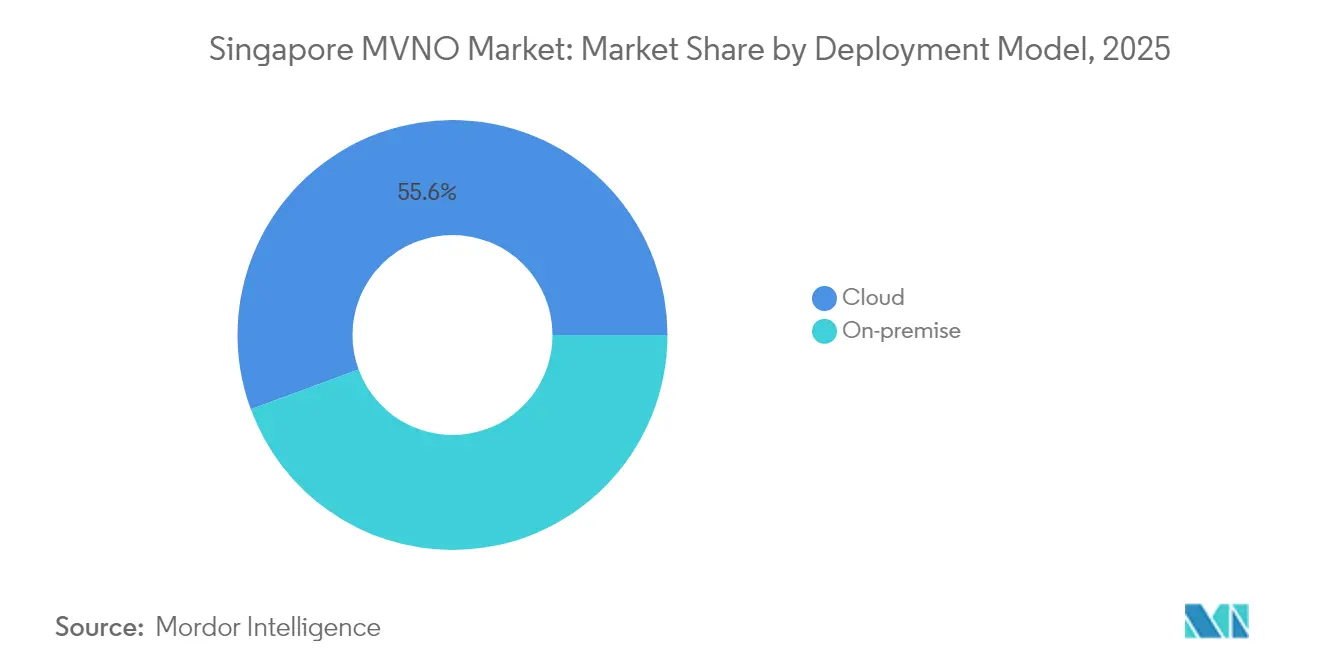

- By deployment model, cloud infrastructure led with 55.62% revenue share in 2025, and it is expanding at a 12.74% CAGR through 2031.

- By operational mode, full MVNOs accounted for a 49.55% Singapore MVNO market share in 2025, while the segment advances at a 10.18% CAGR through 2031.

- By subscriber type, consumer lines held 69.90% of the Singapore MVNO market size in 2025; IoT connections are forecast to climb at a 16.05% CAGR by 2031.

- By application, discount services captured 39.65% share in 2025, whereas cellular M2M lines are progressing at a 15.92% CAGR to 2031.

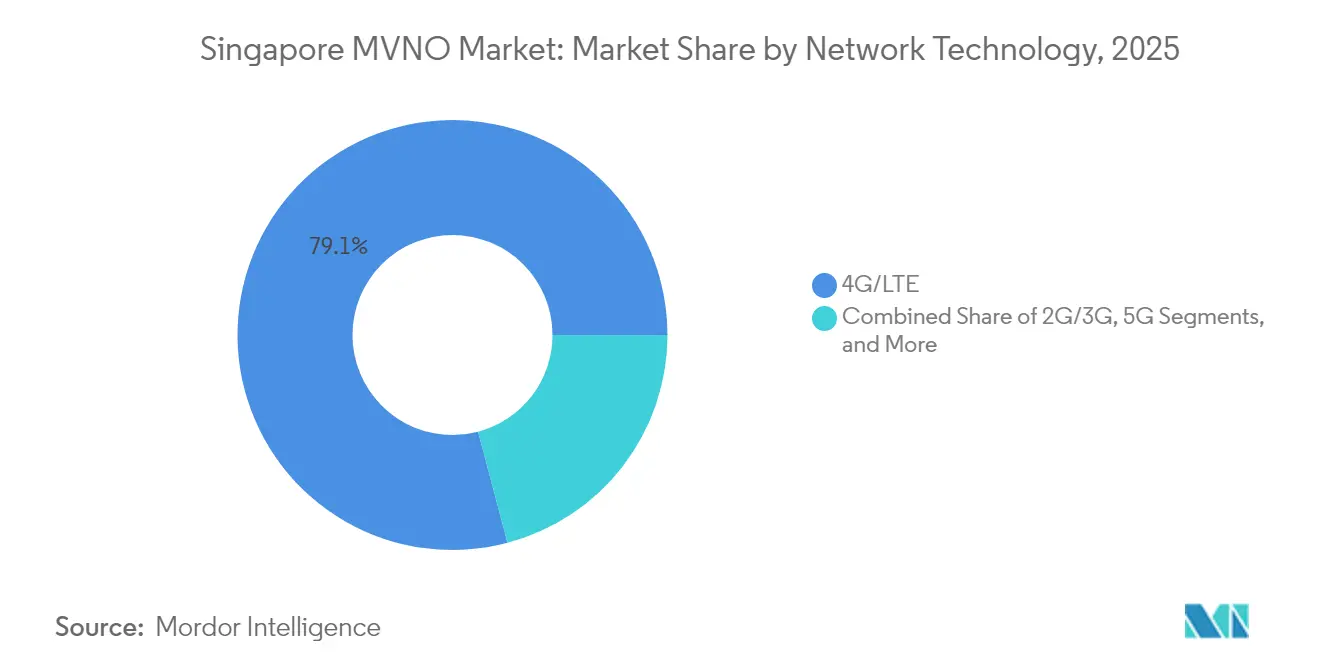

- By network technology, 4G/LTE maintained 79.12% share in 2025, while 5G subscriptions are rising at a 31.15% CAGR during the forecast window.

- By distribution channel, online sales secured 42.48% revenue share in 2025 and are tracking a 13.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Singapore MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G standalone networks enable ultra-low-latency enterprise MVNO services | +1.2% | Central business district and industrial zones | Medium term (2-4 years) |

| E-SIM & fully digital onboarding slash customer-acquisition costs | +0.8% | Nationwide; tech-savvy segments | Short term (≤ 2 years) |

| IMDA spectrum reforms & 3G sunset expand wholesale capacity | +0.6% | Nationwide infrastructure | Long term (≥ 4 years) |

| Influx of expatriate gig-workers drives demand for flexible data plans | +0.4% | Urban employment hubs | Medium term (2-4 years) |

| Port & logistics automation boosts B2B IoT MVNO lines | +0.3% | Western Singapore maritime sector | Long term (≥ 4 years) |

| AI-driven multi-cloud MVNE platforms shorten time-to-market | +0.2% | Nationwide market entry | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G Standalone Networks Enable Ultra-Low-Latency Enterprise MVNO Services

Nationwide 5G standalone coverage, complemented by network slicing, lets virtual operators offer sub-10 ms latency and guaranteed throughput that traditional consumer-grade models cannot match. [1]“Singtel completes 5G network slicing nationwide,” RCR Wireless News, rcrwireless.com Early adopters include logistics firms digitizing Tuas Mega Port operations and financial institutions requiring real-time trading connectivity. Facilities-based carriers expose programmable interfaces, so MVNOs can tailor slices to individual enterprises without duplicating infrastructure. Low-band spectrum at 700 MHz improves indoor penetration by 40%, broadening service availability beyond outdoor hotspots.[2]Allen Lew, “5G+ boosts indoor coverage by 40%,” The Fast Mode, thefastmode.com These technical advantages encourage a shift from price-led consumer segments toward premium enterprise accounts.

E-SIM & Fully Digital Onboarding Slash Customer-Acquisition Costs

Singapore’s eSIM penetration allows virtual brands to issue service profiles instantly, eliminating physical distribution and cutting onboarding expenses by up to 60%. [3]“eSIM onboarding platform cuts acquisition costs,” BeQuick Software, bequick.comDigital-only player GOMO uses Singpass authentication to activate lines in minutes while meeting Know-Your-Customer rules. Funding milestones—such as Airalo’s USD 220 million raise—underline investor confidence in eSIM platforms’ scalability. For IoT fleets, the SGP.32 standard automates global profile swaps, letting device makers ship a single SKU worldwide. Faster, cheaper onboarding uniquely positions MVNOs to pursue narrow demographic or use-case niches at scale.

IMDA Spectrum Reforms & 3G Sunset Expand Wholesale Capacity

The regulator’s coordinated 3G shutdown freed spectrum for 4G and 5G expansion and reduced technical complexity for wholesale interconnect. Parallel investments in a 10 Gbps national fiber backbone support convergence of mobile and fixed services, making triple-play bundles more affordable for smaller brands. Revised allocation rules now permit mmWave leasing for localized private 5G hotspots, a capability prized by factories and event venues. An orderly transition safeguards investment incentives while enlarging the addressable wholesale pool for virtual entrants.

Influx of Expatriate Gig-Workers Drives Demand for Flexible Data Plans

More than 70,500 platform workers—many of them expatriates—prefer month-to-month data packs that flex with variable earnings. MVNOs market large data allowances with roaming and rollover features attractive to gig drivers and freelancers. New CPF contribution rules for platform workers reinforce the need for cost-effective plans that protect take-home pay. Brands targeting the segment rely heavily on digital channels, social media promotions, and community tie-ups to keep acquisition costs low while building loyalty around transparent pricing.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale rates squeeze MVNO ARPU margins | -0.9% | Nationwide | Medium term (2-4 years) |

| Tightening SIM-registration rules raise compliance overheads | -0.3% | Nationwide regulatory requirement | Short term (≤ 2 years) |

| Mobile penetration >175% limits net-new subscriber growth | -0.7% | Nationwide saturation | Long term (≥ 4 years) |

| MNO digital sub-brands cannibalize independent MVNO share | -0.5% | Nationwide competition | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Wholesale Rates Squeeze MVNO ARPU Margins

Despite record data usage, average revenue per user continues to fall, narrowing the spread between wholesale cost and retail price. Facilities-based operators still dictate access fees while competing head-to-head through their own low-cost digital sub-brands, compressing virtual operators’ margins. Successful MVNOs now emphasize premium support, personalized bundles, or enterprise features to lift ARPU rather than chasing volume on razor-thin spreads.

Tightening SIM-Registration Rules Raise Compliance Overheads

The Protection from Scams Act of 2025 imposes steep penalties for fraudulent SIM usage, requiring real-time identity verification and transaction monitoring. MVNOs must invest in advanced fraud analytics and maintain secure API links with national databases, raising fixed costs that weigh heaviest on smaller brands. Although the framework increases consumer trust, it slows fully automated onboarding until systems integration matures, tempering the short-term growth of digital-first entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Architecture Becomes the De-Facto Standard

Cloud-hosted platforms accounted for 55.62% revenue in 2025 and are forecast to grow 12.74% annually, underscoring their role as the engine of digital transformation. Amdocs’ MVNO&GO suite shows how AI-driven charging, customer analytics, and eSIM orchestration can reduce launch cycles from months to mere weeks. Operational savings, scalable capacity, and rapid feature deployment outweigh residual security concerns for most consumer-focused brands. Enterprise-oriented players still favor on-premise stacks to meet sector-specific compliance mandates, but the inclination is shifting as local cloud availability zones secure higher certifications. The Singapore MVNO market size for cloud-based deployments is therefore expanding faster than any other infrastructure category, reinforcing the technology’s strategic centrality.

Second-order impacts include automated disaster recovery, one-click integration with over-the-top partners, and pay-as-you-grow economics that suit smaller entrants. Hybrid models are emerging as transition bridges, permitting sensitive workloads to remain in private data centers while leveraging public clouds for peaks and non-critical functions. Wholesale carriers now bundle cloud BSS with network access, easing entry for niche labels and stimulating further cloud adoption across the Singapore MVNO market.

By Operational Mode: Full MVNOs Translate Control Into Differentiation

Full MVNOs held a 49.55% Singapore MVNO market share in 2025 thanks to their ability to own numbering resources, deploy independent core networks, and craft proprietary user experiences. Their 10.18% CAGR through 2031 reflects a balanced path between capital intensity and service flexibility. Reseller and service-operator models remain useful for brands that value speed over autonomy, especially in limited-duration campaigns or affinity partnerships.

Experience shows that control unlocks innovation: Circles.Life introduced real-time usage gifting, personalized billing, and AI-chat support years ahead of incumbents by virtue of full network access. Yet control carries cost; sustained success depends on lean DevOps, cloud infrastructure, and selective outsourcing. Light or brand MVNOs linked to retail or content ecosystems keep upfront investment minimal, extending mobile services as loyalty tools. Collectively, the operational spectrum lets the Singapore MVNO market cater to diverse strategic objectives while maintaining healthy competitive tension.

By Subscriber Type: IoT Lines Outpace a Maturing Consumer Base

Consumer SIMs still represented 69.90% of revenue in 2025, but growth has flattened under 2% annually as penetration exceeds 175%. In contrast, IoT-only lines are advancing 16.05% each year, reflecting nationwide smart-nation initiatives and industrial digitization. Enterprise mobile-broadband subscriptions occupy the middle ground, propelled by hybrid work and secure-access service edge adoption in regulated sectors.

IoT momentum stems from landmark projects such as Tuas Mega Port automation and municipal environmental sensing, both reliant on low-latency 5G coverage. Wholesale platforms offering unified eSIM orchestration across 200 jurisdictions give Singapore-based MVNOs a competitive gateway into regional IoT deployments. As device counts multiply, the Singapore MVNO market size linked to IoT-specific connections is set to become the primary growth lever over the next decade.

By Application: Discount Plans Dominate, but M2M Use Cases Surge

Discount-oriented offerings captured 39.65% of revenue in 2025 by appealing to price-sensitive consumers through large data buckets and no-contract flexibility. Nevertheless, cellular M2M connections show the steepest climb at 15.92% CAGR, mirroring industrial automation and smart-city buildouts. Business-grade plans command premium pricing by bundling security, priority access, and cloud collaboration tools, though their share remains modest.

Application diversification is widening the Singapore MVNO market. Maritime 5G corridors will enable drone inspection, augmented reality maintenance, and autonomous vessel routing—all dependent on resilient M2M links. Virtual operators that refine vertical-specific propositions are best positioned to escape price erosion in commoditized consumer segments.

By Network Technology: Transition From 4G Dominance to 5G Acceleration

Although 4G/LTE accounted for 79.12% of subscriptions in 2025, 5G is scaling at 31.15% CAGR as device availability broadens and standalone cores mature. The IMDA-supervised 3G sunset completed mid-2024, freeing spectrum for capacity layering and lowering legacy maintenance costs. Non-terrestrial networks, while nascent, are attracting attention for asset tracking and disaster-recovery services that demand ubiquitous coverage.

Nationwide 5G standalone lets MVNOs program quality-of-service parameters per slice, a selling point for mission-critical applications. Opensignal tests rank Singapore first globally in 5G availability and user experience, reinforcing customer willingness to pay a modest premium. Over the forecast horizon, 5G revenue is set to offset inevitable 4G declines, sustaining the aggregate Singapore MVNO market.

By Distribution Channel: Digital-First Engagement Becomes Mainstream

Online channels secured 42.48% of sales in 2025 and are growing 13.98% annually. High smartphone penetration, real-time billing APIs, and eSIM provisioning drive customers toward app-based activation and self-service support. Traditional retail retains value for handset bundling and in-person assistance but faces downsizing as operators optimize cost to serve.

For MVNOs, digital distribution yields granular behavioral data, enabling AI-driven upsell and churn-prevention models. Seamless integration with national digital-ID platform Singpass cuts activation time to under five minutes, proving pivotal in a market where switching barriers are minimal. The Singapore MVNO industry is therefore consolidating acquisition, servicing, and retention workflows inside mobile apps, setting a benchmark for regional peers.

Geography Analysis

Singapore’s city-state structure produces homogenous coverage, yet demand patterns vary by district. Enterprise 5G uptake is strongest in the Central Business District and western industrial corridors, where guaranteed latency underpins automation and high-frequency trading. Residential precincts fuel the bulk of consumer data traffic, prompting operators to densify small-cell grids and deploy in-building repeaters for consistent indoor speeds.

Nationwide fiber backhaul minimizes regional disparity, allowing MVNOs to offer uniform data-heavy plans without network cost surcharges. Sub-1 GHz spectrum ensures seamless transit coverage across MRT tunnels and underground malls, strengthening value propositions for commuters. The Singapore MVNO market has thus evolved into a unified playground for product experimentation; lessons learned locally are quickly exported by ambitious brands.

Regionally, Singapore acts as a telecom launchpad. Circles. Life ported its cloud stack to Taiwan, Australia, and Japan, capitalizing on a blueprint refined in its domestic laboratory. Positioning at the nexus of multiple submarine cables enhances roaming economics, encouraging MVNOs to embed international data packs into core offerings. In sum, geography reinforces scale, quality, and innovation advantages that enhance the market’s global influence.

Competitive Landscape

More than 10 MVNOs jostle with four facilities-based incumbents, resulting in moderate concentration and relentless price pressure. Yet scale efficiencies are emerging: Keppel’s USD 1.43 billion divestment of M1 to Simba Telecom consolidates wholesale bargaining power and accelerates 5G investments. Full MVNO pioneers like Circles. Life sustain 20% higher ARPU than price-led rivals by leveraging AI-powered support and personalized add-ons.

Facilities-based operators hedge against cannibalization by launching digital sub-brands, expanding beyond core voice-data bundles into content and fintech ecosystems. Meanwhile, specialists focus on expatriates, family-sharing plans, or IoT verticals where agility trumps scale. Regulatory neutrality from IMDA levels the playing field, but the rising cost of compliance favors technologically adept entrants. Across the Singapore MVNO market, competitive success hinges on cloud efficiency, data-driven personalization, and strategic partnerships rather than sheer customer volume.

Looking ahead, integration of satellite connectivity, edge computing, and private 5G will open new battlegrounds. Operators primed to bundle heterogeneous access technologies under a single orchestrated platform stand to capture premium enterprise demand. Consequently, the Singapore MVNO industry is transitioning from commoditized retail toward solution-centric value creation.

Singapore MVNO Industry Leaders

Circles.life

GOMO

Zero1

redONE

VIVIFI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Keppel Corporation completed the sale of M1's telecommunications business to Simba Telecom for USD 1.43 billion, opening the door to combined spectrum and infrastructure synergies

- July 2025: eSIM marketplace Airalo secured USD 220 million in Series B funding, attaining unicorn status and signaling strong investor appetite for digital connectivity solutions

- June 2025: Amdocs unveiled MVNO&GO, a SaaS platform that allows virtual operators to launch in weeks using AI-driven digital BSS and eSIM orchestration.

- May 2025: Singtel introduced 5G+ with nationwide network slicing, automatically upgrading 1.5 million users at no extra cost.

Singapore MVNO Market Report Scope

A mobile virtual network operator is a wireless communications service provider that does not own the infrastructure for providing services to its clients.

The Singapore mobile virtual network operator (MVNO) market is segmented by service type (voice, data). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the Singapore MVNO market in 2026?

The Singapore MVNO market size is USD 850.23 million in 2026 with a projected 6.28% CAGR to 2031.

What segment is growing fastest within Singapore MVNO services?

IoT-specific connections are expanding at 16.05% CAGR as smart-city and industrial automation projects scale.

How important is 5G for virtual operators in Singapore?

5G subscriptions are climbing 31.15% per year, enabling network slicing and low-latency enterprise services that differentiate MVNO offerings.

Which deployment model dominates the MVNO landscape?

Cloud-based platforms hold 55.62% share and are growing 12.74% annually due to rapid launch cycles and scalability.

What regulatory change most affects MVNO compliance costs?

The 2025 Protection from Scams Act mandates stringent SIM verification and real-time monitoring, raising operational overhead for all providers.

Are online channels overtaking brick-and-mortar sales?

Yes, digital distribution accounts for 42.48% of subscriptions and is growing 13.98% per year, fueled by eSIM instant activation.

Page last updated on: