Norway Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

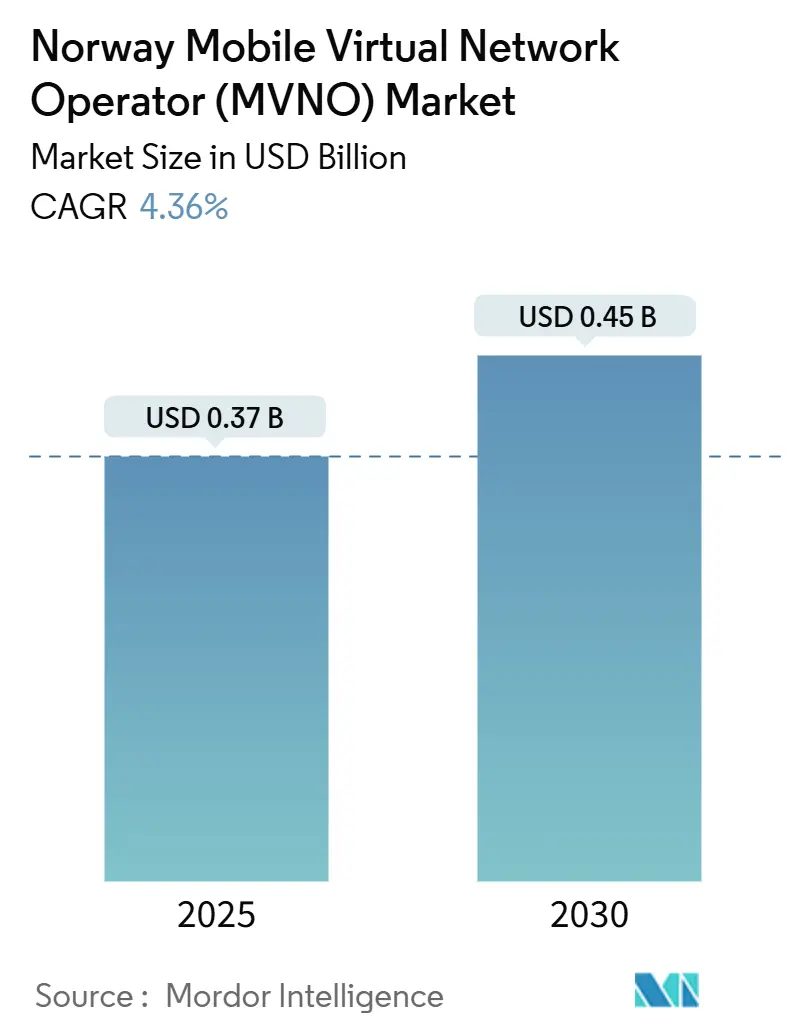

| Market Size (2025) | USD 0.37 Billion |

| Market Size (2030) | USD 0.45 Billion |

| Growth Rate (2025 - 2030) | 4.36% CAGR |

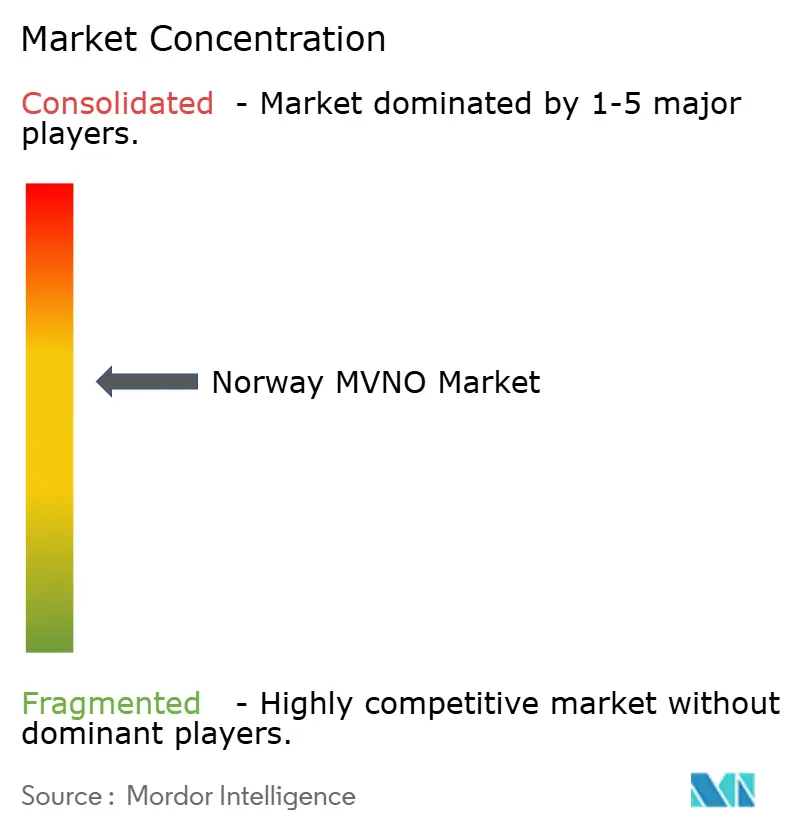

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Norway Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Norway Mobile Virtual Network Operator Market size is estimated at USD 0.37 billion in 2025, and is expected to reach USD 0.45 billion by 2030, at a CAGR of 4.36% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 0.69 million Subscribers in 2025 to 0.82 million Subscribers by 2030, at a CAGR of 3.39% during the forecast period (2025-2030).

Robust fixed-mobile broadband infrastructure, near-universal 4G coverage, and a 99% 5G population footprint provide a stable platform for new virtual operators. Wholesale access rules issued by the Norwegian Communications Authority (NKOM) temper the pricing power of the three host MNOs, yet their oligopoly still weighs on margins. Energy retailers bundling mobile connections to reduce churn, accelerated eSIM uptake, and a sharp rise in machine-to-machine lines are shaping the competitive canvas. The Norway MVNO market, therefore, pivots from price-only competition toward application-driven differentiation, especially in enterprise IoT and satellite-terrestrial hybrid services [1]Norwegian Communications Authority, “Final Decision on Weighted Average Cost of Capital for 2025,” nkom.no .

Key Report Takeaways

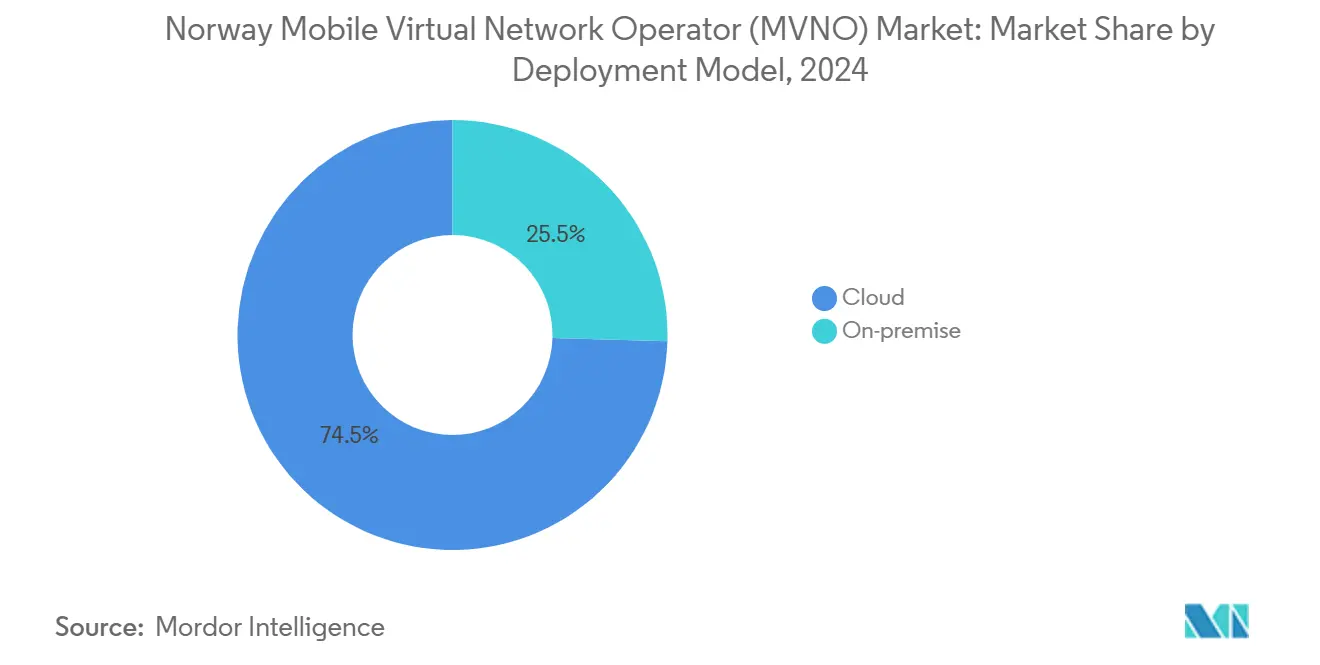

- By deployment model, cloud infrastructure held 74.54% of the Norway MVNO market share in 2024 and is growing at a 7.69% CAGR to 2030.

- By operational mode, resellers/light/ brand MVNOs held 59.29% of the Norway MVNO market share in 2024, while full MVNOs expanded at 16.28% CAGR through 2030.

- By subscriber type, consumer accounts for 81.86% of the Norway MVNO market size in 2024, while IoT connectivity posts a 24.10% CAGR to 2030.

- By application, other application segments held 43.91% of the Norway MVNO market share in 2024, while cellular M2M commands a 23.31% CAGR through 2030, outpacing discount and business use-cases.

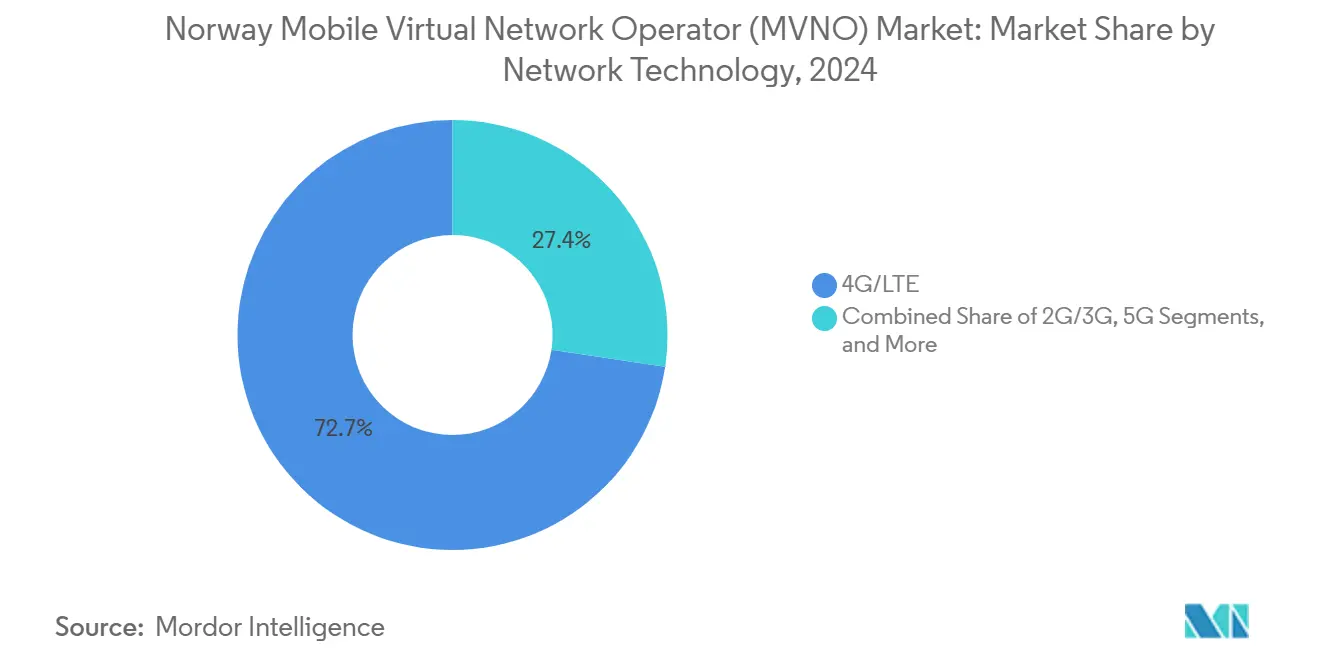

- By network technology, 4G/LTE retains 72.65% share in 2024; satellite/NTN lines are set to soar at an 83.18% CAGR.

- By distribution channel, online/digital-only services account for 57.28% of the Norway MVNO market share and are advancing at a 7.50% CAGR.

Norway Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive consumer segment seeking lower ARPU plans | +0.8% | National (urban hubs) | Short term (≤ 2 years) |

| EU/EEA wholesale-access regulation strengthens MVNO bargaining power | +0.6% | National | Medium term (2-4 years) |

| 98% 4G and 99% 5G coverage enables data-centric MVNO plays | +0.7% | National and rural | Medium term (2-4 years) |

| Energy and retail brands bundling mobile to cut churn | +0.5% | National | Short term (≤ 2 years) |

| Rapid eSIM uptake supports cloud-native, digital-only launches | +0.4% | National | Long term (≥ 4 years) |

| Growing enterprise/IoT demand for tailored SLAs | +0.9% | Industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-sensitive consumer segment seeking lower ARPU plans

Elevated living costs and a cautious spending mindset amplify demand for lean, voice-and-data bundles priced below incumbent offerings. Telenor’s Q1 2025 revenue grew 3.9% on higher ARPU even as subscriber numbers dipped, leaving a vacuum for MVNOs that can monetize price-elastic users through simple, commitment-free plans [2]Investing.com Transcript Team, “Telenor Q1 2025 Earnings Call,” investing.com. Light MVNOs exploit this gap with outsourced core services and minimal overhead. Digital onboarding drives down acquisition cost, but sustained performance hinges on responsive customer support and transparent billing. Operators unable to pair low prices with service reliability risk rapid churn in Norway’s quality-focused consumer base. Complementary energy and loyalty-card bundles further widen the appeal of low-ARPU propositions.

EU/EEA wholesale-access regulation strengthens MVNO bargaining power

Pan-European frameworks mandate fair, cost-oriented wholesale terms and roaming parity, reducing input cost volatility for Norwegian virtual operators. The Roam-Like-at-Home regime alone produced USD 2.4 billion in consumer surplus across the EU, underscoring the economic lift generated by regulatory intervention [3]Martin Quinn et al., “The Welfare Effects of Mobile Internet Access,” Economic Journal, academic.oup.com. NKOM aligns local guidelines with Brussels, improving rate transparency and dispute resolution. Predictable wholesale rates unlock long-range planning for new entrants and support specialty roaming products for expatriates and business travelers. Alignment with EU data-protection statutes also raises privacy compliance costs, creating a barrier to entry that entrenches capable MVNOs.

98% 4G and 99% 5G coverage enables data-centric MVNO plays

Norway’s rapid 5G rollout, Telia reached 99% population coverage by December 2024, giving virtual operators a nationwide canvas for advanced services. Seamless high-bandwidth availability allows MVNOs to pitch high-definition streaming, cloud gaming, and industrial IoT without negotiating regional roaming pacts. Rural reach, critical for maritime, aquaculture, and forestry applications, positions 4G/5G as a practical backbone for nationwide sensor grids. With performance now table-stakes, MVNO competition shifts toward tailored software layers, analytics, and verticalized solutions.

Growing enterprise/IoT connectivity demand for tailored SLAs

Industrial digitalization fuels persistent double-digit growth in cellular M2M lines. Norwegian manufacturers, offshore operators, and logistics firms seek connectivity guarantees that match operational technology uptime targets. MVNOs with full-core control can slice networks, enforce device-level security, and craft bespoke tariffing, aligning cost with usage profiles. Nordic Semiconductor’s NTN collaborations highlight multi-orbit satellite integration as a differentiator for nationwide asset visibility in harsh terrain [4]Nordic Semiconductor, “What Is NTN,” nordicsemi.com . MVNOs that master terrestrial–satellite orchestration stand to monetize premium SLAs commanding higher ARPU and lower churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Only three host MNOs keep wholesale rates structurally high | –1.2% | National | Medium term (2-4 years) |

| Limited spectrum ownership blocks technical differentiation for full MVNOs | –0.8% | National | Long term (≥ 4 years) |

| High brand loyalty to Telenor and Telia raises customer-acquisition cost | –0.6% | National | Short term (≤ 2 years) |

| 3GPP NTN / LEO satellite may divert rural subscribers | –0.4% | Rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Only three host MNOs keep wholesale rates structurally high

Telenor, Telia, and Ice collectively determine capacity pricing, leaving MVNOs little leverage despite formal cost-orientation rules. NKOM’s 2025 weighted average cost of capital recommendation of 5.58% feeds into wholesale benchmarks, but incumbents still bundle volume and duration conditions that tighten MVNO margins. Price rigidity particularly constrains full-core operators, which need multi-layer access to innovate. The limited pool of host networks also reduces MVNO bargaining chips, such as multi-host redundancy, thereby tempering retail price competition.

High brand loyalty to Telenor and Telia raises customer-acquisition cost

MVNOs must deploy aggressive marketing, discounting, and bundled perks to lure subscribers, inflating cost-per-gross-add. Stickiness is acute in the SME and corporate tiers where service disruption translates to revenue loss. High loyalty restricts MVNO addressable volume to price-sensitive or niche users, thereby slowing scale economies and lengthening payback periods on core investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Dominates Scalability Needs

Cloud-hosted cores captured 74.54% of the Norway MVNO market share in 2024 as operators prioritized elasticity over capital-intensive on-premise platforms. This dominance stems from the ability to spin up network functions on demand, manage peaks seamlessly, and shorten product launch cycles. On-premise deployments persist in finance and public-safety verticals that require full data residency. Yet cloud ecosystems now embed carrier-grade encryption and local compute zones, lowering sovereignty concerns.

Widespread eSIM adoption further turbocharges cloud-native models by removing physical logistics and enabling instant activation. Energy conglomerates entering telecoms leverage shared IT talent and centralized CRM databases to integrate usage analytics and cross-sell offers. Against this backdrop, the Norway MVNO market size for cloud deployments is projected to expand in lockstep with a 7.69% CAGR through 2030, reinforcing the architecture as the default for greenfield launches.

By Operational Mode: Full MVNOs Accelerate Service Innovation

Reseller and light MVNOs held a 59.29% share in 2024 due to their low-risk, marketing-centric design. However, full operators post a 16.28% CAGR because enterprises demand network slicing, private APNs, and granular policy control that reseller models cannot supply. The Norway MVNO industry thus sees a gradual shift from pure price arbitrage toward technology-rich value propositions.

Full-core ownership unlocks bespoke roaming, quality-of-service tiers, and API exposure, enabling vertical applications in maritime telemetry and offshore energy. The incremental investment in PCRF, HSS, and SBC infrastructure is offset by high-margin corporate contracts and lower wholesale volume costs through traffic steering. Regulatory compliance burdens remain heavier, but experienced entrants view this as a moat rather than a barrier.

By Subscriber Type: IoT Lines Outpace Human Connections

Consumer accounts for 81.86% of revenue today, yet IoT endpoints generate the steepest growth curve at 24.10% CAGR, reflecting Norway’s automation push across aquaculture, shipping, and renewable energy. Enterprise subscriptions command superior ARPU but require robust field support and multi-site contracts.

The Norway MVNO market size attached to IoT is expected to multiply as government programs digitize public services and industry consortia adopt sensor fleets. MVNOs capable of zero-touch provisioning and secure firmware updates will capture a disproportionate share. Consumer growth stabilizes as penetration nears saturation, making device-centric revenue the long-term expansion frontier.

By Application: M2M Drives Portfolio Diversification

Other applications collectively held 43.91% in 2024, a catch-all encompassing mobile broadband for refugees, short-term tourist SIMs, and loyalty perks. Yet cellular M2M climbs the fastest at 23.31% CAGR, echoing cross-sector automation trends. Discount packages remain the volume anchor, retaining price-led segments and sustaining traffic to obtain wholesale tier rebates.

The shift from generic data buckets to narrow-band IoT, low-latency video links, and mission-critical telemetry expands average revenue per connection. MVNOs that invest in analytics, device management, and vertical compliance can up-sell lifecycle services, monetizing beyond the data pipe. The Norway MVNO market, therefore, evolves from uniform mass plans to a mosaic of specialized offerings.

By Network Technology: Satellite/NTN Becomes Coverage Extender

4G/LTE still accounts for 72.65% of active SIMs, but 5G upgrades and imminent 2G shutdowns accelerate migration. The real disruption lies in satellite/NTN lines set to post an 83.18% CAGR, bridging Norway’s mountainous terrain and offshore zones.

Partnerships between terrestrial carriers and LEO constellations deliver blended coverage and ultra-high availability. MVNOs that certify multi-orbit modules can offer “connect-anywhere” SLAs, differentiating from pure terrestrial rivals. The Norway MVNO market size for hybrid services will likely spike as maritime, forestry, and emergency response agencies standardize on NTN-capable devices.

By Distribution Channel: Digital-Only Retail Reshapes Acquisition

Online-first activation seized a 57.28% share in 2024 as app-centric journeys resonated with Norway’s digitally mature citizens. Self-care portals, chatbots, and ID-verified eSIM downloads slash onboarding friction and cut SIM logistics costs. Traditional shops now focus on device financing, upselling accessories, and handling complex enterprise queries.

Operator web stores integrate with energy billing systems and loyalty apps, enabling bundled discounts that raise stickiness. The channel’s 7.50% CAGR reflects a virtuous cycle: lower cost-to-serve frees budget for UX refinement, which in turn lifts conversion rates. Over time, the Norway MVNO market will see brick-and-mortar presence narrow to demonstration hubs in major cities while rural customers migrate to digital workflows.

Geography Analysis

Norway’s compact yet topographically diverse territory offers dense urban clusters along the southern belt and sparse settlements in the north. Telia’s 99% 5G coverage milestone in 2024 ensures homogenous high-speed service for urban MVNO customers, underpinning premium unlimited data packages. Rural municipalities still rely on 4G but benefit from growing satellite backhaul, making IoT deployments viable in fisheries and agriculture.

The Oslofjord corridor hosts most enterprise headquarters, concentrating high-value B2B contracts. Here, full MVNOs pitch managed connectivity with stringent SLAs, leveraging cloud cores hosted in local green data centers powered by hydroelectric energy. Northern counties such as Troms og Finnmark demand resilient NTN-enabled services for maritime safety and resource extraction. This geographic dichotomy propels the Norway MVNO market toward dual-technology portfolios that mix terrestrial 5G and satellite links.

Regionally, Norway’s EU/EEA alignment enables frictionless roaming across neighboring Nordic states, supporting MVNO expansion into Sweden and Denmark via multi-country SIMs. Government digitalization roadmaps targeting 2030 further stimulate demand for secure connectivity in public services, thereby anchoring long-range growth.

Competitive Landscape

Twelve virtual operators vie for a share, positioning the Norway MVNO market as semi-consolidated. Fjordkraft Mobil leads through bundled energy contracts, achieving 115,000 subscribers after migrating to Telia’s network. Other contenders include Happybytes in youth segments and Lyca Mobile in expatriate calling.

Digital-native challengers differentiate via subscription apps, data rollover, and straightforward cancellation. Energy retailers exploit meter-reading know-how and CRM overlap to cross-sell mobile, cutting churn in liberalized power markets. IoT-centric entrants target fleet telematics and smart-city lighting, underscoring a pivot toward enterprise specialization.

Wholesale leverage remains pivotal: operators negotiating multi-host frameworks secure redundancy and price relief. Compliance proficiency with GDPR and national ID rules further filters newcomers. Cloud-core automation, analytics, and security orchestration emerge as decisive capabilities in a market where coverage parity has eroded traditional service gaps.

Norway Mobile Virtual Network Operator (MVNO) Industry Leaders

Fjordkraft Mobil AS

OneCall (Telia Norge AS)

Happybytes AS

Mycall (Telia Norge AS)

Chilimobil AS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Telia reached 99% national 5G coverage, finishing a four-year roll-out.

- November 2024: StalkIT won Norway’s largest NB-IoT contract with Telia for waste-container tracking.

- May 2024: Ice announced ten new retail stores nationwide to improve brand visibility.

Norway Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Norway MVNO market in 2025?

The Norway MVNO market size is USD 0.37 billion in 2025.

What CAGR is forecast for Norwegian virtual operators to 2030?

Aggregate revenue is expected to grow at a 4.36% CAGR between 2025 and 2030.

Which deployment model leads the segment rankings?

Cloud cores dominate with 74.54% revenue share and a 7.69% CAGR through 2030.

Which subscriber group is expanding fastest?

IoT connections show the highest growth, advancing at a 24.10% CAGR to 2030.

How will satellite technology influence Norwegian MVNOs?

Satellite/NTN access is projected to grow at an 83.18% CAGR, enabling coverage-extending services for remote industries.

Page last updated on: