Electrochemical Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

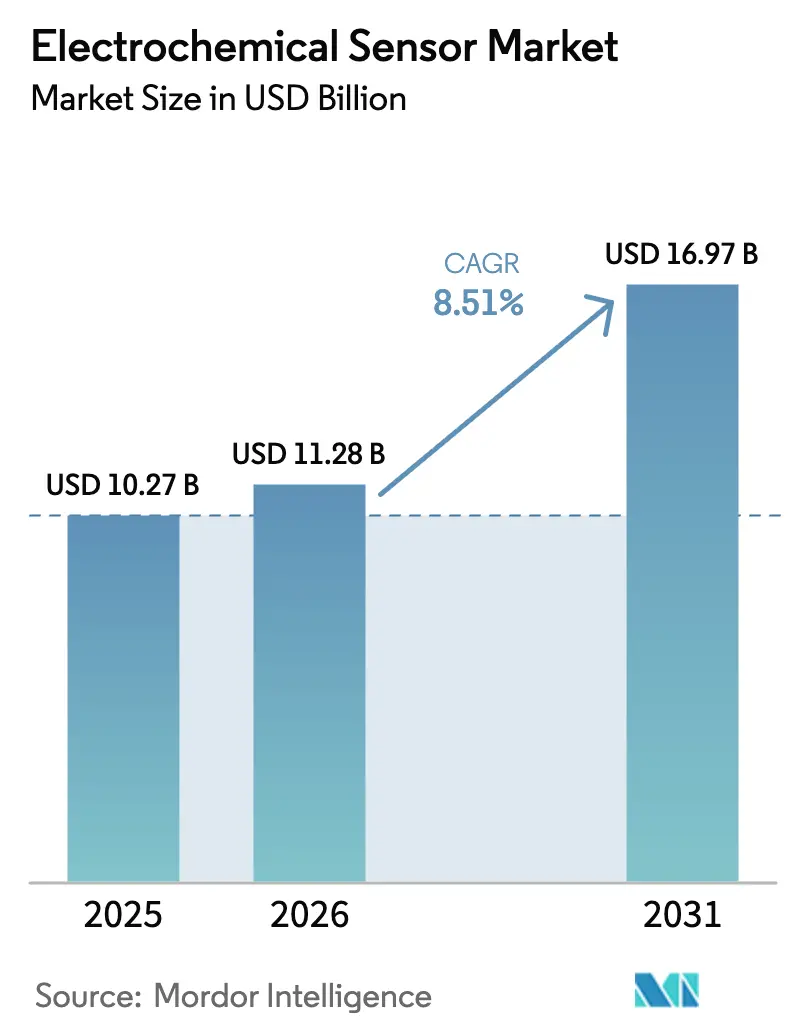

| Market Size (2026) | USD 11.28 Billion |

| Market Size (2031) | USD 16.97 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrochemical Sensor Market Analysis by Mordor Intelligence

The electrochemical sensor market size is expected to increase from USD 10.27 billion in 2025 to USD 11.28 billion in 2026 and reach USD 16.97 billion by 2031, growing at a CAGR of 8.51% over 2026-2031. Adoption is accelerating as regulatory authorities tighten real-time emissions rules, clinicians validate wearable glucose monitors for over-the-counter use, and semiconductor foundries embed micro-electromechanical systems (MEMS) transducers on single silicon dies. Robust capital spending by petrochemical, mining, and food-processing operators continues to buoy demand for industrial safety, while consumer electronics brands integrate multi-analyte arrays into smartwatches and fitness patches. Vendors that can combine ATEX- or IECEx-approved housings with digital self-diagnostics are securing premium contracts, as the feature set reduces annual calibration visits by up to 40%. Printed carbon-ink electrodes, although limited to six-month lifetimes, are enabling network density for urban air-quality programs to reach sub-1-kilometer resolution, a level previously unattainable with reference analyzers that cost an order of magnitude more.

Key Report Takeaways

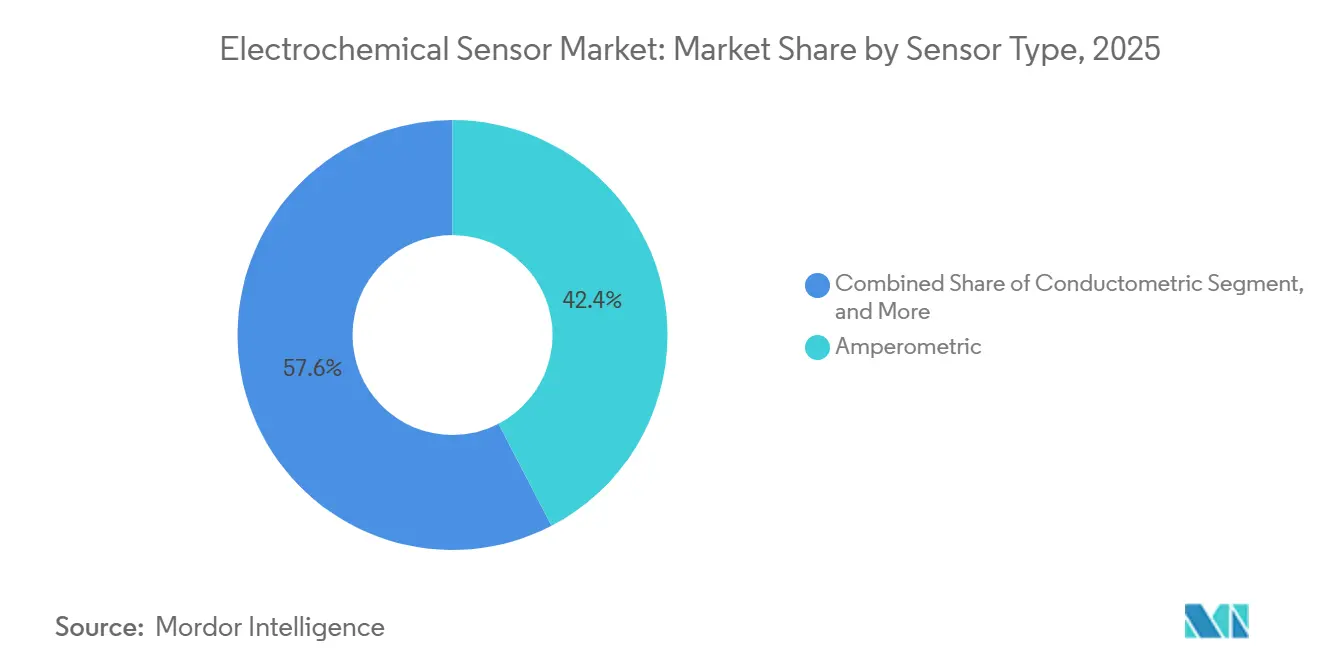

- By Sensor type, amperometric sensors led with 42.38% electrochemical sensor market share in 2025, while conductometric designs are advancing at a 9.43% CAGR through 2031.

- By end-user industry, the healthcare segment led with 29.71% electrochemical sensor market share in 2025, while environmental monitoring and other industries are advancing at a 9.74% CAGR through 2031.

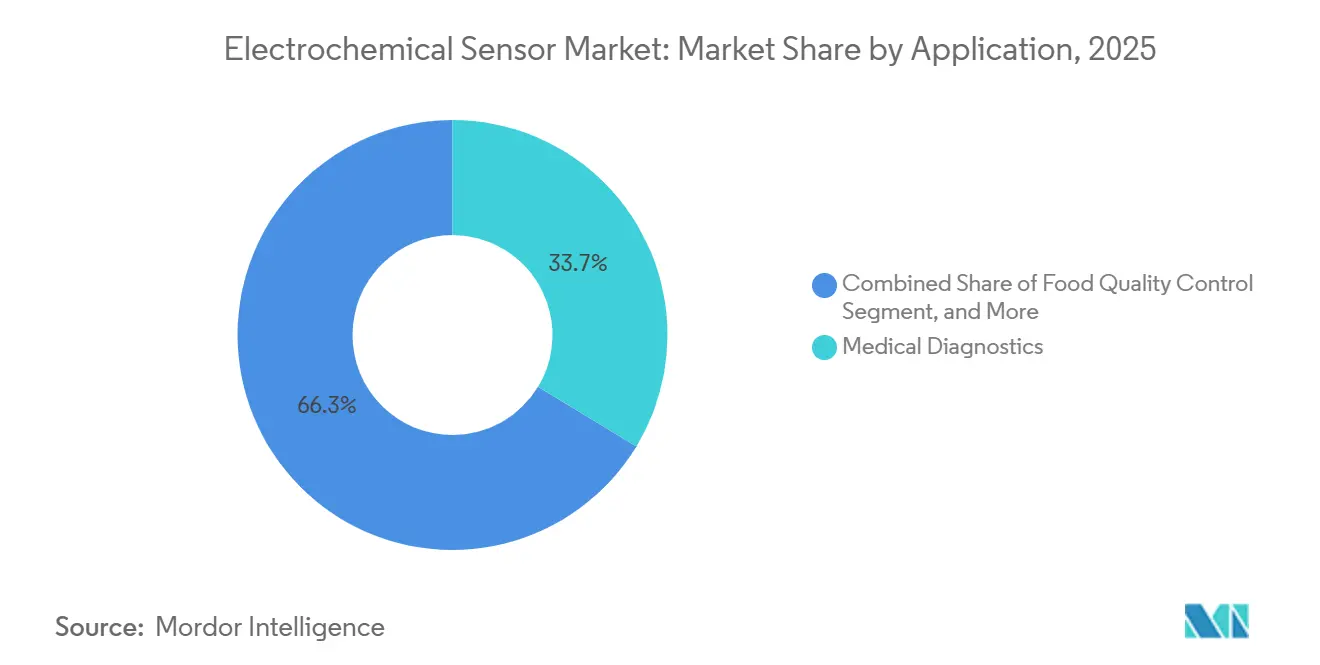

- By application, medical diagnostics captured 33.67% of demand in 2025; wearable and consumer wellness devices are forecast to expand at a 9.79% CAGR through 2031.

- By technology, solid-state architectures accounted for 37.89% of shipments in 2025, whereas MEMS-based sensors are the fastest-growing segment at a 9.39% CAGR through 2031.

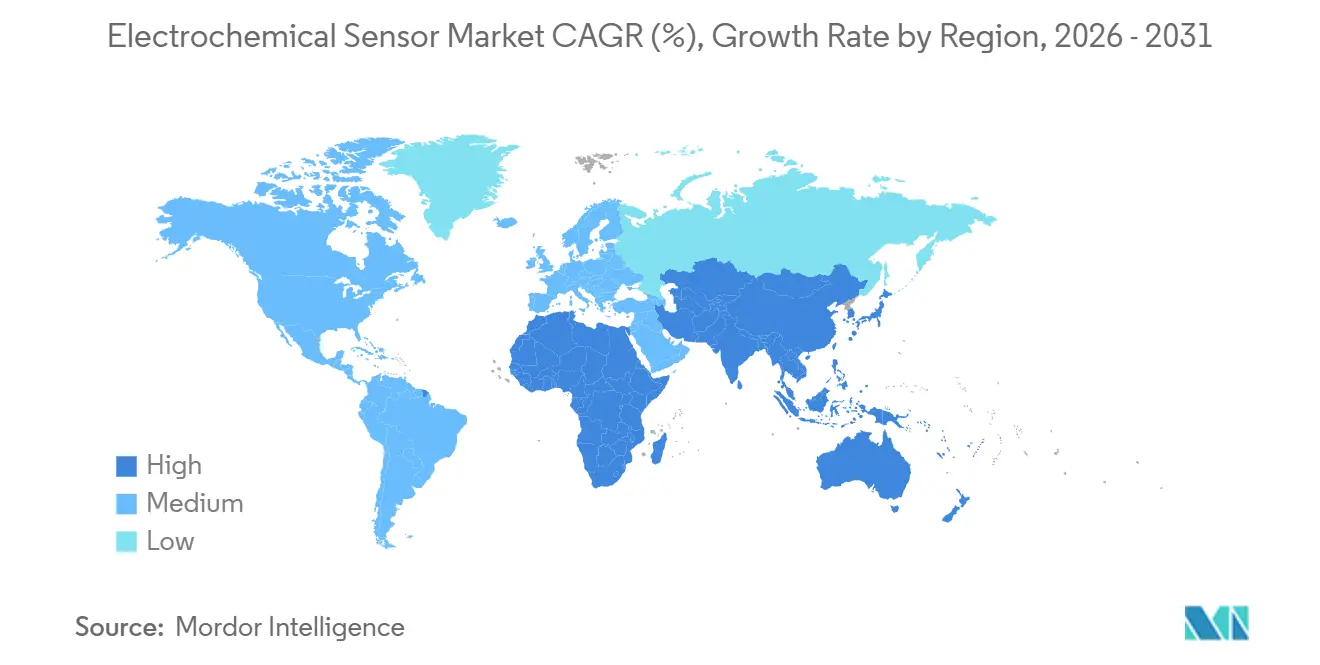

- By geography, North America retained 36.16% of the revenue share in 2025, yet Asia Pacific is poised to deliver the strongest regional performance, with a 9.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrochemical Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Portable and Wearable Detection Devices | +1.8% | Global, with concentration in North America and Europe for medical wearables; Asia Pacific for consumer wellness devices | Medium term (2-4 years) |

| Expansion of Stringent Workplace-Safety Regulations Across Developing Economies | +1.2% | Asia Pacific core, spill-over to Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Integration of Electrochemical Sensors into Industry 4.0 and Smart Manufacturing Platforms | +1.0% | Europe and North America industrial corridors; emerging adoption in China and India | Medium term (2-4 years) |

| Rapid Growth of Continuous Glucose Monitoring and Other Point-of-Care Diagnostics | +2.1% | North America and Europe lead regulatory approvals; Asia Pacific accelerating with local device approvals | Short term (≤ 2 years) |

| Adoption of MEMS-Based Solid-State Architectures Reducing Cost and Footprint | +1.3% | Global, driven by semiconductor hubs in Taiwan, South Korea, Japan, United States | Medium term (2-4 years) |

| Emergence of Printed and Flexible Electrochemical Sensors for Large-Area Environmental Networks | +0.9% | Europe environmental monitoring; China air-quality networks; pilot deployments in urban centers globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Portable and Wearable Detection Devices

Clinical approval for on-body continuous glucose monitors that do not require finger-stick calibration is expanding the market for electrochemical sensors. The United States Food and Drug Administration cleared Abbott FreeStyle Libre 3 in December 2024 and approved Dexcom Stelo for over-the-counter sales in June 2025, opening access for more than 30 million U.S. adults with Type 2 diabetes who do not use insulin.[1]United States Food and Drug Administration, “FDA Clears First Over-the-Counter Continuous Glucose Monitor,” fda.gov Printed electrodes on polyethylene terephthalate, combined with Bluetooth Low Energy modules, keep the bill of materials below USD 50, a threshold that unlocks cash-pay consumer segments. Research groups have already demonstrated amperometric lactate and cortisol patches smaller than 5 square millimeters that operate on 10 microwatts, enabling multi-day monitoring on a coin cell. Sports and wellness brands are using the same platform to measure sweat alcohol and hydration markers, turning biochemical feedback into app-based coaching subscriptions.

Expansion of Stringent Workplace-Safety Regulations Across Developing Economies

India’s 2024 amendments to the Factories Act make continuous hydrogen sulfide and carbon monoxide surveillance mandatory in chemical plants employing more than 50 workers, while China’s Ministry of Emergency Management added wastewater treatment sites and subway tunnels to its gas-monitoring list in the same year.[2]Government of India, “Factories Act Amendment: Toxic Gas Monitoring Requirements,” labour.gov.in Demand centers on amperometric cells that deliver sub-1 ppm sensitivity and operate from -40°C to 50°C without requiring active heating. ATEX Zone 1 enclosures incur an additional cost of USD 200-500 per detector, but are non-negotiable for petrochemical operators. Vendors with pre-certified platforms are shipping upgrade kits that slot into legacy catalytic-bead housings, reducing retrofit downtime to a single shift and accelerating adoption across more than 200,000 aging units in India alone.

Integration of Electrochemical Sensors into Industry 4.0 and Smart Manufacturing Platforms

Automakers in Germany have embedded amperometric oxygen sensors inside paint booths, feeding data through OPC Unified Architecture gateways into machine-learning models that predict drift and autocalibrate before readings move outside ISO 9001 tolerance bands.[3]International Organization for Standardization, “ISO 9001 Quality Management Systems,” iso.org Semiconductor toolmakers now package microcontrollers and electrochemical transducers on the same substrate, shrinking footprints to 1 cubic centimeter and eliminating analog-to-digital conversion noise. Pharmaceutical cleanrooms are another growth area, as Good Manufacturing Practice rules require continuous ammonia checks across air-handling units. These operators require digital outputs and built-in self-diagnostics that flag membrane fouling or electrolyte depletion, enabling maintenance crews to reduce unplanned downtime by 15%.

Rapid Growth of Continuous Glucose Monitoring and Other Point-of-Care Diagnostics

Reimbursement expansion has driven the combined continuous glucose monitoring revenue for Abbott and Dexcom from USD 8.9 billion in 2023 to an estimated USD 12.5 billion in 2025, with analysts projecting that Senseonics received approval for a 365-day implantable sensor in April 2025, eliminating the 26 annual insertions required by earlier models. Medtronic’s MiniMed 780G, cleared in October 2024, ties a 7-day amperometric sensor to automated insulin dosing that cuts hypoglycemic events by 30% in pivotal trials. Success in glucose is spilling into lactate-based sepsis triage and potassium monitoring during renal therapy, reinforcing hospital demand for point-of-care readers and accelerating unit shipments well above consensus forecasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short Operational Life in High-Temperature and High-Humidity Environments | -0.7% | Middle East, Southeast Asia, tropical regions; industrial facilities with steam or chemical exposure | Medium term (2-4 years) |

| Lengthy Certification Cycles for Hazardous-Area Applications (ATEX and IECEx) | -0.5% | Global, with acute impact in Europe (ATEX) and Asia Pacific (IECEx) for oil and gas, chemical sectors | Long term (≥ 4 years) |

| Drift and Re-calibration Burden in Long-Term Continuous-Monitoring Installations | -0.9% | Global industrial and environmental monitoring deployments; particularly acute in remote or offshore sites | Medium term (2-4 years) |

| Fragmented Standardization for Printed and Wearable Sensor Performance | -0.6% | Global, with regulatory bottlenecks in North America (FDA) and Europe (CE marking under Medical Device Regulation) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short Operational Life in High-Temperature and High-Humidity Environments

Electrolyte evaporation and membrane degradation can reduce service life from 24 months to as little as nine in refineries where daytime temperatures exceed 45 °C and humidity exceeds 90%. Operators in Saudi petrochemical complexes report replacement rates triple those in temperate zones. Ionic-liquid electrolytes and hermetic housings extend life but add USD 10-20 per detector and slow response times by up to 30%. Some end-users are switching to metal-oxide or optical sensors for furnace zones, thereby constraining the electrochemical sensor market in precisely the environments where its selectivity would otherwise be most beneficial.

Lengthy Certification Cycles for Hazardous-Area Applications

Achieving ATEX or IECEx approval demands 12-18 months of lab testing and USD 50,000-150,000 per variant. Smaller firms, therefore, steer clear of Zone 0 and Zone 1 opportunities. Novel architectures, such as printed electrodes, must undergo extended evaluation because precedent certifications are lacking, which could delay their launch by another two to three years. These bottlenecks leave the field to incumbents with amortized test budgets, limiting competitive diversity and slowing uptake of disruptive cost-reduction technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Amperometric Sensors Dominate but Conductometric Designs Accelerate

Amperometric models generated 42.38% of 2025 revenue, anchored by glucose monitoring and hydrogen sulfide safety applications, where they combine sub-1 ppm detection with simple two-point calibration. Conductometric sensors, although smaller in absolute terms, are expanding at a 9.43% CAGR because water utilities rely on them for real-time dissolved solids tracking in desalination plants and municipal distribution loops. Potentiometric systems remain the go-to choice for pH and ion-selective bioprocess control, while voltammetric devices serve as a niche tool for heavy-metal analysis. The miniaturization of amperometric cells onto MEMS hotplates underpins the integration of four-electrode arrays inside smartwatches and insulin pumps, a frontier that could add USD 2 billion to the electrochemical sensor market by 2031.

Second-generation amperometric dies already measure 0.3 cubic centimeters and leverage platinum nanofibers that boost signal-to-noise by 25%. Conductometric makers are countering with drift-resistant polymer films that allow six-month deployments without field recalibration, a requirement for distributed water-quality nodes in rural India. Potentiometric vendors are enhancing ion-exchange membranes to withstand industrial cleaners, thereby broadening pH applications from food fermentation to semiconductor rinse baths. Voltammetric entrants are bundling heavy-metal and pesticide assays into cloud-linked kits aimed at agricultural extension officers. Together, these innovations keep the electrochemical sensor market on a steady trajectory of diversification.

By End-User Industry: Healthcare Commands Spend, Environmental Monitoring Gains Momentum

Healthcare represented 29.71% of 2025 demand, powered by double-digit growth in continuous glucose monitoring. Hospital procurement teams favor amperometric cartridges that clip into multi-analyte blood-gas analyzers, enabling sepsis triage to be sped up from hours to minutes. Oil and gas operators account for a similar share, but growth is flatter as mature installations move into replacement mode. The environmental monitoring community is growing more briskly, with a 9.74% CAGR, because cities in China and Europe must hit sub-1 kilometer resolution under the latest Ambient Air Quality Directive. Food and beverage processors continue to adopt dissolved oxygen and pH probes that integrate into Hazard Analysis and Critical Control Points (HACCP) dashboards.

Field interviews reveal that pharmaceutical cleanrooms spend twice as much per sensor as other verticals, due to the requirement for traceable calibration certificates. Mining companies in Australia and South Africa are upgrading portable detectors with Bluetooth connectivity, allowing readings to auto-populate safety logs. Automotive tier-ones in Japan and South Korea now design MEMS amperometric nitrogen oxide modules into exhaust after-treatment systems for Euro 7 compliance. Each of these verticals adds incremental volume, keeping the electrochemical sensor market diversified against shocks from a single industry.

By Application: Medical Diagnostics Still Largest, Wearables Most Dynamic

Medical diagnostics accounted for 33.67% of 2025 sales, while wearable wellness devices are the fastest-growing segment at 9.79% per year. Over-the-counter glucose approvals remove prescription friction, and fitness platforms monetize subscription dashboards that interpret lactate and cortisol curves. Industrial safety remains the second-largest application cluster, as confined-space entry rules require the use of portable hydrogen sulfide and carbon monoxide alarms. Environmental deployments range from sub-USD 1 printed nodes on streetlights to EUR 2,000 reference units in regional supersites.

Food-quality programs embed amperometric amine sensors in refrigerated containers, cutting spoilage claims by 12% for meat exporters in Brazil. Automotive regulations require on-board nitrogen oxide accuracy of around 10 ppm for 500,000 kilometers, a specification now met by silicon hotplate stacks with co-integrated heaters and temperature compensators. Collectively, these use cases broaden the electrochemical sensor market addressable space faster than any single segment could.

By Technology: Solid-State Retains Lead, MEMS Platforms Gain Share

Solid-state designs accounted for 37.89% of shipments in 2025, thanks to their resilience in vibration-heavy settings such as drilling rigs and commercial vehicles. Liquid-state cells still dominate ultra-low-level hydrogen sulfide detection because aqueous electrolytes deliver sub-1 ppm sensitivity with response times of 10 seconds. MEMS-based devices, however, are the growth engine, with a 9.39% CAGR, because photolithography allows for the direct printing of gold working electrodes on silicon, thereby slashing assembly labor and pushing unit cost below USD 5 at 100,000-unit quantities. Thick-film and thin-film hybrids withstand 800 °C exhaust streams, providing a foothold in metal-smelter off-gas analysis.

Hybrid arrays are now shipping with 16 electrodes on a 5-millimeter square die, each coated for a different analyte. Such multiplexing reduces the bill of materials in indoor air-quality monitors by a third, strengthening the case for the electrochemical sensor market in smart-building retrofits. Manufacturers are also layering polymeric membranes onto MEMS stacks to protect enzymes from thermal shock, extending wearables’ shelf life through summer heatwaves. The interplay among these technology tracks keeps innovation cycles tight and pricing competitive.

Geography Analysis

North America generated 36.16% of 2025 revenue, anchored by 8 million insulin-dependent patients who already use continuous glucose monitors and a larger Type 2 cohort now eligible for over-the-counter devices. Occupational Safety and Health Administration codes require sub-1 ppm hydrogen sulfide alarms in wastewater plants, driving the replacement of legacy catalytic-bead units with amperometric cells. Canada funds air-quality grids that deploy thousands of printed nitrogen dioxide nodes across Toronto and Vancouver, while Mexico’s automakers fit MEMS nitrogen oxide probes to comply with United States Environmental Protection Agency Tier 3 rules.

The Asia-Pacific is the fastest-growing region, with a growth rate of 9.57% through 2031. China’s Ministry of Ecology and Environment mandates round-the-clock urban air quality checks in more than 300 cities, ordering domestic vendors to build sensors at a price point of less than USD 50. India’s chemical hubs must install fixed hydrogen sulfide and ammonia detectors under the revised 2024 Factory Act. Japan’s chip foundries co-integrate analog front-ends and electrochemical dies for export-oriented cabin-air modules, while South Korean tier-ones lead in exhaust gas arrays for Euro 7.

Europe maintains a sizeable installed base because the revised Ambient Air Quality Directive forces municipalities to cover every square kilometer with sensors. Germany pioneers Euro 7 exhaust implementations that rely on MEMS nitrogen oxide sensors, and the United Kingdom’s National Health Service reimburses continuous glucose monitoring for Type 2 diabetics, thereby fueling patient uptake. France deploys printed flexible sensors in dense Parisian grids, and Spain upgrades winery fermenters with dissolved-oxygen probes. Eastern European refineries are investing in ATEX Zone 1 electrochemical detectors as they modernize their aging Soviet-era infrastructure.

The Middle East and Africa growth centers on Saudi petrochemical complexes and South African mines that require intrinsically safe detectors. Harsh climate shortens sensor life, so operators pay premiums for ionic-liquid models rated to 55 °C. South America sees momentum in Brazil’s PROCONVE L7 adoption, which involves nitrogen oxide probes on diesel pickups, and in Argentina’s use of soil nitrate sensors to optimize fertilizer use, thereby curbing runoff into the Paraná River basin.

Competitive Landscape

Moderate concentration defines the electrochemical sensor market. Honeywell, MSA Safety, and Drägerwerk dominate the industrial safety market, backed by extensive ATEX and IECEx portfolios. Abbott, Dexcom, Medtronic, and Senseonics control most healthcare revenue through proprietary enzyme-electrode chemistries and cloud algorithms that trim calibration frequency. Combined, the top five vendors captured an estimated 62% of 2025 sales; yet, pricing pressure remains because Taiwanese and South Korean foundries can fabricate MEMS dies at a sub-USD 5.

Crane’s USD 1.06 billion acquisition of Baker Hughes’ instrumentation arm in September 2025 underscores consolidation momentum. Siemens bought a minority stake in Sensirion in August 2024 to secure access to micro-hotplate intellectual property for volatile organic compound analyzers. University spin-outs are commercializing aptamer-based electrodes that eliminate cold-chain requirements and double shelf life, but must still clear lengthy Food and Drug Administration or CE Mark pathways. Platform strategies are increasingly centered on digital outputs, self-diagnostics, and IEC 61508 functional safety certifications, as factory automation buyers value predictive maintenance over hardware price.

Vendors also compete on operating-life extensions in harsh climates. Ionic-liquid electrolytes, desalination of polymer films, and hermetic titanium housings fetch premiums from Middle Eastern oil producers who calculate downtime costs at USD 1 million per hour. Start-ups offering printed carbon-ink arrays aim for sub-USD 1 nodes that municipalities can replace every six months, banking on volume economics rather than lifespan. This spectrum of positioning keeps the electrochemical sensor market dynamic and innovation-driven.

Electrochemical Sensor Industry Leaders

Thermo Fisher Scientific Inc.

MSA Safety Incorporated

Emerson Electric Co.

Honeywell International Inc.

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Crane Company completed its USD 1.06 billion acquisition of Baker Hughes’ pressure and safety instrumentation unit, adding 1,200 engineers and an expanded IECEx portfolio.

- June 2025: Dexcom secured United States Food and Drug Administration clearance for Stelo, the first over-the-counter 15-day continuous glucose monitor for non-insulin-dependent Type 2 diabetics.

- April 2025: Senseonics obtained United States Food and Drug Administration approval for Eversense 365, a subcutaneous electrochemical sensor with a one-year lifespan.

- February 2025: Honeywell launched Sensepoint XRL, a wireless detector for hydrogen sulfide, carbon monoxide, and nitrogen dioxide, guaranteed for five years without recalibration.

Global Electrochemical Sensor Market Report Scope

The Electrochemical Sensor Market Report is Segmented by Sensor Type (Potentiometric Sensors, Amperometric Sensors, Conductometric Sensors, Voltammetric Sensors), End-User Industry (Healthcare, Oil and Gas, Chemical and Petrochemicals, Automotive, Food and Beverage, Environmental Monitoring and Other End-User Industries), Application (Medical Diagnostics, Industrial Safety and Gas Detection, Environmental Monitoring, Food Quality Control, Automotive Emissions Monitoring, Wearable and Consumer Wellness Devices), Technology (Solid-State Sensors, Liquid-State Sensors, MEMS-Based Sensors, Thick-Film / Thin-Film Sensors), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Potentiometric Sensors |

| Amperometric Sensors |

| Conductometric Sensors |

| Voltammetric Sensors |

| Healthcare |

| Oil and Gas |

| Chemical and Petrochemicals |

| Automotive |

| Food and Beverage |

| Environmental Monitoring and Other End-User Industries |

| Medical Diagnostics |

| Industrial Safety and Gas Detection |

| Environmental Monitoring |

| Food Quality Control |

| Automotive Emissions Monitoring |

| Wearable and Consumer Wellness Devices |

| Solid-State Sensors |

| Liquid-State Sensors |

| MEMS-Based Sensors |

| Thick-Film / Thin-Film Sensors |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Potentiometric Sensors | ||

| Amperometric Sensors | |||

| Conductometric Sensors | |||

| Voltammetric Sensors | |||

| By End-User Industry | Healthcare | ||

| Oil and Gas | |||

| Chemical and Petrochemicals | |||

| Automotive | |||

| Food and Beverage | |||

| Environmental Monitoring and Other End-User Industries | |||

| By Application | Medical Diagnostics | ||

| Industrial Safety and Gas Detection | |||

| Environmental Monitoring | |||

| Food Quality Control | |||

| Automotive Emissions Monitoring | |||

| Wearable and Consumer Wellness Devices | |||

| By Technology | Solid-State Sensors | ||

| Liquid-State Sensors | |||

| MEMS-Based Sensors | |||

| Thick-Film / Thin-Film Sensors | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the electrochemical sensor market in 2031?

The electrochemical sensor market size is forecast to reach USD 16.97 billion by 2031.

Which sensor type currently leads global revenue?

Amperometric sensors command 42.38% of 2025 revenue, the largest share among all types.

Which region will grow the fastest through 2031?

Asia Pacific is expected to post the highest CAGR at 9.57% through 2031, fueled by air-quality mandates and industrial safety retrofits.

How are MEMS platforms changing competitive dynamics?

MEMS fabrication cuts unit cost below USD 5 at scale and enables multi-gas arrays on single dies, attracting consumer electronics and automotive customers.

What is the main barrier for new entrants in hazardous areas?

ATEX and IECEx certifications add 12-18 months and up to USD 150,000 per variant, creating a significant time and cost hurdle for startups.

Page last updated on: