South Africa MVNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

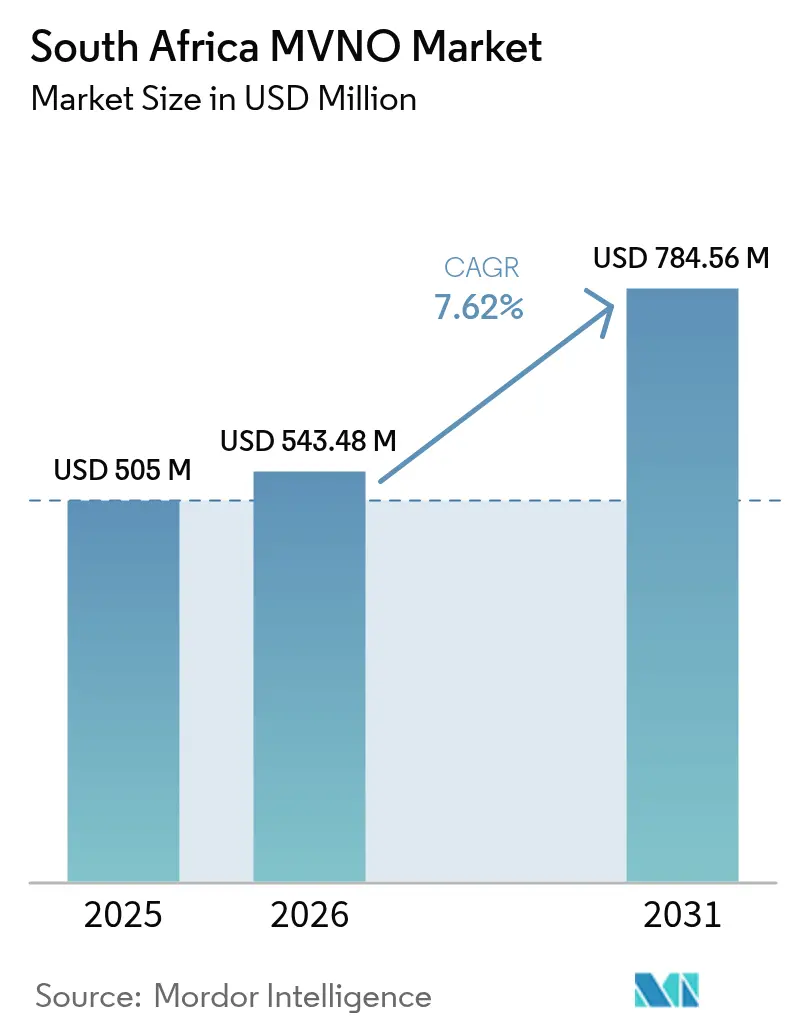

| Base Year Market Size (2025) | USD 505 Million |

| Market Size (2026) | USD 543.48 Million |

| Market Size (2031) | USD 784.56 Million |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa MVNO Market Analysis by Mordor Intelligence

The South Africa MVNO Market size in 2026 is estimated at USD 543.48 million, growing from 2025 value of USD 505 million with 2031 projections showing USD 784.56 million, growing at 7.62% CAGR over 2026-2031.

The trajectory reflects steady migration from generic voice-and-text propositions toward highly segmented offerings that emphasize banking integration, cloud-native operating stacks, and digital-first distribution. Ongoing spectrum liberalization by the Independent Communications Authority of South Africa (ICASA), together with Cell C’s wholesale-focused Virtual RAN arrangement, has lowered entry barriers and intensified competition. Banking-led brands are exploiting deep customer pools and loyalty programs to cross-sell mobile connectivity, while eSIM uptake is accelerating remote onboarding and cutting subscriber acquisition costs. Load-shedding headwinds and persistent data-to-income misalignment remain structural hurdles, yet operators are offsetting these pressures through diversified revenue models, differentiated value-added services, and expanded 4G/5G coverage footprints.

Key Report Takeaways

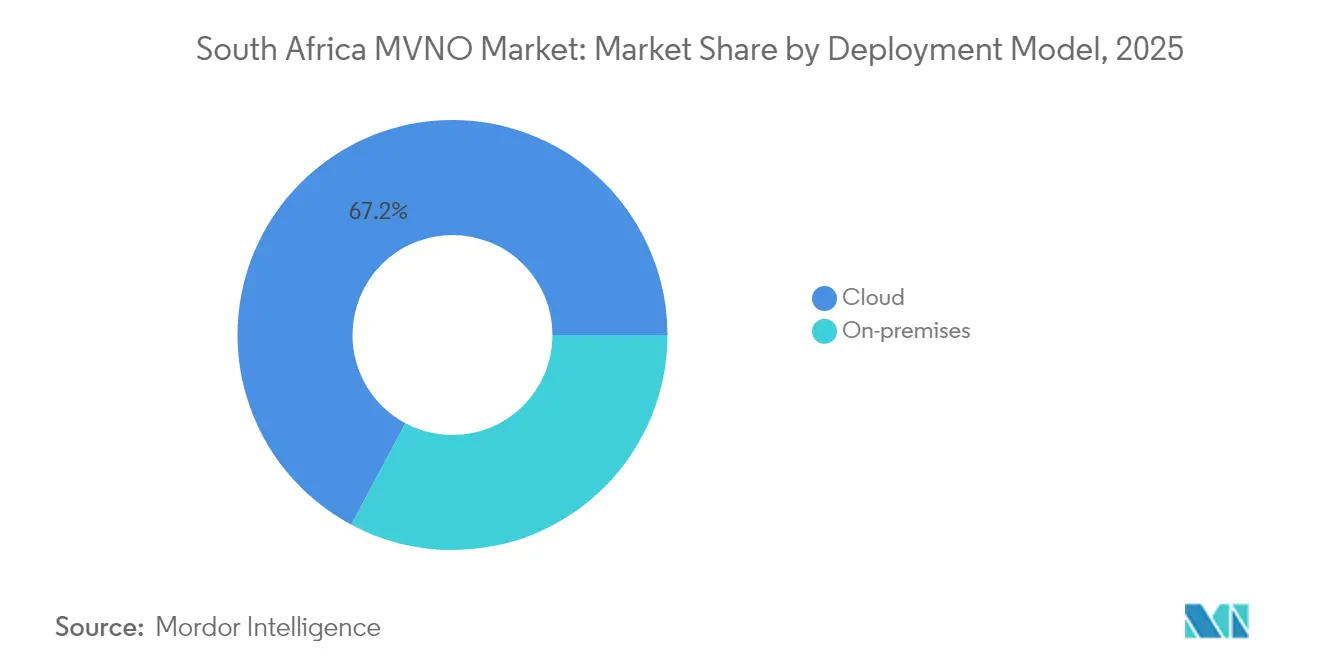

- By deployment model, cloud infrastructure led with 67.20% revenue share in 2025, while cloud-based services are growing at an 11.10% CAGR through 2031.

- By operational mode, Service Operator configurations accounted for 44.60% of the South Africa MVNO market share in 2025, while Full MVNO models are projected to grow fastest at 15.80% CAGR to 2031.

- By subscriber type, consumer plans captured 77.10% of the South Africa MVNO market size in 2025; IoT-specific connections are expanding at a 33.60% CAGR through 2031.

- By application, discount bundles held 47.30% of the South Africa MVNO market size in 2025, whereas cellular M2M links are forecast to accelerate at 23.40% CAGR.

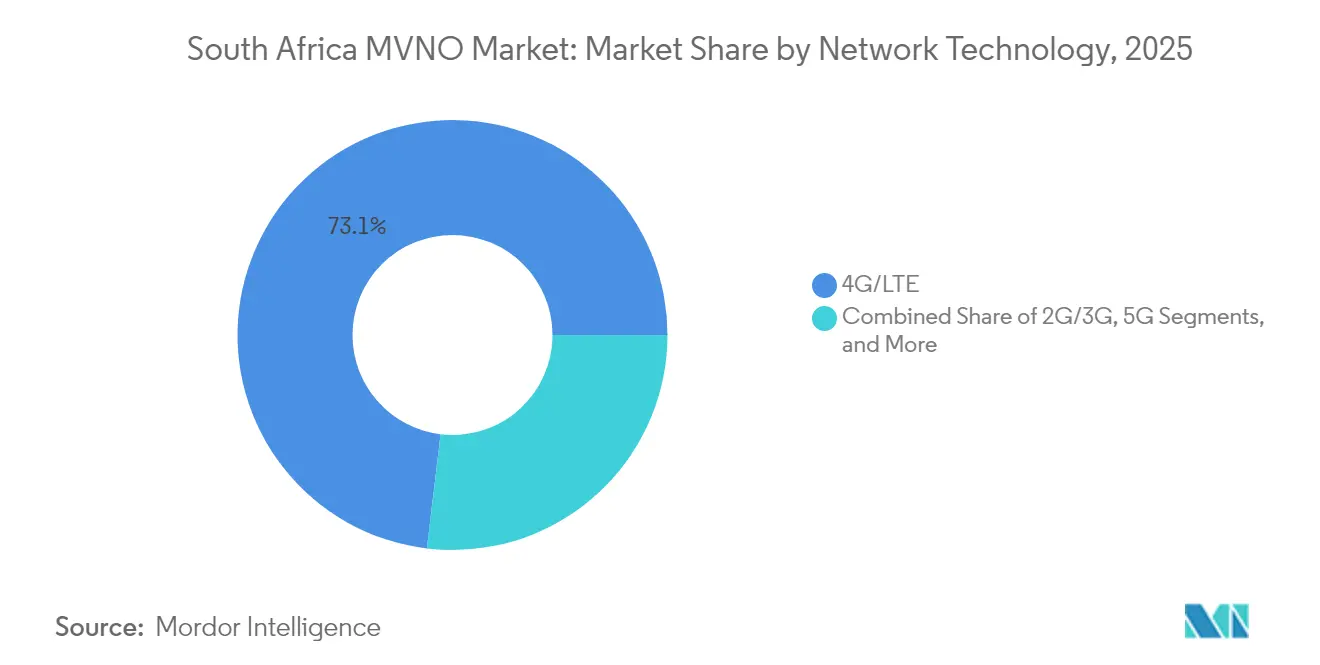

- By network technology, 4G/LTE still dominated with 73.10% share in 2025; 5G services are advancing at 36.10% CAGR toward 2031.

- By distribution channel, traditional retail outlets retained 41.70% share in 2025, but online-only channels are scaling fastest at a 17.20% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Banking-led MVNO bundling | +2.1% | Gauteng, Western Cape | Medium term (2–4 years) |

| ICASA licensing reforms and spectrum auctions | +1.8% | National | Long term (≥ 4 years) |

| Low-cost data demand | +1.5% | Rural provinces | Short term (≤ 2 years) |

| Cell C Virtual RAN wholesale access | +1.3% | National | Medium term (2–4 years) |

| 2G/3G switch-off drives IoT launches | +0.9% | Urban centers | Long term (≥ 4 years) |

| eSIM-enabled digital onboarding | +0.7% | Metro areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Banking-led MVNO Bundling Drives Subscriber Uptake

Financial institutions use established customer bases and rewards ecosystems to push mobile services, creating compelling cross-sell economics. Capitec Connect booked 1.3 million lines within two years, moving airtime worth ZAR 2 billion (USD 118 million) monthly through bank channels. FNB Connect broadened coverage by onboarding MTN alongside Cell C, boosting reliability and network reach. Generous cashback programs such as eBucks, offering up to 40% on mobile spend, deepen retention and encourage bundle uptake. Successes are prompting new entrants, with Old Mutual unveiling an MVNO ahead of its 2025 full-service bank launch. These moves validate the banking playbook as a dominant growth engine for the South Africa MVNO market.

ICASA Licensing Reforms and Spectrum Auction

ICASA’s March 2022 auction distributed prime 700 MHz and 3.5 GHz bands to six bidders, embedding mandated wholesale-access clauses that compel host MNOs to open networks to virtual operators. [1]“South Africa spectrum auction closes,” CMS Law-Now, cms.lawData-expiry rule amendments let MVNOs craft non-expiring and app-specific bundles, directly challenging incumbent value constructs. A parallel consultation on satellite and non-terrestrial networks signals regulatory foresight, ensuring future resilience. Open-access principles combined with infrastructure-sharing directives have shifted operator strategies toward wholesale monetization, underpinning the broader South Africa MVNO market expansion.

Low-Cost Data Demand Among Price-Sensitive Consumers

Mobile data prices fell 88% from 2005 to 2023, yet affordability gaps persist, especially in rural provinces where household income lags. [2]Paula Gilbert, “Data prices under pressure amid power cuts,” Connecting Africa, connectingafrica.com MVNOs exploit this gap with targeted discount bundles; Spot Mobile’s launch offered free ZAR 50 airtime for three months to hook Gen Z users. Prepaid orientation aligns with consumer cash-flow realities, while flexible micro-bundles address sporadic income patterns. Competitive pricing dynamics broaden addressable bases and buttress the South Africa MVNO market’s growth outlook.

Cell C Virtual RAN Wholesale Model Slashes CAPEX for Entrants

Cell C migrated to a Virtual RAN construct that taps MTN and Vodacom towers, giving MVNO partners access to roughly 28,000 sites without capital outlay. FNB Connect, Capitec Connect, Shoprite K’nect, and Mr Price Mobile all benefit from nationwide coverage and 5G readiness. The cost-light entry route accelerates time-to-market and underpins sustained growth momentum for the South Africa MVNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| QoS and pricing dependence on host MNOs | -1.4% | National | Medium term (2–4 years) |

| Persistently high data-to-income ratio | -1.1% | Rural provinces | Short term (≤ 2 years) |

| Load-shedding network disruptions | -0.9% | Industrial provinces | Short term (≤ 2 years) |

| Banking and POPIA compliance costs | -0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Load-Shedding Disruptions to Network Uptime

Rotational outages degrade tower uptime as batteries require 12–18 hours to recharge, yet blackouts often recur sooner. [3]Staff Reporter, “Load-shedding cripples cellular networks,” IOL, iol.co.zaVodacom and Cell C have diverted billions toward diesel generators and lithium-ion battery replacements, constraining innovation spend. MVNOs inherit these vulnerabilities but lack direct control over resilience capex, adding churn risk and tempering expansion velocity in the South Africa MVNO market.

Persistently High Data Pricing Versus Household Income

Fixed broadband averages ZAR 899 (USD 48) monthly, ranking 127th worldwide, while mobile tariffs threaten to climb on energy and inflation pressures. Wholesale rates do not always fall in tandem, squeezing MVNO margins. Operators increasingly rely on loyalty perks and bundled digital services rather than price cuts alone, yet affordability ceilings limit addressable segments outside high-income metros.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Accelerates Digital Transformation

Cloud-based configurations generated 67.20% of 2025 revenue and are compounding at 11.10% through 2031, underscoring the primacy of flexible, scalable architectures in the South Africa MVNO market size. Banking MVNOs derive particular advantage from seamless integration between mobile cores and fintech back-ends, expediting account-linked SIM activation. FNB Connect recorded a 169% rise in eSIM-enabled devices over three years, a milestone enabled by its cloud control plane.

Low infrastructure overhead improves margins, enabling sharper pricing and faster regional rollouts. Cloud schemes also ease regulatory compliance because data-sovereignty policies can be addressed through virtual geographic partitioning. Meanwhile, on-premise deployments persist in enterprise-grade use cases where sensory data residency drives procurement. Nevertheless, long-run consensus positions cloud as the default foundation for most new MVNO launches within the South Africa MVNO market.

By Operational Mode: Service Operator Leads, Full MVNO Picks Up Speed

Service Operator models retained 44.60% share in 2025, balancing control of numbering resources with lean infrastructure dependence. However, Full MVNO status—growing 15.80% CAGR—offers command over BSS/OSS stacks and pricing, a strategic imperative for brands seeking stronger differentiation. Melon Mobile’s shift toward MVNE capability via Amdocs illustrates maturation trends.

The South Africa MVNO market is thus bifurcating: established retail and bank entrants gravitate toward Full status to refine customer experience, while niche discounters stick with Service Operator arrangements for cost containment. ICASA preserves model plurality, sustaining vibrant competition across capital-risk appetites.

By Subscriber Type: Consumer Base Still Dominant but IoT Surges

Consumer lines represented 77.10% of active SIMs in 2025, powered by banking incentives and expansive retail footprints. Yet IoT endpoints are multiplying at a 33.60% CAGR, making them the fastest-expanding slice of the South Africa MVNO market. Vodacom’s NB-IoT overlay now spans 8,000 sites and 80% population coverage, creating fertile ground for meter-reading, asset-tracking, and agriculture sensors.

Consumer segment growth continues albeit hinging on richer digital bundles—streaming, micro-insurance, and instant credit—beyond base connectivity. Enterprise applications benefit from on-premise security guarantees, but IoT is poised to disrupt revenue mix as 2G/3G turndown compels device migration toward 4G and 5G modules, an inflection that elevates specialized IoT-centric MVNO propositions.

By Application: Discount Models Scale, M2M Unlocks Innovation

Price-led propositions commanded 47.30% revenue in 2025. Brands such as Spot Mobile captured urban youth with zero-expiry data top-ups, while Capitec Connect drew mainstream subscribers through competitive prepaid rates. Large customer volumes produce economies of scale, reinforcing discount model relevance in the South Africa MVNO market.

Cellular M2M, advancing 23.40% CAGR, fuels industrial digitization. Smart-grid rollouts, fleet telematics, and cold-chain monitoring require low-power, wide-area coverage, conditions met by NB-IoT and future RedCap standards. MVNOs that bundle connectivity with device management platforms and analytics dashboards are well positioned to monetize this uptick.

By Network Technology: 4G Present, 5G Future

4G/LTE accounted for 73.10% of 2025 SIMs, offering ample capacity for mainstream video and fintech applications. Yet 5G posts the steepest climb at 36.10% CAGR, spurred by mid-band spectrum allocations and aggressive rollouts that reached 50% population coverage by late 2024. Rain’s 5.5G testing signals a roadmap toward higher throughput and reduced latency that will benefit immersive services and enterprise private networks.

Legacy 2G/3G networks face a hard sunset by December 2027, prompting mass device replacements—an upside for IoT MVNOs that can orchestrate smooth migrations. Satellite and non-terrestrial networks remain niche but critical for deep-rural and maritime segments, expanding the diversity of the South Africa MVNO market.

By Distribution Channel: Brick-and-Mortar Persists, Digital Soars

Traditional retail maintained 41.70% share in 2025, reflecting consumer desire for physical assistance with SIM swaps and handset selection. Shoprite’s K’nect kiosks epitomize this reach, leveraging foot traffic to drive activations. Nonetheless, online-only sales logged a 17.20% CAGR, harnessing eSIM instant provisioning and app-based KYC to streamline onboarding in the South Africa MVNO market.

Hybrid strategies dominate: banks embed SIM sales in digital banking apps while offering branch support; fashion chains such as Mr Price rely on in-store displays augmented by QR-code activations. Third-party wholesalers complement coverage in peri-urban locales, ensuring nationwide availability across socio-economic cohorts.

Geography Analysis

Gauteng anchors the South Africa MVNO market, supported by the province’s concentration of corporate headquarters, financial institutions, and an 80% smartphone penetration rate. Bank-run brands use integrated app ecosystems to capture salaried urbanites, yielding superior average revenue per user. Western Cape ranks second, buoyed by tourism-driven demand and strong fiber backhaul that underpins high-capacity 4G/5G traffic. KwaZulu-Natal follows, where retail MVNOs like Mr Price and Shoprite leverage dense store networks to convert footfall into SIM activations.

Rural provinces such as Limpopo and Eastern Cape present untapped potential but are hampered by lower disposable incomes and sporadic network reliability. The 2G/3G shutdown slated for 2027 may initially disadvantage these areas; however, spectrum re-farm will ultimately enhance 4G coverage, improving service quality and paving the way for IoT deployments in agriculture and mining. Cell C’s Virtual RAN footprint, piggy-backing on MTN and Vodacom towers, now spans every district, mitigating historical geographic disparity and granting near-uniform network access to MVNO partners.

Provincial governments are incorporating mobile broadband into economic-development blueprints, especially in Free State and Northern Cape, where digital agriculture pilots rely on low-power IoT SIMs. ICASA enforces spectrum-sharing obligations consistently across provinces, though municipal approval times for tower upgrades differ, causing rollout timelines to vary. Overall, geography-based gaps are narrowing, but affordability divides persist, influencing segmentation strategies within the South Africa MVNO market.

Competitive Landscape

The South Africa MVNO market shows moderate concentration, anchored by Cell C’s wholesale dominance that hosts most high-profile brands. FNB Connect, Capitec Connect, and Standard Bank Mobile exemplify banking synergies, combining loyalty currencies and granular credit scoring to retain users. Retail giants Shoprite and Mr Price bring mass-market reach, pairing airtime sales with consumer-goods promotions.

Competitive levers emphasize customer experience over raw price: Capitec’s non-expiry data bundles tackle bill-shock; FNB exploits multi-network roaming for resilience; Shoprite ties SIM usage to grocery coupons. Technology partnerships are pivotal: Melon Mobile’s alignment with Amdocs delivers MVNE services to smaller entrants, while eSIM orchestration platforms shorten go-to-market cycles for new virtual brands.

The pending 5G investment cycle is shaping strategic alliances. Banks negotiate wholesale 5G rates with host MNOs to safeguard margins, whereas emerging IoT specialists seek sub-gigahertz spectrum slices to guarantee deep-indoor coverage. White-space opportunity remains in agriculture telemetry and low-tier urban youth segments, yet profitability demands lean cost structures and advanced customer analytics.

South Africa MVNO Industry Leaders

FNB Connect

Standard Bank Mobile

Capitec Connect

meandyou Mobile

Afrihost AirMobile

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Maziv achieved a USD 2 billion valuation after revising its fiber partnership with Vodacom, underscoring robust investor appetite for converged infrastructure.

- April 2025: Capitec Connect CEO confirmed rapid subscriber growth driven by value-based pricing.

- March 2025: Telkom announced a ZAR 6.75 billion (USD 360 million) tower sale to reallocate capital toward core mobile services .

- December 2024: eGroupX launched a fintech-integrated MVNO aimed at underserved consumers .

South Africa MVNO Market Report Scope

The MVNO South African market is being driven by increasing demand in a wide range of applications, like retail, cellular M2M, and media and entertainment. The scope of the study tracks the adoption of telecommunication services based on operational modes, such as reseller, service operator, and full MVNO. The study also focuses on the existing vendor landscape of mobile network operators and MVNO vendors, as well as their offerings.

The MVNO South African market is segmented by subscriber (enterprise and consumer). The market sizes and forecasts are provided in value terms (USD) for all the above segments.

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How will the 2027 2G/3G shutdown impact virtual operators?

The sunset will push IoT device migrations to 4G/5G, creating new opportunities for IoT-centric MVNOs but requiring proactive customer transition plans.

Which province currently generates the highest MVNO subscriber volume?

Gauteng leads, benefiting from its economic status, high smartphone adoption, and multiple banking-led MVNOs.

What share of deployments rely on cloud infrastructure?

Cloud models account for 67.20% of deployments, favored for their scalability, cost efficiency, and rapid integration capabilities.

How are power outages influencing MVNO operating costs?

Load-shedding compels host networks to invest heavily in backup power, costs that filter down to MVNOs through wholesale rate structures and service-level variability.

Page last updated on: