5G MVNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.98 Billion |

| Market Size (2031) | USD 17.89 Billion |

| Growth Rate (2026 - 2031) | 5.08% CAGR |

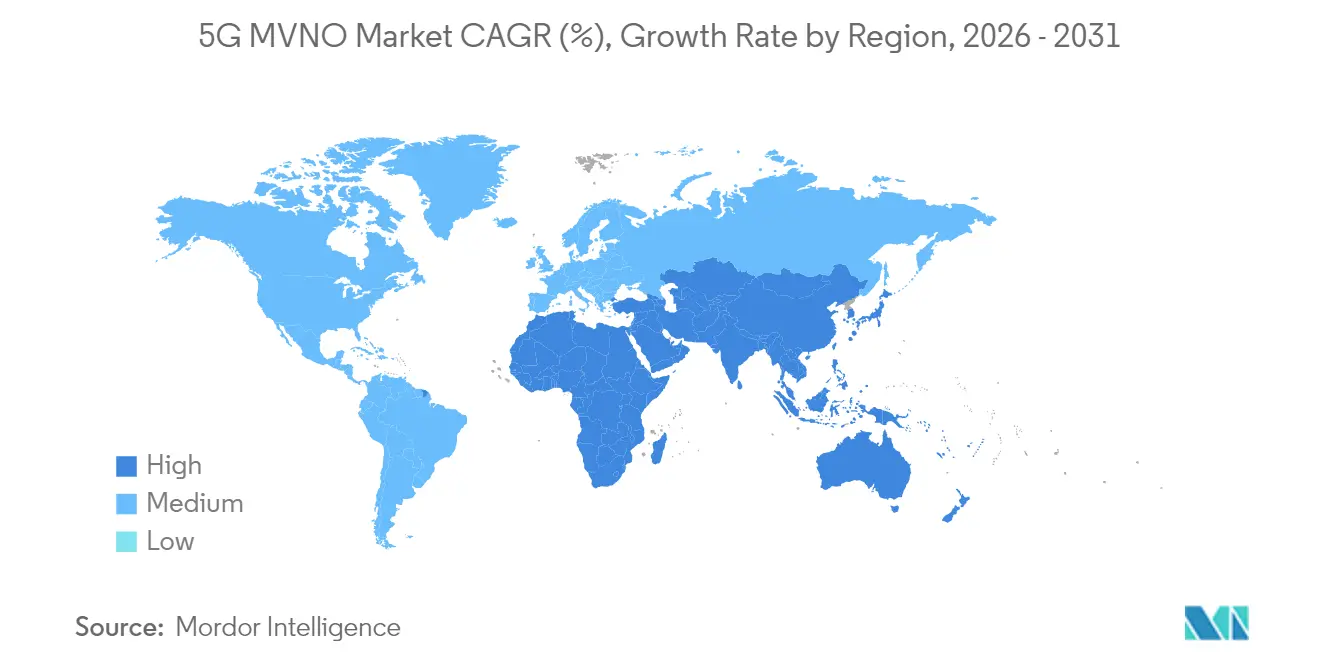

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

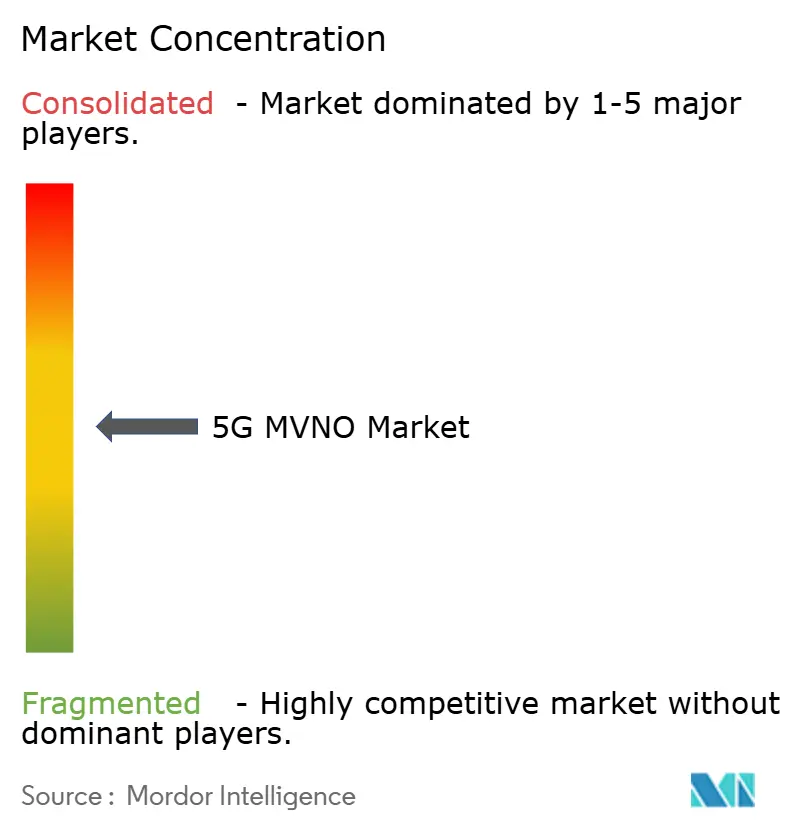

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

5G MVNO Market Analysis by Mordor Intelligence

5G MVNO Market size in 2026 is estimated at USD 13.98 billion, growing from 2025 value of USD 13.30 billion with 2031 projections showing USD 17.89 billion, growing at 5.08% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 295.92 million subscribers in 2025 to 360.52 million subscribers by 2030, at a CAGR of 4.03% during the forecast period (2025-2030). This measured trajectory reflects maturing 5G infrastructure, regulatory tailwinds that mandate wholesale access, and a strategic shift from consumer prepaid plans toward enterprise-grade connectivity. MVNOs are leveraging 5G’s ultra-low latency to sell private-network campus services, software-defined wide-area networking, and fixed-wireless access bundles that bypass legacy wholesale constraints. Asia-Pacific maintains leadership owing to proactive spectrum-sharing rules in Japan and South Korea, while the Middle East and Africa deliver the fastest regional expansion as oil and gas operators and mining groups adopt industrial 5G solutions. Competitive intensity remains moderate because full-stack MVNOs that control billing and service platforms are gaining ground over light resellers, signaling an eventual consolidation toward integrated models. Enterprise subscribers account for over two-thirds of the 5G MVNO market, yet the consumer segment is now growing faster as 5G handsets finally reach mass distribution.

Key Report Takeaways

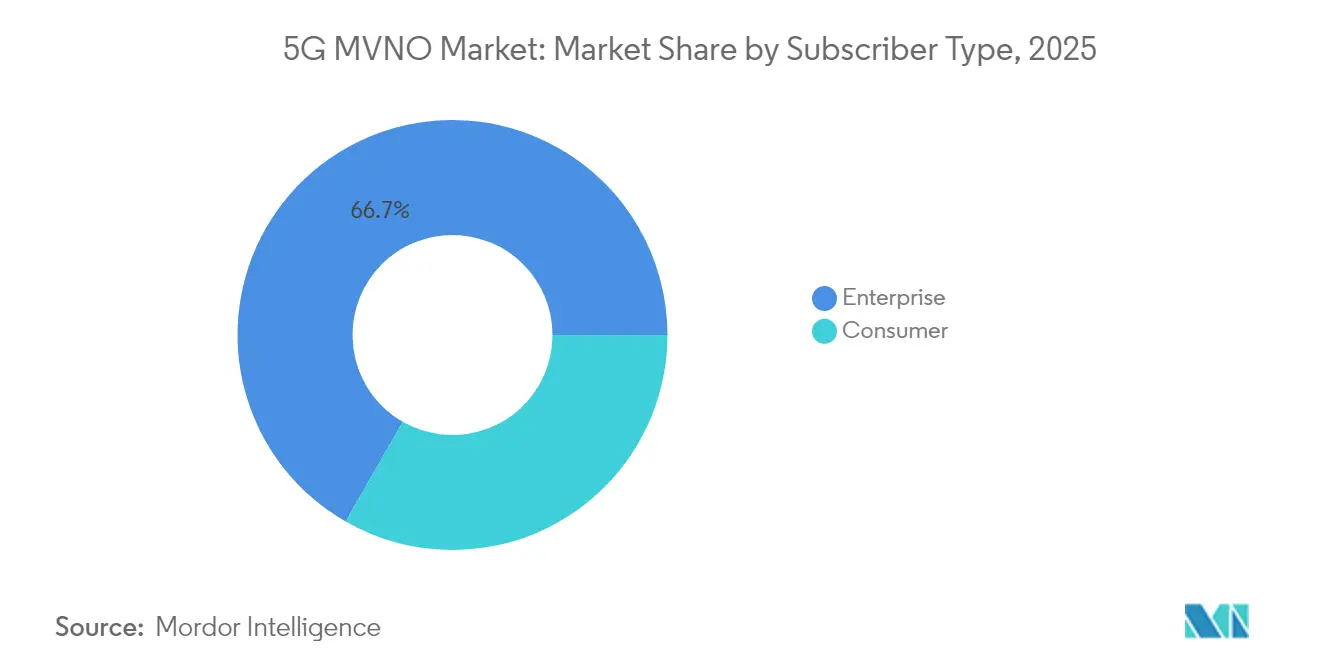

- By subscriber type, enterprise connections held 66.72% of the 5G MVNO market share in 2025, whereas consumer lines are advancing at an 8.52% CAGR through 2031.

- By operational model, resellers/light MVNOs controlled 52.10% revenue share in 2025, but full MVNOs post the highest 16.45% CAGR to 2031.

- By application, B2B data offerings captured 21.60% of the 5G MVNO market size in 2025 and are expanding at a leading 9.48% CAGR to 2031.

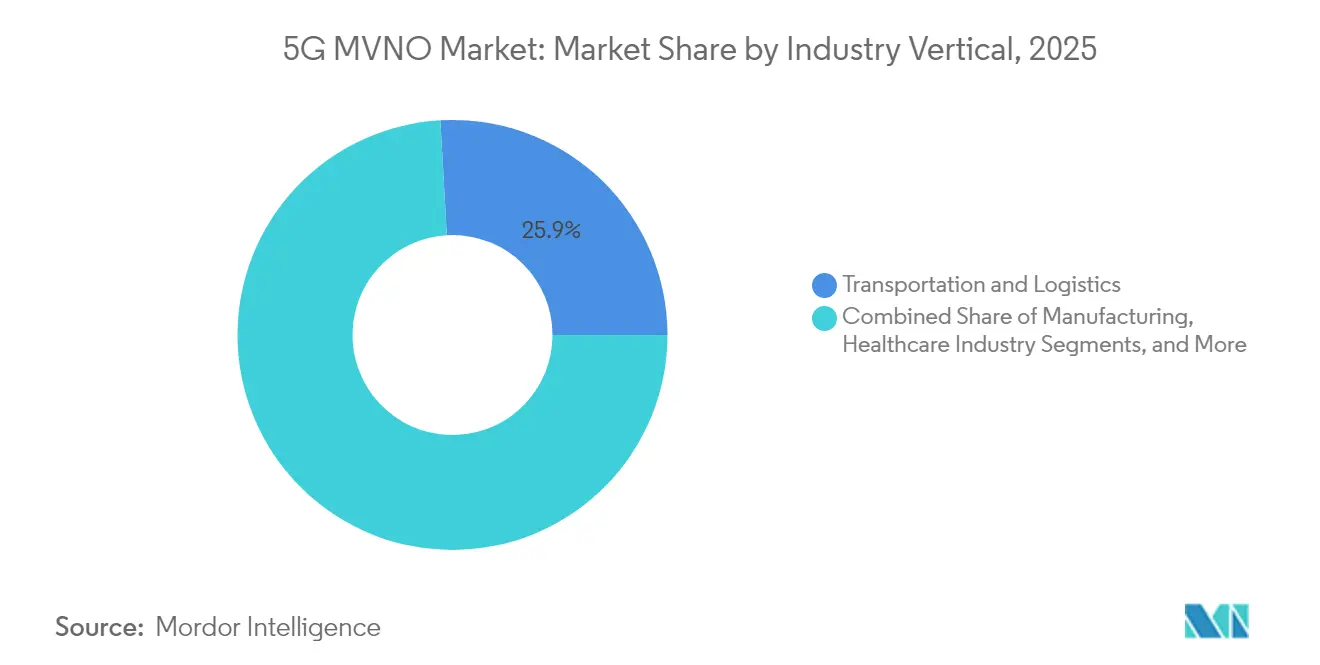

- By industry vertical, transportation and logistics commanded a 25.90% share of the 5G MVNO market size in 2025, while healthcare shows the quickest 9.05% CAGR to 2031.

- By network technology, standalone 5G accounted for 62.10% of the 5G MVNO market size in 2025 and continues to grow at an 8.76% CAGR to 2031.

- By geography, the Asia-Pacific region accounted for 35.55% of the 5G MVNO market size in 2025, while the Middle East and Africa show the quickest 7.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 5G MVNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising enterprise IoT connectivity demand | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Regulatory push for wholesale 5G access | +1.2% | Europe and Asia-Pacific, selective North America markets | Long term (≥ 4 years) |

| eSIM-enabled global roaming propositions | +0.9% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| Cost-efficient B2C data bundles in developed markets | +0.7% | North America and Europe, spillover to developed APAC | Medium term (2-4 years) |

| AI-driven micro-segmentation profitability | +0.6% | Global, led by North America technology adoption | Long term (≥ 4 years) |

| Private-network MVNOs for industrial campuses | +0.5% | North America and Europe industrial corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise IoT Connectivity Demand

Manufacturing, logistics, and healthcare operators are deploying private 5G networks for real-time process control and predictive analytics, creating a USD 2 billion addressable pool for IoT-centric MVNOs. Average revenue per enterprise connection now stands at USD 15-25, roughly double consumer ARPU, because customers pay premiums for guaranteed latency and robust security. Edge-computing tie-ins further lift switching costs, helping MVNOs retain accounts longer than the prepaid handset cycle.[1]CITIC Telecom CPC, “CITIC Telecom Announces 2024 Annual Results,” citictel.com

Regulatory Push for Wholesale 5G Access

Canada’s CRTC, the European Commission, and regulators in South Korea require cost-plus wholesale pricing that lets virtual operators buy 5G capacity without punitive volume commitments. These rules flatten entry barriers, foster price competition, and oblige facilities-based carriers to share network slicing functions, positioning MVNOs to sell differentiated enterprise packages.[2]Global mobile Suppliers Association, “Spectrum Pricing April 2024,” gsacom.com

eSIM-Enabled Global Roaming Propositions

Over-the-air provisioning trims activation windows from days to minutes, letting digital-only brands target business travelers with short-term roaming packs. Forty percent of premium smartphones shipped in 2024 supported eSIM, forming a wide base for multi-country plans that need no physical SIM logistics. Emerging mandates in the European Union that every new handset support eSIM accelerate this trend.

Cost-Efficient B2C Data Bundles in Developed Markets

Digital-first MVNOs market unlimited 5G plans priced 30-50% below incumbent postpaid offers. Multi-month prepaid bundles trim churn, while host-network agreements now allow priority data during congestion, closing the quality gap with tier-one carriers. As a result, family-plan adoption among cost-conscious households is rising, nudging incumbents into defensive price cuts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of affordable 5G-only handsets | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| High 5G wholesale spectrum fees | -1.1% | North America and Europe developed markets | Medium term (2-4 years) |

| National security scrutiny of roaming-only MVNOs | -0.6% | North America and Europe, selective APAC markets | Long term (≥ 4 years) |

| Edge-cloud skill gap within MVNO IT teams | -0.4% | Global, concentrated in smaller MVNOs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Affordable 5G-Only Handsets

Entry-level 5G devices are still priced 40-60% higher than equivalent 4G models, constraining consumer uptake in price-sensitive markets where MVNOs seldom subsidize hardware. Component shortages continue to amplify this hurdle, forcing virtual brands to depend on refurbished stock or BYOD campaigns that slow net-add growth.

High 5G Wholesale Spectrum Fees

Tiered wholesale tariffs charge premiums for standalone features such as network slicing and edge routing, hampering MVNO profitability in segments that rely on aggressive retail pricing. Smaller operators lack the traffic scale to negotiate discounts, leading to slower rollouts of advanced 5G propositions aimed at SMEs and industrial campuses.[3]Global mobile Suppliers Association, “Spectrum Pricing April 2024,” gsacom.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Subscriber Type: Enterprise Dominance Drives Premium Services

The enterprise slice represented 66.72% of the total 5G MVNO market share in 2025 because industrial clients demand secure private networks, IoT connectivity, and service-level agreements. This premium segment underpins predictable cash flows and has spurred NTT Data and Eurofiber to co-launch fully managed private 5G bundles. Consumer lines, however, are projected to outpace enterprises at 8.52% CAGR owing to cheaper entry-level handsets and data bundles. As volumes scale, the consumer slice will remain below the enterprise share but will sustain overall subscriber momentum in the 5G MVNO market.

Enterprise contracts enable MVNOs to offer edge-compute addons, cybersecurity monitoring, and vertical apps that temper margin pressure. Meanwhile, consumer brands rely on digital self-care apps, eSIM onboarding, and multi-month prepaid plans that shrink acquisition costs. This hybrid approach helps operators diversify revenue as handset affordability gradually broadens the consumer base.

By Operational Model: Full Integration Gains Momentum

Reseller and light MVNO structures continued to hold 52.10% revenue in 2025, but the full MVNO cohort is expanding at 16.45% CAGR as control over billing and service orchestration becomes essential for network-slice monetization. Owning a core permits differentiated quality-of-service, faster tariff tweaks, and direct API exposure for enterprise clients, raising switching barriers and justifying premium pricing within the 5G MVNO market.

Service-operator hybrids that outsource the radio link yet keep customer management rank between the two extremes, offering an upgrade bridge for resellers that lack capital for a full core. Consolidation is likely because integrated players negotiate lower wholesale rates and can invest in edge-cloud innovation, creating a structural advantage that erodes the long tail of niche brand resellers.

By Application: B2B Data Services Lead Innovation

B2B data services such as APN, fixed-wireless access, and SD-WAN held 21.60% of the 5G MVNO market size in 2025 and are forecast to rise at a 9.48% CAGR. These bundles embed connectivity deep into enterprise IT stacks, generating multi-year contracts and higher ARPU. Telecom service solutions and machine-to-machine connectivity also benefit from 5G’s latency gains, but their growth trails as enterprises favor turnkey managed offers bundled with analytics.

Private 5G campus networks remain a high-value niche because manufacturing and logistics customers require deterministic latency. Roaming-only packs for digital nomads and media streaming lines for content creators illustrate the growing breadth of the application matrix that MVNOs use to diversify beyond voice and bulk data resale.

By Industry Vertical: Transportation Leads, Healthcare Accelerates

Transportation and logistics commanded a 25.90% share of the 5G MVNO market size in 2025 due to connected-fleet telematics that demand seamless national coverage. Real-time tracking, predictive maintenance, and route optimization rely on always-on 5G links that MVNOs can price at a premium. Healthcare logs the swiftest 9.05% CAGR through 2031 as hospitals roll out tele-ICU services and remote patient monitoring that need ultra-reliable, low-latency connections.

The manufacturing industry shows growth owing to Industry 4.0 robotics and quality inspection use cases that favor standalone 5G slices over Wi-Fi. Retail follows as stores embrace augmented-reality product demos and computer-vision inventory checks. Energy and utilities apply 5G to grid automation, pipeline monitoring, and field-worker safety, rounding out a robust vertical mix that sustains diversification in the 5G MVNO market.

By Network Technology: Standalone 5G Drives Advanced Features

Standalone deployments represented 62.10% of global revenue in 2025 and are expanding at 8.76% CAGR because enterprises require features such as dedicated slicing, ultra-reliable communication, and uplink-heavy throughput. Non-standalone architectures still handle consumer broadband in rural zones where cost sensitivity outweighs advanced feature demand, but carriers are refarming 4G spectrum into full 5G cores to future-proof assets.

The shift unlocks premium wholesale tiers that let MVNOs resell slices with deterministic latency, enabling industrial automation, cloud gaming, and immersive media. Geographic rollouts begin in smart-manufacturing hubs and large metro areas before cascading to suburban markets, ensuring staggered opportunities for MVNO entrants with focused regional strategies.

Geography Analysis

Asia-Pacific claimed 35.55% global revenue in 2025, fueled by mandatory wholesale access in Japan and South Korea and surging enterprise digitization across manufacturing and smart-city projects. China’s enormous factory base drives demand for private 5G, while India’s prepaid boom broadens the consumer segment with digital-only plans and rapid eSIM uptake. Cross-border roaming hubs in the Greater Bay Area let MVNOs provide unified service portals for multinational enterprises.

The Middle East and Africa are the fastest-growing territories at a 7.42% CAGR through 2031. Gulf energy giants deploy private networks for upstream operations, and regulators in Nigeria and South Africa now license multiple MVNOs to widen competition. Falling handset prices, government cloud initiatives, and new subsea cables buoy the 5G MVNO market outlook across the region.

North America and Europe exhibit stable but slower growth. The United States benefits from T-Mobile’s open-MVNO stance and FCC pressure for wholesale parity, whereas the Canadian CRTC mandates lifted entry prospects in 2025. The European Union’s spectrum-sharing directives enable newcomers to integrate slicing and edge computing in cross-border enterprise deals, elevating differentiation beyond basic mobile broadband.

Competitive Landscape

The 5G MVNO market is moderately fragmented. Full-stack operators that own a virtualized core are scaling fastest because they offer bespoke network slices, APIs, and analytics dashboards for Industry 4.0. T-Mobile folded Mint Mobile into its prepaid arm and Verizon absorbed TracFone to capture economies of scale. Digital-native brands harness AI for micro-segmentation and eSIM for instant activation, outmaneuvering legacy resellers that depend on physical retail.

Edge-cloud specialization underpins vertical plays. Healthcare-focused MVNOs tout HIPAA-grade security, while logistics-centric entrants bundle fleet telematics and SD-WAN under one invoice. Platform-as-a-Service vendors now furnish turnkey MVNO kits that compress launch timelines, fostering a pipeline of fintech, media, and IoT specialists keen to monetize connectivity as an adjunct to their core services.

5G MVNO Industry Leaders

TracFone Wireless, Inc. (Verizon Value, Inc.)

Lycamobile USA Inc.

Tesco Mobile Ltd

Lebara Limited

Giffgaff Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NTT Data and Eurofiber launched private 5G services for European manufacturers and logistics hubs.

- March 2025: CITIC Telecom CPC surpassed 760,000 5G users in Macau, reaching 98.4% penetration.

- December 2024: Telstra bought Boost Mobile Australia for USD 57 million to fortify its prepaid footprint.

- September 2024: Sky Mobile entered Ireland with unlimited data plans anchored by Comcast content bundles.

- September 2024: Vodacom unveiled MVNE services in South Africa, opening its 5G network to third-party brands.

- August 2024: Waterland Private Equity acquired Lebara Group to fund pan-European expansion.

Global 5G MVNO Market Report Scope

An MVNO (mobile virtual network operator) offers wireless communications services but does not control the wireless network infrastructure it uses to serve its clients. MVNOs purchase network capacity from network providers to enable their services. They utilize the base carriers' already-existing mobile infrastructure while providing data plans that are less expensive or more flexible.

The 5G MVNO Market is Segmented by Subscriber (Enterprise and Consumer), by Application (M2M Connectivity, Telecom Services Solutions, Bundled Solutions, Retail Solutions, Roaming Solutions, Discount Solutions, Media and Entertainment Solutions, and B2B Data Solutions), and by geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Enterprise |

| Consumer |

| Resellers/Light/ Brand MVNO |

| Service Operator |

| Full MVNO |

| M2M/IoT Connectivity |

| Telecom Service Solutions |

| Bundled Quad-play Solutions |

| Retail Discount Solutions |

| Media and Entertainment |

| Roaming-Only Solutions |

| B2B Data (APN, FWA, SD-WAN) |

| Private-5G Campus Solutions |

| Manufacturing |

| Healthcare |

| Transportation and Logistics |

| Retail and eCommerce |

| Energy and Utilities |

| Standalone 5G |

| Non-Standalone 5G |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Israel | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Subscriber Type | Enterprise | ||

| Consumer | |||

| By Operational Model | Resellers/Light/ Brand MVNO | ||

| Service Operator | |||

| Full MVNO | |||

| By Application | M2M/IoT Connectivity | ||

| Telecom Service Solutions | |||

| Bundled Quad-play Solutions | |||

| Retail Discount Solutions | |||

| Media and Entertainment | |||

| Roaming-Only Solutions | |||

| B2B Data (APN, FWA, SD-WAN) | |||

| Private-5G Campus Solutions | |||

| By Industry Vertical | Manufacturing | ||

| Healthcare | |||

| Transportation and Logistics | |||

| Retail and eCommerce | |||

| Energy and Utilities | |||

| By Network Technology | Standalone 5G | ||

| Non-Standalone 5G | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Indonesia | |||

| Malaysia | |||

| Thailand | |||

| Vietnam | |||

| Philippines | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Israel | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the 5G MVNO space in 2026?

The 5g mvno market size reached USD 13.98 billion during 2026.

What is the expected growth rate through 2031?

Market revenue is projected to rise at a 5.08% CAGR, reaching USD 17.89 billion by 2031.

Which region holds the largest share?

Asia-Pacific leads with 35.55% market share thanks to supportive wholesale regulations and early 5G rollouts.

Which subscriber type generates the most revenue?

Enterprise lines account for 66.72% of global revenue because private 5G and IoT services carry higher ARPU.

What operational model is growing fastest?

Full MVNOs post a 16.45% CAGR as ownership of the core network enables differentiated enterprise services.

Which industry vertical is expanding the quickest?

Healthcare connections are advancing at 9.05% CAGR owing to telemedicine and remote monitoring needs.

Page last updated on: