Ireland Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

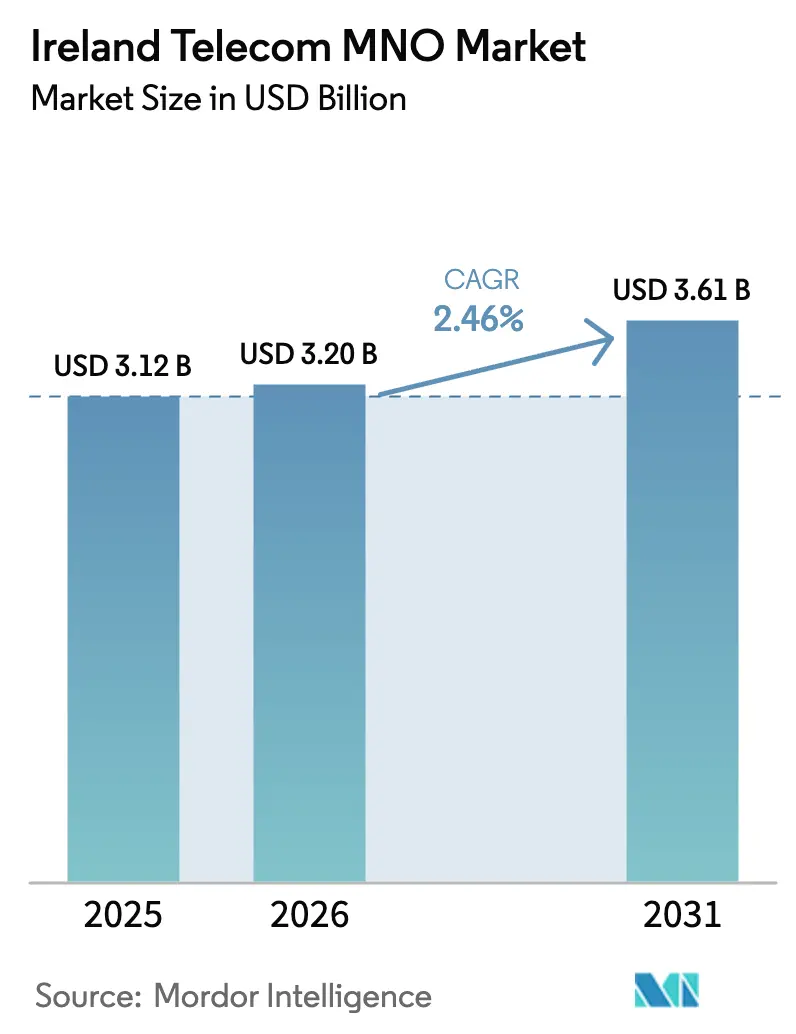

| Base Year Market Size (2025) | USD 3.12 Billion |

| Market Size (2026) | USD 3.2 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 2.46% CAGR |

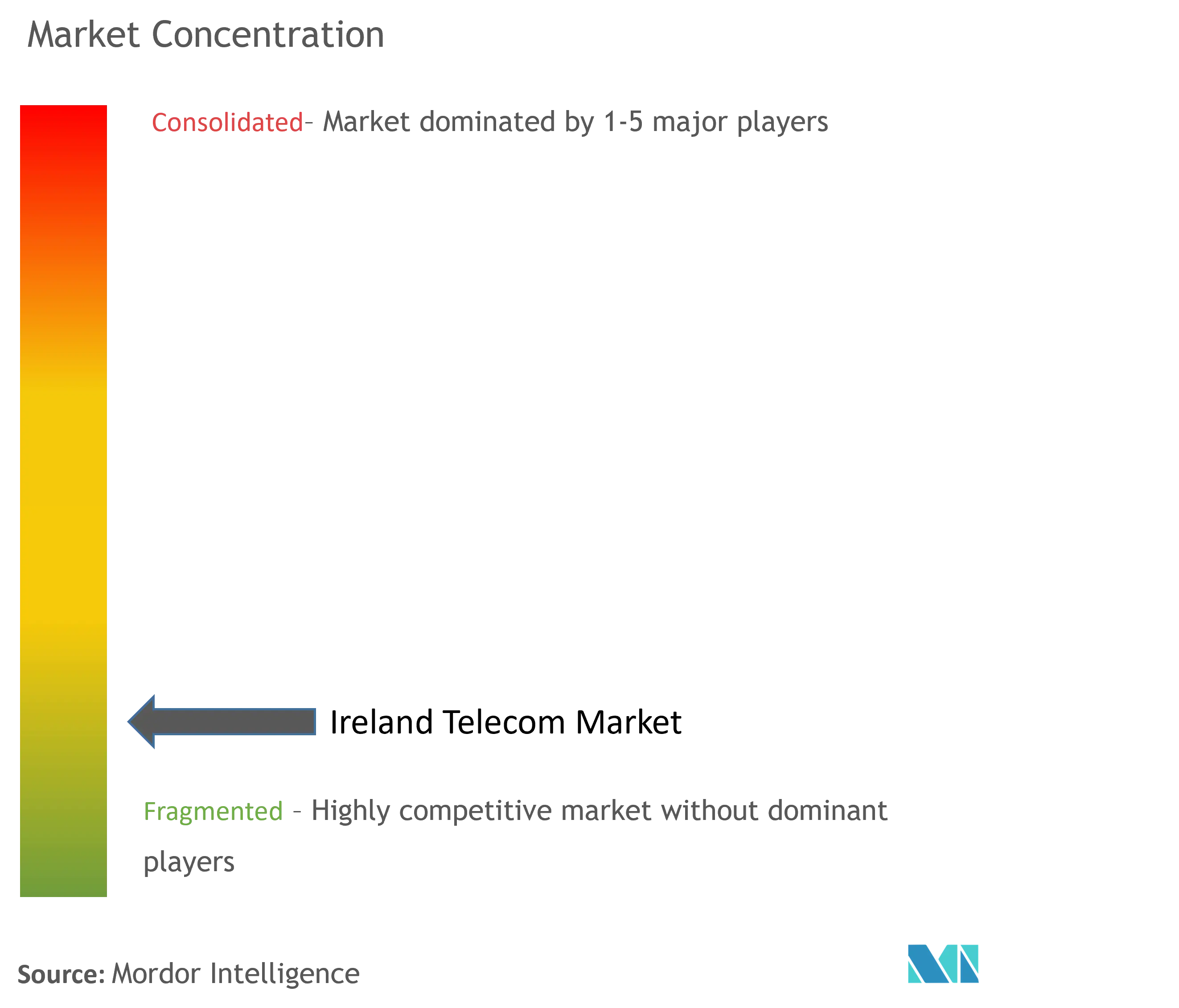

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Telecom MNO Market Analysis by Mordor Intelligence

The Ireland Telecom MNO Market size was valued at USD 3.12 billion in 2025 and estimated to grow from USD 3.2 billion in 2026 to reach USD 3.61 billion by 2031, at a CAGR of 2.46% during the forecast period (2026-2031).

Intensifying price competition, mature voice revenues, and the steady shift of messaging traffic to over-the-top applications explain the modest growth rate. Even so, the Ireland telecom MNO market continues to pivot toward data-centric growth as 5G coverage expands, while wholesale back-haul leasing tied to the National Broadband Plan opens fresh revenue channels. Enterprise digitization, especially software-defined wide-area networking and multi-cloud connectivity, further cushions topline pressure. Consolidation among tower owners and vendor R&D commitments underline the long-term infrastructure outlook.

Key Report Takeaways

- By service type, data and internet services held 52.67% of the Ireland telecom MNO market share in 2025, whereas IoT and M2M services are projected to register the fastest 2.67% CAGR through 2031.

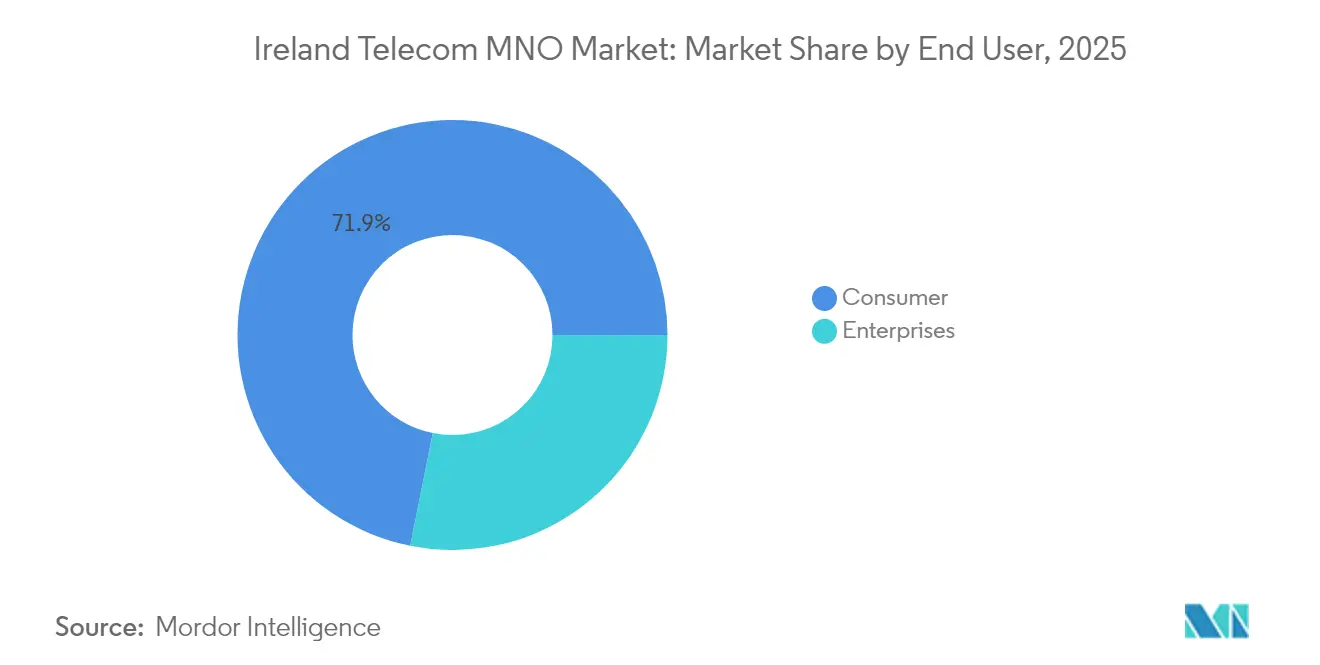

- By end user, consumer services accounted for 71.85% of the Ireland telecom MNO market size in 2025, while the enterprise segment is anticipated to expand at a 2.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ireland Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G stand-alone roll-out catalyzing FWA demand | +0.8% | National, early urban gains | Medium term (2-4 years) |

| EU Digital Decade targets driving fibre subsidies | +0.6% | National, rural focus | Long term (≥ 4 years) |

| Enterprise shift toward SD-WAN and multi-cloud connectivity | +0.5% | Dublin & Cork | Short term (≤ 2 years) |

| New MVNO entrants leveraging eSIM for niche segments | +0.3% | Nationwide | Medium term (2-4 years) |

| National Broadband Plan back-haul leasing revenues | +0.4% | Rural 540,000 premises | Long term (≥ 4 years) |

| Early 6 GHz spectrum refarming for Wi-Fi 7 off-load | +0.2% | Urban enterprise zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Stand-Alone Roll-out Catalyzing FWA Demand

Three Ireland introduced 5G stand-alone service with Ericsson, creating a performance head-start that supports low-latency slices for fixed-wireless access in underserved pockets. Early corporate trials confirm latency gains below 10 ms and throughput peaks above 1 Gbps, signaling commercial potential beyond mobile broadband.[1]Fierce Wireless Staff, “Three Ireland activates standalone 5G core,” fiercewireless.com Eir registered a 130% jump in 5G traffic in 2024, illustrating latent demand once coverage broadens. Yet national 5G availability sits at 9.2% connection time, underscoring room for coverage-driven upside. Fixed-wireless economics are particularly favorable in sparsely populated counties where fiber trenching remains cost-prohibitive. As spectrum refarming and tower-sharing agreements accelerate, the Ireland telecom MNO market is well-positioned to monetize suburban and rural FWA in the medium term.

EU Digital Decade Targets Driving Fibre Subsidies

Ireland committed to gigabit connectivity for all households by 2028 and population-wide 5G by 2030 under the Digital Ireland framework. [2]European Commission, “Ireland’s Recovery and Resilience Plan,” europeancommission.europa.euA EUR 19 million Recovery and Resilience Plan allocation offsets rural build-costs, while the upcoming Gigabit Infrastructure Act streamlines permits. Eir has already reached 70% of its 1.9 million FTTP objective and boasts a 37% take-up rate—the highest in the market [3] Silicon Republic, “Eir hits 70 % of 1.9 million FTTP build,” siliconrepublic.comProgress in the National Broadband Plan enables MNOs to lease finished fiber back-haul, reducing capex and shortening payback periods.

Enterprise Shift Toward SD-WAN and Multi-Cloud Connectivity

Corporate connectivity spend continues to outpace GDP growth as hybrid work, zero-trust security, and cloud migration reshape ICT budgets. Telcos now capture around 27% of enterprise technology outlays that extend beyond pure connectivity. Acquisitions such as IP Telecom’s purchase of Centrecom reveal operators’ intent to deepen managed-service portfolios. McKinsey expects enterprise core connectivity to remain the largest B2B adjacency through 2028, rewarding carriers that package SD-WAN with private 5G and edge compute. Consequently, the enterprise contribution to the Ireland telecom MNO market is forecast to climb from 21% in 2025 to 29% by 2027.

New MVNO Entrants Leveraging eSIM for Niche Segments

Sky Mobile’s September 2024 debut illustrates renewed MVNO momentum. Its EUR 15 “Price for Life” plan exploits Vodafone’s network and eSIM provisioning to target cost-conscious families. Regulatory analysis by ComReg highlights wholesale rate asymmetries that still compress MVNO margins, especially in unlimited data tiers. Even so, eSIM flexibility lowers onboarding friction and supports enterprise fleet-management offers where MVNOs can overlay value-added analytics. With 70% of Irish enterprises expected to adopt cellular IoT by 2028, specialized MVNOs represent a modest but positive tailwind for the Ireland telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale access fees restricting MVNO margins | –0.7% | Nationwide | Short term (≤ 2 years) |

| Fibre build-out delays due to wayleave disputes | –0.5% | Rural planning zones | Medium term (2-4 years) |

| Stagnant voice ARPU amid OTT substitution | –0.9% | All segments | Long term (≥ 4 years) |

| Low rural population density inflating 5G ROI timelines | –0.6% | 25% of territory | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Wholesale Access Fees Restricting MVNO Margins

The 2014 O2–Three merger concentrated network assets in three incumbent hands, and mandated but capacity-capped MVNO access has done little to rebalance pricing power. ComReg studies show wholesale data rates that exceed several EU peers, limiting entrant viability in unlimited data plans. Virgin Mobile exited the segment in 2024, echoing earlier retreats by iD Mobile. Sub-brands such as GoMo and 48 further complicate pricing discipline, eroding room for MVNO differentiation. Unless the upcoming EU cost-model update delivers tangible wholesale relief, MVNO contribution to the Ireland telecom MNO market will stay short of full competitive potential.

Fibre Build-out Delays Due to Wayleave Disputes

Permitting and wayleave negotiations frequently push rural fiber timelines beyond two years. Landowner objections and visual-impact concerns forced multiple reroutes in counties Mayo and Donegal, inflating per-premise cost above EUR 7,000. Overhead alternatives face planning objections, whereas micro-duct solutions raise civil-works outlays. Although the Gigabit Infrastructure Act promises one-stop permitting, implementation lag keeps near-term roll-outs exposed to legal delays. Prolonged fiber deployment slows 5G fronthaul availability, lengthening return-on-investment horizons for the Ireland telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Dominance Amid IoT Acceleratio

Data and internet services controlled 52.67% of the Ireland telecom MNO market share in 2025, reflecting consumers’ pivot to video streaming, remote work, and cloud gaming. Operators recorded double-digit traffic growth, with Eir citing an 80% surge in mobile data since 2020. Voice and SMS revenue continued to erode in parallel as WhatsApp and Teams cannibalized legacy traffic. IoT and M2M connections, while still a small base, are projected to post a 2.67% CAGR to 2031—the swiftest among service lines—supported by LTE-M and 5G NR-RedCap commercialization. The Ireland telecom MNO market therefore leans increasingly on data monetization and machine connectivity to offset voice decline.

The outlook suggests IoT economic contribution could rise fourfold by 2030 as enterprises digitize supply chains. eSIM capabilities enable frictionless device provisioning across Vodafone, Three, and Eir footprints, trimming truck-roll costs. Carriers that bundle connectivity with device management and analytics will capture incremental margin. However, sustained pricing pressure in consumer unlimited data plans means ARPU uplift hinges on differentiated service tiers such as low-latency gaming passes or zero-rating for select streaming platforms.

By End User: Consumer Resilience Versus Enterprise Growth

Consumer accounts delivered 71.85% of the Ireland telecom MNO market size in 2025, underscoring their enduring weight despite a maturing subscriber base. Inflation-indexed tariffs introduced by operators during 2023 and 2024 partially preserved revenue even as churn in low-income cohorts ticked up. Meanwhile, enterprise revenue is on track for a 2.76% CAGR through 2031 as businesses adopt SD-WAN, secure access service edge (SASE), and private 5G. Three Ireland has earmarked EUR 1.1 billion for network modernization that explicitly targets large corporate accounts.

Growing demand for edge compute to support AI workloads is set to amplify corporate bandwidth needs. Analysts forecast that by 2026, 90% of Irish enterprises will integrate generative AI models into operational processes, increasing the criticality of low-latency links. On the consumer side, fixed-mobile convergence packages are gaining traction, aiding retention. Nevertheless, competitive dynamics imply that enterprise digital solutions represent the more lucrative upsell path, giving carriers a hedge against declining consumer ARPU.

Geography Analysis

Urban concentration favors network economics, with Dublin, Cork, and Galway delivering higher utilization and faster 5G time-on-network. Eir now reaches 70% population coverage with 5G, and Three targets 75% by year-end, whereas rural 5G availability averages below 10% connection time. The Ireland telecom MNO market therefore records disparate regional performance as capacity investments prioritize metropolitan corridors.

Rural deployment depends heavily on the National Broadband Plan’s fiber backbone, which aims to pass 540,000 premises by 2026. Wholesale back-haul leases give MNOs economical access to gigabit links, although wayleave delays have kept live connections at only 75,000 so far. Vodafone’s Open RAN pilot across 30 rural sites serves roughly 45,000 customers and demonstrates a lower-cost coverage model. As EU subsidies unlock and tower-sharing expands, MNOs are expected to close the urban–rural gap over the long term.

Spectrum strategy varies by geography. Low-band 700 MHz is the primary rural coverage layer, while mid-band 3.6 GHz clusters in dense suburbs for capacity. Refarming of 6 GHz for Wi-Fi 7 could off-load indoor traffic in business districts, freeing licensed spectrum for mobility. Together, these measures underpin a gradual flattening of regional performance disparities, though returns will manifest mainly beyond 2027.

Competitive Landscape

The Ireland telecom MNO market is an oligopoly anchored by Eir, Vodafone Ireland, and Three Ireland. Combined, the trio controls nearly every macro site, creating high barriers to entry for pure-play network challengers. Three leads on subscriber share at 48.7% following aggressive SIM-only promotions. Eir tops 5G availability at 74%, while Vodafone dominates fiber footprints with 1.7 million homes passed.

Competition has shifted toward value-enhancing bundles rather than headline price cuts. Examples include Vodafone’s unlimited data plus TV streaming add-ons and Eir’s fixed-mobile convergence discounts. Regulatory scrutiny has grown, with ComReg urging a ban on automatic inflation-linked price escalators deemed harmful to consumers. The Ireland telecom MNO industry also witnesses infrastructure realignment: Phoenix Tower’s EUR 971 million purchase of Cellnex assets consolidates passive infrastructure and may spur tenancy expansion for smaller MVNOs.

Vendor alliances matter. Ericsson’s EUR 200 million RandD commitment at Athlone secures on-shore expertise in cloud-native core functions, accelerating stand-alone 5G roll-outs. Parallel Wireless supplies Open RAN kits for Vodafone’s rural program, hinting at a more vendor-diverse supply chain. Collectively, these moves signal that long-run differentiation will hinge on network performance, enterprise solution depth, and the agility to exploit new spectrum bands.

Ireland Telecom MNO Industry Leaders

Eir Mobile

Vodafone Ireland

Three Ireland

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ericsson confirmed a EUR 200 million RandD expansion in Athlone to scale intelligent-automation and stand-alone 5G capabilities.

- March 2025: Three Ireland reported reaching 48.7% subscriber share after EUR 2 billion cumulative investment, including EUR 1.1 billion toward network upgrades.

- February 2025: Virgin Media Ireland scheduled the nation’s first 5-gigabit fiber broadband launch for Q2 2025 amid 11% annual data-consumption growth.

- December 2024: Equinix agreed to acquire BT’s Irish data-center portfolio for EUR 59 million.

Ireland Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means. The telecom MNO market includes in-depth trend analysis based on connectivity like fixed networks, mobile networks, and telecom towers. Several factors, including an increasing demand for 5G, are likely to drive the adoption of telecom services in Ireland.

The Irish telecom MNO market is segmented by services (voice services (wired and wireless), data and messaging services, OTT, and payTV services). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current size of the Ireland telecom MNO market?

The market stands at USD 3.2 billion as of 2026.

At what CAGR is the market expected to grow?

The market is expected to grow at a CAGR of 2.46% and is projected to reach USD 3.61 billion.

How fast is the enterprise segment expanding?

Enterprise connectivity revenue is projected to grow at a 2.76% CAGR between 2026 and 2031.

Which operator leads on subscriber share?

Three Ireland leads with 48.7% subscriber share following strong SIM-only gains.

How will the National Broadband Plan influence MNO revenue?

The plan’s fiber backbone enables wholesale back-haul leasing that can temper revenue decline by opening new rural income streams.

What role do MVNOs play going forward?

MVNOs will target niche consumer and IoT segments, but high wholesale fees limit their immediate scale potential.

Page last updated on: