Germany Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

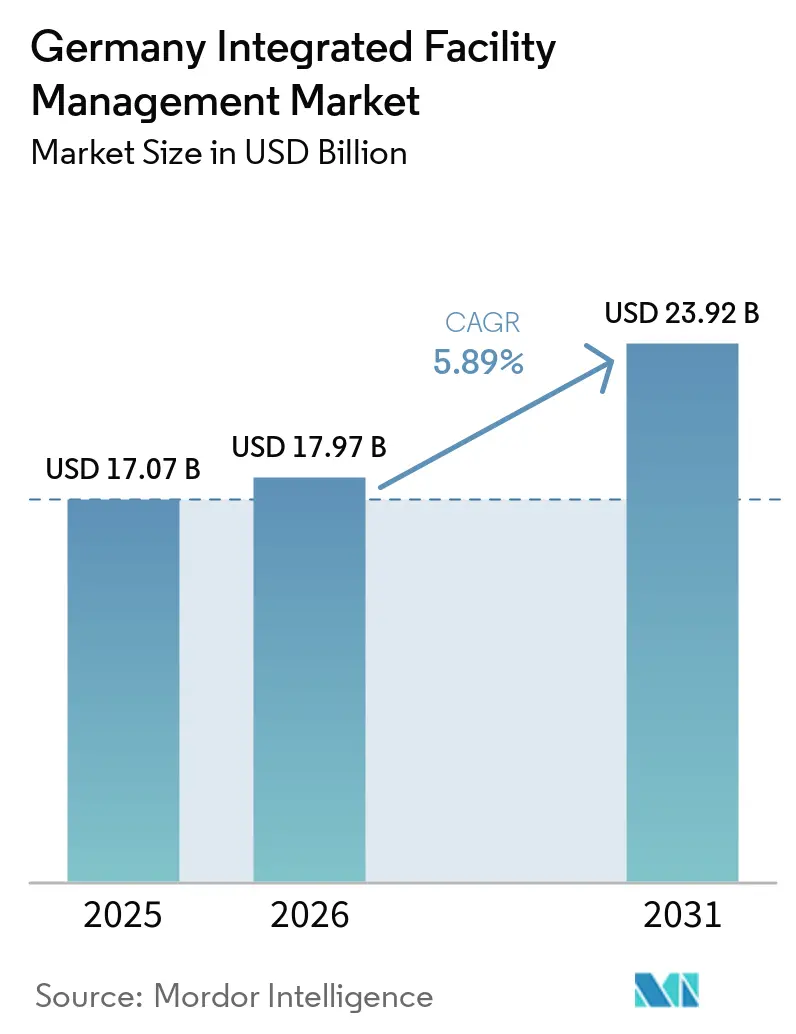

| Base Year Market Size (2025) | USD 17.07 Billion |

| Market Size (2026) | USD 17.97 Billion |

| Market Size (2031) | USD 23.92 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

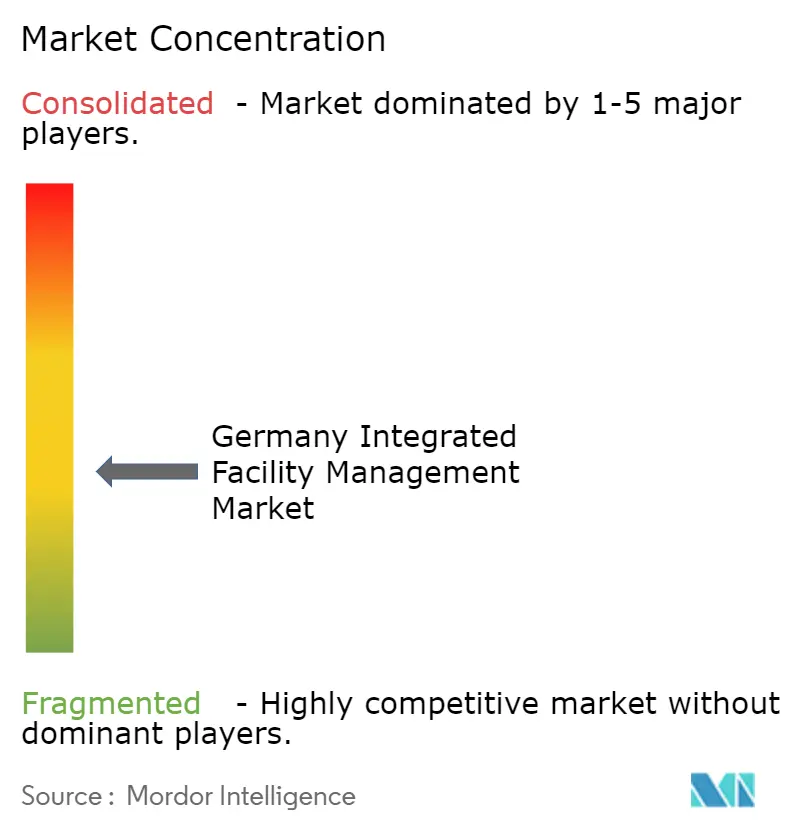

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Integrated Facility Management Market Analysis by Mordor Intelligence

The Germany integrated facility management market size is expected to increase from USD 17.07 billion in 2025 to USD 17.97 billion in 2026 and reach USD 23.92 billion by 2031, growing at a CAGR of 5.89% over 2026-2031. The Germany integrated facility management (IFM) market remains the largest facility services economy in Europe because the country combines a dense industrial base with a large stock of complex commercial, institutional, and public assets that require coordinated operating support. Compliance pressure is rising across the Germany integrated facility management market as the Gebäudeenergiegesetz requires building automation and control systems in large non-residential properties, which increases the need for providers that can operate, monitor, and optimize technical assets after installation. Corporate clients are also moving toward broader outsourcing mandates, and even though integrated procurement still represents the smallest of the three contract types, it reflects a clear preference for single-provider accountability across multi-site portfolios with more demanding governance needs. Data center expansion is adding another layer of recurring technical work in the Germany IFM market because operators need continuous cooling, power oversight, uptime assurance, and energy performance management as installed capacity rises. Competition is intensifying, yet the Germany integrated facility management market still leaves room for operators that combine technical depth, digital reporting capability, labor coverage, and the ability to deliver unified contracts across diverse building portfolios.

Key Report Takeaways

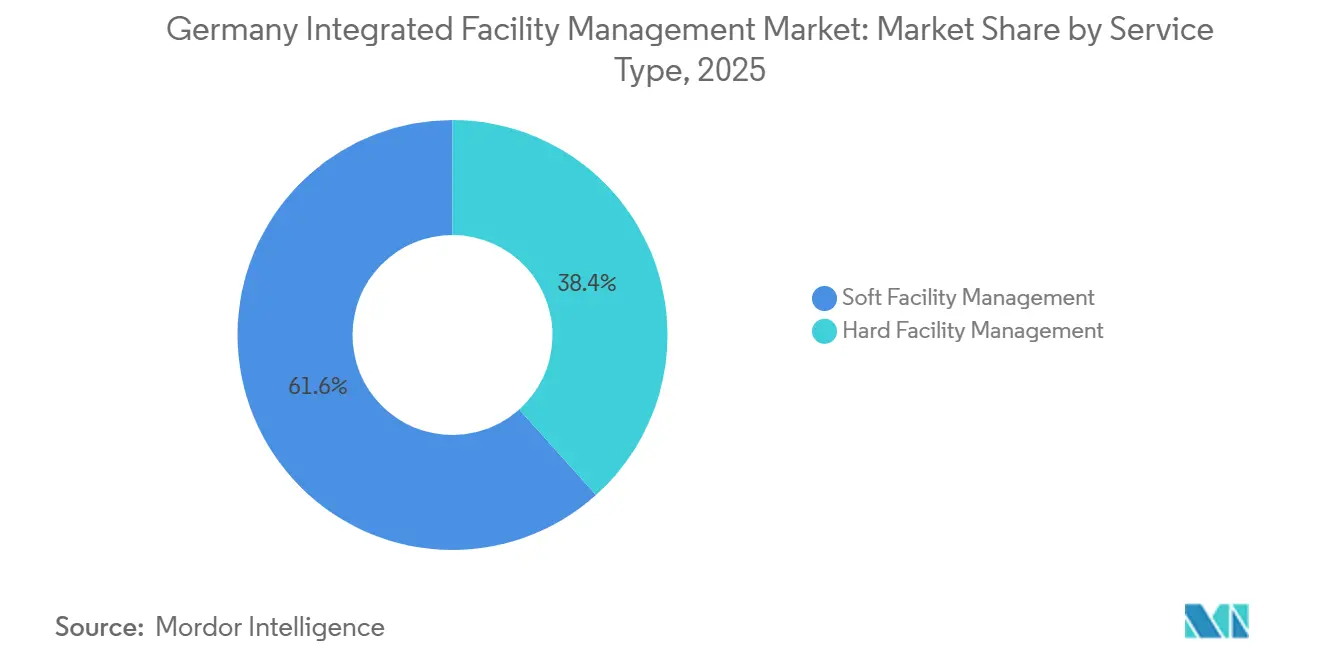

- By service type, soft facility management segment led with 61.64% revenue share of the Germany integrated facility management market in 2025, while hard facility segment management is forecast to expand at a 6.59% CAGR through 2031.

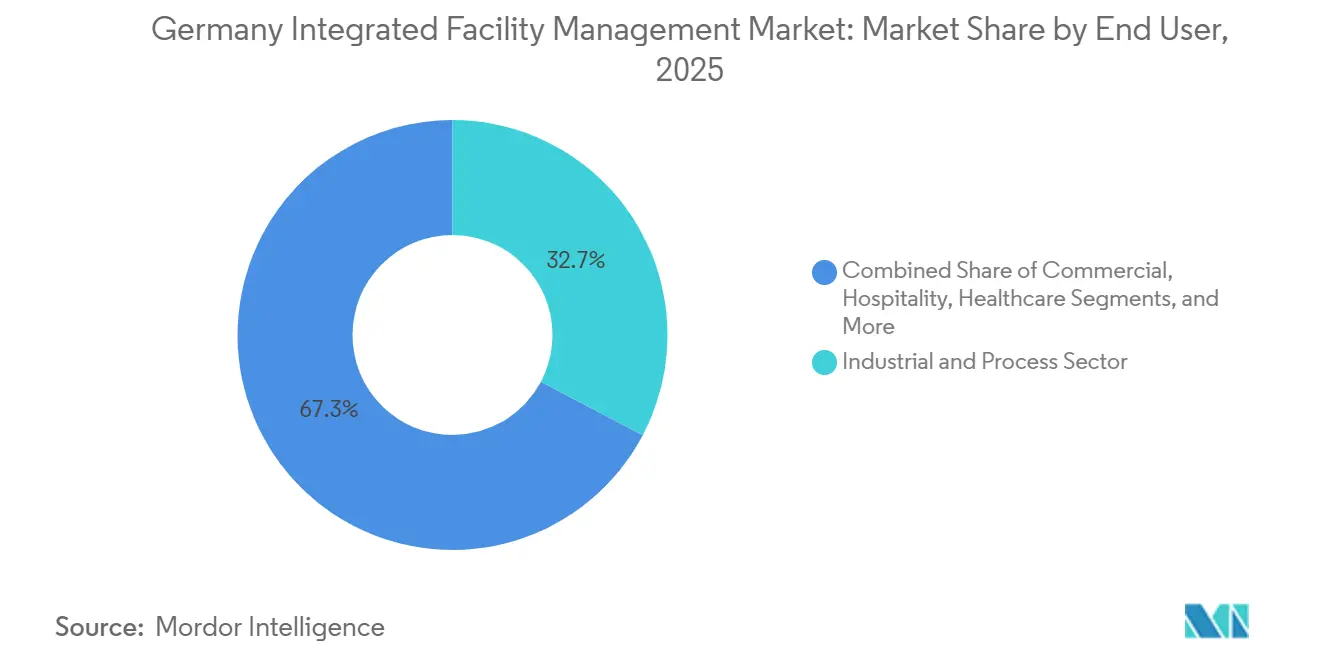

- By end-user, industrial and manufacturing premises held 32.73% of the Germany integrated facility management market share in 2025, while commercial properties recorded the highest projected CAGR at 6.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Efficiency Regulations And Sustainability | +1.3% | National, with early gains in Frankfurt, Munich, Hamburg, and all large cities with more than 100,000 inhabitants | Medium term (2-4 years) |

| Growth Of Data Centers Fueling Specialized Hard FM Demand | +1.1% | National, concentrated in Frankfurt-Rhine-Main, Berlin, and emerging secondary markets including North Rhine-Westphalia and Brandenburg | Long term (≥ 4 years) |

| ESG-Driven Outsourcing To Achieve Scope 3 Emission Reductions | +1.0% | National, with early leadership in industrial hubs including Stuttgart, Munich, and Wolfsburg, and commercial centers including Frankfurt and Berlin | Medium term (2-4 years) |

| Sustainability And Procurement Initiatives By German Companies | +0.9% | National, accelerated in corporate headquarters cities including Munich, Frankfurt, and Hamburg | Medium term (2-4 years) |

| Commercial Real Estate Recovery Supporting FM Demand | +0.7% | National, concentrated in Berlin, Munich, Hamburg, Düsseldorf, and secondary logistics corridors | Medium term (2-4 years) |

| Expansion Of Integrated Platform Billing By Global FM Providers | +0.5% | National, with an advantage in large multi-site corporate portfolios in the top 7 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Energy Efficiency Regulations and Sustainability

Energy regulation is the clearest near-term growth force in the Germany IFM market because it turns compliance obligations into recurring operating work rather than one-time installation projects. GEG Section 71a required non-residential buildings with heating, cooling, or ventilation systems above 290 kW to install certified building automation and control systems by December 31, 2024, which widened the addressable base for technical FM providers across offices, factories, hospitals, universities, and retail assets.[1]Bundesministerium der Justiz, “Law on saving energy and using renewable energies for heat and cold generation in buildings,” gesetze-im-internet.de Once these systems are in place, building owners still need providers that can monitor performance, interpret energy data, maintain controls, and produce regular operating records through open interfaces, which lifts contract value above basic maintenance work. The compliance cycle also extends beyond Germany because the 2024 EPBD and related energy efficiency obligations in public buildings keep pushing owners toward tighter building performance standards and better operating discipline. This makes the Germany integrated facility management market more attractive for firms that can combine field engineering, software-enabled monitoring, and energy optimization within one accountable service structure.

Growth Of Data Centers Fueling Specialized Hard FM Demand

Data centers are pushing the technical edge of the Germany integrated facility management market because they require uptime-focused service models that standard commercial building contracts cannot easily replicate. Germany reached ~3000 MW of installed data center capacity in 2025, and national capacity is expected to expand further by 2030, which creates recurring demand for cooling, power distribution, fire protection, maintenance planning, and 24/7 incident response.[2]Borderstep Institut, “Rechenzentren in Deutschland - Update 2025,” borderstep.de Google’s EUR 5.5 billion (USD 6.40 billion) investment program in Germany for 2026-2029.[3]Google Cloud, “Google Announces EUR 5.5 Billion Investment in Germany,” googlecloudpresscorner.com The program underlines how large operators are still adding new sites and upgrading energy profiles, which extends the pipeline for future technical FM demand in digital infrastructure. Rack densities in AI-oriented environments are moving beyond levels that conventional HVAC contracts can manage efficiently, so providers need liquid cooling knowledge, DCIM integration capability, and waste heat compliance expertise to stay relevant. This part of the Germany IFM market therefore favors firms that invest early in specialized engineering teams, faster response structures, and operational depth in critical environments.

ESG-Driven Outsourcing to Achieve Scope 3 Emission Reductions

ESG reporting is changing why occupiers buy services in the Germany integrated facility management (IFM) market because building operations now feed directly into wider corporate disclosure and decarbonization priorities. Companies need cleaner building-level data on energy use, water, waste, and operational performance, and that task becomes much harder when every site is managed through multiple single-service contracts that store data in different formats. A unified IFM contract reduces that burden because one provider can collect site data, align reporting processes, and connect day-to-day building operations with wider sustainability targets across the estate. The extension of Apleona’s partnership with Deutsche Bank across 825 properties shows how outsourcing is moving beyond maintenance and into energy management, space management, and decarbonization support within the same commercial relationship. The Germany IFM market therefore benefits when sustainability reporting shifts from a corporate disclosure issue into an operating requirement that has to be delivered consistently at property level.

Sustainability and Procurement Initiatives by German Companies

Procurement behavior is becoming more structured across the Germany integrated facility management market because larger buyers want clearer governance, more measurable outcomes, and better control over transition risk. The GEFMA 140 guideline published in March 2026 defines outsourcing, insourcing, and hybrid IFM models for Germany and gives buyers a clearer framework for service levels, governance rules, and transition planning. That change matters because clients are no longer buying only labor inputs and routine tasks, they are buying performance outcomes linked to uptime, energy use, reporting quality, and operational continuity. Sustainable building operation is also becoming a stronger procurement filter as certified and premium assets demand tighter standards in energy management, reporting discipline, and user experience. This trend raises the bar for smaller single-trade firms and supports larger integrated operators in the Germany integrated facility management market that can prove governance maturity and broader delivery capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent FM Talent Shortage And Wage Inflation | -0.9% | National, most acute in Berlin, Hamburg, Munich, Frankfurt, and major data center hubs | Medium term (2-4 years) |

| Volatile Energy Prices Pressuring FM Contract Margins | -0.6% | National, with stronger exposure in industrial FM and data center operations in high-demand grid areas | Short term (≤ 2 years) |

| Fragmented Regulatory Environments Across German States | -0.4% | National, with varying effects by Bundesland and higher complexity in states with active renovation programs | Medium term (2-4 years) |

| Limited Digitalization In SMEs And Enterprises | -0.3% | National, most visible in eastern Germany, rural areas, and smaller city markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent FM Talent Shortage and Wage Inflation

Labor availability remains the main execution risk in the Germany integrated facility management market because demand growth is arriving faster than providers can recruit, train, and retain qualified staff across soft and hard services. Germany’s building cleaning trade reported that 45.3% of firms regularly turned away new orders because they lacked staff, while 47.4% said the shortage caused revenue losses of up to 10%, which shows how labor scarcity is already limiting service delivery rather than only raising costs.[4]Federal Guild Association of the Building Cleaning Trade (BIV), “Spring economic Survey 2024,” die-gebaeudedienstleister.de The pressure is not limited to entry-level roles because automation support, technical FM, and data center operations also require workers with specialized skills that are harder to source and more expensive to keep. The Charité Facility Management labor dispute in March 2025 showed how wage alignment can sharply raise annual labor costs and force contract repricing or margin compression across large portfolios. As a result, providers in the Germany integrated facility management market face a persistent gap between strong client demand and the labor base needed to deliver it at reliable service levels.

Volatile Energy Prices Pressuring FM Contract Margins

Energy volatility continues to reshape pricing across the Germany integrated facility management market because technical service contracts are increasingly tied to equipment upgrades, heating transitions, and more energy-intensive monitoring obligations. Building owners are under pressure to move away from fossil-based heating because German energy law and carbon pricing make older systems harder to operate economically, which raises both planning complexity and operating expectations for FM providers. Providers often sit at the center of this transition because they help scope upgrades, coordinate contractors, maintain new systems, and keep buildings compliant after installation work is complete. When contracts were priced before the latest swing in energy and equipment costs, fixed-fee arrangements became harder to defend, especially in technical FM where spare parts, controls, and specialist interventions all became more expensive. The Germany integrated facility management market therefore sees stronger demand for price indexation, pass-through clauses, and tighter scope design in service agreements that include energy-sensitive components.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Gains Ground Against A Dominant Soft Base

Soft facility management segment held 61.64% of the Germany integrated facility management market share in 2025, which kept it as the largest service group by a clear margin across the country’s commercial, industrial, and institutional building base. That scale comes from cleaning, catering, reception, waste handling, and grounds maintenance, all of which remain embedded in day-to-day building operations and are required across both premium assets and older building stock. The service base is broad, recurring, and labor intensive, which gives larger operators room to bundle routine activities across national contracts and maintain steady revenue flows even when capital spending cycles soften. Even so, the Germany integrated facility management market is gradually moving beyond labor-heavy bundles toward contracts that connect soft services with technical oversight, reporting requirements, and sustainability-linked performance measures. That change matters because clients increasingly want one accountable operating partner that can manage site standards consistently across multi-location portfolios rather than several fragmented vendors with separate service controls.

Hard facility management is the fastest-growing service category in the Germany integrated facility management market, and its Germany integrated facility management market size is projected to expand at a 6.59% CAGR through 2031. The strongest pull comes from building automation mandates, energy retrofit programs, critical environment management, and the broader need to keep technical assets compliant, efficient, and digitally visible across non-residential properties. GEFMA reported that Germany’s real estate-related FM software market grew 12.8% in 2025, while 70% of providers offered CAFM or IWMS tools, which shows how technical service delivery now depends far more on software-enabled monitoring and coordinated work-order management than in the past. In practical terms, the Germany integrated facility management industry is moving from basic maintenance toward service models built around data quality, uptime assurance, and energy performance, especially in buildings with more advanced controls. Smaller technical specialists still hold useful niches, but the Germany integrated facility management market increasingly rewards providers that can combine engineers, digital systems, and round-the-clock service coverage within one contract structure.

By End-User: Industrial Anchor Steady As Commercial Segment Accelerates

Industrial and manufacturing premises accounted for 32.73% of the Germany integrated facility management market share in 2025, making them the largest end-user group and the most stable revenue anchor for many national providers. This position reflects Germany’s large production base and the need for FM contracts that support process-critical systems, waste handling, environmental controls, safety routines, and specialized maintenance cycles that cannot easily be deferred. Industrial sites also tend to favor longer agreements, which gives providers better revenue visibility and a more predictable operating base than shorter-cycle contracts in parts of the commercial real estate market. The Germany integrated facility management market remains anchored in this customer base because factories and advanced production facilities need continuity, uptime, and compliance support even when wider business sentiment becomes more cautious. That stability allows providers to balance faster growth but more variable demand from other building categories, while also deepening relationships in technically demanding environments where switching costs tend to be higher.

Commercial properties are the fastest-growing end-user segment in the Germany integrated facility management market, with a projected 6.73% CAGR through 2031. This acceleration reflects a recovery in office and mixed-use asset activity, a stronger focus on tenant retention, and the rising need for certified, efficient, and well-documented building operation in prime urban locations. Owners and occupiers are placing more weight on energy reporting, predictive maintenance, space management, workplace experience, and sustainability support because those features now shape both tenant quality and long-term asset positioning. Healthcare, education, transportation, and utility sites still contribute meaningful contract volume, but the sharpest near-term specification upgrades are appearing in large office and other commercial portfolios where service standards are being reset upward. Within this mix, the Germany integrated facility management market size for commercial properties is projected to expand through 2031 because owners need higher operating standards to protect occupancy, reputation, and asset value.

Geography Analysis

The Germany integrated facility management market, which keeps Germany as the sole geography in this study and confirms the scale of the national opportunity. National demand is being shaped by three reinforcing forces, wider building retrofit cycles, faster data center development, and deeper outsourcing of complex property portfolios that need more coordinated service delivery. The strongest immediate uplift comes from technical service work tied to building automation, inspections, and energy monitoring in non-residential stock, where operating compliance now carries more weight in procurement decisions. This gives the Germany integrated facility management (IFM) market a broad base because offices, factories, hospitals, universities, retail sites, logistics facilities, and public buildings all face operational tasks that are becoming more formalized and more data dependent. The public sector still lags in digital adoption and in the wider use of integrated outsourcing models, which leaves a long-term opportunity for providers that can deliver standardized reporting, smoother transitions, and stronger governance discipline.

Frankfurt-Rhine-Main remains the most data center-intensive cluster in the Germany integrated facility management market because it combines strong connectivity, a deep enterprise base, and the highest concentration of digital infrastructure demand. The region hosted 1,020 MW of installed IT capacity in 2026, and very low vacancy indicates that new supply continues to be absorbed quickly, which supports sustained demand for specialist technical FM capability. Google is expanding in Dietzenbach and Hanau, which reinforces the role of Hessen as a focal point for high-value contracts involving uptime management, cooling oversight, and energy-conscious facility operations. Berlin is also gaining weight as a secondary digital infrastructure hub, while North Rhine-Westphalia and Brandenburg are drawing more attention for new campus development and wider hyperscale interest. Munich and Bavaria remain central to industrial and automotive demand, where clients place greater emphasis on predictive maintenance, energy management, and technically advanced hard-service delivery across large production estates.

Northern Germany is emerging as an alternative operating zone within the Germany IFM market because cooler temperatures, offshore wind access, and lower land costs make it more attractive for selected digital infrastructure projects. This wider spread of facilities changes service delivery because operators need technicians, spare parts, and rapid response capability outside the traditional big-city footprint where most FM networks were historically concentrated. It also favors providers with denser local coverage, since travel time, labor availability, and inventory positioning now have a direct effect on service quality, uptime assurance, and contract economics. Regional strategy is therefore becoming a core operating issue in the Germany integrated facility management market rather than a secondary expansion question, especially for providers chasing larger integrated mandates across several federal states.

Competitive Landscape

The Germany integrated facility management market remains slightly fragmented, even though a limited group of large providers carries the highest national visibility and secures many of the most complex multi-site mandates. Apleona, SPIE Deutschland, Wisag, Strabag Property and Facility Services, ISS Facility Services, and Engie are among the best-known operators serving large national accounts across corporate, industrial, commercial, and public sector portfolios. The competitive gap is not defined by scale alone because buyers increasingly compare providers on technical depth, labor coverage, mobilization discipline, digital reporting capability, and their ability to manage complex transitions without service disruption. This keeps the Germany integrated facility management market open to firms that can execute demanding contracts well, even when they are not the largest providers by revenue or the broadest by geographic footprint. It also explains why consolidation continues without turning the Germany integrated facility management market into a tightly concentrated structure.

Strategy in the Germany integrated facility management market is moving toward longer IFM mandates that combine hard services, soft services, energy management, and sustainability-linked deliverables under one governance framework. Providers that can connect building operations with ESG reporting, data visibility, and technical performance now hold a clearer advantage in tenders from larger occupiers and institutional owners. The March 2026 GEFMA 140 guideline supports this shift because it gives clients a more formal way to assess transition planning, due diligence, and service governance when they compare integrated proposals. Specialized hard-service capability is becoming another major differentiator, especially in data centers and other regulated environments where standard maintenance models no longer meet client expectations around uptime, efficiency, and compliance. Software is reinforcing that divide because digital work-order tools, monitoring platforms, and reporting layers are increasingly becoming part of the service proposition rather than only an internal operating tool.

Recent contract activity shows how leading firms are positioning themselves in the Germany integrated facility management market around scale, specialization, and long-duration relationships. Apleona extended its IFM partnership with Deutsche Bank through the end of 2029 and secured a 10-year mandate for DHL Group’s Germany portfolio, which highlights the value large clients place on national coverage, transition capacity, and decarbonization support. ISS widened its integrated services footprint through contracts such as Aroundtown and the Haniel Campus, while Colt DCS and CyrusOne are adding large data center capacity that will require specialist technical FM once those facilities move into operation. Competition in the Germany integrated facility management market is therefore tightening around execution quality, technical specialization, and the ability to absorb large portfolios without weakening service standards during mobilization and delivery.

Germany Integrated Facility Management Industry Leaders

ISS A/S

Sodexo SA

Compass Group PLC

Dussmann Stiftung & Co. KGaA

Wisag Facility Service Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SPIE agreed to acquire SGS Industrial Services to strengthen its industrial services presence in Germany. The deal enhances electrical and mechanical capabilities for industrial facilities and energy infrastructure, supporting Germany’s energy transition while expanding service capacity, workforce expertise, and industrial sector opportunities.

- December 2025: Apleona extended its integrated facilities management partnership with Deutsche Bank across Germany and Luxembourg, providing technical, infrastructural, and operational services with energy optimization support, strengthening its market position and sustainability-focused digital solutions.

- September 2025: Apleona expanded its building technology division in Germany through the acquisition of Smart Energy Group (SEG), strengthening its electrical, HVAC, and technical services capabilities while enhancing its position in energy-efficient and decarbonized building solutions across industrial and commercial markets.

- February 2025: ISS won an integrated facility services contract with Aroundtown, covering 47 locations in Germany, including cleaning, building technology, security, landscaping, and winter services.

Germany Integrated Facility Management Market Report Scope

The Germany Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User Industries | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current size of Germany integrated facility management activities?

The Germany integrated facility management market stands at USD 17.97 billion in 2026 and is projected to reach USD 23.92 billion by 2031, growing at a 5.89% CAGR.

Which service category leads demand in Germany?

Soft FM leads with 61.64% share in 2025 because cleaning, catering, reception, waste handling, and landscape services remain embedded across most building portfolios.

Which service category is expanding the fastest?

Hard FM is growing the fastest at a 6.59% CAGR through 2031, supported by building automation rules, retrofit programs, and data center expansion.

Which customer group contributes the most revenue?

Industrial & Process Sectors are the largest end-user group with 32.73% share in 2025, reflecting Germanys large and technically demanding production base.

Why are commercial properties gaining momentum?

Commercial properties are projected to grow at a 6.73% CAGR through 2031 because owners need higher service standards, stronger reporting, and better energy performance to support asset values.

What is the biggest operational challenge for providers?

Labor shortage remains the main challenge because providers face strong demand but still struggle to recruit and retain enough qualified workers across both routine and technical services.

Page last updated on: