Size and Share of Australia Mobile Virtual Network Operator (MVNO)

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

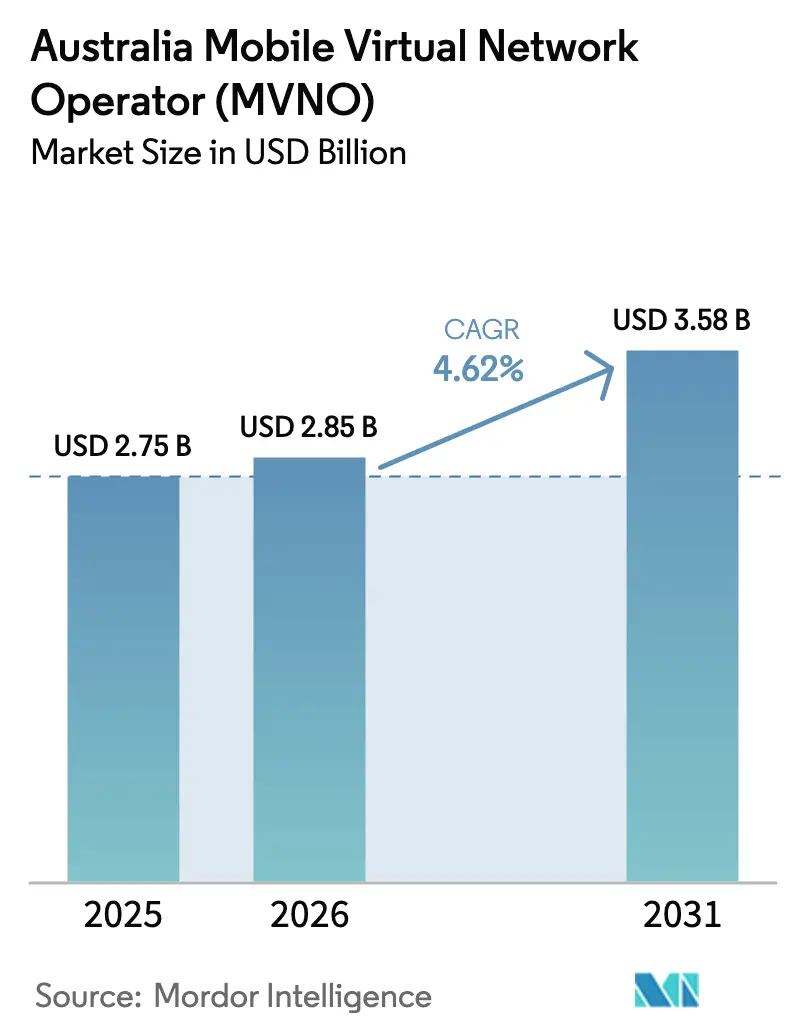

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 3.58 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

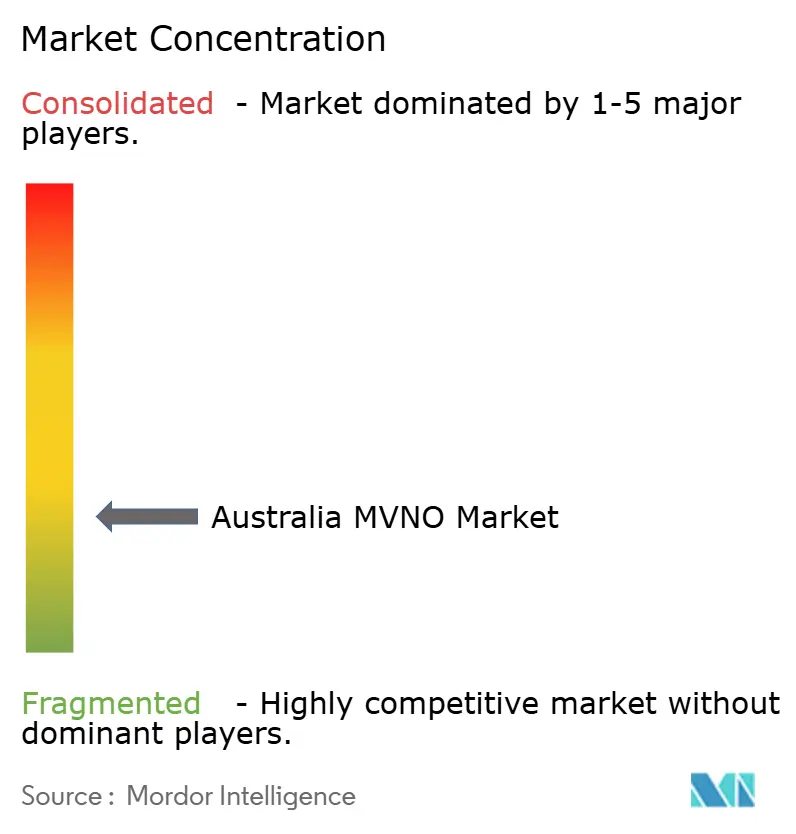

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Australia Mobile Virtual Network Operator (MVNO) by Mordor Intelligence

The Australia Mobile Virtual Network Operator (MVNO) market size was valued at USD 2.75 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 3.58 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). Solid demand for lower-priced mobile plans, newly opened 5G wholesale access, rapid e-SIM uptake, and aggressive retail-brand bundling are widening the addressable base for digital-only and grocery-anchored virtual operators. Consolidation among large independents, tighter fraud-mitigation regulation, and spectrum-related cost pass-through threats from the three incumbent mobile network operators are reshaping competitive tactics. Cloud-native core deployments already account for more than half of MVNO revenue, allowing light and brand MVNOs to launch new offers in weeks, while full MVNOs defend their higher-margin enterprise and IoT niches by exploiting network-slicing and private-5G features. Direct-to-device satellite pilots highlight the upside of future rural coverage, but meaningful revenue will not materialize before 2027. Across segments, operators that balance price leadership with a digital customer experience stand to capture incremental share as households and enterprises seek value amid a prolonged cost-of-living squeeze.

Key Report Takeaways

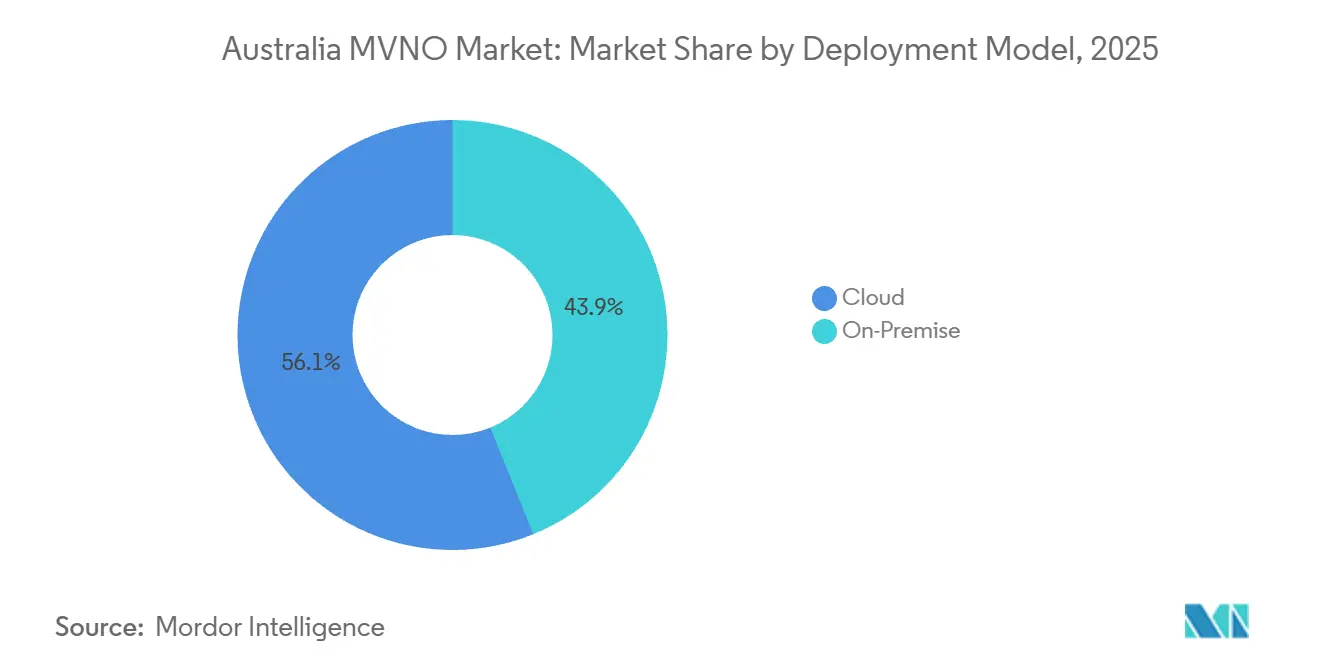

- By deployment model, cloud platforms generated 56.14% revenue in 2025, and is projected to expand at 5.32% CAGR to 2031.

- By operational mode, full MVNOs held 48.37% of Australia Mobile Virtual Network Operator (MVNO) market share in 2025, but light and brand MVNOs are advancing at a 5.63% CAGR through 2031.

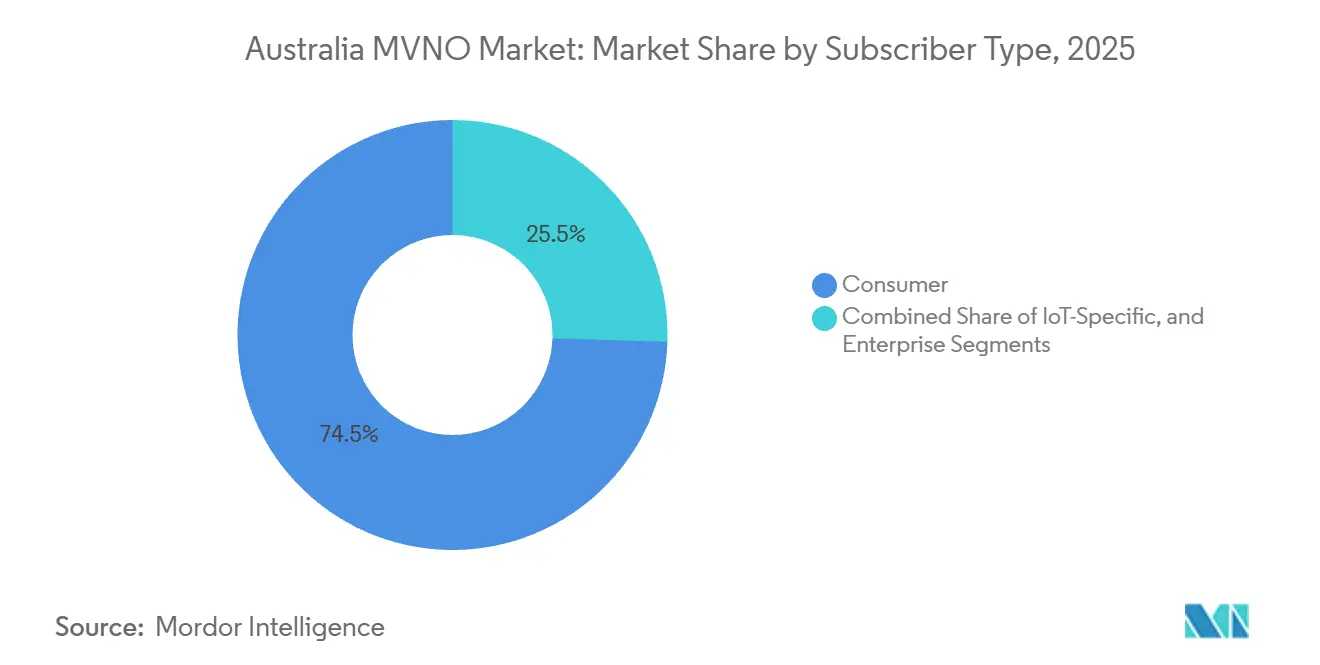

- By subscriber type, consumer lines represented 74.49% of market share in 2025, whereas IoT-specific services are projected to expand at 5.74% CAGR to 2031.

- By application, discount plans led with 32.71% of the Australia Mobile Virtual Network Operator (MVNO) market size in 2025, and cellular M2M posts the fastest 6.22% CAGR outlook.

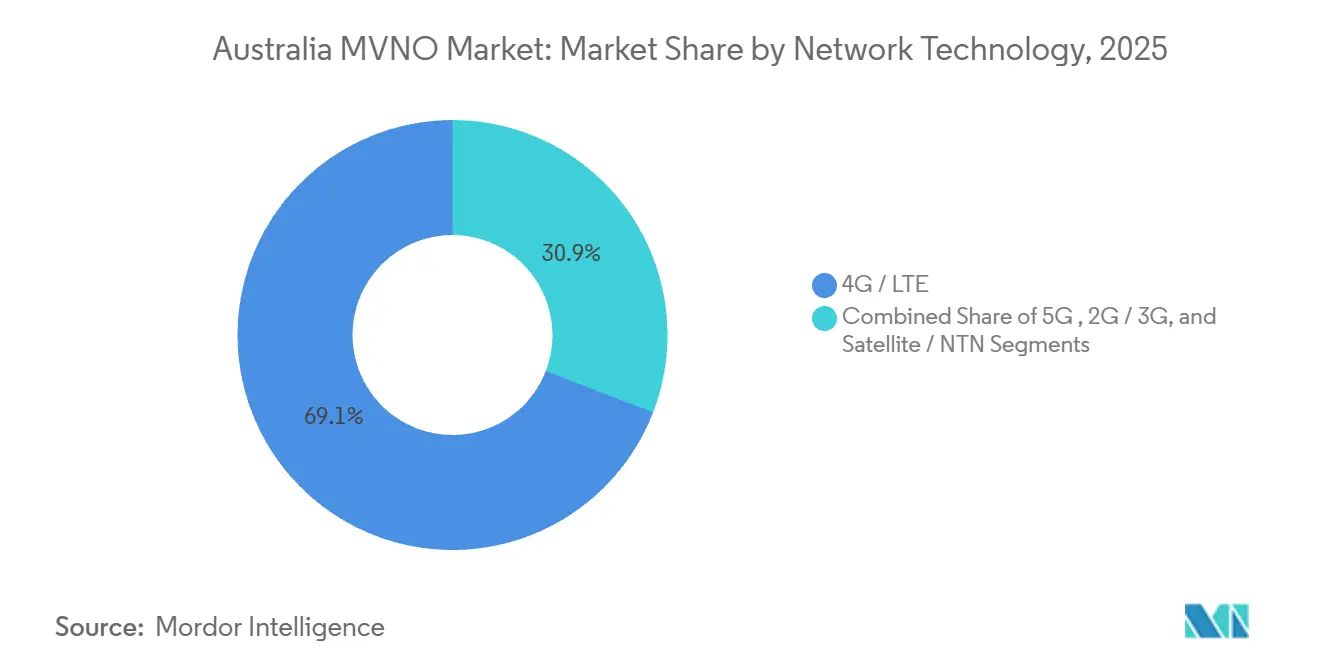

- By network technology, 4G and LTE accounted for 69.14% traffic in 2025, but 5G usage is climbing at a 5.41% CAGR.

- By distribution channel, online and digital-only channels captured 48.37% 2025 activations and are growing at a 5.89% CAGR on the back of e-SIM instant provisioning.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Australia Mobile Virtual Network Operator (MVNO)

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G Wholesale Agreements with MNOs | +1.2% | National, with early gains in Sydney, Melbourne, Brisbane metro clusters | Medium term (2-4 years) |

| Surge in E-SIM Adoption Enabling Digital-Only Onboarding | +1.0% | National, accelerated in urban digital-first demographics | Short term (≤ 2 years) |

| Growing Demand for Budget-Friendly Mobile Plans | +0.9% | National, concentrated in cost-sensitive suburban and regional households | Short term (≤ 2 years) |

| Retail-Brand Bundling of Mobile with Groceries and Loyalty | +0.6% | National, strongest in Woolworths and Coles footprint regions | Medium term (2-4 years) |

| AI-Driven Customer Service Lowering Churn | +0.5% | National, led by digital-only MVNOs with cloud contact centers | Medium term (2-4 years) |

| Private-Network and Slicing Opportunities for Enterprises | +0.4% | National, early adoption in logistics, mining, utilities sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G Wholesale Agreements with MNOs

Optus opened standalone 5G access to wholesale partners in June 2025, giving MVNOs lower latency and higher throughput that support premium tiers such as cloud gaming and industrial automation.[1]Sean Mitchell, “Optus opens 5G standalone fixed wireless access to MVNOs,” channellife.com.au The AUD 1.59 billion Optus-TPG co-location deal widened rural coverage, letting discount MVNOs enter regions historically uneconomic for virtual players. Telstra’s Dynamic 5G slicing went live the same month, offering enterprise MVNOs guaranteed QoS, opening high-margin mission-critical use cases. Long-term wholesale renewals, such as Aussie Broadband’s five-year Optus extension, reduce supply risk and spur service innovation. As a result, performance parity between MNO retail and MVNO wholesale offerings is narrowing, forcing incumbents to differentiate on ecosystem integration instead of raw network exclusivity.

Surge in E-SIM Adoption Enabling Digital-Only Onboarding

App-based QR activation reduces onboarding time from days to minutes, slashing acquisition costs by up to 40% and enabling operators to scale nationally without physical distribution.[2]Telstra Wholesale, “MVNO strategy brief,” telstrawholesale.com.au Digital-only brands Felix Mobile, Gomo, and Amaysim already default to e-SIM, while More Telecom pioneered shared-number smartwatch plans that unlock new device categories. Telna’s USD 100 million fund for travel e-SIM brands signals accelerating capital inflows into e-SIM-native models. Regulatory caps on permanent roaming are pushing foreign aggregators to obtain local MVNO licences, advantaging Australia-based operators with compliant interception systems. Over-the-air provisioning likewise lowers IoT lifecycle costs, catalyzing fleet and utility deployments that require massive device footprints.

Growing Demand for Budget-Friendly Mobile Plans

MVNO penetration rose from 17% in 2021 to 19% in 2025, adding roughly 700,000 subscribers as households chased 20-40% lower monthly charges versus incumbent brands. Despite a 13.3% rise in median MVNO prices during 2023-2024, the gap to MNO tariffs persists, sustaining the value proposition. UBS expects Telstra and TPG to lift postpaid prices by up to 4.5% in July 2026, creating an umbrella under which MVNOs can hold rates steady and scoop up churned customers. Usage analytics show average data consumption of 14 GB, while allowances top 68 GB, proving that many consumers over-buy and are receptive to “right-sized” MVNO bundles. Brands such as Lebara and Lycamobile tailor international calling and long-expiry options to migrants with variable incomes, widening segment reach.

Retail-Brand Bundling of Mobile with Groceries and Loyalty

Woolworths Mobile grants Everyday Rewards members up to AUD 50 monthly grocery savings linked to active phone plans, effectively subsidizing service cost and cementing cross-category loyalty. The retailer’s 10 million-plus loyalty base delivers a vast funnel that traditional telcos lack, and in-store activations boast minimal incremental marketing spend. Coles Mobile tested similar vouchers but withdrew the program, illustrating that sustained analytics and offer personalization are prerequisites for grocery-telco synergies. Aldi Mobile benefits from high-traffic check-outs yet still operates without a formal points program, leaving upside for deeper integration. Consumer advocates warn that data-driven cross-selling may blur price transparency, attracting regulatory scrutiny. In practice, retail brands leverage grocery margins to fund telco discounts, building a formidable moat against standalone MVNOs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price Wars Compressing ARPU | -0.8% | National, most acute in prepaid and discount segments | Short term (≤ 2 years) |

| Regulatory-Mandated Network Coverage Obligations | -0.5% | National, with disproportionate impact on regional wholesale pricing | Medium term (2-4 years) |

| Scarcity of Spectrum Access for Stand-Alone IoT MVNOs | -0.3% | National, limiting dedicated IoT network economics | Long term (≥ 4 years) |

| Rising Fraud and SIM-Swap Security Costs | -0.2% | National, concentrated in digital-only onboarding channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Wars Compressing ARPU

While MVNO median tariffs increased during 2023-2024, they still trail MNO hikes, pushing virtual brands to chase share via headline data allowances rather than sustainable margins. Optus disclosed a blended ARPU of AUD 33 per month, yet discount MVNO plans sit below AUD 30, leaving little headroom for further cuts. Grocery-anchored operators can partly offset losses through basket uplift, whereas digital-only MVNOs must absorb shrinking per-user revenue or rely on costly promotions. The prepaid segment’s near-zero switching friction amplifies elasticity, leading to repeated flash sales that lengthen the payback on acquisition spend. As incumbents test premium-tier pricing in mid-2026, virtual brands face a prisoner's dilemma; hold rates and harvest churn or match increases and risk share stagnation.

Regulatory-Mandated Network Coverage Obligations

ACMA’s proposed AUD 7.3 billion spectrum renewal fee could raise wholesale access prices if MNOs recover outlays through back-ended charges.[3]Ronald Mizen, “Telstra warns of higher mobile bills,” afr.com Consumer advocates want discounted licences tied to rural build mandates, a condition that would swell capital budgets and dampen wholesale capacity. The Universal Outdoor Mobile Obligation, slated for 2027, compels carriers to light up remote areas that deliver marginal returns, risking tiered pricing schemes that penalize discount MVNOs with rural user bases. OECD pressure for a fourth facilities-based entrant might fragment wholesale supply and force MVNOs to renegotiate with a greenfield network lacking scale. Collectively, these mandates introduce cost volatility and planning uncertainty for MVNO wholesalers and resellers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Platforms Accelerate Time-To-Market

Cloud-native architectures accounted for 56.14% of 2025 revenue, and are projected to expand at 5.32% CAGR to 2031, underlining their role as the largest slice of the Australian Mobile Virtual Network Operator (MVNO) market. Elastic scaling and pay-as-you-grow billing allow light operators to avoid heavy capital lock-ins, a decisive edge when launching flash campaigns or seasonal travel e-SIM bundles. Public cloud functions integrate easily with fraud-detection APIs and AI chatbots, enhancing the customer experience. A seven-year, USD 700 million Telstra-Accenture AI program further validates cloud as the bedrock for hyper-personalized services.

On-premise cores remain critical for regulated verticals that demand data sovereignty, lawful intercept, and deterministic routing. Consequently, hybrid topologies are gaining favor; MVNOs externalize non-sensitive workloads while housing authentication and billing in private racks. This balanced approach minimizes latency and regulatory exposure without sacrificing launch agility. With hyperscalers pledging local-zone expansions, the cloud share of Australia Mobile Virtual Network Operator (MVNO) market size is set to climb steadily through 2031.

By Operational Mode: Light MVNOs Capture Capex-Light Growth

Full MVNOs controlled 48.37% of Australia Mobile Virtual Network Operator (MVNO) market share in 2025, buoyed by enterprise and IoT deals that reward infrastructure ownership. Telstra’s Boost buyout removed a full MVNO challenger, underscoring the incumbent's appetite for vertical integration. Yet light and brand MVNOs are pacing a 5.63% CAGR, reflecting demand for fast, low-risk market entry. Capital-light entities leverage pre-integrated billing from host networks, letting retailers, neobanks, and fintech super-apps bolt on connectivity within months.

Regulatory moves that tighten KYC oversight favor full MVNOs capable of end-to-end identity control, but compliance SaaS vendors are closing the gap for light models. M&A remains a growth lever; Amaysim’s Circles. Life asset purchase added 150,000 subs and deeper Optus roots. Looking ahead, mixed portfolios in which a parent firm runs separate full and light brands could become common, allowing strategic segmentation without duplicating heavy infrastructure.

By Subscriber Type: IoT Overtakes Consumer Growth Pace

Consumer lines still dominate, comprising 74.49% connections and underpinning mass prepaid volumes across Aldi Mobile, Kogan Mobile, and Woolworths Mobile. Nevertheless, IoT connections are the fastest-growing slice of the Australia Mobile Virtual Network Operator (MVNO) market, forecast to expand at 5.74% CAGR. Telstra’s 5.6 million IoT SIMs and USD 93 million half-year revenue confirm sustained enterprise appetite.

Enterprise mobility services, sold by Vocus and Aussie Broadband, mix business voice, UC, and managed mobile device fleets. Yet the richest upside lies in private 5 G and network slicing deployments, where multi-year contracts, low churn, and device stickiness boost lifetime value. As 3G sunsets recede, freed spectrum and 5G densification further tilt the economics toward high-density sensor rollouts across agriculture, logistics, and utilities.

By Application: Cellular M2M Leads Future Upside

Discount voice-data bundles held 32.71% revenue in 2025, underscoring their status as the largest application pocket within the Australia Mobile Virtual Network Operator (MVNO) market size. However, cellular M2M’s 6.22% CAGR through 2031 makes it the clear growth spearhead. Logistics firms, utility meters, and on-farm telemetry crave low-latency, low-power links that MVNOs can supply at scale.

Business and retail bundles draw strength from cross-selling; Aussie Broadband folds mobile into fixed fibre while Woolworths Mobile leverages grocery rewards. Streaming and content plays remain experimental, yet Optus’s Perplexity partnership offers a blueprint for value-added digital services. For migrant-focused plans, e-SIM travel bundles threaten traditional calling card economics, pushing incumbents like Lycamobile to simplify SKUs and expand digital sign-ups.

By Network Technology: 5G Deficit Narrows Fast

4G/LTE shouldered 69.14% 2025 traffic, reflecting broad device ubiquity. Standalone 5G wholesale, now accessible on Optus and Telstra cores, is narrowing the quality gap and enabling MVNOs to pitch premium speed tiers. Australia Mobile Virtual Network Operator (MVNO) market share for 5G lines will climb as enterprise slices proliferate and affordable 5G handsets permeate prepaid racks.

Legacy 2G/3G sunsets in 2024 forced 740,000 devices onto VoLTE, cutting support costs and releasing capacity for 5G densification. Satellite-to-device pilots, though commercially limited until 2027, promise future rural redundancy layers. Operators that secure early non-terrestrial wholesale rights could lock in a unique coverage differentiator.

By Distribution Channel: Digital-Only Outruns Brick-And-Mortar

Digital-only activations accounted for 48.37% of 2025 sign-ups, driven by app onboarding, e-SIM scanning, and AI chat support. Felix Mobile, Gomo, and Yomojo prove that a lean tech stack can scale national footprints devoid of storefront leases. Australia Mobile Virtual Network Operator (MVNO) market size captured through online channels is growing at 5.89% CAGR, the highest among distribution modes.

Retail chains still matter for in-person service and impulse prepaid top-ups. Optus’s January 2026 decision to in-house 100% of stores signals renewed faith in controlled physical footprints after compliance setbacks. Grocery aisle SIM racks offer cost-effective reach, but even those programs increasingly direct shoppers to self-service apps upon first recharge, blending offline discovery with online lifecycle management.

Geography Analysis

Metropolitan clusters such as Sydney, Melbourne, Brisbane, and Perth anchor subscription volumes due to dense populations, robust 5G rollouts, and high smartphone ownership. The Optus-TPG co-location pact, worth AUD 1.59 billion, broadened regional coverage and unlocked new prepaid audiences in inner regional corridors. ACMA’s forthcoming Universal Outdoor Mobile Obligation will force deeper remote builds; MVNOs hosting on Telstra or Optus could inherit cost-reflected wholesale surcharges that pressure rural pricing.

Suburban and regional households drive visible penetration gains as cost-of-living pressures intensify, aligning with Roy Morgan’s 700,000 net MVNO subscriber additions between 2021 and 2025. Grocery-anchored brands mirror supermarket catchments, skewing toward commuter belts where Woolworths and Coles maintain high outlet density. Digital-only MVNOs stay urban-leaning, capitalizing on fiber backhaul density and app literacy.

Satellite direct-to-device pilots promise remote safety coverage beyond terrestrial coverage, especially in mining-rich Western Australia and in inland agricultural zones. Private 5G networks led by Orro and the CID-Nokia-Pivotel trio target resource precincts in Queensland and the Northern Territory. Vocus leverages city fiber nodes to upsell business mobile in Sydney, Melbourne and Brisbane. Regional expansion risks include potential spectrum fee pass-throughs and the uncertainty of a prospective fourth network licensee reshaping wholesale terms.

Competitive Landscape

More than 20 active brands split 19% of national mobile services, making the Australia Mobile Virtual Network Operator (MVNO) market fragmented. Incumbent mobile network operators are vertically integrating; Telstra acquired Boost Mobile for USD 67 million, removing an independent full MVNO and retaining subscribers under a sub-brand umbrella. Optus folded Circles. Life’s customer base is incorporated into its retail operation, trimming external wholesale leakage.

Independent MVNO consolidation is accelerating. Aussie Broadband’s USD 77 million purchase of AGL’s telco assets added 250,000 services, turning scale into better wholesale bargaining power. Tangerine’s acquisition of numobile, plus Lycamobile’s double-digit activation surge after product simplification, show nimble operators can still gain ground by tightly managing brand portfolios.

Technology is now a decisive battleground. Telstra’s OpenAI contact-center summarization shaved 30-60 seconds per call, while Optus’s AI Concierge cut human enquiries by 15%, demonstrating cost and satisfaction gains from automation. Retail-brand operators wield grocery loyalty data to subsidize airtime, an advantage that standalone digital players cannot easily replicate. IoT-focused newcomers such as Vocus and Orro differentiate through private-network expertise rather than mass prepaid volume, targeting high-margin verticals that incumbents have not fully monetized.

Leaders of Australia Mobile Virtual Network Operator (MVNO)

ALDImobile

Kogan Mobile

Boost Mobile Pty Ltd

Amaysim Australia Ltd

TPG Telecom Ltd (iiNet, TPG Mobile)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aussie Broadband acquired AGL’s mobile and internet business for AUD 115 million (USD 77 million), adding 250,000 services.

- February 2026: Telstra warned that the proposed AUD 7.2 billion spectrum renewal fee would lift consumer mobile bills.

- February 2026: Telna launched a USD 100 million fund for travel e-SIM and MVNO projects.

- January 2026: OECD urged Australia to reserve spectrum for a fourth mobile operator to spur competition.

- January 2026: Optus said it will buy back all franchised stores nationwide after a regulatory fine.

Scope of Report on Australia Mobile Virtual Network Operator (MVNO)

The MVNOs market is defined based on the revenues generated from the services that are being used by various end-users across Australia. The analysis is based on market insights from secondary and primary research. The market also covers the major factors impacting its growth, including drivers and restraints.

The Australia MVNO Industry Report is Segmented by Deployment Model (Cloud, and On-Premise), Operational Mode (Reseller, Service Operator, Full MVNO, and Light/Brand MVNO), Subscriber Type (Consumer, Enterprise, and IoT-Specific), Application (Discount, Business, Cellular M2M, Media and Entertainment, Retail, Roaming, Migrant, and Telecom Wholesale), Network Technology (2G/3G, 4G/LTE, 5G, and Satellite/NTN), and Distribution Channel (Online/Digital-Only, Traditional Retail Stores, Carrier Sub-Brand Stores, and Third-Party/Wholesale). Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-Specific |

| Discount |

| Business |

| Cellular M2M |

| Media and Entertainment |

| Retail |

| Roaming |

| Migrant |

| Telecom Wholesale |

| 2G / 3G |

| 4G / LTE |

| 5G |

| Satellite / NTN |

| Online / Digital-Only |

| Traditional Retail Stores |

| Carrier Sub-Brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-Premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-Specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Media and Entertainment | |

| Retail | |

| Roaming | |

| Migrant | |

| Telecom Wholesale | |

| By Network Technology | 2G / 3G |

| 4G / LTE | |

| 5G | |

| Satellite / NTN | |

| By Distribution Channel | Online / Digital-Only |

| Traditional Retail Stores | |

| Carrier Sub-Brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the Australia Mobile Virtual Network Operator (MVNO) market today?

The market reached USD 2.85 billion in 2026 and is on track for USD 3.58 billion by 2031.

What is driving MVNO subscriber growth in Australia?

Lower prices, e-SIM adoption, and 5G wholesale access are attracting consumers and enterprises away from incumbent mobile network operators.

Which MVNO segments are expanding fastest through 2031?

Cellular M2M and IoT-specific services show the highest forecast CAGRs at 6.22% and 5.74% respectively.

How are grocery retailers influencing the MVNO landscape?

Woolworths Mobile, Coles Mobile and Aldi Mobile bundle phone plans with loyalty rewards, cutting acquisition costs and deepening customer retention.

What regulatory changes could impact MVNO economics?

Proposed spectrum renewal fees and mandatory rural coverage obligations may raise wholesale costs, while biometric KYC rules add compliance burden.

Where will 5G make the biggest difference for MVNOs?

Standalone 5G and network slicing unlock premium enterprise applications such as autonomous logistics and remote industrial control.

Page last updated on: