Switzerland Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

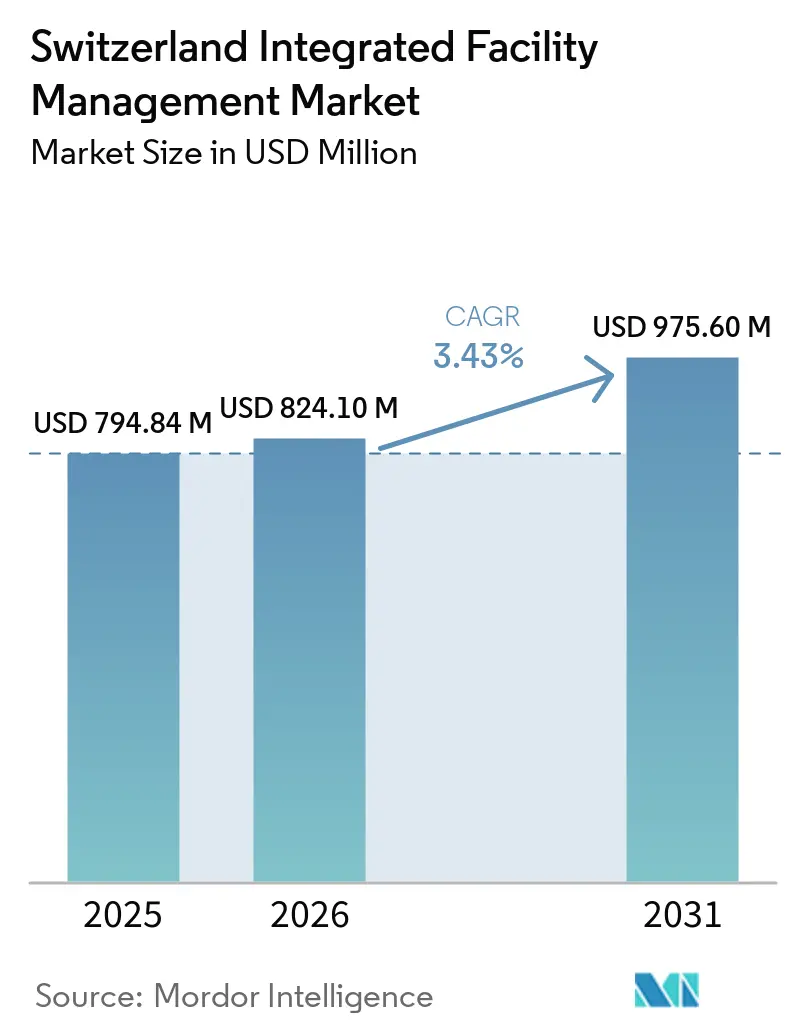

| Base Year Market Size (2025) | USD 794.84 Million |

| Market Size (2026) | USD 824.10 Million |

| Market Size (2031) | USD 975.60 Million |

| Growth Rate (2026 - 2031) | 3.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Integrated Facility Management Market Analysis by Mordor Intelligence

The Switzerland Integrated Facility Management Market size is expected to increase from USD 794.84 million in 2025 to USD 824.10 million in 2026 and reach USD 975.60 million by 2031, growing at a CAGR of 3.43% over 2026-2031.

The Switzerland Integrated Facility Management Market is moving at a measured pace because the country already has a mature building services base, so growth is coming more from broader contract scope than from new capacity creation. Integrated mandates are taking a larger share of new tenders, and 9 out of 10 facility service providers in Switzerland already offer integrated facility management, with such contracts contributing an average 46% of provider revenue in 2025. This shift is raising wallet share per client for integrated providers while narrowing the space for stand-alone service contracts, which supports steady expansion in the Switzerland Integrated Facility Management Market. Building decarbonization rules, hybrid workplace redesign, and wider use of connected building systems are also pushing clients toward providers that can manage technical, infrastructural, and commercial services under one operating model. The market remains competitive for large enterprise mandates, but high retention above 97% at the top tier and a dense base of regional Swiss SMEs mean that new entry opportunities are selective rather than widely available.

Key Report Takeaways

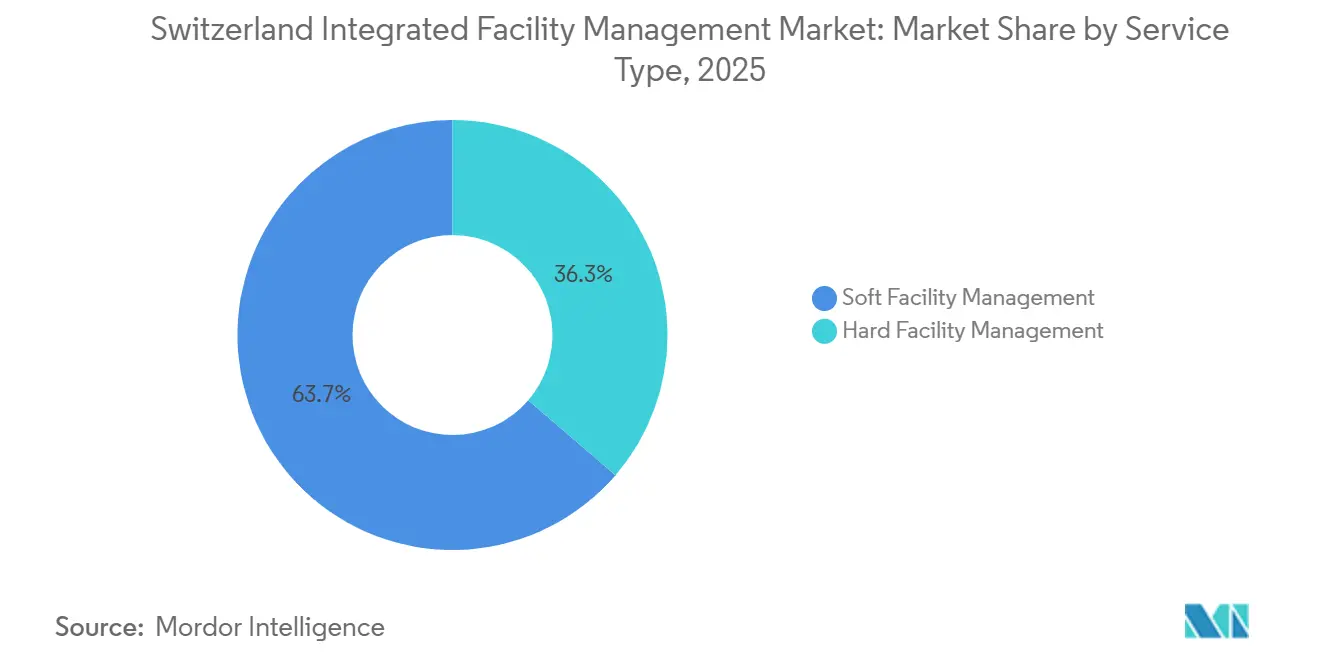

- By service type, soft facility management held 63.7% of the Switzerland integrated facility management market share in 2025, while hard facility management is forecast to grow at a 3.9% CAGR through 2031.

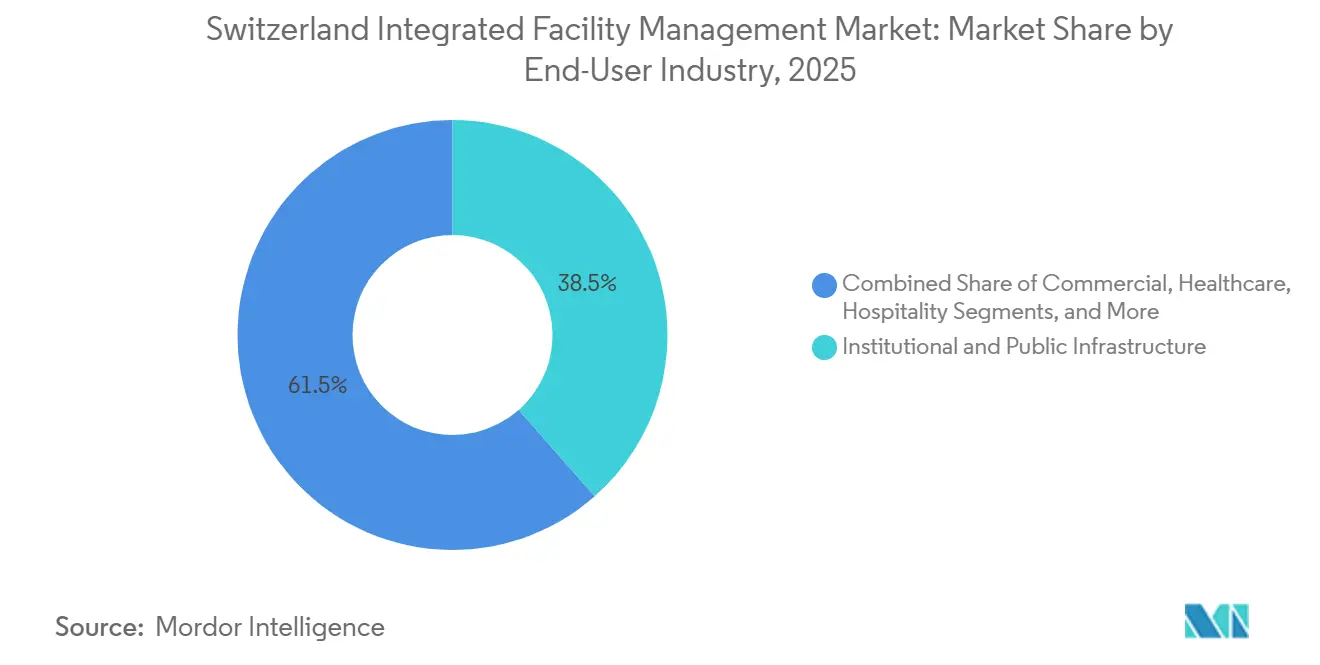

- By end-user, industrial and process sector accounted for 38.5% share of the Switzerland integrated facility management market size in 2025, while commercial sector is projected to expand at a 4.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Switzerland Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Integrated Service Contracts | +1.0% | Global, with concentrated pull in Zurich, Basel, Geneva, and Bern | Short term (≤ 2 years) |

| Stringent Sustainability and Energy Efficiency Regulations | +0.8% | All 26 cantons, with the most advanced enforcement in Zurich, Basel-Stadt, and Geneva | Medium term (2-4 years) |

| Digitalization and Smart Building Adoption | +0.7% | Zurich, Basel, and Zug (corporate clusters), with spill-over to Romandy | Medium term (2-4 years) |

| Post-COVID Hybrid Workplace Transformation | +0.4% | Urban commercial hubs, including Zurich CBD, Geneva CBD, Lausanne, and Bern | Short term (≤ 2 years) |

| Collaborative Public-Private Partnership Wave | +0.3% | National, with early gains in Bern, Basel, and Zurich cantons | Medium term (2-4 years) |

| Government-Driven ESG Rollout Opportunities | +0.3% | National, cantonal public buildings, and federal estate | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Integrated Service Contracts

The move from fragmented contracts to single-source IFM mandates remains the clearest growth driver in the Switzerland Integrated Facility Management Market. Clients want fewer service interfaces, clearer accountability, and more uniform service standards across multi-site portfolios. In 2025, 59% of FM users in the DACH region preferred bundled or integrated procurement over single-service contracts, and integrated models were expected to post the strongest growth among procurement formats in Europe through 2027.[1]SVIT FM Schweiz, “Facility Management Monitor 2025,” SVIT FM Schweiz Industrial users, especially life sciences and pharmaceutical companies, are accelerating this shift because GMP-regulated environments are easier to manage through one integrated operating structure than through multiple specialist vendors. Once a provider is embedded in such a setting, switching becomes harder because the client must manage documented change control, system integrations, and operating continuity, which strengthens renewal prospects for established providers.

Stringent Sustainability and Energy Efficiency Regulations

Energy regulation is creating recurring technical demand rather than one-time retrofit work in the Switzerland Integrated Facility Management Market. The Conference of Cantonal Energy Directors adopted MuKEn 2025 in August 2025, and the framework requires periodic operational optimization of non-residential building systems within 3 years of commissioning, followed by every 5 years thereafter.[2]Conference of Cantonal Energy Directors, “MuKEn 2025 Model Energy Regulations,” EnDK These rules turn HVAC, plumbing, electrical, and building automation upkeep into a recurring compliance requirement that favors IFM providers with technical depth. The same framework also pushes building owners away from fixed electric resistance heating and toward renewable-only replacement systems, which adds to the workload of asset upgrades and operating support. The Swiss Energy Act and recognized sustainability frameworks also increase the value of providers that can document energy performance, audits, and reporting in a way that stands up across both private and public portfolios.

Digitalization and Smart Building Adoption

Digital adoption is still at an early stage in Swiss buildings, which leaves room for deeper service penetration in the Switzerland Integrated Facility Management Market. The ZHAW Smart Building Management Index for 2025 stood at 51 out of 100, and only 35% of Swiss buildings were using smart building management solutions even though 78% of real estate and FM professionals saw high or very high efficiency potential in them.[3]Zurich University of Applied Sciences, “Smart Building Management Index 2025,” ZHAW That gap supports demand for IFM providers that can combine digital tools with day-to-day service delivery rather than sell software alone. ISS Switzerland has already used its Talk to the Building platform to connect real-time sensor data with predictive maintenance, energy optimization, and service scheduling, showing how data tools can lower operating costs and emissions at the same time. The next step is likely to come from AI-led workflows because 63% of Swiss FM stakeholders prioritize digitalization, but only 2% use AI tools regularly in procurement and operations today.

Post-COVID Hybrid Workplace Transformation

Workplace change remains an active demand driver for the Switzerland Integrated Facility Management Market rather than a fading post-pandemic theme. In early 2025, 80% of Swiss companies operated hybrid work programs, and employers expected average office presence to rise from 3 days to 4 days per week within 2 years. This does not automatically lift FM spending per building, but it does change the service mix toward occupancy-based cleaning, flexible reception coverage, and space-use analytics. Vacancy across the 5 largest Swiss office markets reached 5.2% by the end of 2025, with 1.0 million square meters of available space, which means reconfiguration and repurposing activity still feed fit-out, energy upgrade, and operating support demand. Flex-office expansion is also relevant because usable space in Zurich rose from 28,000 square meters in 2019 to 75,000 square meters by 2024, and those operators typically outsource FM in full from the start.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Skilled Labor Shortages and Wage Pressure | -0.8% | National, most acute in Zurich, Basel, and Geneva where competition for technical talent is highest | Short term (≤ 2 years) |

| Fragmented Cantonal Compliance Complexity | -0.7% | National, most complex for multi-canton operators managing portfolios across German-, French-, and Italian-speaking regions | Medium term (2-4 years) |

| High Switching Costs Limiting Contracting Budgets | -0.5% | Global, particularly relevant to large industrials and pharmaceutical clients in Basel and Zug corridors | Medium term (2-4 years) |

| Limited Offshore Cost Arbitrage for Swiss Operations | -0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Skilled Labor Shortages and Wage Pressure

Labor scarcity remains the strongest operating restraint on the Switzerland Integrated Facility Management Market. In 2025, 84% of Swiss FM professionals identified personnel shortages as the main market constraint, which was higher than the comparable rates reported for Germany and Austria. More than 75% of production costs in Swiss facility services are personnel-related, so wage pressure and recruitment costs are hard to absorb without margin erosion. Technical occupations matter most because building engineering and HVAC maintenance sit at the center of Hard FM delivery, and Swiss shortage indicators show that many of the most affected occupations are technical roles. Providers that automate routine tasks, use IoT-triggered workflows, or improve scheduling efficiency gain an advantage in tenders because labour scarcity is now shaping both cost control and service reliability.

Fragmented Cantonal Compliance Complexity

Regulatory fragmentation raises execution difficulty across the Switzerland Integrated Facility Management Market. Providers that operate in several cantons must track different implementation schedules, code interpretations, and procurement frameworks even when the headline policy direction is the same. MuKEn 2025 shows the problem clearly because the model was adopted nationally in 2025, but each canton still decides how and when to transpose the rules locally. This slows national rollout for service offers that rely on standardized compliance packages and forces multi-site operators to maintain local legal, language, and technical expertise. Digital platforms such as cantonal energy reporting systems may reduce friction over time, but full cross-canton interoperability is still not in place.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Accelerates as Compliance Mandate Grows

Soft Facility Management (FM) accounted for 63.7% of the Switzerland Integrated Facility Management (IFM) Market in 2025, which kept it as the largest service category by a clear margin. Cleaning, security, catering, and workplace support remain the services that most clients expect to see wrapped into an integrated contract first. That pattern is especially strong in offices, healthcare sites, pharmaceutical facilities, and food-processing environments, where hygiene, safety, and daily workplace continuity matter. Security and office support have long anchored contract value, while professional cleaning continues to see stable demand because regulatory and quality requirements remain high across controlled environments. Soft FM is also becoming more data-led, as occupancy-based cleaning and service scheduling tools help providers reduce labor hours and chemical use without lowering service quality.

Hard FM is forecast to grow at a 3.9% CAGR through 2031, making it the fastest-expanding service area in the Switzerland IFM Market. Asset management, preventive HVAC maintenance, fire and life safety checks, electrical upkeep, and building controls are increasingly included in the core of integrated contracts because they are tied to compliance rather than optional spending. MuKEn 2025 reinforces that shift by creating a recurring operational optimization cycle for non-residential buildings, which gives providers more regular technical work than in many other European settings. Federal property management also supports this direction, as the Swiss Federal Office for Buildings and Logistics oversees around 750 properties and has expanded professional energy data management across its estate under the Swiss Energy Act and related climate requirements. In the Switzerland IFM industry, this favours larger operators that can combine technical certifications, reporting systems, and multi-site delivery over smaller regional companies that still focus mainly on single-service work.

By End-User: Industrial and Manufacturing Leads, Commercial Outpaces in Growth

Industrial and Process Sector held 38.5% of the Switzerland IFM Market in 2025, which made it the largest end-user group. Switzerland’s pharmaceutical and life sciences base, especially across the Basel, Zug, and Zurich corridor, demands facility services that can work within GMP-regulated environments and handle documentation, validation, and operating discipline without gaps. That makes outsourcing attractive because clients would otherwise need to maintain costly in-house teams for cleaning, inspections, maintenance, and support services that already require specialist operating procedures. A large January 2026 mandate win by ISS Switzerland for a major life sciences and pharmaceutical client, valued at DKK 300 million (USD 43 million) annually across 4 Swiss sites, underscores the scale and strategic weight of industrial IFM outsourcing in the country. Precision engineering and watchmaking sites add to this base because uptime, controlled conditions, and equipment reliability matter more than simple cost reduction in those settings.

Commercial end-users are projected to grow at a 4.5% CAGR through 2031, making them the fastest-growing customer group in the Switzerland IFM Market. Offices, retail properties, logistics hubs, and hospitality venues are changing the way they buy FM because hybrid use patterns have made fixed service schedules less efficient than occupancy-responsive delivery. Providers with IoT-enabled platforms are therefore better placed to win new work, since they can match cleaning, reception, and space support to real-time building use instead of historic headcount assumptions. Flex-office space in Zurich expanded from 28,000 square meters in 2019 to 75,000 square meters by 2024, and those operators usually outsource all FM from the outset. Healthcare, education, retail, and government users fill the rest of the demand base, with public-sector outsourcing likely to deepen as cantonal authorities respond to building decarbonization targets and digital operating requirements without having comparable in-house capacity. In the Switzerland IFM industry, which keeps commercial demand broad even when office occupancies change from one district to another.

Geography Analysis

The largest pool of addressable contracts in the Switzerland IFM Market sits in the German-speaking north and center, where Zurich, Basel, Bern, Zug, and Lucerne concentrate multinational headquarters, pharmaceutical production, finance, and federal assets. Zurich and the wider Deutschschweiz region remain central because portfolio rationalization, office upgrades, and high-value technical estates continue to create demand for integrated operating models. Office vacancy across the 5 largest Swiss markets reached 5.2% by the end of 2025, suggesting ongoing building repositioning and replacement demand rather than a settled office landscape. The Basel-Zug corridor is especially important because pharmaceutical and life sciences sites require cleanroom support, validated cleaning, calibrated maintenance, and high documentation quality under strict operating standards. Federal estate activity also matters in this region, as the Swiss Federal Office for Buildings and Logistics manages around 750 properties and has expanded energy data management systems to support compliance and performance tracking.

French-speaking Switzerland shapes the Switzerland Integrated Facility Management Market with a distinct demand profile driven by international organizations, luxury hospitality, private banking, and healthcare assets. Geneva and Lausanne stand out because tighter occupancy conditions support premium service pricing and longer contract duration in well-located properties. Geneva’s office vacancy stood at 3.9% and Lausanne’s at 1.5%, which signals a firmer occupancy base than many other office districts and helps sustain steady FM demand. Digital transformation in public institutions is also raising service complexity in Romandy, as shown by the Canton of Vaud’s late-2025 investment of CHF 207.6 million, or USD 230 million, in next-generation hospital digital record infrastructure. Geneva has also been one of the more active cantons in the direction of energy compliance, which supports earlier Hard FM demand for building optimization and reporting work than in slower-moving jurisdictions.

Ticino remains the smallest geography by contract volume in the Switzerland Integrated Facility Management Market, but it still holds strategic value because it links Swiss operations with Northern Italian industrial supply chains and a growing life sciences base. Central and Eastern Switzerland, including Lucerne, St. Gallen, Appenzell, and Graubünden, are more reliant on manufacturing SMEs, tourism assets, and cantonal hospitals, so integrated adoption is lower than in the main urban centers but still rising. Across all regions, uneven MuKEn 2025 rollout means demand will arrive in waves rather than all at once, with early-adopting cantons pulling forward technical service cycles and late adopters delaying them. ISS Switzerland’s 2026 expansion of innovation hubs in Zurich and Lausanne reflects a deliberate attempt to serve both Deutschschweiz and Romandy with localized digital and technical capacity.

Competitive Landscape

The Switzerland Integrated Facility Management Market is moderately consolidated at the top, with a limited number of large providers leading major public and multinational contracts. ISS Switzerland sits at the front of that upper tier, with CHF 914 million (USD 1.16 billion) in FY 2025 revenue (USD 1.0 billion) and 83% of turnover generated through integrated mandates. That scale is reinforced by client retention above 97%, which shows how sticky enterprise contracts become once service delivery, helpdesk systems, and compliance processes are fully embedded. EQUANS Switzerland and CBRE Global Workplace Solutions also hold strong positions in technical FM and corporate real estate support, while Apleona Switzerland adds DACH-focused depth in integrated and technical FM with 1,700 employees, CHF 193 million (USD 244.3 million) in Swiss revenue, and 6.3 million square meters under management. The result is a market where the biggest contracts are contested by a limited set of scaled operators, even though regional and single-service activity remains widely dispersed.

Competitive differentiation in the Switzerland Integrated Facility Management Market is moving toward digital platform depth, energy management capability, and compliance credibility rather than price alone. ISS Switzerland’s Talk to the Building platform is a strong example because it uses real-time sensor data for predictive maintenance and energy optimization and won the Digital Economy Award 2025. Smaller technology-led firms are also moving closer to the FM decision chain, especially were data analytics and asset performance management overlap with traditional service delivery. Public and regulated private tenders increasingly value certifications and reporting capability, which makes national-scale operators more competitive than smaller providers that lack the same systems and audit readiness. ProNet Services’ capital transaction in 2024 and Bain Capital’s February 2025 acquisition of Apleona both indicate that investors still see room for consolidation, capability building, and decarbonization-led growth in this field.

The Switzerland Integrated Facility Management Market still offers room in mid-sized industrial sites and in underdeveloped canton-government mandates, but entry is harder than the number of providers might first suggest. High switching costs, long contract lives, and regulated operating environments protect incumbents when service quality is strong. ISS Switzerland’s January 2026 life sciences contract win is a good example because the deal moved the company from subcontractor to primary IFM partner across 4 Swiss locations, which shows how deeper account penetration often matters more than pure new-logo expansion. The same pattern appeared in the company’s earlier integration of gammaRenax AG, which strengthened infrastructure FM density and helped deepen technical talent capacity in a labour-constrained market.

Switzerland Integrated Facility Management Industry Leaders

Coor Service Management Holding AB

ISS Facility Services AB

Sodexo AB

Compass Group Sverige AB

CBRE GWS Integrated Facilities Management AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ISS Switzerland secured a full Integrated Facilities Services contract with a major life sciences and pharmaceutical company, valued at approximately DKK 300 million (USD 43 million), annually and covering four Swiss locations. The three-year mandate, with a two-year extension option commencing in Q2 2026, encompasses technical services, GMP-regulated cleaning, logistics, laboratory support, and a central customer helpdesk, marking ISS's transition from subcontractor to primary IFM partner for this client.

- August 2025: The Conference of Cantonal Energy Directors adopted the revised MuKEn 2025 model energy regulations, mandating renewable-only heating for replacement systems, periodic operational optimization for non-residential buildings, increased on-site PV generation requirements, and CO2-free public building operations by 2040. Cantons are recommended to implement the regulations by 2030, generating a multi-year compliance-driven Hard FM investment cycle across Switzerland.

- March 2025: ISS Switzerland reported FY 2025 revenue of CHF 914 million (USD 1.16 billion), or approximately USD 1.0 billion, up 1.4% from FY 2024, with 990 energy analyses conducted under its Pioneer sustainability program, 48 new photovoltaic systems installed, and a 15% reduction in fossil-fuelled fleet vehicles. The company also received an EcoVadis Gold medal for sustainability performance

- February 2025: Bain Capital announced the acquisition of Apleona, one of Europe’s largest integrated FM providers, from PAI Partners. In Switzerland, Apleona employs 1,700 staff, generates CHF 193 million (USD 244.3 million), or approximately USD 219 million at 2024 exchange rates, in annual revenue, and manages a portfolio of 6.3 million square meters. The transaction is intended to fund digital transformation and expansion in decarbonization-focused FM services across the DACH region.

Switzerland Integrated Facility Management Market Report Scope

The Switzerland Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels), Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the 2031 value forecast for integrated facility management in Switzerland?

The Switzerland Integrated Facility Management Market is forecast to reach USD 975.6 million by 2031, up from USD 824.1 million in 2025, with a 3.4% CAGR over 2026-2031.

Which service category leads demand in Switzerland?

Soft FM led demand with a 63.7% share in 2025 because cleaning, security, catering, and workplace support still form the base of most integrated contracts.

Which service area is growing faster through 2031?

Hard FM is growing faster at a 3.9% CAGR because energy rules, technical compliance, and asset optimization are making preventive maintenance and systems management more important.

Which customer group creates the largest revenue pool?

Industrial and Manufacturing led with 38.5% of demand in 2025, supported by pharmaceutical, life sciences, precision engineering, and watchmaking facilities that need tightly controlled service delivery.

Why are commercial properties becoming a stronger source of growth?

Commercial end-users are growing at a 4.5% CAGR as hybrid workplace models, flex-office growth, and occupancy-based service models raise the value of integrated operating support.

What is the biggest operating risk for providers in Switzerland?

The biggest risk is labour scarcity, with 84% of Swiss FM professionals identifying personnel shortages as the main market constraint in 2025, which puts pressure on cost, service reliability, and tender execution.

Page last updated on: