Industrial Wireless Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.03 Billion |

| Market Size (2031) | USD 17.04 Billion |

| Growth Rate (2026 - 2031) | 13.48% CAGR |

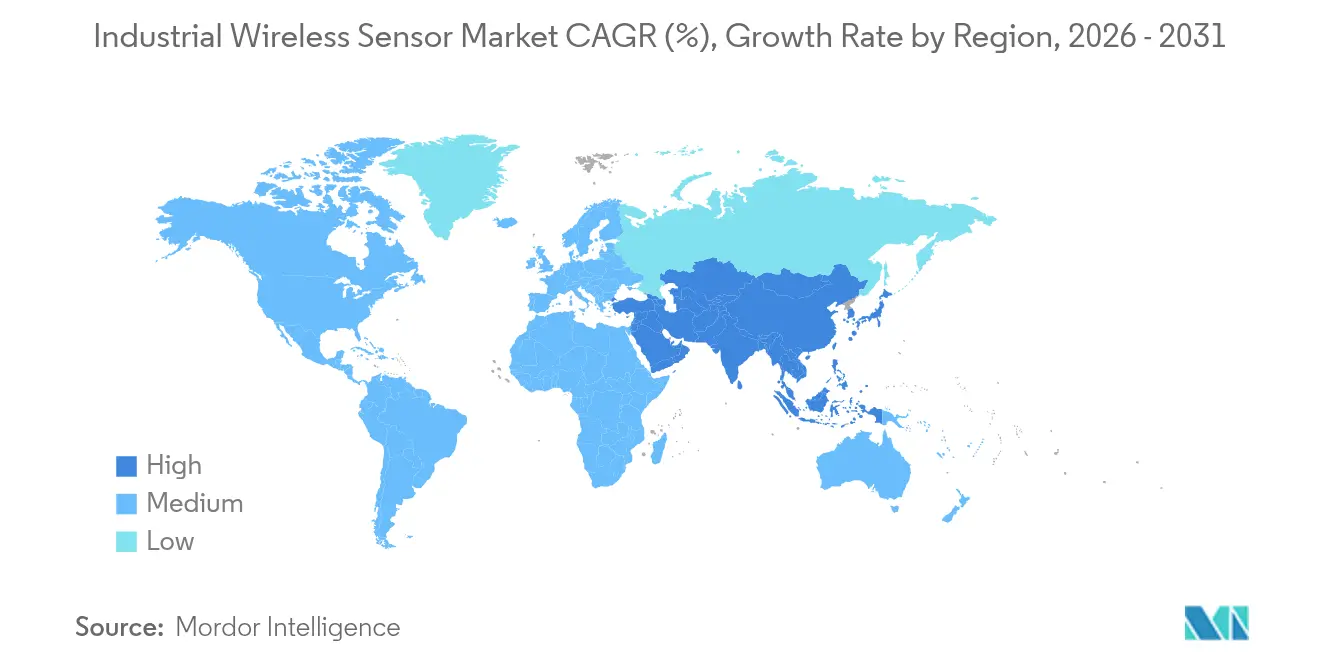

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Wireless Sensor Market Analysis by Mordor Intelligence

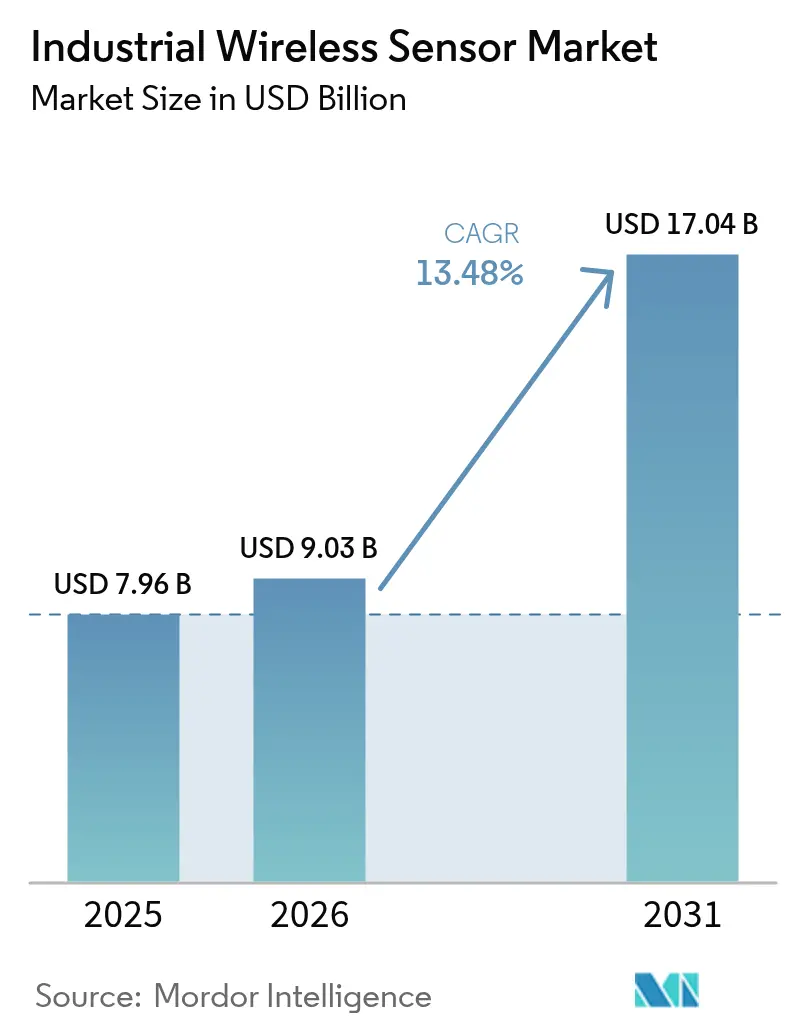

The industrial wireless sensors market size is expected to grow from USD 7.96 billion in 2025 to USD 9.03 billion in 2026 and is forecast to reach USD 17.04 billion by 2031 at 13.48% CAGR over 2026-2031. The expansion signals how digitalization, edge computing, and low-power wide-area networking push wireless sensing from pilot projects into core operational infrastructure. Falling chipset prices lower the total cost of ownership, while protocol innovation reduces integration risk, positioning the industrial wireless sensors market as an attractive investment priority for asset-intensive industries worldwide. Vendors continue to improve cyber-secure, battery-agnostic designs, enabling monitoring in previously inaccessible areas and unlocking data-driven maintenance strategies. This momentum accelerates platform convergence in which sensors, gateways, and analytics merge to create unified edge-to-cloud architectures that shorten decision cycles and raise asset value.[1] Emerson Newsroom, “Emerson’s ‘Project Beyond’ to Modernize and Seamlessly Integrate the Industrial Automation Technology Stack,” emerson.com

Key Report Takeaways

- By product type, pressure sensors led with 26.65% of industrial wireless sensors market share in 2025.

- By communication protocol, Wi-Fi held 44.65% of industrial wireless sensors market size in 2025, while LPWAN posted the fastest 23.55% CAGR through 2031.

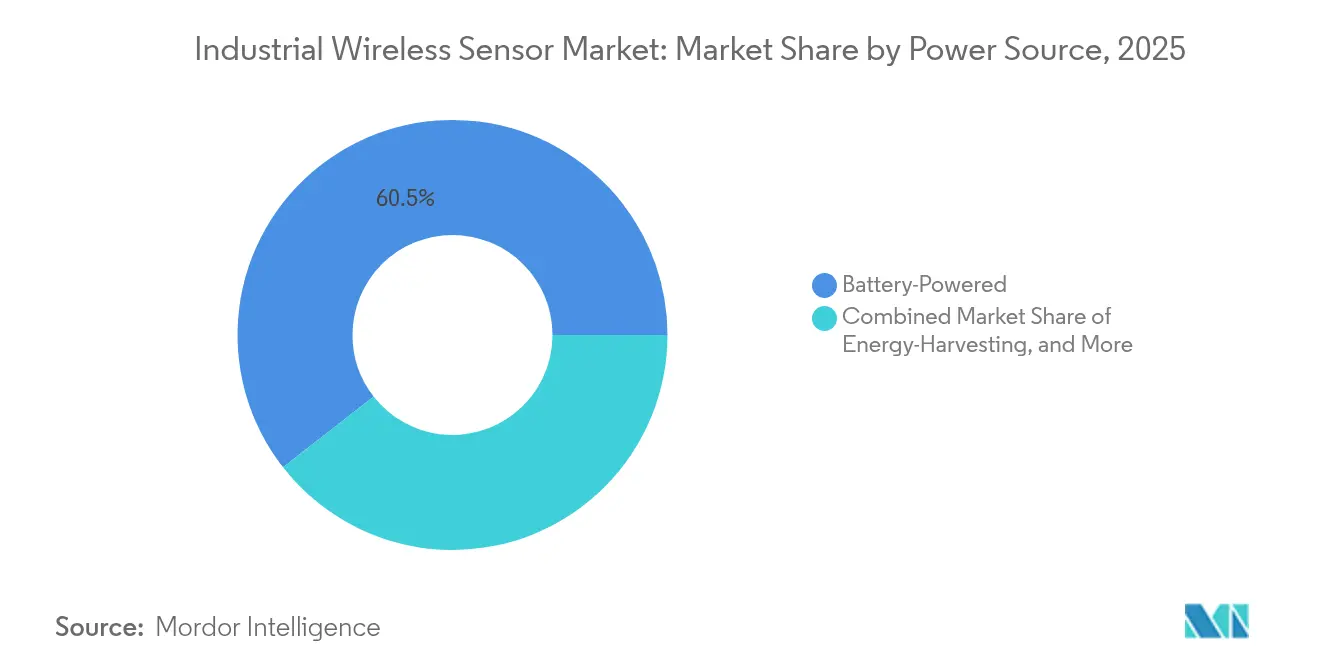

- By power source, battery-powered designs commanded 60.55% of industrial wireless sensors market share in 2025; energy-harvesting solutions will expand at a 15.55% CAGR to 2031.

- By end-user industry, oil & gas accounted for 31.05% revenue in 2025; mining and metals will accelerate at a 15.2% CAGR over the forecast horizon.

- By region, North America retained 34.35% revenue share in 2025; Asia Pacific will outpace all regions at a 13.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Wireless Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-to-cloud analytics demand surge | +2.8% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Retrofit digitalization of brown-field plants | +2.1% | North America and EU legacy facilities, expanding to APAC | Long term (≥ 4 years) |

| Low-power wide-area (LPWA) chipset price collapse | +3.2% | Global, strong benefit for APAC cost-sensitive markets | Short term (≤ 2 years) |

| Shift to predictive maintenance service models | +2.5% | Global, led by manufacturing and mining sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Edge-to-Cloud Analytics Demand Surge

Industrial operators now send only distilled insights instead of raw data to enterprise platforms, easing bandwidth burdens and cutting latency. Ultracompact sensors with embedded AI algorithms from firms such as TDK run machine-learning routines locally, shrinking transmitted payloads by up to 90%. Private 5G networks pair with edge servers to deliver sub-millisecond responsiveness for motion control, a milestone that broadens industrial wireless sensors market applicability into closed-loop automation. Factories deploying edge-to-cloud frameworks report 20-25% productivity gains through real-time anomaly detection. The capability aligns with sustainability goals by reducing compute energy requirements and enables predictive maintenance strategies that detect failures days in advance.

Retrofit Digitalization of Brown-Field Plants

Legacy facilities avoid disruptive rewiring costs by adding wireless nodes to equipment already running at capacity. ISA data show retrofit projects using wireless instrumentation achieve payback periods 60% shorter than wired equivalents. European chemical producers install vibration nodes on pumps and compressors to extend operating life and satisfy strict emission rules. Wireless attributes are compelling in hazardous zones where replacing or adding cables demands explosion-proof conduits, making wireless sensors a low-risk path to compliance. As brownfield estates outnumber new builds, retrofit activity will sustain double-digit volume growth across the industrial wireless sensors market well into the next decade.

Low-Power Wide-Area (LPWA) Chipset Price Collapse

LoRaWAN chipsets now cost under USD 5 in high-volume orders, down more than 70% from 2024 levels.[2]LoRa Alliance, “Smart Industry,” lora-alliance.org The price shift expands large-area monitoring in mining, utility networks, and agriculture, where previous cellular or mesh solutions were uneconomical. STMicroelectronics integrated sensing, processing, and LPWA connectivity into single MCUs that simplify design and compress the bill-of-materials expenses. Lower entry costs accelerate adoption in emerging markets, lifting the industrial wireless sensors market as labor-intensive industries digitize field operations.

Shift to Predictive Maintenance Service Models

OEMs increasingly sell performance outcomes rather than hardware, charging for guaranteed uptime based on data streams from machine-mounted sensors. Mining firms such as BHP report 75% reductions in unplanned downtime after deploying wireless vibration kits across haul trucks and crushers.[3]BHP Insights, “Artificial Intelligence Is Unearthing a Smarter Future,” bhp.comDigital twins generated from continuous sensor feeds enable virtual scenario testing that reduces maintenance interventions and extends equipment life. The service shift multiplies sensor node counts per asset, deepening penetration across the industrial wireless sensors market as capital-intensive sectors prioritize resilience and safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reliability concerns in RF-noisy industrial sites | -1.8% | Global, especially heavy manufacturing and steel production | Medium term (2-4 years) |

| Scarcity of OT-centric cybersecurity talent | -1.2% | North America and EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reliability Concerns in RF-Noisy Industrial Sites

Variable-frequency drives, welding lines, and power converters emit electromagnetic interference that degrades packet success rates beyond 90% reliability thresholds in some factories. Operators resort to redundant networks or revert to wired links for safety-critical loops. Mesh topologies, frequency hopping, and advanced antennas mitigate disruptions yet add cost and complexity. As interference remains prevalent in metals and automotive plants, operators apply strict qualification tests before approving wireless for real-time control, a cautionary stance that tempers portions of the industrial wireless sensors market expansion.

Scarcity of OT-Centric Cybersecurity Talent

IEC 62443 compliance demands skills that blend network security with process control expertise, a combination still rare in most labor pools. The U.S. Department of Homeland Security flagged the shortage as a critical infrastructure vulnerability and launched workforce initiatives to bridge the gap. Hiring challenges prolong project cycles and inflate integration costs, particularly in small-to-mid-size enterprises without dedicated security resources. Universities and vendors now partner on specialized curricula, yet talent pipelines will take years to satisfy growing demand as the industrial wireless sensors market proliferates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pressure Sensors Anchor Market Leadership

Pressure devices secured 26.65% industrial wireless sensors market share in 2025, reflecting their mandatory use for pipeline integrity and safety across process industries. Continuous pressure tracking avoids catastrophic leaks and satisfies stringent regulatory audits, justifying accelerated wireless retrofits where cabling through Class I Div 1 zones is cost-prohibitive. Vibration nodes grow fastest at 18.92% CAGR as predictive maintenance evolves from early pilots to corporate-wide standards, driving multi-sensor installations on rotating assets.

Temperature, flow, and gas categories secure broad adoption for environmental and quality control, while humidity and level units address niche but rising regulatory mandates in food, pharma, and tank storage. Imaging and biosensing remain nascent yet illustrate how edge AI will broaden sensing modalities within the industrial wireless sensors industry over the coming decade. Industrial buyers favor modular form factors and intrinsically safe housings that slash installation labor by up to 40%. Vendors now embed edge analytics to rank alarm severity, reducing false positives and maintenance tickets.

By Communication Protocol: Wi-Fi Scale Meets LPWAN Reach

Wi-Fi retained a 44.65% share due to its ubiquity in enterprise networks and alignment with IT security controls. Plants often deploy Wi-Fi in control rooms and indoor process areas where bandwidth enables high-definition video or advanced analytics streams. Yet LPWAN’s 23.55% CAGR indicates shifting preferences toward kilometer-scale coverage with multi-year battery life, critical for mines and pipeline corridors.

WirelessHART stays entrenched in petrochemical sites because it overlays existing HART loops, safeguarding decades of capital investment. ISA100.11a appeals to deterministic control scenarios despite higher engineering expense. Bluetooth and Zigbee service short-range mobile worker and building automation use cases. 5G NR industrial slices debut in ultra-low latency motion control, yet ecosystem maturity will dictate adoption pace.

By Power Source: Batteries Dominate, Harvesting Gains Momentum

Battery-Powered designs comprised 60.55% of 2025 shipments due to proven lithium chemistries that guarantee a 10-year operating life. However, energy harvesting grows at highest 15.55% CAGR as solar, vibration, and thermoelectric options eliminate truck rolls for remote nodes. Operators view harvesting as a pathway to net-zero maintenance in deserts, offshore platforms, and high-temperature furnaces, cutting lifetime ownership costs by double digits.

Hybrid architectures that juggle battery and harvested inputs extend deployment cycles, a feature increasingly standard in next-generation platforms. Gateways and routers remain wired for power and backhaul redundancy, creating anchor points for star-and-mesh topologies within the industrial wireless sensors market.

By End-User Industry: Oil & Gas Retains Demand Crown, Mining Accelerates

Oil & gas contributed 31.05% of 2025 revenue due to large-scale monitoring needs across pipelines, wellheads, and refineries, where hazardous zones complicate wired installs. Regulations obligate continuous leak detection, and wireless solutions prevent multimillion-dollar cabling projects, cementing oil & gas as the largest revenue base in the industrial wireless sensors market. Mining’s 15.2% CAGR reflects automation programs that rely on sensor-fed autonomy for haul trucks and drilling rigs.

Manufacturing verticals—automotive, food, chemical, pharma, and electronics—deploy wireless nodes for condition monitoring, quality assurance, and cleanroom integrity. Power utilities embed sensors in substations and renewable assets for real-time status checks. Healthcare and smart-building segments emerge as adjacent arenas as facility managers chase energy savings and occupant safety.

Geography Analysis

North America preserved a 34.35% revenue share in 2025, supported by sprawling oil pipelines, shale assets, and established brown-field factories embracing Industry 4.0 retrofits. U.S. policy spurs private 5G networks, and federal tax incentives for digital infrastructure accelerate deployments. Canadian miners deploy LoRaWAN over thousands of square kilometers to supervise autonomous haulage fleets, while Mexican maquiladoras adopt wireless nodes to enhance production traceability under nearshoring contracts.

Asia Pacific records the fastest 13.95% CAGR and will surpass North America before 2029. China targets 10,000 fully connected factories by 2027, requiring millions of sensors for process, environmental, and predictive functions. Local OEMs offer cost-optimized LPWAN devices, lowering entry barriers for tier-two manufacturers. Japanese automotive and electronics giants refine just-in-time workflows through edge-enabled sensors that spot quality drifts early.

Europe grows steadily as Industrie 4.0 policies and the EU Green Deal compel factories to audit energy and emissions. German process plants integrate WirelessHART with OPC UA gateways for holistic visibility. Nordic wind and solar farms blanket turbines with vibration and strain sensors to pre-empt mechanical faults under harsh climate loads. The continent maintains stringent cybersecurity mandates, elevating demand for IEC 62443-validated devices.

Regulatory Landscape

The regulatory environment for industrial wireless sensors is shaped by radio equipment compliance, spectrum access, and industrial cybersecurity expectations. In Europe, the European Commission published Commission Implementing Decision (EU) 2025/893 in May 2025 to support harmonised standards for wireless technologies used by short range devices and wideband data transmission systems. This affects the conformity pathways for Wi-Fi, LPWAN, and other industrial radios sold across EU markets.

Standards activity is also tightening requirements for coexistence, deterministic networking, and security. EN IEC 62657-4:2025 (published May 2025) codifies concepts for central coordination of industrial wireless applications to manage coexistence in dense plants. In the United States, the FCCs 900 MHz band rule changes that became effective in April 2026 strengthen the case for private industrial broadband networks. On the industrial networking side, IEEE/IEC 60802-2026 (released June 2026) defines time-sensitive networking profiles for industrial automation, and IEEE 802.15.4ae-2026 (published May 2026) adds MAC-level updates including Ascon cryptographic algorithms, reinforcing security-by-design expectations for low-rate industrial sensor networks.

Value Chain Analysis

The industrial wireless sensor value chain begins with upstream semiconductors (sensing elements, MCUs/SoCs, radios, secure elements, and power-management ICs) and materials (enclosures, intrinsically safe components, batteries, or harvesting transducers). These feed device OEMs that package sensors and embedded firmware, followed by gateway and edge-compute suppliers that translate field protocols (Wi-Fi, LPWAN, WirelessHART, ISA100.11a, and others) into plant networks and cloud connectors. Interoperability standards influence architecture choices across these tiers, including IEEE 1451.0-2024 for smart transducer interfaces and common data-sheet formats (TEDS), and IEEE 1451.5.5 for LoRa smart sensor interfaces spanning end devices, gateways, and server-side APIs.

Midstream system integrators and industrial automation vendors increasingly bundle sensors with commissioning, cybersecurity hardening, and lifecycle services, shifting value capture toward managed connectivity, performance assurance, and data integration into SCADA, historians, and analytics. Downstream, end users in oil and gas, manufacturing, mining, and utilities procure through direct enterprise deals, automation-channel partners, and industrial distributors, with deployment labor, site RF planning, and security compliance as recurring cost drivers. Supply constraints and qualification friction can also arise from long-lifecycle component requirements (industrial temperature ranges and ruggedization) and from the need to validate coexistence and reliability in RF-noisy facilities. In practice, standards-led interfaces and centralized coordination methods reduce integration risk across multiple supplier layers.

Competitive Landscape

Incumbent automation majors—ABB, Siemens, and Rockwell Automation—bundle sensing, control, and analytics in vertically integrated stacks, raising customer switching costs. Siemens’ AI foundation models and virtual PLCs expand addressable use cases, while ABB’s Margo initiative seeks open edge application layers. Competition remains moderate as top players collectively hold less than 50% revenue, leaving room for semiconductor challengers and specialized connectivity firms to grow.

Chipmakers such as STMicroelectronics, NXP, and Texas Instruments push system-on-chip innovations that shrink board area, lower power, and integrate secure elements. STMicroelectronics’ SESIP-3 certified STM32WBA6 MCU exemplifies how built-in crypto and multi-protocol radios serve rising cybersecurity and flexibility needs.[4]IoT Now, "STMicroelectronics' new integrated STM32WBA6 wireless microcontrollers combine extra features and performance with power efficiency.", iot-now.com Qualcomm collaborates with Honeywell to fuse AI inference engines with proprietary sensing technologies, aiming to shorten edge decision loops and open cross-licensing revenue streams. These alliances illustrate convergence between IT silicon roadmaps and operational technology requirements, reshaping supplier power within the industrial wireless sensors market.

Niche specialists address protocol interoperability and energy harvesting. Firms developing Matter-compliant gateways position for standardization tailwinds, while energy harvesting pioneers co-design sensors with battery manufacturers to deliver maintenance-free nodes. Competitive intensity fuels rapid feature cycles but also drives consolidation prospects as larger players acquire niche IP to complete portfolios.

Industrial Wireless Sensor Industry Leaders

-

ABB Ltd.

-

Rockwell Automation Inc.

-

Honeywell International Inc.

-

Siemens AG

-

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunity is scaling wireless condition monitoring and predictive maintenance in asset-intensive sectors where vibration and pressure measurements directly shape safety and uptime decisions. In July 2026, IMI secured a contract in Oman to supply more than 500 battery-powered triaxial vibration sensors (TWTG NEON) with condition monitoring software. The award supports production-scale rollouts for refinery rotating equipment and expands the addressable footprint for packaged sensor-plus-software offerings in hazardous and hard-to-wire zones.

Another whitespace involves deterministic and mobility-tolerant industrial wireless that supports operational continuity across large industrial sites, ports, and mining complexes, where connectivity gaps can disrupt control systems. Cisco cited a deployment of Ultra-Reliable Wireless Backhaul (URWB) with Multipath Operations at an Amazon Port in Brazil to address connectivity interruptions that triggered shutdowns, pointing to demand for higher-reliability wireless backhaul and edge connectivity layers between sensor networks and control or analytics platforms. Asset-tracking and logistics workflows within industrial campuses are also converting into measurable productivity projects, with Sensolus deployments such as Vaillant tracking 1,600 carts at its Nantes factory (May 2026). These implementations create pull-through demand for low-power trackers, gateways, and integration tooling that ties location and condition data into maintenance and operations systems.

Recent Industry Developments

- July 2026: IMI secured a contract to supply over 500 TWTG NEON battery-powered triaxial vibration sensors and SolidRed condition monitoring software to a major refinery operator in Oman. The award underscores ongoing scale-up of wireless condition monitoring in refineries, supporting larger node counts per site and tighter linkage between sensor hardware and analytics software.

- May 2025: Emerson launched Project Beyond, a software-defined operations platform integrating AI orchestration and zero-trust security to unify legacy automation islands. The move strengthens end-to-end edge-to-cloud offerings where wireless sensor data, gateways, and cybersecurity are delivered as a unified modernization stack.

- May 2024: Rockwell Automation announced a strategic partnership with Everactive to integrate batteryless, energy-harvesting wireless sensors into Rockwells digital automation platforms for industrial condition monitoring. The partnership expands maintenance-free sensor options and accelerates integration of self-powered sensing into broader OT software environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers wireless sensors used in industrial sites to measure process and asset conditions and transmit readings over wireless links to monitoring, control, or analytics systems. It includes sensor nodes used across factories, process plants, utilities, and similar operating environments.

Scope exclusions: consumer smart-home sensors, stand-alone personal gadgets, and wired industrial transmitters are excluded from this sizing.

Segmentation Overview

-

By Product Type

- Temperature Sensor

- Pressure Sensor

- Flow Sensor

- Gas Sensor

- Humidity Sensor

- Vibration Sensor

- Level Sensor

- Imaging Sensor

- Biosensor

- Other Product Types

-

By Communication Protocol

- WirelessHART

- ISA100.11a

- Wi-Fi

- Bluetooth / BLE

- Zigbee

- 6LoWPAN / Thread

- LPWAN (LoRa, Sigfox)

- 5G NR (Rel-17 Industrial)

-

By Power Source

- Battery-Powered

- Energy-Harvesting

- Wired-Powered Gateways

-

By End-user Industry

-

Manufacturing

- Automotive

- Food and Beverage

- Chemicals

- Pharmaceuticals

- Electronics and Semiconductor

- Oil and Gas

- Energy and Power

- Mining and Metals

- Healthcare Facilities

- Smart Buildings and Infrastructure

- Other Industries

-

Manufacturing

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

APAC

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is actually installed in plants and how it is bought, used, and maintained, so the model reflects real industrial purchasing cycles. For grounding, we rely on public sources such as US Census manufacturing data, Eurostat industrial production series, International Energy Agency statistics, International Telecommunication Union connectivity indicators, and standards and guidance published by bodies such as NIST.

To turn that foundation into sizing inputs, we also review company annual reports and investor presentations, customs and trade statistics for related components where helpful, and credible industry press that tracks automation spending and wireless adoption. In a few places, paid subscriptions are used for company financials and patent databases to validate product positioning and timing of technology shifts. These desk sources are not exhaustive, and we checked many other references to fill gaps, validate numbers, and clarify assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test adoption assumptions and the pricing logic behind wireless sensor nodes across discrete and process industries. We speak with a balanced mix of sensor manufacturers, industrial automation ecosystem participants, system integrators, and end users, then reconcile differences across regions so one geography does not over-influence the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 46% |

| Mid tier: 56% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 18% | Managers: 43% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool approach where industrial automation activity and wireless penetration are used to reconstruct the addressable installed base and annual additions, which are then converted to revenue using typical device and system pricing. To keep totals realistic, the output is cross-checked with selective bottom-up approximations such as sampled average selling prices multiplied by shipment proxies, along with channel checks from integrators and large end users.

Key inputs that shape the model include the pace of Industry 4.0 and IIoT rollouts, plant-level upgrade cycles, adoption of low-power wireless protocols in industrial settings, replacement rates driven by battery life and maintenance intervals, and the mix shift between process industries and discrete manufacturing. Where local data is thin, gaps are handled by applying region-level adoption ranges validated in interviews and by aligning with observable industrial production and capex trends.

For forecasting, scenario analysis is used because adoption often moves in steps when plants standardize on a protocol or when safety and cybersecurity requirements change. The final trajectory is adjusted using expert consensus on how fast wireless displaces incremental wiring in brownfield sites versus new builds.

Data Validation & Update Cycle

Outputs are checked against independent signals, including regional industrial production trends, automation spending direction, and the implied device volumes that the revenue number would require. When a result looks unusual, the assumptions are revisited, the math is rechecked, and follow-up calls are triggered to confirm whether the variance reflects a real market shift or a modeling artifact.

Before sign-off, the model and notes go through a multi-step analyst review so definitions, currency handling, and time alignment are consistent across regions. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp pricing changes, major regulatory moves, or step-changes in industrial investment. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Industrial Wireless Sensors Market Size Compared With Other Published Estimates

Published numbers for industrial wireless sensors often differ because each publisher draws the line around what counts as a sensor, which industrial sites are included, and which year is treated as the anchor for pricing and adoption. Differences also show up when one estimate emphasizes networks and gateways, while another focuses mainly on sensor nodes.

Key gaps usually come from scope and timing choices, such as whether industrial wireless sensor networks are counted as a broader system market, how fast average selling prices are assumed to decline, and whether forecast growth is built from cautious adoption ranges or from aggressive Industry 4.0 rollout assumptions. A practical spread is seen when 2023 to 2024 base years are converted forward without re-validating penetration and replacement cycles, and when currency timing is not aligned across regions, which is handled differently in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.03 B (2026) | |

| Global Consultancy A | USD 5.74 B (2024) | Uses an industrial wireless sensor network framing with a 2023 to 2024 base and a shorter horizon, so the value reflects earlier adoption levels and may include broader network components that do not map one-to-one to sensor node revenue. |

| Industry Research Publisher B | USD 5.90 B (2024) | Starts from a 2024 base year and extends to 2034, which can shift the current value depending on what is grouped under industrial wireless sensors and how price erosion and penetration are rolled forward from the base year. |

The table shows that the spread is mainly explained by base-year selection and whether the market is treated as sensor-node revenue versus a wider network and component bundle. By keeping the demand pool tied to industrial adoption drivers and then cross-checking with practical price and volume signals, the final number stays traceable to clear assumptions that can be revisited as the market changes.

Key Questions Answered in the Report

What is the projected size of the industrial wireless sensors market by 2031?

It is forecast to reach USD 17.04 billion by 2031, expanding at a 13.48% CAGR.

Which product segment currently leads the industrial wireless sensors market?

Pressure sensors held 26.65% market share in 2025, driven by pervasive use in oil & gas safety monitoring

Why are LPWAN technologies growing so quickly in the industrial wireless sensors industry?

LPWAN chipset prices have fallen more than 70% since 2024, enabling long-range, low-power deployments that cost less than mesh or cellular alternatives.

Which region will see the fastest growth in industrial wireless sensors adoption?

Asia Pacific will register a 13.95% CAGR through 2031, propelled by China’s push for fully connected smart factories.

What is the main barrier to wider deployment of wireless sensors in heavy manufacturing?

Electromagnetic interference from high-power equipment can cause packet loss rates above acceptable thresholds, prompting cautious adoption for safety-critical loops.

How are vendors addressing cybersecurity concerns in wireless sensor networks?

They integrate hardware roots of trust, adhere to IEC 62443 standards and bundle zero-trust architectures to offset the scarcity of OT cybersecurity talent.

Page last updated on: