Ireland Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

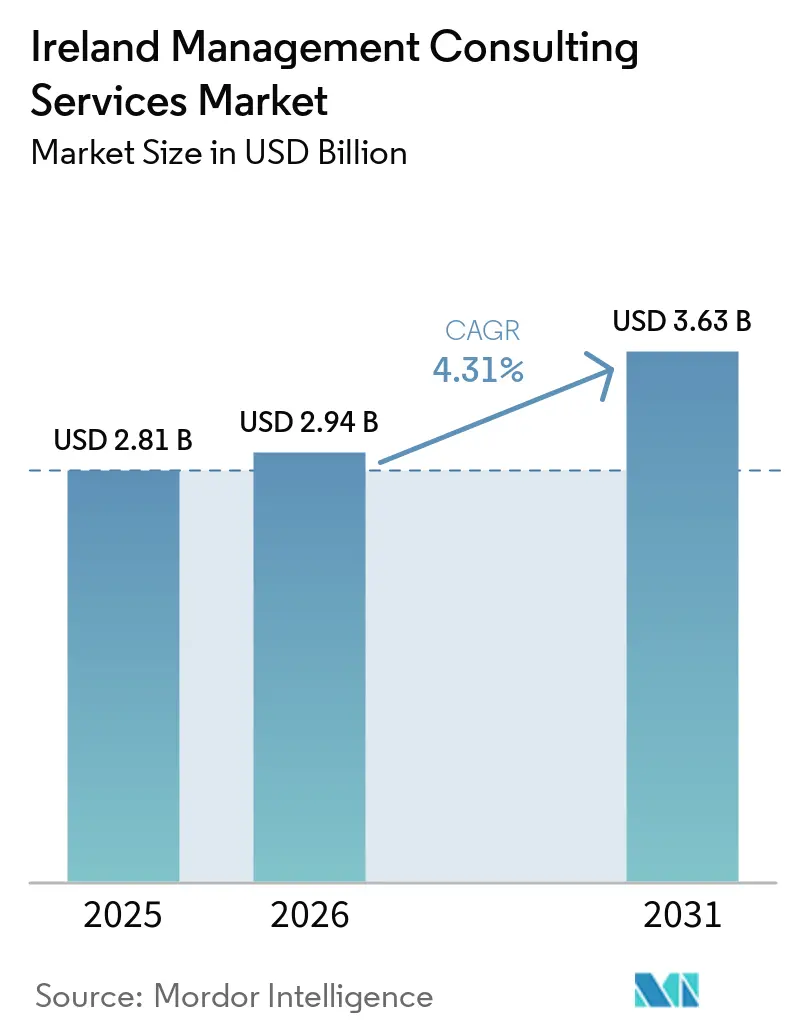

| Base Year Market Size (2025) | USD 2.81 Billion |

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.63 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ireland Management Consulting Services Market Analysis by Mordor Intelligence

The Ireland management consulting services market size is expected to increase from USD 2.81 billion in 2025 to USD 2.94 billion in 2026 and reach USD 3.63 billion by 2031, growing at a CAGR of 4.31% over 2026-2031. Intensifying regulation, digital-first public policies and the post-Brexit relocation of advisory work to Dublin keep growth on a stable trajectory despite skills shortages and cautious enterprise budgets. Demand concentrates in technology, financial services and healthcare, where overlapping EU mandates are forcing rapid operating-model change. At the same time, escalating wage inflation and housing constraints inside Dublin and Cork squeeze delivery capacity and nudge firms toward hybrid and remote execution models. Competitive pressure continues to rise as platform vendors and specialist boutiques challenge the Big Four with lower-cost, automation-enabled offerings, prompting incumbents to invest in regional hubs and generative artificial intelligence accelerators to protect margins and relevance.

Key Report Takeaways

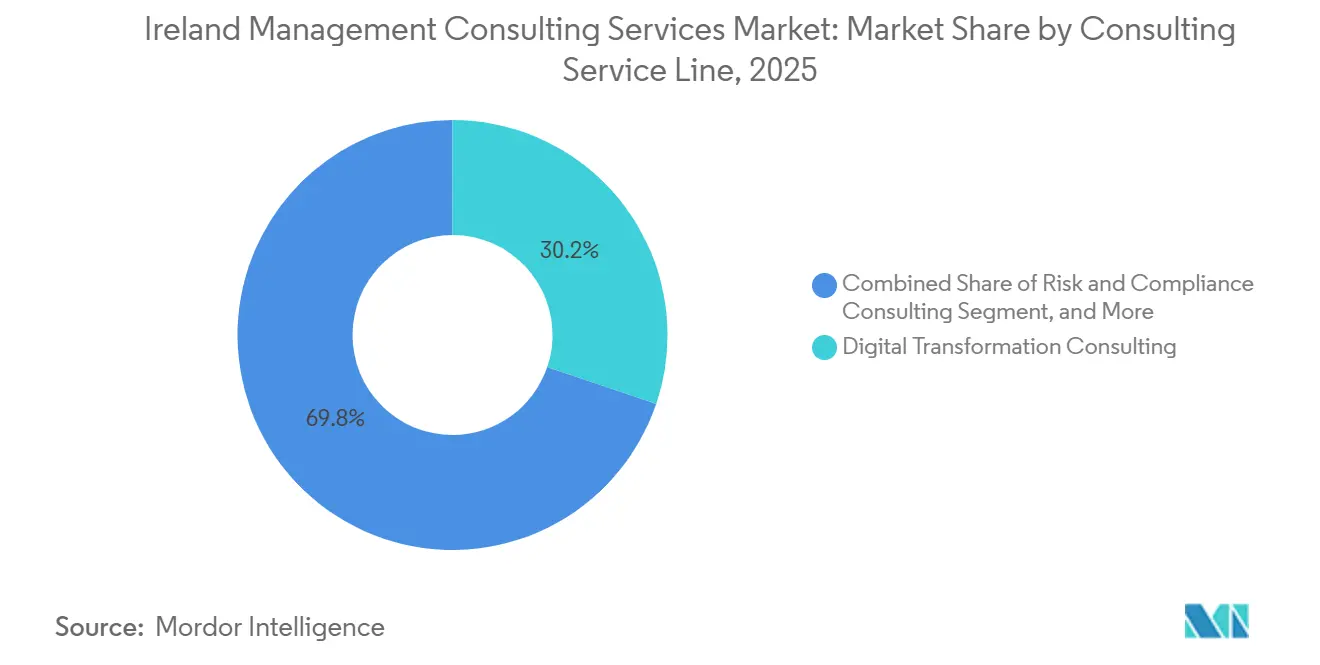

- By consulting service line, Digital Transformation Consulting led with 30.19% of the Ireland management consulting services market share in 2025 while Risk and Compliance Consulting is projected to post the fastest 4.72% CAGR through 2031.

- By organization size, large enterprises held 68.73% of the Ireland management consulting services market size in 2025 whereas small and medium-sized enterprises are forecast to expand at a 4.37% CAGR to 2031.

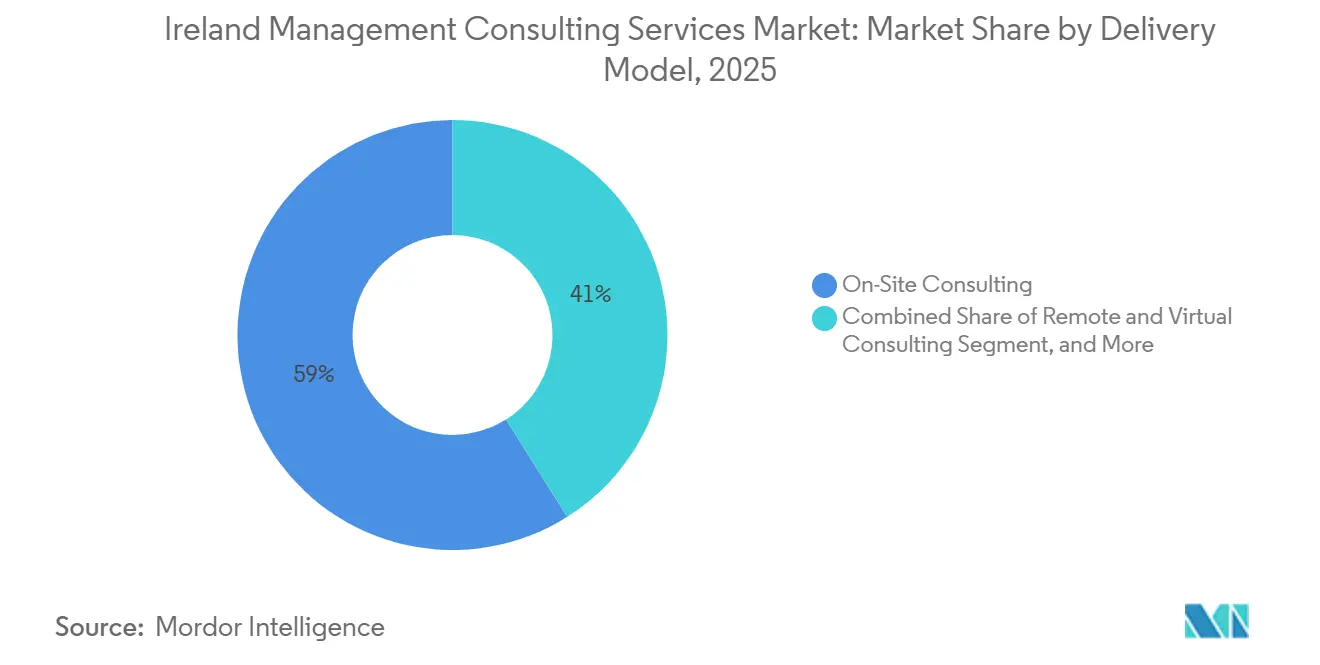

- By delivery model, on-site engagements captured 58.97% revenue in 2025, yet remote and virtual consulting is set to advance at a 4.83% CAGR during 2026-2031.

- By end-user industry, information technology and telecommunications accounted for 24.48% demand in 2025, while healthcare is positioned to grow quickest at a 4.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ireland Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Initiatives Among Irish Enterprises | +1.2% | National, Dublin and Cork hubs | Medium term (2-4 years) |

| Post-Brexit Near-Shoring of EU Advisory Work to Ireland | +0.9% | Dublin International Financial Services Centre, regional spillover | Long term (≥4 years) |

| AI Act and EU Digital Finance Package Compliance Advisory | +0.8% | National, all regulated firms | Short term (≤2 years) |

| Increasing Regulatory Complexity and Compliance Requirements | +0.7% | National, financial services and healthcare | Medium term (2-4 years) |

| Rising Demand for Cost Optimization and Operational Efficiency in SMEs | +0.5% | Munster, Connacht and rural hubs | Long term (≥4 years) |

| Growing Adoption of Cloud and Artificial Intelligence Technologies | +0.6% | National, led by multinationals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Initiatives Among Irish Enterprises

National policy requires 90% of SMEs to reach basic digital intensity and 75% of all firms to adopt cloud, artificial intelligence and big data by 2030, but only one-fifth of enterprises used artificial intelligence in 2025 and a mere 13% achieved enterprise-wide cloud scale.[1]Central Statistics Office, “Information Society Statistics – Enterprises 2025,” CSO.ie This sizable execution gap sustains advisory demand for cloud road-maps, FinOps and change-management programs. Public subsidies amplify uptake: the EUR 58 million (USD 63.8 million) Digital Transition Fund and Enterprise Ireland’s consultancy grant of up to EUR 35,000 (USD 38,500) per firm lower cost barriers. Large enterprises paused broad digital agendas in 2025, yet 68% still expect IT budgets to rise over the next year, shifting spend toward ROI-proven, consultant-led sprints.

Post-Brexit Near-Shoring of EU Advisory Work to Ireland

Dublin’s International Financial Services Centre now hosts 9,100 investment funds with net asset value above EUR 5.3 trillion (USD 5.83 trillion) and 136 fund management companies, each facing delegation and resilience reviews through 2027.[2]Central Bank of Ireland, “Regulatory and Supervisory Outlook 2026,” Centralbank.ie Consulting briefs cover board composition, outsourcing redesign and liquidity testing as firms adapt to Central Bank inspections. Productized offerings such as Deloitte’s Brexit Lab map supply-chain risk and regulatory alignment into repeatable modules. Government financing, including the EUR 300 million (USD 330 million) Brexit Loan Scheme, widens the client pool to export-oriented SMEs.

AI Act and EU Digital Finance Package Compliance Advisory

Ireland’s Regulation of Artificial Intelligence Bill 2026 enforces the EU AI Act via sectoral surveillance authorities, compelling companies to inventory systems, classify risks and embed human oversight within 18 months. Parallel mandates under the Digital Operational Resilience Act require banks and insurers to run threat-led penetration tests every three years and standardize incident reporting, seeding multi-year governance and cyber-resilience engagements. The modernized Consumer Protection Code, effective March 2026, adds anti-greenwashing and digital-design principles, further heightening compliance workloads.

Increasing Regulatory Complexity and Compliance Requirements

The Central Bank’s 2026 outlook layers five cross-sectoral priorities onto banking, payments, funds and insurance, triggering concurrent reviews of valuation, liquidity and ESG disclosures. Budget 2026 increased the R&D tax credit to 35%, yet only 45% of prior claims cleared without intervention, pushing firms toward tax-advisory optimization. Imminent overhaul of the Fund Service Provider Framework adds outsourcing and leverage rules in 2027, meaning governance architectures must be redesigned in parallel with ongoing supervisory audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Talent Shortage and High Consultant Turnover | -0.8% | Dublin and Cork hot spots | Medium term (2-4 years) |

| Heightened Price Sensitivity Amid 2026-2027 Fiscal Tightening | -0.6% | Nationwide budgets | Short term (≤2 years) |

| Commoditization of Entry-Level Consulting via Freelance Platforms | -0.3% | Digital and process segments | Long term (≥4 years) |

| Expansion of In-House Strategy and Transformation Teams | -0.4% | Multinational HQs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Talent Shortage and High Consultant Turnover

Ninety percent of technology executives describe recruitment as challenging, while 96% of firms executed redundancies in 2025, producing simultaneous scarcity and churn.[3]RSM Ireland, “Technology Industry Outlook 2026,” RSM.global Median tax-professional tenure fell from 2.7 to 2.3 years between 2024 and 2026, compressing payback on training investments.[4]Barden, “Tax Talent Monitor Q1 2026,” Barden.ie Skill premiums are rising: 72% of companies offer higher salaries for AI expertise and 63% lost staff owing to strict office-attendance rules. Housing shortages near urban offices further erode mobility and intensify wage inflation.

Heightened Price Sensitivity Amid 2026-2027 Fiscal Tightening

Sixty-three percent of leaders expect the Irish economy to weaken in 2026 and 64% forecast softer global conditions, triggering ROI scrutiny on every advisory dollar.[5]Expleo, “Business Transformation Index 2025,” Expleo.com Innovation investment climbed to 26% of capital budgets by late 2025, yet generic technology spend slid to 22%, illustrating selective funding for high-impact projects. Rising labor costs absorb discretionary funds and propel procurement toward fixed-price, outcome-based models mandated by Central Bank cost-control guidance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Momentum Outpaces Digital Maturity

Digital Transformation Consulting captured the largest slice of the Ireland management consulting services market size in 2025, yet clients now pivot from broad digitization to laser-focused regulation-ready programs. Risk and Compliance Consulting, propelled by AI Act, DORA and Consumer Protection Code timelines, is on track for the fastest growth, reflecting urgency among banks, insurers and digital health providers to embed controls before supervisory deadlines. Strategy Consulting remains critical for post-Brexit supply-chain diversification, with modular Brexit-impact diagnostics offering quick wins. Operations Consulting secures steady demand from indigenous manufacturers pursuing the government’s annual 1% productivity target, blending lean, automation and green process redesign. Human Resources and Talent Advisory helps navigate dual pressures of skills shortages and generative AI workforce redesign. Across these lines, proof-of-value metrics, hybrid delivery and platform orchestration define winning propositions, underscoring how the Ireland management consulting services market aligns specialist knowledge with time-bound regulatory and performance milestones.

Consultancies now bundle automation accelerators, regulatory content libraries and managed-services hand-offs to defend margins. This approach resonates because only 22% of Irish organizations have scaled agentic AI and just 36% of SMEs invested in digital activities in 2023, down from 41% in 2021, signaling unmet transformation ambitions. Program road-maps increasingly anchor to board-approved risk appetites as firms choose certainty over experimentation. Consequently, the Ireland management consulting services industry expects compliance-led engagements to outstrip discretionary innovation spend until macro visibility improves after 2027, solidifying a revenue mix tilted toward governance, risk and compliance deliverables.

By Organization Size: Policy Supports Unlock SME Consulting Uptake

Large enterprises still deliver the lion’s share of the Ireland management consulting services market size, benefiting from global delivery models and complex multi-year deals such as the Health Service Executive’s Electronic Health Record program. Yet public incentives are shifting momentum. Local Enterprise Offices issued EUR 44.8 million (USD 49.28 million) in capital grants and run low-fee capability programs, while Enterprise Ireland funds up to EUR 35,000 (USD 38,500) per firm for external strategy expertise. These mechanisms are expanding the SME client base, supporting a 4.37% CAGR outlook through 2031. Government aims to double new exporters to 360 annually and add 2,000 Irish-owned exporters by 2030, each requiring market-entry strategy, export compliance and digital readiness advice.

SME consulting engagements differ in cadence and scope. They favor phased sprints, remote workshops and templated toolkits over bespoke, on-site teams, aligning to tighter budgets. Nonetheless, SMEs present rich cross-sell potential: once exporters scale, they purchase governance, cybersecurity and operational efficiency services, reinforcing lifetime advisory value. For large enterprises, board scrutiny on consulting value is heightening, pushing providers toward outcome-based pricing and data-driven benefit realization. This bifurcated dynamic positions the Ireland management consulting services market to balance volume growth from scaling indigenous firms with high-value programs in multinationals, securing diversified revenue streams.

By Delivery Model: Hybrid Gains as Resilience and Talent Pressures Converge

On-site delivery commands a majority share because sensitive data, audit trails and executive workshops still necessitate physical presence. However, continuity obligations inside the Digital Operational Resilience Act validated distributed models, and 63% of businesses lost staff due to stricter office mandates. Consequently, remote and virtual engagements are forecast to expand fastest, reinforced by collaboration platforms and standardized security protocols accepted by regulators. Hybrid consulting blends the two, preserving stakeholder intimacy while unlocking nationwide talent pools and cost arbitrage from 10-15% salary differentials outside Leinster.

Client attitudes are evolving: procurement frameworks now accept virtual milestones, and Office of Government Procurement contracts allow remote delivery for specified tasks, provided data residency is maintained. Providers leverage regional delivery centers in Galway, Waterford and Limerick to scale specialized skills, reduce travel emissions and meet sustainability scoring criteria in public tenders. Over the forecast horizon, hybrid will represent the default for multi-year transformation, while critical board-level and crisis assignments continue to rely on high-touch, on-site teams, ensuring diversified channel strategies across the Ireland management consulting services market.

By End User Industry: Digital Health Ambitions Accelerate Consulting Spend

Technology and telecommunications firms generated almost one-quarter of 2025 revenue, yet healthcare is primed for the highest growth as the Health Service Executive targets 4-6% of national health spending for digital initiatives. Forty-eight programs spanning Electronic Health Records, Shared Care Records and e-prescribing mandate advisory across interoperability, cybersecurity and change management. The 2021 ransomware attack sharpened executive focus on resilience, leading to multi-year cybersecurity assessments aligned with DORA principles.

Financial services remain a core market. The Central Bank oversees EUR 5.3 trillion (USD 5.83 trillion) in fund assets, demanding liquidity, leverage and outsourcing reviews that translate directly into governance consulting. Manufacturing and energy clients seek advisory on sustainability transitions, green hydrogen and circular bioeconomy, supported by IDA Ireland’s EUR 7 billion (USD 7.7 billion) research and development target. Public-sector demand benefits from centralized consultancy frameworks, with sustainability and social value now weighted up to 20% in awards, pushing firms to document carbon-reduction road-maps in their own delivery approaches. Together, these sectoral vectors cement a resilient, multi-industry opportunity set for the Ireland management consulting services market through 2031.

Geography Analysis

Dublin and the wider Leinster region continue to anchor the Ireland management consulting services market, capturing the bulk of advisory spend because most multinational headquarters, government departments and the International Financial Services Centre cluster inside the capital. The city also houses core delivery teams for the Big Four, Accenture and IBM, all of which rely on proximity to clients in banking, technology and the public sector. Rapid rental inflation and a limited housing pipeline, however, are prompting firms to diversify into lower-cost urban centers while retaining a client-facing presence in Dublin. As a result, firms are rolling out hybrid delivery models that mix onsite executive workshops in Dublin with remote execution from regional hubs, conserving margin and broadening the labor pool. This redistribution of activity keeps Leinster dominant yet opens space for balanced national growth.

Munster, led by Cork, is emerging as the fastest-growing region within the Ireland management consulting services market. Deloitte’s pledge to double its Cork workforce by 2027, EY’s two-thirds expansion of floor space at Lapp’s Quay and IBM’s addition of security, automation and hybrid-cloud roles illustrate a clear momentum shift. Life-sciences majors, semiconductor plants and scaling technology firms in the county underpin year-round demand for digital transformation, tax structuring and sustainability road-maps. Nearby Waterford and Limerick supplement this ecosystem with specialist analytics and SAP teams that feed into national projects through virtual collaboration platforms. Salary differentials of up to 15% versus Dublin, combined with strong regional university pipelines, reinforce Munster’s position as a value-efficient delivery corridor.

The West and Mid-West regions, encompassing Galway, Mayo, Roscommon, Limerick, Clare and Tipperary, focus on renewable energy, AgTech and film production, domains that rely heavily on niche consulting skills. IDA Ireland’s Adapt Intelligently strategy targets at least 550 regional foreign direct investment wins by 2029, and the Regional Building Programme is addressing property bottlenecks for knowledge-industry tenants. Local Enterprise Offices act as front-door channels, guiding approximately 370,000 eligible SMEs toward subsidized advisory, including the twelve-month Strategic Growth Programme offered in Galway. Public-sector buyers outside Leinster leverage Office of Government Procurement frameworks to source consulting services through standardized mini-competitions, embedding social and green criteria that favor bidders with local supply chains. Collectively, these initiatives enable a more distributed footprint while keeping Dublin the undisputed command center of the Ireland management consulting services market.

Competitive Landscape

Big Four firms, PwC, KPMG, Deloitte and EY, still dominate the Ireland management consulting services market share, together accounting for about 86% of accounting-heritage advisory revenue. Their scale advantages include proprietary accelerators, deep regulatory relationships and roughly 15,000 professionals across the island, traits that secure multi-year mandates in financial services and public administration. To defend this lead, each has announced regional expansions: Deloitte’s Technology and Analytics Hub in Cork concentrates on generative artificial intelligence, cloud FinOps and Environmental, Social and Governance analytics, while EY is consolidating its Dublin workforce into a new Wilton Park headquarters slated to open in summer 2026. PwC has invested in cloud and cyber labs, and KPMG is marketing turnkey DORA readiness packages, underscoring a pivot toward productized, platform-enabled consulting.

Mid-tier networks are scaling niche plays to chip away at Big Four incumbency. Grant Thornton boosted partner count by a dozen in March 2026 and positions itself as a full-service alternative for asset-management, aviation and life-sciences clients that value a single relationship across audit, tax and advisory. BDO, Forvis Mazars and Crowe lean on sector specialization, especially government, hospitality and sustainability, to win targeted framework lots and outcome-based contracts. Boutique consultancies in regulatory technology, grant advisory and green transition further fragment the landscape, often winning sub-projects within large transformation programs where agility and cost discipline are prized. These smaller players typically recruit Big Four alumni and pair lower overhead with automation toolkits, letting them undercut standard time-and-materials rates by 15-20%.

Technology vendors are also entering the advisory arena, adding fresh competitive heat to the Ireland management consulting services industry. IBM intends to recruit up to 800 professionals across research, digital sales and consulting, centered on Red Hat hybrid-cloud stacks and security automation, blurring lines between software implementation and strategic advice. Accenture’s economic-impact research on generative artificial intelligence positions the firm as a thought leader, helping it cross-sell a five-imperative reinvention framework spanning value strategy, digital core, talent, responsible artificial intelligence and continuous transformation. Meanwhile, SaaS platforms bundle best-practice blueprints, enabling clients to self-configure functions that were once consultant-led, pressuring firms to prove unique value through domain depth and measurable outcomes. Together, these forces are compressing pricing, accelerating specialization and reinforcing the need for talent differentiation across the Ireland management consulting services market.

Ireland Management Consulting Services Industry Leaders

Accenture plc

Deloitte Ireland LLP

PricewaterhouseCoopers Ireland

KPMG Ireland

Ernst & Young Ireland LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Grant Thornton Ireland appointed 12 new partners across advisory, tax and audit to expand leadership capacity and deepen sector coverage.

- February 2026: EY Ireland enlarged its Cork office to 30,000 square feet, lifting headcount to 420 to meet regional client demand for assurance, tax and consulting services.

- May 2025: Deloitte opened its new Belfast headquarters in the Ewart building and announced plans to hire 500 additional technology specialists over three years.

- March 2025: The Central Bank of Ireland released the modernized Consumer Protection Code, triggering one-year implementation programs across the financial sector.

Ireland Management Consulting Services Market Report Scope

The Ireland Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected value of the Ireland management consulting services market by 2031?

It is forecast to reach USD 3.63 billion by 2031, reflecting a 4.31% CAGR over 2026-2031.

Which consulting service line is expected to grow fastest through 2031 in Ireland?

Risk and Compliance Consulting is projected to post the strongest 4.72% CAGR because of EU AI Act, DORA and consumer-protection deadlines.

How are small and medium-sized enterprises influencing consulting demand?

Public grants and subsidized programs are lowering entry barriers, driving a 4.37% CAGR in SME consulting spend through 2031.

What delivery model is gaining momentum among Irish clients?

Hybrid engagements that blend onsite governance with remote execution are expanding quickest as firms seek resilience and talent flexibility.

Which end-user industry offers the most attractive growth outlook?

Healthcare shows the highest potential, supported by the Health Service Executive's plan to raise digital health spending to 4-6% of total health expenditure.

How concentrated is Ireland's consulting vendor landscape?

The top five firms control more than 80% of revenue, but growing boutique and platform competition is slowly diluting that dominance.

Page last updated on: