North America Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

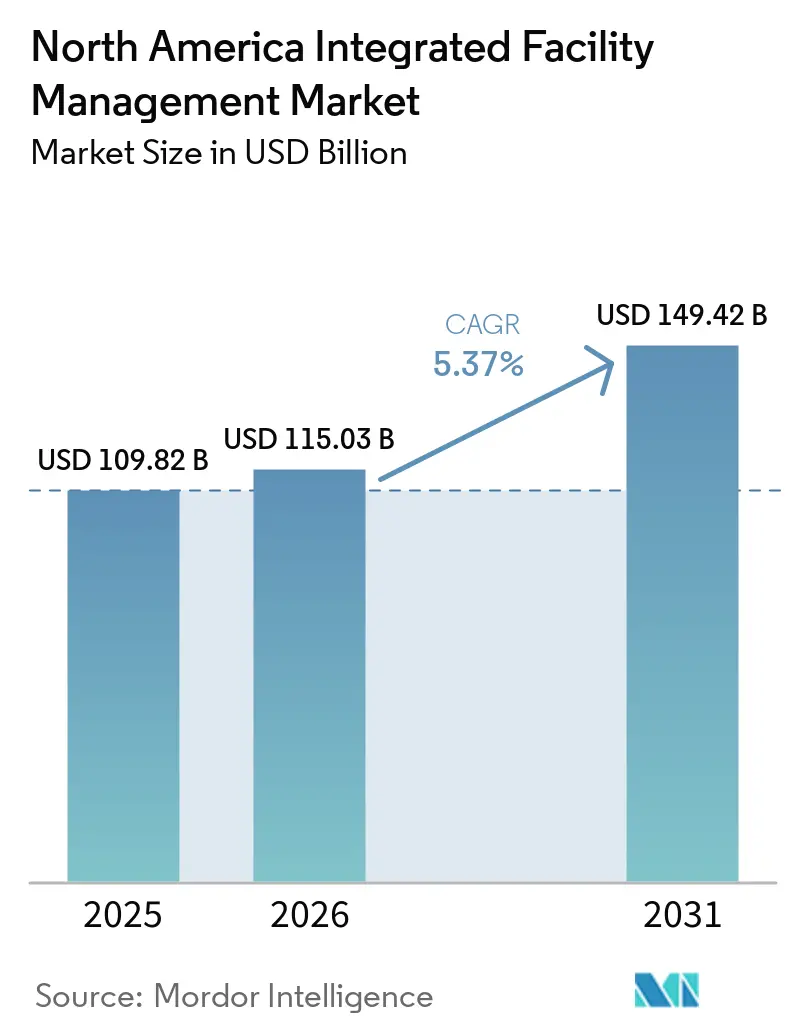

| Base Year Market Size (2025) | USD 109.82 Billion |

| Market Size (2026) | USD 115.03 Billion |

| Market Size (2031) | USD 149.42 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Integrated Facility Management Market Analysis by Mordor Intelligence

The North America integrated facility management market size is projected to expand from USD 109.82 billion in 2025 and USD 115.03 billion in 2026 to USD 149.42 billion by 2031, registering a CAGR of 5.4% between 2026 to 2031. In the North America integrated facility management (FM) market, outsourcing cycles are moving faster as organizations combine fragmented contracts into unified delivery models to control operating costs. JLL reported that 84% of FM leaders cited rising operating costs and budget constraints as their top concern, while 81% said cost efficiency was the leading priority for the coming year, which continues to favor bundled contracts over multi-vendor structures.[1]JLL, “Global State of Facilities Management Report 2025,” JLL, jll.com This budget pressure is shifting spending away from reactive maintenance and toward contracts that combine asset lifecycle management with predictive tools, which reduces administrative overlap and lowers subcontractor complexity. The market is also being supported by tighter energy compliance requirements, rapid data center construction, and wider use of AI across facility operations, all of which increase the value of providers that can manage technical services at scale. Competition remains moderately concentrated among global providers, while continuing mid-market acquisitions are narrowing the fragmented tier and adding pricing pressure for incumbent vendors.

Key Report Takeaways

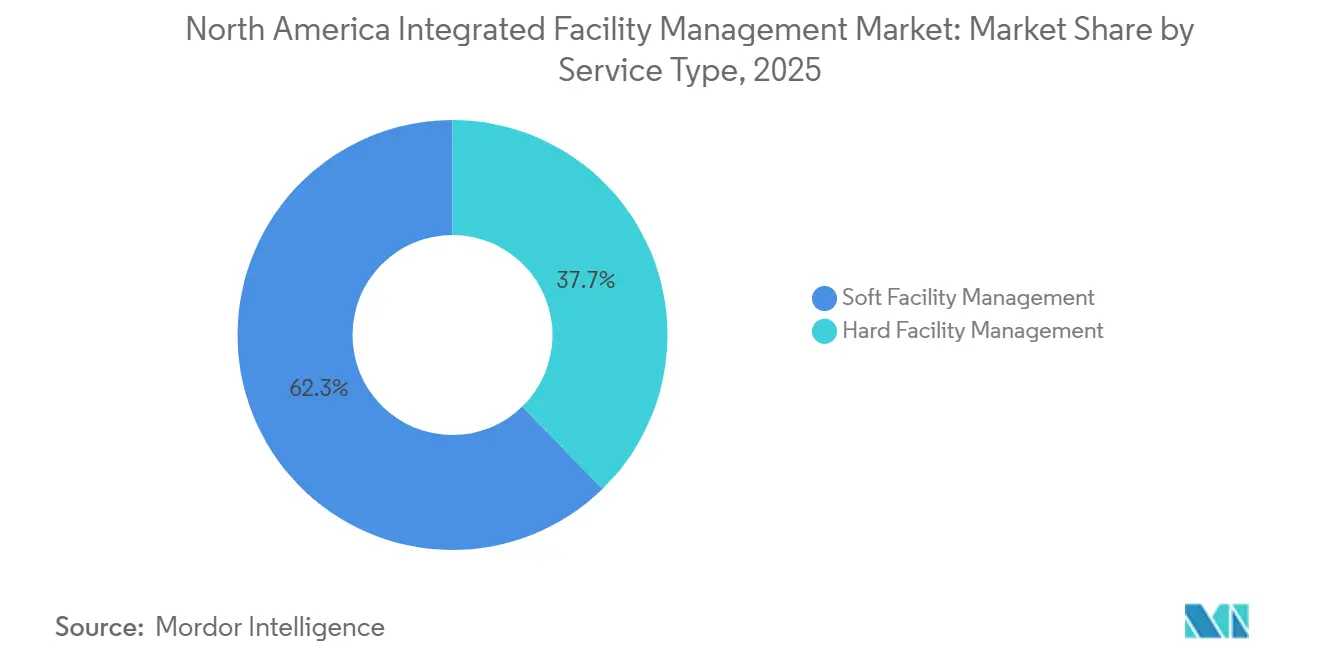

- By service type, Soft facility management held 62.3% of the North America integrated facility management market share in 2025, while Hard facility management is forecast to expand at a 6.7% CAGR through 2031.

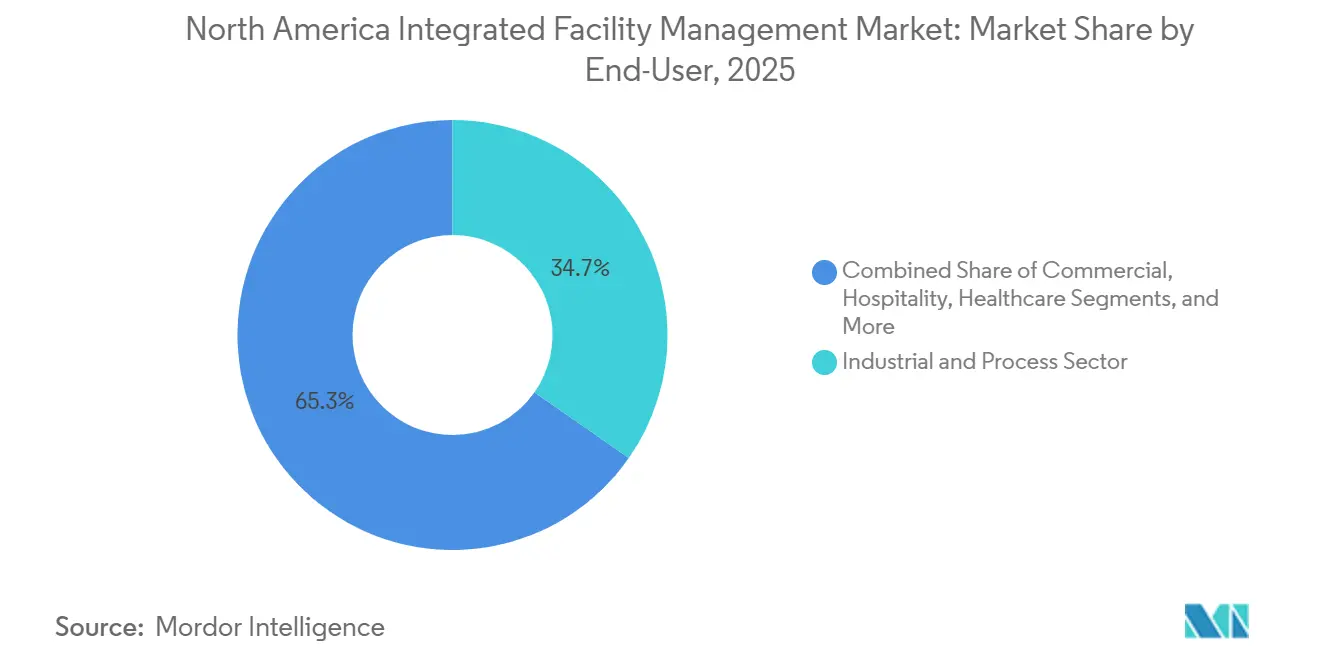

- By end user, the industrial and process sector accounted for 34.7% of the North America integrated facility management (FM) market size in 2025, while commercial is projected to advance at a 6.4% CAGR through 2031.

- By geography, the United States held 81.2% share of the North America integrated FM market in 2025, while Mexico is forecast to grow at a 5.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Operational Cost Optimization | +1.5% | Global, strongest in United States and Canada | Short term (≤ 2 years) |

| Increased Outsourcing of Non-Core Services | +1.2% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Rapid Adoption of Smart Building Technologies | +1.0% | United States and Canada, early gains in Mexico industrial zones | Medium term (2-4 years) |

| Stringent Energy Efficiency and Sustainability Regulations | +0.8% | United States, federal and state level, and Canada | Medium term (2-4 years) |

| Rising Tariff-Induced Supply Chain Reconfigurations Favoring Local IFM Providers | +0.5% | United States industrial belt, Mexico border manufacturing hubs | Medium term (2-4 years) |

| Expansion of Data Center Corridors Driving Specialized 24/7 FM Contracts | +0.4% | United States primary markets, expanding to secondary and Canadian markets | |

| Source: Mordor Intelligence | |||

Growing Demand for Operational Cost Optimization

The North America integrated facility management market is being pushed by cost control more than by short-term inflation concerns. JLL found that 81% of FM leaders planned to consolidate contracts with fewer suppliers and use data-led benchmarking as their main cost-reduction tools, which directly favors integrated providers over single-service vendors. ABM reported record new sales bookings of USD 1.9 billion in fiscal 2025, up 12% year over year, and linked that performance to client demand for single-source accountability and measurable operating savings.[2]ABM Industries Incorporated, “ABM Reports Fourth Quarter and Full Fiscal 2025 Results and Provides Fiscal 2026 Outlook,” ABM Industries, investor.abm.com This means IFM is increasingly being assessed as a way to reduce total occupancy cost, not only as an outsourced service package. That shift is especially relevant for organizations with large and dispersed portfolios because each contract consolidation expands the service scope that one IFM provider can hold.

Increased Outsourcing of Non-Core Services

The North America integrated facility management market is also benefiting from broader outsourcing across technical and workplace support functions. The outsourcing trend now extends beyond janitorial and catering into building automation, energy management, and MEP maintenance, which raises the average value of each contract. ABM said its self-performing workforce model can keep as much as 90% of staff directly employed rather than subcontracted, and that feature is gaining procurement appeal because it reduces service variability across locations. Johnson Controls reported in 2026 that 95% of employees were in the office at least 3 days per week, which means occupiers now need more consistent onsite response and service density than many in-house teams can deliver at scale. This is widening the buyer base for outsourced FM and pulling more organizations into integrated contracts that they had previously delayed for internal reasons.

Rapid Adoption of Smart Building Technologies

The North America integrated facility management market is moving deeper into digital operations as smart building systems become more common across commercial portfolios. ASHB reported that 91% of commercial building operators in the United States and Canada had smart building systems in place in 2025, and average organizational spending on smart technologies exceeded USD 550,000 per year.[3]Association for Smarter Homes and Buildings, “New Research on Smart Building Trends and Technology Adoption,” ASHB, ashb.com Johnson Controls found that 65% of business leaders and 67% of FM professionals already used AI in facility operations, utilization, and maintenance, with predictive maintenance ranked as the top planned AI investment for 2026. The practical effect is that monitoring is turning into active control, which gives providers stronger evidence of cost savings and uptime improvement at renewal. Providers that do not build analytics, interoperability, and predictive maintenance into their service model are more exposed when large contracts come up for rebid.

Stringent Energy Efficiency and Sustainability Regulations

The North America integrated facility management market is also being lifted by tighter building energy and sustainability requirements. ASHRAE approved Addendum aq to Standard 90.1-2022 in May 2025, which raised the required onsite renewable energy capacity threshold for commercial buildings from 0.5 W/ft² to 0.75 W/ft². California published its 2025 Building Energy Efficiency Standards in July 2025 and expanded requirements around heat pump transitions and photovoltaic integration for new nonresidential construction. The U.S. Department of Energy also stated that new federal buildings in fiscal years 2025 to 2029 must meet a 90% reduction in onsite fossil fuel consumption under EISA Section 433, which broadens demand for providers with energy-specialized operating capability. As a result, compliance work is becoming a regular part of contract scope and is tying FM providers more closely to client reporting, performance tracking, and long-term building upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Technicians and FM Workforce | -0.8% | Nationwide, most acute in rural, remote, and high cost-of-living areas | Short term (≤ 2 years) |

| High Upfront Costs of Integrated Digital Platforms | -0.6% | United States and Canada mid-market, early-stage Mexico markets | Medium term (2-4 years) |

| Client Concerns Around Vendor Lock-In in Single-Source Contracts | -0.4% | United States and Canada enterprise segment | Medium term (2-4 years) |

| State-Level Variability in Licensing and Compliance Standards | -0.3% | United States, multi-state operators, with spillover to cross-border North American operators | |

| Source: Mordor Intelligence | |||

Shortage of Skilled Technicians and FM Workforce

The North America integrated facility management market continues to face a structural labor constraint that limits how quickly providers can scale. IFMA data cited by REMI Network showed that the average time to fill a facility management role in North America reached 3.6 months in Q3 2025.[4]REMI Network, “FMs Brace for Rising Workloads and Tight Budgets,” REMI Network, reminetwork.com JLL also found that 45% of FM leaders viewed skilled trade labor shortages as a primary concern, with the pressure strongest in rural locations and high cost-of-living areas. In healthcare FM, HFM Magazine reported a 94% fill difficulty rate for HVAC trades, which shows how severe the shortage has become in technically sensitive environments. The problem is larger than recruitment alone because IFMA estimates that 40% of existing facilities managers will retire by 2026, which raises the risk of knowledge loss at the same time that contract complexity is rising in the NA integrated facility management market.

High Upfront Costs of Integrated Digital Platforms

The North America integrated facility management market also faces slower adoption among buyers that struggle with the initial cost of digital upgrades. ASHB found that purchase and implementation cost was the leading barrier to smart building adoption in 2025, cited by 36% of current users and 34% of non-users, with the range extending from 30% to 45% across building segments. The cost issue matters most in the mid-market, where many clients want integrated building systems and AI-enabled CMMS tools but still delay full rollout because the capital case is harder to justify. That leaves a band of portfolio owners in a partial transition stage, which can narrow contract scope and hold back margin expansion for providers. Vendors that can package digital tools through subscription or service-based models are better placed to win this demand without asking clients to absorb the full upfront investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Facility Management Ascending on the Back of Asset-Intensive Demand

Hard facility management is the fastest-growing service type in the North America integrated facility management market and is forecast to expand at a 6.7% CAGR through 2031. Demand is rising across asset management, MEP services, and fire systems and safety as investment continues in data centers, semiconductor fabs, and healthcare campuses where uptime has direct operating value. CBRE reported record net absorption of 2,497.6 MW in North American data centers during 2025, while vacancy in primary markets fell to 1.4%, which supports a long pipeline of technically intensive service contracts.[5]CBRE, “North America Data Center Trends H2 2025,” CBRE, cbre.com Johnson Controls also found that predictive maintenance was the top AI investment priority for 52% of facility managers planning new AI deployments in 2026, which strengthens the position of Hard FM providers with engineering and data capability.

Soft facility management held 62.3% of the North America integrated facility management market share in 2025 and remains the largest revenue base across commercial, institutional, and hospitality properties. In the North America integrated facility management industry, cleaning services, office support and security, and catering services still account for most Soft FM demand, although cleaning remains the most price-sensitive part of the mix. Johnson Controls reported that 75% of organizations used workplace management technology for space management and planning in 2026, which is pushing soft service delivery closer to occupancy analytics and real-time staffing decisions. That shift is making Soft FM contracts more data-aware and more defensible when providers can connect service output with utilization trends and user experience.

By End User: Industrial and Process Sector Leads While Commercial Gains Speed

The industrial and process sector accounted for 34.7% of the North America integrated facility management market size in 2025 and remains the main demand anchor in the region. This reflects the scale of manufacturing reshoring, energy infrastructure expansion, and the service intensity required across oil and gas, critical utilities, and advanced production facilities. ABM reported that its Technical Solutions segment, which serves industrial and critical power environments, grew 18.7% year over year to USD 960.6 million in fiscal 2025, which matches the rising demand for specialized support in technical environments. ABM also announced in December 2025 that it had agreed to acquire WGNSTAR for USD 275 million to expand its semiconductor fabrication facility capabilities, which reflects how the North America integrated facility management industry is moving toward higher-value technical categories.

The commercial segment is projected to grow at a 6.4% CAGR through 2031 and is the fastest-rising end-user group in the North America integrated facility management market. Return-to-office densification, broader BFSI and IT occupier footprints, and continued growth in logistics and warehousing are all increasing service demand per site. Healthcare remains a technically demanding sub-market because ventilation, life safety, and compliance obligations favor providers with specialized engineering depth and documented process control. Institutional and public infrastructure also provide stable demand, and JLL’s December 2024 GSA contract for 22 federal facilities across Atlanta and South Carolina shows how public-sector procurement continues to support multi-site FM pipelines.

Geography Analysis

The United States held 81.2% of the North America integrated facility management market share in 2025 and remains the center of regional demand. Its position is supported by the size of its commercial real estate stock, its mature outsourcing culture, and a large public-sector procurement base linked to the GSA. The U.S. also has the deepest pipeline for technical FM because data center activity remains intense, with CBRE reporting a 36% year-over-year increase in supply to 9,432 MW and a year-end 2025 vacancy rate of only 1.4% in primary markets. Energy and sustainability compliance further strengthen the local market because ASHRAE 90.1, DOE federal rules, and ENERGY STAR benchmarking keep performance management embedded in building operations. JLL’s 2026 office fit-out cost guide also identified North America as the most expensive region globally for M&E fit-out at USD 3,200 per square meter, which reflects the intensity of technical building work that feeds service demand in the United States.

Mexico is the fastest-growing geography in the North America integrated facility management market and is forecast to expand at a 5.7% CAGR through 2031. Growth is being driven by nearshoring-led industrial investment that is creating newly commissioned facilities with multi-service operating needs. Rice University’s Baker Institute noted in February 2026 that nearly 45% of 2024 FDI committed to North America went toward manufacturing hub development, which supports a multi-year FM pipeline in cross-border production corridors . The result is a larger opportunity for providers that can handle bilingual service delivery, industrial uptime requirements, and regional contract coordination across the United States and Mexico.

Canada contributes a smaller but strategically important position in the North America integrated facility management market. Bell Canada announced in March 2026 a CAD 1.7 billion (USD 1.24 billion) investment in a 300 MW AI data center in Saskatchewan, which points to rising demand for critical environment FM in secondary Canadian locations. IFMA data cited by REMI Network showed strong workload growth expectations in Ontario and the Prairie region during Q3 2025, which suggests that FM sourcing activity is broadening beyond the largest urban markets. JLL’s September 2025 WestJet contract, covering 1.9 million square feet across 17 airport locations, also shows how transportation and aviation are emerging as valuable national sub-markets in Canada.

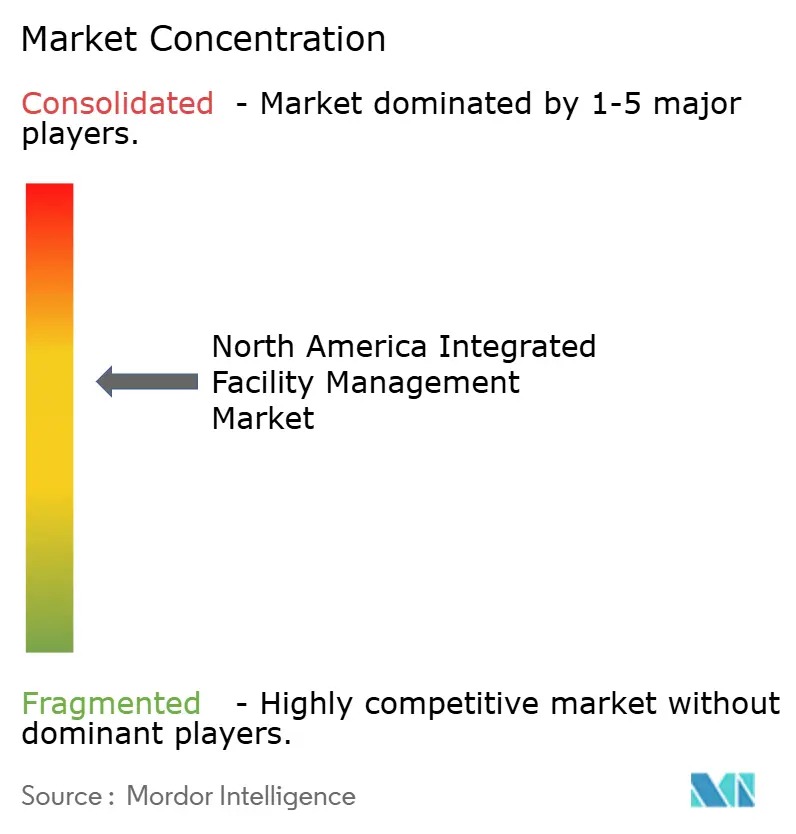

Competitive Landscape

The North America integrated facility management market remains moderately consolidated at the top end, where CBRE Group Inc., Jones Lang LaSalle Incorporated, ABM Industries Incorporated, Cushman and Wakefield plc, and ISS A/S compete for large enterprise and public-sector contracts. Beneath that tier, the market still contains a wide range of regional and specialty operators that compete on local responsiveness, sector depth, and self-performance models. A clear strategic pattern is capability expansion into technical categories that are harder to commoditize. ABM’s December 2025 agreement to acquire WGNSTAR for USD 275 million is a direct example because it strengthens the company’s position in semiconductor fabrication facility services, which are more specialized than general commercial FM. That direction fits the broader structure of the North America integrated facility management market, where providers are seeking revenue streams tied to critical environments, engineering depth, and longer contract duration.

Technology is becoming a stronger differentiator in the North America integrated facility management market because clients increasingly want platforms that connect service delivery, workflow, and building data. Johnson Controls reported that 33% of business leaders wanted to change their current FM management system due to integration complexity, which points to a real switching opportunity for providers with better interoperability. JLL’s May 2024 alliance with ServiceNow and the use of its Falcon platform show how large providers are shifting beyond labor scale and into workflow automation as a source of differentiation. That matters because buyers now expect a cleaner link between maintenance activity, occupancy trends, energy performance, and contract reporting.

White-space demand remains visible in mid-market healthcare portfolios, public-sector secondary markets, and Mexico industrial zones where technical integrated delivery is still developing. JLL’s March 2026 selection by Siemens Healthineers for a 5.3-million-square-foot portfolio across 32 states in the United States and Canada shows that life sciences and healthcare-related facilities are attracting large multi-site IFM mandates. GDI’s March 2026 go-private transaction also points to continuing interest in strategic reinvestment and cross-border expansion among established regional platforms. Compliance with ASHRAE standards, DOE rules, and ENERGY STAR benchmarking is also becoming a practical filter in vendor selection, which gives an advantage to providers that can show measurable execution in energy, maintenance, and reporting performance

North America Integrated Facility Management Industry Leaders

CBRE Group Inc.

Jones Lang LaSalle Incorporated

Sodexo S.A.

ISS A/S

ABM Industries Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: JLL was selected by Siemens Healthineers to provide integrated facilities management services across a 5.3-million-square-foot portfolio spanning 32 states in the United States and Canada. The contract covers engineering, HVAC maintenance, janitorial, fire and life safety, and workplace services, marking a significant expansion of JLL's life sciences FM footprint.

- March 2026: Bell Canada announced a CAD 1.7 billion (USD 1.24 billion) investment in a 300 MW AI data center in Saskatchewan, Canada's largest purpose-built AI data center, with construction commencing spring 2026 and first-stage commissioning expected in the first half of 2027. The facility is expected to generate a minimum of 80 full-time operational roles and create demand for critical environment FM services in a secondary Canadian market.

- March 2026: GDI Integrated Facility Services Inc. completed its go-private transaction, with Birch Hill Equity Partners acquiring all outstanding subordinate voting shares at CAD 36.60 (USD 26.5) per share, and GDI's shares were delisted from the Toronto Stock Exchange. The privatization is expected to accelerate GDI's strategic investments and cross-border expansion in Canada and the United States without public reporting pressures.

- December 2025: ABM Industries announced a definitive agreement to acquire WGNSTAR for approximately USD 275 million, targeting expansion into semiconductor fabrication facility management and benefiting from U.S. reshoring-driven domestic fab construction. The deal is expected to be accretive to ABM's earnings by 2027 and adds specialized cleanroom and critical environment capabilities.

North America Integrated Facility Management Market Report Scope

The North America Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)), and Geography (United States, Mexico, and Canada). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| United States |

| Canada |

| Mexico |

| By Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the expected value of the North America integrated facility management market by 2031?

The North America integrated facility management market is forecast to reach USD 149.42 billion by 2031, up from USD 115.03 billion in 2026.

Which service category leads revenue in North America integrated facility management?

Soft facility management led with 62.3% share in 2025, supported by strong outsourcing in cleaning, catering, office support, and related workplace services.

Which service category is growing fastest through 2031?

Hard facility management is the fastest-growing service type, with a 6.7% CAGR through 2031, supported by demand from data centers, healthcare campuses, and semiconductor facilities.

Which end-user group generates the most demand for integrated facility management in North America?

The industrial and process sector led with 34.7% share in 2025, reflecting manufacturing reshoring, energy infrastructure expansion, and demand from technical operating environments.

Why is Mexico growing faster than the rest of the region?

Mexico is forecast to grow at a 5.7% CAGR through 2031 because nearshoring and new manufacturing hub development are creating demand for multi-service FM contracts in industrial sites.

What are the biggest constraints on adoption across the region?

The main limits are skilled labor shortages and the high upfront cost of digital platforms, especially for mid-market buyers that want integrated systems but face tighter capital budgets.

Page last updated on: