IoT MVNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

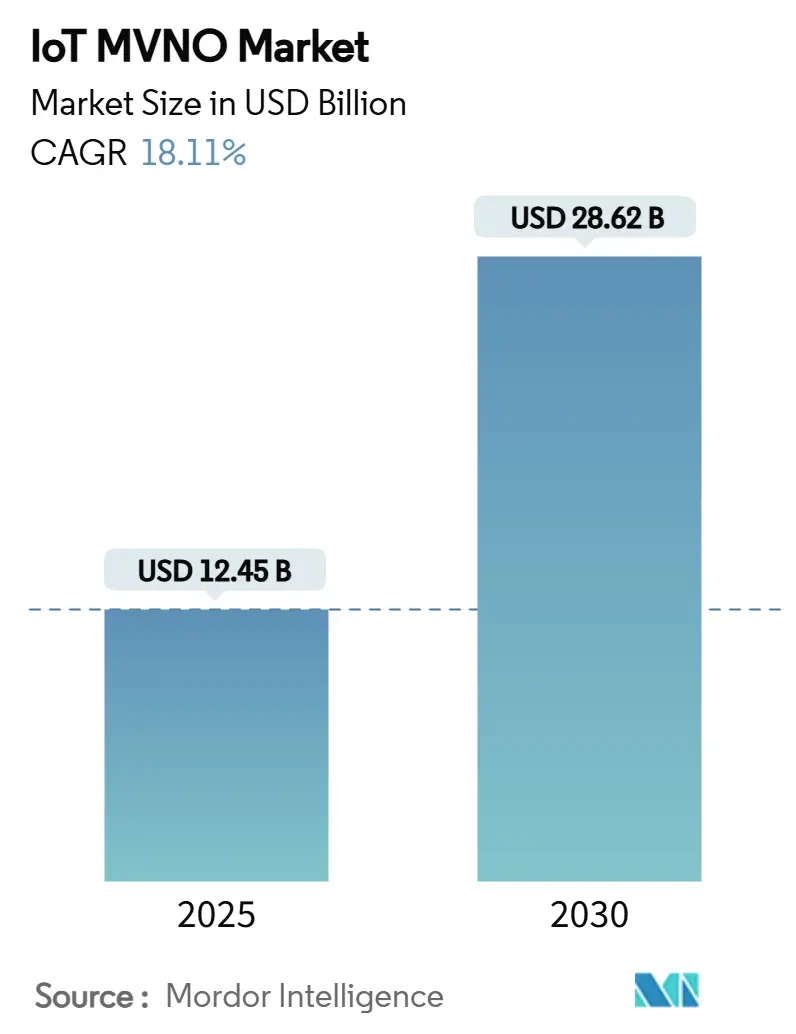

| Market Size (2025) | USD 12.45 Billion |

| Market Size (2030) | USD 28.62 Billion |

| Growth Rate (2025 - 2030) | 18.11% CAGR |

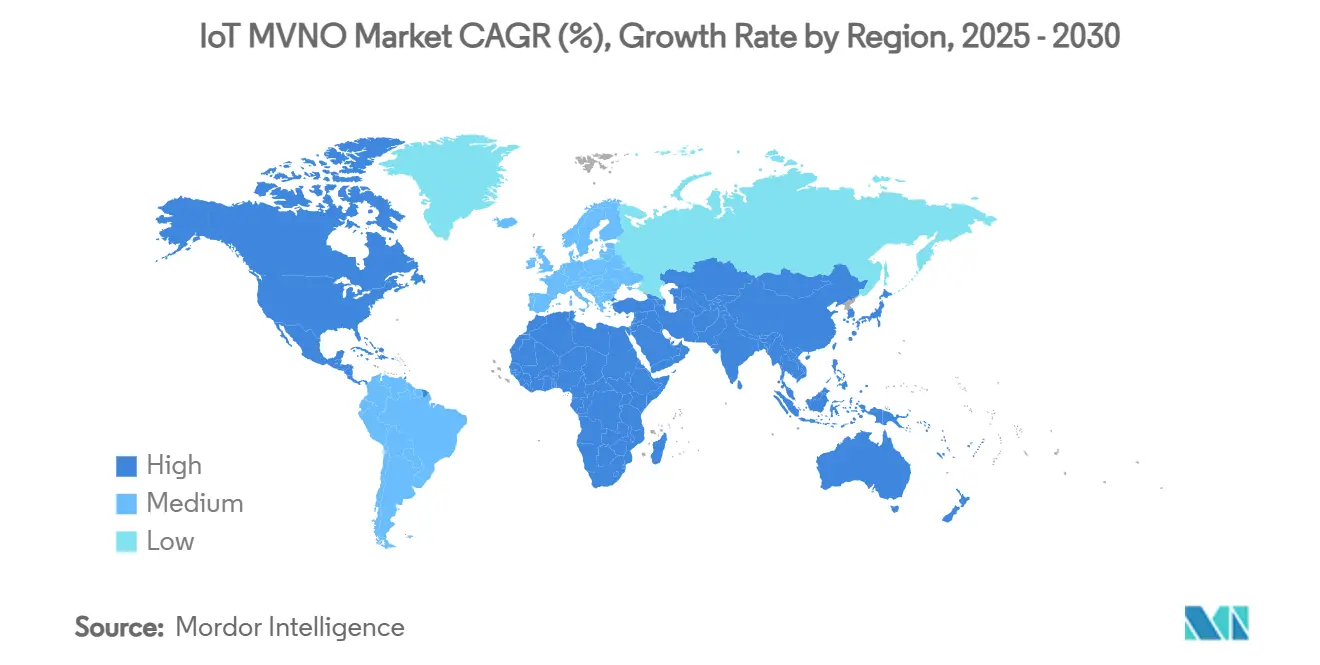

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT MVNO Market Analysis by Mordor Intelligence

The IoT MVNO market size reached USD 12.45 billion in 2025 and is projected to climb to USD 28.62 billion by 2030, translating into an 18.11% CAGR. This expansion reflects the growing preference for specialized connectivity services that address device-specific power, cost, and coverage needs across industrial verticals. Low-Power Wide-Area (LPWA) rollouts, expanding eSIM/iSIM deployments, and regulatory support for 5G network slicing underpin demand, while automotive OEMs, smart-grid operators, and manufacturers increasingly outsource connectivity management to full-service MVNO partners. Competitive strategies now revolve around multi-operator wholesale agreements, AI-driven network-optimization platforms, and value-added security features that combat connectivity commoditization. Geographic growth opportunities concentrate in Asia–Pacific, where smart-city investments and manufacturing digitization outpace global averages, even as North America maintains leadership through advanced IoT ecosystems and favorable wholesale-access rules.

Key Report Takeaways

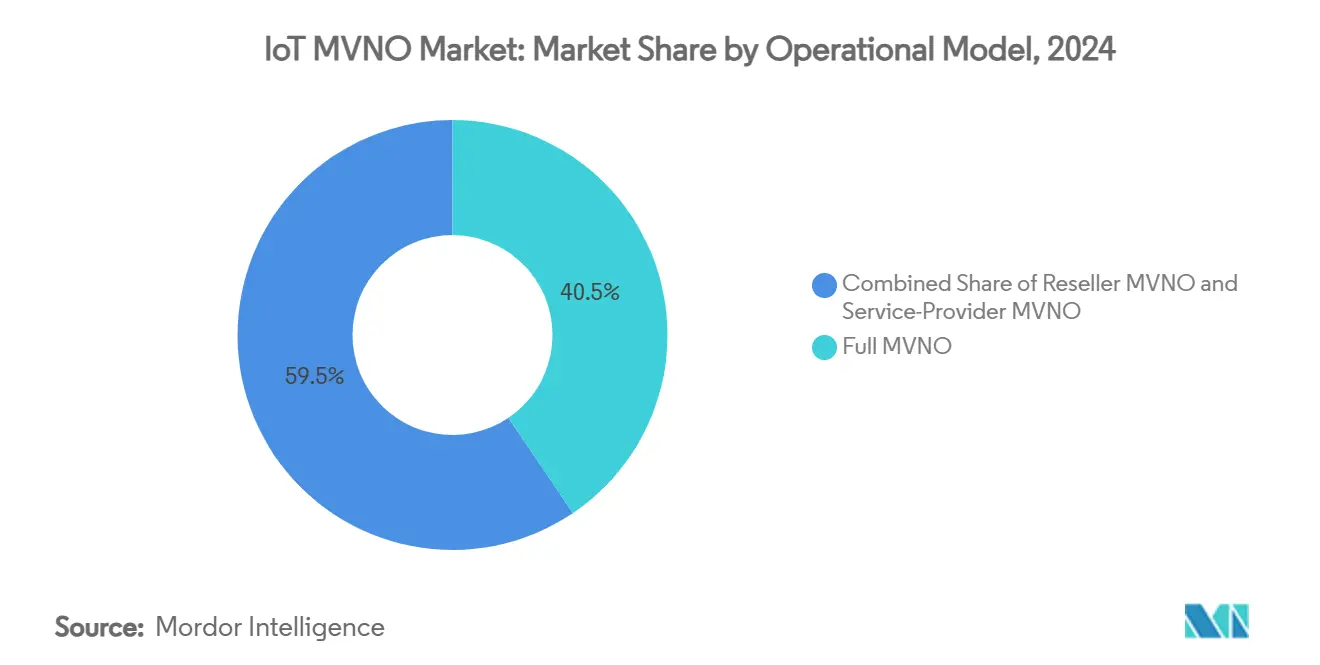

- By operational model, full MVNO operations captured 40.54% IoT MVNO market share in 2024 while reseller MVNOs are advancing at a 20.15% CAGR through 2030.

- By application vertical, automotive and transport led with a 28.54% revenue share in 2024, whereas energy and utilities connectivity is forecast to expand at a 22.32% CAGR to 2030.

- By connectivity technology, 4G/LTE retained 46.25% share of the IoT MVNO market size in 2024 and 5G services are progressing at a 21.87% CAGR through 2030.

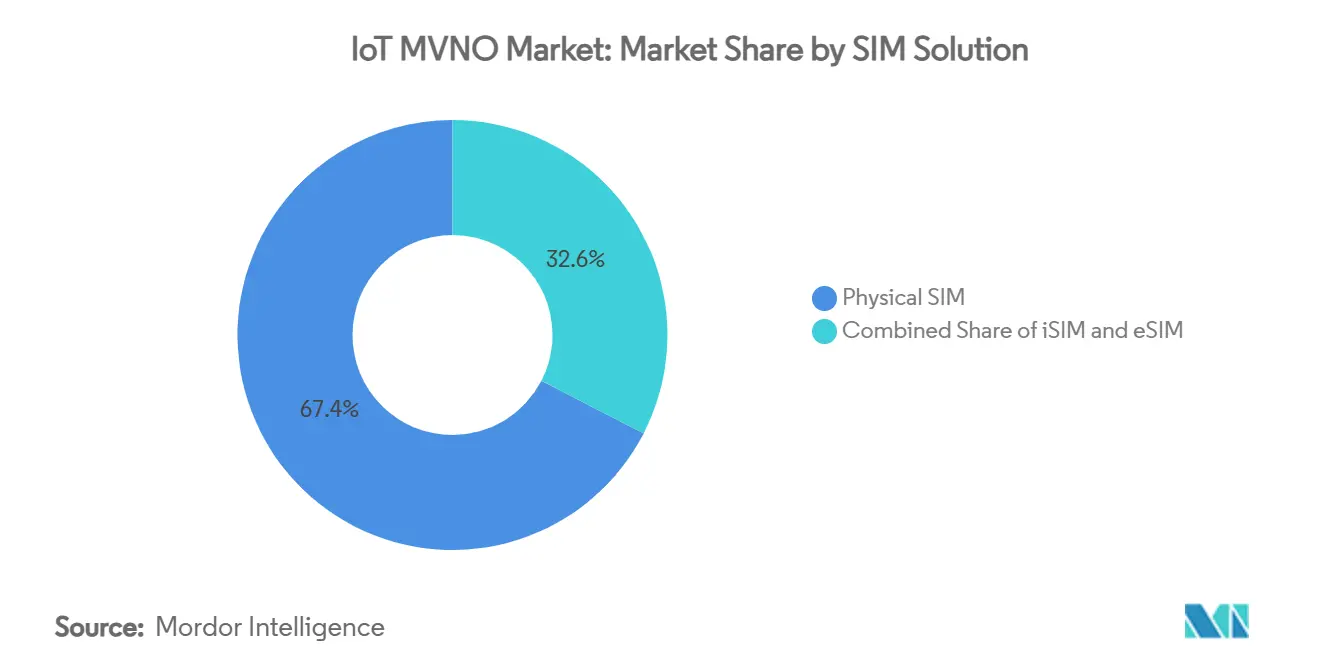

- By SIM solution, physical SIMs held 67.43% of the IoT MVNO market size in 2024, while iSIM shipments are projected to rise at a 20.56% CAGR between 2025-2030.

- By geography, North America accounted for 38.54% IoT MVNO market share in 2024, but Asia–Pacific is expected to post the fastest regional CAGR at 19.7% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IoT MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of LPWA (NB-IoT & LTE-M) | +3.2% | Global, strong in Europe & Asia–Pacific | Medium term (2-4 years) |

| Expansion of eSIM/iSIM deployments | +2.8% | North America & EU leading, APAC following | Long term (≥ 4 years) |

| AI-driven network-optimization platforms | +2.1% | Global, concentrated in developed markets | Medium term (2-4 years) |

| OEM carbon-reporting compliance needs | +1.9% | EU & North America, expanding to APAC | Long term (≥ 4 years) |

| 5G network-slicing mandates for MVNOs | +2.4% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Connected-vehicle programme expansion | +3.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of LPWA (NB-IoT and LTE-M)

LPWA technologies enable battery-powered devices to operate for up to 10 years while remaining connected, and commercial NB-IoT/LTE-M networks now span over 100 countries. [1]GSMA, “SGP.32 v1.2 Technical Specification,” gsma.com MVNOs aggregate this capacity across multiple operators, cutting device-level connectivity costs by up to 70% compared with traditional cellular alternatives. Cost efficiency accelerates adoption in environmental monitoring and asset-tracking, but lower entry barriers intensify rivalry, shifting competition toward service-quality metrics and global coverage breadth.

Expansion of eSIM/iSIM Deployments

The GSMA SGP.32 specification standardizes remote-SIM provisioning for IoT devices, eliminating physical-SIM handling and enabling multi-operator profile downloads. Industry forecasts show eSIM connections capturing 37% of cellular IoT endpoints by 2030, followed closely by iSIM at 34%. MVNOs gain the flexibility to switch networks on demand, optimize cost-performance trade-offs, and support truly global deployments without manual intervention, thereby commanding premium pricing for software-defined connectivity bundles.

AI-Driven Network-Optimization Platforms

AI analytics detect anomalies, predict congestion, and automate resource allocation to maintain agreed service-levels at scale. These capabilities become critical as IoT device density climbs and latency requirements tighten for healthcare, manufacturing, and transportation applications. MVNOs integrating AI can cut unplanned downtime, shrink operational expenditure, and introduce usage-based pricing models that align connectivity charges with network conditions, delivering measurable total-cost-of-ownership benefits that counter ARPU erosion pressures.

OEM Carbon-Reporting Compliance Needs

EU Corporate Sustainability Reporting Directive obligations require enterprises to monitor Scope 3 emissions, creating demand for connected sensors that track location, temperature, and energy usage in real time. [2]MDPI, “Blockchain-Driven Carbon Accountability in Supply Chains,” mdpi.com Ambient IoT tags such as Wiliot’s battery-free IoT Pixels provide low-cost data streams that feed automated carbon dashboards. MVNOs offering secure, low-power connectivity for carbon-footprint monitoring secure long-term contracts and premium margins because compliance-critical data transfer remains non-negotiable in corporate budgets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connectivity ARPU erosion | -2.7% | Global, most pronounced in mature markets | Short term (≤ 2 years) |

| Permanent-roaming regulatory barriers | -1.8% | EU, Middle East, select APAC markets | Medium term (2-4 years) |

| Limited MVNO access to private-5G spectrum | -1.4% | North America, Europe, developed APAC | Long term (≥ 4 years) |

| Escalating IoT-SAFE security-certification costs | -1.2% | Global, significantly affecting smaller MVNOs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Connectivity ARPU Erosion

Average revenue per IoT connection is slipping toward USD 1 per month, as illustrated by KORE Wireless’ 19 million-connection portfolio. [3]KORE Wireless, “Q3 2024 Results,” korewireless.comCommoditization pressures intensify where LPWA standards equalize technical capabilities and large enterprises negotiate steep volume discounts. MVNOs hedge margin risk by bundling device management, security, and analytics into tiered offerings that shift price competition toward value recognition rather than megabyte rates.

Permanent-Roaming Regulatory Barriers

EU rules restricting permanent roaming oblige MVNOs to establish local wholesale deals or operate country-specific IMSIs, raising operational costs and complicating global rollouts. Divergent approaches across the Middle East and parts of APAC similarly inhibit seamless cross-border deployments, reducing economies of scale and elongating time-to-market for multinational IoT projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operational Model: Full MVNOs Lead Infrastructure Control

Full MVNOs captured 40.54% IoT MVNO market share in 2024, reflecting customer demand for granular traffic control, private APNs, and bespoke billing. Operators adopting this model negotiate direct wholesale rates across multiple networks, improving margin leverage and enabling differentiated service-level agreements. The IoT MVNO market size attributable to full MVNOs is projected to expand at 16.2% CAGR through 2030 as mission-critical deployments favor infrastructure ownership for long-term stability and regulatory compliance.

Reseller MVNOs record the fastest 20.15% CAGR by emphasizing quick service activation and zero infrastructure overhead. Enterprises adopting a cloud-first procurement mindset select reseller offers to avoid capital commitments, even though feature depth remains thinner. Competitive positioning therefore hinges on whether customers prioritize time-to-market and simplicity or bespoke functionality and margin control.

By Application Vertical: Automotive Dominance Meets Utilities Growth

Automotive and transport maintained a 28.54% revenue lead in 2024, driven by mandatory eCall, usage-based-insurance telemetry, and over-the-air software delivery. Connected-car lifecycles exceed consumer device refresh rates, guaranteeing multi-year subscription revenues that anchor MVNO cash flows. Utilities, however, post a 22.32% CAGR as smart-meter rollouts, grid-edge sensor adoption, and renewable-energy balancing requirements multiply device counts, signaling new scale opportunities for the IoT MVNO market.

As industrial automation, healthcare remote monitoring, and smart-city projects mature, diversified vertical exposure becomes critical for revenue resilience. MVNOs with vertical-specific application programming interfaces, compliance credentials, and ecosystem partnerships deepen customer stickiness, protecting premium-pricing capacity even in commoditized bandwidth scenarios.

By Connectivity Technology: 4G Stability Enables 5G Transition

4G/LTE maintained 46.25% share of active IoT lines in 2024, underpinning applications where coverage ubiquity and module affordability outweigh 5G performance gains. Nevertheless, 5G subscriptions are growing at 21.87% CAGR, powered by network slicing and ultra-reliable low-latency communications for factory automation and autonomous-mobility pilots. The IoT MVNO market size attributable to 5G connections is forecast to reach USD 6.3 billion by 2030, emphasizing the importance of future-proof orchestration platforms that span both generations.

NB-IoT and LTE-M fill low-throughput niches such as environmental sensing, offering decade-long battery life and deep-indoor penetration. Satellite NB-IoT and non-terrestrial 5G complements cellular footprints, assuring global reach for maritime, aviation, and remote-asset segments. MVNOs integrating terrestrial and LEO satellite profiles in a single SIM enhance service continuity and unlock differentiated revenue streams.

By SIM Solution: Physical Dominance Faces Digital Disruption

Physical SIMs still accounted for 67.43% of deployed IoT units in 2024 as enterprises favored proven logistics workflows and device-vendor compatibility. Yet iSIM shipments are rising at 20.56% CAGR as chip-level integration reduces bill-of-materials cost and shrinks form factors. eSIM penetration exceeds 30% in automotive and industrial gateways, where remote profile swaps cut truck-roll expenses and regulatory compliance mandates local-network fall-back options.

The IoT MVNO market now clusters around orchestration capabilities that support hybrid SIM estates, enabling customers to migrate from physical to embedded form factors without service disruption. Providers that invest early in interoperable remote-SIM-provisioning hubs secure switching-cost advantages and gain visibility into twin revenue streams: connectivity and lifecycle management.

By Enterprise Size: Large Enterprises Drive Revenue, SMEs Show Growth

Large enterprises contributed 59.43% of 2024 revenue as global supply chains, multinational fleet operators, and tier-1 manufacturers demanded high-touch support, redundant carrier coverage, and stringent security controls. High average device counts and multi-year contracts bolster cash flow stability for service providers. In parallel, SME adoption is accelerating at a 19.86% CAGR, signaling the broadening appeal of IoT use cases such as predictive maintenance, cold-chain monitoring, and smart building automation.

IoT MVNO market offerings packaged with low-code dashboards, pay-as-you-grow price models, and rapid onboarding lower friction for resource-constrained SMEs. Providers that blend automated provisioning with dedicated channel-partner ecosystems tap a long-tail growth engine that offsets slowing ARPU trajectories in saturated enterprise accounts.

Geography Analysis

North America remained the largest regional contributor in 2024, claiming 38.54% IoT MVNO market share on the back of advanced 4G/5G rollouts, mandated wholesale access, and early adoption of connected-vehicle and healthcare-monitoring services. Private-5G pilots in manufacturing hubs and federal guidance on IoT cyber-labeling sustain demand for secure, slice-enabled connectivity.

Asia–Pacific is the fastest-growing region, set to contribute 270 million licensed cellular IoT connections by 2030, fuelled by government-backed smart-city projects, digital-manufacturing incentives, and accelerating 5G coverage. Regulatory diversity across India, China, and Southeast Asian nations necessitates localized compliance and multi-operator roaming strategies, but scale economics and urbanization trends outweigh complexity costs.

Europe sustains a sizeable installed base through stringent cybersecurity legislation and proactive network-slicing guidelines that reward MVNOs able to deliver vertically tuned service tiers. New EU cybersecurity obligations applicable from December 2024 elevate demand for secure-element-enabled modules and managed-connectivity bundles. Elsewhere, the Middle East and Africa gain momentum via smart-city and energy-digitization projects, while South America increasingly embraces precision-agriculture use cases requiring dual satellite-cellular coverage to overcome rural connectivity gaps.

Competitive Landscape

The IoT MVNO market features moderate fragmentation, with top players such as KORE Wireless, Aeris Communications, and 1NCE leveraging multi-operator wholesale agreements, eSIM orchestration, and vertical-specific value-adds to differentiate. KORE continues to rationalize operations while expanding AI-based security offerings to defend margins amid ARPU compression. Aeris launched a fully integrated IoT security stack in 2025 that embeds threat detection into the connectivity layer, signaling convergence between managed connectivity and cybersecurity services.

M&A activity intensifies as scale and technology capabilities become competitive necessities. SoftBank’s acquisition of Cubic Telecom and Wireless Logic’s reseller pact with Starlink illustrate moves toward integrated terrestrial-satellite propositions and expanded geographic reach. Competitors are also investing in AI-enabled network optimization and 5G slice management to deliver SLA-based products. While hyperscale cloud providers and legacy carriers threaten to commoditize transport, specialist MVNOs preserve their advantage by bundling application programming interfaces, device-onboarding automation, and domain-specific compliance toolkits.

Emergent white-space opportunities include carbon-footprint monitoring, precision agriculture, and low-cost asset-tracking, segments where providers cultivate domain expertise and leverage LPWA or satellite overlays to de-risk coverage gaps. Strategic differentiation thus pivots on the breadth of global access agreements, orchestration depth, and the ability to integrate connectivity within broader digital-transformation workflows.

IoT MVNO Industry Leaders

KORE Wireless Group Holdings Inc.

Aeris Communications Inc.

1NCE GmbH & Co. KG

Wireless Logic Ltd.

Cubic Telecom Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 1NCE raised USD 60 million to expand across the United States, Asia–Pacific, and Latin America, bringing total funding to USD 160 million while supporting 30 million active devices.

- March 2025: Thales selected Wireless Logic as its IoT partner to extend global solution reach and enrich security capabilities.

- February 2025: Aeris launched IoT Watchtower, a fully integrated cellular security service aimed at mitigating device-level threats.

- January 2025: Truphone’s acquisition by TP Global Operations finalized, focusing on eSIM enablement for financial-services clients across nine jurisdictions.

Global IoT MVNO Market Report Scope

| Full MVNO |

| Service-Provider MVNO |

| Reseller MVNO |

| Automotive and Transport |

| Energy and Utilities |

| Industrial and Manufacturing |

| Healthcare |

| Smart Cities and Public Sector |

| Agriculture |

| 2G / 3G |

| 4G / LTE |

| 5G |

| NB-IoT |

| LTE-M |

| Satellite IoT |

| Physical SIM |

| eSIM |

| iSIM |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC Countries |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Operational Model | Full MVNO | ||

| Service-Provider MVNO | |||

| Reseller MVNO | |||

| By Application Vertical | Automotive and Transport | ||

| Energy and Utilities | |||

| Industrial and Manufacturing | |||

| Healthcare | |||

| Smart Cities and Public Sector | |||

| Agriculture | |||

| By Connectivity Technology | 2G / 3G | ||

| 4G / LTE | |||

| 5G | |||

| NB-IoT | |||

| LTE-M | |||

| Satellite IoT | |||

| By SIM Solution | Physical SIM | ||

| eSIM | |||

| iSIM | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC Countries | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the IoT MVNO market?

The IoT MVNO market size reached USD 12.45 billion in 2025 and is forecast to grow to USD 28.62 billion by 2030 at an 18.11% CAGR.

Which application vertical generates the most IoT MVNO revenue?

Automotive and transport holds the largest revenue share at 28.54% due to connected-vehicle mandates and telematics subscriptions.

Why is Asia–Pacific the fastest growing region?

Manufacturing digitization programmes, large-scale smart-city initiatives, and rapid 5G rollouts are driving a regional CAGR exceeding 19%.

How are eSIM and iSIM technologies influencing the market?

Embedded SIM solutions remove physical-SIM logistics, support remote provisioning, and are expected to represent more than 70% of cellular IoT connections by 2030.

What strategies are leading MVNOs using to protect margins amid ARPU decline?

Top providers bundle AI-driven network optimization, security services, and vertical-specific platforms to shift competition from price to value.

Page last updated on: