Vehicles Intelligence Battery Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 0.38 Billion |

| Market Size (2030) | USD 0.53 Billion |

| Growth Rate (2025 - 2030) | 6.91% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vehicles Intelligence Battery Sensor Market Analysis by Mordor Intelligence

The vehicles intelligence battery sensor market size stands at USD 0.38 billion in 2025 and is predicted to reach USD 0.53 billion by 2030, translating into a 6.91% CAGR through the forecast period. This sustained increase reflects rapid electrification across all vehicle classes, the compulsory roll-out of 12 V start-stop systems in response to tightening CO₂ rules, and original-equipment manufacturers (OEMs) shifting toward predictive maintenance that relies on continuous, over-the-air monitoring. Heightened demand for mild-hybrid 48 V architectures, the growing integration of advanced driver assistance features that place heavier loads on low-voltage networks, and the emergence of insurance telematics business models that link premiums to real-time state-of-health (SoH) data also play material roles in the vehicles intelligence battery sensor market expansion. At the same time, supply chain disruptions in automotive semiconductors raise near-term cost pressure, and cybersecurity mandates such as UN-R155 add design complexity, yet both forces ultimately favor higher-value intelligent sensors that help OEMs future-proof electrical architectures.

Key Report Takeaways

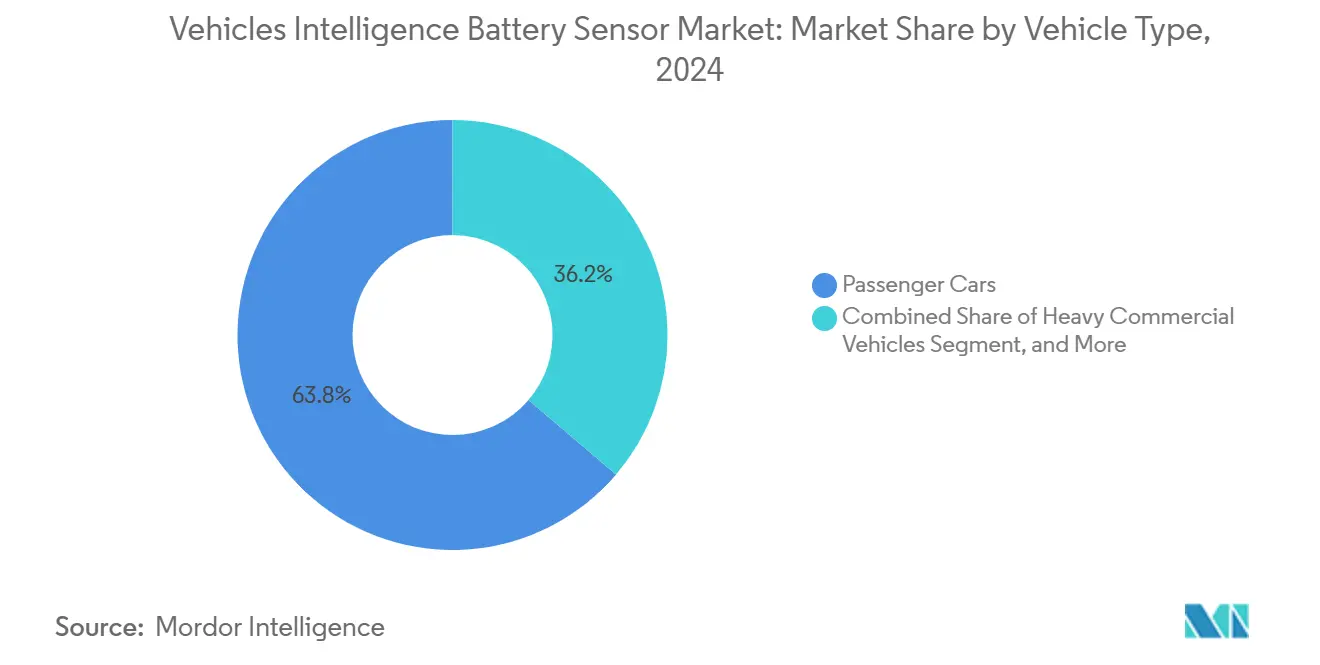

- By vehicle type, passenger cars led with a 63.76% revenue share in 2024, while heavy commercial vehicles are advancing at a 7.23% CAGR through 2030.

- By sensor technology, Hall-effect-based intelligent battery sensors held 71.24% of the vehicles intelligence battery sensor market share in 2024; shunt-type devices record the highest projected CAGR at 8.46% through 2030.

- By voltage range, 12 V systems accounted for 57.63% of the vehicles intelligence battery sensor market size in 2024, and 48 V+ + architectures are projected to rise at a 7.79% CAGR between 2025-2030.

- By sales channel, OEM-fitted units captured 83.94% of the 2024 value, yet the aftermarket segment is forecast to climb at an 8.68% CAGR to 2030.

- By geography, Europe commanded 28.76% of 2024 revenue, while South America records the fastest regional CAGR at 7.56% through 2030.

Global Vehicles Intelligence Battery Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global CO₂ / fuel-economy norms driving 12 V start-stop adoption | +1.5% | EU, China, spillover global | Medium term (2-4 years) |

| Accelerated electrification of auxiliary loads in ICE and xEV models | +1.2% | North America, EU, Asia-Pacific emerging | Long term (≥ 4 years) |

| OEM push for predictive maintenance and OTA battery-health data | +0.8% | Global, premium early adopters | Short term (≤ 2 years) |

| Growing penetration of 48 V mild-hybrid architectures | +0.6% | EU, North America core | Medium term (2-4 years) |

| Rising insurance telematics linking premiums to real-time battery SoH | +0.4% | North America, EU, Asia-Pacific | Long term (≥ 4 years) |

| EU passenger-car cybersecurity regulation (UN-R155) mandating secure in-battery sensing | +0.3% | EU first, global adoption trends | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Global CO₂ / Fuel-Economy Norms Driving 12 V Start-Stop Adoption

Regulatory authorities in the European Union and China require every new passenger-car platform to realize quantifiable fuel-economy gains, and intelligent battery sensors have become indispensable because they prevent restart failures inherent in frequent engine stop-start events. Euro 7 guidelines explicitly reference stringent voltage accuracy thresholds that legacy shunt solutions cannot meet, and China National VI extends similar logic to light commercial fleets. Bosch’s Battery-in-the-Cloud program demonstrates the commercial value: by pairing intelligent battery sensors with predictive algorithms, the system prolongs battery life by 20% in start-stop use cases, eliminating warranty claims and safeguarding brand equity. [1]Robert Bosch GmbH, “Battery in the Cloud,” bosch.com Municipalities that enforce low-emission zones also accelerate adoption, as fleet operators now quantify a 3–8% CO₂ reduction during urban duty cycles once an intelligent sensor is in place.

Accelerated Electrification of Auxiliary Loads in ICE and xEV Models

Electric power steering, e-turbo compressors, and active suspension elevate instantaneous current demand far above levels foreseen in legacy 12 V designs. OEM benchmarking shows that steering assist alone can draw peaks of 80 A, necessitating real-time current, voltage, and temperature sampling to avoid brownouts. Tesla’s overcharge-detection patent illustrates how every auxiliary domain must feed accurate data into a centralized battery-management hub to preserve long-term pack health. Continental’s zone-based architecture further highlights that non-contact Hall-effect sensors simplify harnesses, cutting wiring weight by 2 kg per vehicle and saving USD 35 per unit in material cost. Combined, these factors enhance the commercial case for advanced sensors that can safely orchestrate multiple electric loads simultaneously.

OEM Push for Predictive Maintenance and OTA Battery-Health Data

Connected-vehicle platforms allow automakers to transform battery data into recurring revenue streams. HARMAN’s partnership with Microsoft shows that cloud analytics can forecast battery failures two to three months ahead of time, cutting roadside-assistance incidents in half and enabling subscription-based battery-health dashboards for end users. [2]HARMAN International, “Connected Vehicle Solutions,” harman.com Commercial fleets derive even stronger value; every unscheduled downtime incident costs up to USD 500 per day, and predictive maintenance nearly eliminates that exposure. T-Systems processes over one million vehicles’ battery telematics in real time, feeding insights into continuous software improvements and laying the foundation for pay-as-you-drive warranty extensions.

Growing Penetration of 48 V Mild-Hybrid Architectures

BMW’s deployment of 48 V mild-hybrid systems across its mainstream lineup improves fuel efficiency by 10–15% and unlocks electric turbocharging, electric superchargers, and regenerative dampers. [3]Veratron AG, “24 V Intelligent Battery Sensor Datasheet,” veratron.com Each 48 V domain still relies on a parallel 12 V network, which demands bidirectional power flow and galvanic isolation that intelligent sensors handle elegantly. Design verification reports show that sensors with dual-voltage capability cut calibration effort by 30%, helping OEMs meet launch timelines even as electrification complexity rises. Volvo’s FH Electric truck pushes the same architecture into heavy-duty territory, where 600 kWh packs require hundreds of synchronized sensors to meet thermal-runaway prevention standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in automotive semiconductor and Hall-effect IC supply | -0.9% | Global, Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| High average selling price of intelligent sensors versus legacy shunt solutions | -0.7% | Asia-Pacific, emerging markets | Medium term (2-4 years) |

| OEM hesitation on cybersecurity implementation cost for LIN-to-CAN gateways | -0.5% | Cost-sensitive regions | Short term (≤ 2 years) |

| Persistently low two-wheeler adoption owing to price sensitivity | -0.4% | India, ASEAN, LATAM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive Semiconductor and Hall-Effect IC Supply

Automotive-grade Hall-effect sensors depend on advanced 200 mm and 300 mm fabs that are already at full utilization due to surging demand from ADAS radars and traction inverters. When fire damage temporarily closed a single Japanese foundry in 2024, lead times for Allegro MicroSystems’ automotive Hall devices stretched to 26 weeks, prompting line-down warnings at five European OEMs simultaneously. Analysts expect semiconductor cost per vehicle to double toward 2030, compressing OEM gross margins and forcing procurement teams to stockpile silicon inventory, a practice that keeps short-term sensor shipments volatile.

High ASP of Intelligent Sensors vs. Legacy Shunt Solutions

Cost deltas of USD 3–4 per vehicle may appear modest in isolation, yet on a 2-million-unit platform they translate into more than USD 6 million in incremental bill-of-materials expense. Veratron’s 24 V commercial-vehicle sensor underscores the challenge: although the device delivers SoH precision within ±2 %, its price is nearly twice that of a classic low-side shunt. Passenger-car OEMs in cost-sensitive segments therefore dual-source Hall and shunt designs, limiting intelligent sensor penetration until volume ramps drive down per-unit prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Heavy-Duty Electrification Outpaces Passenger-Car Baseline

The vehicles intelligence battery sensor market size for passenger cars remained dominant at USD 0.24 billion in 2024, equal to 63.76% share, as every new European and Chinese model launches with mandatory start-stop functionality. Heavy commercial vehicles, however, represent the primary growth vector: their 7.23% CAGR through 2030 surpasses the overall market expansion by 32 basis points, a sign of accelerating fleet electrification mandates. IVECO’s S-eWay Rigid electric truck integrates modular 280–490 kWh battery strings that require granular cell-level sensing, translating into sensor content of nearly USD 210 per unit. Two-wheelers trail materially; adoption remains low because paying USD 10 extra for a sensor on a USD 1,000 scooter erodes price positioning.

Fleet operators also deploy predictive maintenance software that leverages sensor data to reduce unscheduled stops. Case studies from long-haul fleets in North America show a 2.3-month payback when intelligent sensors avert just one roadside battery failure. Passenger-car aftermarket retrofits rise in parallel as ride-hailing drivers install sensors voluntarily to avoid income-losing breakdowns and to qualify for telematics-linked insurance discounts.

By Sensor Technology: Shunt-Type Accuracy Gains Challenge Hall-Effect Dominance

Hall-effect devices secured 71.24% of vehicles intelligence battery sensor market share in 2024 by offering galvanic isolation and ±1 % accuracy without drift. Technological advances in coefficient-of-temperature compensation now allow shunt-type devices to reach the same accuracy envelope for half the cost, stimulating an 8.46% CAGR forecast that puts incremental stress on Hall-effect pricing. TDK’s TMR current sensor, for instance, consumes one-fifth the power of a comparable Hall IC while cutting offset error in half. Tier-one suppliers build algorithmic error correction into microcontroller firmware, shrinking the performance gap further and allowing shunt-based reference designs to clear ISO 21498 accuracy targets.

Industry sourcing trends signal a blended procurement strategy. OEMs specify Hall-effect sensors on premium EV architectures where cold-crank compliance and electromagnetic immunity are critical, while deploying cost-optimized shunt solutions on high-volume ICE platforms in emerging markets. The hybrid approach maximizes economies of scale and diversifies supply risk, ensuring that no single silicon node can paralyze an entire vehicle program.

By Voltage Range: 48 V Adoption Rises on Mild-Hybrid Benefits

Higher-voltage power nets captured only 42.37% of 2024 revenue, yet their 7.79% CAGR eclipses the broader vehicles intelligence battery sensor market. BMW’s mainstream rollout of 48 V mild hybrids demonstrates how elevated bus voltages unlock 10–15% fuel savings and quieter engine restarts, features that align with looming Euro 7 acoustics limits. Every 48 V pack requires dual-domain sensing to coordinate energy flow to the legacy 12 V board net, increasing sensor unit count by almost 80% per vehicle and growing the vehicles intelligence battery sensor market size faster than underlying vehicle production.

At the same time, 12 V remains essential for legacy fleets and aftermarket retrofits. That installed base justifies upgraded replacement sensors with LIN or CAN interfaces that feed data into smartphone apps, creating repeat-purchase revenue streams for back-channel distributors. Regulatory headwinds such as UN GTR No. 20 on battery safety push high-voltage architectures to adopt gas-detection sensors like Honeywell’s Li-ion Tamer, expanding total addressable market scope beyond simple current and voltage sensing.

By Sales Channel: Aftermarket Emerges as Profit Pool

OEM-fitted sensors represented 83.94% of 2024 sales thanks to favorable in-line assembly economics and the ability to bundle costs into vehicle sticker prices. However, the aftermarket channel grows at 8.68% CAGR as fleet managers retrofit existing assets to avoid premature battery failures. Heavy-duty trucks approaching their sixth year in service show a 35 % jump in battery-related breakdowns; a USD 40 retrofit sensor mitigates that risk and qualifies owners for insurance rebates.

Digitally native consumers further amplify demand: ride-sharing drivers in Europe now receive usage-based insurance quotes that incorporate SoH telemetry sourced from OBD-dongle-connected sensors. Aftermarket suppliers differentiate through plug-and-play kits that auto-register on mobile apps, circumventing dealer networks and capturing higher gross margins. The vehicles intelligence battery sensor industry, therefore, treats the aftermarket less as a tail but more as a growth engine that balances the cyclicality of OEM production schedules.

Geography Analysis

Europe’s 28.76% share reflects aggressive electrification timelines and cybersecurity prescriptions under UN-R155 that require secure in-battery authentication chains. German premium OEMs specify dual-redundant sensors on flagship EVs, lifting average content per vehicle in the region to USD 18, nearly double the global mean. South America, by contrast, records the highest CAGR at 7.56%, fueled by new mild-hybrid assembly plants in Brazil and Argentina that localize sensor sourcing to sidestep import tariffs. Inter-American Development Bank financing accelerates infrastructure readiness, giving fleets confidence to invest in battery-intensive applications.

North America benefits from federal tax credits, and the California Air Resources Board (CARB) mandates that shift last-mile delivery vans toward electrified platforms requiring sophisticated low-voltage monitoring. Asia-Pacific reveals a bifurcated story: China sets the pace with strong government mandates and vertically integrated supply chains, whereas ASEAN markets lag because cost pressures limit intelligent-sensor take-rates on economy motorcycles. The Middle East and Africa remain nascent but show pockets of demand in zero-emission port logistics where battery safety is paramount.

Competitive Landscape

Dominant tier-one suppliers-Continental, Bosch, and HELLA-integrate sensors into holistic battery-management solutions that dovetail with zonal electrical architectures. Their multi-decade OEM relationships secure design wins well into the next model cycle, reinforcing entry barriers. Semiconductor firms such as Melexis, NXP, and Texas Instruments capture value at the die level, investing in Hall and TMR innovations that safeguard gross margins even as unit ASPs drift downward.

White-space entrants target software layers. Cloud analytics specialists ingest edge sensor data to offer SoH dashboards, warranty risk scoring, and residual-value prediction services. Such platforms turn raw amperage readings into actionable insights, augmenting hardware and embedding switching costs that favor long-term subscriptions. Tesla’s expanding patent wall in overcharge detection and voltage regulation highlights the strategic importance of algorithmic IP in protecting differentiation.

Strategic collaborations blur traditional boundaries: Continental’s partnership with semiconductor foundries secures wafer allocation, while HELLA and TDK co-develop reference designs that marry magnetoresistive sensing with in-house microcontroller firmware to accelerate certification cycles. The vehicles intelligence battery sensor market, therefore, illustrates classic industry convergence, where electronics, software, and cloud services merge into unified value propositions.

Vehicles Intelligence Battery Sensor Industry Leaders

Continental AG

Robert Bosch GmbH

HELLA GmbH & Co. KGaA

DENSO Corporation

Melexis NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CATL unveiled the TECTRANS battery system featuring a 15-year service life and superfast charging, enabled by dense, high-precision battery-sensor networks.

- April 2025: NITI Aayog stated in The Economic Times that semiconductor costs per vehicle could reach USD 1,200 by 2030, heightening cost pressure on intelligent battery sensor suppliers.

- February 2025: Bosch rolled out its second-generation Battery-in-the-Cloud platform, extending coverage to heavy commercial vehicles equipped with 48 V intelligent battery sensors.

- January 2025: HARMAN and Microsoft launched a production-scale predictive battery analytics service that uses intelligent battery sensors to forecast failures several months in advance.

Global Vehicles Intelligence Battery Sensor Market Report Scope

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Off-Highway Vehicles |

| Hall-Effect Based IBS |

| Shunt-Type IBS |

| 12 V Systems |

| 24 V Systems |

| 48 V Systems and Above |

| OEM-Fitted |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Two-Wheelers | |||

| Off-Highway Vehicles | |||

| By Sensor Technology | Hall-Effect Based IBS | ||

| Shunt-Type IBS | |||

| By Voltage Range | 12 V Systems | ||

| 24 V Systems | |||

| 48 V Systems and Above | |||

| By Sales Channel | OEM-Fitted | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the vehicles intelligence battery sensor market in 2025?

It is valued at USD 0.38 billion in 2025 and is forecast to grow at a 6.91% CAGR to 2030.

Which vehicle class drives the highest sensor demand?

Passenger cars account for 63.76% of 2024 revenue, but heavy commercial trucks show the fastest growth at 7.23% CAGR.

Why are 48 V systems important for sensor suppliers?

Mild-hybrid 48 V networks require dual-domain monitoring, boosting sensor content per vehicle and expanding addressable market by 7.79% CAGR.

What is the main restraint on wider sensor adoption?

Volatile Hall-effect IC supply and higher unit prices versus legacy shunt solutions slow short-term adoption, especially in cost-sensitive regions.

Who are the leading companies?

Continental, Bosch, and HELLA dominate through integrated battery-management portfolios, while semiconductor firms such as Melexis and NXP supply core sensing ICs.

Page last updated on: