Sweden Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.02 Billion |

| Growth Rate (2025 - 2030) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

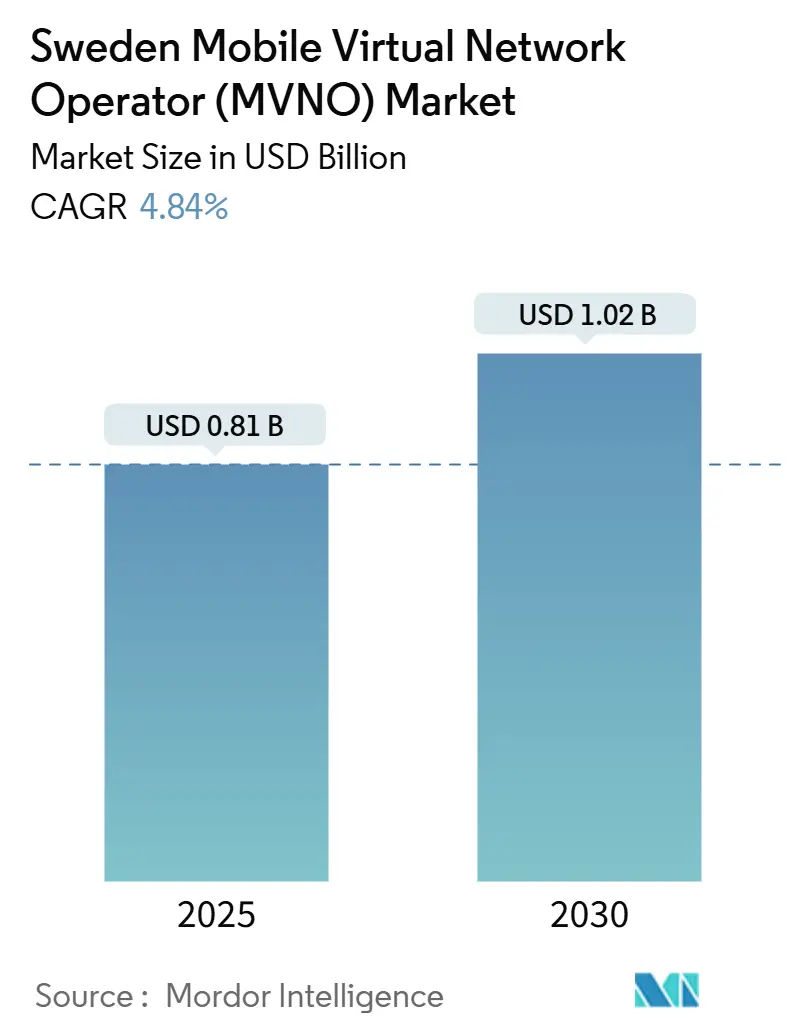

The Sweden Mobile Virtual Network Operator Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 1.02 billion by 2030, at a CAGR of 4.84% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 0.86 million Subscribers in 2025 to 1.06 million Subscribers by 2030, at a CAGR of 4.31% during the forecast period (2025-2030).

The growth is driving as operators leverage 5G wholesale access frameworks and cloud-native platforms. Continued policy support from the Swedish Post and Telecom Authority (PTS) keeps wholesale prices competitive, allowing new entrants to sustain lower tariffs while established brands prioritize profitability over rapid expansion. The Sweden MVNO market now pivots on digital-only onboarding, eSIM activation, and cloud orchestration, each trimming operating costs and shortening time-to-market for niche propositions. 5G coverage already reaches more than 90% of residents through the Net4Mobility partnership, positioning MVNOs to monetize premium data tiers and IoT bundles without costly radio investments [1]Tele2 AB, “Tele2 and Telenor Now Cover Over 90% of Sweden’s Population with 5G,” TELE2.COM. Meanwhile, Telia, Tele2, and Telenor deploy “fighter brands” to defend share in discount segments, intensifying competition yet stimulating service innovation across the Sweden MVNO market.

Key Report Takeaways

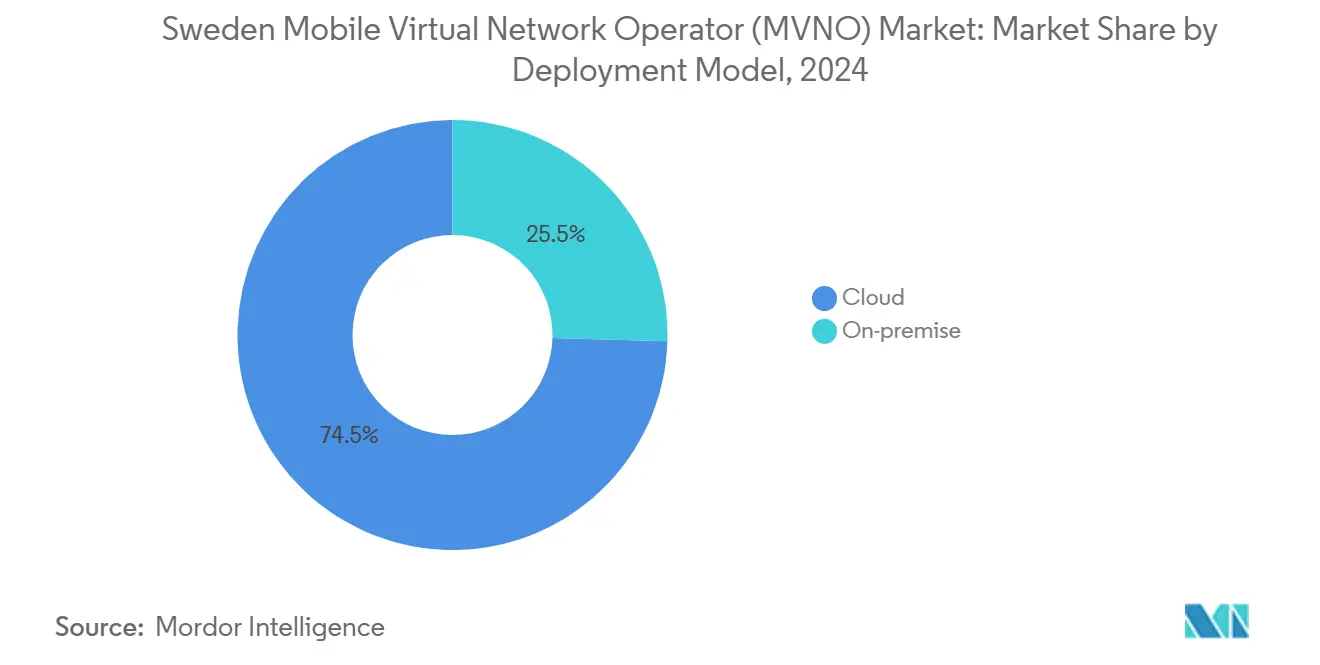

- By deployment model, cloud infrastructure led with 74.54% of the Sweden MVNO market share in 2024, and is projected to grow at an 8.18% CAGR through 2030.

- By operational mode, reseller and light MVNOs controlled 57.33% of the Sweden MVNO market size in 2024, while full MVNOs are expected to expand at a 15.69% CAGR to 2030.

- By subscriber type, consumer lines captured 78.87% share in 2024; IoT subscriptions are forecast to accelerate at 17.56% CAGR through 2030.

- By application, the other application segment, largely discount propositions, held 43.60% of the Sweden MVNO market size in 2024, whereas cellular M2M is poised for a 23.88% CAGR to 2030.

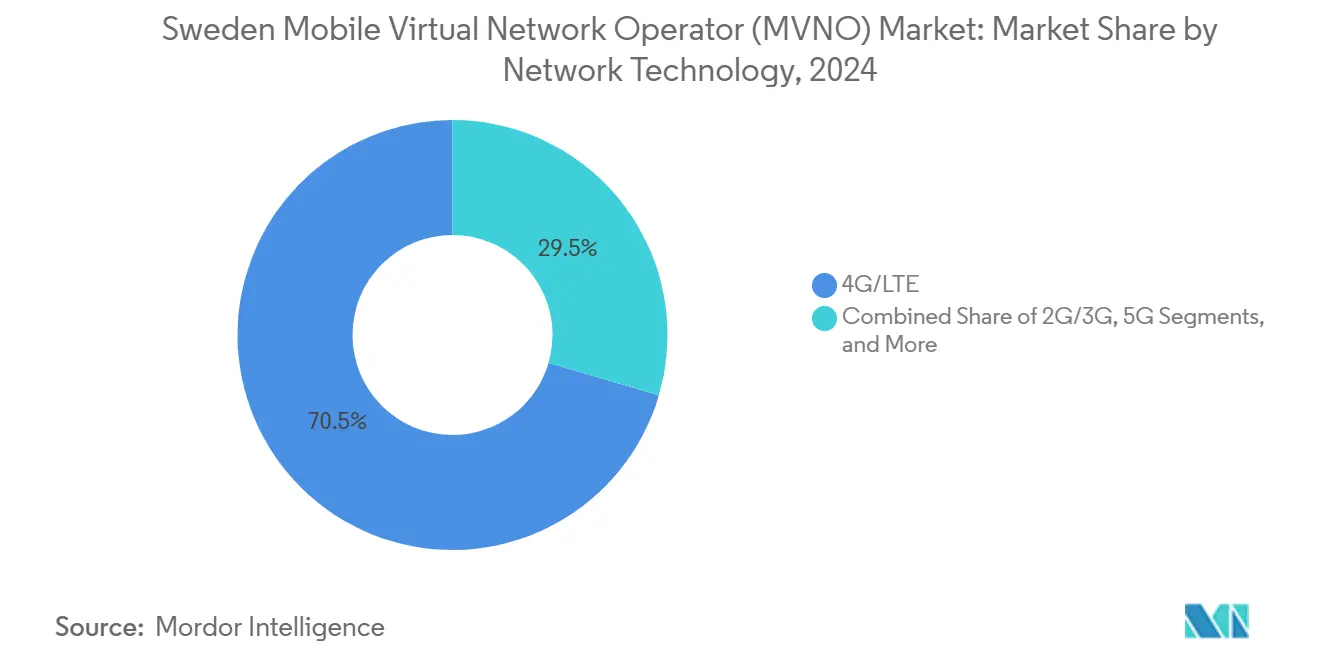

- By network technology, 4G/LTE remained dominant with 70.47% share in 2024; satellite-NTN solutions are on course for an 84.03% CAGR up to 2030.

- By distribution channel, digital-only onboarding accounted for 57.08% of 2024 activations and is projected to rise at a 7.74% CAGR toward 2030.

Sweden Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G wholesale access and network-sharing frameworks | +1.2% | Stockholm, Gothenburg, Malmö | Medium term (2-4 years) |

| Growing demand for low-cost, digital-only SIM plans | +0.8% | Urban centers nationwide | Short term (≤ 2 years) |

| Rapid eSIM uptake streamlining customer onboarding | +0.6% | National | Short term (≤ 2 years) |

| Fintech-telco convergence unlocking bundled revenue | +0.4% | Financial hubs | Long term (≥ 4 years) |

| Carbon-neutral IoT connectivity appealing to ESG-driven enterprises | +0.3% | Industrial regions | Medium term (2-4 years) |

| Public-sector tenders mandating multi-operator redundancy | +0.2% | Government agencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Wholesale Access and Network-Sharing Frameworks

Net4Mobility’s lattice of shared 5G sites gives MVNOs coast-to-coast reach at wholesale rates well below stand-alone roll-outs [2]Ookla, “Nordics Lead in 5G Availability,” OOKLA.COM. Obligatory coverage clauses baked into Swedish spectrum auctions ensure rural footprints rival urban performance, letting brands cultivate uniform service tiers without capex strain. Competitive parity forces Telia to replicate wholesale price points, widening the addressable base for premium data bundles while supporting measured growth of the Sweden MVNO market.

Growing Demand for Low-Cost, Digital-Only SIM Plans

Operators like Chilimobil advance pure-online models that bypass retail rents; the brand turned first-time positive EBITDA in 2024 on 15% revenue growth by touting unlimited data under SEK 300 (USD 28) plans. A 76% share of MVNO subscribers rate price over speed, validating the digital-only playbook and consolidating churn toward apps that promise instant activation and transparent bills.

Rapid eSIM Uptake Streamlining Customer Onboarding

Comviq’s app-based flow activates service in minutes with Mobilt BankID, shaving SIM logistics costs and elevating net-promoter scores above the MNO average [3]Comviq, “Get Started with Your eSIM,” COMVIQ.SE. The frictionless start drives cross-border travelers and digital nomads to the Sweden MVNO market, positioning eSIM-first operators to capture incremental roaming spend.

Fintech-Telco Convergence Unlocking Bundled Revenue

Klarna’s teaser of a bundled wallet-plus-connectivity service hints at Sweden’s appetite for hybrid propositions that entwine payments, credit, and mobile data [4]Sifted, “Klarna Mobile Plans,” SIFTED.EU . MVNOs see higher ARPU and lower churn when financial features anchor subscribers, signaling a runway for revenue layering once regulatory nods align.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale access fees from dominant MNOs | -0.9% | National | Short term (≤ 2 years) |

| MNO “fighter brands” tightening retail pricing | -0.7% | Major cities | Short term (≤ 2 years) |

| Scarcity of E.212 MNC codes limiting full-MVNO scaling | -0.4% | National | Long term (≥ 4 years) |

| 3G/2G sunset forcing expensive SIM-swap campaigns | -0.3% | Rural zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Wholesale Access Fees from Dominant MNOs

With three network owners, bargaining power stays skewed; interconnect and data-haul rates remain above the modeled cost in Brussels benchmarks, curbing margin expansion for new entrants. MVNOs counter by pruning channel costs and upselling value-added services rather than chasing headline-price wars.

MNO “Fighter Brands” Tightening Retail Pricing

Telia’s multi-brand ladder lets it slash entry-level tariffs without bruising premium flags, effectively setting a ceiling on MVNO discounting headroom. Sustained cross-subsidy from enterprise contracts means MVNOs must pivot from price leadership to experiential or vertical differentiation to sustain their stake in the Sweden MVNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud platforms held 74.54% of the Sweden MVNO market share in 2024 as operators sought elastic core networks without capital-heavy hardware. That dominance enabled a lean opex structure and sharp release cycles for tariff tweaks, pushing cloud deployments toward an 8.18% CAGR to 2030. The Sweden MVNO market size for on-premise installations still caters to regulated verticals, yet the cloud’s trajectory will compress its footprint below 20% before the decade-end. In parallel, hyperscale hosting strengthens data analytics and AI-driven marketing, letting MVNOs segment prospects granularly and surface contextual upsells without human intervention.

The transition aligns with Sweden’s wide-ranging “Digital First” agenda, which standardizes API-based exchanges between public and private services and validates cloud compliance for telecom workloads. Swedish brands integrate billing, campaign management, and care bots within a single SaaS instance, minimizing vendor lock-in and accelerating feature rollouts across the Sweden MVNO market.

By Operational Mode: Full MVNO Models Gain Strategic Importance

Reseller and light variants managed 57.33% of the Sweden MVNO market size in 2024, a testament to their low entry hurdles. Yet the full MVNO archetype is on pace for a 15.69% CAGR to 2030, driven by firms that value SIM provisioning and traffic steering for differentiation. Early movers report gross-margin lifts above 35% once voice and SMS breakage remain in-house, thereby cushioning net-income exposure when MNOs squeeze wholesale rates.

Investor enthusiasm is visible in Telness Tech’s EUR 5 million raise to export its full-stack enablement engine to North America. The Sweden MVNO market, therefore, inches toward a maturity curve where enhanced network control supersedes pure resale economics, mirroring shifts seen earlier in broadband.

By Subscriber Type: IoT Segments Drive Future Growth

Consumer accounts comprised 78.87% of active SIMs in 2024, but IoT lines will expand at a 17.56% CAGR as Sweden’s factories, ports, and logistics corridors digitize processes. Industrial customers require contractual uptime and metrics-rich dashboards, both of which fetch premium ARPU levels multiple times the consumer average.

MVNOs partner with integrators to bundle device management, cybersecurity, and cloud exchange under one invoice, taming complexity for mid-size manufacturers. Tele2’s IoT alliance with Enjay on waste-heat monitoring underscores how sensor fleets can amplify sustainability targets while extending the Sweden MVNO market beyond smartphones.

By Application: Cellular M2M Emerges as Growth Driver

The other application segment kept a 43.60% share in 2024, yet cellular M2M connections will clip along at a 23.88% CAGR into 2030 as smart grids, vending, and surveillance cams enforce always-on links. MVNOs that pre-package secure VPNs and data pooling counter steep roaming costs inherent in machine traffic.

In Sweden, utility‐meter swap-outs to LTE-M or NB-IoT modems underpin predictable, low-volume payloads that favor MVNO cost structures. This opens a lane for long-term, sticky contracts that dilute the seasonality of consumer churn and revitalize the Sweden MVNO market with higher lifetime value.

By Network Technology: Satellite-NTN Poised for Disruption

While 4G/LTE still served 70.47% of traffic in 2024, satellite-NTN services could grow by 84.03% CAGR, especially as maritime, forestry, and emergency-response agencies demand universal reach. Sateliot’s 5G NB-IoT test with Telefónica bumps the conversation from proof-of-concept to commercial road-map, signaling that spectrum harmonization hurdles are surmountable.

Swedish MVNOs envisage pay-as-you-go satellite overlays that pop in only when terrestrial signals fade, trimming monthly spend yet guaranteeing connectivity. 5G SA software cores simplify traffic hand-offs between Earth and orbit, making a hybrid footprint realistic well before 2030 for the Sweden MVNO market.

By Distribution Channel: Digital Transformation Accelerates

Digital-only sign-ups accounted for 57.08% of total activations in 2024, buoyed by Sweden’s near-universal BankID adoption that validates identity within seconds. The channel will rise at a 7.74% CAGR as virtual assistants, embedded plan marketplaces, and direct-to-device provisioning become familiar.

Physical storefronts remain a bridge for senior citizens and device finance, but each closure saves operators about USD 140,000 in annual lease and staffing, bolstering EBITDA. MVNOs notching over 80% e-care interactions report churn reductions nearing 2 percentage points annually, reinforcing digital’s pivotal role across the Sweden MVNO market.

Geography Analysis

Urban corridors from Stockholm to Malmö host the densest MVNO adoption, reflecting tech-savvy demographics and abundant 5G capacity. Data allowances per user average 37 GB monthly in inner-city postcodes, roughly 1.4 times rural usage, anchoring upside for premium tiers. Rural communities, historically underserved by terrestrial coverage, now test satellite-NTN pilots that promise 100% nationwide reach by 2028.

Northern municipalities bet on IoT for forestry and mining automation, translating into early demand for narrow-band connections and edge analytics. Government tenders stipulate multi-operator redundancy for critical services, granting MVNOs a seat at procurement tables typically reserved for MNOs. Cross-border commuters into Denmark and Norway benefit from EU zero-roam rules that flatten charges, augmenting the stickiness of Swedish brands abroad.

Region-wide, the Nordic ethos of sustainability elevates carbon-neutral SIM propositions that track supply-chain emissions. Operators certify renewable power use in cloud regions housing their virtual cores, a credential resonating across the Sweden MVNO market and neighboring Finland, where green KPIs already steer purchasing policies.

Competitive Landscape

Sweden MVNO market presents a semi-consolidated market concentration. Vimla grabbed pole position in the 2025 consumer polls for price clarity and contract-free ethos. Hallon widened its automation stack via Billogram-powered e-billing, slashing payment-related calls by 60% and reallocating agents to upsell roles.

MNO fighter brands Still, Fello, and Halebop tightly flank MVNO price points, curbing runaway share grabs; however, incumbents shy from cannibalizing flagship ARPU, thereby ceding experiential niches to agile challengers. Cloud-native newcomers deploy Ericsson’s Aduna API fabric, which unlocks network slicing, quality-of-service toggles, and location triggers once reserved for MNO verticals. These capabilities let MVNOs craft tiered latency or security grades that attract enterprises reluctant to negotiate bespoke deals with large carriers.

As 3G sunsets complete by 2027, SIM-swap campaigns offer a land-grab for providers bundling free device upgrades; cost structures will favor those with digital-first logistics over stores. Private-equity funds circle niche IoT MVNOs, lured by high-gross-margin, low-churn books. The Sweden MVNO market thus remains a contest of operational efficiency, technology leverage, and micro-segment focus rather than sheer scale.

Sweden Mobile Virtual Network Operator (MVNO) Industry Leaders

Comviq (Tele2 Sverige AB)

Hallon (Hi3G Access AB)

Vimla (Telenor Sverige AB)

Fello AB

Lycamobile Sweden Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chilimobil rolls out eSIM to all customers, enabling same-day activation without physical SIMs.

- December 2024: Net4Mobility, the Tele2–Telenor JV, surpasses 90% population 5G coverage milestone.

- April 2024: Telness Tech raises EUR 5 million to finance U.S. launch of its cloud MVNO platform.

Sweden Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller/ Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller/ Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How large is the Sweden MVNO market in 2025?

The Sweden MVNO market size reached USD 0.81 billion in 2025 and is on track for USD 1.02 billion by 2030.

What is the projected growth rate through 2030?

Aggregate revenue is forecast to rise at a 4.84% CAGR over the 2025–2030 period.

Which deployment model leads today?

Cloud-based cores dominate with 74.54% share owing to scalable opex and faster service launches.

Which segment is growing fastest?

Satellite-NTN connectivity shows the highest CAGR at 84.03% as coverage gaps drive demand for space-based back-haul.

Why are full MVNOs gaining traction?

Full control of SIMs and traffic enables richer service quality, lifting gross margins versus light resale models.

How will the 3G shutdown affect subscribers?

Legacy users will need SIM swaps or device upgrades before 2027, presenting a churn opportunity for eSIM-ready providers.

Page last updated on: