Integrated Vehicle Health Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

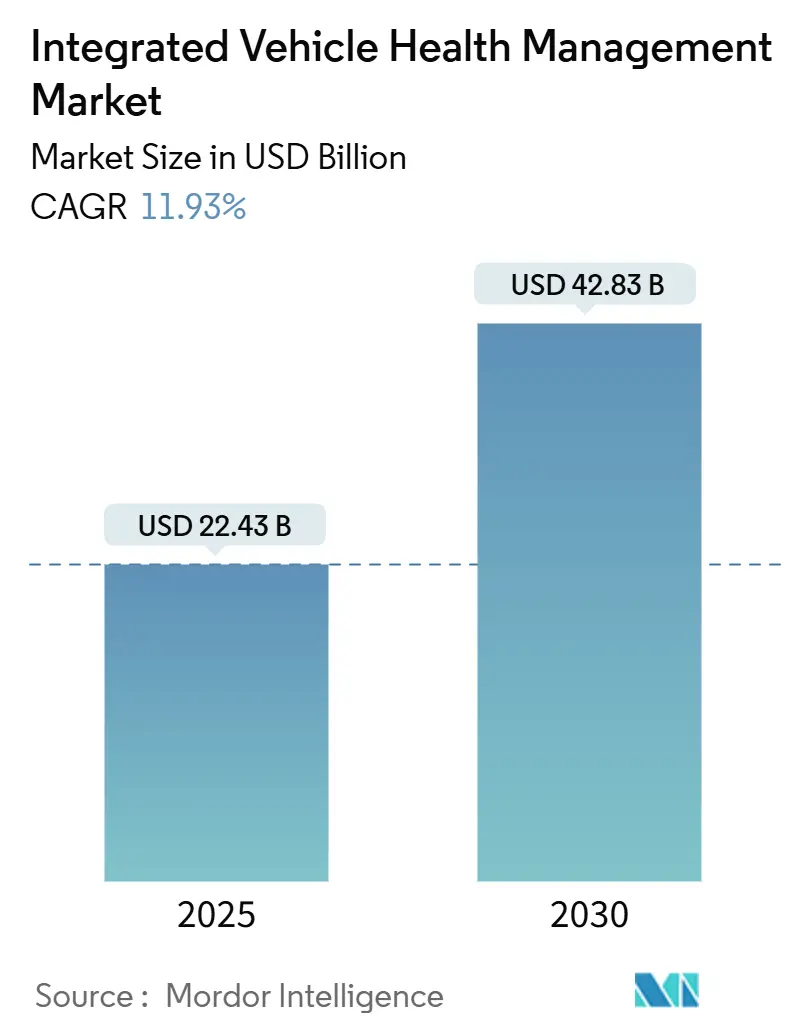

| Market Size (2025) | USD 22.43 Billion |

| Market Size (2030) | USD 42.83 Billion |

| Growth Rate (2025 - 2030) | 11.93% CAGR |

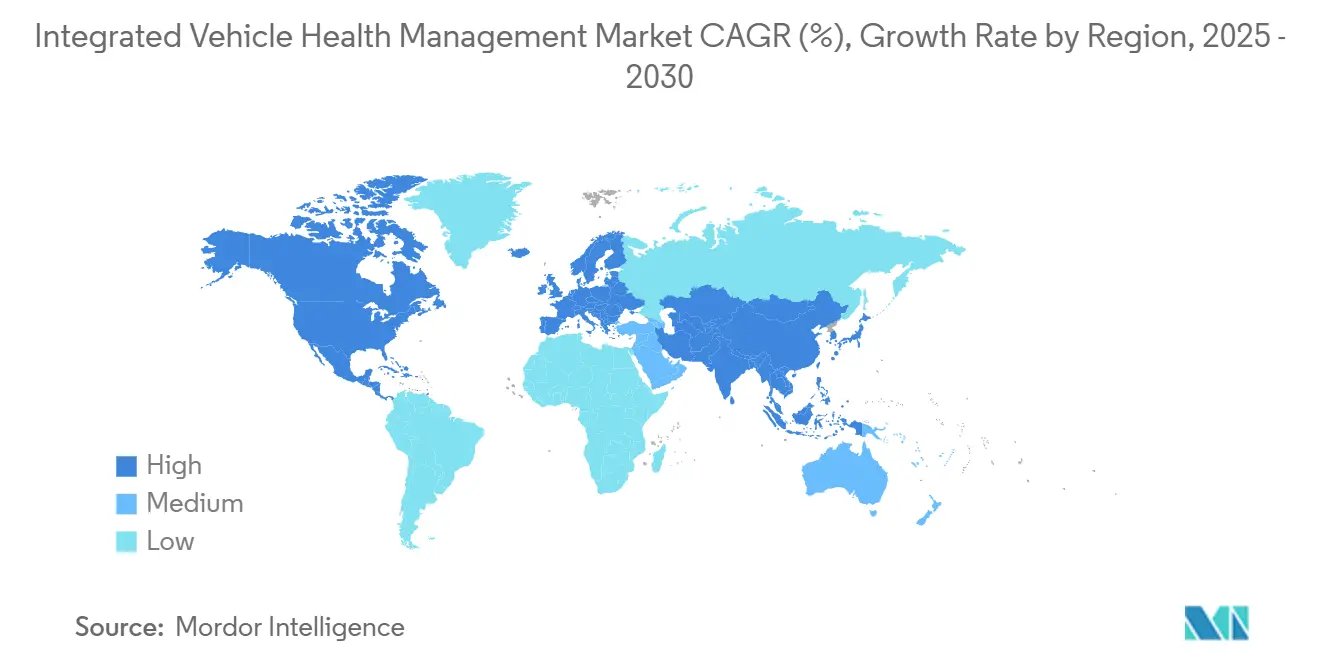

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Integrated Vehicle Health Management Market Analysis by Mordor Intelligence

The Integrated Vehicle Health Management market size is valued at USD 22.43 billion in 2025 and is forecast to reach USD 42.83 billion by 2030, expanding at an 11.93% CAGR during the forecast period. Greater sensor density in electric and autonomous platforms, combined with 5G-enabled edge analytics, transforms maintenance from reactive repair to near-real-time prognostics. Vehicle makers are redesigning electronics with secure over-the-air update pathways, while fleets demand guaranteed uptime metrics to meet e-commerce delivery windows. Cloud-native telematics ecosystems now ingest high-frequency health data that feeds machine-learning models for component-level life predictions. Rising cybersecurity compliance costs under ISO/SAE 21434 and China’s Network Data Security Regulations reshape deployment roadmaps and open service revenue streams for vendors able to certify secure data flows.

Key Report Takeaways

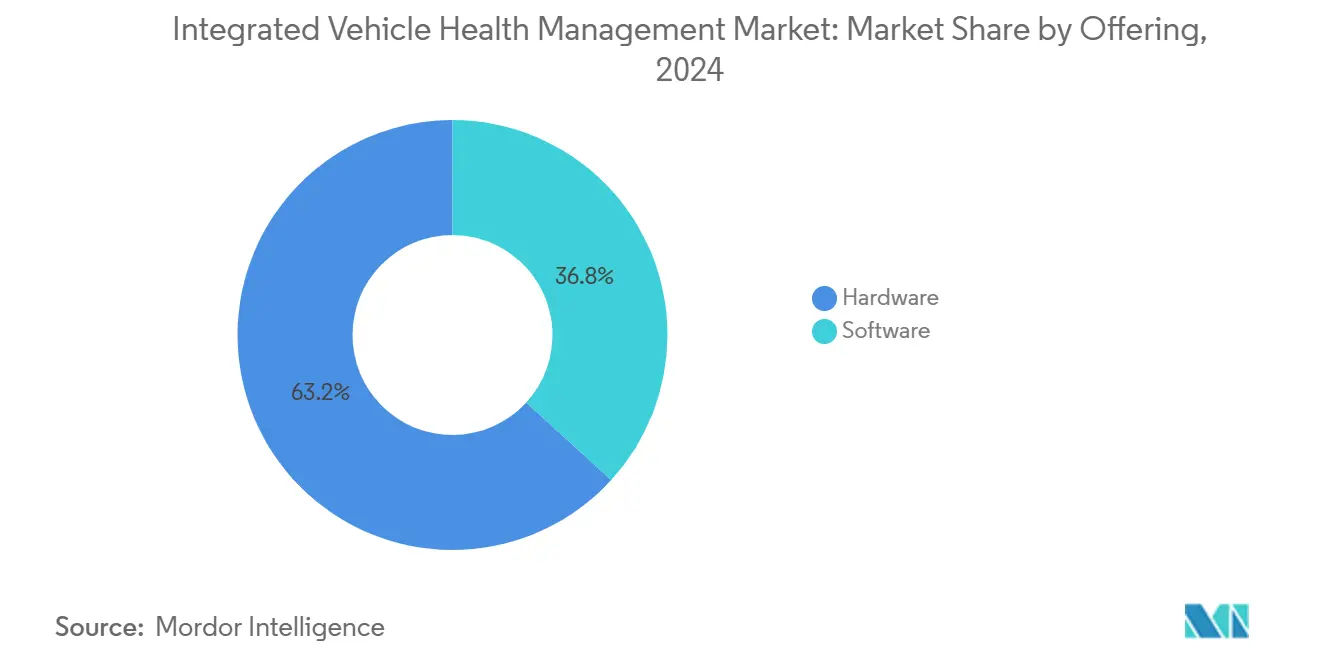

- By offering, hardware accounted for 63.21% of revenue in the integrated vehicle health management market in 2024, while software is projected to grow at a 14.87% CAGR through 2030.

- By channel, OEM service centers led with 48.32% share of the Integrated Vehicle Health Management market in 2024, while remote diagnostics platforms are on track for an 18.14% CAGR to 2030.

- By application, predictive maintenance held 36.59% of the Integrated Vehicle Health Management market share in 2024; driver monitoring solutions are advancing at a 19.46% CAGR through 2030.

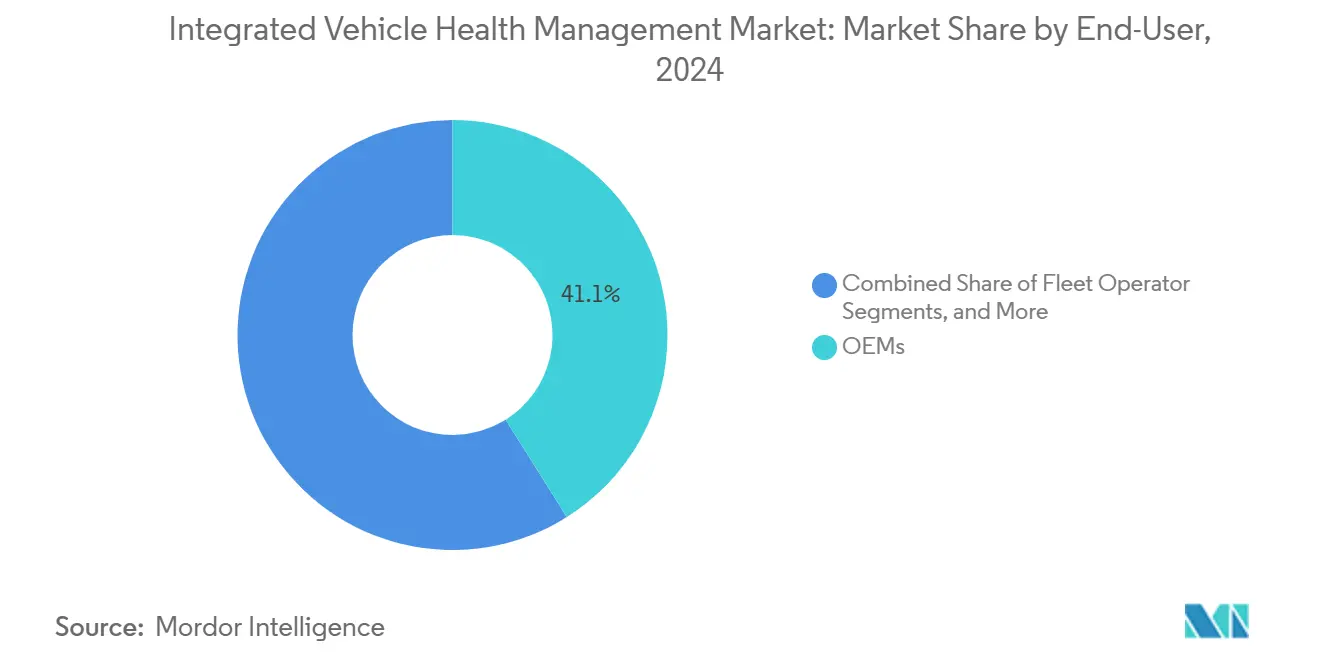

- By end-user, OEMs accounted for a 41.08% share of the Integrated Vehicle Health Management market in 2024, yet service providers are set to expand at a 17.13% CAGR to 2030.

- By vehicle type, passenger vehicles represented a 52.07% share of the Integrated Vehicle Health Management market in 2024, whereas medium and heavy commercial vehicles are poised for a 12.26% CAGR to 2030.

- By geography, Asia-Pacific commanded 38.04% share of the Integrated Vehicle Health Management market in 2024 and is estimated to grow at a 15.92% CAGR through 2030.

Global Integrated Vehicle Health Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEMs Shifting to Service-Based Revenue Models | +2.1% | Global, with Early Adoption in North America and Europe | Medium Term (2-4 Years) |

| Surge in EV Sensor Counts Enabling Richer Health Data | +1.8% | Asia-Pacific Core, Spill-Over to North America | Short Term (≤ 2 Years) |

| 5G/Edge-AI Lowering Latency for Prognostics | +1.5% | North America and EU, Expanding to Asia-Pacific | Medium Term (2-4 Years) |

| Stricter Uptime SLAs in E-Commerce Fleets | +1.3% | Global, with Concentration in Urban Logistics Hubs | Short Term (≤ 2 Years) |

| Standard SAE JA6268 "Health-Ready" Mandate Adoption | +1.0% | North America and Europe Regulatory Domains | Long Term (≥ 4 Years) |

| Defence Programmes Funding IVHM for Autonomous Assets | +0.8% | North America, Europe, Asia-Pacific Defense Corridors | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

OEMs Shifting to Service-Based Revenue Models

Automotive manufacturers are fundamentally restructuring their business models to capture aftermarket revenue streams. This transition compels OEMs to invest heavily in IVHM capabilities that enable predictive maintenance services, remote diagnostics, and usage-based insurance products. BMW's strategic partnerships with Tata Technologies and NTT DATA exemplify this shift, focusing on software-defined vehicle architectures that generate recurring service revenue. The TRATON GROUP's collaboration with Applied Intuition for software-defined commercial vehicles demonstrates how commercial vehicle OEMs prioritize IVHM integration to differentiate their service offerings. This strategic pivot creates sustained demand for IVHM technologies that enable OEMs to monetize vehicle data throughout the ownership lifecycle.

Surge in EV Sensor Counts Enabling Richer Health Data

Electric vehicles incorporate significantly more sensors than internal combustion engines, particularly for battery thermal management, state-of-charge monitoring, and power electronics diagnostics. Embitel's Battery Management System technology solutions demonstrate ASIL-D safety compliance requirements, requiring comprehensive sensor integration for EV health monitoring. Neural Concept's EV battery cooling optimization techniques reveal how thermal sensors enable predictive maintenance algorithms that prevent battery degradation and extend vehicle range. The proliferation of IoT-based thermal management systems, including liquid cooling, phase change materials, and immersion cooling technologies, generates unprecedented volumes of health data that IVHM systems can analyze for predictive insights. AVL's battery lifetime prediction capabilities illustrate how sensor fusion enables accurate prognostics for critical EV components. This sensor density explosion creates a data-rich environment that enhances IVHM algorithm accuracy and allows more sophisticated predictive maintenance strategies.

5G/Edge-AI Lowering Latency for Prognostics

Fifth-generation cellular networks combined with edge computing architectures enable real-time vehicle health analysis with minimal latency, which is crucial for safety-critical prognostic applications. Indian automotive suppliers are adopting edge computing solutions with 5G rollout through platforms like Tata Communications CloudLyte, demonstrating regional infrastructure readiness[1]"Uncomplicate and Innovate with the Tata Communications Digital Fabric," tatacommunications.com. Ford's partnership with AT&T for factory Multi-Access Edge Computing and Mercedes-Benz's collaboration with Telefónica for private 5G networks showcase OEM investments in ultra-low latency connectivity. GIGABYTE's Ultra-Reliable Low Latency Communication solution for autonomous vehicle networks exemplifies the hardware infrastructure supporting 5G-enabled IVHM deployments. Technical research on 5G vehicular MEC with guaranteed task completion demonstrates the mathematical frameworks enabling real-time prognostic algorithms. This connectivity evolution enables IVHM systems to process complex diagnostic algorithms at the network edge, reducing response times for critical vehicle health events.

Stricter Uptime SLAs in E-Commerce Fleets

E-commerce logistics operators are implementing increasingly stringent service-level agreements that penalize vehicle downtime, creating demand for predictive maintenance solutions that maximize fleet availability. Verizon Connect's 2025 Fleet Technology Trends report indicates that 80% of fleet operators use technology solutions, with 22% achieving cost reduction through predictive maintenance implementations[2]Tessa Giammona, "Verizon Connect report highlights fleet tech adoption, ROI gains, and safety improvements," verizon.com. SIXT van & truck's deployment of Geotab predictive maintenance across 6,500 UK commercial vehicles demonstrates how rental operators invest in IVHM to meet contract compliance requirements. ZM Trucks' selection of Sibros' Deep Connected Platform for zero-emission commercial vehicles illustrates how electrification amplifies uptime requirements due to charging infrastructure dependencies. Bridgestone's strategic partnership with Geotab to access connected-vehicle network data from vehicles enables tire manufacturers to optimize fleet performance through predictive analytics. These stringent uptime requirements drive fleet operators to invest in comprehensive IVHM solutions that prevent unplanned maintenance events.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security and Data-Sovereignty Compliance Burden | -1.4% | Global, with Stricter Requirements in EU and China | Short Term (≤ 2 Years) |

| Inter-Platform Data-Model Fragmentation | -1.1% | Global, Affecting Cross-OEM Compatibility | Medium Term (2-4 Years) |

| Shortage of Prognostics/Data-Science Talent at OEMs | -0.9% | North America and Europe Primarily | Medium Term (2-4 Years) |

| High Initial Sensor and Connectivity Capex for Legacy Fleets | -0.7% | Global, with Higher Impact in Cost-Sensitive Markets | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Sovereignty Compliance Burden

Automotive cybersecurity regulations impose significant compliance costs and technical complexity that constrain IVHM deployment, particularly for smaller fleet operators and aftermarket solution providers. China's Network Data Security Regulations, effective January 1, 2025, mandate strict cross-border data transfer controls that complicate cloud-based IVHM architectures. The ISO/SAE 21434 automotive cybersecurity standard requires comprehensive Cybersecurity Management Systems that increase development costs and time-to-market for IVHM solutions. UNECE WP.29 R155/R156 cybersecurity and software update management requirements create additional regulatory compliance burdens for OEMs implementing IVHM capabilities. China's automotive-specific data security standards T/CAAMTB 189-2024 demonstrate the proliferation of regional cybersecurity requirements that fragment global IVHM development strategies. These regulatory requirements increase IVHM system complexity and deployment costs while potentially limiting cross-border data sharing capabilities essential for international fleet management.

Inter-Platform Data-Model Fragmentation

The lack of standardized data models and communication protocols across OEMs and IVHM solution providers creates integration challenges that limit market scalability and increase deployment costs. Proprietary data formats prevent seamless integration between different vehicle brands within mixed fleets, forcing operators to maintain multiple IVHM platforms. The absence of universal diagnostic interfaces complicates aftermarket IVHM solution development, as providers must customize their offerings for each OEM's specific data architecture. This fragmentation increases software development costs and reduces the economic viability of comprehensive IVHM solutions for smaller fleet operators. Cross-platform compatibility issues also limit the effectiveness of predictive maintenance algorithms that rely on large datasets from diverse vehicle populations. Industry standardization efforts through organizations like SAE International are addressing these challenges, but implementation remains inconsistent across the automotive ecosystem.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Amid Software Acceleration

Hardware components hold a 63.21% share of the integrated vehicle health management market in 2024, reflecting the fundamental requirement for sensors, connectivity modules, and processing units that enable vehicle health monitoring capabilities. The sensor-intensive nature of IVHM systems necessitates significant hardware investments, particularly for electric vehicles, where battery management systems require comprehensive thermal and electrical monitoring infrastructure. Software solutions, despite representing a smaller current share, are experiencing rapid growth at 14.87% CAGR through 2030, as OEMs prioritize cloud-based analytics platforms and artificial intelligence algorithms for predictive maintenance.

The transition toward software-defined vehicles enables OEMs to monetize IVHM capabilities through subscription-based services and over-the-air feature updates. Regulatory compliance frameworks like ISO/SAE 21434 for automotive cybersecurity increasingly emphasize software security requirements that drive investment in secure IVHM platforms. This segmentation dynamic reflects the automotive industry's evolution from hardware-centric to software-enabled business models.

By Channel: OEM Dominance with Remote Platform Emergence

OEM Service Centers maintain the largest channel share at 48.32% of the integrated vehicle health management market in 2024, leveraging their direct customer relationships and comprehensive vehicle data access to deliver integrated vehicle health management (IVHM) services. This dominance reflects OEMs' strategic focus on capturing aftermarket revenue through factory-authorized service networks that can access proprietary diagnostic protocols and warranty management systems. Independent Service Centers represent a significant but constrained segment due to limited access to OEM-specific health data and diagnostic interfaces. Remote Diagnostics Platforms are experiencing the fastest growth at 18.14% CAGR through 2030, driven by cloud computing capabilities and 5G connectivity that enable real-time vehicle health monitoring without physical service interventions.

Geotab's partnerships with multiple OEMs, including Kia Corporation and 42dot, demonstrate how telematics providers integrate with factory systems to enable cloud-to-cloud data sharing. Sibros' Deep Connected Platform deployment across commercial vehicle manufacturers illustrates the growing importance of cloud-based IVHM architectures that bypass traditional service channel limitations. The COVID-19 pandemic accelerated remote diagnostics adoption as fleet operators sought to minimize physical service interactions while maintaining vehicle uptime. Fleet Europe analysis indicates that by 2030, over 90% of vehicles sold in Europe will be connected, fundamentally shifting service delivery toward remote diagnostics capabilities. This channel evolution reflects the automotive service industry's digital transformation and the increasing sophistication of cloud-based IVHM platforms.

By Application: Predictive Maintenance Leadership with Driver Monitoring Surge

Predictive Maintenance applications hold the largest share at 36.59% share of the integrated vehicle health management market in 2024, reflecting the fundamental value proposition of integrated vehicle health management (IVHM) systems in preventing unplanned downtime and optimizing maintenance schedules. Driver Monitoring systems are experiencing exceptional growth at a 19.46% CAGR through 2030, driven by regulatory mandates, including the EU General Safety Regulation that requires driver attention monitoring in new passenger cars and light commercial vehicles from 2024. Euro NCAP and ANCAP rating systems now incorporate direct driver monitoring system assessments, creating competitive pressure for OEMs to implement advanced camera-based monitoring capabilities.

Fleet Management applications benefit from the integration of telematics data with vehicle health information, enabling comprehensive asset optimization strategies. Vehicle Diagnostics applications remain essential for regulatory compliance and warranty management, particularly as automotive cybersecurity standards require comprehensive system monitoring capabilities. Neonode's MultiSensing platform for driver monitoring demonstrates how AI-powered in-cabin sensing technologies are expanding beyond basic distraction detection to include occupant position tracking and hands-on-wheel detection. The convergence of driver monitoring with vehicle health management creates opportunities for integrated safety systems that respond to both driver state and vehicle condition simultaneously. Regulatory influence from bodies like the European Commission and NHTSA continues to drive adoption across safety-critical applications.

By End-User: OEM Leadership with Service Provider Acceleration

OEMs hold a 41.08% share of the integrated vehicle health management market in 2024, leveraging their comprehensive vehicle data access and customer relationships to deliver integrated IVHM services through factory-authorized channels. Service Providers are experiencing the fastest growth at 17.13% CAGR through 2030, as third-party maintenance specialists integrate IVHM capabilities into their service offerings to compete with OEM-authorized networks. This growth reflects the increasing sophistication of independent service providers investing in diagnostic equipment and cloud-based analytics platforms to access vehicle health data.

Fleet Operators constitute a significant user segment driven by stringent uptime requirements and total cost of ownership optimization strategies. Individual Vehicle Owners represent the smallest but growing segment as consumer awareness of predictive maintenance benefits increases through connected car services and mobile applications. LLumin's partnership with Azuga demonstrates how specialized CMMS providers integrate with telematics platforms to deliver comprehensive fleet asset management solutions. Sumitomo Rubber's strategic investment in Viaduct Inc. for AI-powered vehicle health analytics illustrates how traditional automotive suppliers are expanding into service provider roles. The end-user landscape is evolving toward ecosystem partnerships where OEMs, service providers, and technology specialists collaborate to deliver comprehensive IVHM solutions.

By Vehicle Type: Commercial Vehicle Growth Momentum

Passenger Vehicles hold a 52.07% share of the integrated vehicle health management market in 2024, reflecting the large installed base and consumer market size, but growth rates are moderating as the market matures. Light Commercial Vehicles benefit from urban delivery applications where uptime requirements are becoming increasingly stringent due to last-mile logistics demands.Medium and Heavy Commercial Vehicles exhibit the strongest growth momentum at 12.26% CAGR through 2030, driven by e-commerce logistics requirements and the increasing adoption of autonomous freight systems that demand comprehensive health monitoring capabilities.

ZM Trucks' selection of Sibros' Deep Connected Platform for battery-electric medium and heavy-duty commercial vehicles demonstrates how electrification amplifies IVHM requirements in the commercial segment. The U.S. Army's Ground Equipment Autonomous Resupply System project illustrates how autonomous commercial vehicles require advanced health monitoring capabilities for unmanned operations. Commercial vehicle operators face higher penalties for unplanned downtime than passenger vehicle owners, creating more substantial economic incentives for IVHM investment. Geotab's cold chain telematics integration with Thermo King demonstrates how specialized commercial applications drive demand for industry-specific IVHM solutions. The commercial vehicle segment's growth reflects the increasing sophistication of fleet management operations and the transition toward autonomous freight systems.

Geography Analysis

Asia-Pacific led with 38.04% share of the integrated vehicle health management market in 2024 and is expected to grow at a CAGR of 15.92% through 2030, owing to accelerated EV uptake, 5G roll-outs, and data-security mandates that compel sophisticated on-shore analytics. China’s cross-border data licensing rules drive local cloud deployments with advanced encryption and audit logging. India’s 5G corridor along major freight routes hosts edge nodes for real-time truck prognostics, demonstrating national digital-infrastructure readiness. Japanese OEMs invest in software-defined vehicle platforms that embed health analytics as standard, raising regional baseline functionality.

North America remains an innovation hotbed, propelled by e-commerce fleets that quantify every downtime hour financially. The U.S. Army’s autonomous resupply projects steer defense dollars into ruggedized sensor suites and AI inference silicon. Private 5G pilots at vehicle plants exemplify industry-telecom collaboration to close feedback loops between manufacturing defects and field failures. Interstate telematics regulations are comparatively permissive, easing data aggregation across states and accelerating Integrated Vehicle Health Management market adoption.

Europe experienced legislated demand surges as the General Safety Regulation and UNECE WP.29 cybersecurity rules rolled out. BMW and Mercedes allocate substantial budgets to private 5G networks and secure connectivity stacks to remain compliant while unlocking paid digital services. Continental and Bosch test digital twins that simulate component lifecycles against real-world usage patterns, supporting predictive warranties across the continent. With connected-vehicle penetration expected to grow by 2030, Europe's integrated vehicle health management market is positioned for robust gains despite macroeconomic headwinds.

Competitive Landscape

The top five suppliers dominate the integrated vehicle health management market, leaving room for agile telematics entrants. Bosch channels sizeable funds into middleware platforms that fuse in-vehicle diagnostics with cloud twins.

Telematics natives like Geotab scale cloud ecosystems that integrate with disparate OEM APIs, boasting installations on vehicles. Sibros positions itself as firmware-agnostic middleware, capturing complete life-cycle logs, necessary for battery warranty analytics. Viaduct specializes in post-processing high-frequency sensor streams to model component aging, attracting investment from tire giant Sumitomo. Competitive differentiation increasingly centers on inference accuracy, update cadence, and certified cybersecurity compliance, rather than raw sensor count.

Strategic moves in 2024–2025 include SIXT’s mass deployment of Geotab predictive analytics across rental vans, ZM Trucks’ selection of Sibros for electric freight platforms, and Bridgestone’s tie-up with Geotab for tire-integrated health dashboards. Patent landscapes reveal clustering around battery prognosis and edge AI co-processors, underscoring a race to control IP critical for the next wave of Integrated Vehicle Health Management market expansion.

Integrated Vehicle Health Management Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Aptiv PLC

-

Garrett Motion Inc.

-

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: SIXT van & truck selected Geotab for predictive maintenance deployment across 6,500 UK commercial vehicles, representing one of the largest European fleet IVHM implementations with comprehensive telematics integration and real-time vehicle health monitoring capabilities.

- May 2025: Geotab partnered with Thermo King to integrate TracKing Pro cold chain telematics into the MyGeotab platform. This enables real-time cargo temperature monitoring and automated alert systems for temperature-sensitive goods transportation across North American fleets.

Global Integrated Vehicle Health Management Market Report Scope

| Hardware |

| Software |

| OEM Service Centers |

| Independent Service Centers |

| Remote Diagnostics Platforms |

| Predictive Maintenance |

| Fleet Management |

| Driver Monitoring |

| Vehicle Diagnostics |

| OEMs |

| Fleet Operators |

| Service Providers |

| Individual Vehicle Owners |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Offering | Hardware | |

| Software | ||

| By Channel | OEM Service Centers | |

| Independent Service Centers | ||

| Remote Diagnostics Platforms | ||

| By Application | Predictive Maintenance | |

| Fleet Management | ||

| Driver Monitoring | ||

| Vehicle Diagnostics | ||

| By End-User | OEMs | |

| Fleet Operators | ||

| Service Providers | ||

| Individual Vehicle Owners | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the Integrated Vehicle Health Management market?

The market stands at USD 22.43 billion in 2025 with an 11.93% CAGR toward 2030.

Which region leads adoption of Integrated Vehicle Health Management solutions?

Asia-Pacific accounts for 38.04% of global value thanks to EV uptake and supportive data-security regulations.

Which application segment is growing fastest within Integrated Vehicle Health Management?

Driver monitoring solutions are registering a 19.46% CAGR because of new safety mandates in Europe.

How are OEMs monetizing Integrated Vehicle Health Management capabilities?

Manufacturers sell predictive maintenance subscriptions and remote diagnostic updates that generate recurring revenue beyond vehicle sales.

What is the biggest restraint limiting Integrated Vehicle Health Management deployment?

Meeting diverse cybersecurity and data-sovereignty rules raises cost and complexity, especially for global fleet operators.

Page last updated on: