UK Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

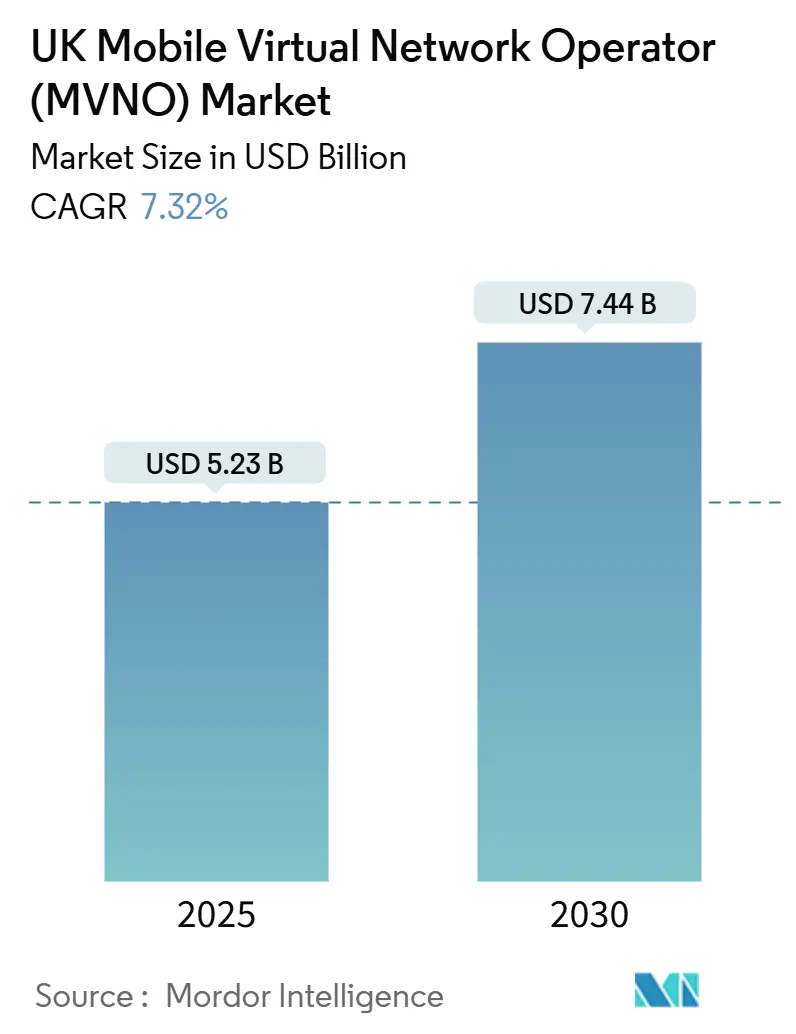

| Market Size (2025) | USD 5.23 Billion |

| Market Size (2030) | USD 7.44 Billion |

| Growth Rate (2025 - 2030) | 7.32% CAGR |

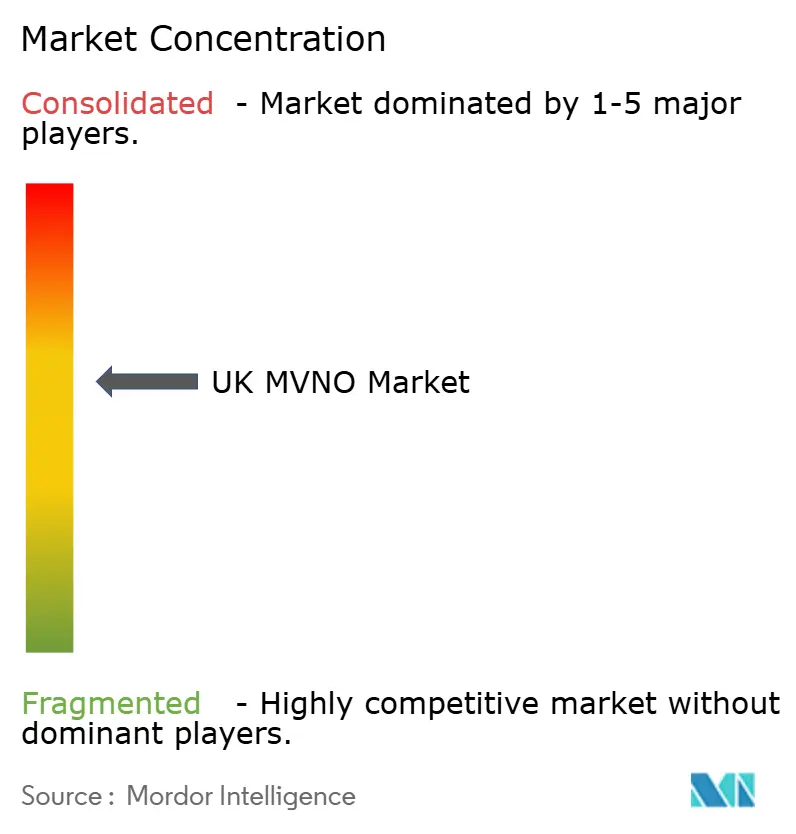

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The UK Mobile Virtual Network Operator Market size is estimated at USD 5.23 billion in 2025, and is expected to reach USD 7.44 billion by 2030, at a CAGR of 7.32% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 20.19 million Subscribers in 2025 to 26.18 million Subscribers by 2030, at a CAGR of 5.34% during the forecast period (2025-2030).

Sustained wholesale 5G price erosion, eSIM-led digital entry models, and a pro-consumer regulatory stance are accelerating virtual operator growth while reshaping competitive bargaining power. The Vodafone-Three merger, completed in 2025, compressed the host-network pool from four to three but, under OFCOM-mandated conditions, locked in MVNO-friendly access terms for 36 months, lowering the cost of service and encouraging aggressive pricing [1]Fierce Network, “Vodafone UK and Three UK Complete $20B Merger After 2 Years,” fierce-network.com. Virgin Media O2’s GBP 343 million spectrum purchase further intensified wholesale competition by injecting fresh mid-band capacity into the negotiation mix [2]Telecoms.com, “VMO2 Finalises £343 Million Spectrum Deal with VodafoneThree,” telecoms.com. Parallel regulatory moves, such as the nationwide ban on inflation-linked mid-contract price rises effective January 2025, have improved price transparency, reduced switching friction, and widened the addressable customer base for every UK MVNO market participant [3]ISPreview, “Ofcom UK Approve Plan to Ban Some Mid-Contract Broadband Price Hikes,” ispreview.co.uk .

Key Report Takeaways

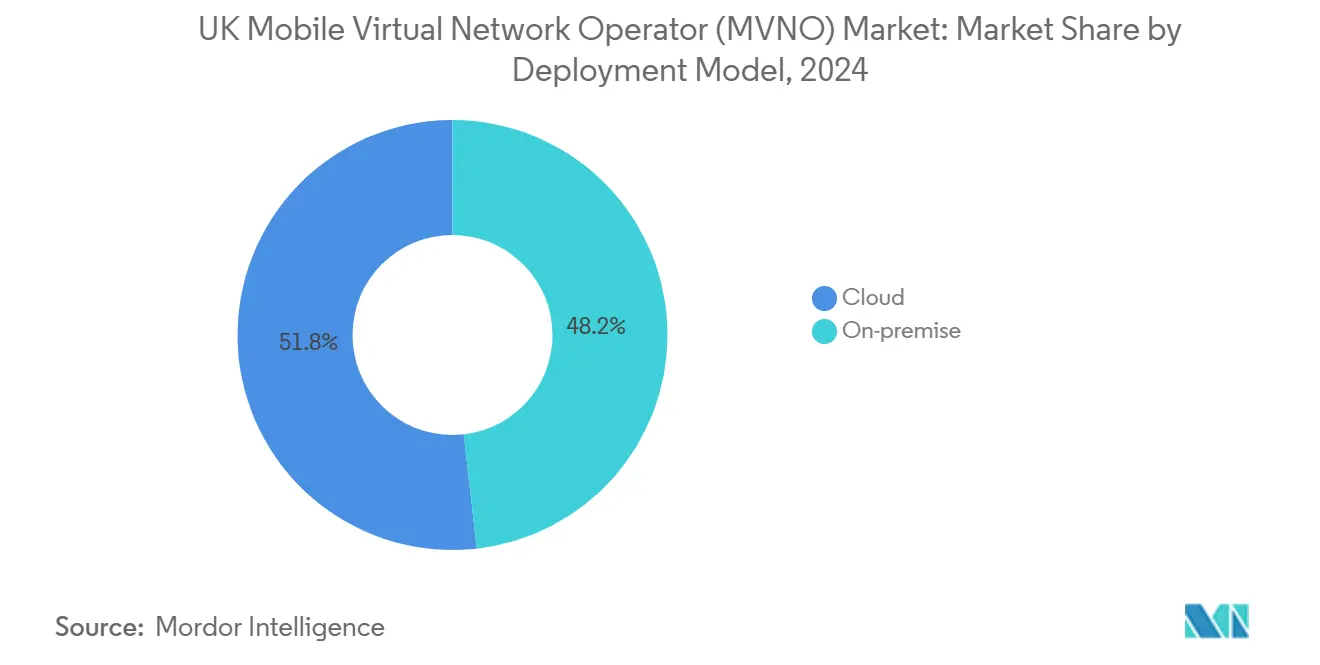

- By deployment model, cloud solutions accounted for 51.80% share of the UK MVNO market size in 2024 and are forecast to expand at 14.82% CAGR to 2030.

- By operational mode, Full MVNOs captured 58.00% of the UK MVNO market share in 2024 and are advancing at a 9.39% CAGR through 2030.

- By subscriber type, consumer connections held 81.80% revenue share in 2024, whereas IoT-specific lines are projected to post the fastest 23.49% CAGR between 2025 and 2030.

- By application, other applications held 31.00% revenue share in 2024, whereas Cellular M2M is projected to post the fastest 18.26% CAGR between 2025 and 2030.

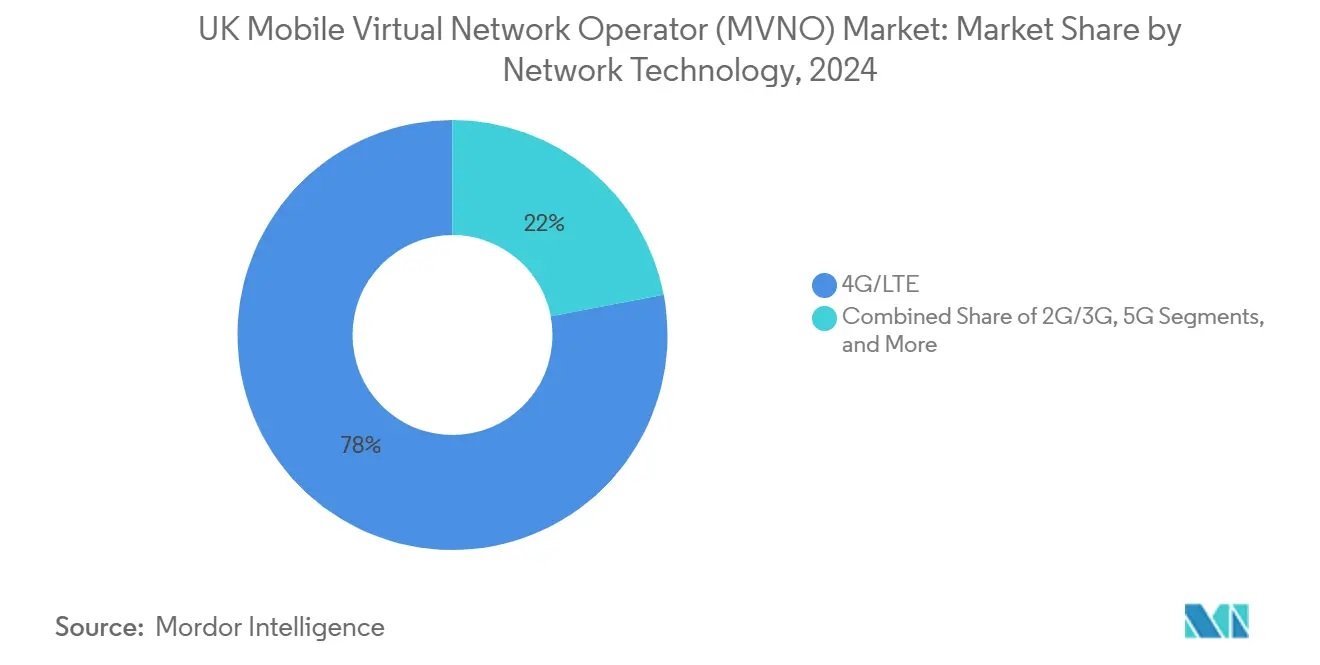

- By network technology, 4G/LTE remained dominant at 78.00% share in 2024, while Satellite/NTN is expected to surge at an 88.39% CAGR through 2030.

- By distribution channel, online and digital-only routes commanded 42.00% revenue share in 2024 and are growing at a 15.36% CAGR through 2030.

UK Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising wholesale 5G access price declines | +1.2% | UK nationwide, concentrated in urban centers | Medium term (2-4 years) |

| Regulatory pressure for fair use and roaming transparency | +0.8% | UK nationwide with EU regulatory alignment | Short term (≤ 2 years) |

| E-SIM–first digital brands lowering entry barriers | +1.5% | UK nationwide, higher adoption in London and major cities | Short term (≤ 2 years) |

| Convergence demand from fiber/quad-play bundles | +1.1% | UK nationwide, stronger in suburban markets | Medium term (2-4 years) |

| Growth of ethnic/expat remittance corridors | +0.7% | London, Birmingham, Manchester, Leicester | Long term (≥ 4 years) |

| Post-Brexit enterprise IoT private-label niches | +0.9% | UK nationwide, concentrated in industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising wholesale 5G access price declines

Regulatory undertakings tied to the VodafoneThree merger compel the newly formed operator to keep wholesale 5G rates “fair and reasonable” until 2028, effectively subsidizing virtual access to standalone 5G features such as network slicing [4]CMS, “5G Regulation and Law in United Kingdom,” cms.law. Concurrently, Virgin Media O2’s mid-band spectrum acquisition of 78.8 MHz for GBP 343 million has created a competing wholesale channel that exerts downward pricing pressure across the UK MVNO market. More than 3,300 standalone 5G sites are now live, giving MVNOs ready access to premium latency-sensitive capabilities without investing in radio hardware. Lower input costs have cascaded into consumer tariffs, broadening uptake of unlimited-data plans and reinforcing the growth trajectory of the UK MVNO market.

eSIM-first digital brands lowering entry barriers

Vodafone’s API-driven partnership with eSIM Go permits any qualified firm to spin up an MVNO in weeks rather than months, trimming launch budgets by roughly 40%. VOXI’s December 2024 eSIM rollout added same-day activation nationwide, while Ymobile debuted as the country’s first data-driven eSIM-only operator. Device readiness is also climbing: eSIM-capable smartphones are forecast to reach 58% share by 2028, multiplying the addressable base for digital-native offers. The result is intensified competition and quicker tariff innovation across the UK MVNO market.

Convergence demand from fiber/quad-play bundles

Virgin Media O2’s Volt proposition grants double mobile data and broadband speed boosts to dual-service households, proving that bundled value, instead of pure price discounting, drives retention and higher revenue per user. Giffgaff’s 500 Mbps fiber trial via Nexfibre shows even low-cost brands see strategic merit in fixed-mobile convergence. Bundled customers churn 35% less frequently, which stabilizes lifetime value and allows MVNOs to reinvest in differentiated services, sustaining the revenue expansion of the UK MVNO market.

Post-Brexit enterprise IoT private-label niches

OFCOM’s Shared Access licensing has issued more than 1,500 localized 3.8-4.2 GHz licenses since 2019, giving MVNOs spectrum autonomy for industrial campuses. Verizon and Nokia are building six private 5G networks across Thames Freeport’s logistics zone under long-term contracts worth GBP 2.5 billion, which illustrates the revenue depth of enterprise niches. These vertical deployments grant MVNOs higher-margin, service-level-agreement-backed revenues insulated from retail price wars.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Looming spectrum re-farm costs passed to MVNOs | -0.9% | UK nationwide, higher impact in dense urban areas | Medium term (2-4 years) |

| OFCOM-mandated price caps on out-of-bundle data | -0.6% | UK nationwide | Short term (≤ 2 years) |

| Limited 5G SA wholesale availability beyond 2026 | -1.1% | UK nationwide, concentrated in rural areas | Long term (≥ 4 years) |

| Rising fraud/SIM-swap compliance expenses | -0.8% | UK nationwide, higher costs for international MVNOs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Looming spectrum re-farm costs passed to MVNOs

OFCOM will revoke unpaired 2100 MHz licenses by April 2029 and increase auction deposits for forthcoming 26 GHz and 40 GHz bands to GBP 1 million, up from GBP 100,000, lifting annual spectrum fees by an estimated GBP 320 million for host MNOs. Historical precedent shows carriers transfer 12-18 months of incremental spectrum cost directly into wholesale tariffs. For cost-sensitive MVNOs, the ripple effect threatens margin compression and could slow service innovation within the UK MVNO market.

Rising fraud/SIM-swap compliance expenses

England and Wales now impose unlimited fines for SIM-farm abuse, compelling MVNOs to deploy enhanced Know-Your-Customer checks, biometric verification, and traffic-monitoring platforms. Implementation outlays run between GBP 2 million and GBP 5 million for mid-tier operators, while ongoing analytics costs trim EBITDA margins. Lycamobile’s GBP 51 million VAT dispute highlights the financial exposure of compliance missteps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud infrastructure widens scale advantages

Cloud-hosted environments accounted for 51.80% of the UK MVNO market size in 2024, and their 14.82% CAGR makes them the fastest-growing deployment choice to 2030. API-first platforms from vendors such as Gigs allow non-telco brands to embed connectivity in weeks, sharpening competitive pressure across the UK MVNO market. Full-stack cloud control lets operators implement AI-based support; VOXI’s generative chatbot raised first-contact resolution while cutting live-agent loads. On-premise deployments still command mindshare in heavily regulated or latency-sensitive industrial IoT cases, but their relative share will slide as public-cloud security accreditation improves.

Cloud adoption also underpins dynamic pricing engines that continuously test tariff bundles, crucial for defending acquisition cost efficiency in the UK MVNO market. Lower CapEx burdens and elastic scaling smooth seasonal traffic spikes, which is vital for consumer-heavy brands running time-bound promotional campaigns.

By Operational Mode: Full MVNOs consolidate leadership

Full MVNOs controlled 58.00% revenue in 2024 and will compound at 9.39% yearly through 2030, owing to their ownership of core network elements that enable flexible service packaging. iD Mobile surpassed 2 million lines after adding data rollover and inclusive EU roaming, functions complex to replicate under lighter MVNO models. Reseller MVNOs retain appeal for celebrity or retail brands needing quick market entry, but wholesale margin exposure limits profitability if scale plateaus. Service-operator hybrids bridge the gap yet face rising compliance overhead, pushing more players toward full-stack control.

Regulatory symmetry has also improved; OFCOM now applies many core-network compliance frameworks uniformly across host and virtual networks, rewarding MVNOs that already manage their own HLR/HSS platforms. That dynamic further entrenches the market clout of Full MVNOs within the UK MVNO market.

By Subscriber Type: Consumer base dominates, IoT lines surge

Consumers delivered 81.80% of 2024 revenue, proving that voice-data bundles and handset financing remain lucrative. However, IoT lines will grow at a sector-leading 23.49% CAGR, expanding the UK MVNO market into vehicle telematics, smart metering, and logistics-tracking verticals. Virgin Media O2 closed 2024 with 45.7 million total connections, citing IoT as a prime growth vector. Enterprise lines occupy the strategic midpoint: volumes trail consumer totals, but ARPU is higher and churn is lower. Overall, subscriber-type diversification cushions revenue cyclicality and widens monetization pathways across the UK MVNO market.

Scrutiny over corporate cybersecurity and data residency rules will favor MVNOs offering granular SIM-level policy controls, enhancing their relevance in Industry 4.0 frameworks. That positioning aligns with national digital-transformation funding schemes in manufacturing hubs, fostering long-run IoT adoption.

By Application: Cellular M2M accelerates industrial digitization

The other application category, including fintech bundles and community-focused plans, contributed 31.00% of the 2024 value, signaling continued creativity in service design. Cellular M2M, though representing a smaller base, is ramping at an 18.26% CAGR through 2030, driven by factory automation and smart-city projects that demand fixed public IPs and guaranteed latency. BetterM2M’s unlimited 5G plan with a static IP illustrates the premium clients will pay for niche functionality. Discount voice-centric offers remain sticky among price-sensitive families, while business applications carve mid-tier ARPU.

By Network Technology: Satellite-terrestrial integration reshapes coverage math

4G/LTE still anchors 78.00% of traffic in 2024, but standalone 5G adoption is accelerating under wholesale rate cuts. Satellite/NTN services are forecast to post an 88.39% CAGR as Virgin Media O2 deploys Starlink backhaul to plug rural not-spots. O2’s Direct-to-Cell pilot in Northumberland provided live proof of remote coverage viability. Eutelsat OneWeb completed the UK’s first 5G NTN trial in February 2025, signaling imminent commercial rollouts. As NTN handsets reach the mass market in 2027-2028, coverage economics will tilt further toward hybrid architectures, reinforcing competitive parity among nationwide MVNOs.

By Distribution Channel: Digital-only routes capture value chain margin

The online/digital-only channels generated 42.00% of revenue in 2024, rising at a 15.36% CAGR. Ymobile’s launch without any physical touchpoints confirmed that data-heavy, eSIM-only propositions resonate with younger demographics. Eliminating plastic SIM logistics cuts acquisition cost by roughly 30%, funds richer loyalty rewards, and speeds onboarding, critical weapons in the UK MVNO market’s ongoing price-value contest. Brick-and-mortar retail endures for device financing and face-to-face support, but its relative share will continue to fall as handset vendors push direct-to-consumer online sales.

Geography Analysis

The UK MVNO market enjoys 99% population reach through host-network roaming agreements, yet revenue density varies. Greater London alone delivers over one-quarter of total turnover owing to a concentration of affluent, data-hungry users who adopt 5G unlimited plans early. Birmingham, Manchester, and Leicester underpin high-margin ethnic-calling traffic, reflecting the continued vitality of international corridors. Rural Scotland and Northern Ireland historically suffered a patchy signal, but now gain from Shared Rural Network towers and LEO satellite backhaul; Virgin Media O2 even used helicopter air-lifted eNodeBs in the Highlands to expedite coverage.

Wales gains from targeted GBP 1 billion public-private investment aimed at hitting 95% 4G availability by late 2025, broadening the potential subscriber base for smaller MVNOs that specialize in utility bundles. In northern industrial belts, private 5G campus networks support smart-factory upgrades, letting enterprise-focused MVNOs pitch tailored SLAs. Geographic parity clauses in OFCOM’s wholesale-access code mean MVNOs cannot be refused service on cost grounds in any county, reinforcing national uniformity and enhancing consumer trust in the UK MVNO market.

Competitive Landscape

Market rivalry is intense yet moderately fragmented. Revenue crosses many hands, from grocery-anchored Tesco Mobile, which smashed GBP 1 billion turnover in 2024, to fintech newcomer Revolut, aiming for pan-European plans priced at GBP 12.50 a month. Technology innovation is a core weapon: VOXI’s AI chatbot boosted containment and trimmed care opex, while Utility Warehouse leverages an energy-broadband-mobile bundle that cuts household bills under one account.

Consolidation continues, Lebara’s 2024 sale to Waterland PE and Lycamobile’s downsized footprint create acquisition targets for digital-native entrants. Patent activity in eSIM orchestration and network-slicing shows MVNOs evolving into software companies capable of micro-segmenting quality of service tiers, defending margins against retail price erosion. Satellite collaborations with OneWeb or Starlink mark another differentiator by giving MVNOs a unique rural reach at minimal CapEx. Those that master convergence, AI operations, and hybrid network access will outpace voice-price discounters in the UK MVNO market.

UK Mobile Virtual Network Operator (MVNO) Industry Leaders

Tesco Mobile Limited

giffgaff Limited

Sky Mobile Services Limited

Lycamobile USA Inc.

Lebara Mobile

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: VodafoneThree completed a GBP 15 billion merger, forming the UK’s largest host operator with 27 million customers and pledging GBP 11 billion for nationwide 99% 5G coverage by 2034.

- June 2025: Virgin Media O2 secured 78.8 MHz of spectrum for GBP 343 million, bolstering 4G and 5G capacity while extending network-sharing accords.

- June 2025: Verizon and Nokia won contracts to roll out six private 5G networks across Thames Freeport’s 1,700 acres, supporting 5,000 jobs and industrial automation goals.

- April 2025: Revolut announced UK-Germany MVNO plans, bundling unlimited calls, texts, and 20 GB roaming for GBP 12.50 monthly.

- April 2025: Giffgaff began a 500-customer trial of 500 Mbps fiber broadband via Nexfibre for GBP 10 per month.

- January 2025: O2 used Starlink links to deliver 4G to Craster village, showcasing practical satellite-terrestrial integration.

UK Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller/ Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online / Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party / Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller/ Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online / Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party / Wholesale |

Key Questions Answered in the Report

How big is the UK MVNO market today?

The UK MVNO market size reached USD 5.23 billion in 2025 and is forecast to climb to USD 7.44 billion by 2030.

What is the expected growth rate for virtual operators in the UK?

Aggregate revenue is projected to grow at a 7.32% CAGR between 2025 and 2030, supported by lower wholesale 5G costs and eSIM adoption.

Which operational model leads the segment?

Full MVNOs dominate with 58.00% 2024 revenue share and are expanding at 9.39% CAGR through 2030 due to greater infrastructure control.

Why are eSIM-only brands gaining traction?

ESIM provisioning cuts launch costs by around 40%, enables instant activation, and aligns with rising device compatibility that should reach 58% penetration by 2028.

How will satellite connectivity influence UK virtual operators?

Satellite/NTN lines are poised for an 88.39% CAGR as Starlink and OneWeb backhaul fill rural gaps and enable emergency coverage without new towers.

What challenges could temper MVNO growth?

Spectrum re-farm fees passed down by host MNOs and rising fraud-mitigation compliance costs may trim margins, although regulatory safeguards aim to preserve competition.

Page last updated on: