United Kingdom Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

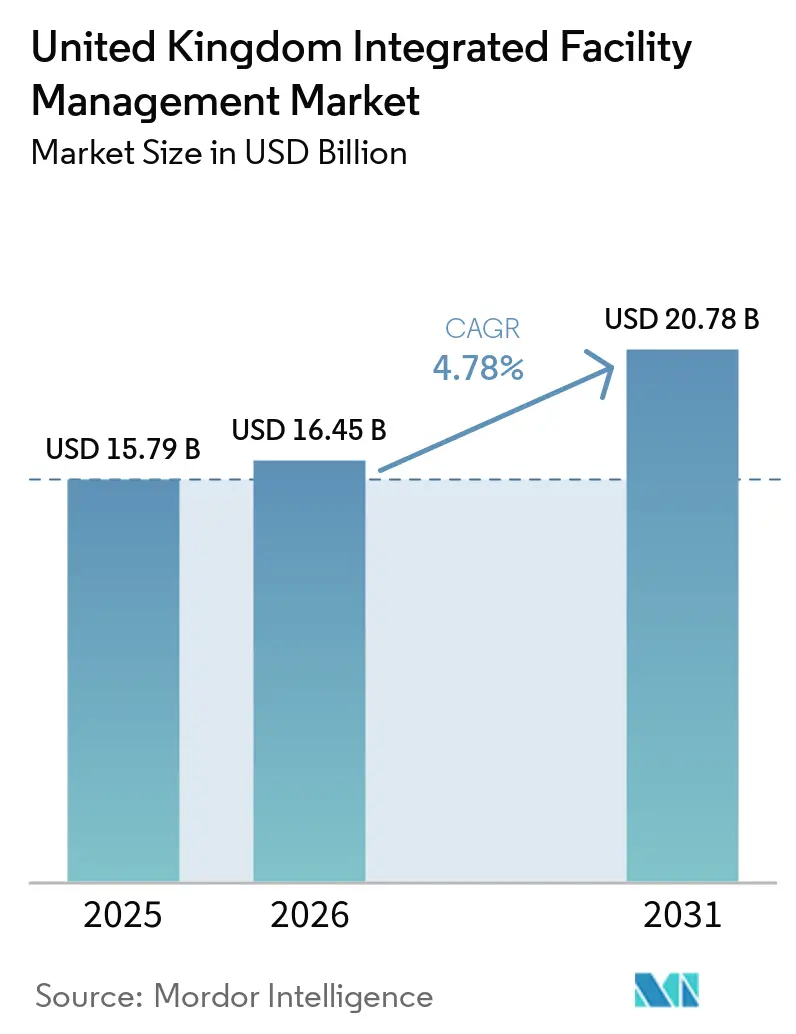

| Base Year Market Size (2025) | USD 15.79 Billion |

| Market Size (2026) | USD 16.45 Billion |

| Market Size (2031) | USD 20.78 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

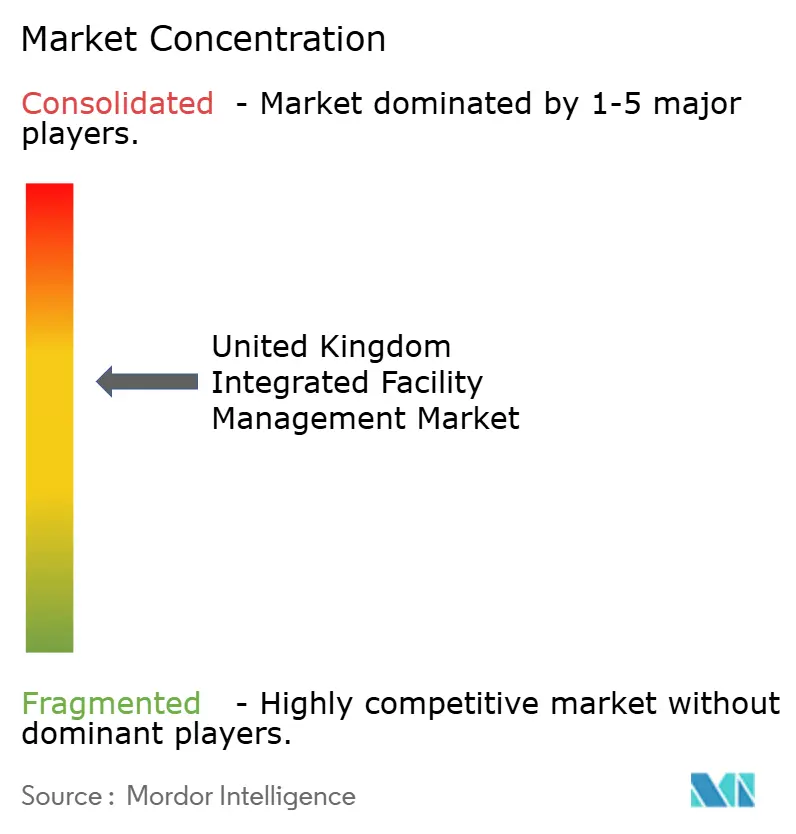

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Integrated Facility Management Market Analysis by Mordor Intelligence

The United Kingdom integrated facility management market size was valued at USD 15.79 billion in 2025 and is estimated to grow from USD 16.45 billion in 2026 to reach USD 20.78 billion by 2031, at a CAGR of 4.78% during the forecast period 2026-203. The United Kingdom integrated facility management market is expanding because hybrid work has changed how occupiers use offices, while the 2024 classification of data centers as critical national infrastructure has widened demand beyond traditional office and public estate contracts. Non-domestic buildings account for 12% of the country’s greenhouse gas emissions, which keep compliance, energy monitoring, and retrofit activity close to the center of FM buying decisions. The United Kingdom integrated facility management (IFM) market is also being reshaped by contract consolidation, as large occupiers and public bodies prefer fewer suppliers that can combine engineering, cleaning, security, and reporting under one operating model. Competition remains active rather than closed, as scale operators such as Mitie, OCS, ISS, Sodexo, CBRE GWS, Serco, and ENGIE UK continued to pursue large mandates across both public and private estates. The main constraint on the United Kingdom IFM market is margin pressure from labor shortages, higher employer costs, and fixed-price contracts, which favors providers with scale, better systems, and stronger specialist capability.

Key Report Takeaways

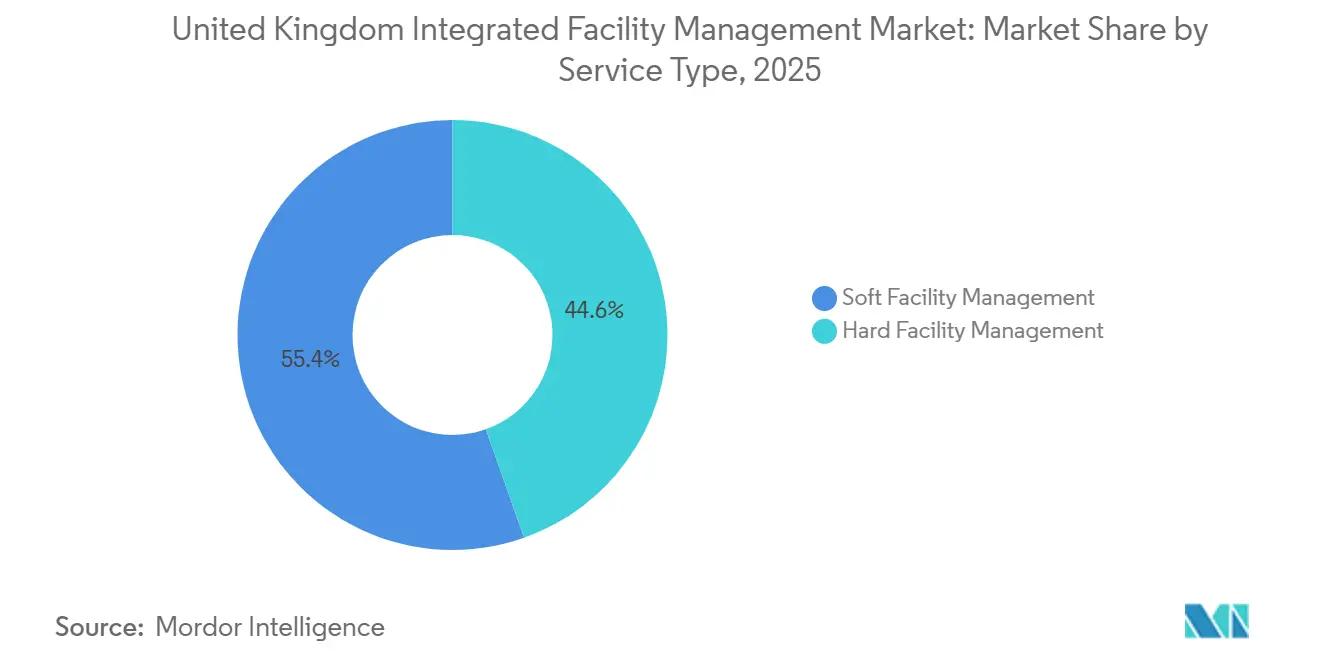

- By service type, soft facility management segment held 55.41% market share of the United Kingdom integrated facility management in 2025, while hard facility management segment recorded the fastest projected growth at a 5.38% CAGR through 2031.

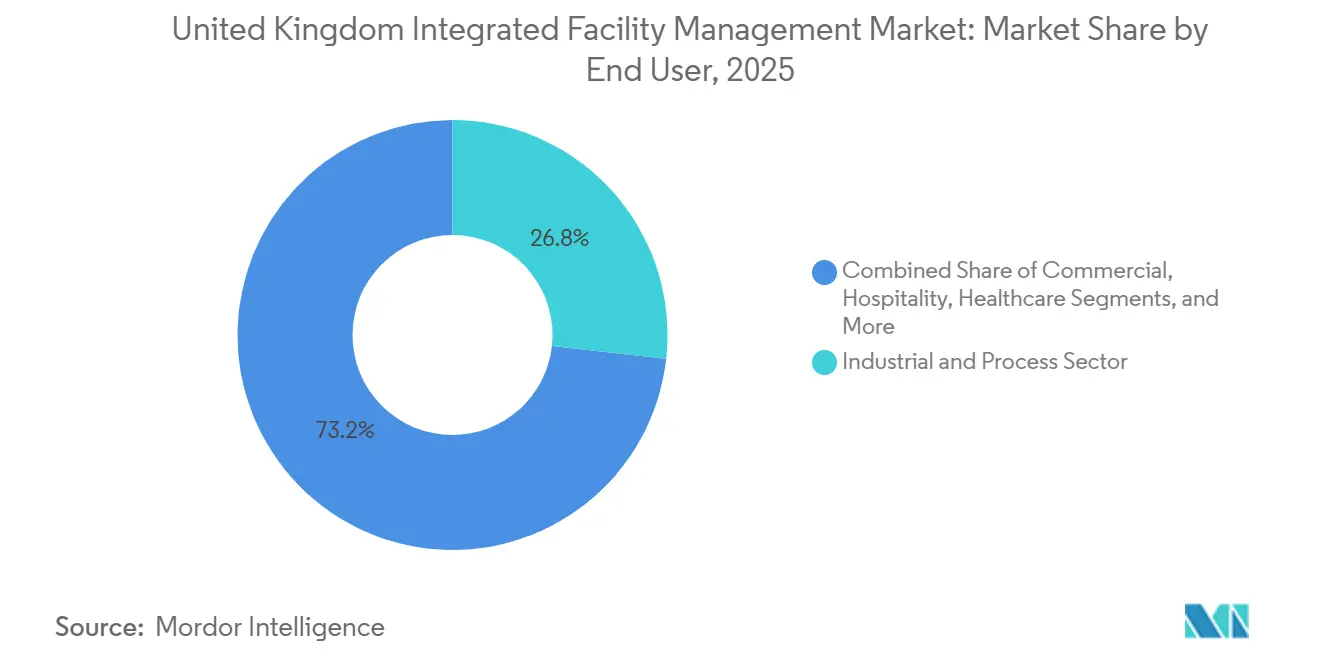

- By end-user, Industrial & Process held 26.77% share of the United Kingdom integrated facility management (IFM) market in 2025, while Commercial is forecast to expand at a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Data Centre Demand Driving Specialized FM | +1.4% | South East, M62 corridor, Wales, Scotland | Short term (≤ 2 years) |

| Adoption of Smart Building IoT Platforms for Productivity | +1.0% | Global, with concentrated gains in London, Manchester, Birmingham | Medium term (2-4 years) |

| Consolidating Procurement Among UK Corporates and Public Sector | +0.8% | National, with early gains in London, Edinburgh, Manchester | Medium term (2-4 years) |

| Rising FM Service Demand and Growth in Non-Core Facilities | +0.7% | National, with NHS and public estate concentration in the North and Midlands | Medium term (2-4 years) |

| Performance-Based FM Contracts Post-COVID | +0.5% | National, with higher adoption in Central Government and Defence | Long term (≥ 4 years) |

| Increased Supply Chain Consolidation with Tier FM Firms | +0.3% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Centre Expansion is Creating a New FM Demand Category

The 2024 reclassification of UK data centers as critical national infrastructure changed the service expectations around uptime, resilience, and physical security. January 2025 AI Opportunities Action Plan reinforced that direction by linking digital capacity expansion to new technical facilities and supporting infrastructure. For the United Kingdom integrated facility management market, this means demand is shifting toward round-the-clock M&E maintenance, cooling oversight, high-voltage electrical management, fire suppression controls, and specialist cleaning for sensitive environments. A February 2026 AECOM assessment warned that specialist mechanical, electrical, and public health subcontractor demand was already outstripping supply in London, which shows how quickly critical-environment demand is tightening labor capacity. CBRE’s December 2024 appointment across Kao Data’s UK portfolio showed that occupiers increasingly want one provider that can manage both hard and soft services across these sites. This leaves the UK integrated facility management market with a clear divide between scaled providers that already have critical-environment capability and generalists that still need to build it.

Smart Building IoT and CAFM Platforms are Raising the Productivity Baseline

The United Kingdom integrated facility management (IFM) market is moving away from a reactive work-order model as IoT sensors, BMS platforms, and CAFM systems become more closely connected across occupied estates. ESOS and SECR continue to support that shift because both frameworks increase the need for regular energy monitoring, documentation, and asset-level visibility. An IES digital twin deployment at Queen Margaret University in Edinburgh, which began in August 2025, identified annual energy savings of GBP 64,000 (USD 81,280), or 11% of the building’s energy spend through low-capital scheduling and control changes.[1]Integrated Environmental Solutions Limited, “Queen Margaret University,” iesve.com Clients are also writing energy and carbon KPIs into service agreements more often, which turns sustainability reporting into a contract performance issue rather than a separate ESG ambition. Late 2025 survey evidence showed that many FM leaders still had a large share of compliance tasks untracked or unautomated, which raises the risk of poor reporting, missed actions, and weak renewal discussions. In the United Kingdom IFM market, providers that can prove asset performance with live data are gaining a clearer edge in tenders and renewals.

Corporate Procurement Consolidation is Compressing the Supplier Base

Large occupiers and public bodies are reducing the number of FM suppliers they use, because bundled contracts lower coordination effort and make compliance reporting easier to manage across large estates. HMRC moved from five suppliers to two in late 2024, awarding Mitie a GBP 130 million (USD 165.1 million) contract, for the East Region.[2]Mitie plc, “HMRC East Region Contract Announcement,” Mitie, mitie.com Whereas Sodexo took a comparable integrated workplace services contract across 24 western region sites. The transaction pattern supports the same direction, as the average number of services offered by target companies in UK FM M&A rose to 2.1 in 2024 from 1.8 in 2022-2023. Mitie’s August 2025 acquisition of Marlowe for GBP 366 million (USD 464.8 million), brought engineering maintenance together with fire and security compliance under one broader facilities compliance proposition. This is making the United Kingdom IFM market harder for undifferentiated mid-tier providers, because contract wins now depend more on breadth, reporting capability, and specialist credibility than on price alone. The net effect is a smaller supplier field at the top end, even though the wider market remains crowded.

Public Sector Estate Backlog is Driving Non-Discretionary FM Demand

The UK government’s maintenance backlog rose from GBP 14.8 billion (USD 18.8 billion) in January 2019 to at least GBP 49 billion (USD 62.2 billion), by October 2024.[3]BCIS, “Maintenance and Cleaning Cost Forecasts,” BCIS, bcis.co.uk Ministry of Defence properties, NHS sites, and schools accounted for most of that burden, which means the need for outsourced upkeep is tied to essential public services rather than optional upgrades. The practical effects are immediate because deferred maintenance has already been linked to hospital ceiling failures, court delays, and thousands of clinical service incidents each year. The 2024 Autumn Budget allocated GBP 1 billion (USD 1.3 billion), to NHS maintenance, and NHS Shared Business Services launched GBP 375 million (USD 476.3 million), in new soft FM framework agreements in November 2024. Public bodies also face recruitment limits for in-house property specialists, which increases reliance on outsourced providers with established delivery teams and public-sector compliance experience. This supports medium-term visibility for the UK integrated facility management market, especially among providers with NHS and defense credentials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skills and Inadequate HR Service Capabilities | -1.2% | National, most acute in London, Manchester, and technically complex estate clusters | Short term (≤ 2 years) |

| Inflationary and Cost Pressures on Hard FM Industry | -1.0% | National, with cleaning and maintenance cost escalation most pronounced in high-wage urban centres | Medium term (2-4 years) |

| Post-Brexit Labour Mobility Constraints | -0.6% | National, most acute for low-skilled and specialist EU-origin roles in London and South East | Medium term (2-4 years) |

| Supplier Service Risks in Contract Bidding and Delivery | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills Shortage is More Than a Recruitment Problem

The United Kingdom integrated facility management market faces a structural labor gap rather than a short hiring cycle, because the issue now combines post-COVID attrition, an ageing workforce, and weak new entrant volumes. More than two-thirds of FM leaders said in 2025 that recruiting and retaining staff was difficult, and this fed directly into missed service levels and weaker day-to-day contract control. The technical side of the problem is even sharper, because HVAC, M&E, and fire systems roles need specialist training and multi-year qualification paths before staff can work independently. The commercial effect is severe because clients judge contracts on live service quality, not only on whether the contractor can point to effort or intent. That is why service complaints and non-renewal risk are rising even where providers are still delivering most contracted tasks. In the United Kingdom IFM market, the firms with stronger training pipelines, apprenticeship capacity, and better scheduling systems are pulling away from those that still rely on a thin external labor pool.

Cost Escalation in Hard FM Is Eroding Contract Profitability

BCIS expects building maintenance costs to rise by 15% and cleaning costs to rise by 23% over the five years to 2029-2030, with labor inflation as the main driver.[4]BCIS, “Maintenance and Cleaning Cost Forecasts,” BCIS, bcis.co.uk The April 2025 step-up in employer National Insurance contributions and the National Living Wage increase to GBP 12.21 (USD 15.5) per hour, added a direct cost layer across large frontline workforces. Mitie’s FY26 trading update estimated NIC-related cost headwinds at GBP 50 million, which was approximately USD 63.5 million, which shows the scale of exposure even for the market leader. Fixed-price contracts are the most exposed because providers that signed before April 2025 labor cost changes have limited room to recover margin unless renegotiation clauses were already in place. Labor accounts for most maintenance expenditure, so small efficiency gains cannot fully offset the underlying wage and tax pressure. In the United Kingdom integrated facility management market, this pressure is thinning the subcontractor base and making regional delivery harder for contractors that depend on small specialist firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard FM's Technical Complexity Premium Reshapes Margin Architecture

Hard FM is the fastest-growing service type in the United Kingdom integrated facility management market, with a projected 5.38% CAGR over 2026-2031. That growth is tied to higher technical intensity across data centers, life sciences sites, NHS estates, and older buildings that now face firmer safety and compliance requirements. Building fabric work, HVAC servicing, high-voltage electrical management, and fire safety compliance are all becoming more demanding in skill and documentation, which lifts both service complexity and the value of accredited teams. Deal activity points in the same direction, because energy services transactions in UK FM M&A rose by 67% between 2021 and 2024, while fire systems and lift services made up nearly one-third of 2025 FM deals. The plumbing and hard services contractor base also remains large, with an adjacent market valued at more than GBP 27 billion (USD 34.3 billion), in 2024 and projected to reach GBP 32.5 billion (USD 41.3 billion) by 2029.

Soft FM held 55.41% of the United Kingdom integrated facility management market size in 2025, which shows that recurring frontline services still form the volume base of the United Kingdom IFM market. Hybrid working has changed the pattern of those services rather than reduced their needs, because cleaning is now more occupancy-led, security is increasingly layered with CCTV and access control, and catering is being redesigned around hub-and-spoke office use. November 2024 NHS Shared Business Services launch covered linen and laundry, grounds maintenance, and security with a combined value of GBP 375 million (USD 476.3 million), underlining how institutional demand remains steady and large. Public-sector buyers are also raising entry thresholds through audit, health and safety, and infection-control requirements, which gives an advantage to providers with mature management systems and repeat public-sector experience. Within the integrated facility management industry, this leaves Soft FM as the scale anchor and Hard FM as the technical growth engine rather than a substitute.

By End-User: Industrial and Process Leads Share, Commercial Leads Growth

Industrial and Process end-users held 26.77% of the United Kingdom integrated facility management market share in 2025, making them the largest end-user group in the United Kingdom IFM market. This cluster includes data centers, manufacturing plants, energy infrastructure, and oil and gas assets, which all require more continuous and technically controlled service delivery than standard office buildings. The data center component is especially important because UK data center electricity demand is projected to reach 26.2 TWh by 2030, or 8.8% of total UK electricity demand, which implies a larger operational burden around uptime, cooling, and resilience. These contracts are also more likely to use outcome-based measures such as asset uptime, energy performance, and compliance reporting, which gives skilled providers a path to stronger contract quality over time. In the United Kingdom integrated facility management market, that combination of technical depth and continuous service need keeps Industrial & Process at the center of value creation.

Commercial end-users are the fastest-growing group, with a 5.63% CAGR projected through 2031 in the United Kingdom integrated facility management market. The driver is not simple office recovery, because tenants now expect higher air-quality visibility, quicker maintenance response, stronger workplace experience, and more consistent ESG-linked retrofit activity across Grade-A portfolios. Hybrid work has created a practical tension, since average occupancy can be lower while service expectations are higher, which means occupiers still need responsive FM even with fewer people on site each day. Hospitality contracts are also recovering, and CBRE’s September 2025 award at Coventry Building Society Arena showed how venues are turning to professional FM partners to improve daily operations and efficiency planning. Institutional and public infrastructure contracts remain the deepest long-duration pool, while utilities and leisure sites are widening the addressable base as PPP and PFI handbacks reach later stages. Across the integrated facility management industry, end-user growth is therefore broad, but Commercial is setting the pace.

Geography Analysis

Greater London and the Southeast command the largest revenue pool in the United Kingdom integrated facility management market because they hold the highest concentration of government estate, financial headquarters, healthcare infrastructure, and major logistics assets. Government clients represented 52% of Mitie’s FY25 revenue base, which shows how strongly public estate concentration still shapes competitive priorities in and around London. The same region remains central to current data center activity, with 7 of the 29 projects expected to start in 2026 located in London. That concentration supports demand for engineering, security, and compliance-heavy contracts, but it also raises wage pressure and tightens specialist labor supply. The United Kingdom integrated facility management market therefore remains anchored in the Southeast even as future capacity additions start to spread more widely.

The M62 corridor and Wales are emerging as the fastest-moving demand pockets in the United Kingdom integrated facility management (IFM) market because digital infrastructure investment is no longer centered only on London and the M4 route. The M62 corridor accounted for 44 projects and 3,361 MW in planning or construction, while London and the M4 corridor accounted for 40 projects and 2,283 MW, which shows how the development balance is shifting north. Wales also drew the CWL41 development in Bridgend, valued at GBP 5 billion (USD 6.35 billion), adding another specialist FM demand node outside the traditional core. Providers are adapting through broader national coverage, and Mitie’s GBP 297 million (USD 377.2 million) contract, with the Department for Transport across more than 800 sites shows how contract pools are becoming more geographically dispersed. These shifts support regional delivery models that balance technical coverage with better wage-to-cost economics than central London can offer.

Scotland and Northern Ireland remain smaller in size, but both are strategically important to the United Kingdom integrated facility management market. Scotland continues to offer stable public-sector demand, and NHS Forth Valley’s seven-year soft FM re-award to Serco in September 2024 showed the strength of long-duration healthcare contracts under the Scottish procurement framework. Northern Ireland is more exposed to labor availability issues because post-Brexit mobility constraints have reduced access to both low-skilled and specialist workers. CER research cited in 2026 estimated that the UK had 460,000 fewer EU workers than in 2019, with lower-skilled roles disproportionately affected. Separate analysis of job postings showed the UK still stood 20% below pre-pandemic levels in late 2025, which points to a slower hiring backdrop for frontline FM roles than in other major European economies. For the United Kingdom IFM market, this means regional opportunity is widening, but labor depth remains uneven.

Competitive Landscape

The United Kingdom integrated facility management market is moderately concentrated at the top and highly fragmented below that level. Companies such as Mitie, ISS, Sodexo, CBRE GWS, OCS, Serco, and ENGIE UK continued to compete for large public and private contracts. The decisive move in 2025 was capability-led consolidation, with OCS completing the EMCOR UK acquisition in December and creating a hard-services platform with more than 7,000 engineers and revenue above GBP 1 billion (USD 1.27 billion). Private equity remained highly active, accounting for 54% of UK FM transactions in 2024 and 90 deals in 2025, with more than 80% structured as bolt-on acquisitions. This shows that the United Kingdom integrated facility management (IFM) market is rewarding firms that can assemble broader technical, compliance, and ESG reporting capability rather than rely on price-led bids.

The most attractive white space still sits in specialist niches that are growing faster than traditional delivery models can fully support. Data center FM, life sciences estate management, and energy advisory embedded inside service contracts all offer stronger margins and clearer barriers to entry than generalist delivery. Apleona’s August 2025 acquisition of Corrigenda illustrated that logic, because the deal added technical energy management and M&E maintenance capability in public-sector and education estates rather than basic scale alone. Mitie’s earlier Marlowe deal followed the same pattern by strengthening fire, security, and environmental services within a wider compliance platform. In the United Kingdom integrated facility management market, acquisition strategy is therefore less about size for its own sake and more about filling technical gaps that clients now treat as essential.

Technology is also changing how competition works inside the United Kingdom IFM market. Pure-play software and managed-service providers are adding AI-led asset management, workflow automation, and CAFM optimization layers that can either support or strip value from traditional contracts. Sodexo’s October 2025 Home Office partnership, with a 24/7 helpdesk, CAFM support, and fire risk assessment scope, shows that service integration and systems capability now matter as much as headcount scale. ISO 41001 certification is becoming a stronger tender differentiator in government and defence work, because buyers want third-party assurance that service management processes are controlled and auditable. The result is a market where the largest providers still set the pace, but specialist and technology-led challengers can still win ground when they solve a defined capability gap.

United Kingdom Integrated Facility Management Industry Leaders

Mitie Group plc

CBRE Group, Inc.

ISS Facility Services Ltd.

Sodexo Limited

Compass Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Transport for London awarded Mitie a new five-year cleaning and associated services contract covering the entire Tube and bus network, deploying over 2,000 colleagues; Mitie committed GBP 400,000 (USD 535,012) annually in social enterprise initiatives and established a dedicated TfL Cleaning Centre of Excellence in London.

- December 2025: OCS completed the acquisition of EMCOR UK from EMCOR Group Inc., creating a combined hard-services platform with 7,000+ engineers and annual revenues exceeding GBP 1 billion (USD 1.34 billion), targeting defense, data centers, government, healthcare, and life sciences.

- October 2025: Sodexo was selected by the Home Office as a five-year performance partner to support its transition to an in-house FM function for 677 built assets across the UK, including data centers and ports, with services including 24/7 helpdesk, CAFM, and fire risk assessments; the contract commences in October 2026.

- August 2025: Apleona acquired Corrigenda, a Hampshire-based FM firm with approximately 200 employees specializing in technical energy management and M&E maintenance for public sector, education, and local authority clients in southern England, marking Apleona's third UK acquisition since 2022.

United Kingdom Integrated Facility Management Market Report Scope

The United Kingdom Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial [includes BFSI, IT and Telecom, Retail and Warehouses, etc.], Hospitality [includes Eateries, Restaurants and Large-Scale Hotels], Institutional and Public Infrastructure [includes Government Establishments, Education, Transportation such as Airports and Railways, etc.], Healthcare [includes Public and Private Healthcare Facilities], Industrial and Process Sector [includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.], and Other End-User Industries [includes Multi-House Residential, Entertainment, Sports and Leisure]). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Hard Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| Segmentation by Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Hard Facility Management Services | ||

| Segmentation by End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the 2026 to 2031 growth outlook for integrated facility management in the United Kingdom?

The United Kingdom integrated facility management market is projected to rise from USD 16.45 billion in 2026 to USD 20.78 billion by 2031 at a 4.78% CAGR.

Which service category is expanding fastest in the United Kingdom?

Hard FM is the fastest-growing service type, with a projected 5.38% CAGR through 2031, supported by data center demand, retrofit activity, and tighter compliance needs.

Which end-user group currently contributes the most revenue?

Industrial & Process led with 26.77% share in 2025 because data centers, manufacturing, energy, and other technically complex sites need continuous FM coverage.

Why are commercial occupiers still increasing FM spend after hybrid work?

Commercial demand is still rising because occupiers want better air quality visibility, faster maintenance response, and higher workplace standards to support office use and retention.

What is the main operating challenge for FM providers in the United Kingdom?

Labour remains the biggest pressure point, as skills shortages, rising wages, and higher employer costs are making it harder to staff contracts and protect margins.

How concentrated is the competitive environment?

The market remains moderately concentrated, with Mitie, ISS, Sodexo, CBRE GWS, OCS, Serco, and ENGIE UK competing actively for major public and private sector contracts.

Page last updated on: