Switzerland MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.89 Billion |

| Market Size (2030) | USD 2.40 Billion |

| Growth Rate (2025 - 2030) | 4.95% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland MVNO Market Analysis by Mordor Intelligence

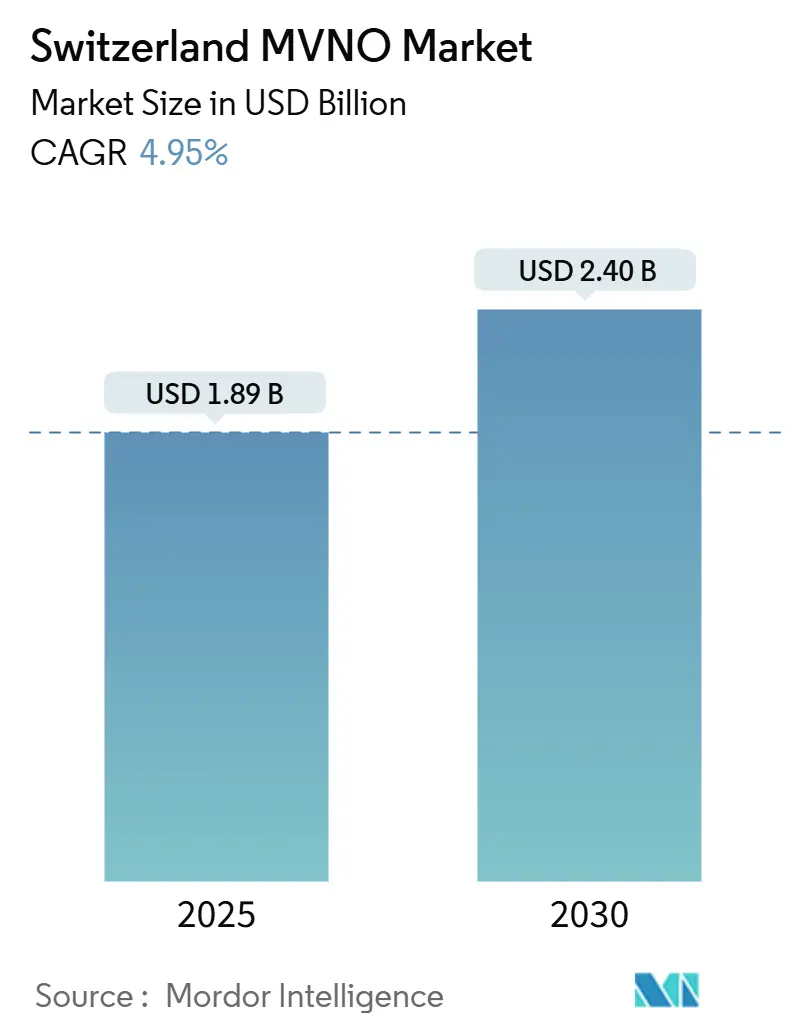

The Switzerland MVNO Market size is estimated at USD 1.89 billion in 2025, and is expected to reach USD 2.40 billion by 2030, at a CAGR of 4.95% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 0.41 million subscriber in 2025 to 0.52 million subscriber by 2030, at a CAGR of 4.57% during the forecast period (2025-2030).

This growth reflects persistent demand for value-driven mobile services, the rapid commercialization of 5G and the migration of operating models from traditional resellers toward cloud-based full MVNO configurations. Operators are capitalizing on Switzerland’s nationwide 5G footprint to launch premium data tiers, while the ongoing squeeze on household spending intensifies subscriber shifts to discount-oriented brands. Competitive positioning hinges on wholesale pricing, digital-only acquisition channels and differentiated eSIM propositions that lower distribution costs. Rising industrial IoT deployments, particularly in connected manufacturing and smart city projects, are opening high-margin enterprise opportunities that reinforce long-term revenue resilience even as consumer ARPU moderates.

Key Report Takeaways

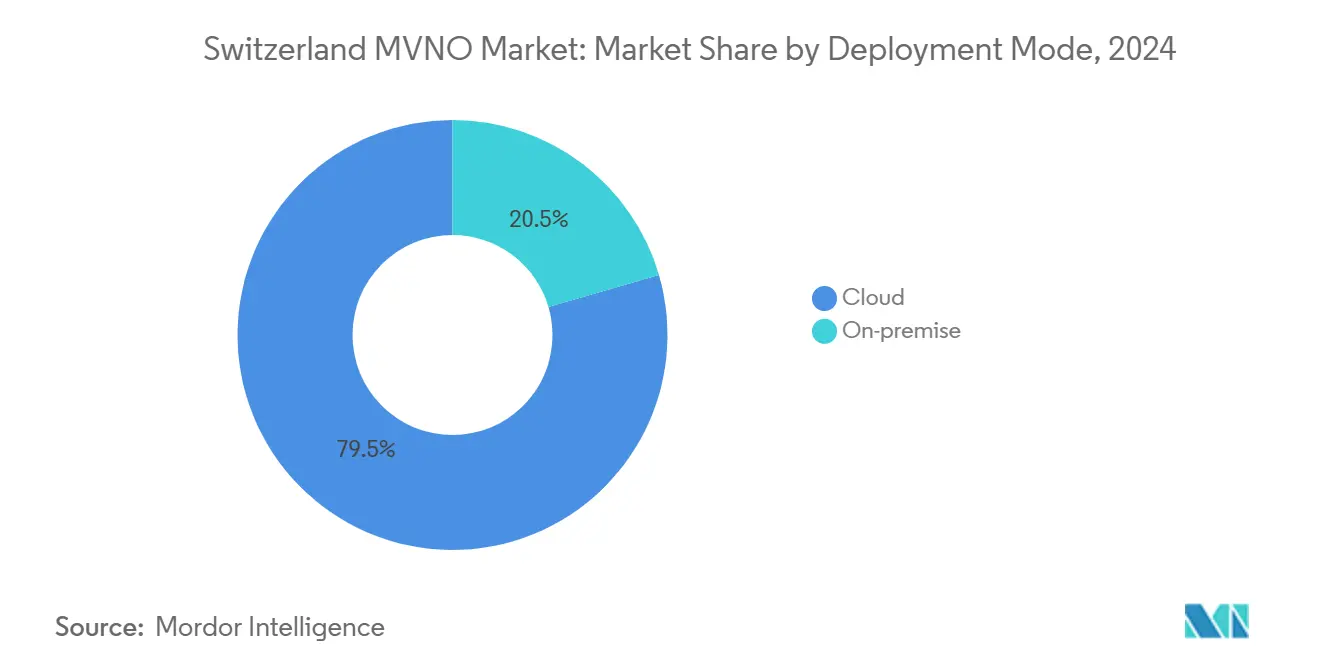

By deployment model, cloud captured 79.5% of Switzerland MVNO market share in 2024; on-premise is projected to grow at a 7.34% CAGR to 2030.

By operational mode, resellers and light MVNOs held 50.79% revenue share in 2024, while full MVNOs are forecast to post the fastest 14.91% CAGR through 2030.

By subscriber type, consumer accounts for 76.55% of Switzerland MVNO market size in 2024 and IoT-specific connections are advancing at a 17.69% CAGR.

By application, discount plans led with 40.14% of Switzerland MVNO market share in 2024; cellular M2M subscriptions are set to accelerate at a 20.40% CAGR by 2030.

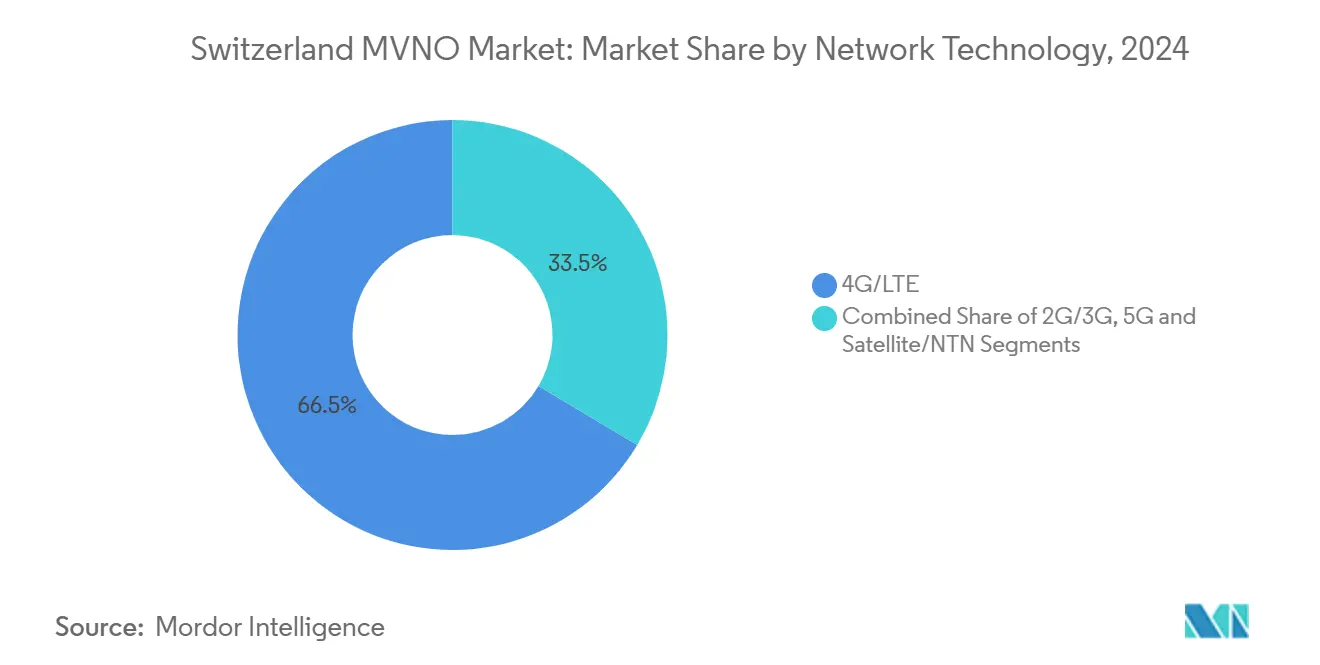

By network technology, 4G/LTE contributed 66.46% of Switzerland MVNO market size in 2024, whereas 5G subscriptions are expanding at a 21.61% CAGR to 2030.

By distribution channel, online and digital-only routes commanded 58.48% revenue share in 2024 and are growing at an 8.74% CAGR over the forecast period.

Switzerland MVNO Market Trends and Insights

Escalating demand for cost-efficient mobile plans amid high living costs

Swiss households allocate a sizeable share of disposable income to telecom services, heightening price sensitivity and fueling subscriber churn toward low-cost MVNO propositions that undercut MNO tariffs by 20–30%. [1]Moneyland GmbH, “Telecom Price Monitor 2025,” moneyland.ch Yallo and Lebara price hikes in early 2025 intensified this migration and enabled digital-first challengers such as Digital Republic to scale unlimited data plans at CHF 13 per month, illustrating how aggressive pricing drives rapid acquisition among 18- to 25-year-olds who value flexibility over legacy customer support. [2]Data Center Dynamics, “Swisscom’s 5G SA Deployment,” datacenterdynamics.com

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating demand for cost-efficient mobile plans amid Switzerland's high cost of living | +1.2% | National, with strongest impact in urban centers like Zurich, Geneva, Basel | Medium term (2-4 years) |

| Growth in migrant and expatriate population boosting demand for ethnic-focused MVNO offerings | +0.8% | National, concentrated in major cities and border regions | Long term (≥ 4 years) |

| Accelerated 5G network rollouts by MNOs enabling premium MVNO service tiers | +1.5% | National, with early deployment in metropolitan areas | Short term (≤ 2 years) |

| Retailer loyalty-data integration with eSIM MVNO propositions | +0.6% | National, led by major retail chains | Medium term (2-4 years) |

| Fintech and digital banking apps embedding white-label MVNO connectivity for PSD2/KYC use cases | +0.4% | National, focused on financial services hubs | Long term (≥ 4 years) |

| Corporate sustainability goals favouring low-carbon, fully-digital MVNO models | +0.5% | National, driven by corporate ESG mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G network rollouts enabling premium MVNO tiers

Swisscom’s 99% population coverage and Sunrise’s nationwide standalone 5G activation allow MVNO partners to negotiate access to network slicing and ultra-low latency features that underpin enterprise IoT, edge analytics and high-definition streaming propositions. [3]Swisscom AG, “Annual Report 2024,” swisscom.ch Full MVNOs now bundle differentiated latency commitments for industrial automation clients and in-car entertainment partnerships, illustrating the leap from basic resale toward value-added connectivity layers.

Growth in migrant and expatriate population boosting ethnic-focused offerings

Lycamobile’s long-running presence on Salt’s infrastructure shows that inexpensive international calling bundles secure strong loyalty inside immigrant communities, which account for one-quarter of the Swiss population. Multilingual support and prepaid flexibility reduce churn and broaden addressable revenue pools as cross-border commuters seek high-value roaming packs.

Retailer loyalty-data integration with eSIM MVNO propositions

Retailers such as Coop and Galaxus extend their loyalty ecosystems by embedding eSIM subscriptions that auto-activate at the point of sale, slashing SIM logistics and unlocking cross-selling of grocery rewards with mobile packages. Access to granular purchase histories lets these brands tailor data allowances to shopper profiles, enhancing retention across both retail and telecom verticals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising wholesale access and interconnect fees compressing MVNO margins | -1.8% | National, affecting all MVNO operators | Short term (≤ 2 years) |

| Planned 2025–26 price hikes across budget sub-brands triggering subscriber churn | -1.1% | National, concentrated in price-sensitive segments | Short term (≤ 2 years) |

| Draft amendments to Swiss Data Protection Act limiting data-driven MVNO marketing | -0.7% | National, with compliance costs varying by operator size | Medium term (2-4 years) |

| Limited IPv6 support on legacy intelligent-network platforms throttling IoT-specific MVNO scale | -0.4% | National, affecting IoT and M2M service providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising wholesale access and interconnect fees compressing margins

Swisscom’s EUR 8 billion acquisition of Vodafone Italia reinforces network-investment payback pressures, prompting MNOs to lift wholesale rates that feed directly into MVNO cost bases. Smaller operators lacking scale struggle to renegotiate favorable terms, increasing the likelihood of market exits or consolidation.

Draft amendments to the Swiss Data Protection Act limiting data-driven marketing

Alignment with stricter GDPR-style consent rules obliges MVNOs to overhaul analytics pipelines and maintain detailed processing logs, inflating compliance overhead—especially for digital-only entrants that differentiate on personalized offers. The uncertainty surrounding cross-border data transfers further complicates expansion plans for ethnic-focused operators with offshore support centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure drives digital transformation

Cloud-hosted platforms generated 79.5% of Switzerland MVNO market size in 2024 and are pacing a 7.34% CAGR to 2030. Most new entrants sidestep legacy core network investment by leasing virtualized BSS and OSS capabilities that scale on demand. Cloud frameworks shorten time to market for promotional tariffs and enable real-time analytics that fine-tune acquisition campaigns. On-premise environments persist mainly among full MVNOs serving regulated verticals such as banking, where data residency mandates favor local processing.

Digitally native brands highlight the agility edge: Galaxus Mobile slashed international package pricing after usage analytics revealed lower data consumption, a change enacted within weeks through cloud-based rating engines. The model’s resilience is underscored by rising energy prices, as public-cloud operators amortize power costs more efficiently than individually hosted MVNO cores.

By Operational Mode: Full MVNOs emerge as growth leaders despite reseller dominance

Reseller and light MVNOs represented 50.79% of Switzerland MVNO market share in 2024, reflecting cost-effective entry pathways that rely on MNO billing stacks. Yet the fastest 14.91% CAGR belongs to full MVNOs that own IMSIs, HLR/HSS elements and steering logic, giving them latitude to design differentiated QoS, bespoke billing cycles and IoT-optimized APNs. Digital Republic exemplifies the transition by evolving from SIM-only resale to a full core that supports pay-as-you-go tiers tailored for gig-economy subscribers. Regulatory clarity and low spectrum barriers accelerate this shift, allowing successful resellers to climb the value chain without prohibitive license fees.

By Subscriber Type: IoT-specific segments drive future growth despite consumer dominance

Consumer subscriptions still command 76.55% of Switzerland MVNO market size, but enterprise digitalization pivots the spotlight to IoT lines that are forecast to expand 17.69% annually. Industrial groups leverage Swisscom’s LoRaWAN and 5G slicing to connect machinery, meters and vending assets; MVNOs wrap these links with vertical dashboards and predictive maintenance APIs. Enterprise contracts typically bundle thousands of SIMs, lifting average line profitability even when ARPU per unit remains low.

By Application: Cellular M2M adoption accelerates despite discount-plan leadership

Discount plans retain 40.14% revenue share as inflation drives households toward no-frills connectivity. However, M2M lines register a 20.40% CAGR powered by connected vehicle rollouts and smart manufacturing that demand reliable, always-on data. Selecta’s national vending network now uses cellular M2M to monitor stock levels and optimize routes, illustrating tangible ROI that offsets higher per-SIM fees.

By Network Technology: 5G deployments accelerate amid 4G/LTE leadership

4G/LTE supplied 66.46% of subscriptions in 2024, underscoring the continuing relevance of legacy radio layers for nationwide coverage. Sunrise began a 3G sunset in mid-2025, freeing spectrum for 5G; MVNO customers were prompted to adopt VoLTE-capable devices, smoothing the upgrade path. 5G’s 21.61% CAGR is stimulated by handset price declines, enterprise latency requirements and emerging use cases such as cloud gaming.

By Distribution Channel: Digital-only routes lead market transformation

Online acquisition delivered 58.48% of revenue in 2024 and is compounding at 8.74% per year as eSIM removes physical barriers to switching. Yallo, Lebara and new entrants alike exploit automated KYC workflows that activate lines in minutes. Brick-and-mortar retains relevance for device financing and upselling among older demographics, yet even traditional retailers leverage QR code-based eSIM provisioning that marries in-store engagement with digital fulfillment.

Geography Analysis

German-speaking cantons collectively account for the largest Switzerland MVNO market size on the back of dense urbanization in Zurich, Basel and Bern. High purchasing power sustains premium 5G bundles, while a vibrant start-up ecosystem fuels IoT experimentation in manufacturing and fintech. French-speaking regions enjoy strong cross-border synergies with France; MVNOs implement roaming add-ons tailored to commuters between Geneva and neighboring Auvergne-Rhône-Alpes. Italian-speaking Ticino, though smaller, records above-average growth as operators localize offers in Italian and aggregate data buckets for frequent travel to Lombardy.

Switzerland’s extensive rail and road infrastructure links rural mountainous areas where terrestrial coverage challenges open niches for satellite-backhauled MVNO solutions. Government fiber subsidies narrow the urban-rural divide, ensuring customers in cantons such as Valais gain access to similar data speeds as metropolitan peers. Uniform wholesale regulations enforced by ComCom safeguard non-discriminatory network access across all regions, preventing tariff disparities that once hindered smaller cantons.

Positioning as a pan-European financial center attracts expatriate executives who demand multi-country connectivity and prioritize service reliability over headline price. These users underpin premium ARPU tiers and stimulate competition among full MVNOs that can guarantee seamless roaming in EU markets without rate shocks.

Competitive Landscape

Roughly 17 MVNOs vie for share, yielding a moderately fragmented environment where the top five brands collectively hold just under 60% of revenue. Yallo and Lebara leverage early-mover awareness and cross-channel distribution, yet Digital Republic’s digital-only model captures tech-savvy youth. Retail-integrated players such as Coop Mobile and Galaxus Mobile exploit existing shopper relationships to cut acquisition expense by bundling mobile benefits with loyalty points.

Strategic pivots emphasize cloud migration, eSIM and aggressive social media outreach, while network access negotiations grow more complex following Swisscom’s Vodafone Italia purchase that boosts the MNO’s regional bargaining clout. Full MVNO newcomers deploy multi-IMSI profiles to circumvent roaming mark-ups, appealing to border commuters and gig-economy drivers. Regulatory guardrails compel Swisscom, Sunrise and Salt to publish transparent wholesale reference offers, curbing potential abuse of dominant bargaining positions and preserving room for niche entrants.

Convergence between banking, retail and telecom intensifies: fintech apps now embed white-label SIMs for instant KYC verification, and energy utilities pilot smart-meter bundles backed by MVNO platforms. Sustainability credentials also shape differentiation, with certain operators issuing carbon-neutral SIM kits and pledging renewable energy hosting for core nodes to attract ESG-minded enterprises.

Switzerland MVNO Industry Leaders

Coop Mobile

M-Budget Mobile

Yallo

Lebara

Galaxus Mobile

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Wingo introduced CHF 1 price increases on all mobile tiers yet extended 5G access up to 300 Mbps to every user, citing 50% energy cost inflation since 2021.

- June 2025: Sunrise began shutting down its 3G network, instructing customers to migrate to VoLTE-ready devices to maintain service continuity.

- May 2025: Galaxus Mobile lowered its International plan from CHF 39 to CHF 29 and Basic from CHF 14 to CHF 12 after analyzing lower-than-forecast data usage patterns.

- March 2025: Galaxus launched 10 Gbps fiber broadband at CHF 39 with no minimum term, challenging incumbent fixed-line operators.

Switzerland MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the projected revenue for the Switzerland MVNO market in 2030?

The Switzerland MVNO market is forecast to reach USD 2.40 billion by 2030 based on a 4.95% CAGR.

Which deployment model leads MVNO operations in Switzerland?

Cloud platforms dominate with 79.5% revenue share due to faster service launches and lower capital outlay.

Which network technology is growing fastest among Swiss MVNOs?

5G connections are expanding at a 21.61% CAGR as nationwide standalone coverage becomes available.

What subscriber segment offers the highest growth potential?

IoT-specific lines, particularly cellular M2M, are growing at 17.69% annually as industries digitalize.

How are wholesale cost changes affecting Swiss MVNOs?

Rising access and interconnect fees are compressing margins, pushing smaller players toward operational consolidation.

Which channels account for most new MVNO customer acquisitions?

Online and digital-only routes drive 58.48% of sales, aided by eSIM that enables instant self-activation.

Page last updated on: