Oman MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

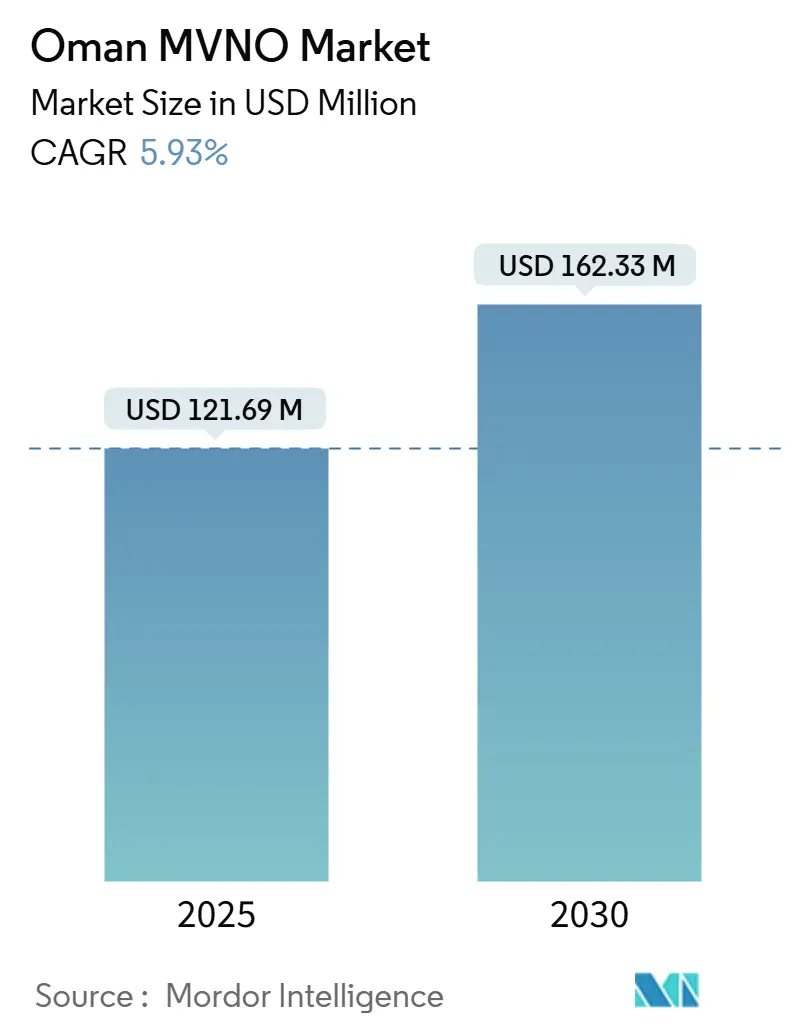

| Market Size (2025) | USD 121.69 Million |

| Market Size (2030) | USD 162.33 Million |

| Growth Rate (2025 - 2030) | 5.93% CAGR |

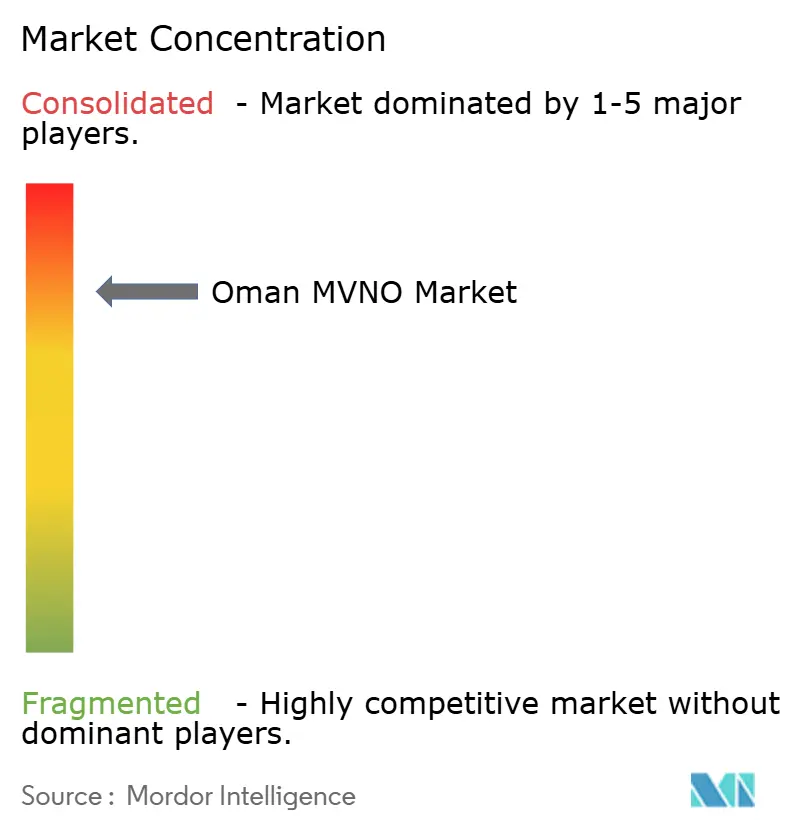

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman MVNO Market Analysis by Mordor Intelligence

The Oman MVNO Market size is estimated at USD 121.69 million in 2025, and is expected to reach USD 162.33 million by 2030, at a CAGR of 5.93% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 266.81 thousand subscriber in 2025 to 334.69 thousand subscriber by 2030, at a CAGR of 4.64% during the forecast period (2025-2030).

Scale is shifting from infrastructure build-outs toward service-based differentiation, a change enabled by the Telecommunications Regulatory Authority’s (TRA) streamlined Class II licensing and Oman Vision 2040’s digital priorities. Incumbent operators still rely on on-premise systems, yet cloud-native architectures are gathering pace as mobile virtual network operators (MVNOs) pursue faster onboarding, lower capital intensity, and data-driven product design. Demand is anchored in a large expatriate prepaid base that favors discount propositions, while enterprise appetite for 5G, eSIM, and IoT subscriptions is unlocking higher-value niches. Competitive intensity is moderate, ruled by FRiENDi Mobile, Renna Mobile, and a handful of new entrants, but wholesale access conditions remain the key constraint that shapes pricing flexibility and service innovation.

Key Report Takeaways

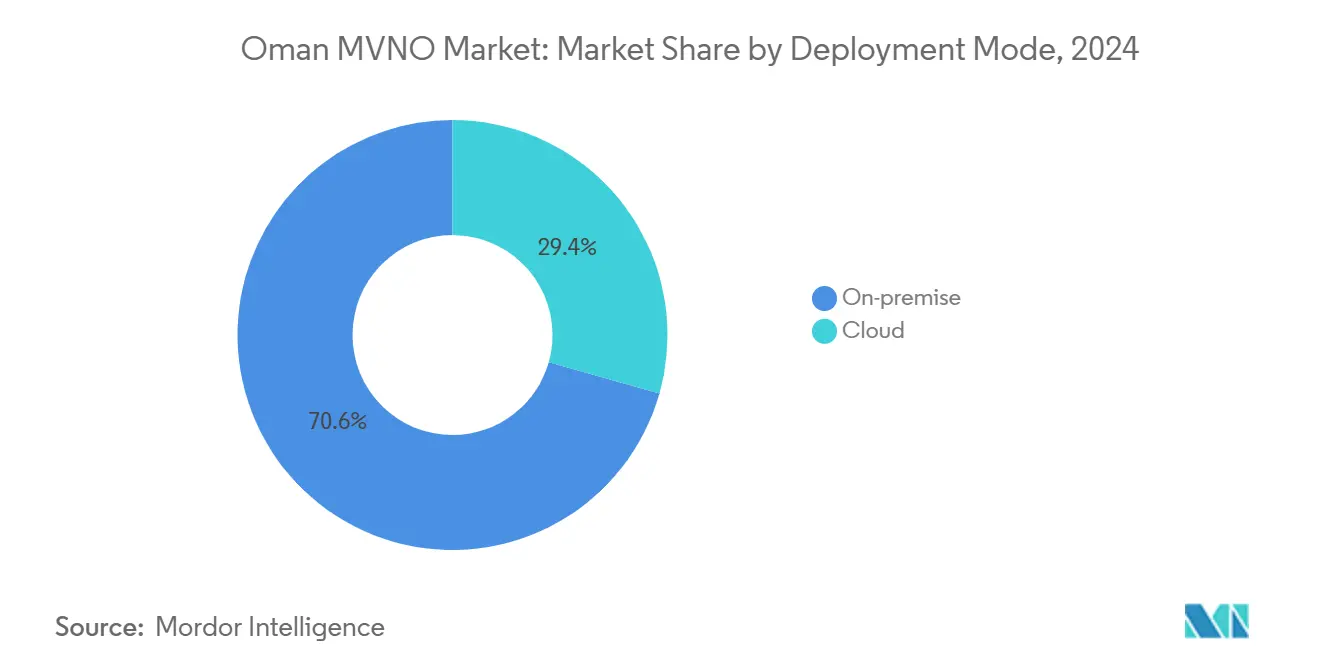

- On-premise deployment captured 70.62% of the Oman MVNO market share in 2024, whereas cloud deployment is projected to grow at a 22.42% CAGR through 2030.

- Resellers and light MVNOs held 62.16% of the Oman MVNO market size in 2024, while the service-operator tier is expected to advance at a 16.23% CAGR over the same horizon.

- Consumer subscribers commanded 73.19% of 2024 revenue, but IoT-specific subscriptions are set to expand at an 18.18% CAGR to 2030.

- Discount applications led with a 50.09% revenue share in 2024, whereas cellular M2M use cases will climb at a 16.68% CAGR going forward.

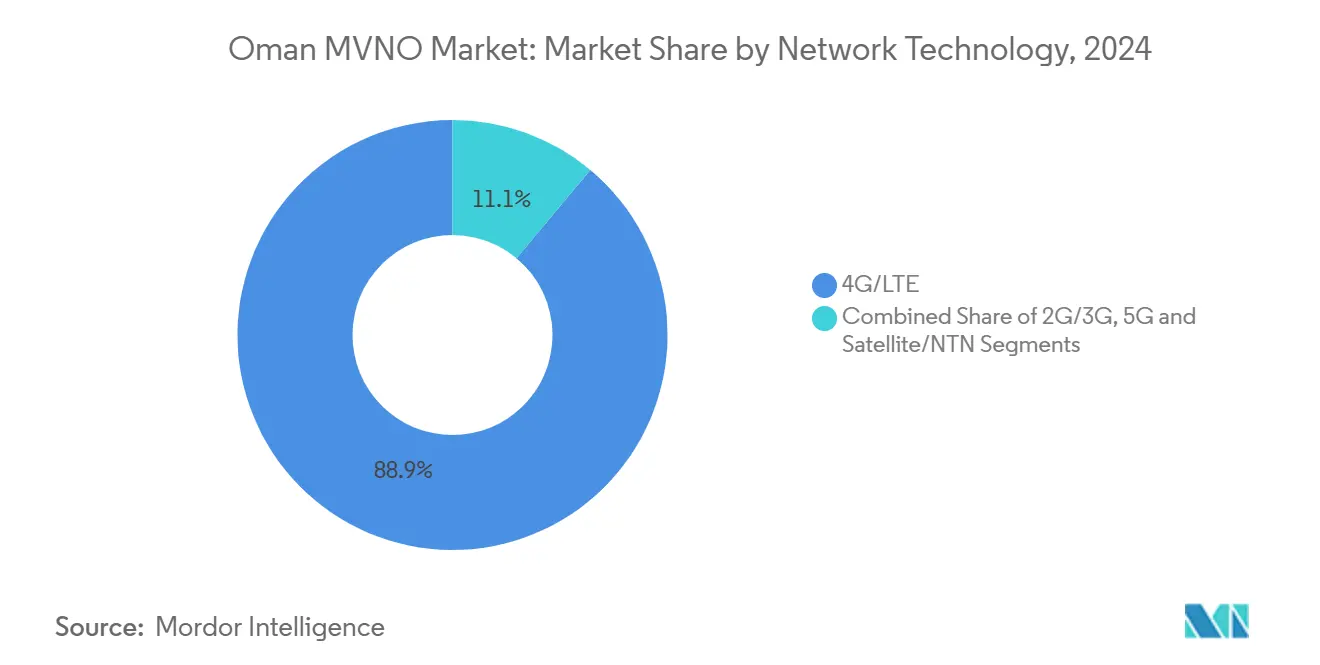

- 4G/LTE networks delivered 88.93% of mobile resale traffic in 2024, yet 5G subscriptions are projected to log a 56.77% CAGR through 2030.

- Traditional retail still accounted for 40.72% of new SIM activations in 2024, though digital-only channels are expected to progress at a 12.13% CAGR by 2030.

Oman MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| TRA streamlined MVNO licensing & wholesale | +1.2% | National, Muscat focus | Medium term (2-4 years) |

| Expat-heavy prepaid base | +0.8% | Urban & industrial zones | Short term (≤ 2 years) |

| Nationwide 5G plus eSIM rollout | +1.5% | Countrywide | Medium term (2-4 years) |

| Digital-first onboarding cuts OPEX | +0.9% | Tech-savvy segments | Short term (≤ 2 years) |

| Oman Vision 2040 IoT incentives | +1.1% | Energy, logistics hubs | Long term (≥ 4 years) |

| Hybrid satellite/NTN for remote sites | +0.4% | Remote & maritime areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

TRA streamlined MVNO licensing and wholesale

TRA’s Class II regime lets service resellers operate without spectrum rights and mandates non-discriminatory access to incumbent networks. Entry cost is low and compliance steps are clear, prompting both foreign brands and local entrepreneurs to launch Oman MVNO market offerings. [1]Telecommunications Regulatory Authority, “Annual Telecommunications Indicators 2025,” tra.gov.omCommercial talks still set wholesale prices, but the regulatory guardrails have shortened launch times, expanded geographic reach, and nudged incumbents to improve onboarding processes.

Expat-heavy prepaid base

Expatriates make up a significant share of Oman’s 4.61 million residents and favor flexible prepaid plans for international calls and short-term stays. [2]Telecom Review, “Oman Records 5,238 Active 5G Sites,” telecomreview.comMVNOs tailoring language-specific customer care and low-cost roaming packages win rapid subscriber traction, yet churn risk stays high, so digital loyalty and segmented pricing are now critical.

Nationwide 5G plus eSIM rollout

More than 5,238 5G sites delivered 88% population coverage by early 2025, and eSIM activation can be completed within minutes through mobile apps. MVNOs gain the freedom to offer sliced 5G capacity for IoT, gaming, or corporate VPNs while avoiding physical SIM logistics. The new capabilities open doors for differentiated service tiers that go beyond basic voice and data bundles.

Digital-first onboarding cuts OPEX

Cloud billing engines, AI identity checks, and self-care apps reduce per-subscriber acquisition costs and slash service-delivery times. Operators deploying cloud-native BSS record faster break-even cycles and can reinvest savings into niche propositions such as fintech wallets or OTT bundling. The model favors small MVNOs that lack retail footprints yet must scale quickly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation and falling prepaid ARPU | -0.7% | Urban markets | Short term (≤ 2 years) |

| Intense price wars with Vodafone and incumbents | -0.9% | Nationwide | Short term (≤ 2 years) |

| Unfavorable wholesale migration terms | -0.5% | Countrywide | Medium term (2-4 years) |

| Stricter online-marketing rules | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Market saturation and falling prepaid ARPU

Mobile penetration exceeds 151% of population, limiting room for organic user growth. [3]International Monetary Fund, “Oman Country Report 2025,” imf.orgOoredoo’s 2024 ARPU slid to USD 10.8, a warning that price cuts outweigh upsell potential. MVNOs chasing volume in the Oman MVNO market face razor-thin margins unless they secure value-added upsells or cross-border niches.

Intense price wars with Vodafone and incumbents

Vodafone Oman reached 14% share in under three years and spurred retaliatory discounts from Omantel and Ooredoo. MVNOs must either undercut already low tariffs or pivot toward differentiated services such as diaspora bundles, enterprise IoT, or satellite-backed maritime plans to defend profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Adoption Reshapes Infrastructure

In 2024 on-premise platforms held 70.62% of revenue because legacy operators still prioritize controlled data centers for compliance and latency. Cloud instances, however, are scaling at a 22.42% CAGR, and their share of the Oman MVNO market size is projected to double by 2030. The cloud model lowers capital outlays, allows iterative software upgrades, and speeds product launches, which is critical for new entrants competing with established brands.

Cloud billing also paves the way for AI-driven promotions and dynamic network resource allocation. Omantel completed a full migration of 200-plus services onto a cloud-native charging engine in late 2024, cutting time-to-market for partner offerings and improving retail price elasticity. These operational gains will keep tilting the Oman MVNO market toward SaaS-based support systems.

By Operational Mode: Service Operators Gain Momentum

Reseller and light MVNO formats controlled 62.16% of 2024 revenue thanks to lower technical hurdles and faster go-live options. Service-operator MVNOs, which manage their own core network functions, are predicted to compound at 16.23% a year. Their deeper control over billing, customer-care, and value-added services lets them craft multi-play bundles that rival incumbents.

Upgrading from resale to full-service status is costly, yet wholesale core-connectivity fees drop once operators bring critical functions in-house, improving lifetime economics. As enterprise IoT and 5G slicing grow, self-managed quality-of-service becomes an edge only service-operator models can supply, pushing the Oman MVNO market toward richer service layers.

By Subscriber Type: IoT Drives Enterprise Growth

Consumer lines delivered 73.19% of sales in 2024, anchored by expatriate voice and data demand. IoT SIMs, although still small, are rising at an 18.18% CAGR, supported by Oman Vision 2040 incentives for energy, logistics, and smart city deployments. Enterprise contracts sit between the two, contributing predictable cash flow from managed connectivity deals.

IoT growth is visible in Ooredoo’s 450,000 smart water meters and the 1.1 million nation-wide IoT SIMs logged in 2024. Low-power, wide-area modules plus eSIM simplify massive device provisioning, enabling MVNOs to carve vertical plays around utilities, fleet, and remote asset management within the Oman MVNO market.

By Application: M2M Connectivity Fuels Industrial Digitization

Discount consumer plans produced 50.09% of revenues in 2024 due to the price-centric nature of prepaid users. Cellular machine-to-machine lines are rising the fastest at 16.68% CAGR. Oil and gas majors now demand continuous sensor feeds to offshore rigs, while logistics groups deploy real-time container tracking that uses encrypted narrowband 5G links.

TRA cleared Starlink Muscat for commercial satellite broadband in March 2025, a step that will extend hybrid M2M connectivity to deserts and maritime corridors. MVNOs combining terrestrial LTE with low Earth orbit backhaul can now serve energy installations beyond fiber reach, giving the Oman MVNO market an industrial revenue stream with higher ARPU levels.

By Network Technology: 5G Spurs Service Innovation

4G/LTE accounted for 88.93% of active MVNO traffic in 2024, reflecting fully built nationwide coverage. 5G subscriptions are forecast to accrue a 56.77% CAGR to 2030. Vodafone Oman alone installed 2,572 5G sites, achieving over 98% population coverage two years ahead of obligation.

Network slicing supports guaranteed bandwidth tiers for gaming, real-time industrial control, and mission-critical communications. MVNOs renting slices can package differentiated offers such as ultra-low-latency plans for autonomous trucks or dedicated secure channels for remote surgeries, a shift that will redefine revenue mix inside the Oman MVNO market.

By Distribution Channel: Digital-Only Sales Gain Ground

Physical retailers enabled 40.72% of SIM activations in 2024 because many users still prefer in-store KYC and device bundling. Digital-only onboarding is growing at a 12.13% CAGR, underpinned by eSIM, biometric ID verification, and embedded payments.

MVNOs without storefronts can now reach remote users instantly and save on rent, logistics, and staff costs. Yet walk-in outlets remain vital for complex service issues and smartphone financing schemes. Operators are therefore blending app-centric sign-ups with selective micro-franchises in high-traffic malls, achieving broad reach at sustainable cost in the Oman MVNO market.

Geography Analysis

Muscat, Salalah, and Sohar together host more than 60% of total mobile lines and sit atop dense fiber and 5G coverage, making them the prime launch pads for any new Oman MVNO market service. Retail networks are mature, while data center capacity is scaling due to joint ventures such as the Salalah SN1 facility, creating a low-latency backbone for cloud billing and AI analytics.

Remote industrial zones in Dhofar, Duqm, and offshore maritime lanes demand hybrid terrestrial-satellite coverage. TRA’s blanket license for Starlink Muscat has removed connectivity blackspots that once limited real-time monitoring of drilling platforms and shipping lanes. MVNOs with maritime or energy specialization are tapping these corridors with bundled narrowband 5G and satellite backhaul plans.

Cross-border traffic flows are rising thanks to USD 35 billion UAE-Oman infrastructure pacts signed in April 2024, which include fiber corridors and data-exchange platforms. Omantel’s 20-plus subsea cables and 120 international landing points further bolster regional roaming packages, letting MVNOs craft diaspora products that appeal to migrant communities traveling between Gulf states.

Competitive Landscape

The Oman MVNO market comprises around eight active brands, with FRiENDi Mobile and Renna Mobile sharing about 45% of subscriber counts. FRiENDi’s 2023 acquisition by Beyond ONE broadened its capital base and introduced AI-enabled customer-lifecycle tools, accelerating youth-oriented plan releases. Renna Mobile has responded by partnering with local fintech wallets for real-time top-ups that reinforce stickiness among blue-collar expatriates.

Vodafone Oman, though an infrastructure player, influences MVNO economics by setting promotional price floors that incumbents reluctantly match. Price pressure forces MVNOs to seek margins via niche IoT or premium diaspora bundles rather than headline tariffs. TRA supervision prevents discriminatory wholesale blocking but does not cap prices, so savvy contract negotiation remains a core competency for every Oman MVNO market participant.

Forward strategy pivots on digital-first service layers. FRiENDi Mobile is piloting AI-chatbot care in three languages, while Renna Mobile is trialing a 5G gaming pass riding on sliced capacity from Omantel. New entrants are expected to target enterprise verticals, bundling managed IoT with cloud analytics in energy and logistics parks where latent demand is under-served.

Oman MVNO Industry Leaders

FRiENDi Mobile

Renna Mobile

Red Bull Mobile Oman

TeO (Integrated Telecommunications Oman)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Starlink Muscat secured nationwide approval to supply satellite broadband up to 100 Mbps for universal service areas, broadening backhaul options for industrial MVNOs.

- February 2025: Vodafone Oman finished the country’s fastest 5G rollout with 2,572 sites and 98% population coverage, expanding wholesale slices for virtual operators.

- October 2024: Omantel migrated 200-plus offerings to a cloud-native charging platform in partnership with Optiva, enabling real-time pricing models.

- July 2024: TRA introduced four-year device accreditation validity and SME-specific provisions, easing handset approval for MVNO bundles.

Oman MVNO Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How big is the Oman MVNO market in 2025?

It is valued at USD 121.69 million and is projected to post a 5.93% CAGR to 2030.

Which subscriber type is expanding fastest?

IoT-specific subscriptions are expected to grow at an 18.18% CAGR through 2030.

What drives the strong uptake of discount plans?

A large expatriate prepaid base seeks flexible, low-cost international calling and data options.

How will 5G change MVNO offerings?

5G slicing lets MVNOs sell guaranteed bandwidth tiers for gaming, industrial IoT, and mission-critical apps.

Which deployment model shows the highest growth?

Cloud-native platforms lead with a 22.42% CAGR as operators chase agility and lower capital needs.

What role does satellite play in future growth?

Hybrid satellite-terrestrial links extend coverage to offshore rigs and desert sites, unlocking new industrial revenue streams.

Page last updated on: