Battery Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.22 Billion |

| Market Size (2031) | USD 10.48 Billion |

| Growth Rate (2026 - 2031) | 10.27% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

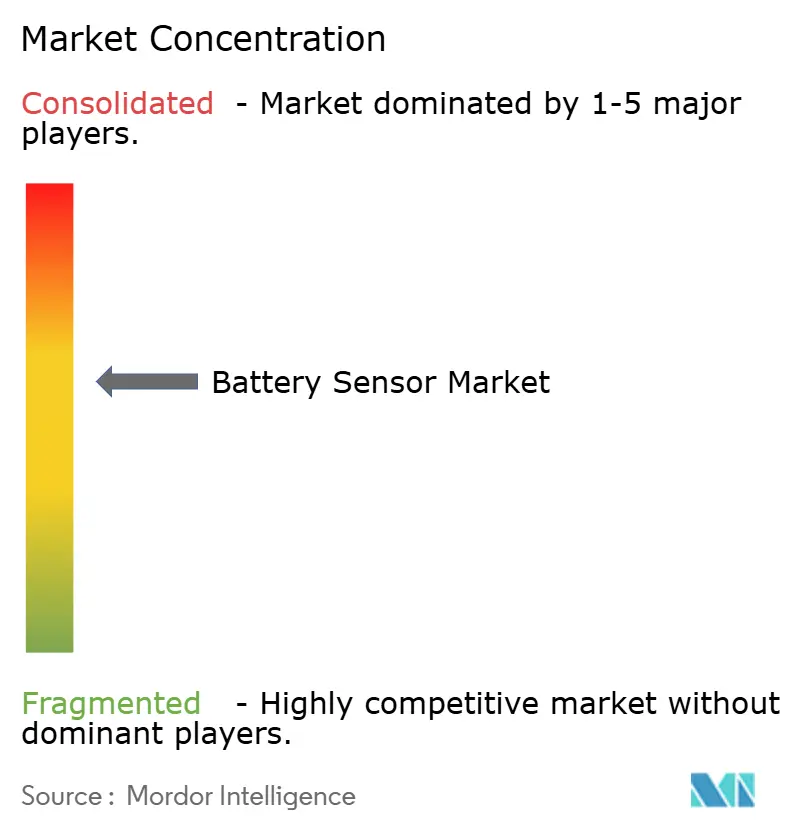

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Sensor Market Analysis by Mordor Intelligence

The Battery sensor market size is expected to increase from USD 5.64 billion in 2025 and USD 6.22 billion in 2026 to reach USD 10.48 billion by 2031, growing at a CAGR of 10.27% over 2026-2031. Demand is being buoyed by rising electric-vehicle volumes, utility-scale energy-storage roll-outs, and tighter functional-safety mandates that force pack designers to adopt multi-sensor fusion. Automakers are shifting from discrete voltage taps to integrated sensor hubs, trimming harness mass and assembly hours, while grid operators are embedding impedance spectroscopy in containerized systems to extend useful life. Competition is intensifying in the Battery sensor market as wireless architectures threaten wired incumbency and fiber-optic arrays gain traction in solid-state battery pilots. Meanwhile, price volatility in magnetic-core alloys and calibration overhead in resistive shunts create procurement and engineering headwinds.

Key Report Takeaways

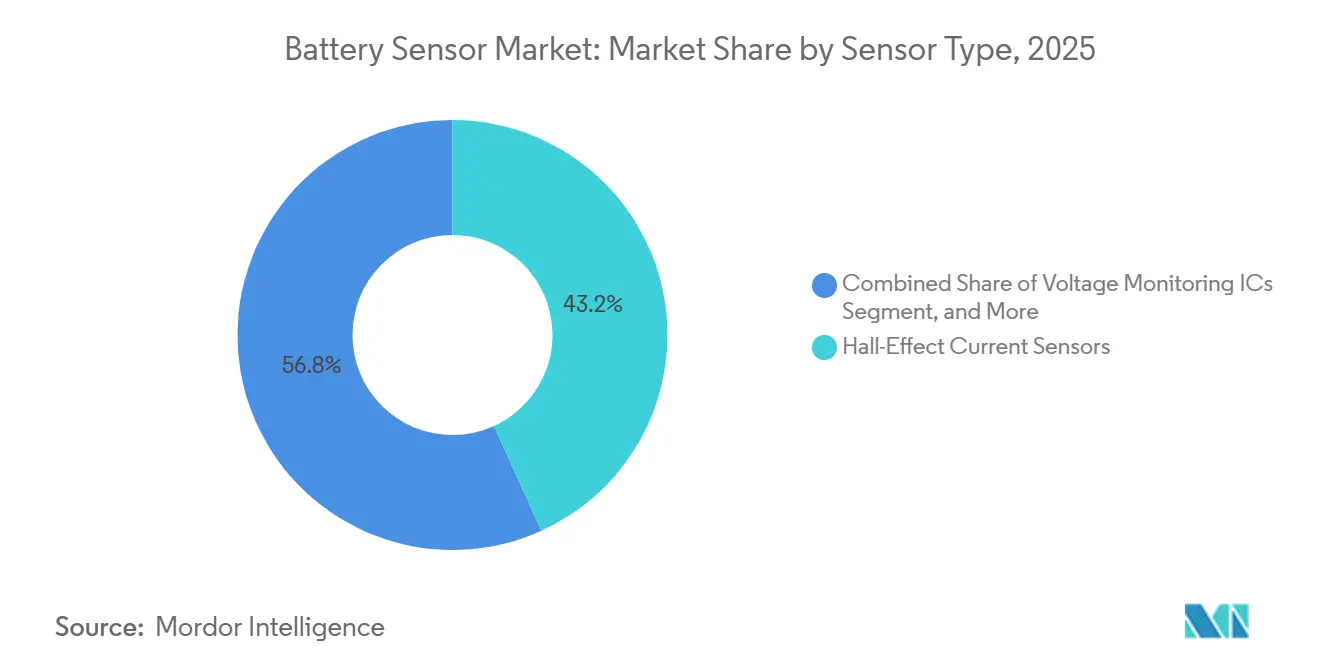

- By sensor type, Hall-effect current sensors led with 43.2% of the battery sensor market share in 2025, while fiber-optic sensors are projected to expand at an 11.9% CAGR through 2031.

- By technology, closed-loop isolated sensors captured 40.5% revenue of the battery sensor market in 2025, and wireless architectures are advancing at an 11.7% CAGR to 2031.

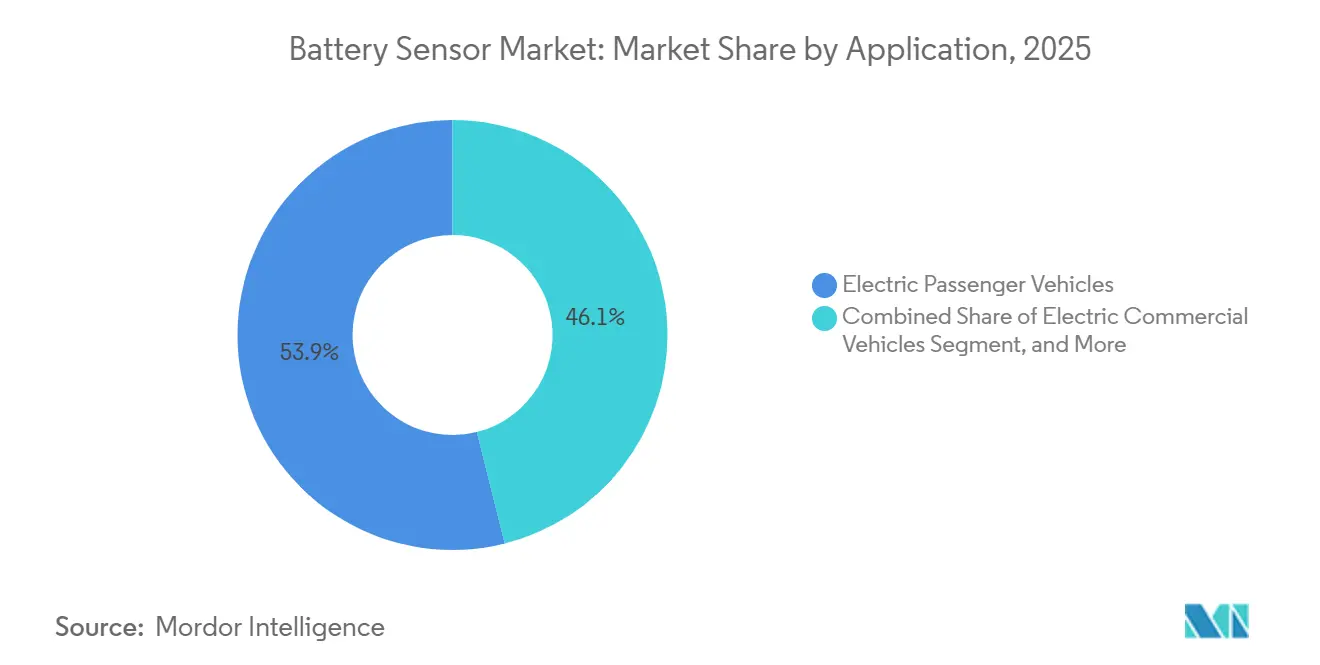

- By application, electric passenger vehicles accounted for 53.9% of the battery sensor market size in 2025, and stationary energy-storage systems are forecast to grow at an 11.5% CAGR through 2031.

- By end-user industry, automotive players held 46.7% share of the battery sensor market size in 2025, whereas the energy and utilities segment is set to record an 11.4% CAGR up to 2031.

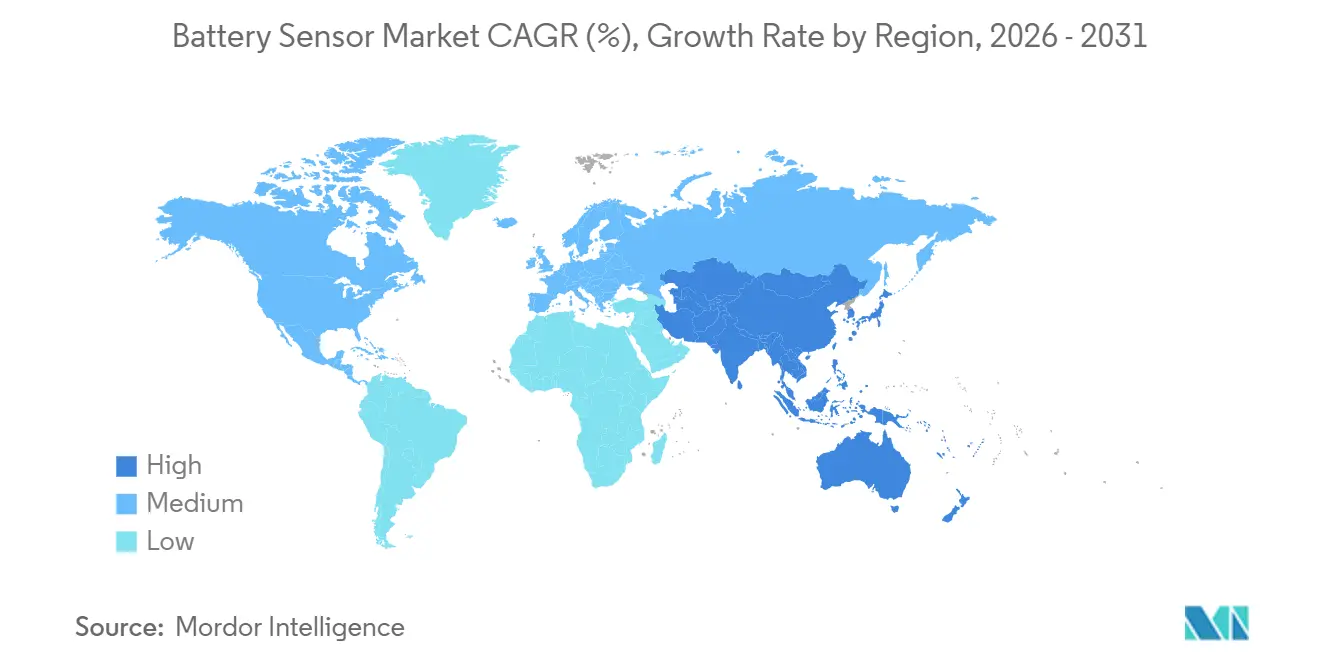

- By geography, Asia-Pacific commanded 33.3% revenue share of the battery sensor market in 2025 and is on track for an 11.1% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Battery Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Production Surge And Stringent xEV Battery-Safety Mandates | +2.8% | Global, led by Asia-Pacific and Europe | Medium term (2-4 years) |

| Rapid Growth Of Utility-Scale Energy-Storage Installations | +2.3% | North America and Asia-Pacific, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Falling Cost And Accuracy Gains In Hall-Effect Current Sensors | +1.5% | Global | Short term (≤ 2 years) |

| Standardization Of ISO 21498 Battery Monitoring Interfaces | +1.2% | Global, early uptake in Europe and North America | Long term (≥ 4 years) |

| Integration Of Cell-Level Fiber-Optic Sensing In Solid-State Battery Pilots | +0.9% | Asia-Pacific and North America R&D clusters | Long term (≥ 4 years) |

| Adoption Of Wake-On-CAN Ultra-Low-Power Sensing For Micro-Mobility Packs | +0.6% | Asia-Pacific and Europe urban hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Production Surge And Stringent xEV Battery-Safety Mandates

China’s GB38031-2025 standard obliges passenger cars and fleets to detect thermal runaway within five minutes, forcing a shift from simple thermistor strings to multi-sensor fusion that couples Hall-effect current, fiber-optic temperature, and MEMS pressure channels.[1]GB Standards, “GB38031-2025 Electric Vehicle Battery Safety Standard,” gb-standards.com The ISO 21498 interface, ratified in 2024, adds bidirectional data paths between battery management systems and vehicle control units, enabling real-time power limitation that curbs over-discharge events.[2]ISO, “ISO 21498 Battery Monitoring Interfaces,” iso.org ZOE Energy Storage fielded a four-parameter detection stack in 2025 that identifies runaway 20 times earlier than legacy packs, illustrating how regulatory pressure is reshaping design rules.

Rapid Growth Of Utility-Scale Energy-Storage Installations

Alliant Energy’s 200 MW-400 MWh site in Wisconsin, commissioned in March 2026, relies on 12,000 monitored cells across 50 containers, highlighting the scale of sensor deployment in modern grids.[3]Alliant Energy, “200 MW LFP Storage Installation,” alliantenergy.com SSE’s 100 MW Ferrybridge system uses impedance spectroscopy to flag internal resistance drift and lengthen service life. Wireless monitors at Georgia Power’s 65 MW facility removed two kilometers of copper harness, cutting installation outlay by USD 120,000. These installations show how sensor-enabled predictive maintenance underpins lower levelized cost of storage.

Falling Cost And Accuracy Gains In Hall-Effect Current Sensors

Fabrication on 180 nm CMOS has pushed Hall sensor average selling prices down 18% since 2024 while boosting accuracy past 0.5% error at temperature extremes.[4]Allegro MicroSystems, “ACS37017 Coreless Hall Sensor,” allegromicro.com Allegro’s ACS37017, launched in February 2026, achieves 0.55% total error without magnetic cores, aligning with ISO 26262 ASIL C accuracy needs. Infineon’s TLE4978 hybrid Hall-coil variant blends DC and high-frequency measurement, detecting lithium plating via harmonic analysis during 350 kW charging.[5]Infineon Technologies, “TLE4978 Hybrid Hall-Coil Sensor,” infineon.com The shrinking price gap between Hall sensors and shunt solutions is accelerating their uptake in the Battery sensor market.

Standardization Of ISO 21498 Battery Monitoring Interfaces

A common protocol eliminates the proprietary gateways that once walled off state-of-charge data, lowering aftermarket diagnostic cost by 25%. Texas Instruments’ BQ79826Z-Q1 embeds impedance spectroscopy compliant with the new call-and-response structure, flagging internal shorts 72 hours in advance. NXP’s BMx7318 streams 18-channel cell metrics on CAN FD at 5 Mbps, feeding cloud analytics that anticipate warranty claims with 92% accuracy. Although accreditation labs remain scarce outside Germany and Japan, OEMs value the lifetime data transparency unlocked by the standard.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide Temperature-Drift And Offset Errors In Low-Cost Shunt Solutions | -1.8% | Global, acute in cost-sensitive Asia-Pacific and South America | Short term (≤ 2 years) |

| Volatile Pricing And Supply Of Ferrite Or Permalloy Magnetic Cores | -1.3% | Global, with pressure in North America and Europe | Medium term (2-4 years) |

| EMC Compliance Hurdles For 1 MHz Isolated Current-Sensor Modulation | -0.7% | Europe and North America | Medium term (2-4 years) |

| Scarcity Of Certification Labs For Wireless Battery-Sensor Protocols | -0.5% | Global, regions lacking ISO 17025 sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wide Temperature-Drift And Offset Errors In Low-Cost Shunt Solutions

Automotive temperature cycles induce 50 µV °C⁻¹ offset drift in bare shunts, translating into 3% range-prediction error over vehicle life. External op-amps with 120 dB common-mode rejection are required, adding USD 1.20 in components and offsetting shunts’ perceived savings. EMI from 800 V inverters further pushes total error beyond 0.5%, breaching ISO 21498 accuracy limits.

Volatile Pricing And Supply Of Ferrite Or Permalloy Magnetic Cores

Neodymium-praseodymium spot quotes jumped 6.5% in one week during early 2025, unsettling cost models for closed-loop Hall modules. LEM’s Hybrid Supervising Unit slashes core metal by 60% by activating Hall sensing only during transients. Infineon’s coreless Hall plates skirt the material issue entirely, albeit with a 20% sensitivity trade-off.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Fiber-Optic Arrays Challenge Hall Dominance

Hall-effect devices owned 43.2% Battery sensor market share in 2025, thanks to contactless bidirectional measurement vital for regenerative braking. Fiber-optic sensors are on an 11.9% CAGR path to 2031, propelled by solid-state battery pilots that require ceramic-safe, distributed temperature reading. Shunts stay relevant in consumer gadgets where ±1% suffices, yet ISO 21498 pushes automotive platforms toward Hall accuracies. Texas Instruments’ 18-channel voltage IC, shipping since August 2025, resolves 1 mV differentials, reinforcing integrated monitoring roadmaps.

Fiber Bragg grating strings are gaining in utility-scale systems, resisting electromagnetic interference that plagues thermistors near high-voltage inverters. MEMS pressure chips, such as Honeywell’s 0.25%-FS BPS line, detect 2 kPa gas buildup well before exothermic escalation. Growth is tempered by the lack of automotive-rated fiber connectors that survive 3,000 matings and -40 °C to 125 °C cycles, a gap both Corning and Prysmian address with rugged LC variants.

By Technology: Wireless Architectures Disrupt Wired Incumbents

Closed-loop isolated designs delivered 40.5% revenue in 2025, driven by the increasing demand for drift-free 1,000 A sensing in 800 V platforms, which are critical for high-performance electric vehicles and industrial applications. Wireless nodes are forecast to grow at an 11.7% CAGR, as Dukosi’s C-SynQ technology demonstrated a 15% reduction in pack mass and a 40% decrease in assembly time, particularly benefiting commercial fleet operators. NXP’s ultra-wideband platform offers precise 10 cm 3-D cell location capabilities, simplifying warranty forensics by enabling quick identification and mapping of faulty units, which is crucial for minimizing downtime and operational inefficiencies.

Digital output sensors utilizing CAN FD and I²C protocols are expanding rapidly, with Infineon’s XDM700-1 sensor transferring 18-channel data at 5 Mbps, catering to the growing need for high-speed data communication in modern battery management systems. Meanwhile, analog variants are increasingly relegated to legacy industrial UPS roles due to their limited capabilities. Renesas’ DA14533 sensor supports a 10-year coin-cell lifetime for Bluetooth Low Energy sensors, making it an ideal solution for e-scooters and other compact mobility devices. However, the dual certification process for CAN-to-Bluetooth gateways has been identified as a bottleneck, extending product launch timelines by approximately 9 months, posing challenges for manufacturers aiming to meet market demand swiftly.

By Application: Stationary Storage Outpaces Passenger Vehicles

Electric passenger cars accounted for 53.9% of the Battery sensor market in 2025, driven by the increasing adoption of electric vehicles globally. Stationary storage, however, is advancing at an 11.5% CAGR as grid codes require impedance tracking and gas detection, ensuring compliance with evolving energy regulations. IONCOR’s Pack Long module integrates ASIL C electronics to meet the needs of bus and truck OEMs requiring ±3% SOC precision, addressing the growing demand for accurate state-of-charge monitoring in commercial vehicles.

Consumer electronics maintain volume but rely on advanced fuel gauges, like Nordic Semiconductor’s adaptive model, which has trimmed degradation by 15% over 3 years, enhancing battery performance and longevity. Industrial UPS conversions from lead-acid to lithium-ion rely on diagnostics that Voltica Diagnostics shows detect 72% of early-life failures, providing a reliable solution for industrial power backup systems.

By End-User Industry: Energy Sector Challenges Automotive Leadership

Automotive users held a 46.7% share in 2025, driven by advancements in battery management systems and the increasing adoption of electric vehicles. However, energy and utilities are projected to grow at an 11.4% CAGR through 2031, as technologies like impedance spectroscopy and cloud analytics demonstrate a 13% life extension, validated through Ricardo field pilots. Telecommunications firms are transitioning from diesel gensets to lithium-ion backups, where the ability to detect single-cell failures is critical for maintaining operational reliability.

Industrial campuses are increasingly deploying microgrids integrated with battery buffers, leveraging OxMaint’s platform, which predicts 92% of thermal events and extends battery life by 3.5 times. Consumer electronics brands are embedding machine-learning SOC models at a growing rate, achieving significant improvements by reducing residual error to below 0.01 MAE, enhancing device performance and reliability.

Geography Analysis

Asia-Pacific generated 33.3% of the battery sensor market revenue in 2025 and is set for an 11.1% CAGR to 2031 as GB38031-2025 makes thermal-runaway detection compulsory. Japanese vendors, exemplified by B-and-Plus’s April 2026 wireless monitor, scrap harnesses in automated guided vehicles, improving swap speed. South Korea specifies impedance spectroscopy for 350 kW charging, satisfied by NXP’s BMA7418 chipset. India’s above 50 MW renewable projects mandate battery energy-storage add-ons, spurring demand for cost-optimized sensors.

North America and Europe prioritize ISO 26262 ASIL D dual-channel current sensing. Germany champions coreless Hall sensors, with Infineon trimming EUR 0.80 (USD 0.85) per unit by deleting ferrite cores. The United Kingdom’s Ferrybridge site projects an 8% lower levelized storage cost via impedance spectroscopy. U.S. utilities in Wisconsin and Georgia illustrate the cost case for wireless monitors that wipe out thousands of dollars in copper.

The Middle East and Africa adopt battery storage in megaprojects such as Saudi Arabia’s NEOM, specifying hydrogen gas detection to tackle high-ambient heat. South Africa’s renewables program turns to shunt solutions at 40% lower cost where 1% accuracy suffices. South American adoption is concentrated in Brazil, where NOM-194-SCFI-2015 aligns with digital monitors built on CAN FD.

Competitive Landscape

The Battery sensor market remains moderately fragmented. Leading suppliers, including Texas Instruments, Infineon Technologies, Allegro MicroSystems, NXP Semiconductors, and Analog Devices, dominate the market, while opportunities remain for smaller, niche players to establish a foothold. Texas Instruments has been actively expanding its portfolio of monitoring ICs, securing design wins across multiple segments. Analog Devices has introduced advanced solutions, such as the ADBMS2970, which provides redundant impedance readings to meet the stringent requirements of premium electric vehicle applications. Additionally, Infineon Technologies has been focusing on expanding its product portfolio with advanced battery management solutions, targeting high-growth markets such as electric vehicles and renewable energy storage systems.

Disruptors such as Dukosi and Volytica Diagnostics capitalize on wireless and analytics white space. Dukosi’s cell-level RF tag bypasses voltage taps, shrinking harness weight by 15%. Volytica’s SOBx algorithm localizes defects within 48 hours, allowing utilities to cut commissioning time by 35%. LEM’s hybrid shunt-Hall concept reduces magnetic-core dependence by 60% and has already shipped into European light commercial vehicles. Furthermore, startups are leveraging machine learning and AI-driven analytics to enhance battery performance monitoring, enabling predictive maintenance and reducing downtime for industrial and automotive applications.

Patent activity shows a pivot toward hybrid sensing that balances cost, accuracy, and material risk. Companies are increasingly investing in R&D to develop next-generation battery sensors capable of handling higher voltages and extreme operating conditions. For instance, advancements in solid-state battery technology are driving demand for sensors that can provide precise thermal and voltage readings. Additionally, the integration of IoT-enabled sensors is gaining traction, allowing real-time monitoring and data transmission to cloud platforms for advanced analytics. These trends are expected to shape the competitive landscape, with both established players and new entrants vying for market share in the forecast period.

Battery Sensor Industry Leaders

Allegro MicroSystems, Inc.

Asahi Kasei Microdevices Corporation

Melexis NV

LEM Holding SA

Sensata Technologies Holding plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nordic Semiconductor released Fuel Gauge v2.0 beta with adaptive state-of-health logic, reducing cell degradation by 15% over three years in consumer devices.

- April 2026: B-and-Plus launched a wireless battery monitor for automated guided vehicles, trimming pack mass by 12% in warehouse fleets.

- March 2026: Murata Manufacturing and QuantumScape initiated a collaboration to develop high-volume ceramic film production for solid-state batteries. Murata Manufacturing.

- March 2026: Infineon Technologies unveiled the TLE4978 hybrid Hall-coil sensor that detects lithium plating by measuring current harmonics above 10 kHz.

Global Battery Sensor Market Report Scope

The Battery Sensor Market Report is Segmented by Sensor Type (Hall-Effect Current Sensors, Shunt-Based Current Sensors, Voltage Monitoring ICs, Temperature Sensors, Fiber-Optic Battery Sensors, MEMS Pressure Sensors), Technology (Closed-Loop Sensors, Open-Loop Sensors, Digital Output, Analog Output, Wireless Battery Sensors), Application (Electric Passenger Vehicles, Electric Commercial Vehicles, Hybrid and Plug-in Hybrid Vehicles, Stationary Energy-Storage Systems, Consumer Electronics, Industrial UPS and Backup), End-User Industry (Automotive, Energy and Utilities, Consumer Electronics, Industrial and Manufacturing, Telecommunications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hall-Effect Current Sensors |

| Shunt-Based Current Sensors |

| Voltage Monitoring ICs |

| Temperature (NTC / PTC) Sensors |

| Fiber-Optic Battery Sensors |

| MEMS Pressure Sensors (Cell-Level) |

| Closed-Loop (Isolated) Sensors |

| Open-Loop Sensors |

| Digital (I2C / CAN / SENT) Output |

| Analog Output |

| Wireless Battery Sensors |

| Electric Passenger Vehicles |

| Electric Commercial Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| Stationary Energy-Storage Systems |

| Consumer Electronics |

| Industrial UPS and Backup |

| Automotive |

| Energy and Utilities |

| Consumer Electronics |

| Industrial and Manufacturing |

| Telecommunications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Hall-Effect Current Sensors | ||

| Shunt-Based Current Sensors | |||

| Voltage Monitoring ICs | |||

| Temperature (NTC / PTC) Sensors | |||

| Fiber-Optic Battery Sensors | |||

| MEMS Pressure Sensors (Cell-Level) | |||

| By Technology | Closed-Loop (Isolated) Sensors | ||

| Open-Loop Sensors | |||

| Digital (I2C / CAN / SENT) Output | |||

| Analog Output | |||

| Wireless Battery Sensors | |||

| By Application | Electric Passenger Vehicles | ||

| Electric Commercial Vehicles | |||

| Hybrid and Plug-in Hybrid Vehicles | |||

| Stationary Energy-Storage Systems | |||

| Consumer Electronics | |||

| Industrial UPS and Backup | |||

| By End-User Industry | Automotive | ||

| Energy and Utilities | |||

| Consumer Electronics | |||

| Industrial and Manufacturing | |||

| Telecommunications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Battery sensor market by 2031?

The Battery sensor market size is forecast to reach USD 10.48 billion by 2031, growing at a 10.27% CAGR between 2026 and 2031.

Which sensor type will grow the fastest through 2031?

Fiber-optic battery sensors are expected to post the highest growth at an 11.9% CAGR as solid-state pilots demand distributed, contactless temperature sensing.

Which geography offers the strongest growth potential?

Asia-Pacific leads on growth with an 11.1% CAGR, helped by China's GB38031-2025 safety mandate and rapid electric-vehicle production.

How are wireless technologies shaping competitive strategy?

Wireless battery sensors trim pack mass by 15% and assembly time by 40%, giving innovators like Dukosi an edge over wired incumbents.

What is driving sensor adoption in utility-scale storage?

Grid operators deploy impedance spectroscopy and multi-sensor fusion to extend battery life and meet reliability standards, boosting demand for high-accuracy sensors.

Which standard is harmonizing battery monitoring interfaces?

ISO 21498, published in 2024, sets common voltage and current accuracy benchmarks and lowers aftermarket diagnostics cost by 25%.

Page last updated on: