Intelligent Battery Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

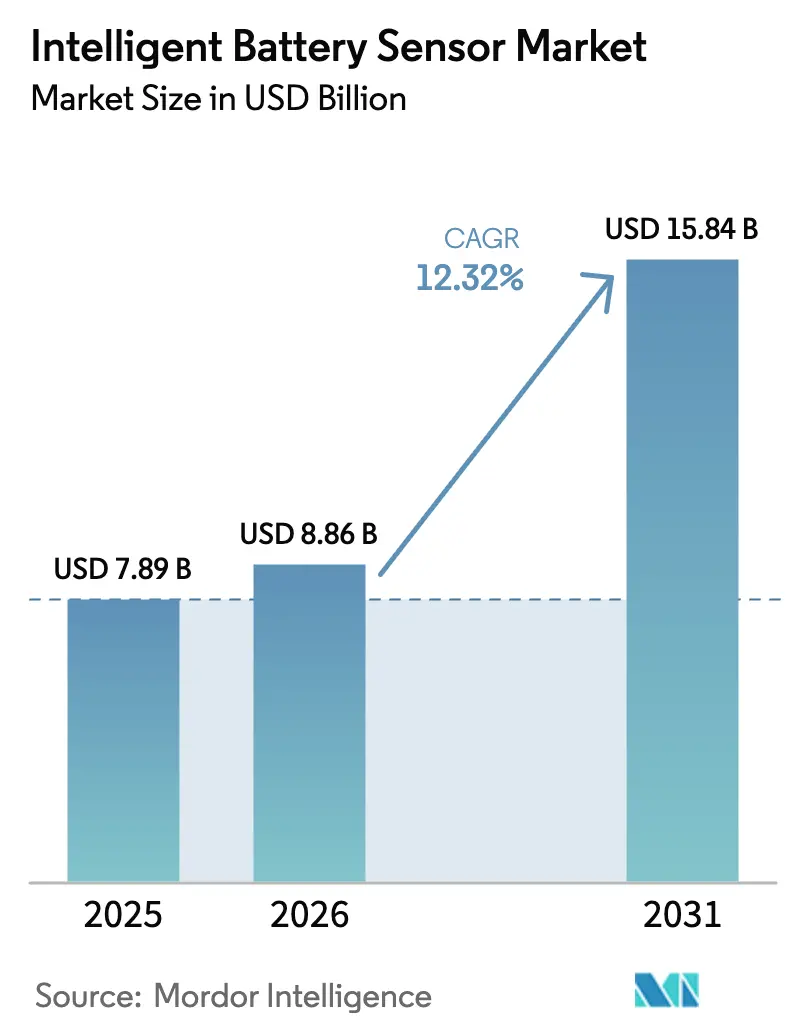

| Market Size (2026) | USD 8.86 Billion |

| Market Size (2031) | USD 15.84 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Battery Sensor Market Analysis by Mordor Intelligence

The Intelligent Battery Sensor Market size was valued at USD 7.89 billion in 2025 and estimated to grow from USD 8.86 billion in 2026 to reach USD 15.84 billion by 2031, at a CAGR of 12.32% during the forecast period (2026-2031). This acceleration is anchored in regulatory mandates for on-board diagnostics, rapid vehicle electrification, and OEM moves toward software-defined platforms that treat sensors as high-value data nodes. Increasing integration of AI-enabled edge analytics allows real-time state-of-health estimation, while cost reductions in mixed-signal ASICs broaden adoption across vehicle classes. Demand growth also stems from grid-scale storage owners who seek predictive maintenance to control lifecycle costs, and from aging vehicle fleets where retrofit start-stop systems extend useful life. Asia-Pacific remains the production hub due to tight vertical supply chains for semiconductors and battery packs, enabling lower unit costs and faster design iterations.

Key Report Takeaways

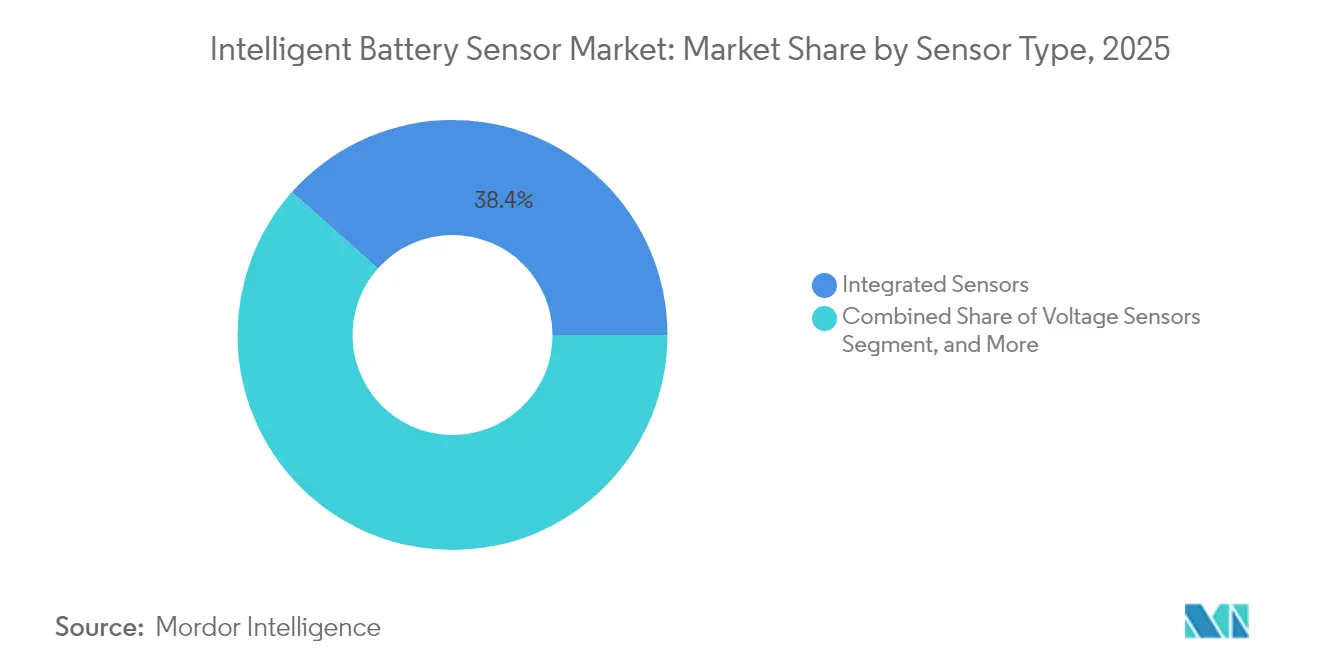

- By sensor type, integrated sensors led with 38.42% revenue share in 2025 while voltage sensors are advancing at 13.05% CAGR through 2031.

- By vehicle type, passenger vehicles held 47.05% of the intelligent battery sensor market share in 2025; electric vehicles are expanding at 13.62% CAGR to 2031.

- By sales channel, OEM installations commanded 71.05% share in 2025, whereas aftermarket sales are projected to grow at 12.74% CAGR.

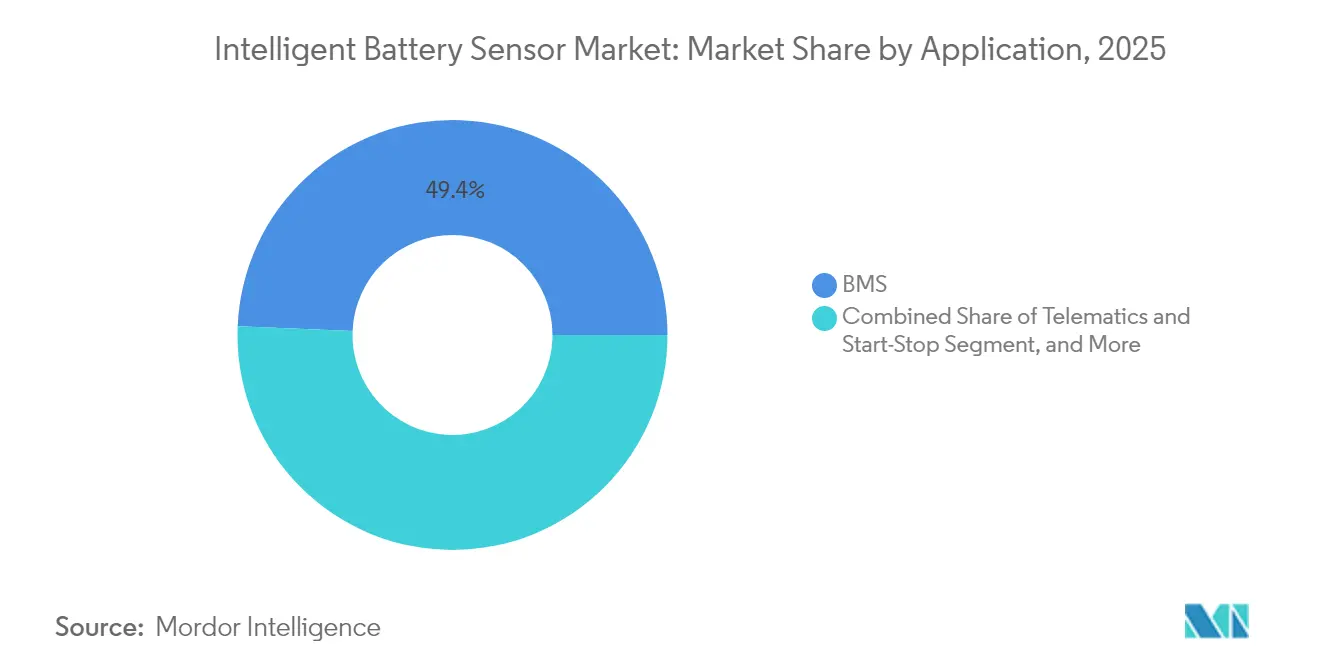

- By application, battery management systems accounted for 49.35% share of the intelligent battery sensor market size in 2025, and telematics plus start-stop systems are forecast to rise at 14.15% CAGR.

- By end user, automotive manufacturers dominated with 50.40% share in 2025, while the renewable energy sector is predicted to progress at 13.98% CAGR.

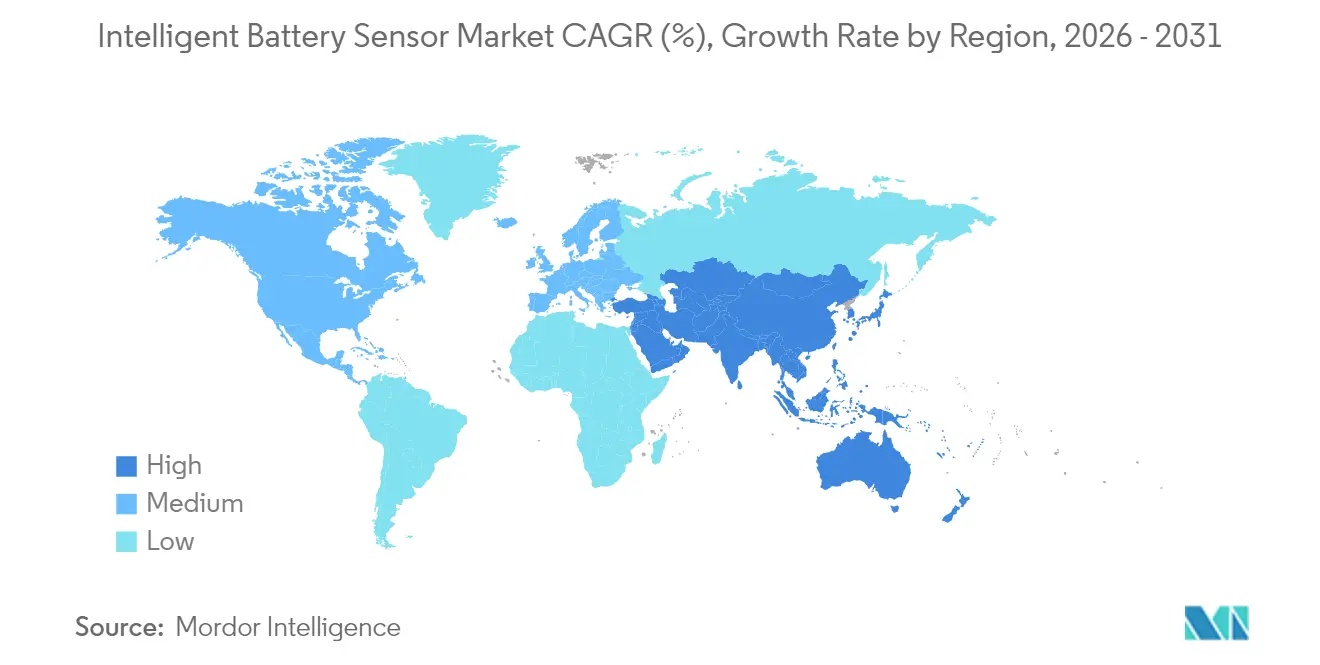

- By geography, Asia-Pacific dominated with 43.62% revenue share in 2025 and is projected to expand at a 12.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intelligent Battery Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates for on-board battery diagnostics | +2.80% | Global, with EU and North America leading | Short term (≤ 2 years) |

| Rapid electrification across passenger and commercial fleets | +3.20% | Global, APAC core with spillover to Europe and North America | Medium term (2-4 years) |

| OEM transition to software-defined vehicles and zonal EE architectures | +2.10% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Drop-in retrofit demand for start-stop and micro-hybrid systems | +1.40% | Europe and North America, emerging in APAC | Short term (≤ 2 years) |

| AI-enabled predictive maintenance business models (fleet and ESS) | +1.90% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) |

| Circular-economy digital-passport compliance requirements | +1.10% | EU primary, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates for On-Board Battery Diagnostics

Safety and emissions regulations are pushing OEMs to embed sophisticated sensors that verify battery health in real time. Euro 7 rules effective 2025 oblige hybrid and electric vehicles sold in Europe to report depth-of-discharge and thermal events, compelling automakers to specify higher-accuracy voltage and current measurement components.[1]European Commission, “Commission Proposes New Euro 7 Standards to Reduce Pollutant Emissions from Vehicles and Improve Air Quality,” EUROPA.EU Parallel UNECE cybersecurity rules demand encrypted data links, driving up content per vehicle and favouring suppliers with ISO 21434-compliant firmware. Certified platforms thus gain a cost-of-entry advantage, especially when stationary storage systems in Europe and North America adopt the same diagnostic language for grid interconnection.

Rapid Electrification Across Passenger and Commercial Fleets

Mass electrification amplifies sensor demand because lithium-ion chemistries require tight thermal and current control to maximize life. Commercial fleets add urgency; each unplanned truck outage may cost USD 500 per day in idle assets, encouraging operators to adopt predictive maintenance dashboards powered by live impedance data.[2]Continental AG, “Continental Automotive Technologies: Electrification and Digitalization Drive Growth,” CONTINENTAL.COM China’s subsidy programs and Japan’s semiconductor ecosystem jointly accelerate installations as regional manufacturers bundle sensors in every traction battery pack.

OEM Transition to Software-Defined Vehicles and Zonal EE Architectures

Automakers are collapsing hundreds of electronic control units into a handful of domain controllers that require high-bandwidth, low-latency sensor feeds. Battery monitors now send raw waveforms for on-board machine-learning models that adjust cooling loops in milliseconds, extending pack life by up to 20%.[3]Chris Clonts, “New Marelli BMS Uses Electrochemical Impedance Spectroscopy,” SAE.ORG Suppliers offering edge-analytics features unlock recurring revenue via software updates, transforming sensors from commodity items into upgradable assets.

AI-Enabled Predictive Maintenance Business Models

Fleet owners and energy-storage operators increasingly pay for performance guarantees based on cloud analytics that ingest continuous cell-level data. Electrochemical impedance spectroscopy embedded in new sensor ASICs allows algorithms to predict capacity fade weeks ahead, reducing warranty claims and shaving 15% off lifecycle costs.[4]MarkLines, “ACCURE Battery Intelligence Raises New Investment,” MARKLINES.COM Digital twins that mirror every pack in operation underpin emerging battery-as-a-service contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-term EV program delays and inventory corrections | -1.80% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Commodity-price volatility in shunt metal and ASIC supply chain | -1.20% | Global, with APAC manufacturing concentration | Medium term (2-4 years) |

| Lack of global data-interoperability standards for battery health | -0.90% | Global, with fragmentation across regions | Long term (≥ 4 years) |

| Cyber-security certification costs for ISO 21434 and WP.29 | -0.70% | Global, particularly Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short-Term EV Program Delays and Inventory Corrections

Automakers have postponed several 2025 EV launches, slowing sensor orders as production targets are trimmed. Because most intelligent battery sensor contracts follow just-in-time delivery, even minor schedule shifts ripple down the supply chain, leaving smaller suppliers with idle capacity and pricing pressure.

Commodity-Price Volatility in Shunt Metal and ASIC Supply Chain

Copper shunt and semiconductor substrate prices can swing 20-30% within a quarter, squeezing margins since auto OEMs expect annual cost downs. Smaller sensor vendors without multi-year hedging contracts are most exposed, sometimes surrendering share to tier-1 suppliers with stronger procurement leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Integrated Solutions Remain Dominant

Integrated sensors held 38.42% of the intelligent battery sensor market in 2025 because OEM engineers favour single-package devices that combine current, voltage, and temperature measurement to simplify harness design and cut installation labour. These modules have also evolved to include built-in edge processors that run anomaly-detection algorithms, enabling faster fault isolation during drive cycles. Voltage sensors are the fastest risers at 13.05% CAGR, propelled by 800 V vehicle architectures that demand millivolt-level precision for each cell. Current sensors continue to sell briskly into legacy 12 V systems, while advanced temperature probes see renewed demand in packs designed for ultra-fast charging.

Functional integration is also a cost-reduction pathway. Suppliers such as Marelli now embed electrochemical impedance spectroscopy in integrated modules, creating a premium tier that assesses state-of-health without intrusive test equipment. This capability positions integrated sensors as strategic components in battery-as-a-service offerings where uptime guarantees hinge on accurate degradation forecasts.

By Vehicle Type: Commercial Electrification Ups the Stakes

Passenger vehicles retained 47.05% share in 2025 due to sheer unit volume, yet electric vehicles will register a brisk 13.62% CAGR through 2031 as OEM lineups pivot toward zero-emission drivetrains. Commercial fleets, from urban delivery vans to city buses, present higher content per vehicle because demanding duty cycles require redundant current and temperature measurements at module and pack levels.

In commercial settings, intelligent battery sensor market size for heavy trucks is poised to expand sharply as operators chase total cost of ownership savings via predictive maintenance. Vendors like LEM now offer compact, ASIL-B compliant modules that bolt directly to busbars, easing packaging constraints in tight chassis envelopes. Meanwhile, hybrid-electric and plug-in hybrid platforms continue to provide a transitional revenue base, ensuring diversified demand across drivetrain categories.

By Sales Channel: Aftermarket Emerges as a Growth Engine

OEM installations dominated with 71.05% share in 2025 because factory-fit sensors satisfy warranty rules and reduce recall risk. The aftermarket, however, will climb at 12.74% CAGR as owners retrofit start-stop or micro-hybrid functions into aging vehicles to meet local emissions ordinances. Wireless, plug-and-play sensor kits shorten installation to less than one hour, minimizing downtime for commercial fleets.

Subscription-based diagnostics services built on aftermarket sensors create recurring revenue, an attractive model especially for fleet maintenance providers. As unit costs fall, the intelligent battery sensor market is likely to witness rising retrofit penetration in developing economies where average fleet age exceeds 11 years and full vehicle replacement remains cost prohibitive.

By Application: Telematics Integration Gains Pace

Battery management systems accounted for 49.35% of 2025 revenue, cementing their role as the default placement for sensors delivering pack protection, cell balancing, and performance optimization. Yet telematics and start-stop systems will surge at 14.15% CAGR because sensor data combined with GPS and usage analytics supports remote prognostics, energy-aware route planning, and dynamic warranty pricing.

Grid-scale renewable storage sites represent another emerging application cluster. These installations require low-maintenance, high-accuracy sensors that deliver continuous voltage and impedance data to asset-management dashboards. Vendors leveraging cloud APIs to push real-time state-of-health readings into enterprise resource-planning software gain an early-mover advantage in the intelligent battery sensor industry.

By End User: Renewable Energy Sector Scales Fast

Automotive manufacturers generated 50.40% of demand in 2025 as sensor supply naturally aligns with vehicle output. Renewable-energy operators, however, will expand purchases at 13.98% CAGR because battery replacement can account for up to 60% of lifetime plant costs. Accurate, real-time degradation metrics help optimize dispatch schedules and protect revenue streams tied to performance contracts.

Telecommunications providers also increase spend as 5G densification raises backup-power complexity. High-cycle lithium-ion racks deployed at cell towers need temperature and current sensing that outperforms legacy lead-acid systems, creating another vertical for suppliers with harsh-environment certification.

Geography Analysis

Asia-Pacific led the intelligent battery sensor market with 43.62% share in 2025 and is forecast to grow at 12.61% CAGR through 2031. Chinese EV mandates, local semiconductor fabs, and vertically integrated battery producers compress development cycles, allowing rapid sensor iteration for each new cell chemistry. Japanese and South Korean firms contribute high-accuracy ASICs, reinforcing the region’s leadership.

North America follows, buoyed by Inflation Reduction Act incentives that spur domestic battery-pack assembly and demand stringent diagnostics for federal safety reporting. Suppliers offering ISO 21434-compliant encryption gain preference for government-fleet tenders. Canada’s push into raw material refining further anchors the regional supply chain.

Europe’s market growth is anchored in the Digital Battery Passport regulation, which will require serial-number tracing of every pack component starting in 2027. Sensors capable of storing immutable usage logs within on-chip memory position suppliers to capitalize on this compliance wave. Although production costs remain higher than in Asia-Pacific, local content rules help preserve share for European manufacturers.

Competitive Landscape

Tier-1 automotive suppliers such as Continental, Bosch, and DENSO leverage deep OEM relationships and system-integration strengths to bundle sensors with full battery-management controllers. Their vertical integration allows tight cost control and faster certification cycles. Semiconductor specialists, notably Texas Instruments, Infineon, and Analog Devices, compete by pushing envelope-tracking, low-noise amplifiers, and machine-learning accelerators onto monolithic dies, refining performance for high-voltage packs.

Niche innovators disrupt with wireless or contactless cell-monitoring techniques. Dukosi’s chip-on-cell platform eliminates daisy-chain wiring, cutting harness weight and easing pack assembly. ACCURE Battery Intelligence, meanwhile, offers SaaS analytics that can ingest any sensor brand’s data, creating pull-through demand for higher-resolution measurements.

Consolidation continues as larger players acquire niche firms to secure intellectual property around electrochemical impedance spectroscopy, high-frequency wireless links, or secure bootloaders. IP portfolios increasingly matter because OEM contracts stipulate royalty-free access to patented safety functions, rewarding suppliers that invest early in R&D. Overall, moderate fragmentation persists, but the trajectory points toward greater concentration over the medium term.

Intelligent Battery Sensor Industry Leaders

Robert Bosch GmbH

Continental Automotive Technologies GmbH

FORVIA HELLA GmbH & Co. KGaA

DENSO Corporation

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ACCURE Battery Intelligence raised USD 16 million in Series B funding to speed global rollout of its AI-enabled diagnostic platform.

- January 2025: Marelli announced a next-generation BMS incorporating real-time electrochemical impedance spectroscopy for cell-level degradation tracking.

- December 2024: Marelli introduced a cost-optimized EIS solution aimed at high-volume EV programs.

- September 2024: LEM debuted the SMU sensor family with integrated busbar design and ASIL-B compliance for BEV applications.

Global Intelligent Battery Sensor Market Report Scope

The Intelligent Battery Sensor Market Report is Segmented by Sensor Type (Integrated Sensors, Voltage Sensors, Current Sensors, Temperature Sensors), Vehicle Type (Passenger Vehicles, Electric Vehicles, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles, Commercial Vehicles), Sales Channel (OEM, Aftermarket), Application (Battery Management Systems, Telematics and Start-Stop Systems, Renewable Energy Storage, Industrial Applications), End User (Automotive Manufacturers, Fleet Operators, Telecommunications, Renewable Energy Sector, Aerospace Defense and Electronics), and Geography (North America, South America, Europe, APAC, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated Sensors |

| Voltage Sensors |

| Current Sensors |

| Temperature Sensors |

| Passenger Vehicles |

| Electric Vehicles (EVs) |

| Hybrid Electric Vehicles (HEVs) |

| Plug-In Hybrid Electric Vehicles (PHEVs) |

| Commercial Vehicles (Trucks, Buses, Large Machinery) |

| OEM |

| Aftermarket |

| Battery Management Systems (BMS) |

| Telematics And Start-Stop Systems |

| Renewable Energy Storage |

| Industrial Applications |

| Automotive Manufacturers |

| Fleet Operators |

| Telecommunications |

| Renewable Energy Sector |

| Aerospace, Defense, And Electronics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia And New Zealand | |

| Middle East And Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria |

| By Sensor Type | Integrated Sensors | |

| Voltage Sensors | ||

| Current Sensors | ||

| Temperature Sensors | ||

| By Vehicle Type | Passenger Vehicles | |

| Electric Vehicles (EVs) | ||

| Hybrid Electric Vehicles (HEVs) | ||

| Plug-In Hybrid Electric Vehicles (PHEVs) | ||

| Commercial Vehicles (Trucks, Buses, Large Machinery) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Application | Battery Management Systems (BMS) | |

| Telematics And Start-Stop Systems | ||

| Renewable Energy Storage | ||

| Industrial Applications | ||

| By End User | Automotive Manufacturers | |

| Fleet Operators | ||

| Telecommunications | ||

| Renewable Energy Sector | ||

| Aerospace, Defense, And Electronics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia And New Zealand | ||

| Middle East And Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

Key Questions Answered in the Report

What is the current valuation of the intelligent battery sensor space and how fast is it expanding?

The segment is valued at USD 8.86 billion in 2026 and is forecast to reach USD 15.84 billion by 2031 on a 12.32% CAGR.

Which region is expected to contribute the most revenue through 2031?

Asia-Pacific accounts for 43.62% of 2025 revenue and is projected to keep the lead with a 12.61% CAGR as Chinas EV production and Japans semiconductor output scale further.

Which sensor type commands the largest share today?

Integrated sensors hold 38.42% share because OEMs favor single-package solutions that cut wiring and boost diagnostic depth.

Why are electric-vehicle programs driving new sensor demand?

EV battery packs require higher-precision voltage and temperature readings to manage 800 V architectures and fast-charge profiles, lifting sensor shipments at a 13.62% CAGR.

How quickly is the aftermarket channel growing for retrofit installations?

Aftermarket sales are rising at 12.74% CAGR as fleet operators retrofit start-stop and predictive-maintenance kits into aging vehicles.

What is the main barrier that could slow near-term sensor adoption?

Short-term delays in EV launch schedules and inventory corrections are trimming OEM call-offs, moderating growth until production programs normalize.

Page last updated on: