Japan Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

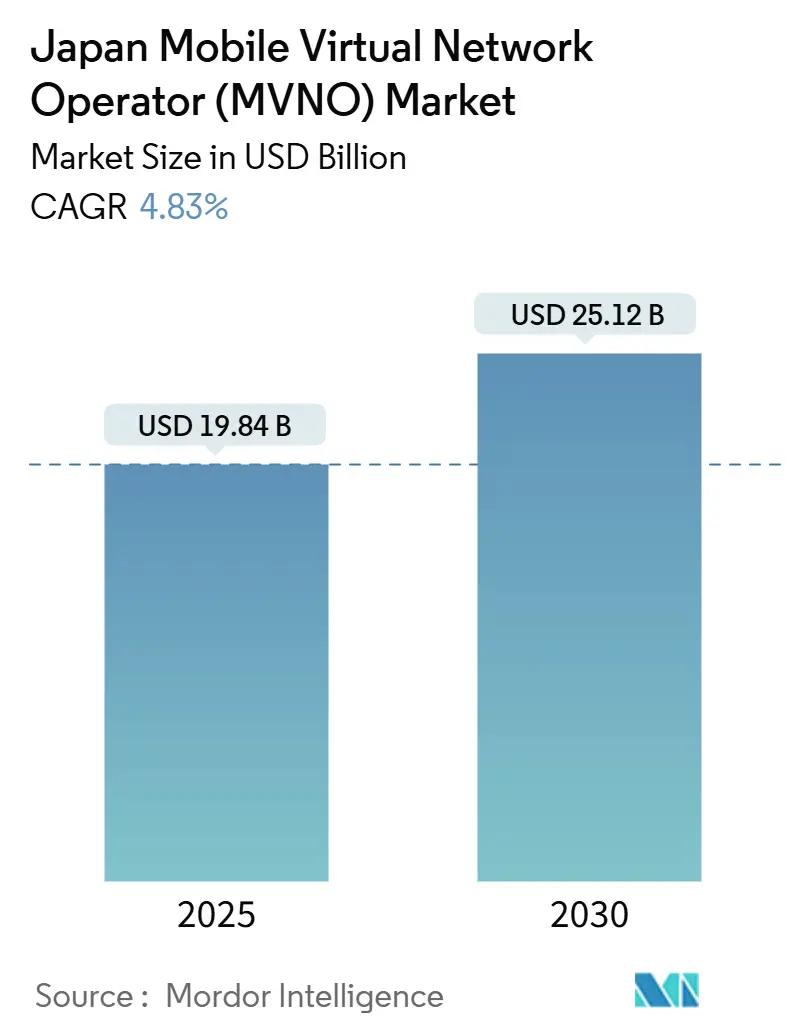

| Market Size (2025) | USD 19.84 Billion |

| Market Size (2030) | USD 25.12 Billion |

| Growth Rate (2025 - 2030) | 4.83% CAGR |

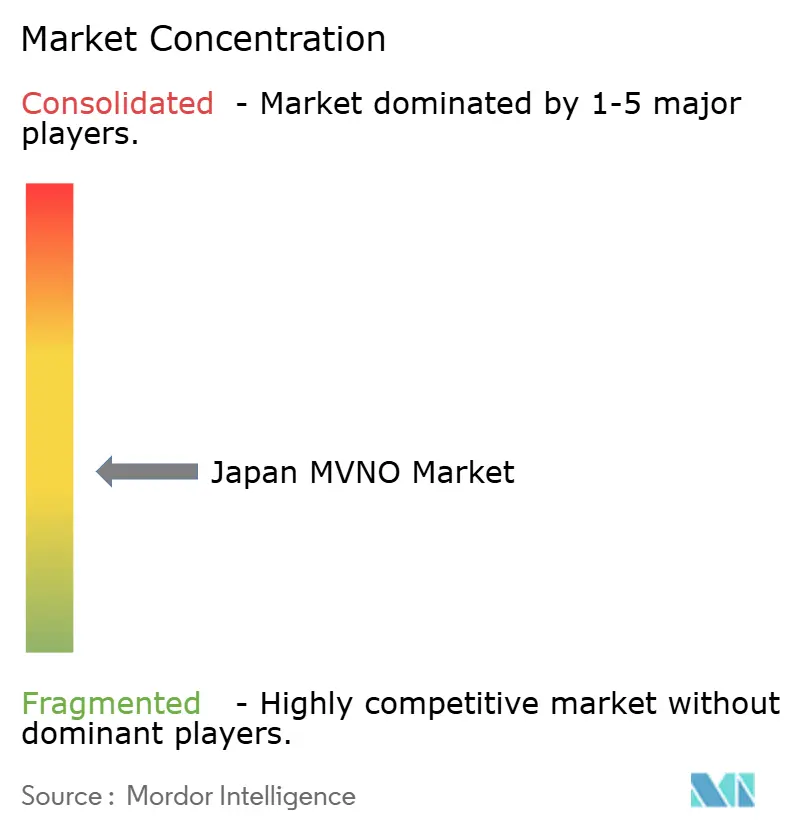

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Japan MVNO Market size is estimated at USD 19.84 billion in 2025, and is expected to reach USD 25.12 billion by 2030, at a CAGR of 4.83% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 35.39 million Subscribers in 2025 to 43.10 million Subscribers by 2030, at a CAGR of 4.02% during the forecast period (2025-2030). The growth path shows a shift from tariff-led competition to service differentiation as operators integrate satellite links, enterprise IoT bundles, and embedded fintech features. Cloud-native platforms dominate the studied market because software-defined cores let virtual operators launch services quickly and scale nationwide without heavy capex. Full MVNOs are accelerating the growth as tighter control over the core network enables bespoke plans, network slicing pilots, and bundled digital services. Enterprise IoT demand and rural coverage mandates are nudging MVNOs toward high-value industrial use cases, while regulatory wholesale-rate cuts continue to squeeze consumer ARPU. Satellite and Non-Terrestrial Network (NTN) trials, though still small in absolute revenue, are building a new layer of national resilience and unlocking future coverage in underserved regions.

Key Report Takeaways

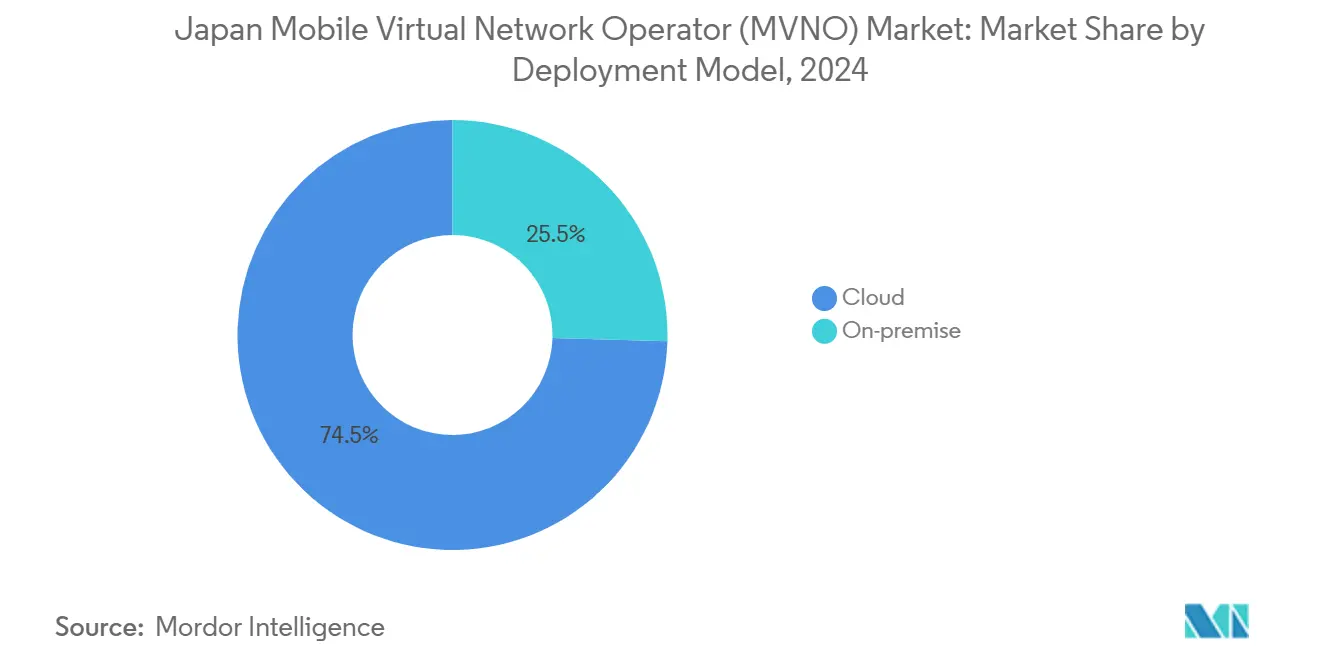

- By deployment model, cloud platforms held 74.54% of Japan's MVNO market share in 2024 and are expanding at an 8.17% CAGR through 2030.

- By operational mode, reseller and light MVNOs accounted for 59.05% of the Japan MVNO market size in 2024, while Full MVNO operations recorded the fastest growth at 23.31% CAGR through 2030.

- By subscriber type, consumer lines commanded 81.10% share of the Japan MVNO market size in 2024; enterprise lines are advancing at 11.38% CAGR.

- By application, the cellular M2M segment captured 17.55% CAGR, the highest within the application mix, while the Others category retained 43.36% revenue share in 2024.

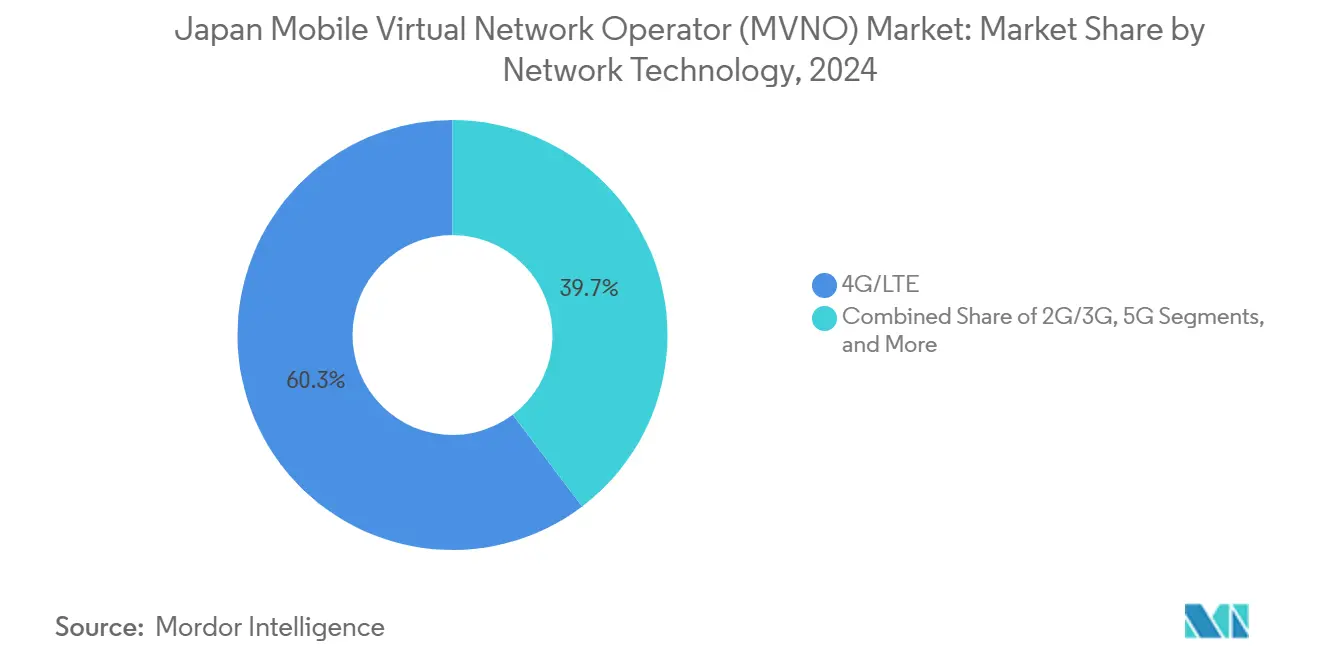

- By network technology, 4G/LTE services maintained a 60.30% revenue share in 2024, whereas satellite and NTN connections are rising at a 99.55% CAGR from a small base.

- By distribution channel, online/digital-only held 53.69% of Japan's MVNO market share in 2024 and are expanding at an 9.55% CAGR through 2030.

Japan Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying consumer price-sensitivity amid wage stagnation | +0.7% | Urban prefectures nationwide | Short term (≤ 2 years) |

| MIC-mandated wholesale-rate reductions and SIM unlocking | +0.6% | National regulatory framework | Medium term (2–4 years) |

| Rapid eSIM uptake lowering switching friction | +0.4% | Metropolitan areas | Short term (≤ 2 years) |

| Enterprise IoT boom requiring tailored connectivity bundles | +0.9% | Aichi, Kanagawa, and other industrial hubs | Long term (≥ 4 years) |

| Satellite / NTN trials to extend rural coverage | +0.3% | Remote prefectures nationwide | Long term (≥ 4 years) |

| Fintech “super-app” bundling to lift ARPU | +0.5% | Tokyo, Osaka, and growth suburban corridors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Intensifying Consumer Price-Sensitivity Amid Wage Stagnation

Stagnant wages keep household telecom budgets flat, so subscribers gravitate toward lower-cost data plans while demanding stable network quality. Rakuten Mobile reported average monthly usage of 18.4 GB per consumer in 2024, validating data-heavy consumption even within tight budgets [1]Rakuten Group, “Rakuten Group Q1 FY2025 Financial Results Highlights,” global.rakuten.com. MVNOs respond by launching unlimited-style or high-cap data tiers that preserve margins through wholesale efficiencies. Discount positioning widens the virtual operator funnel, helping the consumer segment retain 81.10% share of the Japan MVNO market. The same dynamic pushes operators to cross-sell content and lifestyle perks so that perceived value, not just price, drives retention. As price-sensitive users migrate from incumbent MNOs, MVNO subscriber additions continue even amid ARPU pressure.

MIC-Mandated Wholesale-Rate Reductions and SIM Unlocking

Regulatory wholesale-access discounts implemented by the Ministry of Internal Affairs and Communications lower network input costs, permitting aggressive retail pricing without eroding margins. Simpler SIM unlocking rules, effective 2023, remove device lock-in barriers and slash porting friction, accelerating net subscriber gains for digital-first MVNOs [2]KDDI Digital Life, “ConnectIN povo Device-Embedded Service,” prtimes.jp. Full MVNOs benefit most because their own core networks capture a higher proportion of the cost savings, funding investment in value-added services such as real-time data dashboards for SMEs. Over the medium term, consistent wholesale fee visibility encourages new entrants and strengthens the competitive fabric, reinforcing a structural tailwind for the Japan MVNO market.

Enterprise IoT Boom Requiring Tailored Connectivity Bundles

Industrial firms seek low-power, high-reliability SIMs for factory robotics, smart logistics, and asset telemetry. Soracom’s agreement with Suzuki to test micro e-mobility data links shows how IoT-focused MVNOs win by delivering programmable SIMs, cloud APIs, and analytics hooks[3]Soracom, “Suzuki Micro e-Mobility IoT Proof-of-Concept,” iotbusinessnews.com. MEEQ’s triple-carrier MVNE solution for automotive sensors underscores rising demand for multi-profile, multi-host SIM management. These tailored bundles carry higher ARPU, buffering operators against consumer-segment margin compression.

Rapid eSIM Uptake Lowering Switching Friction

eSIM provisioning embedded at the OEM stage allows subscribers to activate or swap carriers instantly via QR code or app, removing the physical SIM from the signup funnel. KDDI’s ConnectIN povo service, pre-installed in HP laptops with a 300 GB, five-year plan, demonstrates device-integrated connectivity that bypasses retail stores. Online-only MVNOs, already holding 53.69% of the distribution channel, gain disproportionate benefit because digital self-activation aligns with their low-touch acquisition model. As handset OEMs standardize eSIM, barriers to churn drop, forcing every carrier to deepen value-added layers in order to curb defection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyper-competition driving ARPU compression | −1.2% | Urban markets nationwide | Short term (≤ 2 years) |

| Limited access to premium 5G SA slices | −0.7% | All prefectures | Medium term (2–4 years) |

| Multi-host network integration complexity | −0.4% | National technical deployments | Medium term (2–4 years) |

| Cannibalization by MNO sub-brands | −0.6% | National consumer segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyper-Competition Driving ARPU Compression

Dozens of discount MVNOs plus sub-brands such as Y! mobile and LINEMO crowd the same price band, forcing operators to undercut or add non-core perks to differentiate. Rakuten’s Q1 2025 consumer ARPU sat at JPY 2,827 (USD 19.10), well below legacy MNO averages, yet still required scale boosts to offset slim unit margins. Sustained price warfare compels efficient back-office automation, lean distribution, and wholesale cost leverage. Operators unable to bundle extra services or reach economies of scale risk exit, fueling market consolidation pressures despite overall subscriber growth.

Limited Access to Premium 5G SA Slices from Host MNOs

Host carriers guard low-latency 5G standalone features and full network slicing, limiting MVNOs' ability to serve high-value enterprise workloads that need deterministic bandwidth or ultra-reliable links. Without exposure to premium slicing APIs, Full MVNOs cannot deliver end-to-end SLAs demanded by advanced robotics or telemedicine projects. The cap keeps MVNOs concentrated in consumer broadband and basic IoT, muting revenue-per-bit potential until wholesale terms improve. Some virtual players turn to satellite or private-LTE overlays to fill the feature gap, but those workarounds raise opex and dilute focus.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Digital Transformation

Cloud platforms controlled 74.54% of the Japan MVNO market in 2024, reflecting operator preference for scalable virtual cores that sit atop multiple host networks. This dominance equates to reduced capex and faster time-to-launch, translating into an 8.17% CAGR through 2030 for the segment. The Japan MVNO market size, attributed to cloud footprints, gains further momentum from eSIM onboarding, where server-side profile downloads eliminate logistics costs. Operators harness cloud analytics to segment churn risk and push targeted upsell campaigns within minutes, an agility unavailable to on-premise systems.

On-premise deployments persist in regulated verticals such as healthcare and defense, where data sovereignty mandates local packet cores. Even so, hybrid architectures arise: MVNOs host subscriber databases in private racks while offloading non-sensitive functions, like billing mediation, to public clouds. This blended approach keeps compliance bodies satisfied yet retains the cost curve benefits of cloud. As 5G SA adoption widens, network-function virtualization spurs real-time traffic steering between terrestrial and satellite beams, reinforcing the cloud’s systemic advantage.

By Operational Mode: Full MVNO Growth Signals Market Evolution

Reseller and light MVNOs captured a 59.05% share in 2024 thanks to low entry hurdles, but their growth plateaus as price competition intensifies. In contrast, Full MVNOs expand at 23.31% CAGR because ownership of the mobile core lets them issue SIMs, manage authentication, and brand value-added services without MNO approval. The Japan MVNO market size for Full operators swells as they package APIs for developers, monetize location data, and trial private 5G slices for factories.

Service Operator models sit between the two extremes, leasing radio access yet owning billing stacks, thereby unlocking mid-level customization for enterprise accounts. Regulatory inspection favors operators with transparent call data records and robust consumer protection measures, a compliance field in which established Full MVNOs like IIJmio excel. Their 21.6% slice of the consumer sub-segment illustrates how network control becomes a durable moat when combined with aggressive digital acquisition strategies.

By Subscriber Type: Enterprise Acceleration Reshapes Revenue Mix

Consumers command 81.10% of current lines, but enterprise SIMs grow at 11.38% CAGR as factories retrofit equipment for Industry 4.0. The Japan MVNO market size linked to enterprise lines is climbing because industrial customers prize flexible data caps, static IP options, and layered security. Premium connectivity for logistics tracking, connected retail kiosks, and predictive maintenance use cases fetch higher ARPU than vanilla consumer data.

IoT-specific MVNOs position themselves as horizontal enablers, bundling SIM management portals, over-the-air firmware updates, and pay-as-you-go tariffs. Mitsui Fudosan’s LTE-enabled HVAC monitoring deployment with partner MVNOs highlights the appetite for managed connectivity that wraps analytics and alerting around raw data feeds. This shift strengthens the long-term stability of operator revenue, diluting exposure to consumer discount cycles.

By Application: M2M Cellular Drives Next-Generation Connectivity

The Others bucket holds 43.36% revenue because lifestyle and content bundles remain popular among urban youths and gig-economy workers. Nonetheless, cellular M2M subscriptions exhibit the fastest growth at 17.55% CAGR as smart-industry projects migrate sensors from short-range protocols to LTE-M and 5G LPWA. The Japan MVNO market size for M2M lines scales with each new microcontroller that needs nationwide reach for diagnostics or asset tracking.

Semtech’s HL7900 module gained Japanese regulatory clearance in March 2025, enabling battery-efficient 5G LPWA devices that slot seamlessly into MVNO SIM portfolios. MVNOs that expose developer-friendly APIs and per-kilobyte billing capture the wave of embedded modules rolling off assembly lines. Even within consumer-oriented MVNOs, add-on IoT lines for pet trackers and wearables deepen stickiness and raise blended ARPU.

By Network Technology: Satellite Integration Transforms Coverage Paradigms

4G/LTE retains 60.30% share because most Japanese handsets and IoT modules still rely on mature LTE radios. 5G subscriptions rise gradually as device refresh cycles unfold and MVNO wholesale terms widen. The Japan MVNO market size tied to 5G services expands in tandem with gaming, AR shopping, and real-time drone control applications, yet coverage gaps linger in mountainous and island regions.

Satellite and NTN links race ahead at 99.55% CAGR from a tiny base. KDDI’s au Starlink Direct service, launched in April 2025, allows direct smartphone-to-satellite messaging for disaster resilience and remote work crews. Virtual operators piggybacking on these NTN channels can promise “anywhere connectivity” SLAs, an attractive contract clause for logistics firms and rural municipalities. Integration of satellite backhaul into cloud-native cores also reduces failover latency, improving network reliability metrics that enterprises monitor closely.

By Distribution Channel: Digital Platforms Reshape Customer Acquisition

Online and digital-only channels command 53.69% market share in 2024 and are projected to grow at 9.55% CAGR through 2030, reflecting consumer preference for self-service activation and competitive plan comparison capabilities. While traditional retail stores continue to play a pivotal role for customers seeking hands-on support and device consultations, carrier sub-brand stores are emerging as hybrid entities, blending physical presence with efficient digital processes. Meanwhile, third-party and wholesale channels are proving instrumental for MVNOs, allowing them to tap into specialized customer segments via partner networks and B2B distribution arrangements.

The evolution of distribution channels is gaining momentum, driven by strategic retail partnerships and innovative embedded connectivity models that sidestep conventional acquisition methods. A case in point is KDDI's collaboration with Mitsubishi Corporation and Lawson, which has birthed integrated retail-telecom touchpoints in roughly 14,600 convenience stores. This move highlights how MVNOs can harness physical retail networks for customer acquisition, all while upholding a digital service delivery model.

Geography Analysis

Tokyo, Kanagawa, and Osaka prefectures collectively generate the largest slice of the Japan MVNO market because of dense populations, high smartphone penetration, and a large corporate headquarters cluster there. Consumer acquisition costs are lower in such urban corridors due to digital marketing reach and gigabit fiber backhaul that supports cloud core hosting close to the user plane. The Japan MVNO market size derived from these metropolitan areas continues to expand as population inflows, especially among young professionals, drive data demand for streaming, ride-hailing, and contactless payments.

Second-tier industrial regions such as Aichi, Shizuoka, and Hiroshima exhibit accelerated enterprise IoT uptake, stimulating demand for multi-host SIMs capable of seamless roaming among carrier footprints. Manufacturing plants retrofit legacy equipment with cellular gateways to capture operational data, while logistics firms deploy real-time tracking across supply chains that span ports and expressways. MVNOs specializing in telematics, predictive maintenance, and factory automation tap these corridors for higher-margin contracts.

Rural prefectures across Hokkaido, Tohoku, and Kyushu present untapped potential that satellite augmentation aims to unlock. Conventional macro tower economics struggle in sparsely populated zones, but NTN links enable intermittent or mission-critical coverage without the burden of ground infrastructure. Convenience-store chains such as Lawson, fortified by a 14,600-store KDDI partnership, provide physical service points and distribution for SIM activation even in small towns. As disaster-preparedness grants and smart-agriculture pilots expand, MVNOs with satellite fallback stand positioned to win public-sector and farming cooperative contracts, supporting inclusive connectivity objectives.

Competitive Landscape

The competitive field hosts more than 30 active brands, yet concentration remains moderate because MIC policies keep wholesale access affordable and device unlocking simple. IIJmio, with 21.6% of consumer lines, leverages its ISP pedigree to cross-bundle broadband and cloud services. Rakuten Mobile, though an MNO, influences virtual competition through its aggressive pricing that sets consumer expectations across the channel. KDDI’s povo 2.0 and SoftBank’s LINEMO exemplify incumbent sub-brands that shield host networks from MVNO erosion while squeezing pure-play newcomers on price positioning.

Strategic moves show three clusters: cost-leaders such as mineo and nuro aiming for lean digital ops; technology-forward players trialing direct-to-cell satellite meshes; and ecosystem bundlers knitting fintech, media, or health services around the SIM. Xmobile’s acquisition of consumer-goods firm Sanritsu illustrates horizontal diversification designed to lift average revenue per account through cross-selling. Dstyle Mobile’s July 2025 launch with wellness bundles targets lifestyle communities underserved by generic plans.

Entry of IoT-first MVNOs such as Soracom expands the competitive canvas beyond human subscribers. Their developer-centric billing and API toolkits attract equipment makers that value frictionless provisioning over headline data quotas. Meanwhile, satellite partnerships promise fresh differentiation; operators aligning early with SpaceX, AST SpaceMobile, or domestic LEO projects can promise 100% population coverage, a claim that pure terrestrial rivals cannot match. Competition, therefore, tilts increasingly toward service breadth, vertical know-how, and ecosystem lock-ins rather than lowest unit price alone.

Japan Mobile Virtual Network Operator (MVNO) Industry Leaders

IIJmio (Internet Initiative Japan Inc.)

OCN Mobile ONE (NTT Communications Corporation)

mineo (K-Opticom Corporation)

Y!mobile (SoftBank Corp.)

BIC SIM (Bic Camera Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: KDDI released the ConnectIN povo embedded eSIM service with Japan HP, bundling a 300 GB, five-year allocation directly into laptops.

- June 2025: Dstyle Holdings introduced Dstyle Mobile in partnership with Xmobile, mixing beauty, health, and mobile plans from JPY 1,078 per month.

- May 2025: Xmobile acquired a 51% stake in Sanritsu Corporation to deepen product bundling between telecom and consumer goods.

- April 2025: KDDI commercially debuted au Starlink Direct, enabling basic satellite-to-smartphone messaging for emergencies, with data services scheduled for summer 2025.

- March 2025: Soracom partnered with Suzuki to test IoT connectivity for a micro e-mobility platform targeting urban delivery fleets.

Japan Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

What is the current value of the Japan MVNO market?

The market is valued at USD 19.84 billion in 2025 and is projected to grow steadily through 2030.

Which operational mode is expanding fastest among Japanese MVNOs?

Full MVNO models lead with a 23.31% CAGR because owning the core network enables richer service differentiation.

How significant is satellite connectivity for Japanese virtual operators?

Satellite and NTN lines, while small today, are rising at a 99.55% CAGR as operators pursue rural coverage and disaster-resilient networks.

Why are enterprise lines important to MVNO growth strategies?

Enterprise SIMs grow at 11.38% CAGR and carry higher ARPU due to tailored IoT solutions and managed services.

How do eSIM trends affect competition in Japan?

ESIM uptake lowers switching friction, helping digital-only MVNOs enlarge their customer base without costly physical retail channels.

Which geographic areas present the next growth frontier for MVNOs?

Rural prefectures such as Hokkaido and regions across Kyushu offer new revenue pools as satellite backhaul overcomes terrestrial coverage gaps.

Page last updated on: