Denmark Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

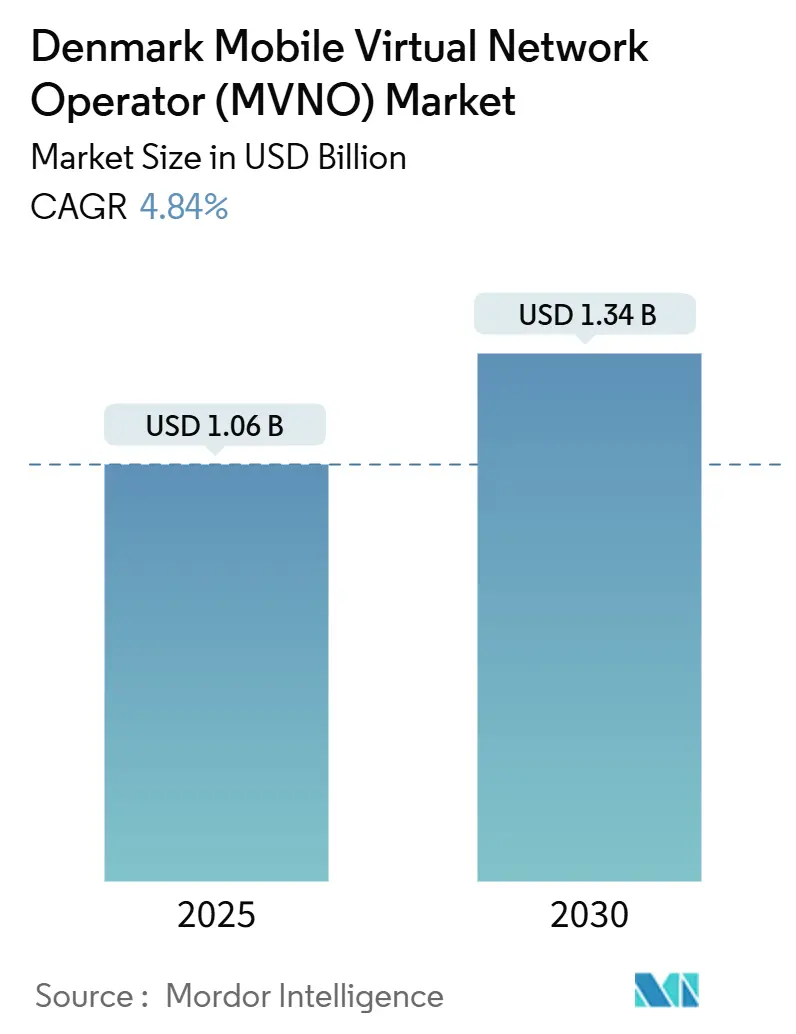

| Market Size (2025) | USD 1.06 Billion |

| Market Size (2030) | USD 1.34 Billion |

| Growth Rate (2025 - 2030) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Denmark Mobile Virtual Network Operator Market size is estimated at USD 1.06 billion in 2025, and is expected to reach USD 1.34 billion by 2030, at a CAGR of 4.84% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 3.73 million Subscribers in 2025 to 4.64 million Subscribers by 2030, at a CAGR of 4.49% during the forecast period (2025-2030).

The growth trajectory balances a near-saturated subscriber base with fresh revenue streams from 5G-enabled services, IoT-centric offerings, and satellite–terrestrial hybrid connectivity. Intense competition, price transparency, and EU-mandated wholesale access have lowered entry barriers, while Denmark’s 83.4% 5G population coverage in 2024 supplies the bandwidth and latency profile virtual operators need to monetize premium data products [1]Ookla, “Speedtest Connectivity Report | Denmark H1 2024,” ookla.com. Cloud-native core networks, eSIM uptake, and sustainability branding provide additional levers for differentiation as MVNOs pivot from pure discount propositions toward value-based segmentation. Consolidation moves such as Telia’s USD 915 million sale to Norlys reshape the competitive field, offering scale benefits but also heightening wholesale-price negotiations [2]Telia Company, “Sale of Telia Denmark to Norlys Closes,” teliacompany.com .

Key Report Takeaways

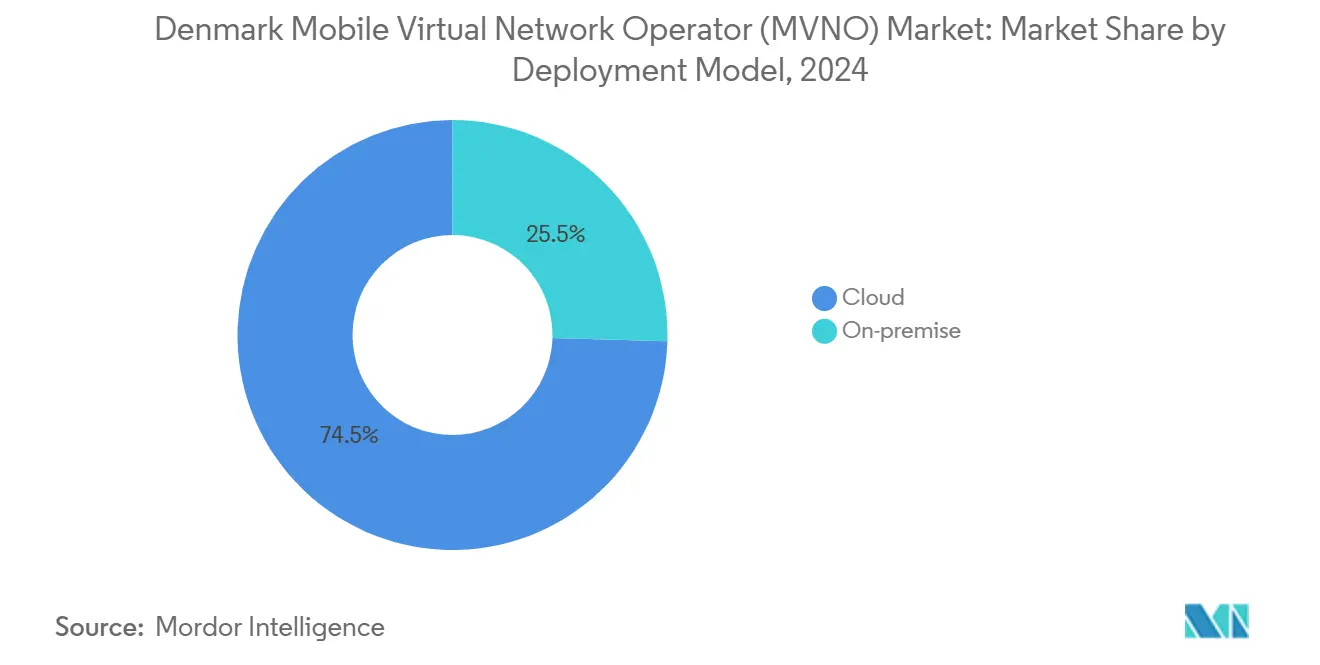

- By deployment model, cloud infrastructure captured 74.54% of Denmark's MVNO market share in 2024. Cloud deployments recorded the fastest 8.18% CAGR through 2030.

- By operational mode, reseller/light/brand MVNOs held 55.84% of the Denmark MVNO market share in 2024. Full MVNOs exhibited the highest 16.56% CAGR through 2030.

- By subscriber type, consumers accounted for 80.11% of the Denmark MVNO market size in 2024. IoT-specific lines are projected to grow at a 20.27% CAGR between 2025-2030.

- By application, discount plans retained a 37.22% share of the Denmark MVNO market size in 2024, whereas cellular M2M connectivity is expanding at a 17.56% CAGR toward 2030.

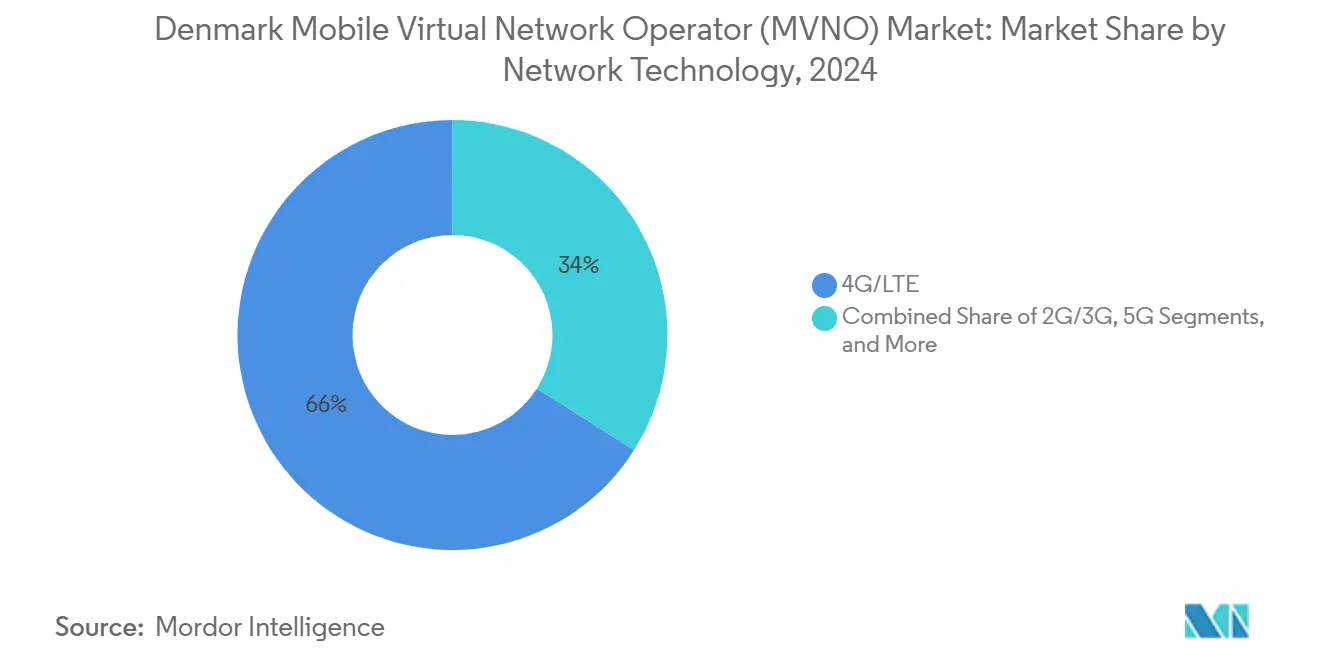

- By network technology, 4G/LTE maintained a 66.01% share in 2024, while satellite/NTN lines posted a 44.65% CAGR outlook.

- By distribution channel, online/digital-only sales delivered 57.19% of 2024 revenue and are scaling at 7.84% CAGR to 2030.

Denmark Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High smartphone and mobile-data consumption surge | +1.2% | National – urban focus | Short term (≤ 2 years) |

| EU-mandated open-network access spurring competition | +0.8% | EU-wide – Denmark early adopter | Medium term (2-4 years) |

| Price-sensitive consumers demanding flexible low-cost plans | +0.6% | National – rural and suburban | Short term (≤ 2 years) |

| Rapid IoT/M2M adoption across Danish verticals | +0.9% | National – industrial hubs | Long term (≥ 4 years) |

| eSIM uptake lowering entry barriers for digital-only MVNOs | +0.7% | Global trend – early adopter | Medium term (2-4 years) |

| Sustainability-minded users fueling eco-oriented brands | +0.4% | National – urban cohorts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High smartphone and mobile-data consumption surge

Median mobile download speeds climbed to 148.44 Mbps in H1 2024, a double-digit increase over H2 2023, signaling persistent data appetite among Danish users. MVNOs exploit this consumption spike by negotiating deeper volume discounts from MNOs and bundling unlimited or high-cap data allowances that resonate with heavy streamers. Digital-only brands swiftly re-bundle plans via cloud billing engines, avoiding legacy OSS constraints. Network slicing on Denmark’s standalone 5G core lets virtual operators guarantee bandwidth for gaming or UHD streaming at premium rates. Unlimited data success stories from OiSTER and Telmore bolster confidence that higher-value data propositions can offset churn even in a price-driven arena [3]OiSTER, “Mobilabonnement med Fri Tale & Fri Data,” oister.dk. As video streaming shifts toward 4K and cloud gaming matures, data-centric differentiation gains strategic importance.

EU-mandated open-network access spurring competition

The forthcoming Digital Networks Act will compel harmonized MVNO access rights and wholesale pricing across the bloc, strengthening Denmark’s role as an early compliance test bed [4]Bird & Bird, “EU Telecoms Reform: Digital Networks Act,” twobirds.com. Denmark’s early implementation of cost-oriented termination rates at EUR 0.2 cents per minute already signals regulatory friendliness. Predictable pricing and non-discriminatory terms shrink the risk profile for new entrants, encouraging niche MVNO launches focused on expatriates, students, or sustainability enthusiasts. Infrastructure-sharing clauses under EU Regulation 2024/1309 unlock very-high-capacity networks for virtual players, lowering entry CapEx. While GDPR compliance raises operational overhead, it also builds trust among privacy-conscious Danish subscribers, providing an edge to operators with established governance frameworks.

Price-sensitive consumers demanding flexible low-cost plans

Competitive monthly tariffs beginning at DKK 59 motivate rapid switching behavior and elevate comparison sites such as Samlino, intensifying price transparency. MVNOs harness no-commitment models to trim acquisition costs and present clear value in a marketplace that shuns lock-in contracts. Bundles combining streaming subscriptions or roaming add-ons deliver upsell paths without undermining headline pricing. Economic headwinds through 2025 heighten household budget scrutiny, making flexibility and perceived fairness decisive. Operators therefore refine digital journeys, enabling immediate plan swaps via apps and leveraging AI chatbots to prevent churn by offering micro-discounts in real time.

Rapid IoT/M2M adoption across Danish industry verticals

Industrial firms in manufacturing, logistics, and energy sectors deploy connected sensors at scale, escalating demand for low-power wide-area connectivity and dedicated service-level agreements. Onomondo’s SoftSIM for Nordic Semiconductor illustrates the specialized tools emerging MVNOs must furnish for large-volume device onboarding. The 5G standalone network rolled out by TDC NET provides millisecond-latency profiles suitable for robotics and time-sensitive production lines. Hybrid terrestrial–satellite links extend coverage to offshore wind farms and remote utility assets, enlarging the addressable base. Multi-MNO subscription models allow IoT-focused MVNOs to steer each packet via the most economical radio path, protecting margins while meeting mission-critical uptime metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-saturated mobile-subscriber base curbing volume growth | -0.9% | National – urban markets | Short term (≤ 2 years) |

| Fierce price wars compressing MVNO ARPU and margins | -1.1% | National – consolidation pressure | Medium term (2-4 years) |

| 5G standalone-core upgrade costs straining full-MVNO economics | -0.7% | National – infrastructure-heavy | Long term (≥ 4 years) |

| Sparse satellite/NTN roaming deals limiting niche coverage | -0.3% | Remote and maritime areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-saturated mobile-subscriber base curbing volume growth

SIM penetration in Denmark surpasses 100%, limiting net additions and shifting the growth game to churn capture. Discount MVNOs that once thrived on luring first-time mobile users must now wrest subscribers from rivals in an environment of converged bundles and quadruple-play packages. Acquisition cost-to-lifetime-value ratios tighten, prompting operators to pour resources into retention analytics, personalized upselling, and loyalty perks. The mature landscape reduces responsiveness to flash promotions, demanding more sophisticated segmentation and lifestyle-based propositions to eke out incremental revenue.

Fierce price wars compressing MVNO ARPU and margins

Monthly plan races to the bottom, highlighted by sub-60 DKK tiers, erode per-user margins across the board. Consolidation events like Telia-Norlys and Lebara’s private-equity backing amplify purchasing power, enabling bulk wholesale rate negotiations that squeeze smaller independents. Sustainability-branded entrants such as Worthmore still resort to aggressive introductory pricing, proving that even mission-driven niches cannot escape cost competition. Voice termination-rate cuts, while consumer-friendly, remove a historical revenue cushion. To sustain EBITDA, MVNOs are automating support via AI, adopting usage-based billing, and exploring ancillary digital services from device insurance to cybersecurity add-ons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud deployments accounted for 74.54% of Denmark's MVNO market share in 2024 and are expected to drive growth at a CAGR of 8.18% over the forecast period, reflecting widespread migration away from on-premise cores. This dominance is supported by the elasticity that turns CapEx into pay-as-you-grow OpEx, aligning perfectly with subscriber-base volatility. Full-stack digital-only brands leverage cloud OSS/BSS to cut launch times from months to weeks, feeding the Denmark MVNO market’s appetite for rapid service refreshes. Nuuday’s 2023 IT modernization underscored the efficiencies attainable through cloud-native stacks.

On-premise installations persist for financial services and public-sector MVNOs that must host data locally under stringent sovereignty rules. Even here, a shift to micro-services architecture allows selective cloud bursting for analytics workloads, balancing compliance with cost. The Denmark MVNO market size for cloud deployments is projected to grow alongside enterprise SaaS adoption, as operators integrate AI-driven quality-of-experience dashboards and real-time fraud analytics.

By Operational Mode: Full MVNOs Emerge as Growth Leaders

Reseller and light MVNOs held 55.84% share of the Denmark MVNO market size in 2024, capitalizing on fast time-to-market and minimal network commitments. Yet Full MVNOs clock a 16.56% CAGR outlook through 2030, indicating an industry pivot to network ownership elements that unlock distinctive service levers. The economics improve as Denmark’s 5G standalone architecture permits dynamic multi-MNO routing, transforming what was once a heavy fixed-cost model into a variable-cost play. Telenor Denmark’s partnership with CSG underlines how cloud-delivered policy control arms Full MVNOs with comparable agility to light peers while preserving margin upside.

Middle-ground service-operator MVNOs offer managed solutions attractive to industrial clients that prize dedicated APNs and secure tunneling without the full burden of core ownership. Such hybrids are expected to proliferate as IoT deployments demand granular control mixed with cost restraint.

By Subscriber Type: IoT Segments Drive Future Growth

Consumers comprised 80.11% of total SIMs in 2024, anchoring the revenue base for most brands. Enterprise lines contribute higher average revenue and longer contracts, safeguarding cash flow but representing a smaller volume. The IoT segment, though currently niche, is forecast to grow at a 20.27% CAGR, reshaping the Denmark MVNO market by 2030. Onomondo’s evolved eSIM orchestration exemplifies the specialized onboarding tools required to efficiently provision millions of low-power devices.

Regulated industries such as utilities, transportation, and healthcare value MVNOs able to guarantee low-latency links and offer specialized billing, often per-byte or per-event rather than per-SIM. This shift hedges operators against softness in consumer ARPU and creates cross-selling opportunities with analytics and cloud dashboards.

By Application: M2M Connectivity Transforms Market Dynamics

Discount mobile plans held a 37.22% share in 2024, driven by Denmark’s price-savvy households and student population. Business applications add stickiness through unified communication suites, VPN integration, and centralized device management, a segment strengthened by Telenor’s AI-infused TrueTalk B2B platform. The fastest expansion, at 17.56% CAGR, occurs in cellular M2M uses, connected manufacturing gear, smart meters, and telematics, because these applications suit Denmark’s automation push and climate-tech investments.

As M2M volumes rise, MVNOs must adjust SIM lifecycle processes, switching from human-centric marketing to API-driven device onboarding, and from monthly invoicing to real-time micro-billing. Operators able to bridge cellular and satellite links win contracts for offshore wind monitoring and maritime tracking, reinforcing satellite/NTN’s rapid uptick.

By Network Technology: Satellite Integration Reshapes Coverage

4G/LTE services delivered 66.01% of revenue in 2024, remaining the workhorse for voice and most data. Denmark’s lead in 5G coverage, reaching 83.4% of the population by Q4 2024, provides a foundation for network-sliced, low-latency vertical solutions. Operators phase out 3G early to repurpose spectrum, compelling some MVNOs to accelerate handset refresh campaigns.

Satellite/NTN subscriptions, albeit small today, score a 44.65% CAGR outlook. Nordic Semiconductor’s guidance on NTN IoT modules underscores device-side readiness. Hybrid architectures permit uninterrupted coverage for maritime transport, fisheries, and renewable-energy platforms in the North Sea, extending MVNO addressable markets and reinforcing Denmark’s smart-harbor initiatives.

By Distribution Channel: Digital Transformation Accelerates

Online/digital-only channels secured a 57.19% share in 2024, boosted by high credit-card penetration, strong consumer trust in e-commerce, and the proliferation of 337 eSIM plans tailored for instant activation. Physical retail slowly recedes as Danes grow comfortable performing KYC via NemID and MitID. Still, brick-and-mortar stores survive as experiential hubs for device upselling and troubleshooting.

Carrier sub-brand shops leverage incumbents’ retail footprints to showcase differentiated propositions without cannibalizing flagship price points. Third-party/wholesale partnerships allow niche MVNOs to piggyback on electronics retailers and energy cooperatives, mirroring Norlys’s converged service play across fiber, energy, and mobile. Overall, the Denmark MVNO market anticipates deeper integration of subscription management into super-apps, loyalty wallets, and smart-home dashboards.

Geography Analysis

Denmark boasts 98.8% access to next-generation fixed access networks, ensuring that backhaul constraints rarely throttle MVNO downlink performance. Urban centers such as Copenhagen and Aarhus concentrate premium-ARPU segments demanding unlimited data and bundled entertainment. Rural Jutland, while fully covered by 4G, shows elevated elasticity to price, reinforcing discount MVNO traction.

Nine of eleven administrative regions exceed 95% VHCN coverage, opening opportunities for region-specific offers, such as agricultural IoT packages in North Denmark. The cross-border Nordic market presents a natural expansion terrain thanks to cultural affinity and aligned regulatory regimes. Failed mega-mergers like Telenor–Telia demonstrate regulators’ resolve to preserve MVNO headroom, a precedent that benefits Danish virtual operators exploring Sweden or Norway.

EU integration, coupled with standardized wholesale charges, eases multi-country eSIM plan launches. Danish brands can therefore upsell roaming-free Nordic or EU packages to digital nomads and export-oriented SMEs, layering connectivity atop Denmark’s reputation for telecom innovation and data-privacy rigor.

Competitive Landscape

The Denmark MVNO market hosts a blend of legacy heavyweights (Telmore, CBB Mobil, OiSTER) and international specialists (Lycamobile, Lebara). The Telia-Norlys deal forged Denmark’s largest integrated energy-telecom group, enabling bundle cross-sell across 1.7 million energy customers and strengthening wholesale bargaining clout. Lebara’s Waterland buyout injects fresh capital for 5G core upgrades, VoNR rollout, and marketing to immigrant communities.

Disruptors such as Worthmore appeal to eco-conscious Millennial and Gen Z customers by pledging handset recycling and charity contributions with every subscription. Technology partnerships form a key competitive lever, like Norlys contracted RADCOM for AI-based quality analytics, promising superior network experience insights for its MVNO tenants.

Strategic positioning now tilts toward service innovation rather than price alone. MVNOs integrate OTT streaming, cloud gaming passes, or carbon-footprint dashboards to increase ARPU and cement brand loyalty. As satellite/NTN access matures, expect maritime MVNOs targeting Denmark’s shipping cluster, further fragmenting the competitive map yet opening lucrative vertical silos.

Denmark Mobile Virtual Network Operator (MVNO) Industry Leaders

Telmore A/S

CBB Mobil A/S

Oister (Hi3G Denmark ApS)

Lycamobile

Lebara Group B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Telenor Denmark launched the “TrueTalk” B2B solution powered by Gintel, targeting enterprise users with AI-driven omnichannel communications Total Telecom.

- September 2024: Swedish broadband operator Bahnhof entered Denmark via a Norlys partnership, intensifying wholesale-rate negotiations Mobile Europe.

- August 2024: MVNO Lebara was acquired by Waterland Private Equity, securing funds for 5G expansion Total Telecom.

Denmark Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How fast is the Denmark MVNO market expected to grow to 2030?

It is projected to reach USD 1.34 billion by 2030, expanding at a 4.84% CAGR.

Which subscriber segment is growing the quickest?

IoT-specific lines, forecast to register a 20.27% CAGR through 2030.

What share do cloud deployments hold in Denmark’s MVNO ecosystem?

Cloud models commanded 74.54% of 2024 revenue and remain the fastest-growing deployment choice.

Why are Full MVNOs gaining traction?

Greater control over the core network and the ability to deploy differentiated 5G services support a 16.56% CAGR outlook.

How significant is satellite connectivity for Danish MVNOs?

Satellite/NTN remains small today yet shows a 44.65% CAGR, extending coverage to maritime industries and remote renewables.

Which distribution channel dominates sales?

Online/digital-only platforms captured 57.19% of 2024 revenue thanks to eSIM and app-based onboarding.

Page last updated on: