Ireland Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

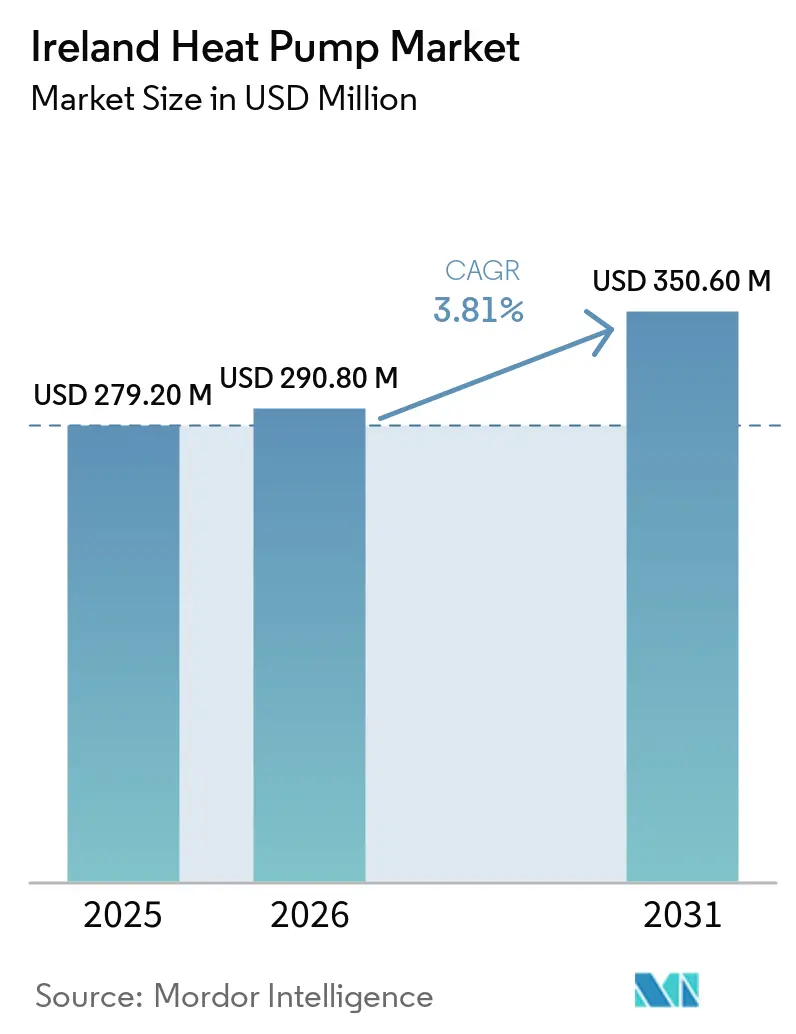

| Base Year Market Size (2025) | USD 279.20 Million |

| Market Size (2026) | USD 290.80 Million |

| Market Size (2031) | USD 350.60 Million |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Heat Pump Market Analysis by Mordor Intelligence

The Ireland heat pump market size is expected to increase from USD 279.2 million in 2025 to USD 290.8 million in 2026 and reach USD 350.6 million by 2031, growing at a CAGR of 3.81% over 2026-2031. Policy momentum, generous Sustainable Energy Authority of Ireland (SEAI) grants, and the rising cost of fossil fuels sustain demand, yet deployment remains hampered by installer shortages, rural grid constraints, and strict Heat Loss Indicator thresholds that screen out many C-rated dwellings. Multinational manufacturers are expanding European production capacity, while domestic specialists leverage familiarity with Ireland’s aging housing stock to defend share. Commercial retrofits accelerate on European Union (EU) Energy Performance of Buildings Directive compliance pressure, and a high-temperature heat-pump pilot widens the addressable retrofit pool. Together, these factors underpin steady but not explosive growth as Ireland pursues its 680,000-unit 2030 target.

Key Report Takeaways

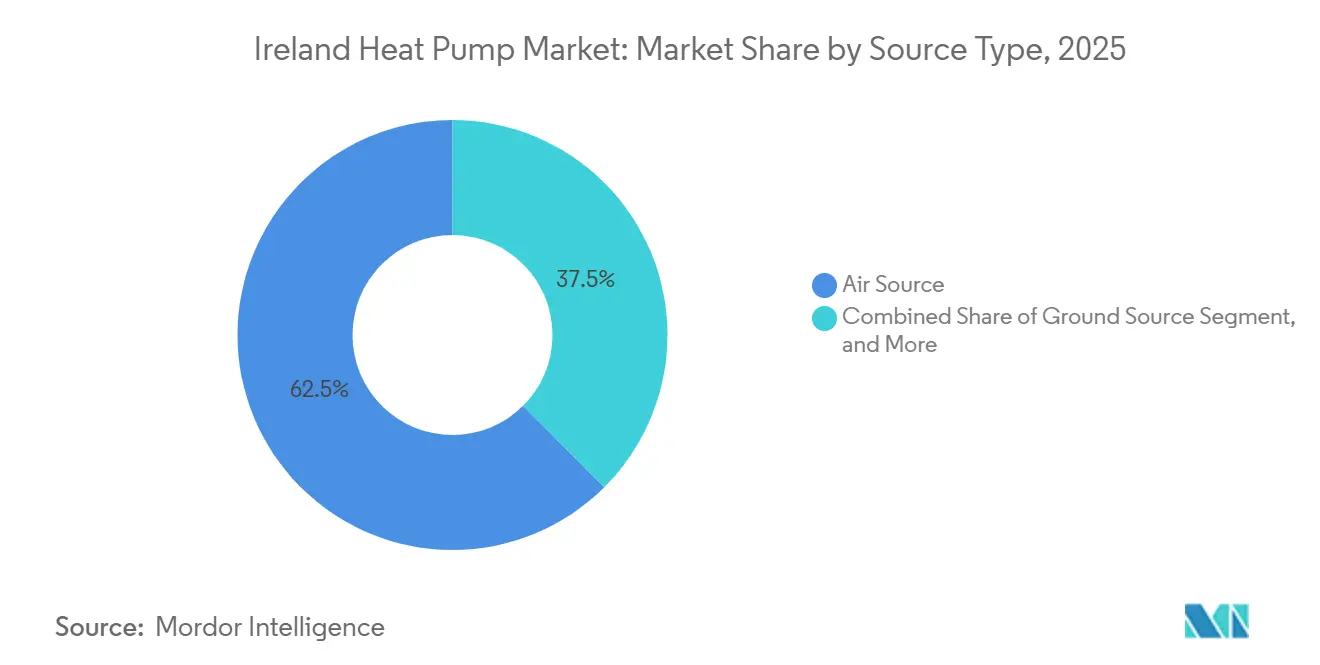

- By type, air-source systems led with 62.48% of Ireland heat pump market share in 2025, while hybrid configurations are projected to expand at a 4.13% CAGR through 2031.

- By technology, air-to-water units captured 54.03% share of the Ireland heat pump market size in 2025; ground-to-water solutions are set to grow at 4.28% CAGR between 2026-2031.

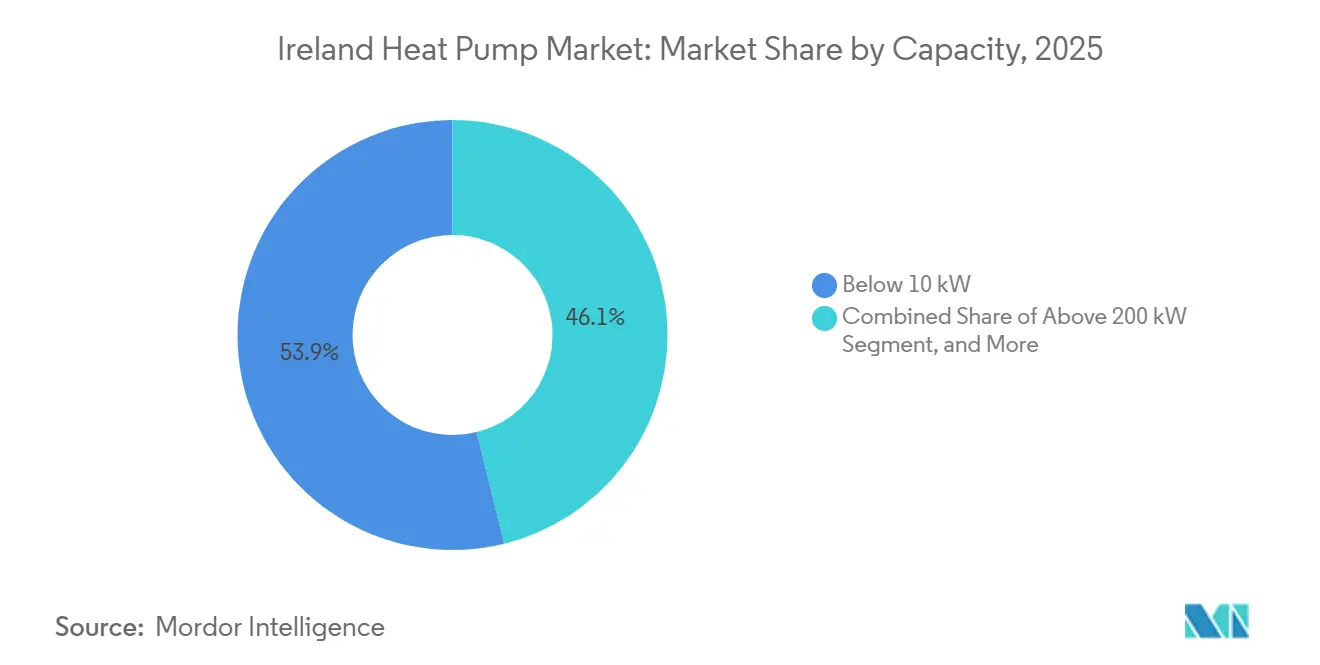

- By capacity, systems below 10 kilowatts held 53.87% share in 2025, whereas the 10-50 kilowatt band is forecast to advance at 4.19% CAGR to 2031.

- By application, space heating accounted for 70.86% of 2025 demand, yet space cooling is expected to rise at 4.62% CAGR over 2026-2031.

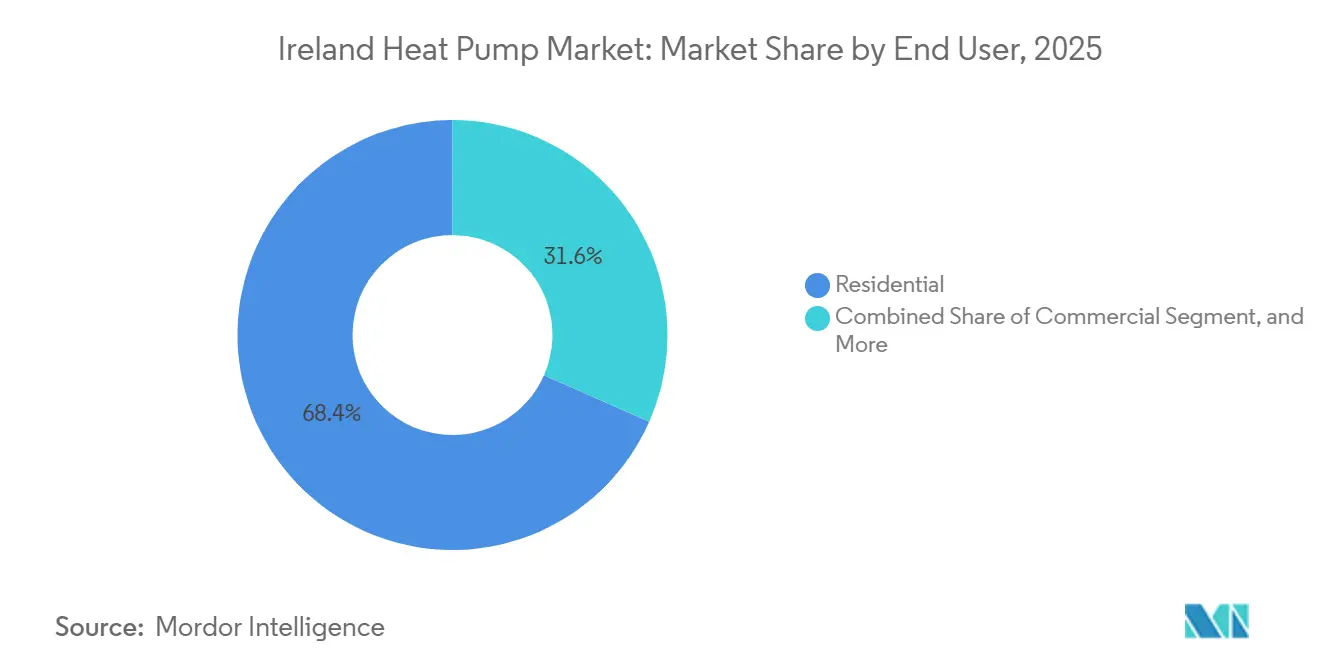

- By end user, residential installations dominated with 68.39% share in 2025; commercial projects are poised for 4.23% CAGR through 2031.

- By installation, retrofit activity represented 58.93% of 2025 revenue, while new-build adoption is projected to increase at 4.18% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ireland Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Prices Boosting Efficiency Payback | +1.2% | National, acute in oil-heated rural counties (Cork, Kerry, Galway) | Short term (≤ 2 years) |

| Smart-Tariff Demand-Response Integration | +0.8% | Dublin, Cork, Limerick metro areas with high smart-meter use | Medium term (2-4 years) |

| Electrification of Off-Grid Oil-Fired Homes | +0.9% | Rural counties (Donegal, Mayo, Roscommon, Wexford) | Medium term (2-4 years) |

| Supportive SEAI Grants and Tax Incentives | +1.5% | National, higher uptake in owner-occupied homes | Short term (≤ 2 years) |

| EU NZEB and Renovation-Wave Mandates | +0.7% | New builds and public sector retrofits nationwide | Long term (≥ 4 years) |

| Heat-as-a-Service Subscription Models | +0.3% | Urban centers and pilot commercial schemes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Prices Boosting Efficiency Payback

Irish electricity tariffs climbed 4.7% in 2025, yet household gas bills surged 28% to EUR 1,249 (USD 1,411) by 2026, narrowing the operating-cost gap between heat pumps and gas boilers and shortening payback periods in well-insulated homes.[1]NRG Panel, “Are Air To Water Heat Pumps Worth It In Ireland (2026)?,” nrgpanel.ie Rural oil-heated households spend EUR 1,500-2,500 (USD 1,695-2,825) annually on fuel, versus EUR 500-1,000 (USD 565-1,130) for air-source heat pumps, magnifying the economic appeal when combined with grants.[2]Enable Research, “Heat Pumps Ireland: Costs, Grants and Installation Guide,” enable-research.ie The SEAI’s high-temperature pilot tests systems delivering 65 °C flow to unlock savings in less-insulated dwellings, signaling that technological advances can offset fabric limitations. As fossil-fuel volatility persists, homeowners prioritize lifetime cost certainty over lower boiler capex, reinforcing demand for efficient electrification solutions.

Smart-Tariff Demand-Response Integration

Ireland’s smart-meter rollout reached 1.9 million devices in 2025, paving the way for dynamic time-of-use tariffs launching in June 2026 that cut off-peak power prices by up to 60%. Panasonic’s Aquarea M heat pump paired with tado° controls claims 22% cost reduction through schedule optimization, reframing heat pumps as grid-interactive assets rather than static appliances.[3]Panasonic Heating and Cooling Solutions, “Panasonic Unveils New Aquarea EcoFlex,” aircon.panasonic.eu Yet only 30% of installed units use load-shifting algorithms, leaving sizable unrealized savings. Early adopters cluster around Dublin, Cork, and Limerick where smart-meter penetration tops 85%, whereas rural progress is hampered by delayed meter installs and patchy broadband. Supplier obligations under the 2026 Renewable Heat Scheme are expected to bundle tariffs with equipment, mainstreaming demand-response participation.

Electrification of Off-Grid Oil-Fired Homes

The Renewable Heat Act bans new oil boilers by 2025 and mandates full phase-out by 2035, targeting roughly 350,000 oil-reliant dwellings that emit three-quarters of residential heating carbon enable. SEAI’s EUR 4,000 (USD 4,520) switching bonus cuts net heat-pump costs to EUR 5,500-8,500 (USD 6,215-9,605), yet grid upgrades and installer shortages slow rural uptake.[4]Renewable Heating Hub, “Ireland Doubles Heat Pump Grants to EUR 12,500 (USD 13,700),” renewableheatinghub.co.uk ESB Networks cites 18-24-month connection delays where clustered conversions overload aging transformers. Demand is set to peak between 2028-2032, but current contractor capacity maxes out at 40,000 installs annually, exposing a material gap versus policy ambition.

Supportive SEAI Grants and Tax Incentives

In February 2026 the SEAI doubled its top residential grant to EUR 12,500 (USD 14,125) and introduced a EUR 2,000 (USD 2,260) allowance for radiator upgrades, directly attacking a key retrofit cost barrier. A parallel value-added tax cut from 23% to 9% trims roughly EUR 2,100 (USD 2,373) from a EUR 15,000 (USD 16,950) installation. Nevertheless, grant uptake lags solar photovoltaic incentives by a factor of seven, reflecting the greater complexity and lead times tied to heat pumps.[5]Precision Heating, “Higher Retrofit Grants to Boost Home Energy Upgrades,” precisionheating.ie Enhanced 75% funding for social-housing retrofits further widens eligibility, but procurement hurdles keep volumes modest. Expanded loan schemes remain underused, indicating either household liquidity or aversion to additional debt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Installation Cost Versus Gas | -1.1% | National, acute in C-rated homes and rental properties | Short term (≤ 2 years) |

| Shortage of Certified Installers | -0.9% | National, longest wait times in Donegal, Leitrim, Longford | Medium term (2-4 years) |

| Rural Distribution-Grid Capacity Limits | -0.6% | Mayo, Kerry, Galway, and other rural counties | Medium term (2-4 years) |

| Noise and Aesthetic Concerns in Dense Housing | -0.4% | Urban terraced housing in Dublin, Cork, Galway city centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Installation Cost Versus Gas

Heat-pump capex of EUR 12,000-20,000 (USD 13,560-22,600) dwarfs the EUR 3,000-5,000 (USD 3,390-5,650) cost of a gas boiler, even after subsidies, leaving many owners with EUR 2,000-7,500 (USD 2,260-8,475) out-of-pocket. C-rated homes, one-third of the stock, meet comfort needs with current boilers, reducing urgency to switch and extending paybacks to 7-10 years.[6]TheJournal.ie, “The ‘comfort barrier’: Why Irish homeowners aren’t going for heat pumps,” thejournal.ie Grant rules require a stringent Heat Loss Indicator that ignores modern cold-climate pump performance, excluding many viable dwellings. Split incentives deter landlords from investing when tenants reap energy savings. Absent further capex relief or mandatory replacement triggers, many households defer adoption until boiler failure forces action.

Shortage of Certified Installers

Ireland had about 1,000 SEAI-registered installers in 2024 but needs 3,000 by 2030 to hit climate targets, implying a threefold scale-up over four years. Multi-week certification courses, travel distances to training centers, and limited apprenticeships slow workforce growth. Wait times ballooned to 6-12 months in 2025, diverting urgent replacements back to fossil fuel systems. Panasonic’s EUR 320 million (USD 361 million) Pilsen factory includes a 600 square-meter training campus, underscoring industry recognition that supply-side skill gaps, not consumer demand, govern deployment velocity. Rural counties suffer most, with fewer than 20 qualified installers serving populous territories, inflating project costs by 10-15% through travel surcharges and raising quality-assurance concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Air Source Dominance, Hybrid Upswing

Air-source heat pumps retained 62.48% of Ireland heat pump market share in 2025 thanks to modest capex, straightforward siting, and compatibility with legacy radiator networks. Within the Ireland heat pump market, hybrid systems that pair electric compressors with existing gas or oil boilers are predicted to post the fastest 4.13% CAGR to 2031, as homeowners in C- and D-rated properties hedge against electricity-price swings while preserving fossil back-up for extreme cold spells. Water-source variants remain niche near lakes or rivers, serving under 2% of installs, yet seasonal performance factors above 4.5 entice hospitality operators seeking operating-cost certainty. Ground-source units held near 8% share, concentrated in rural self-builds and commercial estates where trenching or borehole costs can be spread across larger projects, even after SEAI grants offset half of eligible outlays. Natural-refrigerant R290 launches from Grant Engineering and Warmflow flag the transition away from high-GWP synthetics ahead of EU F-Gas cutbacks.

The Ireland heat pump market size for air-source units is expected to expand steadily as manufacturers roll out quiet-mark products tailored for dense estates, addressing aesthetic objections that slow uptake in terraced rows. Marketing campaigns now emphasize lifecycle running-cost relief rather than pure carbon messaging, aligning with household budget priorities. Hybrid solutions benefit from relaxed planning rules that classify outdoor condensers as permitted development, reducing administrative friction in conservation zones. Conversely, limited drilling contractors and soil-type uncertainty continue to restrain ground-source acceleration, despite compelling long-run economics for high-duty commercial loads.

By Technology: Air-to-Water Retains Lead, High-Temp Systems Broaden Appeal

Air-to-water systems, covering space heating and domestic hot water (DHW), accounted for 54.03% of 2025 revenue within the Ireland heat pump market size. Mitsubishi Electric’s 75 °C Ecodan R290 models signal that high-temperature capability can meet oversized radiator expectations without wholesale distribution upgrades, a breakthrough for older stone houses that currently fail Heat Loss tests. Ground-to-water configurations should grow at 4.28% CAGR to 2031 as resorts, hospitals, and light-industry premises chase seasonal coefficients of 4.0 plus, leveraging Better Energy Communities capital grants that reach EUR 1.8 million (USD 2.03 million). Air-to-air units serve about 12% of volume, popular in new builds offering reversible cooling, yet grant ineligibility for DHW keeps them niche among owner-occupiers. Water-to-water machines linger below 3% share, restricted to specialized agricultural or process-heat deployments where secure abstraction rights exist.

Innovation pipelines center on integrated hybrids such as Panasonic’s EcoFlex, which harnesses rejected cooling energy to pre-heat DHW, lifting total system efficiency. Remote monitoring apps quantify savings, supporting pay-as-you-save financing pilots. Meanwhile, EU F-Gas quotas push suppliers toward propane (R290) and lower-pressure blends like R454C, differentiating portfolios on future-proof compliance. The Ireland heat pump market therefore tilts toward technologies that combine high output temperatures, flexible refrigerants, and smart-grid readiness, satisfying both regulatory and consumer risk criteria.

By Capacity: Mid-Range Equipment Captures Commercial Retrofits

Below-10 kilowatt units served most semi-detached and terraced homes, taking 53.87% share in 2025, yet growth slows as eligible owner-occupied stock becomes saturated. The 10-50 kilowatt bracket is forecast at a 4.19% CAGR as offices, hotels, and schools retrofit ahead of the May 2026 EU directive deadline. Mitsubishi Electric Trane’s 40 kilowatt Pro CAHV, scalable to 640 kilowatts in cascade, illustrates supplier pivot toward modular flexibility that eases plant-room integration. Systems of 50-200 kilowatts satisfy district energy, supermarket, and process-heat needs, roughly 8% of installations, but require bespoke design and long planning horizons. Above-200 kilowatt packages remain scarce, confined to hospitals and municipal leisure centers where fuel-switch paybacks hinge on 24-hour load profiles.

Financiers now view mid-range heat pumps as critical to green-bond eligibility on commercial property refinancings, spurring landlords to replace boilers ahead of lease renewals. Aggregators exploring heat-as-a-service bundles focus on the 10-50 kilowatt range where predictable usage and pooled maintenance drive attractive annuity revenue. Conversely, sub-10 kilowatt suppliers battle margin compression from aggressive Asian brands, prompting domestic players to upsell silent enclosures and Internet-of-Things (IoT) diagnostics as differentiators.

By Application: Cooling Demand Reshapes Value Proposition

Space heating still accounts for 70.86% of 2025 installations in the Ireland heat pump market, reflecting a climate with heating degree days outstripping cooling needs tenfold. Yet space-cooling demand is set for a 4.62% CAGR as summer peaks climb 1-2 °C and building owners chase year-round comfort. Reversible pumps now emphasize quiet night cooling to comply with 42 dB boundary limits, addressing urban planning constraints. DHW-only units hold near 15% share, boosted by combined cylinder replacements during deep retrofits. Industrial and process-heat uses represent under 5% of volume but deliver the highest runtime hours, especially in food and pharma clusters along the Cork-Waterford spine.

Growing awareness that a single appliance can meet heating and cooling boosts consumer willingness to accept higher capex, particularly when hybrid PV-plus-heat-pump packages provide summer self-consumption of solar over-generation. Commercial landlords integrate pumps with building-management systems to offset rising office cooling loads and satisfy tenant wellness standards. In contrast, niche applications such as pool heating and greenhouse control remain specialty contractor domains offering premium service margins.

By End User: Compliance Push Lifts Commercial Share

Residential customers captured 68.39% of 2025 value, buoyed by doubled grants and reduced VAT. However, hotels, offices, and retail centers now face mandatory energy-performance upgrades, propelling commercial uptake toward a 4.23% CAGR. Better Energy Communities funding of up to EUR 1.8 million (USD 2.03 million) per project lowers hurdle rates for large retrofits, while property investors link heat-pump adoption to Environmental, Social, and Governance (ESG) scorecards. Industrial deployments remain below 5% of count but account for outsized kilowatt capacity, as continuous process loads justify ground-source capital intensity.

Complex decision matrices slow commercial projects; planners must balance noise, façade heritage constraints, and lease structures. Pilot successes, such as Parknasilla Resort’s 87% energy cut, demonstrate bankable outcomes, nudging lenders to bundle capex into green-loan tranches. Conversely, the rental residential sector lags due to split savings between landlords and tenants, highlighting the need for heat-as-a-service models that allocate cost and benefit more equitably.

By Installation: New-Build Momentum, Retrofit Complexity

Retrofits held 58.93% share in 2025 given Ireland’s aging stock and National Residential Retrofit Plan funding. Yet new-build penetration is growing at 4.18% CAGR as developers install heat pumps to satisfy Near Zero Energy Building mandates and sidestep gas-network connection fees. Whole-house design lets pumps run at 35-45 °C flow, hitting seasonal performance factors above 4.0, higher than the 3.0-3.5 typical in radiator retrofits. SEAI’s EUR 2,000 (USD 2,260) allowance for radiator upgrades reduces retrofit friction, but fabric-first sequencing still elongates project timelines.

Manufacturers address retrofit pain points with compact integrated cylinders, while contractors experiment with phased installs where building fabric is improved ahead of heat-pump commissioning. Digital twin audits estimate paybacks, fostering homeowner confidence. Meanwhile, new estates pre-lay communal ground loops, cutting individual borehole costs and future-proofing against tighter refrigerant rules. Thus, although retrofits remain numerically dominant, the structural simplicity of new-builds enables faster scaling once planning approvals clear.

Geography Analysis

Dublin, Cork, Limerick, and Galway metro areas anchor roughly half of Ireland heat pump market demand because they combine higher Building Energy Rating scores, dense installer networks, and ample grid headroom. Smart-meter penetration above 85% in these cities accelerates adoption of dynamic tariffs, reinforcing load-shifting economics. Suburban homeowners rapidly integrate photovoltaic arrays with reversible pumps, capturing self-consumption gains that shorten payback timelines. However, terrace rows in conservation districts confront 42 dB noise limits, façade placement rules, and limited rear-yard space for outdoor units, tempering uptake among pre-1910 brick homes.

Rural counties, Donegal, Mayo, Roscommon, Wexford, house Ireland’s largest pool of oil-fired systems, exceeding 40% prevalence, yet face persistent deployment bottlenecks. Grid reinforcement lags despite ESB Networks’ EUR 5 billion (USD 5.65 billion) 2021-2030 investment plan, leading to 18-24-month connection queues where clustered conversions overwhelm legacy transformers. Installer scarcity compounds delays, with fewer than 20 certified contractors in some counties, inflating travel surcharges by up to 15%. Broadband gaps further hinder real-time tariff applications, capping achievable efficiencies.

Counties surrounding Dublin, Louth, Meath, Kildare, benefit from proximity to urban contractor bases and a high concentration of C- and D-rated dwellings earmarked in the National Residential Retrofit Plan. Here, grant-driven retrofit consortia bundle fabric upgrades with heat-pump installs, enabling economies of scale and minimizing customer acquisition costs. Conversely, apartment retrofits lag nationwide; shared ownership structures, limited roof space for PV pre-heating, and planning rules on balcony units restrict deployment, risking asset obsolescence as regulatory standards tighten. Commercial adoption skews toward Dublin and Cork central business districts, where impending EU performance deadlines and green-lease provisions compel early boiler replacement, while industrial heat pumps cluster around Cork-Waterford food and pharmaceutical corridors that capitalize on process-heat recovery benefits.

Competitive Landscape

The Ireland heat pump market exhibits moderate fragmentation: the top five multinational brands and a handful of domestic specialists control a majority of shipments but no single firm holds dominance. Panasonic’s EUR 320 million (USD 361 million) expansion in Pilsen lifts European supply resilience, complemented by training centers that funnel certified installers into the Irish channel. Mitsubishi Electric enriches its R290 Ecodan portfolio, offering 75 °C flow to unlock heritage retrofits, whereas Bosch absorbs Johnson Controls’ residential business to deepen scale and product breadth. Trane Technologies pivots toward digital energy-management platforms, acquiring Stellar Energy Digital and LiquidStack, and collaborates with Garrett Motion on high-temperature compressors, betting that performance data and remote diagnostics will differentiate offerings.

Domestic manufacturer Grant Engineering positions its Aerona R290 line at the premium retrofit tier, leveraging Quiet Mark accreditation and free commissioning to reassure noise-sensitive homeowners. Warmflow’s Zeno series likewise adopts natural refrigerant to sidestep impending F-Gas quotas and aligns with installer training subsidies. Smaller players such as MasterTherm and Heliotherm court bespoke commercial jobs, integrating cascade ground-source arrays where performance trumps first cost. Yet installer scarcity, SEAI eligibility audits, and tight planning rules erect entry barriers that favor vendors with robust after-sales networks and compliance support teams.

High-temperature and heat-as-a-service models remain nascent but represent white-space growth avenues. Service-subscription penetration sits below 5%, limited by consumer unfamiliarity and financier risk aversion, yet rising borrowing costs could tilt households toward off-balance-sheet solutions that package equipment, maintenance, and energy guarantees into fixed monthly fees. Meanwhile, multi-unit residential systems utilizing central R290 loops promise to unlock the under-served apartment segment, provided developers can navigate fire-safety and acoustic standards.

Ireland Heat Pump Industry Leaders

Glen Dimplex

Grant Engineering

LG electronics Inc.

Trane Technologies Plc

Johnson Controls International Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mitsubishi Electric Trane HVAC US introduced the 40 kW Ecodan Pro CAHV hydronic heat pump with 74 °C output and 16-unit cascade capability.

- February 2026: SEAI raised the maximum residential heat-pump grant to EUR 12,500 (USD 14,125) and added a EUR 2,000 (USD 2,260) central-heating upgrade allowance.

- February 2026: Trane Technologies partnered with Garrett Motion to co-develop advanced compressors for ≥70 °C applications.

- February 2026: MasterTherm documented an 87% energy-savings retrofit at Parknasilla Resort via five BA60iS ground-source units.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Ireland heat pump market as the annual revenue generated from sales of air-source, water-source, and ground-source heat pump units plus their associated standardized installation kits and commissioning fees across residential, commercial, industrial, and institutional premises.

Scope Exclusions: Portable room coolers, reversible air-conditioners marketed primarily for cooling, and aftermarket service contracts remain outside the sizing scope.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed licensed installers, distributor managers, homeowner retrofit coordinators, and policy officials across Leinster, Munster, and Ulster. Their inputs clarified installer margin structures, grant approval lead times, and forthcoming SEAI scheme tweaks, letting us stress-test cost and uptake assumptions.

Desk Research

We began by mining authoritative public datasets such as SEAI grant uptake dashboards, Central Statistics Office dwelling-completion files, Eurostat trade codes 841861-63, and European Heat Pump Association shipment briefs, which anchor technology penetration and unit values. Complementary insight flowed from peer-reviewed journals on coefficient of performance trends, Irish Parliament committee minutes on the 9% VAT rate, and company 10-Ks that disclose local ASP bands. Subscription resources, including D&B Hoovers for producer revenues and Dow Jones Factiva for deal flow, enriched the desk review. These sources are indicative; analysts referenced many additional materials for validation and clarification.

Market-Sizing & Forecasting

A top-down model starts with SEAI-reported unit installations and Eurostat import volumes, which are then priced using weighted average selling prices gathered from installer quotes and supplier filings. Results are cross-checked through selective bottom-up roll-ups of leading vendor shipments and channel checks. Key variables, including new-build completions, retrofit approval ratios, electricity-to-gas price differentials, average grant size, and installer capacity, feed multivariate regression and scenario analysis to project demand through 2030. Where distributor data proved patchy, unit counts were gap-filled with customs entries and reconciled during expert calls.

Data Validation & Update Cycle

Outputs pass two-level analyst review, variance thresholds trigger model reruns, and anomalies are re-queried with field sources before sign-off. The report refreshes every twelve months, with interim updates if grant rules, energy prices, or major policy announcements shift materially.

Why Our Ireland Heat Pump Baseline Commands Reliability

Published estimates often diverge because firms slice the product set differently, convert currencies on assorted dates, or lock forecasts before policy changes land.

Key gap drivers include: some studies consider only Prodcom category 28251380 (excluding hybrid and monobloc units); others rely on historic turnover without updating ASP escalators; several roll global averages onto Ireland without adjusting for SEAI grants or the 400,000-unit 2030 target, whereas Mordor Intelligence integrates these local drivers and refreshes numbers annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 279.2 M (2025) | Mordor Intelligence | - |

| USD 53 M (2024) | Regional Consultancy A | Trade-code scope only, omits installation revenue |

| USD 53.7 M (2018) | Industry Association B | Pre-pandemic baseline, excludes hybrid units and services |

Taken together, the comparison shows that our carefully layered scope, live policy variables, and synchronized currency treatment offer decision-makers a balanced, transparent baseline they can retrace and update with ease.

Key Questions Answered in the Report

How large is the Ireland heat pump market in 2026?

It is estimated at USD 290.8 million in 2026, on track to reach USD 350.6 million by 2031.

What is the current growth rate for heat pumps in Ireland?

From 2026 to 2031, the market is forecast to post a 3.81% CAGR as grant support and policy mandates offset structural bottlenecks.

Which heat-pump type leads sales in Ireland?

Air-source units dominate with 62.48% share because of lower installation costs and retrofit suitability.

Why are installer shortages a major issue?

Only about 1,000 certified contractors operated in 2024, versus roughly 3,000 needed by 2030, resulting in wait times of 6-12 months in high-demand regions.

How do SEAI grants reduce up-front costs?

Homeowners can now claim up to EUR 12,500 (USD 14,125) toward equipment, plus EUR 2,000 (USD 2,260) for radiator upgrades and a EUR 4,000 (USD 4,520) bonus when switching from fossil fuels.

Which segment will grow fastest through 2031?

Hybrid heat-pump systems combining electric and fossil back-up are forecast to expand at a 4.13% CAGR as households manage electricity-price volatility.

Page last updated on: