Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

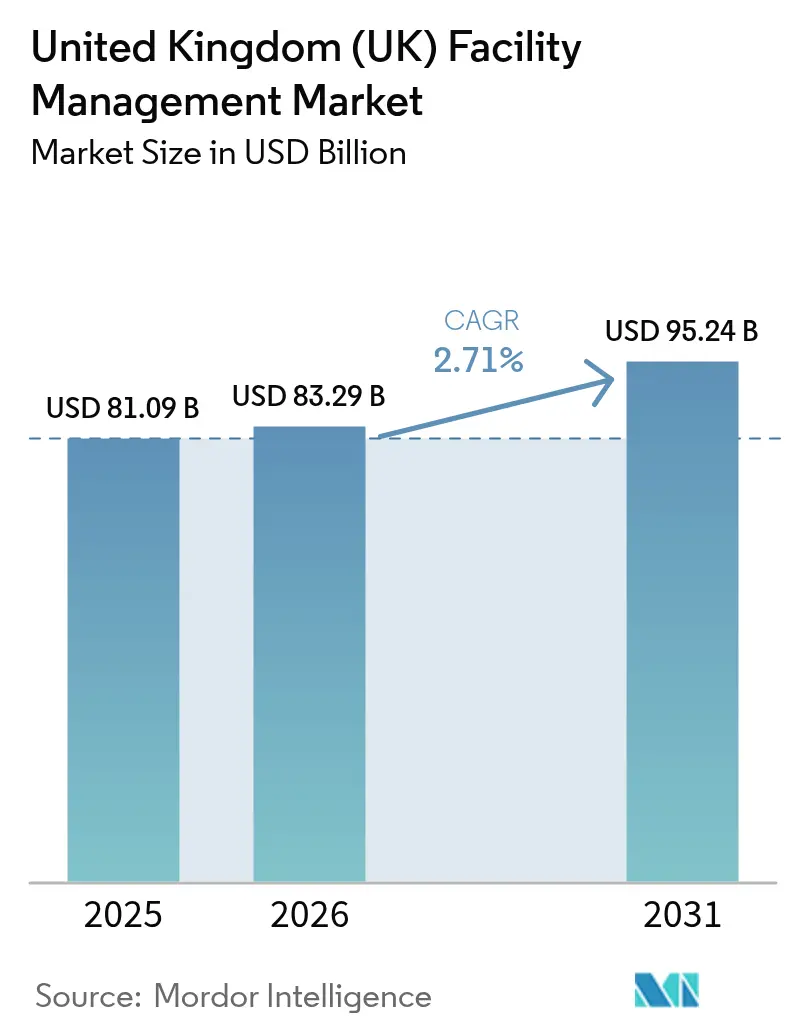

| Base Year Market Size (2025) | USD 81.09 Billion |

| Market Size (2026) | USD 83.29 Billion |

| Market Size (2031) | USD 95.24 Billion |

| Growth Rate (2026 - 2031) | 2.71% CAGR |

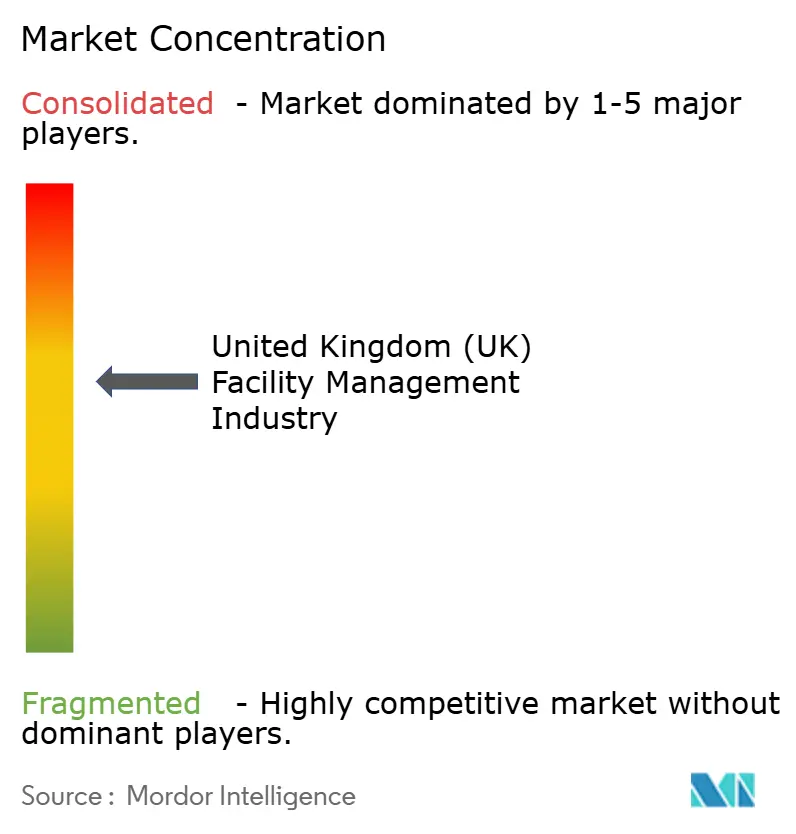

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom (UK) Facility Management Market Analysis by Mordor Intelligence

The United Kingdom facility management market size was valued at USD 81.09 billion in 2025 and estimated to grow from USD 83.29 billion in 2026 to reach USD 95.24 billion by 2031, at a CAGR of 2.71% during the forecast period (2026-2031). The measured trajectory signals a mature sector advancing under energy-efficiency mandates, digital transformation, and a sustained preference for outsourced service models. Hard services hold prime importance because ageing building stock demands strict mechanical, electrical, and plumbing upkeep to meet Minimum Energy Efficiency Standards, while soft services evolve quickly to address workplace well-being and stringent hygiene rules. Technology integration from IoT sensor grids to AI-powered analytics—cuts response times, trims energy consumption, and enables outcome-based contracts that grow revenue without proportionate head-count expansion. Outsourcing momentum continues as public and private clients seek specialist expertise that guarantees compliance and delivers cost certainty amid volatile input prices. Although Brexit-linked labour shortages and cost inflation compress margins, rising public-sector refurbishment funding and the spread of flexible workspaces offer expansion lanes for providers that innovate fast.

Key Report Takeaways

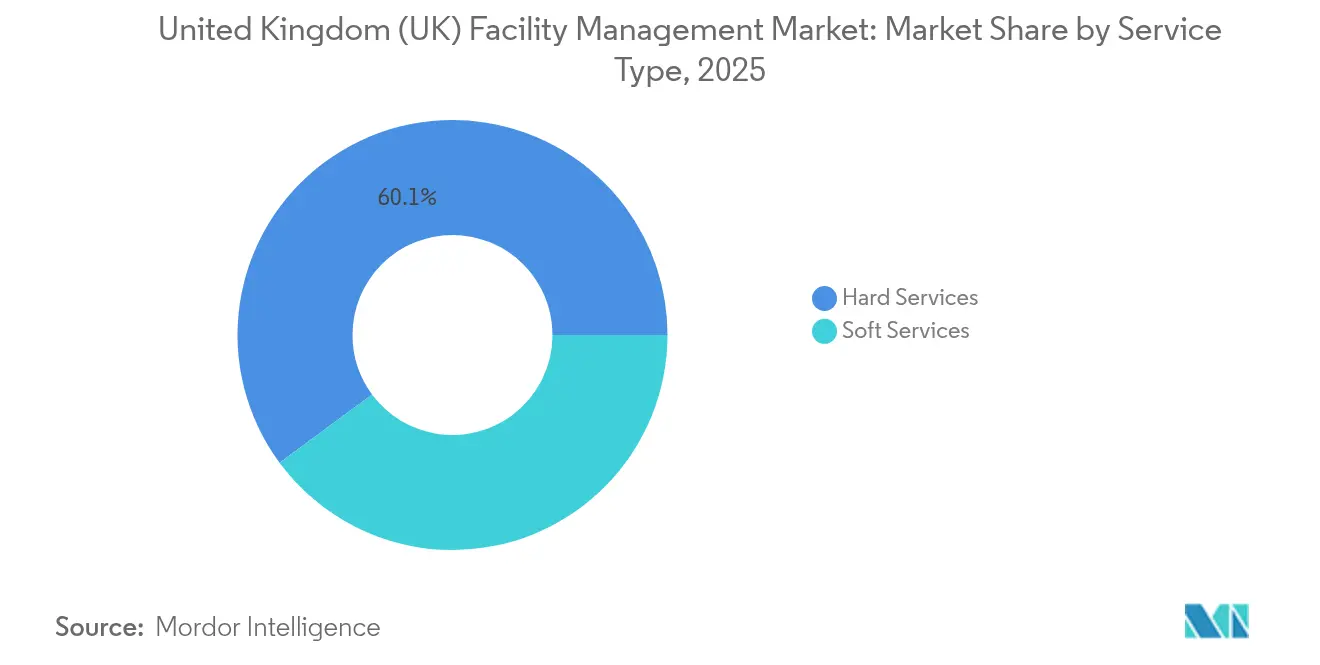

- By service type, hard services led with 60.12% of United Kingdom facility management market share in 2025, while soft services are projected to advance at a 2.78% CAGR through 2031

- By offering type, the outsourced model accounted for 63.85% share of the United Kingdom facility management market size in 2025 and is forecast to grow at a 2.77% CAGR to 2031

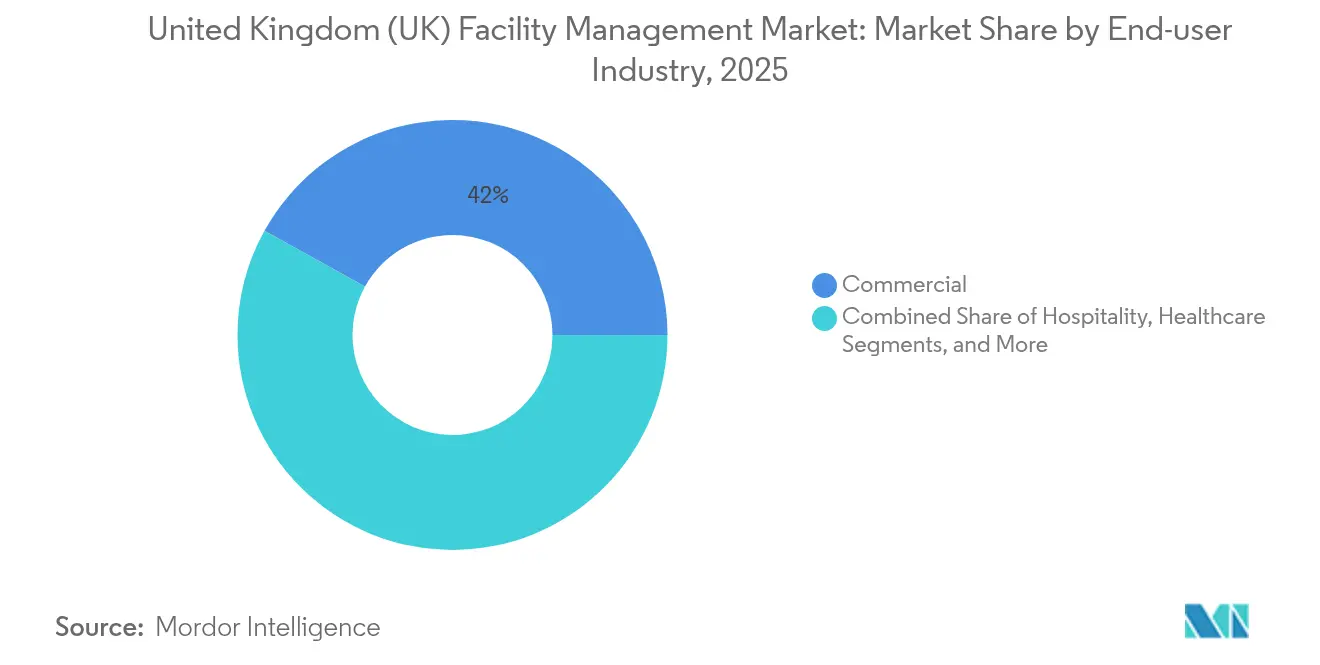

- By end-user industry, commercial facilities held 41.95% of the United Kingdom facility management market share in 2025; institutional and public-infrastructure segments are expanding at a 2.72% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom (UK) Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid commercial real estate expansion | +0.8% | London, Manchester, Birmingham | Medium term (2-4 years) |

| Technology integration (IoT, AI, automation) | +0.6% | National, concentrated in major cities | Long term (≥ 4 years) |

| Increasing outsourcing trend | +0.5% | National | Short term (≤ 2 years) |

| Rising focus on workplace experience and employee well-being | +0.4% | London, Edinburgh, Cardiff | Medium term (2-4 years) |

| Stringent energy-efficiency and net-zero regulations | +0.3% | National | Long term (≥ 4 years) |

| Rise of flexible workspaces requiring agile FM contracts | +0.2% | London, Manchester, Bristol | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technology Integration (IoT, AI, Automation)

AI-driven building-management platforms are redefining service delivery, with the Intellectual Property Office cutting maintenance response times from 14 days to seconds after launching a digital work-order portal. [1]Intellectual Property Office, “IPO Celebrates First Filing in New Digital Service,” GOV.UK Smart sensors relay live occupancy, temperature, and air-quality data, letting providers shift from reactive to predictive maintenance while lowering energy use and elevating employee comfort. CBRE’s entry into hyperscale data-center facilities management underscores the high-margin potential in segments that demand 24-hour analytical monitoring. Healthcare and education clients lead adoption because compliance regimes mandate continuous environmental monitoring. As digital dashboards merge soft and hard services, providers package cleaning, security, office support, and asset maintenance into data-rich contracts that command price premiums.

Rapid Commercial Real Estate Expansion

Royal Institution of Chartered Surveyors data show occupier demand turned positive in Q1 2025, and prime office rents in Central London are projected to rise nearly 5% in the year. [2]Royal Institution of Chartered Surveyors, “UK Commercial Property Shows Early Signs of Recovery,” RICS.ORG Industrial assets register the strongest investment appetite, with an +18% net balance in investor demand, propelled by e-commerce and near-shoring. New developments increase demand for commissioning, lifecycle asset management, and ongoing compliance auditing. Facility managers partnering early with developers secure multi-year revenue streams in smart-ready buildings that integrate ESG dashboards from day one. Logistics growth similarly drives tailored FM packages that combine inventory tracking technologies, dock management, and advanced fire-suppression maintenance for high-throughput warehouses.

Increasing Outsourcing Trend

The Crown Commercial Service’s RM6232 framework, valued up to GBP 35 billion (USD 9.63 billion), exemplifies public-sector reliance on external FM specialists. NHS Hard Facilities Management 2 framework contracts deliver about 10% savings versus in-house operations while upgrading COVID-19 resilience. Private companies also outsource to navigate hybrid work complexity and decarbonization mandates, gravitating toward outcome-based agreements that tie provider remuneration to uptime, energy-efficiency, or occupant-satisfaction metrics. Providers respond by broadening engineering, IoT, and analytics capabilities to own more of the built-environment value chain.

Rising Focus on Workplace Experience and Employee Well-being

Seventy-eight percent of facility managers cite sustainability as top priority in delivering healthier workplaces. Air-quality sensors and ergonomic design upgrades boost productivity and retention rates; Biological Preparations research correlates pathogen-controlled cleaning with measurable employee satisfaction gains. Flexible-workspace operators like Workspace Group hosted 81 on-site community events in 2024 to nurture tenant engagement while meeting low-carbon targets. FM providers thus bundle hospitality-style services, environmental analytics, and wellness programming into integrated offerings that command premium fees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and skill gaps | -0.4% | National, acute in London and Southeast | Short term (≤ 2 years) |

| Margin pressure from rising operational costs | -0.3% | National | Medium term (2-4 years) |

| Fragmented supplier ecosystem hindering service standardization | -0.2% | National | Long term (≥ 4 years) |

| Data-security concerns in smart-building systems | -0.1% | Major cities with high-tech buildings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Skill Gaps

Hospitality, cleaning, and catering units face 132,000 job vacancies post-Brexit, straining FM rosters. [3]The Guardian, “Brexit Staff Shortages Scupper Plans to Reopen Clarence House,” THEGUARDIAN.COMThe 2025 Immigration White Paper raises the Skilled Worker visa threshold to RQF Level 6, curtailing access to international staff for entry-level FM roles. Employer training investment has fallen 28% since 2005, creating a skills deficit just as buildings adopt sophisticated digital systems. Firms counteract with supervisor academies such as JPC by Samsic’s 12-module Next Gen programme focusing on leadership and technical upskilling. Nonetheless, high turnover and an aging workforce continue to limit sector capacity.

Margin Pressure from Rising Operational Costs

Construction inflation stood near 10% in 2024, raising the price of refurbishment inputs critical to hard-FM contracts. Post-Brexit customs checks add 25% to imported consumables, with some FM firms expecting GBP 1.5 million (USD 0.41 million) annual logistics cost increases. National Insurance hikes compound wage bills; Mitie has flagged the need for pricing resets to preserve margins. Advanced energy-management systems deliver partial relief but require up-front capital, tempering near-term profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Compliance

Hard services held 60.12% of United Kingdom facility management market share in 2025, anchored by the NHS’s GBP 11.6 billion (USD 3.19 billion) maintenance backlog and stringent EPC upgrade timelines. The United Kingdom facility management market size for hard-service contracts is poised to expand as 28% of commercial properties still rate D or lower on EPC scale, forcing accelerated mechanical, electrical, and plumbing overhauls. MEP and HVAC segments benefit from regulatory pathways to net-zero that mandate 47%-62% emissions cuts by 2035. Asset digitization further lifts demand for predictive-maintenance analytics, letting providers intervene before asset failure while meeting compliance reporting needs.

Soft services, while smaller today, are forecast to grow 2.78% CAGR through 2031, propelled by hospital-grade cleaning standards and workplace-experience innovations. Heightened infection-control rules elevate the premium for robotic disinfection systems and sensor-verified hygiene protocols. Co-working operators require smart access control, driving security-service modernization. Fire-safety upgrades tied to post-Grenfell legislation amplify demand for integrated alarm testing and evacuation-planning services. Together, these forces shift provider offerings toward comprehensive packages that merge soft-service excellence with data-backed compliance.

By Offering Type: Outsourcing Accelerates Through Specialization

Outsourced models commanded 63.85% of the United Kingdom facility management market size in 2025 and will lead growth at 2.77% CAGR to 2031. Integrated FM sits at the apex, with ISS extending its global Barclays mandate to cover cleaning, technical support, catering, and workplace solutions. Government procurement alone contributes USD 16.5 billion equivalent each year, reinforcing scale advantages for large integrators.

Single-service specialists retain footholds where compliance is narrow yet critical, exemplified by Compass Healthcare’s focus on hospital infection-control cleaning. Bundled FM gains traction among mid-market enterprises needing coordination without relinquishing in-house oversight. Hybrid models arise in security-sensitive facilities, integrating internal governance with external engineering know-how. Outcome-based contracts accelerate the outsourcing shift by proving tangible savings and improved KPIs, steering even conservative organizations toward third-party expertise within the broader United Kingdom facility management industry.

By End-user Industry: Institutional Growth Outpaces Commercial Demand

Commercial operators ranging from tech offices to retail parks drove 41.95% of United Kingdom facility management market demand in 2025. Retail supermarkets refresh back-of-house logistics and front-of-house ambience to satisfy omnichannel shoppers. Warehousing benefits from automated materials-handling equipment, pushing FM providers to add telemetry-enabled conveyor maintenance and 24-hour asset monitoring. Hyperscale data centers grow at 20% from 2021 to 2026, necessitating specialist cooling and power-system upkeep.

Institutional and public-infrastructure clients will grow the fastest at 2.72% CAGR through 2031 thanks to modernization drives in hospitals, schools, and administrative offices. The Department for Work and Pensions’ GBP 945 million (USD 260.04 million) annual integrated-service award to ISS illustrates contract scale. Universities and schools invest in smart-campus energy dashboards and security upgrades, while hospitals demand negative-pressure cleaning regimes and critical-asset redundancy. Transport networks, such as Great Western Railway’s 1,997-kilometre route, require multi-disciplinary station upkeep and rolling-stock depot services.

Geography Analysis

London and the Southeast represent the largest regional slice of the United Kingdom facility management market, anchored by dense commercial real estate and strict EPC enforcement. Prime Central London offices are projected to post nearly 5% rental growth in 2025, fuelling premium FM demand that integrates ESG-compliance analytics, dynamic cleaning schedules, and energy-performance guarantees. Flexible workspace booms in the capital, requiring agile contracts that adjust services in line with daily occupancy variances. Labour shortages hit hardest here, compelling providers to deploy automation and targeted training to uphold service levels.

Northern England and Scotland show robust expansion in industrial FM as policy incentives drive logistics and manufacturing reshoring. Sodexo’s HMRC contract across Belfast, East Kilbride, and Glasgow illustrates growing decentralization of public-sector estates. Midlands manufacturing clusters invest in predictive maintenance and environmental monitoring, creating demand for multi-skill engineering teams. Scottish renewable-energy projects introduce opportunities for specialists in turbine-maintenance facilities and low-carbon asset stewardship.

Wales and Northern Ireland benefit from infrastructure upgrades and transportation-hub refurbishments that demand FM expertise in safety compliance, passenger-service environments, and cost-efficient asset renewal. Regional variance in workforce availability and enforcement intensity prompts providers to tailor staffing models, regulatory support, and technology investments by locale while leveraging national buying power to keep costs competitive. Across the United Kingdom facility management market, a regionalized yet standardized service approach proves critical to winning and retaining geographically diverse portfolios.

Regulatory Landscape

United Kingdom facility management (FM) operations sit under a tightening compliance stack spanning building safety, energy performance, and security-sensitive works in occupied assets. The Building Safety Act 2022 and the Building Safety Regulator (BSR) are central for higher-risk buildings, shaping documentation, competence, and building-control interactions that directly affect hard FM delivery (fire systems, MEP and HVAC, and refurbishment works). In January 2026, government actions signaled further consolidation and direction-setting for the built-environment regime, reinforcing the need for auditable maintenance, inspection, and resident- or occupier-facing safety processes.

Energy and digital infrastructure policy increasingly steers FM scope. In June 2026, the governments interim response on non-domestic MEES confirmed a proposal for private rented buildings over 1,000 square metres to meet EPC B by 2031, keeping EPC uplift programs and energy-management services prominent in contract requirements. On the planning side, the Infrastructure Planning (Business or Commercial Projects) (Amendment) Regulations 2026 added data centres to the prescribed list of nationally significant infrastructure projects under the Planning Act 2008. In July 2026, Circular 02/2026 issued directions under the Building Act 1984 to dispense with specific procedural building control requirements for telecommunications-related work in higher-risk buildings from 1 September 2026, which increases the pace of in-building connectivity upgrades that FM teams must manage safely.

Value Chain Analysis

The UK FM value chain begins with asset owners and occupiers (commercial estates, healthcare, education, and central government) defining service outcomes, compliance obligations, and reporting needs, then procuring delivery through single-service specialists or bundled and integrated FM providers. Upstream inputs include labour (engineers, cleaners, security staff), regulated materials and components for MEP and fire safety works, and software layers such as CAFM, building management systems, and IoT and analytics tools that turn work orders and sensor data into planned maintenance and compliance evidence. Midstream, prime contractors and integrators (including large listed providers) coordinate subcontractors across hard and soft services, while increasingly embedding helpdesk automation, compliance tracking, and supplier-performance monitoring into standardized operating models.

Downstream delivery is executed on-site through planned maintenance, reactive response, and lifecycle projects, with outputs captured as KPI dashboards, statutory logs, and ESG reporting to support audits and renewals. Labour availability and cost inflation constrain the chain, which increases reliance on training, automation, and tighter supplier governance; industry commentary in 2026 highlighted ongoing financial pressure across the profession, encouraging providers to rationalize supply bases and enforce common data requirements. As contracts demand energy dashboards, waste audits, and supplier carbon reporting (observed in 2026 market discussions), technology vendors and data standards become more influential nodes in the chain, alongside traditional MEP, fire, cleaning, catering, and security sub-trades.

Competitive Landscape

The market remains moderately fragmented. Global players Mitie, ISS, Serco leverage scale and integrated digital platforms to win multi-site contracts, evidenced by Mitie’s record GBP 3.7 billion (USD 1.02 billion) pipeline of new awards. Consolidation quickened in 2024 when OCS acquired FES FM and Compass Group purchased CH&CO, adding 10,000 staff and broadening hard-service depth. Hard-service segments erect technical barriers that favour established firms, while soft-service arenas remain more price-sensitive and open to niche entrants.

Technology emerges as the central differentiator. Providers invest in AI analytics, patent smart-maintenance algorithms, and deploy IoT sensors at scale to guarantee uptime and energy-performance gains. ESG compliance, healthcare specialization, and outcome-based pricing are attractive white-space areas where domain expertise trumps commoditised labour. Start-ups often target single-service niches, yet competing for integrated national contracts demands financial capacity and proven delivery frameworks. As procurement frameworks favour fewer, larger suppliers able to shoulder compliance risk, the competitive field slowly concentrates, even as local specialists thrive in sub-regional hard-service engineering and boutique workplace-experience roles.

United Kingdom (UK) Facility Management Industry Leaders

ISS UK

Mitie Group PLC

Serco Group PLC

Kier Group PLC

G4S Facilities Management UK Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Public-sector estate digitalization and common data standards create a route for FM providers that can operationalize asset data into measurable maintenance and energy outcomes. In February 2026, the Department for Education launched Manage Your Education Estate, a digital service that consolidates estates guidance, funding, and data for schools and colleges, aligning with demand for condition surveys, backlog reduction planning, and digitally enabled service delivery across large, distributed portfolios. In April 2026, the Government Property Function began publishing common data and digital structures, standards, and guides for responsible bodies to collect and commission estate data to a common minimum standard, opening whitespace for providers and CAFM and BMS partners that can implement data capture, interoperability, and governance at scale.

Technology-led integrated FM is also a practical opportunity area because buyer intent and capability gaps coexist. Corporate and professional-body research cited in 2026 points to widespread plans to increase FM technology investment, while a substantial share of practitioners report unfamiliarity with newer AI approaches (including agentic AI), indicating demand for managed services that package tooling with training, change management, and compliance-ready workflows. Energy-performance compliance pressure keeps EPC improvement programs and ongoing energy-management services central to hard FM, and the Future Buildings Standard and related commissioning rigor increase the value of providers that can link MEP performance, occupant experience, and ESG reporting within outcome-based contracts.

Recent Industry Developments

- June 2026: Mitie secured a water network management contract with AWE Nuclear Security Technologies to manage critical water infrastructure across three Berkshire sites, using capabilities associated with its Marlowe acquisition. The award broadens Mitie's addressable scope in high-assurance technical estates where compliance, resilience, and specialist engineering are decisive buying factors. It also supports deeper penetration of critical-infrastructure FM work that carries higher technical requirements than commoditized soft services.

- May 2026: Mitie won a GBP 27 million, three-year facilities management contract with Kingston and Richmond NHS Foundation Trust. The deal reinforces NHS demand for integrated providers that can support operational continuity while aligning service delivery with healthcare estates priorities. It also strengthens Mitie's positioning in healthcare, where hard-FM compliance and infection-control adjacent requirements raise barriers to entry.

- December 2024: OCS completed its acquisition of FES FM and FES Support Services, adding engineering capacity to its UK footprint. The transaction increased OCS depth in hard services, supporting delivery of compliance-heavy MEP and lifecycle programs across multi-site estates. It also contributed to ongoing consolidation dynamics in a market where procurement frameworks and technical requirements favor scaled suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the United Kingdom facility management market is defined as the revenue generated from hard and soft services delivered to operate, maintain, and support buildings and sites, across in-house teams and outsourced contracts.

Scope exclusions: We exclude pure construction and one-off capital projects, standalone real estate brokerage or leasing fees, and unrelated business process outsourcing that is not tied to running a facility.

Segmentation Overview

- By Service Type

- Hard Services

- Asset Management

- MEP and HVAC Services

- Fire Systems and Safety

- Other Hard FM Services

- Soft Services

- Office Support and Security

- Cleaning Services

- Catering Services

- Other Soft FM Services

- Hard Services

- By Offering Type

- In-house

- Outsourced

- Single FM

- Bundled FM

- Integrated FM

- By End-user Industry

- Commercial (IT and Telecom, Retail and Warehouses, etc.)

- Hospitality (Hotels, Eateries, Large-scale Restaurants)

- Institutional and Public Infrastructure (Govt, Education, Transportation)

- Healthcare (Public and Private Facilities)

- Industrial and Process (Manufacturing, Energy, Mining)

- Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set up the model structure and anchor assumptions that need to match the UK context. We reviewed public sources such as Office for National Statistics releases, UK government procurement and public-spend publications, Health and Safety Executive guidance and incident series, and energy performance regulations and updates that influence building operations. We also referred to trade and member association materials from facilities and building services bodies, and to peer-reviewed papers that discuss maintenance practices, energy services, and outsourcing trends.

To keep the numbers realistic, we cross-checked supplier disclosures such as annual reports, investor presentations, and statutory filings where service revenue could be linked to the UK footprint. In a few places, paid subscriptions already available to our team were used for company financial intelligence, news tracking, and import and export shipment-level checks for select inputs tied to hard-services activity. This desk source list is illustrative and not exhaustive, and other public references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions, especially where outsourcing mix, contract pricing, and service scope vary by client type and region. We spoke with service providers, subcontractors, and large buyers of FM services across the UK, and then revisited a few topics when early responses showed wide ranges. Coverage was kept balanced across hard and soft services so the final totals reflect what clients typically contract and renew year to year.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 31% | |

| Smaller Players: 15% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs UK demand by linking the serviceable building base and FM outsourcing adoption to typical annual spend patterns for hard and soft services. Those totals are then corroborated with selective bottom-up checks, such as rolling up a sample of provider revenues attributable to UK FM, channel discussions on contract ticket sizes, and spot checks of average pricing against service frequency.

Key model inputs include the split between in-house and outsourced delivery, contract types (single, bundled, and integrated), labor cost movement tied to wages and staffing intensity, energy-services activity that can shift hard FM spend, and end-user exposure across commercial, public and infrastructure, institutional, and industrial sites. Where bottom-up visibility is incomplete, gaps are handled through conservative coverage factors tied back to the number of sites served and typical contract scope, and then reviewed again with interview feedback.

Forecasts are built using scenario analysis, since inflation, wage pressure, and outsourcing decisions can move differently across client sectors. Assumptions for renewal cycles, pricing escalation clauses, and service mix shifts are adjusted only when they are supported by repeated primary feedback and by observable signals from public data series.

Data Validation & Update Cycle

Validation is done through repeated cross-checks so the final series stays consistent with real operating signals. Model outputs are compared against independent indicators like outsourcing penetration direction, public sector procurement tone, and the implied spend per site for major end-user groups. If a number looks out of line, the underlying driver is revisited, and targeted follow-ups are done with respondents to confirm whether the variance is real or caused by an assumption mismatch.

Before sign-off, the model and write-up go through multi-step analyst reviews that focus on math integrity, year-to-year logic, and alignment between scope and totals. Reports are refreshed annually, and interim updates are made when material events change pricing, regulation, or outsourcing behavior. Right before delivery, we run a final pass to capture the latest public releases and incorporate any late-breaking market moves.

Mordor Intelligence's United Kingdom Facility Management Market Size Compared Against Other Published Estimates

Published market sizes for UK facility management do not always match, even when the topic label looks the same. Differences usually come from what each publisher counts as FM revenue, the year selected for the headline number, and how pricing and outsourcing shifts are treated in the forecast.

Some estimates appear to use a narrower service basket or a different handling of in-house activity and bundled contracts. Some figures lean more heavily on outsourced-only spending. For Mordor Intelligence, totals include both in-house and outsourced delivery across hard and soft FM, and bundled and integrated contracts are standardized so packaged services do not get counted twice.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 81.09 B (2025) | |

| Regional Consultancy A | USD 70.35 B (2024) | Uses an earlier base year and provides limited clarity on whether in-house FM and bundled multi-service contracts are fully captured, which can reduce the implied total versus a full-market definition. |

| Industry Research House B | USD 46.75 B (2024) | Shows a much smaller 2024 value with a very high growth rate, suggesting a tighter service scope or different treatment of offerings and models, which can materially change the market total. |

Taken together, the spread is mainly explained by scope choices and the way contract packaging and delivery mode are counted. By keeping service inclusions consistent across years, and by checking pricing escalation and outsourcing mix against interview feedback and visible demand signals, the final estimate stays transparent and repeatable.

Key Questions Answered in the Report

What is the current size of the United Kingdom facility management market?

The market is valued at USD 83.29 billion in 2026.

How fast is the United Kingdom facility management market expected to grow?

It is forecast to expand at a 2.71% CAGR, reaching USD 95.24 billion by 2031.

Which service type dominates the market?

Hard services lead with 60.12% share due to critical infrastructure and compliance needs.

Why is outsourcing prominent in the sector?

Outsourced models deliver specialized expertise and compliance assurance, capturing 63.85% share in 2025.

What are the main challenges facing providers?

Labour shortages, cost inflation, and data-security concerns in smart buildings compress margins and raise operational risk.

Which end-user segment is growing the fastest?

Institutional and public-infrastructure clients show the highest CAGR at 2.72% through 2031, driven by government modernization projects.

Page last updated on: