United States Automotive Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

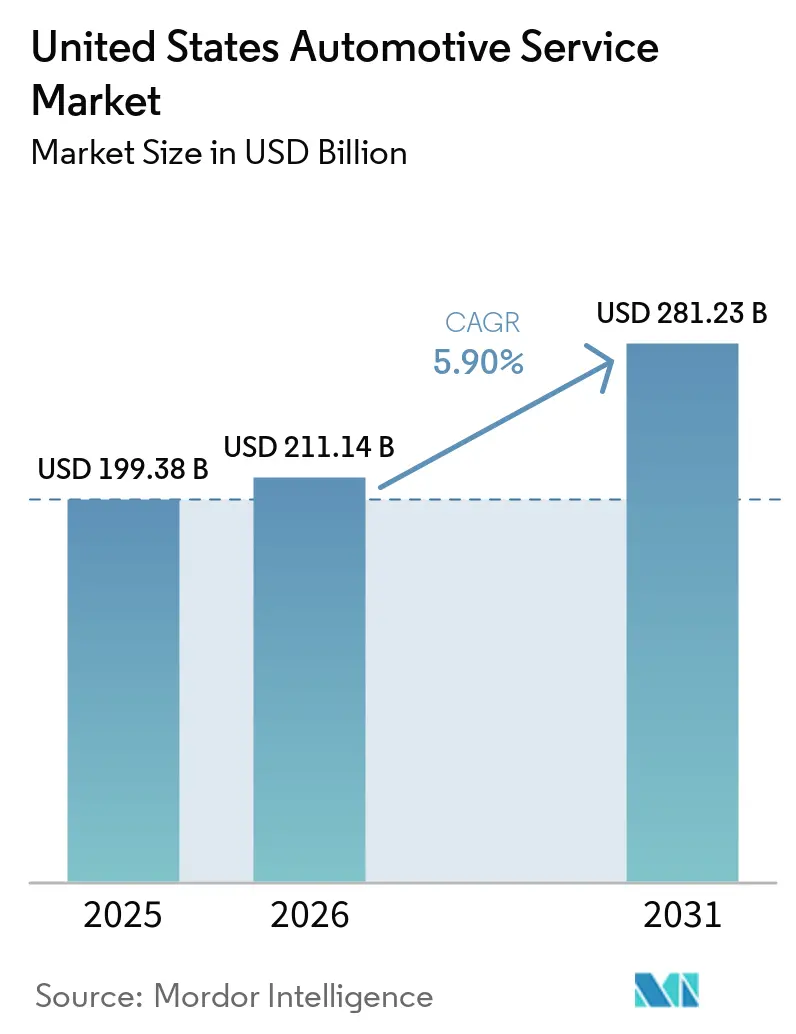

| Base Year Market Size (2025) | USD 199.38 Billion |

| Market Size (2026) | USD 211.14 Billion |

| Market Size (2031) | USD 281.23 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

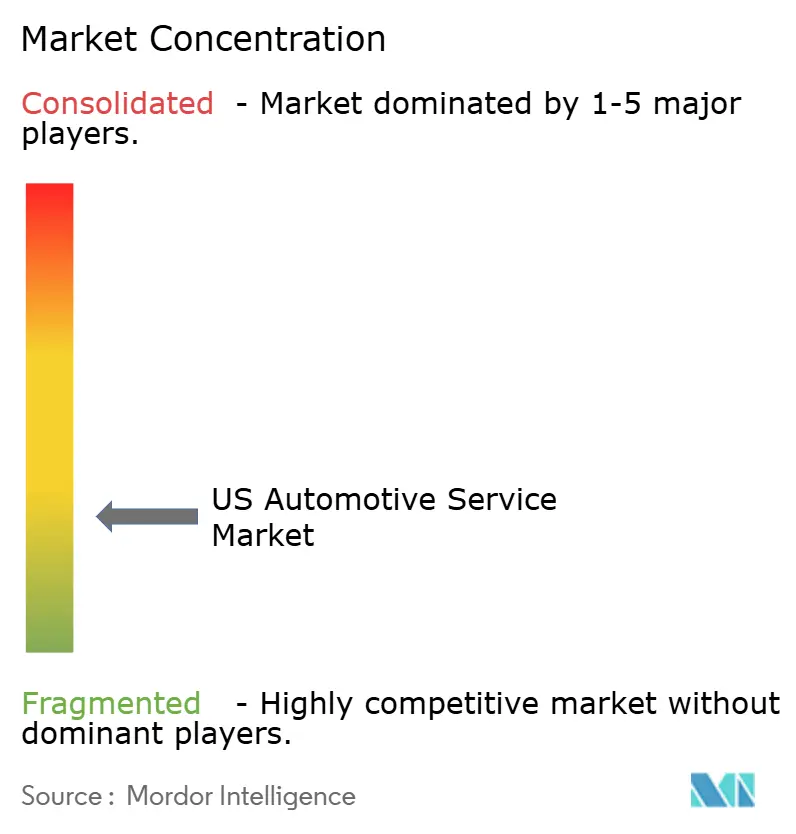

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Automotive Service Market Analysis by Mordor Intelligence

The United States automotive service market size in 2026 is estimated at USD 211.14 billion, growing from 2025 value of USD 199.38 billion with 2031 projections showing USD 281.23 billion, growing at 5.9% CAGR over 2026-2031. Robust demand comes from an aging national vehicle fleet that averages 12.6 years, a rebound in vehicle miles traveled, and rising light commercial vehicle utilization that intensifies service requirements. Accelerating electrification lifts repair complexity and ticket values, even lowering routine maintenance frequency, prompting providers to invest in technician upskilling and high-voltage tooling. Digital booking platforms, subscription-based maintenance bundles, and right-to-repair legislation are reshaping competitive strategies, while mobile on-demand services gain traction among urban consumers. Collectively, these forces position the US automotive service market for sustained revenue growth and operational transformation

Key Report Takeaways

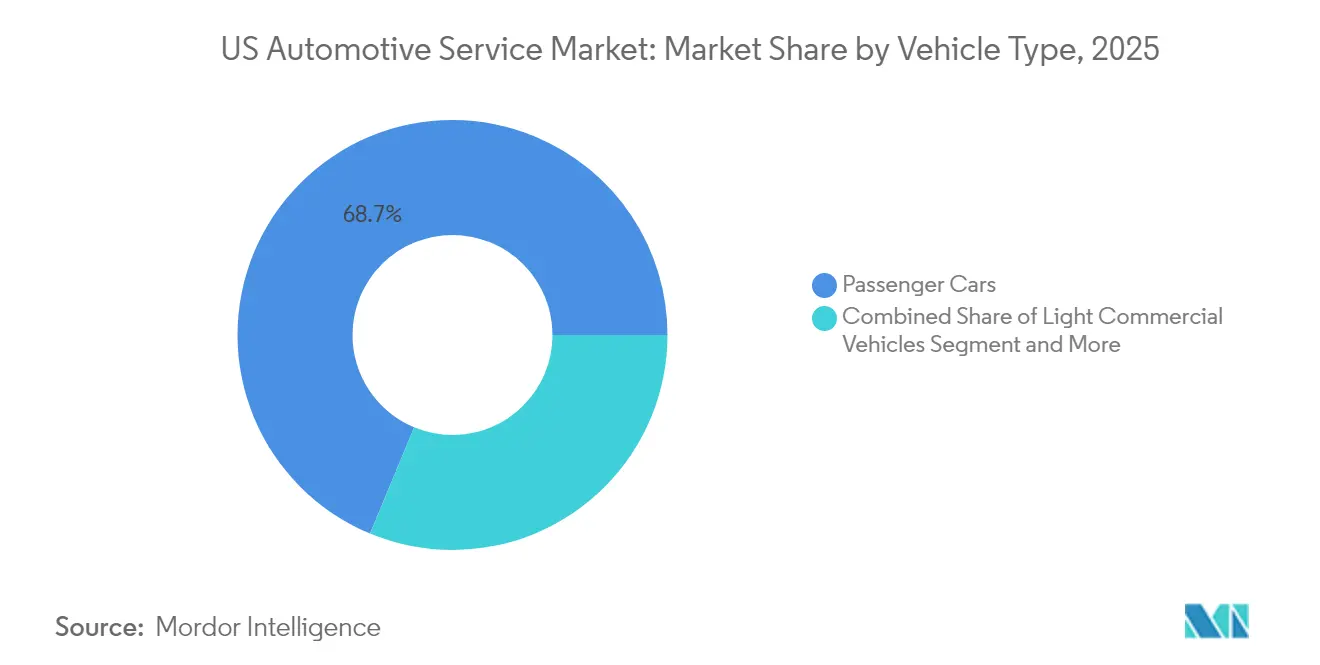

- By vehicle type, passenger cars held 68.74% of the US automotive services market share in 2025, while light commercial vehicles posted the highest forecast CAGR at 8.55% through 2031.

- By service type, mechanical repair and maintenance accounted for 42.67% revenue in 2025, whereas electrical and electronics services are expected to expand at a 9.02% CAGR to 2031.

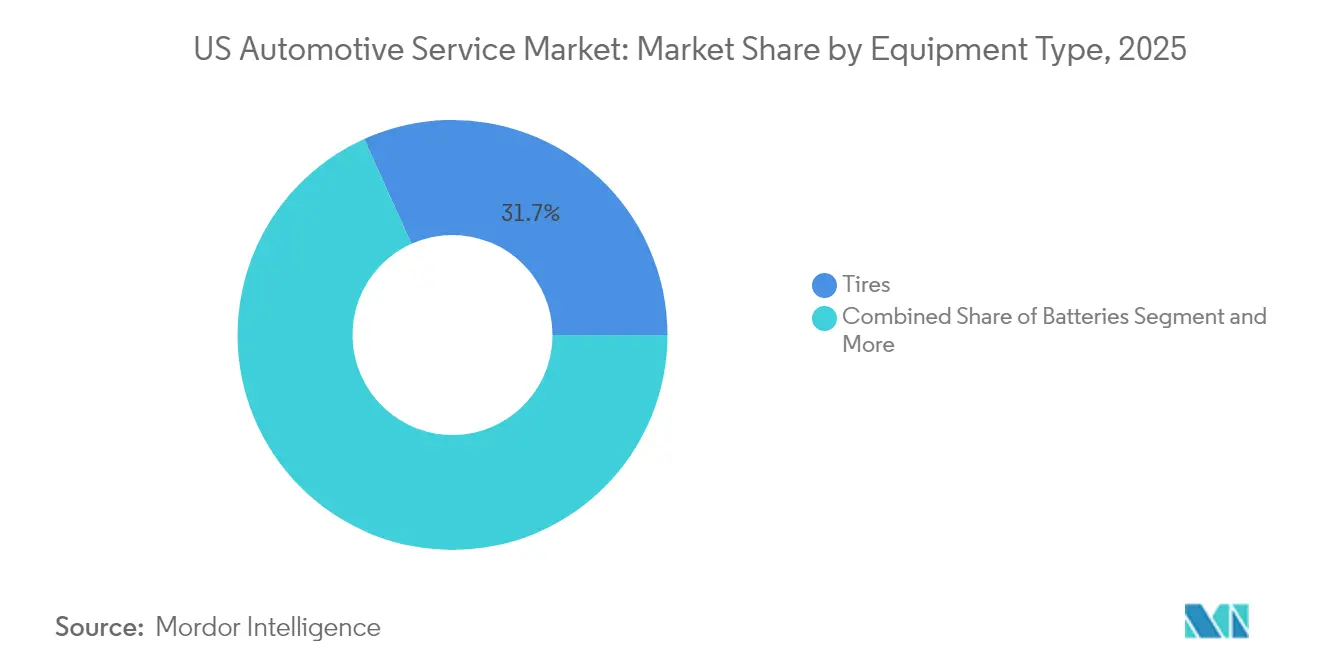

- By equipment type, tires represented 31.74% of the US automotive services market in 2025; ADAS sensors and cameras will advance the fastest, at a 9.14% CAGR through 2031.

- By service channel, OEM dealerships commanded a 41.05% share in 2025, yet mobile and on-demand services are projected to climb at a 9.18% CAGR over the forecast period.

- By geography, the South led with 34.71% revenue share in 2025, while the West is projected to register the strongest 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Automotive Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Vehicle Parc | +1.8% | National; Midwest & Northeast focus | Long term (≥ 4 years) |

| VMT Rebound Post-COVID | +1.2% | National; stronger in South and West | Medium term (2–4 years) |

| OEM After-Sales Programs | +0.9% | National; premium focus in coastal markets | Medium term (2–4 years) |

| Digital Booking Platforms | +0.7% | National; urban leadership | Short term (≤ 2 years) |

| Subscription Maintenance Bundles | +0.6% | National; early in West and Northeast | Medium term (2–4 years) |

| Right-to-Repair Laws | +0.5% | Regional; led by Massachusetts & Maine | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Vehicle Parc Surpassing 12.6 Years

Average vehicle age reached 12.6 years in 2024, creating a structural tailwind as units between six and fourteen years now form the largest service cohort. High new-vehicle prices above USD 45,000 and constrained inventories have extended ownership cycles, pushing more owners toward essential maintenance rather than replacement. Hybrid registrations swelled 181% from 2021 to 2024, setting the stage for future battery replacement revenue. Independent repair specialists captured nearly 45% of incremental service spend during the 2021 rebound, evidencing the segment’s appeal. High interest rates reinforce consumer emphasis on longevity, anchoring steady parts replacement demand even during economic slowdowns[1]“Consumer View on Connected Services,”, Auto Care Association, autocare.org.

Post-COVID Rebound in Vehicle Miles Traveled

Federal Highway Administration data show national VMT climbing 1.4% year-over-year to 274.8 billion miles in February 2024, fully matching pre-pandemic baselines and supporting growth in the US Automotive Service Industry. Long-haul truck mileage is projected to expand 1.1% annually through 2050, while single-unit truck activity may grow 1.9% per year, reinforcing commercial fleet maintenance needs. Higher miles intensify wear across an aging vehicle mix, boosting brake, tire, and fluid service demand. As post-pandemic driving surges, weekly mileage trends emerge as a key indicator for workshop activity. Relatively stable gasoline at USD 2.85 per gallon supports sustained travel, and rising consumer credit balances continue to divert budgets from new-car purchases toward aftermarket services.

OEM-Branded After-Sales Program Expansion

Automakers such as BMW, Volvo, and Porsche now bundle maintenance, software updates, and roadside assistance into subscription packages that streamline lifecycle management, reshaping customer expectations across the US Automotive Service Industry. Volkswagen’s Flex pilot in Atlanta integrates subscription fees with financing, embedding service retention inside monthly payments. Connected-car telematics allow automatic fault code transmission and proactive parts staging, delivering convenience that can shift loyalty away from independent shops. US drivers are willing to switch brands for superior connected services, underscoring the strategic value of data-enabled maintenance channels.

Digital Booking and CRM Platforms Proliferation

AI-driven scheduling tools raise booking conversion by up to 40% and cut administrative workload, according to Cox Automotive’s 2024 Vehicle Service Study[2]“2024 Vehicle Service Industry Study,”, Cox Automotive, coxautoinc.com. Steer CRM and AutoOps merged in 2024 to create an integrated platform bundling automated marketing, text reminders, and real-time capacity management. Online scheduling has become a trust builder as dealer ratings decline. Service centers leveraging predictive diagnostics roll out personalized maintenance plans based on driving patterns, enhancing upsell opportunities. Over 90% of consumers accepted mobile service appointments in recent dealer pilots, indicating a rapid shift toward convenience-first engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Lowers Routine Svc | -1.4% | National; highest in California & Northeast | Long term (≥ 4 years) |

| Technician Shortage | -1.1% | National; acute in urban markets | Medium term (2–4 years) |

| Inflation Defers Repairs | -0.8% | National; heavier in lower-income areas | Short term (≤ 2 years) |

| Telematics Dealer Lock-in | -0.6% | National; premium-brand concentration | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

EV Adoption Lowers Routine Service Intensity

Electric vehicles require fewer mechanical fluids and belts, trimming routine visits, yet each repair averages almost 50% higher than on an internal-combustion model, mainly due to battery and electronic complexity. Powertrain-agnostic work, such as tires and wiper blades, remains resilient, but the conventional aftermarket could contract by 2035. Only some of technicians report substantial EV training, generating a skills gap that favors large chains and dealer groups capable of funding high-voltage safety infrastructure. Independent shops servicing BEVs claimed a significant share in 2024, yet over half lack dedicated marketing to showcase that capability.

OEM Telematics Locking Customers into Dealerships

Proprietary data gateways let automakers transmit diagnostic trouble codes directly to dealer CRM systems, scheduling service without customer input. More EV owners choose dealer service for software and high-voltage work, reinforcing lock-in. The GAO found independent shops still face hurdles with advanced diagnostics, though the 2014 agreement covers basic mechanical information[3]“Vehicle Repair Data Access,”, U.S. Government Accountability Office, gao.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Dominate Volume While LCVs Accelerate Growth

Passenger cars accounted for 68.74% of the US automotive service market in 2025 as the segment’s large installed base demanded consistent maintenance. The US automotive service market size linked to passenger cars is projected to grow steadily as the average age surpasses 12 years and hybrid penetration deepens. Light commercial vehicles, buoyed by e-commerce and last-mile delivery, are set to record the fastest 8.55% CAGR through 2031, reshaping shop capacity planning and parts inventory strategies.

Fleet operators now specify preventative maintenance contracts that minimize downtime, driving predictable parts ordering for brakes, tires, and suspension. Tesla opened seventy new service centers in 2024, many exceeding 100,000 square feet, to cater to rising EV volume across both passenger and commercial segments. Medium and heavy trucks, though smaller in count, remain lucrative due to stringent uptime requirements and federal safety regulations that drive specialized service demand.

By Service Type: Electrical Work Surges Amid Mechanical Core

Mechanical repair and maintenance retained a 42.67% revenue share in 2025, anchoring the US automotive service market. Electrical and electronics work is forecast to grow at a 9.02% CAGR as ADAS penetration rises by 2031.

Shops invest in scan tools, calibration frames, and static targets to capture this margin-rich business. Due to mixed-material body structures, exterior and structural repairs remain stable yet more complex. Quick-lube chains diversify into battery, tire, and light mechanical jobs to offset longer EV oil-change intervals, preserving customer frequency.

By Equipment Type: ADAS Components Reshape Parts Mix

Tires held 31.74% of the US automotive service market in 2025, given predictable wear cycles and nationwide parts availability. ADAS sensors and cameras represent the fastest 9.14% CAGR through 2031, reflecting safety-system adoption mandates as the demand for precision calibration and OE-spec replacement parts increases.

Battery sales grew year-on-year as hybrid and start-stop systems aged into replacement windows. Seat and interior refurbishments maintain steady volumes thanks to ride-share wear and owner personalization. Tire service increasingly bundles post-alignment sensor resets, turning once-separate procedures into a unified value proposition

By Service Channel: Mobile Delivery Challenges Traditional Footprint

OEM dealerships retained 41.05% channel share in 2025 by pairing warranty coverage with connected-car diagnostics that drive service lane traffic. Independent general repair shops continue to thrive on localized relationships and competitive pricing, though telematics barriers test their resilience. Mobile and on-demand providers are projected to rise at a 9.18% CAGR, redefining convenience as a key differentiator in the US automotive service market.

More consumers are accepting of at-home appointments, and Ford, GM, and Volvo have each piloted mobile vans that handle light mechanical and software recalls. Valvoline’s USD 625 million Breeze Autocare buyout underscores quick-lube chains’ appetite for digital scheduling and regional economies of scale. GM dealers have serviced more than 11,000 Tesla vehicles since 2021, illustrating cross-brand service potential when tooling and training align

Geography Analysis

The South leads with 34.71% of the US automotive service market in 2025, supported by high vehicle ownership, pro-business regulations, and strong population growth in Texas and Florida. Service networks benefit from lower real estate costs and plentiful labor, allowing dense shop footprints catering to consumer and commercial fleets. Rural mileage exposure further enlarges replacement part demand, particularly for tires and suspension components.

The West records the fastest 8.12% CAGR through 2031 thanks to aggressive EV adoption and supportive infrastructure investments. California repair facilities report 45% more EV work orders in 2024, and 30% of collision claims now involve electric models. High disposable incomes in Western metros encourage uptake of premium subscription plans and mobile services, driving revenue per repair order above national averages.

Northeast and Midwest markets remain stable yet face harsh weather that accelerates corrosion and seasonal tire changeover, sustaining demand for underbody, brake, and battery work. Dense independent networks and long-standing customer relationships offset some dealership telematics advantages. Right-to-repair momentum is strongest in these regions, with Massachusetts pioneering data-access mandates that could influence national policy.

Competitive Landscape

The US automotive service market exhibits moderate fragmentation. Deals such as Mavis Tires & Brakes’ pending acquisition of the 1,200-store Midas chain and Valvoline’s USD 625 million purchase of Breeze Autocare add scale and digital capability to multistate operators. Thousands of independents still command meaningful local share, leveraging personalized service and community ties.

Strategic investment now centers on ADAS calibration bays, battery-handling equipment, and technician training scholarships tied to OEM partners. Goodyear’s Fleet HQ surpassed 5 million service events after integrating AI dispatch that pairs breakdown data with parts availability, demonstrating the technology’s role in utilization gains. White-space growth lies in mobile repair, EV-only service brands, and data-driven maintenance subscriptions.

Emerging disruptors blend software and service: Cox Mobile Service coordinates remote repairs; Tesla’s parts catalog and digital service manual access redefine transparency; and Bosch’s nationwide EV Training Tour supplies the credential pipeline. Sustainability also factors in, with Stonebriar Auto Services partnering with Quest Resource Management to close the loop on oil, tire, and antifreeze waste streams.

United States Automotive Service Industry Leaders

Monro Inc.

Firestone Complete Auto Care

Jiffy Lube International, Inc.

Valvoline Instant Oil Change

Goodyear Auto Service

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mavis Tires & Brakes reached terms to buy the 1,200-location Midas network, with closing expected by June 2025.

- April 2025: Big Brand Tire & Service acquired Reese’s Tire & Automotive Tire Pros, entering the Arizona market

- February 2025: Valvoline agreed to acquire Breeze Autocar for USD 625 million, adding about 200 Oil Changers stores across 17 states.

United States Automotive Service Market Report Scope

Automobile mechanical and electrical inspection, maintenance, and repair are examples of automotive services. The service industry includes routine services like oil changes, tire repair, and air conditioning and non-routine services like rust-proofing and exterior painting.

The United States Automotive Service Market is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Service Type (Mechanical, Exterior and Structural, and Electrical and Electronics), and Equipment Type (Tires, Seats, Batteries, and Other Equipment Types). The report offers market size and forecasts for the United States Automotive Service Market in value (USD Billion) for all the above segments.

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy Trucks |

| Mechanical Repair & Maintenance |

| Exterior & Structural (Body / Paint / Glass) |

| Electrical & Electronics |

| Quick Services (Oil, Fluids, Filters) |

| Tires |

| Batteries |

| Seats & Interiors |

| ADAS Sensors & Cameras |

| OEM Dealerships |

| Independent General Repair Shops |

| Quick-Lube & Tire Chains |

| Mobile / On-Demand Services |

| Northeast |

| Midwest |

| South |

| West |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium & Heavy Trucks | |

| By Service Type | Mechanical Repair & Maintenance |

| Exterior & Structural (Body / Paint / Glass) | |

| Electrical & Electronics | |

| Quick Services (Oil, Fluids, Filters) | |

| By Equipment Type | Tires |

| Batteries | |

| Seats & Interiors | |

| ADAS Sensors & Cameras | |

| By Service Channel | OEM Dealerships |

| Independent General Repair Shops | |

| Quick-Lube & Tire Chains | |

| Mobile / On-Demand Services | |

| By U.S. Census Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the US automotive after-sales services market?

The US automotive after-sales services market size is USD 211.14 billion in 2026, with a 5.90% CAGR outlook to 2031.

How will electrification affect service demand?

EVs need fewer routine jobs but drive higher-value repairs, requiring shops to add battery and high-voltage expertise.

Which region offers the fastest growth potential?

The West is forecast to grow at an 8.12% CAGR through 2031 thanks to aggressive EV adoption and supportive policies.

Why are technician shortages a critical issue?

The industry must replace technicians yearly, pushing wages up and stretching customer wait times beyond four weeks.

What service channel is expanding the quickest?

Mobile and on-demand services show a 9.18% CAGR outlook as consumers prioritize convenience and digital engagement.

Page last updated on: