Current Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

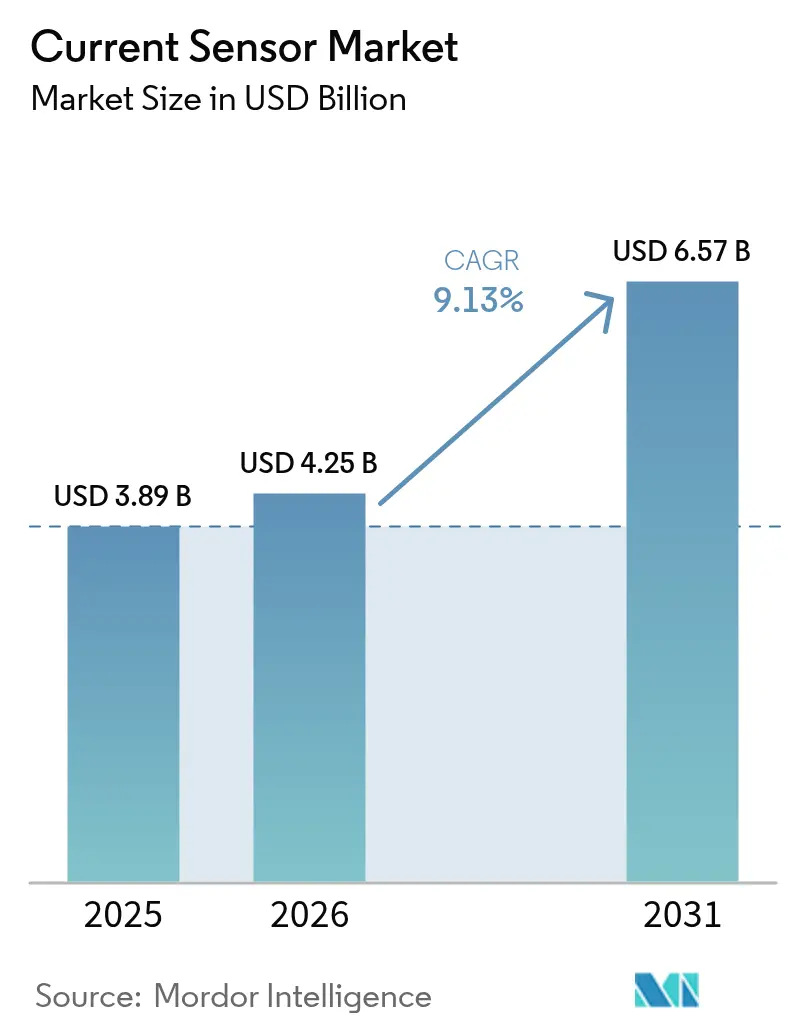

| Market Size (2026) | USD 4.25 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 9.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Current Sensor Market Analysis by Mordor Intelligence

The current sensor market size is expected to grow from USD 3.89 billion in 2025 to USD 4.25 billion in 2026 and is forecast to reach USD 6.57 billion by 2031 at 9.13% CAGR over 2026-2031. This expansion mirrors surging electrification mandates, functional-safety requirements, and rising power-density targets across automotive, industrial, and energy domains. Demand for precise battery monitoring in electric vehicles (EVs) anchored growth, while renewable-energy installations multiplied sensor nodes per megawatt. Manufacturers pursued integrated Hall-effect and tunnelling-magnetoresistance (TMR) solutions to meet isolation, bandwidth, and efficiency needs. Supply‐chain volatility for magnetic alloys and cybersecurity compliance costs in smart-grid rollouts tempered momentum, yet data-center power monitoring for artificial-intelligence (AI) workloads opened a new revenue stream[1]Allegro MicroSystems, “What is TMR: Tunnel Magnetoresistance – Blog,” allegromicro.com .

Key Report Takeaways

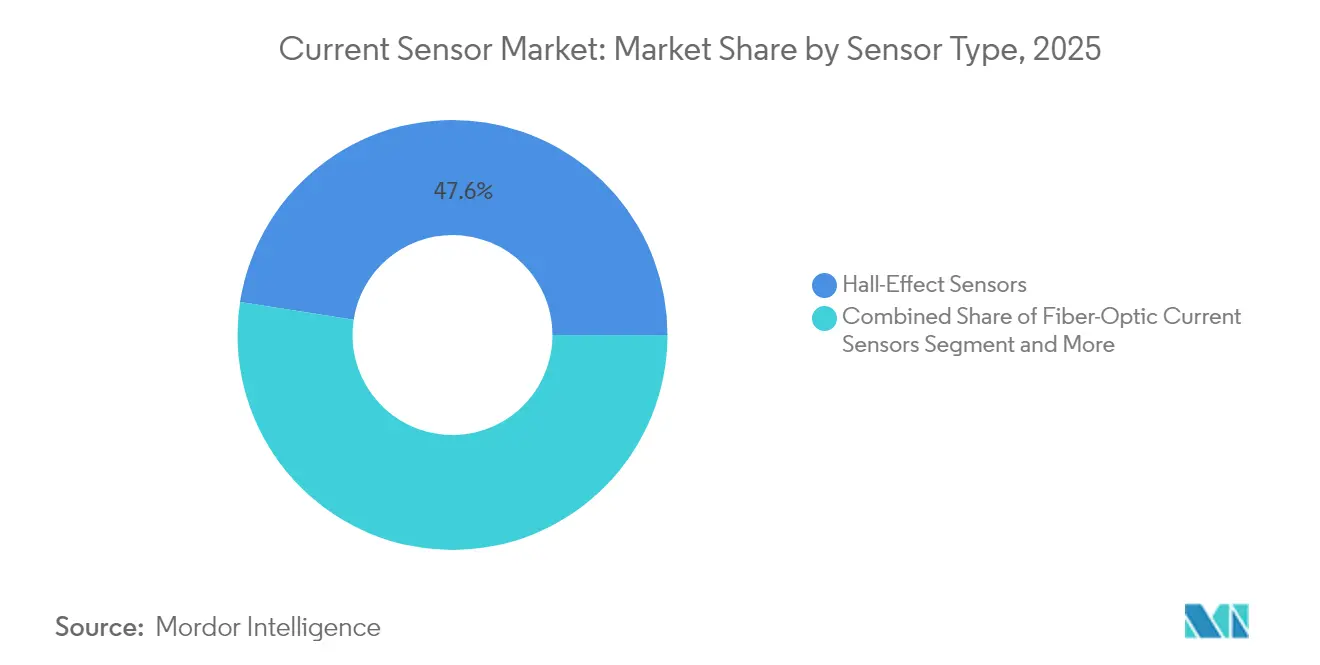

- By sensor type, Hall-effect devices led with 47.55% revenue share in 2025, whereas fiber-optic devices are projected to expand at a 12.21% CAGR to 2031.

- By isolation technology, the open-loop segment held 56.58% of the current sensor market share in 2025; closed-loop devices are growing at 11.12% CAGR through 2031.

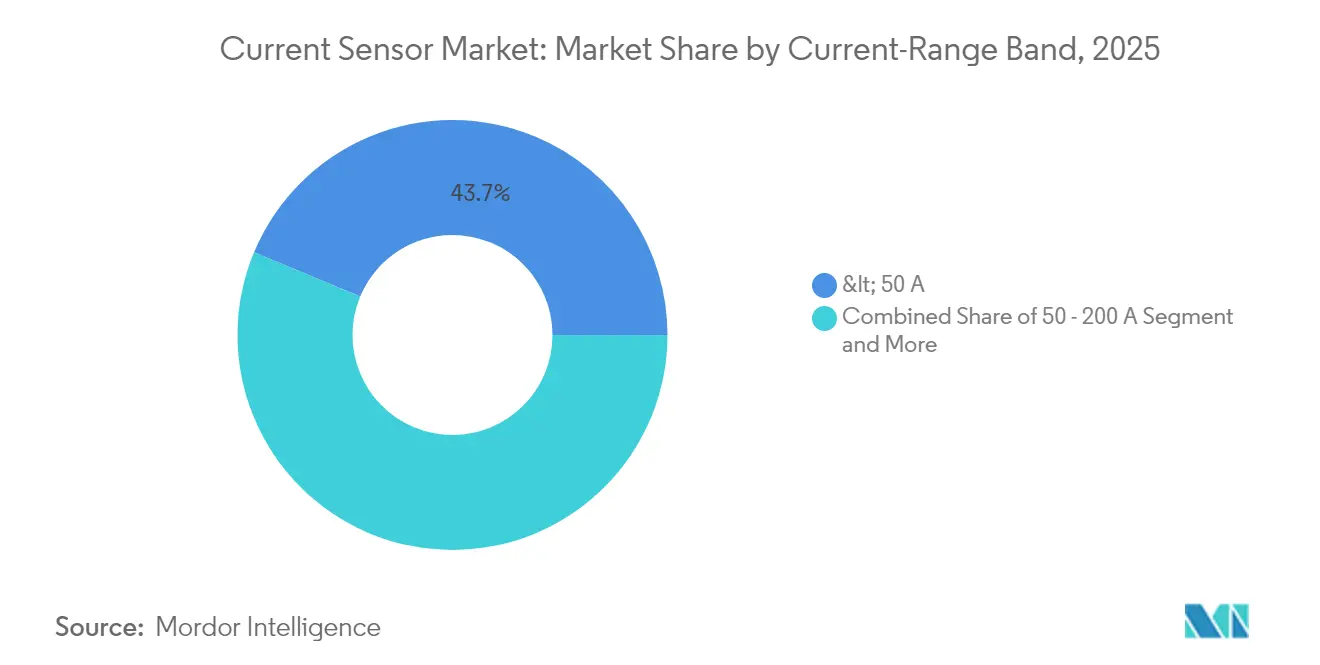

- By current range, sensors above 600 A accounted for 13.66% of the current sensor market size and deliver the fastest 13.62% CAGR between 2026-2031.

- By end-user industry, automotive and transportation commanded 37.88% of the current sensor market size in 2025, while the energy and power segment is advancing at 10.61% CAGR to 2031.

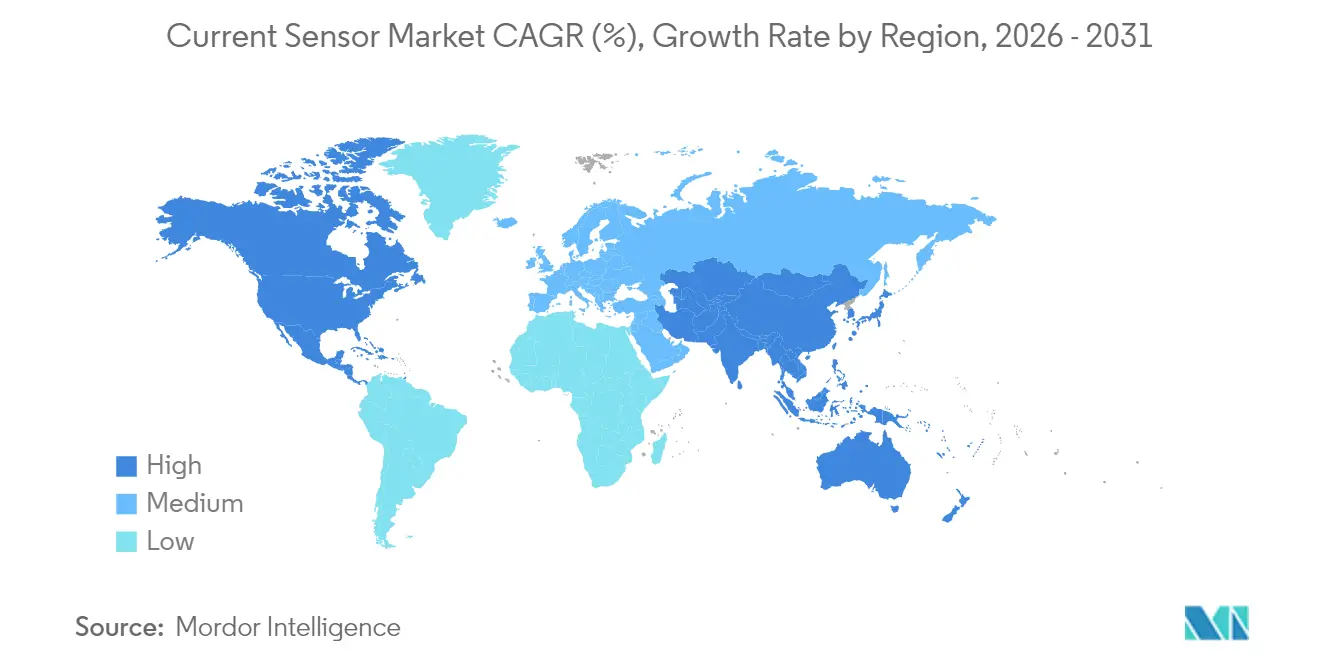

- By geography, Asia-Pacific captured 46.27% revenue share in 2025 and continues to outpace global growth at a mid-single-digit CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Current Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of battery-powered and renewable energy systems | +2.1% | Global, with Asia-Pacific leading deployment | Medium term (2-4 years) |

| Acceleration of EV electrification and ADAS integration | +1.8% | Global, concentrated in China, the EU, and North America | Short term (≤ 2 years) |

| Functional-safety mandates (ISO 26262, IEC 61508) | +1.3% | EU and North America, primarily, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Surge in bidirectional on-board charger (V2G) deployments | +0.9% | Early adoption in Japan, California, and expanding globally | Medium term (2-4 years) |

| High-frequency GaN/SiC power-electronics miniaturization | +1.1% | Global, with manufacturing concentrated in Asia-Pacific | Medium term (2-4 years) |

| Data-center power monitoring for AI workloads | +0.7% | North America and Asia-Pacific data center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Battery-Powered and Renewable-Energy Systems

Utility-scale solar and storage projects installed multiple monitoring points—DC combiner boxes, inverter inputs, and grid-tie links—creating a multiplier effect on sensor demand per megawatt. Bidirectional vehicle-to-grid (V2G) interfaces required sub-1% accuracy when measuring charge and discharge currents, pressuring traditional Hall-effect devices and boosting fiber-optic adoption for their electromagnetic immunity[2]Delta Electronics, “Delta Provides Telecom Energy Solutions to Ensure Customer Success,” deltaww.com. Asia-Pacific installations paired renewable-energy mandates with EV incentives, compounding sensor demand across automotive, industrial, and grid markets. Distributed-energy deployments also favored non-intrusive Rogowski coils for retrofit accuracy checks. Integrators increasingly specified digital interfaces, so field data fed directly into predictive-maintenance platforms.

Acceleration of EV Electrification and ADAS Integration

Premium EVs migrated to 800 V architectures, compelling sensors to sustain ≥5 kV isolation while delivering microsecond response times. A single battery-electric vehicle already required up to 50 current measurement points spanning traction inverters, battery-management systems (BMS), and thermal loops. ADAS actuators in steer-by-wire and brake-by-wire modules added redundant sensing channels for ISO 26262 compliance. TMR solutions gained share through superior temperature stability and lower quiescent current, positioning suppliers like Allegro MicroSystems to replace legacy Hall-effect parts in powertrain and chassis domains. SiC inverters, switching above 100 kHz, stretched bandwidth expectations beyond conventional current transformers, spurring investment in integrated sensing within power modules.

Functional-Safety Mandates (ISO 26262, IEC 61508)

Automakers escalated from performance-centric to safety-critical designs, embedding dual-channel architectures plus internal diagnostics that flag latent sensor drift in real time. TDK’s TAS8240 redundant TMR angle sensor exemplified this shift with four analog outputs, enabling ASIL-D compliance for steering-torque feedback. European regulators enforced stringent timelines, encouraging suppliers to offer pre-certified components and shortening vehicle validation cycles. Safety-oriented firmware updates required secure over-the-air (OTA) protocols, so sensors adopted authenticated digital buses to preserve integrity. These requirements widened the competitive gap between multinational incumbents and low-cost Hall-effect vendors lacking automotive safe-launch credentials.

High-Frequency GaN/SiC Power-Electronics Miniaturization

Wide-bandgap devices switched beyond 100 kHz, invalidating traditional CT bandwidth. Rogowski coils and fiber-optic alternatives sustained flat response curves, while module makers co-packaged sensors to cut parasitic inductance. ON Semiconductor integrated current-sense pads within SiC half-bridges aimed at Chinese EV traction platforms, enhancing loop stability and easing thermal design. Data-center operators adopted 48 V intermediate buses and placed sensors on every power shelf, raising attach rates per rack. Space-constrained power supplies demanded PCB-embedded solutions, prompting new SiP offerings where sensing ASICs resided beside GaN FETs without magnetic cores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Average-selling-price erosion in Hall-effect sensors | -0.8% | Global, most pronounced in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Accuracy drift vs. shunt / CT alternatives | -0.5% | Global, affecting precision applications | Medium term (2-4 years) |

| Supply-chain tightness for high-permeability core alloys | -1.2% | Global, with acute shortages in rare earth materials | Medium term (2-4 years) |

| Cybersecurity compliance costs in smart-grid metering | -0.4% | EU and North America primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Average-Selling-Price Erosion in Hall-Effect Sensors

Chinese fabs flooded commodity automotive grades, squeezing gross margins and triggering consolidation among incumbent suppliers. Tier-1 integrators centralized procurement to extract volume discounts, accelerating a race-to-bottom dynamic in the entry-level Hall-effect tier. Vendors attempted to differentiate through system-in-package features—diagnostics or digital interfaces—but price gaps still widened. Many niche manufacturers pivoted toward TMR or fiber-optic portfolios; however, the steep R&D commitment and lengthy automotive qualification deterred smaller firms. Integrated module strategies partly countered price pressure by bundling sensor plus MCU supervision within power stages, aligning with OEM value-based sourcing models.

Supply-Chain Tightness for High-Permeability Core Alloys

Fluxgate and CT designers relied on high-permeability alloys rich in rare earths, yet geopolitical tension and limited smelting capacity lengthened lead times beyond five months. Western suppliers scrambled for alternative sources outside China, while some redesigned products around synthetic ferrites. Delivery gaps forced OEMs to dual-source or switch to non-core technologies like TMR, accelerating technology substitution. Cost escalations flowed downstream to end users, particularly in grid instrumentation contracts that locked pricing up to five years. Innovation shifted toward core-less architectures, mitigating material risk and reducing sensor mass for high-volume EV applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Hall-Effect Retained Scale While TMR Disrupted Premium Niches

Hall-effect devices captured 47.55% revenue in 2025 due to mature production lines and proven reliability across traction inverters and industrial drives. Yet their bandwidth ceiling and thermal drift propelled designers toward TMR and fiber-optic options. Fiber-optic sensors recorded a 12.21% CAGR for 2026-2031 as renewable-energy installers specified galvanic-free measurement in high-voltage switchyards. TMR delivered 10× sensitivity over legacy Hall-effect, enabling low-ohmic drop in BMS shunt replacements and cutting standby power in battery packs.

Advanced EV inverters integrated a co-packaged TMR die for instantaneous phase-current feedback that met 1 MHz bandwidth targets. The current sensor market size for fibre-optic devices is forecast to reach USD 1,012 million by 2031 amid HVDC expansion. Inductive CTs retained a foothold above 1,000 A, while Rogowski coils addressed retrofit audits without interrupting conductors. The transition accelerated as power-density roadmaps demanded non-saturating, low-profile options suitable for tight module footprints.

By Isolation Technology: Closed-Loop Gained Precision Ground

Open-loop architectures dominated with 56.58% share, balancing cost and safety for 400 V EV packs and 600 V solar inverters. Closed-loop devices—leveraging magnetic feedback for ±0.5% accuracy—posted an 11.12% CAGR as designers sharpened efficiency metrics. These sensors offset ambient temperature drift in onboard chargers and servo drives, ensuring regulators met eco-design standards in Europe. Current sensor market share for closed-loop options is expected to climb toward 41.05% by 2031.

Non-isolated shunt sensors thrived in emerging 48 V mild-hybrid platforms where galvanic isolation was non-mandatory. However, pack-level voltages creeping toward 60 V threatened their addressable window, inciting suppliers to pair shunts with digital isolators in hybrid packages. The convergence of analog front-end, sigma-delta converter, and isolation channel in a single IC redefined BOM costs and shrank PCB real estate, strengthening the closed-loop value proposition.

By Current Range: High-Power Segments Accelerated

Sub-50 A units held 43.72% share in 2025, buoyed by consumer electronics, chargers, and factory automation I/O modules. The 50-200 A class powered mainstream EV traction motors and forklifts, forming an entrenched mid-market. From 200-600 A, adoption remained steady in commercial-vehicle drivelines and mid-scale storage inverters.

Above 600 A, demand surged at 13.62% CAGR as gigawatt-hour battery farms and 350 kW fast chargers proliferated. Current sensor market size for >600 A devices is set to exceed USD 1.35 billion by 2031, underpinned by grid-scale storage and V2G rollouts. Rogowski and fiber-optic platforms dominated here thanks to non-saturation at kiloamp levels and sub-microsecond response, meeting dynamic grid-code requirements for fault ride-through.

By End-User Industry: Energy and Power Took Growth Crown

Automotive and transportation retained 37.88% share in 2025 as EV volumes compounded and ADAS penetrated mid-range vehicles. Industrial automation trailed, benefiting from robotics densification and predictive-maintenance programs. Energy and power posted the fastest 10.61% CAGR, driven by national renewable targets and multimegawatt storage projects.

Telecom and data-centre operators ramped power-shelf monitoring to optimize AI server loads, boosting attach rates for high-bandwidth sensors. Consumer electronics sustained meaningful volume through wearables and IoT nodes, though ASPs stayed low. Medical devices grew steadily on chronic-disease monitoring, demanding high-reliability, low-noise performance under stringent regulatory review.

Geography Analysis

Asia-Pacific led with 46.27% revenue in 2025 because China scaled EV output and maintained dominant semiconductor packaging capacity. Governments funded renewables, prompting domestic fiber-optic sensor startups to emerge. Japan leveraged precision-manufacturing heritage to commercialize advanced TMR products, while South Korea integrated current sensing in SiC power-module export lines.

North America ranked second. Hyperscale data-center spending and Inflation Reduction Act incentives for clean-energy projects spurred sensor procurement. United States reshoring programs favored local fabrication of safety-critical components destined for grid infrastructure and defense. Canada’s push for battery-raw-material autonomy underpinned regional sensor demand tied to mining electrification.

Europe pursued stringent CO₂ targets and functional-safety mandates, sustaining high ASPs for automotive-grade closed-loop devices. Germany and France hosted key R&D hubs linking sensor design with GaN inverter start-ups. The Middle East and Africa recorded emerging demand via solar-park investments, whereas Latin America’s growth followed automotive assembly clusters in Mexico and Brazil. Across regions, the current sensor market size co-moved with battery manufacturing footprints and renewable-energy capex.

Competitive Landscape

The sector exhibited moderate fragmentation as top five suppliers controlled under 60% combined sales. Allegro MicroSystems, Infineon Technologies, and TDK Corporation leveraged IDM fabs and broad patent portfolios to dominate high-volume automotive and industrial sockets. Infineon paired Hall-effect sensing with gate drivers, capturing BOM synergies in traction inverters.

Specialist firms targeted niches: LEM focused on railway and high-current modules, while startup MDT pushed TMR angle sensors into collaborative robots. Collaboration surged; ON Semiconductor aligned with module packagers to embed sensing dice inside SiC half-bridges, shrinking loop area and improving EMI. Tesla patented integrated flux shields, signalling OEM in-house sensor development and raising competitive tension.

Price rivalry stayed muted at the premium end; differentiation revolved around bandwidth, safety certification, and isolation-voltage headroom. Suppliers invested in cybersecurity stacks so sensors met smart-grid IEC 62443 guidance. Consolidation was anticipated as scale became vital to fund R&D in core-less magnetic materials and AI-enabled diagnostics.

Current Sensor Industry Leaders

-

Allegro MicroSystems, LLC

-

TDK Corporation (TDK-Micronas GmbH)

-

Infineon Technologies AG

-

Melexis NV

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ON Semiconductor reported USD 1.45 billion Q1 revenue, citing SiC traction design-wins in nearly 50% of new EV models.

- May 2025: TDK published guidance positioning TMR sensors over resolvers for e-motor control.

- May 2025: MDT unveiled high-precision TMR angle sensors for robotics control.

- January 2025: TDK Corporation announced sensing solutions for smart-home IoT with embedded edge processing.

Global Current Sensor Market Report Scope

A current sensor is a machine that detects and converts current to an easily measurable output voltage, which is proportionate to the current through the measured path. It accomplishes this by precisely measuring the drop in voltage at a resistor placed in the path of the current. This allows the current sensor to generate an estimate of the level of current flowing through the line.

The current sensor market is segmented by type (hall effect sensors (open loop, closed loop, and other hall effect sensors), fiber optic current sensors, inductive current sensors), end-user (automotive, consumer electronics, telecom, and networking, medical, energy and power, industrial, and other end users), and geography (North America (United States and Canada), Europe (Germany, United Kingdom, France and Rest of Europe), Asia Pacific (India, China, Japan and rest of the Asia Pacific), and other countries ( Latin America and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Hall-Effect Sensors |

| Fiber-Optic Current Sensors |

| Inductive / CT Sensors |

| Fluxgate Sensors |

| Rogowski-Coil Sensors |

| Open-Loop (Isolated) |

| Closed-Loop (Isolated) |

| Non-Isolated (Shunt-based) |

| <50 A |

| 50 – 200 A |

| 200 – 600 A |

| >600 A |

| Automotive and Transportation |

| Industrial Automation and Robotics |

| Energy and Power (Solar, Wind, ESS) |

| Consumer Electronics |

| Telecom and Data-Centers |

| Medical Devices |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Sensor Type | Hall-Effect Sensors | ||

| Fiber-Optic Current Sensors | |||

| Inductive / CT Sensors | |||

| Fluxgate Sensors | |||

| Rogowski-Coil Sensors | |||

| By Isolation Technology | Open-Loop (Isolated) | ||

| Closed-Loop (Isolated) | |||

| Non-Isolated (Shunt-based) | |||

| By Current Range | <50 A | ||

| 50 – 200 A | |||

| 200 – 600 A | |||

| >600 A | |||

| By End-User Industry | Automotive and Transportation | ||

| Industrial Automation and Robotics | |||

| Energy and Power (Solar, Wind, ESS) | |||

| Consumer Electronics | |||

| Telecom and Data-Centers | |||

| Medical Devices | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected growth rate of the current sensor market between 2026 and 2031?

The market is projected to expand at a 9.13% CAGR, rising from USD 4.25 billion in 2026 to USD 6.57 billion by 2031.

Which region leads current sensor demand?

Asia-Pacific held 46.27% revenue share in 2025 on the back of China’s EV production scale and integrated semiconductor supply chains.

Which sensor technology is growing the fastest?

Fiber-optic current sensors are forecast to grow at a 12.21% CAGR through 2031 as high-voltage renewable-energy installations favor galvanic-free measurement.

How are functional-safety regulations affecting design?

Standards such as ISO 26262 and IEC 61508 push adoption of redundant architectures with built-in diagnostics, boosting demand for closed-loop and TMR solutions with ASIL-D compliance.

Page last updated on: