Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

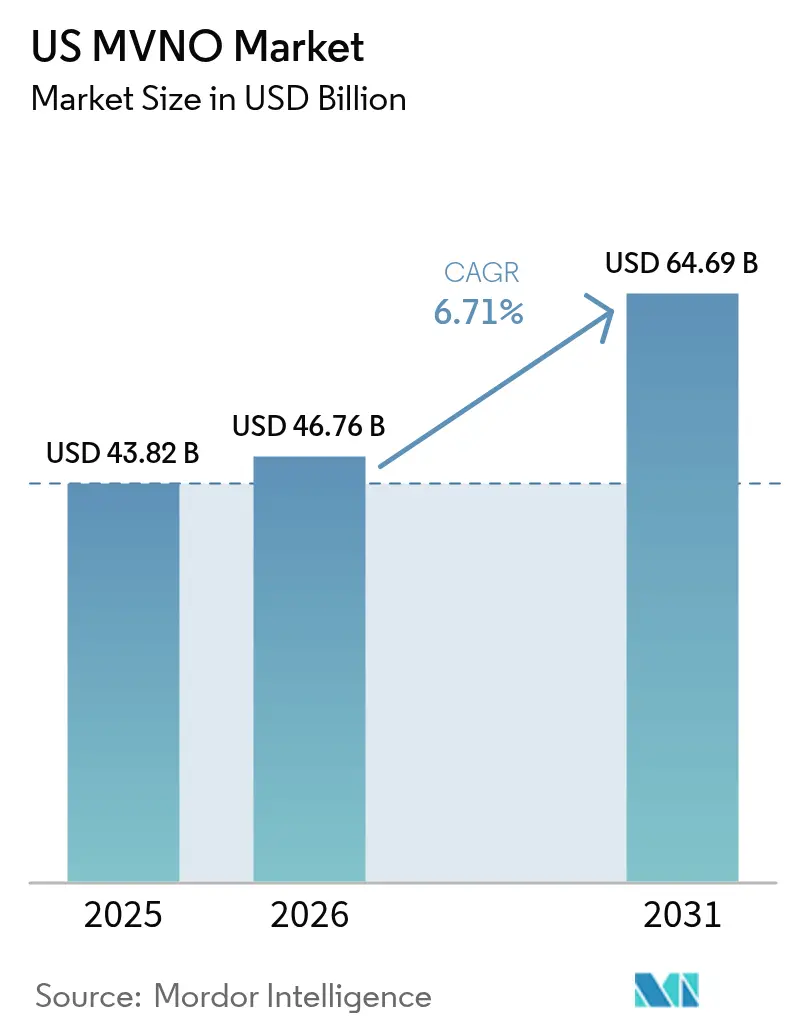

| Base Year Market Size (2025) | USD 43.82 Billion |

| Market Size (2026) | USD 46.76 Billion |

| Market Size (2031) | USD 64.69 Billion |

| Growth Rate (2026 - 2031) | 6.71% CAGR |

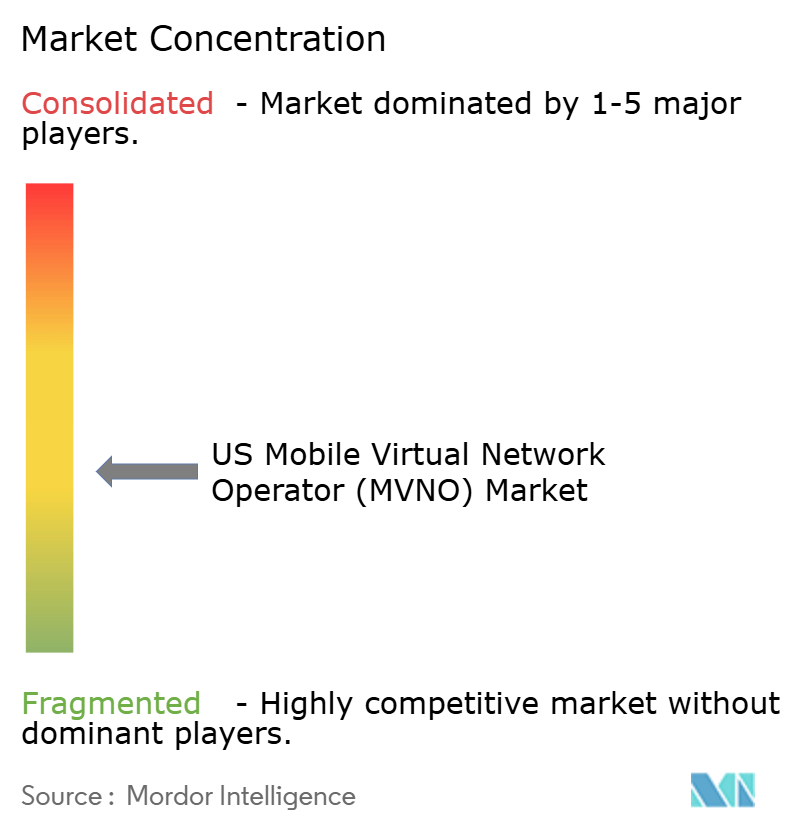

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US MVNO Market Analysis by Mordor Intelligence

The US MVNO Market size was valued at USD 43.82 billion in 2025 and estimated to grow from USD 46.76 billion in 2026 to reach USD 64.69 billion by 2031, at a CAGR of 6.71% during the forecast period (2026-2031).

Robust growth comes from sustained consumer appetite for lower-cost plans, enterprise outsourcing of IoT connectivity, and rapid cloud adoption that cuts time-to-market. Cable operators translate broadband strength into wireless cross-sell gains, while retailers launch eSIM-only brands that deepen digital engagement. Large carriers, worried about revenue dilution, counter with network slicing and strategic acquisitions that keep wholesale traffic—and profit streams—inside their own ecosystems. The steady influx of API-first wholesale platforms further flattens entry barriers and stimulates service innovation, ensuring that competitive pressure remains intense across every segment of the US MVNO market.

Key Report Takeaways

- By deployment model, cloud solutions led with 57.25% of US MVNO market share in 2025; the segment is advancing at a 12.89% CAGR through 2031.

- By operational mode, full MVNOs captured 45.30% of the US MVNO market size in 2025 and are progressing at a 10.73% CAGR to 2031.

- By subscriber type, consumer services commanded 73.20% share of the US MVNO market size in 2025 while IoT connectivity is expanding at a 16.95% CAGR through 2031.

- By network technology, satellite/NTN services are recording the fastest growth at a 63.20% CAGR through 2031 as operators diversify beyond terrestrial footprints.

- By distribution channel, digital-only sales accounted for 49.40% of the US MVNO market size in 2025 and are rising at a 11.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for budget-friendly wireless plans | 1.8% | National, with concentration in price-sensitive demographics | Short term (≤ 2 years) |

| 5G coverage expansion supporting MVNO feature parity | 1.5% | National, with urban markets leading adoption | Medium term (2-4 years) |

| Enterprise & IoT connectivity outsourcing to MVNOs | 1.2% | National, with enterprise hubs showing early adoption | Long term (≥ 4 years) |

| FCC pro-competition policies and wholesale mandates | 0.9% | National regulatory framework | Medium term (2-4 years) |

| Rise of eSIM-only digital brands launched by retailers | 0.8% | National, with tech-savvy demographics leading | Short term (≤ 2 years) |

| API-driven wholesale marketplaces lowering entry barriers | 0.6% | National, with technology centers as early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for budget-friendly wireless plans

Inflation keeps household budgets tight, pushing more consumers toward low-cost offerings in the US MVNO market. Operators answer with transparent, fee-free pricing that undercuts major carrier plans by 30–40%. Visible’s five-year USD 15 rate guarantee directly counters Mint Mobile’s headline promotions and illustrates how price competition now shapes brand perception. [1]“Visible sets price lock,” Verizon News Center, verizon.comBulk wholesale agreements, lean back-end operations, and digital onboarding let MVNOs preserve margins even while rates fall. Word-of-mouth referrals and flexible prepaid terms push churn down, reinforcing the cost advantage loop that sustains subscriber expansion.

5G coverage expansion supporting MVNO feature parity

Nationwide standalone 5G deployments erase the performance gap that once separated discount brands from network owners. Access to network slicing allows MVNOs to offer differentiated security, latency, and throughput tiers once reserved for direct carrier contracts. Feature parity reshapes competitive positioning: brands now lead with service innovation—gaming passes, AR perks, or bundled cloud storage—rather than apologizing for slower data. As device upgrade cycles accelerate, new 5G-only handsets default to eSIM provisioning, further smoothing customer migration to the US MVNO market.

Enterprise and IoT connectivity outsourcing to MVNOs

Manufacturers, logistics players, and utilities want a single pane of glass for thousands of sensors that cross domestic and international borders. Specialist MVNOs respond with bundled SIM management portals, pooled data allowances, and multi-network redundancy. Canada’s CRTC recently opened wholesale access for enterprise-grade MVNO services, underscoring regulatory endorsement of the model and signaling parallel momentum in U.S. policymaking. Satellite-cellular hybrids extend reach to remote mines and offshore platforms, turning connectivity into a strategic enabler of predictive maintenance and real-time analytics.

FCC pro-competition policies and wholesale mandates

The FCC’s proposed 60-day device-unlock rule cuts switching friction by ending long lock-in periods imposed by host carriers. [2]“Device unlocking proposal,” Federal Register, federalregister.govSupplemental coverage-from-space guidelines clarify spectrum and power limits, giving MVNOs legal footing to integrate satellite links. Regulators also continue to monitor wholesale pricing, deterring discriminatory on-net prioritization that could stifle MVNO competitiveness. These guardrails enlarge the addressable pool of switchers and trim entry risks for new brands, thus boosting growth prospects in the US MVNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Network deprioritization impacting perceived QoS | -1.4% | National, with congested urban areas most affected | Short term (≤ 2 years) |

| Price wars compressing already thin MVNO margins | -1.1% | National competitive landscape | Short term (≤ 2 years) |

| Rising digital-ad CAC for niche MVNO customer acquisition | -0.8% | National, with digital marketing channels affected | Medium term (2-4 years) |

| MNO 5G-SA slice-access lockouts limiting service innovation | -0.6% | National, with enterprise segments most impacted | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Network deprioritization impacting perceived QoS

Most wholesale contracts allocate QCI 9 during peak congestion, leaving subscribers with slower speeds than postpaid carrier users. Complaints of unusable data during city-center rush hours dent brand credibility, forcing US MVNO market players to double down on price or negotiate costly premium QCI 8 access. [3]“QCI and deprioritization explained,” Best Phone Plans, bestphoneplans.netVisible downtime in early 2025 and Mint Mobile’s intermittent throttling issues highlight how quickly social media amplifies negative user experiences. Unless MVNOs secure higher priority lanes or lean on satellite fallback, the gap between promise and reality could flare into churn spikes.

Price wars compressing already thin MVNO margins

Aggressive discounting has become a defensive reflex: when one provider unveils a USD 15 unlimited tier, rivals match within days. The resulting revenue squeeze is roughest on smaller entrants that lack scale purchasing power and must dig into marketing budgets to stay visible. Recent quarters show a 20% jump in average digital campaign costs for telecom keywords, shrinking contribution margins just as customer expectations for unlimited data harden. Deep pockets and diversified revenue streams give cable MVNOs and post-acquisition sub-brands more stamina, heightening survival risk for fringe players in the US MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Digital Transformation

Cloud deployments held a 57.25% share of the US MVNO market in 2025 and are growing at a 12.89% CAGR. These architectures strip away capex-heavy hardware and let operators scale subscribers in line with demand surges. Platform-as-a-Service offerings—such as ATandT’s MVNX stack—bundle billing, policy, and analytics into modular APIs that speed launch cycles from months to weeks. The shift lowers operating costs by up to 40%, freeing resources for marketing and feature development. On-premise solutions remain the pick for heavily regulated verticals, but their share erodes as cloud certifications expand. The flexibility of containerized microservices also future-proofs integrations with satellite gateways and IoT device clouds, positioning cloud MVNOs to capture the next wave of US MVNO market growth.

The cloud mindset fosters a fail-fast culture: brands A/B test plan mixes in real time, push over-the-air updates to companion apps, and surface churn-risk signals that prompt targeted retention offers. Data residency concerns, once a stumbling block, now find remedies in sovereign cloud zones that meet state privacy statutes. Early adopters report subscriber NPS gains after migrating to fully automated support chatbots anchored on cloud AI. Together, these factors make cloud operation the engine room of experimentation that keeps the US MVNO market vibrant and fiercely competitive.

By Operational Mode: Full MVNOs Assert Market Leadership

Full MVNOs represented 45.30% of US MVNO market share in 2025 and are expanding at a 10.73% CAGR. Ownership of core network elements lets these players customize rate plans, embed fintech add-ons, and harvest granular usage data that refines upsell algorithms. CompaxDigital’s BSS/OSS link-up with T-Mobile demonstrates the strategic tooling now available to brands that want deeper integration without building infrastructure from scratch. Light MVNOs still appeal when speed to launch outweighs differentiation needs, but price compression forces many to graduate toward full control as soon as subscriber bases hit breakeven scale.

Operational autonomy shields full MVNOs from abrupt wholesale policy changes, such as new throttling rules or SIM swap fees. It also simplifies multi-carrier negotiations, a critical advantage when bundling terrestrial and satellite links into single SKUs. As consumer acquisition costs rise, the value of owning cross-sell touchpoints—from device insurance to streaming bundles—climbs sharply, reinforcing the strategic migration toward full MVNO status in the US MVNO market.

By Subscriber Type: Consumer Dominance with IoT Acceleration

Consumers represented 73.20% of total lines in 2025, securing the revenue backbone of the US MVNO market. Sticky family plans drive low churn by pooling data and devices under single dashboards, while referral bonuses catalyze viral growth. Yet the IoT slice, advancing at a 16.95% CAGR, promises healthier margins and longer contract durations. Logistics firms deploy ruggedized trackers that ride on satellite fallback, paying premiums for uninterrupted coverage of cross-border fleets. Enterprises act as gateway customers, piloting connectivity bundles before scaling across global asset inventories. High-speed failover routers for branch retail also underpin the IoT surge, creating wide lanes of opportunity well beyond consumer phones.

This two-speed dynamic stabilizes cash flow: consumer plans supply predictable monthly ARPU, whereas IoT wins unlock lump-sum hardware revenues and multi-year service contracts. MVNOs that master dual go-to-market motions—TikTok ads for Gen-Z on one hand and channel partnerships with systems integrators on the other—will outpace the broader US MVNO market over the forecast horizon.

By Application: Discount Services Lead with M2M Innovation

Discount voice-and-data bundles retained 31.55% share in 2025, reflecting the price anchor that even premium brands must reference to stay competitive. However cellular M2M links are marching ahead at a 16.10% CAGR, energized by public-safety drones, smart-meter rollouts, and connected farm equipment. Business-grade subscriptions layer priority routing, static IPs, and dedicated support crews on top of baseline connectivity, addressing a willingness-to-pay gap that consumer segments cannot match. The most creative MVNOs wrap application-specific dashboards—fuel theft alerts for fleet managers, vacancy analytics for real-estate landlords—around the SIM, pushing the US MVNO market beyond raw bandwidth resale.

Regulatory initiatives that sunset 2G/3G finally nudge holdout industries to modernize devices, filling M2M order books. Meanwhile Web3-native MVNOs experiment with crypto-denominated micro-payments for tiny data bursts, hinting at future composability where connectivity becomes just one widget in a programmable value stack. Such experimentation underscores how rapidly use-case frontiers expand once API access democratizes core network functions.

By Network Technology: 4G Dominance with Satellite Disruption

4G/LTE still underpins 67.40% of active lines, favored for its mature handset ecosystem and stable wholesale economics. Yet satellite/NTN connectivity is the fastest riser, clocking a 63.20% CAGR. OQ Technology’s tie-in with Transatel on global 5G satellite IoT illustrates how orbital capacity is no longer a niche add-on but a strategic lever for ubiquitous coverage, especially across logistics corridors and disaster-response zones. Early consumer trials bundle text-only SOS messaging into mainstream plans, paving the way for fuller mobile-satellite convergence.

5G consumption grows steadily but trails initial hype; many subscribers cannot yet distinguish practical benefits over robust 4G, especially after cost-optimized cores deliver downlink speeds above 100 Mbps. As more mmWave small cells light up dense metros, MVNOs will cherry-pick slices for latency-sensitive gaming or VR, creating micro-segments that command premium pricing. By 2031 the US MVNO market will likely balance three pillars—enhanced LTE, flexible 5G, and global satellite—under a single billing roof.

By Distribution Channel: Digital-First Strategies Dominate

Digital-only storefronts accounted for 49.40% of subscriber additions in 2025 and are growing at a 11.98% CAGR. eSIM onboarding cuts SIM kit logistics, lets users activate within five minutes, and reduces first-month churn often triggered by port-in delays. Data-driven funnels leverage pixel-level attribution to refine creative, pushing CPA down even as broader ad rates rise. Physical retail hangs on by catering to seniors, corporate procurement officers, and tourists needing instant local numbers. Hybrid pop-up kiosks in big-box stores bridge both worlds, serving as high-touch demo zones that end with QR-code provisioning.

Chatbot-led support slashes call-center minutes, freeing headcount budgets for loyalty perks like bundled streaming or cloud games. As AI assistants mature, simple mid-tier plans will sell via conversational commerce embedded in social feeds, boosting reach to demographics that seldom visit traditional websites. The relentless digitization cycle cements self-service as the default customer expectation across the US MVNO market.

Geography Analysis

Regional penetration inside the US MVNO market maps tightly to population density, network congestion, and legacy broadband footprints. Urban cores such as New York and Los Angeles show churn toward premium MVNOs that negotiate QCI 8 lanes to keep video streams from buffering during rush hour. Rural zones across the Midwest and Mountain West represent latent growth pools unlocked by satellite-cellular hybrids that wipe out coverage dead spots. FCC guidance on supplemental space coverage clarifies technical coexistence with terrestrial bands, giving MVNOs legal confidence to advertise “nationwide—including remote areas” without caveats.

Cable MVNO performance skews heavily toward regions where the parent company already enjoys broadband scale. Comcast’s 1.2 million mobile line adds in Q4 2024 clustered in the Northeast and Pacific Northwest, demonstrating the potency of bundle discounts when home internet subscribers seek wireless savings. In contrast, primary-brand carrier sub-labels flourish in the Sun Belt, where population inflows create a steady stream of first-time customers.

State-level consumer-protection statutes also sway adoption. California’s strict bill-transparency rules favor MVNO offers with no fees, lifting brand trust scores. Meanwhile, the T-Mobile–UScellular transaction reshapes competitive intensity across the rural Upper Midwest, prompting local MVNOs to tout hometown customer service as differentiation. Collectively, these geographic nuances confirm that the US MVNO market is not monolithic; localized factors often outweigh national advertising in determining uptake rates.

Competitive Landscape

Competition in the US MVNO market blends scale power and niche agility. Top-line concentration remains moderate: the five largest brands combined controlled slightly above 55% of active lines in 2024. T-Mobile’s acquisitions of Mint Mobile and UScellular added more than 8 million users, narrowing the gap with Verizon-hosted sub-brands and immediately pressing smaller discount operators. Despite consolidation, new entrants appear each quarter thanks to turnkey MVNO-as-a-Service platforms that need minimal upfront capital.

Technology partnerships act as force multipliers. The Aduna network API exchange, endorsed by AT&T, Verizon, and T-Mobile, standardizes hooks into priority lanes, network analytics, and billing resources, allowing boutique brands to launch bespoke offers—say, unlimited gaming traffic with jitter guarantees—without negotiating bespoke contracts each time. Cable MVNOs lean on Wi-Fi offload to suppress variable wholesale costs, letting them bundle unlimited data at profit-friendly margins.

Strategic moves in 2025 underline a sharpened focus on enterprise and IoT. T-Mobile’s SIM-based SASE rolls security and connectivity into a single product, targeting mid-market businesses that lack dedicated IT teams. SurgePays aligns convenience-store footprints with low-income lifeline subsidies, capturing a demographic under-served by mainstream postpaid carriers. These examples illustrate how differentiation increasingly hinges on vertical integration—whether through spectrum, security, distribution, or localized engagement—rather than a race to the bottom on price alone.

US MVNO Industry Leaders

Tracfone Wireless

H2O Wireless

Visible

Mint Mobile

Consumer Cellular

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: T-Mobile completed its USD 4.3 billion acquisition of UScellular’s wireless operations, absorbing 4 million customers and 30% of the regional carrier’s spectrum.

- July 2025: Comcast reported record wireless growth, adding 378,000 lines and reaching 8.5 million total.

- May 2025: T-Mobile launched SIM-based SASE with dedicated network slices for zero-trust security.

- December 2024: SurgePays signed a multi-year 5G MVNO agreement with AT&T to serve rural communities.

US MVNO Market Report Scope

The United States MVNO market is defined based on the revenues generated from the MVNO operating models offered by the various players operating in the market across end-users. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The US MVNO Market is segmented by operating model (reseller, service operator, full MVNO, and other models), and by end user type (business and consumer). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Deployment Model

| Cloud |

| On-premise |

By Operational Mode

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

By Subscriber Type

| Consumer |

| Enterprise |

| IoT-specific |

By Application

| Discount |

| Business |

| Cellular M2M |

| Others |

By Network Technology

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

By Distribution Channel

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How big will the US MVNO market be in 2031?

Forecasts place it at USD 64.69 billion, up from USD 46.76 billion in 2026.

Which deployment model is growing fastest?

Cloud-based MVNO architectures are advancing at a 12.89% CAGR to 2031 on the back of scalability and lower capex.

What subscriber segment shows the highest growth?

IoT lines are increasing at a 16.95% CAGR as enterprises outsource device connectivity.

How are satellite networks affecting MVNO offers?

Satellite/NTN links are rising at a 63.20% CAGR, extending coverage to rural and remote zones without terrestrial service.

Why are full MVNOs gaining traction?

Control over core elements lets brands craft custom pricing, embed value-added features, and capture detailed usage data for targeted upselling.

What role do FCC policies play in MVNO growth?

Device-unlock mandates and transparent wholesale rules reduce switching friction and level the playing field for new entrants.

Page last updated on: