Norway Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

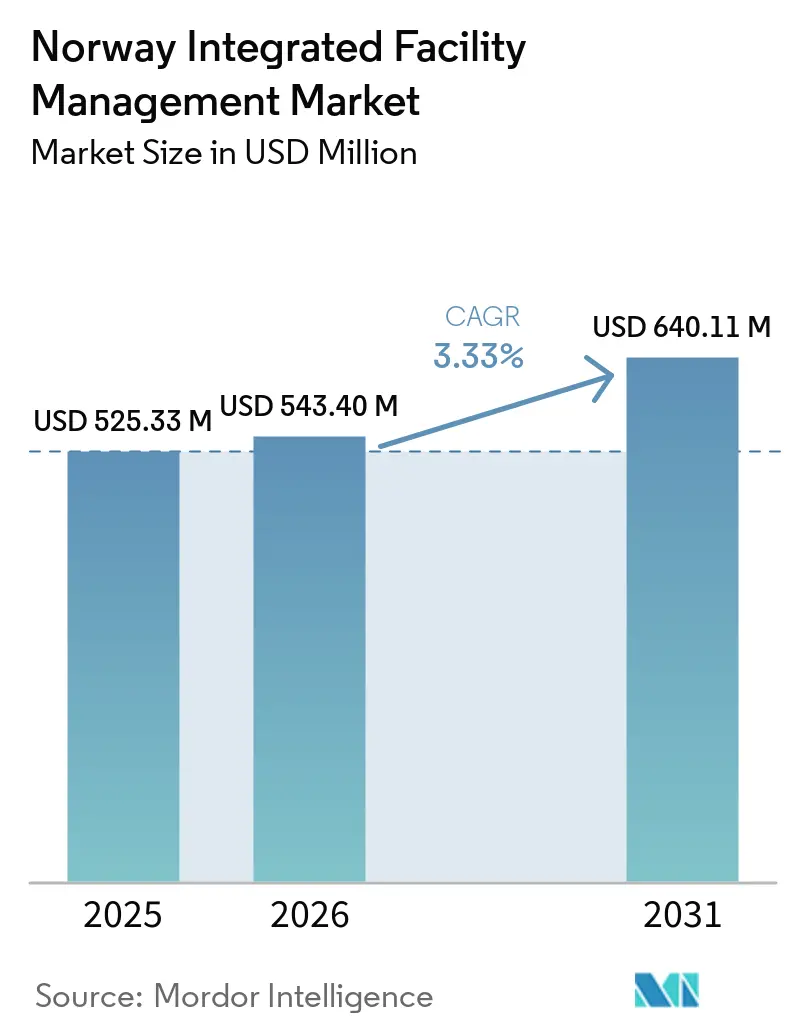

| Base Year Market Size (2025) | USD 525.33 Million |

| Market Size (2026) | USD 543.40 Million |

| Market Size (2031) | USD 640.11 Million |

| Growth Rate (2026 - 2031) | 3.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Integrated Facility Management Market Analysis by Mordor Intelligence

The Norway integrated facility management market size is projected to expand from USD 525.33 million in 2025 and USD 543.40 million in 2026 to USD 640.11 million by 2031, registering a CAGR of 3.33% between 2026 to 2031. The Norway integrated facility management (IFM) market is supported by a high-income domestic economy, stable public capital planning, and a building base that is aging while also facing rising retrofit requirements. Public procurement remains a core demand anchor because state-backed infrastructure renewal has been less exposed to short-term budget swings than in many other European markets, which supports longer contracts and broader service bundling. The 2024 procurement rule change that raised the weight of environmental criteria in public tenders has pushed buyers toward providers that can combine technical capability, compliance delivery, and measurable sustainability outcomes. Large maintenance backlogs in public buildings are also moving more work toward bundled contracts instead of stand-alone service lines, which strengthens the role of integrated operators with wider delivery scope. Labor shortages, margin pressure in soft services, and the cost of digital platform investment remain the main constraints, which means scale, workforce depth, and technology capacity are becoming more important in competitive positioning in the Norway IFM market.

Key Report Takeaways

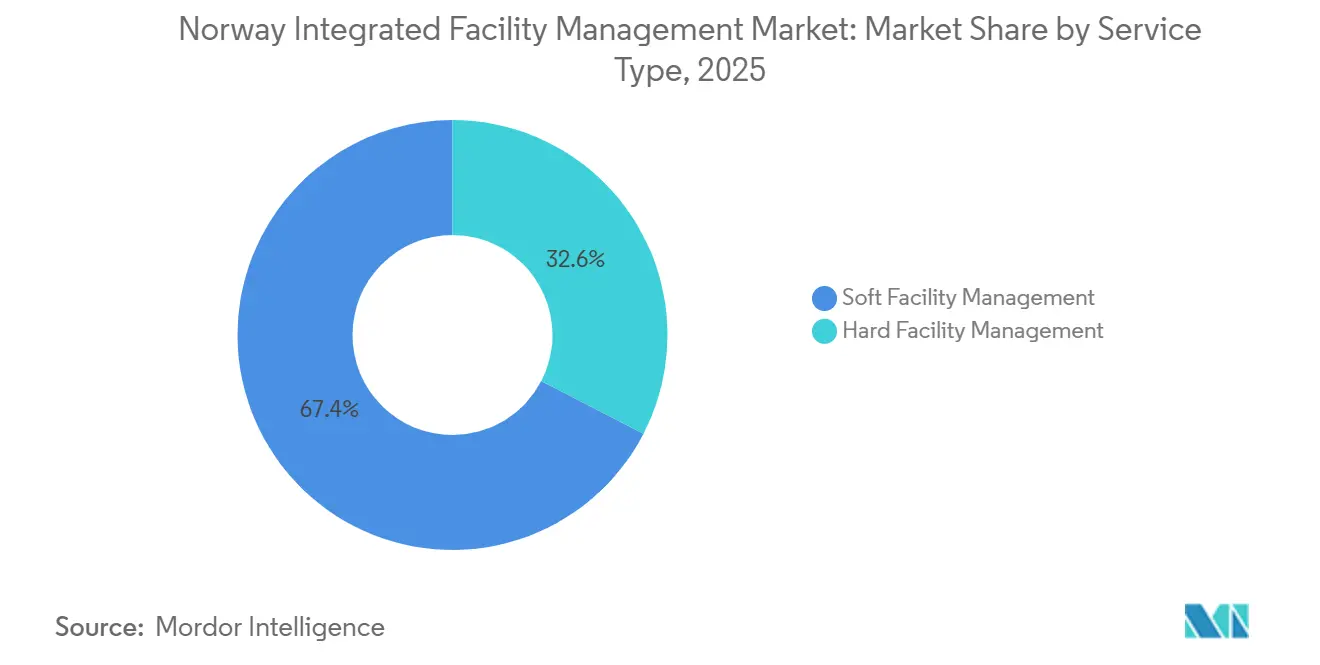

- By service type, Soft Facility Management (soft FM) held 67.41% of the Norway integrated facility management market share in 2025, while Hard Facility Management (hard FM) is forecast to expand at a 4.18% CAGR through 2031.

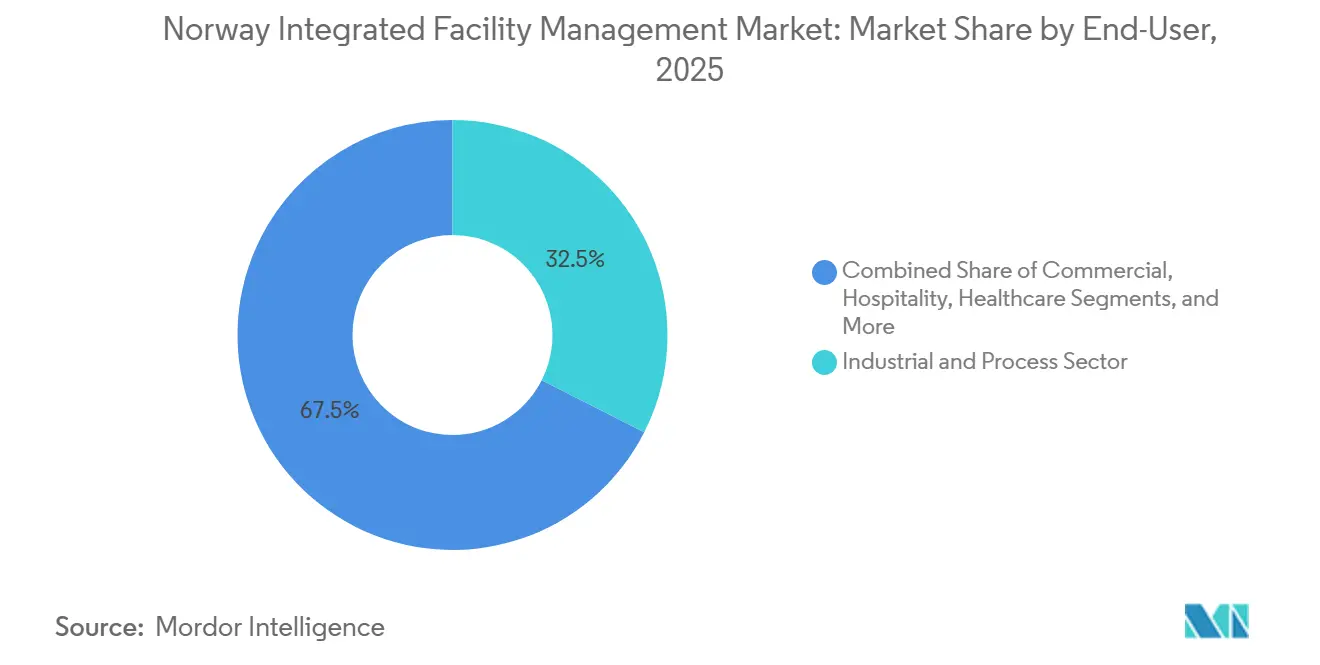

- By end-user, industrial held 32.47% of the Norway integrated facility management (IFM) market share in 2025, while commercial is forecast to grow at a 4.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Norway Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Public Procurement Frameworks and Mandatory Compliance Requirements | +0.7% | National, with concentrated demand in Oslo, Bergen, Stavanger | Short term (≤ 2 years) |

| Aging Physical Construction Towards Emerging Facility Management Awareness | +0.6% | National | Medium term (2-4 years) |

| Increasing Sustainability and Energy Efficiency Requirements Driving the Shift | +0.5% | National | Medium term (2-4 years) |

| Digital Transformation, Adoption of Smart Building Technologies and Automation | +0.4% | National, urban-led with Oslo and Trondheim as early adopters | Long term (≥ 4 years) |

| Health-Conscious Estate Culture Strengthening Post-Market Pull | +0.2% | National | Short term (≤ 2 years) |

| Local Construction Landscape Supporting FM Demand | +0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Public Procurement Frameworks and Mandatory Compliance Requirements

The Norway integrated facility management (IFM) market continues to benefit from a procurement structure that creates reliable demand beyond what the private sector alone would support. Statens innkjøpssenter, administered by DFØ, had total contract value of NOK 85.15 billion (USD 8.1 billion) across 297 tender notices as of May 2026, with 50 notices active at that date.[1]Anbudsregisteret, “Statens Innkjøpssenter v/DFØ, Anbud Og Kontrakter,” Anbudsregisteret, anbudsregisteret.no The 2024 amendment to Anskaffelsesforskriften requires environmental criteria to account for at least 30% of award weighting in most public tenders, which has changed how IFM providers present bids and document results. This rule now acts as a practical entry filter because providers that cannot prove performance on energy, waste, and labor conditions are less competitive in structured public contracts. The procurement framework also supports dynamic purchasing systems and framework agreements, which creates recurring entry points across service categories instead of a single closed tender cycle. That structure supports continued outsourcing in the Norway integrated facility management market while also favoring providers that can bundle compliance, service delivery, and long contract management under one operating model.

Aging Physical Construction Towards Emerging Facility Management Awareness

The Norway integrated facility management market is also being lifted by a large and persistent maintenance burden across public buildings. Norges Tilstand 2025 estimated total upgrade need for Norwegian public buildings at nearly NOK 300 billion (USD 28.5 billion), with hospitals facing a NOK 67 billion (USD 6.4 billion) backlog and many public buildings already at advanced age.[2]Rådgivende Ingeniørers Forening and Multiconsult, “Norges Tilstand 2025,” RIF, rif.no The same body of assessment gave condition score 3, which signals extraordinary maintenance need, across hospitals, municipal and county buildings, and the defense estate portfolio. In healthcare, 47% of Norwegian hospital buildings were reported to be in unsatisfactory technical condition, and the government in 2026 is proposing NOK 26 billion (USD 2.5 billion) in loan authorizations for five new hospital projects. Defense infrastructure adds another layer of demand because Forsvarsbygg faces an estimated NOK 30-36 billion (USD 2.9-3.4 billion) upgrade requirement on assets that are more than 40 years old on average. As owners shift these needs into life-cycle maintenance and energy performance contracts, larger IFM providers gain an advantage because they can absorb both the technical scope and the contractual risk over longer terms.

Increasing Sustainability and Energy Efficiency Requirements Driving the Shift

The Norway integrated facility management (IFM) market is being reshaped by climate compliance and by a stronger link between building performance and service scope. Norway’s Climate Act keeps a 2030 target of 55% reduction in greenhouse gas emissions relative to 1990 levels, which keeps building operations under close policy focus. In H1 2025, Enova allocated NOK 593 million (USD 56.3 million) across 894 building and property projects, with more than 500 of those projects tied to commercial building mapping or performance improvement.[3]Enova, “Bygg Og Eiendom, Enovas Halvårsrapport H1 2025,” Enova, enova.no From January 2026, Enova tightened its commercial building support rules by requiring at least 20% reduction in both delivered and net energy demand for each project, which moves support toward deeper retrofit measures rather than stand-alone installations. That change increases the relevance of IFM providers that can manage HVAC optimization, insulation coordination, controls, and performance follow-up within one service package. It also strengthens contract renewal prospects for providers that help owners align projects with incentive requirements, because FM delivery is now tied more closely to measurable energy outcomes than to routine service quality alone.

Digital Transformation, Adoption of Smart Building Technologies and Automation

The Norway integrated facility management market is moving through a gradual but important digital upgrade, especially in higher-value contracts. SINTEF launched the Nordic Smart Building Initiative in 2025 with 40 participants from 27 institutions across 13 countries, which gives the Norwegian market a broader development base for smart building use cases. SINTEF also launched the jAInitor project for 2025-2029 to develop AI-based tools that detect and diagnose HVAC faults linked to an estimated 0.5-1TWh of unnecessary energy use in Norwegian commercial buildings. In the private building base, Jarlhalla Group reported 10-20% reductions in delivered energy and 10-15% reductions in peak power over 12 months after deploying digital twins in Norwegian non-residential buildings. These results are pushing digital tools from optional add-ons toward expected capability in technically complex tenders. Providers that still rely on manual workflow, limited analytics, or third-party systems without integration depth are therefore at a growing disadvantage in the upper tier of the Norway IFM market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled and Qualified FM Talent | -0.5% | National, most acute in Oslo, Western Norway, and Agder | Short term (≤ 2 years) |

| High Provider Saturation Compressing Margins | -0.3% | National | Medium term (2-4 years) |

| Fragmented Building Ownership Among Housing and Long-Term Owners | -0.2% | National | Long term (≥ 4 years) |

| Limited Standardization and Prevalence of Bilateral Contract Practices | -0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled and Qualified FM Talent

Labor availability remains one of the clearest limits on the Norway integrated facility management market, especially in hard services. Norway recorded a workforce deficit of nearly 39,000 workers in 2025, and skilled trades accounted for more than 43% of unfilled positions, including electricians, plumbers, industrial mechanics, and welders that are central to technical FM delivery. NAV’s 2025-2035 outlook also showed that the population aged 67 and above will account for most national population growth by 2035, which means the pressure on the working-age base will continue. The strain is already visible in adjacent service settings, where a SINTEF study published in February 2026 found that nursing staff were still taking on cleaning and kitchen tasks because support labor was not sufficient. EURES also reported active shortages of construction and building trades workers across Oslo, Agder, and Western Norway, which confirms the geographic spread of the issue. With employment immigration to Norway down sharply from earlier years, providers in the Norway IFM market face higher labor costs, slower mobilization, and greater delivery variance when contracts require technically qualified staff at scale.

High Provider Saturation Compressing Margins

Margin pressure is the second major brake on the Norway integrated facility management market, especially in the soft-service layer. Coor has stated that it holds around 40% share in large, complex IFM delivery in Norway and the Nordic region, which shows how strongly the upper tier is already concentrated among a small group of providers. ISS then raised the consolidation signal further in May 2026 by signing an agreement to acquire Tomagruppen, adding annual revenue of DKK 1.8 billion (USD 261 million) and more than 4,000 employees, subject to approval from the Norwegian Competition Authority. This concentration narrows the pool of large bundled contracts available to mid-tier rivals, while framework agreement structures in cleaning and catering keep buyer pricing power high. At the same time, regional specialists and subcontractors still compete in narrow scopes where inflation recovery is harder to secure and contract terms are less flexible. The result is a two-layer market where large players defend scale contracts through breadth and technology, while smaller firms face tighter pricing and weaker room for reinvestment across the Norway integrated facility management (IFM) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM Gains Ground Through Technical System Upgrading

Soft Facility Management (Soft FM) held 67.41% of the Norway integrated facility management market share in 2025, while hard FM will expand at a 4.18% CAGR through 2031. This lead reflects the steady use of cleaning, catering, office support, security, and receptionist services across public buildings, offices, healthcare estates, and institutional facilities. Cleaning remains the largest activity area inside soft services because hygiene standards stayed elevated and because cleaning is often bundled into wider service agreements instead of being bought separately. Catering is the second major contributor, and ISS secured a catering and guest services contract for the new Norwegian Government Quarter in October 2025 with annual value of NOK 62 million (USD 5.9 million), which shows the scale available in bundled public-service food operations.

Hard Facility Management (Hard FM) is gaining share because technical building management is moving closer to the center of contract design in the Norway integrated facility management market. HVAC services remain the largest hard-service activity because energy performance, retrofit support, and system reliability now matter more across aging estates and regulated buildings. Asset management is also advancing as public owners and industrial operators move from periodic inspection cycles toward condition-based maintenance supported by digital monitoring and structured data use. Fire and safety scope is rising with building age and compliance needs, which adds another recurring line of technical work for integrated providers. A peer-reviewed study published in Frontiers in Built Environment in March 2026, using Norwegian building data, reported more than 99% fault classification accuracy for hybrid AI-APAR models in commercial HVAC systems, which supports the case for predictive hard FM delivery rather than reactive maintenance alone.

By End-User: Industrial Volume Leads While Commercial Growth Stays Strongest

Industrial held 32.47% of the Norway integrated facility management market share in 2025, while commercial will grow at a 4.25% CAGR through 2031. Industrial demand stays large because Norway’s oil and gas assets, offshore platforms, manufacturing sites, and energy infrastructure need mixed service bundles that combine technical system oversight with cleaning, catering, accommodation, and safety support. Coor renewed its offshore FM agreement with Equinor in February 2025 for five years at annual value of SEK 260 million (USD 24.4 million), which underlines how durable and specialized offshore service contracts remain. Bravida also signed a multi-year Technical FM contract with Aker Solutions for the Verdal shipyard from January 2025, covering more than 90,000 sq m of property, which confirms the continued movement of site-level technical work into structured outsourced mandates.

Commercial is the fastest-growing end-user area because prime offices, hospitality assets, and other service-led properties continue to raise expectations on uptime, comfort, presentation, and sustainability. Multi-site commercial owners are using broader FM frameworks to standardize soft services and improve operating consistency across portfolios. Healthcare remains a major adjacent demand pool because Helse Sør-Øst managed around 2.8 million sq m of hospital property and allocated NOK 200 million (USD 19 million) annually for extraordinary maintenance in 2025 and 2026, while planned new hospital investments reached NOK 90 billion (USD 8.6 billion) through 2034. In March 2024, Oslo University Hospital awarded Norway’s largest energy performance contract to Caverion, targeting 60GWh of annual energy reduction by 2030 across 1 million sq m, and that structure has become a visible model for technically intensive FM procurement in hospital estates. The remaining end-user base, including civic facilities, prisons, residential cooperatives, and leisure assets, continues to add stable demand through municipal agreements and long-duration management arrangements that sustain the Norway IFM market outside the largest contract tier.

Geography Analysis

The Norway integrated facility management market size stands at USD 543.40 million in 2026, and the country functions as a single national market with clear concentration around its largest public, commercial, and industrial property clusters. Public procurement remains one of the strongest geographic demand anchors, and the national framework administered through DFØ continues to channel large volumes of tender activity into major urban and institutional property portfolios. Oslo has particular weight because municipal and government property programs create repeated demand for bundled services, data systems, and sustainability-linked service models. Western and offshore-oriented parts of the country remain important because industrial and energy assets require technically heavier FM packages that combine accommodation, cleaning, maintenance, and operational support. Even without domestic sub-segmentation in the table of contents, national demand in the Norway integrated facility management market is not evenly spread, because contract scale is visibly higher in urban public estates and in energy-linked asset corridors.

Public buildings create the broadest nationwide service base because the maintenance backlog runs across hospitals, municipal buildings, county assets, and defense estates. Norges Tilstand 2025 estimated nearly NOK 300 billion (USD 28.5 billion) of upgrade need for Norwegian public buildings, which means outsourcing demand is supported across far more than just Oslo-based assets. Healthcare is especially important geographically because Helse Sør-Øst alone manages around 2.8 million sq m of property, while new hospital projects and maintenance programs are expanding across several locations. Defense and municipal infrastructure also extend the national footprint of the Norway integrated facility management market because older assets outside the main cities still require structured technical upkeep and life-cycle management.

Labor and operating conditions vary by place, and that makes geography important even in a single-country market. EURES identified shortages of building and trades workers in Oslo, Agder, and Western Norway, which means mobilization pressure is not limited to one local labor pool. Digital adoption is also developing first in larger urban and institutional settings, where programs such as NSBI and projects such as jAInitor are closer to practical deployment in commercial buildings and large public estates. For that reason, the geography of the Norway integrated facility management market is best understood as a national opportunity with stronger intensity in public-sector centers, healthcare estates, and industrial corridors rather than as a simple uniform domestic demand field.

Competitive Landscape

The Norway integrated facility management market remains moderately concentrated in its upper tier, where ISS, Coor Service Management, and Assemblin Caverion hold much of the structured contract space while a fragmented regional layer handles smaller scopes and specialist work. Coor has stated that it holds around 40% share in large, complex IFM delivery in Norway and the Nordic region, which illustrates the scale advantage already present at the top end. ISS also entered a major consolidation step in May 2026 through its planned acquisition of Tomagruppen, which would add more than 4,000 employees and broaden its reach across cleaning, catering, and property management in Norway. This leaves the Norway integrated facility management market with a clear split between a few full-scope operators and a wider field of subcontractors, local specialists, and narrow-service providers.

Strategy is increasingly shaped by technical depth, digital tools, and contract design rather than by labor scale alone. Coor uses SmartEnergy, SmartClimate, and SmartDrone capabilities as part of its integrated offer, which supports more data-led cleaning schedules, energy control, and predictive maintenance positioning. CBRE Norway also highlights analytics drawn from more than 15 million annual work orders in its global FM platform, showing how technology-backed routing and asset management are becoming standard competitive claims in larger accounts. Caverion has reinforced its technical profile through the Oslo University Hospital energy performance contract and through its five-year agreement with Telenor Towers Norway that began from January 2026, covering cooling, emergency power, and energy-efficient solutions. Specialist capability still matters below the top tier, and KTV Group secured a nationwide framework with ISS in March 2025 and later won an Oslobygg framework in May 2026 for drone-based façade and window cleaning, which shows that targeted expertise can still open access to larger supply chains.

The clearest white space sits below the major contract layer, where housing cooperatives, smaller municipalities, and mid-sized landlords still use bilateral or less formal sourcing practices. That fragmentation keeps contract values smaller and slows formal market development, but it also creates room for providers that can offer structured quality without the cost base of a top-tier operator. Procurement compliance and ESG documentation are gradually pushing more buyers toward formal selection models, which should favor providers with certified systems and stronger reporting capacity. Over the forecast period, the Norway IFM market is likely to reward scale, workforce resilience, and digital operating capability more than broad geographic presence alone.

Norway Integrated Facility Management Industry Leaders

ISS Facility Services AS

Coor Service Management Group AB

Toma Gruppen AS

Sodexo Norge AS

Compass Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ISS signed an agreement to acquire Tomagruppen AS, a Norwegian majority family-owned FM company operating in Norway and Denmark, with a workforce of over 4,000 employees and 2025 total revenue of DKK 1.8 billion (USD 261 million). The transaction was subject to approval from the Norwegian Competition Authority and was expected to materially strengthen ISS's position across cleaning, catering, and property management in Norway.

- May 2026: KTV Group won a framework agreement with Oslobygg KF for drone-based façade and window cleaning services for Oslo municipality's building portfolio.

- April 2026: KTV Group announced its integration into Dura Group, a Nordic group, to support further growth and development across its Norwegian operations.

- March 2026: ISS received an EcoVadis Gold Sustainability Rating, placing the company among the top 5% of all globally assessed organizations for sustainability performance.

Norway Integrated Facility Management Market Report Scope

The Norway Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-user Industries |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

What is the Norway integrated facility management market size in 2026 and how large will it be by 2031?

The Norway integrated facility management market size is USD 543.40 million in 2026 and is forecast to reach USD 640.11 million by 2031 at a 3.33% CAGR.

Which service category leads demand in Norway integrated facility management?

Soft FM leads the market, holding 67.41% share in 2025, supported by cleaning, catering, office support, security, and reception services across public and commercial buildings.

Which end-user group contributes the most revenue in Norway?

Industrial is the largest end-user segment with 32.47% share in 2025, driven by offshore energy assets, industrial sites, and infrastructure that need broad technical and support service bundles.

Which end-user segment is growing the fastest through 2031?

Commercial is the fastest-growing end-user segment with a 4.25% CAGR, supported by rising service expectations in offices, hospitality, and other private property portfolios.

What is pushing hard FM demand higher in Norway?

Hard FM is gaining momentum because aging buildings, energy-efficiency rules, and digital maintenance tools are raising demand for HVAC, asset management, fire systems, and predictive technical services.

What are the biggest challenges for providers operating in Norway?

The main challenges are shortages of skilled FM labor, margin pressure in soft services, and the investment needed for digital systems, all of which make scale and workforce depth more important.

Page last updated on: