Car Subscription Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

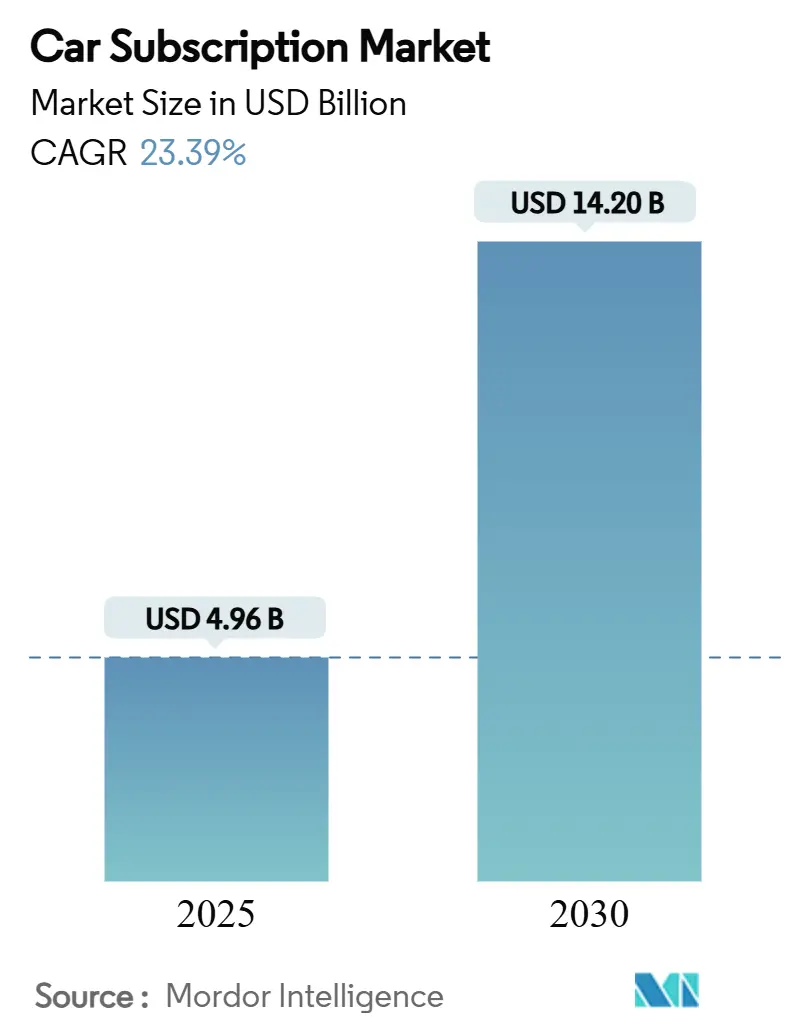

| Market Size (2025) | USD 4.96 Billion |

| Market Size (2030) | USD 14.20 Billion |

| Growth Rate (2025 - 2030) | 23.39% CAGR |

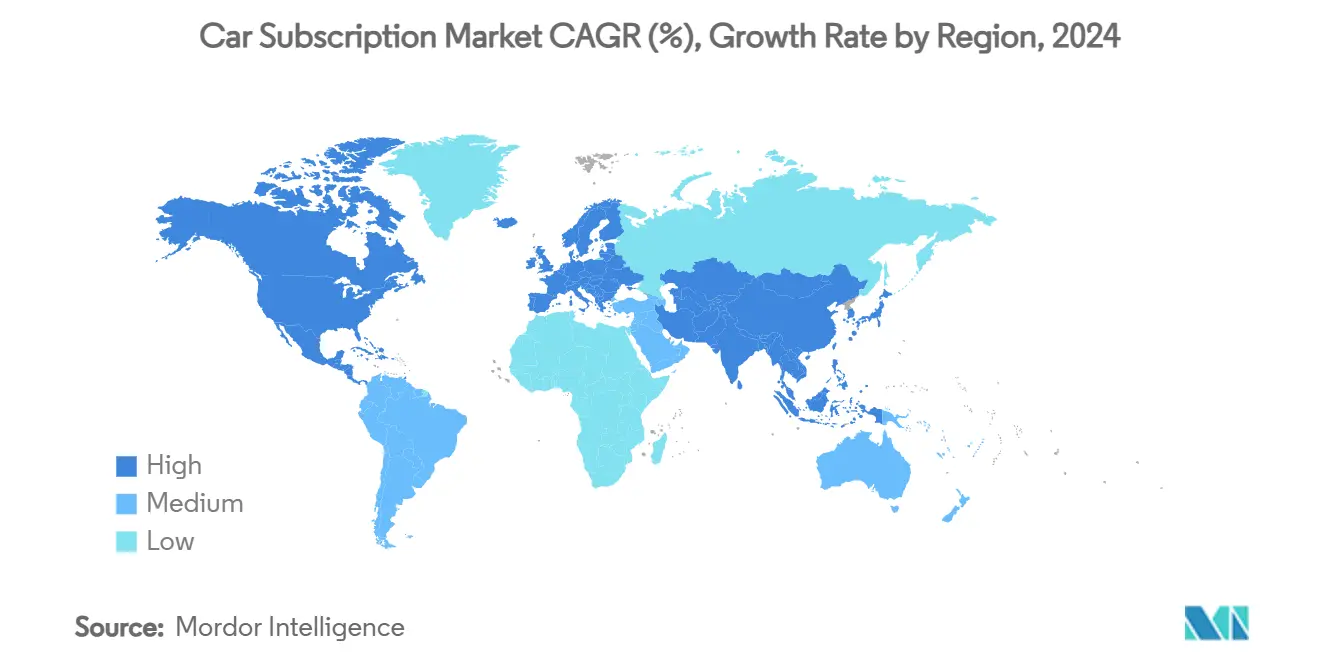

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Car Subscription Market Analysis by Mordor Intelligence

The car subscription market size stands at USD 4.96 billion in 2025 and is forecast to reach USD 14.20 billion by 2030, expanding at a 23.39% CAGR over the period. Demand accelerates as consumers shift from ownership to access-based mobility, a trend reinforced by OEM efforts to secure recurring revenue and by governments piloting distance-based road-usage charges. SaaS platforms that manage billing, telematics, and fleet logistics reduce entry costs, enabling dealers and technology firms to launch services quickly. Subscription propositions also resonate with prospective electric-vehicle (EV) users who worry about depreciation, battery obsolescence, and charging availability. Moderate competitive rivalry persists; OEM captives still hold scale advantages, yet agile mobility providers grow rapidly by offering multi-brand flexibility. Residual-value insurance products, data-driven pricing models, and policy support for low-emission transport together create sizable white-space opportunities for new entrants.

Key Report Takeaways

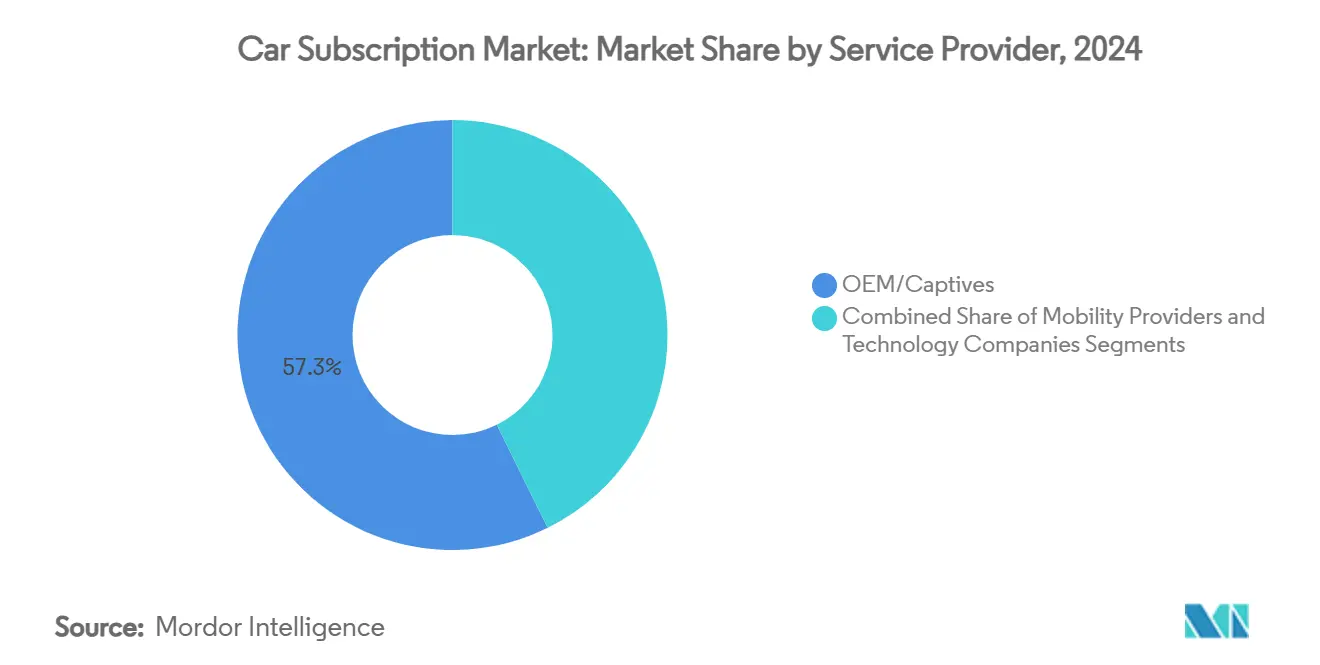

- By service provider, OEM/captives commanded 57.35% of the car subscription market share in 2024, while mobility providers recorded the highest projected CAGR at 28.65% through 2030.

- By subscription period, 6–12-month plans captured 48.10% revenue in 2024; 1–6-month plans are expected to advance at a 31.05% CAGR to 2030.

- By subscription type, single-brand programs held a 61.85% share in 2024, whereas multi-brand programs are poised to expand at a 29.35% CAGR over the forecast window.

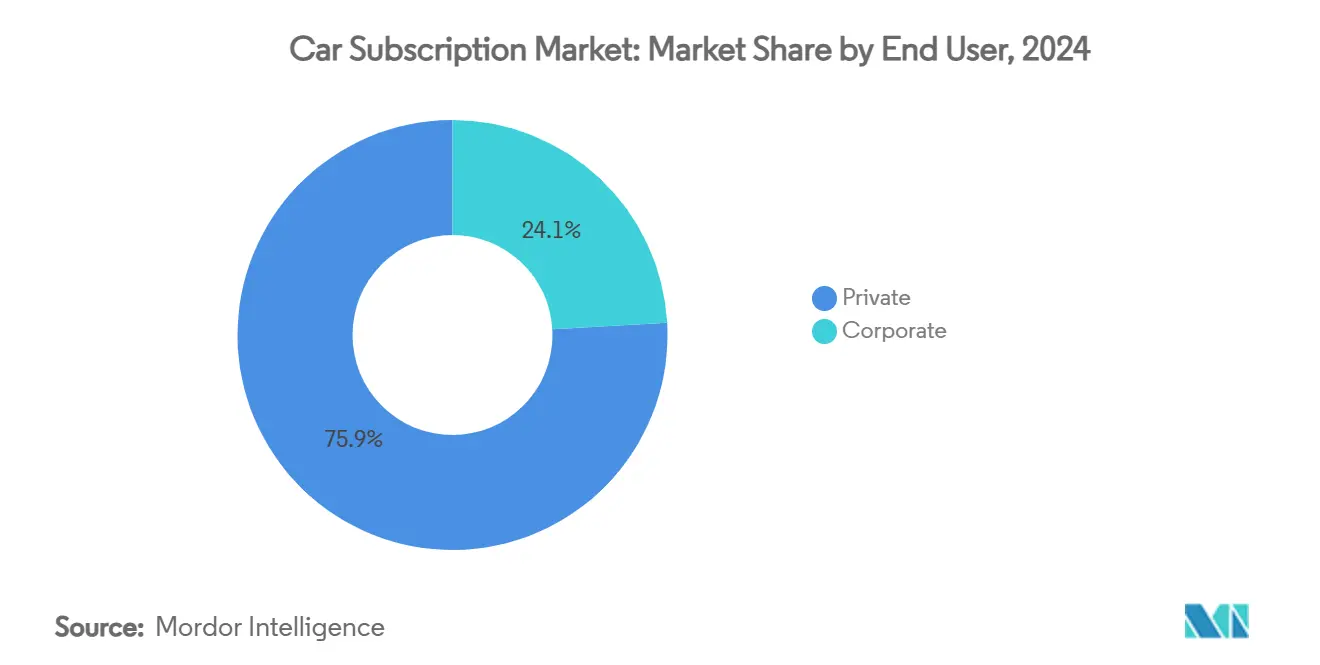

- By end user, private customers accounted for 75.95% of 2024 revenue, yet corporate plans show a robust 24.75% CAGR outlook to 2030.

- By propulsion, internal-combustion vehicles remained dominant at 82.60% share in 2024, but EV subscriptions are projected to surge at 37.65% CAGR through 2030.

- By geography, North America dominated with a 38.25% share in 2024, while Asia-Pacific demonstrated fastest growth at a CAGR of 32.15%.

Global Car Subscription Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flexible, Hassle-Free Vehicle Access | +5.8% | Global urban centers | Medium term (2–4 years) |

| OEM and Captive Lifetime-Value Strategies | +4.2% | North America, Europe | Long term (≥ 4 years) |

| EV Depreciation Mitigation | +3.7% | EV-leading regions | Short term (≤ 2 years) |

| SaaS Platform Proliferation | +2.9% | Tech-enabled markets | Medium term (2–4 years) |

| White-Label Dealer Platforms | +2.1% | APAC, Latin America | Long term (≥ 4 years) |

| Road-Usage-Pricing Pilots | +1.8% | Emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Flexible, Hassle-Free Vehicle Access

Consumer behavior transformation accelerates subscription adoption as consumers express interest in vehicle subscription services, with particularly strong appeal among the 18-44 year demographic. This shift reflects broader subscription economy penetration where convenience and predictable costs outweigh ownership benefits. The COVID-19 pandemic catalyzed preference changes as consumers prioritized safety, flexibility, and reduced financial commitments during economic uncertainty. Subscription models eliminate traditional ownership friction points, including maintenance scheduling, insurance management, and resale complexity. Urban consumers particularly value subscription services as parking costs, congestion charges, and limited vehicle utilization make ownership economically inefficient compared to on-demand access models.

OEM and Captive Financing Push to Retain Lifetime Customer Value

OEMs increasingly view subscriptions as customer retention mechanisms that extend engagement beyond traditional 3-4 year ownership cycles, with BMW's Financial Services segment reporting 12.7% growth in new leasing contracts during 2024[1]"BMW Group Corporate Communications," bmwgroup.com.. Mercedes-Benz Mobility integrates subscription offerings within broader digital transformation initiatives, targeting recurring revenue streams that stabilize cash flows and reduce dependence on cyclical vehicle sales. Toyota's KINTO expansion across Europe demonstrates OEM commitment to mobility services as strategic differentiators rather than ancillary revenue sources[2]"Toyota launches KINTO, a single brand for mobility services in Europe", kinto-mobility.eu.. Captive financing arms leverage existing customer relationships and credit expertise to offer competitive subscription terms while maintaining direct customer touchpoints. This strategy proves particularly effective in premium segments where brand loyalty and service quality command subscription premiums over third-party providers.

EV-Specific Depreciation Mitigation via Subscription Models

Electric vehicle depreciation challenges create compelling subscription use cases as EV residual values decline 15-20% faster than internal combustion vehicles, complicating traditional leasing economics. Subscription models allow providers to extend vehicle utilization periods before resale, potentially stabilizing residual values through increased mileage distribution across multiple users. Tesla's subscription approach for Full Self-Driving capabilities demonstrates how software-defined vehicles enable feature monetization throughout vehicle lifecycles, reducing dependence on hardware depreciation patterns. Battery technology advancement creates obsolescence risks that subscription models can mitigate by allowing consumers to access newer EV generations without ownership commitment. Insurance companies increasingly recognize residual value risks in EV transitions, with growing demand for residual value insurance products particularly in markets like China where manufacturers face regulatory pressure to develop leasing products.

SaaS Platform Proliferation Lowering Entry Barriers

Technology platform providers democratize subscription service deployment through white-label solutions that enable traditional automotive players to launch subscription offerings without extensive technology development. Loopit's USD 3.95 million funding round in 2024 demonstrates investor confidence in subscription enablement platforms that reduce operational complexity for OEMs, dealerships, and rental companies. Cloud-based subscription management systems integrate with existing dealer management systems, fleet tracking, and financial services infrastructure to streamline operations. API-driven architectures enable rapid deployment and customization of subscription offerings across different market segments and geographic regions. The convergence of connected vehicle data, mobile payment systems, and AI-driven customer experience platforms creates comprehensive subscription ecosystems that extend beyond basic vehicle access to include predictive maintenance, usage optimization, and personalized mobility services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thin Unit Economics and Residual-Value Risk | –3.4% | Global, EV-dense markets | Short term (≤ 2 years) |

| Low Consumer Awareness and Trust | –2.8% | Emerging markets, rural areas | Medium term (2–4 years) |

| Limited Residual-Value Insurance | –1.9% | Asia-Pacific emerging, Latin America, MEA | Long term (≥ 4 years) |

| OEM Channel Conflict | –2.1% | Dealer-centric jurisdictions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Thin Unit-Economics and Residual-Value Risk

Subscription providers face persistent profitability challenges as vehicle acquisition costs, insurance premiums, and maintenance expenses often exceed monthly subscription revenues, particularly during initial customer acquisition phases. FINN's strategic focus on core German markets and US operations pause reflects the capital intensity required to achieve sustainable unit economics. EV residual value volatility compounds these challenges as rapid technological advancement and changing consumer preferences create uncertainty around vehicle values at subscription term completion. Rental companies' retreat from EV fleets due to 56% higher repair costs and 50% lower resale values illustrates the operational complexity subscription providers must navigate[3]George Skentzos, "Why Rental Car Companies Are Breaking Up With EVs (And How Subscription Could Rekindle the Spark)," loopit, loopit.co.. Successful providers require sophisticated pricing models that account for utilization rates, customer behavior patterns, and regional market dynamics to achieve positive contribution margins. The approximately USD 200 billion in residual values tied to 8-10 million leased vehicles in the US demonstrates the scale of financial risk that subscription models must address through improved asset management and insurance strategies.

Low Consumer Awareness/Trust in New Model

Consumer education remains a significant barrier as subscription models blur traditional boundaries between ownership, leasing, and rental, creating confusion about value propositions and contractual obligations. Many consumers lack familiarity with subscription pricing structures, mileage limitations, and termination procedures, leading to hesitation in adoption despite stated interest in flexible mobility solutions. Trust concerns emerge around vehicle condition, maintenance standards, and provider reliability, particularly among consumers accustomed to ownership control over vehicle care and modifications. The UK government's consultation on subscription contract regulations reflects growing recognition that consumer protection frameworks must evolve to address subscription-specific issues including cooling-off periods, refund processes, and clear pre-contract information requirements. Marketing and customer acquisition costs remain elevated as providers invest in education campaigns and trial programs to build consumer confidence in subscription alternatives to traditional ownership models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Provider: OEM Captives Leverage Brand Loyalty

OEM/Captives command 57.35% market share in 2024, while Mobility Providers demonstrate the strongest growth trajectory at 28.65% CAGR through 2030, reflecting the competitive tension between established automotive players and technology-driven disruptors. Mercedes-Benz Mobility's integration of subscription services within broader digital transformation initiatives exemplifies how OEMs leverage existing customer relationships and brand equity to drive subscription adoption. Technology Companies maintain a smaller but strategically important position, focusing on platform enablement and data analytics capabilities that support subscription ecosystem development.

Mobility Providers gain market share through operational agility and customer-centric service design, often partnering with multiple OEMs to offer diverse vehicle portfolios that single-brand captives cannot match. Stellantis's Free2Move app launch demonstrates platform aggregation strategies that integrate car-sharing, rentals, and subscription services within unified digital experiences. Technology Companies increasingly focus on white-label solutions and data services, with Deloitte's partnership with Autonomy to launch Autonomy Data Services highlighting the convergence of consulting expertise and subscription technology platforms.

By Subscription Period: Flexibility Drives Shorter Terms

The 6-12 months segment holds 48.10% market share in 2024, though 1-6 months subscriptions expand at 31.05% CAGR as consumers prioritize maximum flexibility over cost optimization. This trend reflects broader subscription economy patterns where consumers prefer shorter commitment periods even at premium pricing, particularly in uncertain economic environments. More than 12 months subscriptions appeal to corporate customers and fleet managers seeking predictable costs and simplified vehicle management, though growth remains modest as these users often transition to traditional leasing arrangements for longer-term needs.

Consumer behavior research indicates that subscription appeal correlates inversely with commitment duration, with 78% of FINN's customers being first-time new car users who value the ability to exit subscriptions without penalties. Hyundai's Evolve+ program demonstrates market evolution toward ultra-flexible 28-day terms that accommodate seasonal usage patterns and life transitions. Pricing strategies increasingly reflect this flexibility premium, with shorter-term subscriptions commanding 20-30% higher monthly rates compared to longer commitments, though improved utilization rates and reduced customer acquisition costs may narrow these spreads over time.

By Subscription Type: Multi-Brand Platforms Gain Traction

Single-brand subscriptions will maintain 61.85% of the market share in 2024, leveraging OEM brand loyalty and simplified operations, while Multi-Brand offerings will grow at 29.35% CAGR as consumers seek vehicle variety and providers pursue platform economies. The single-brand dominance reflects OEM captive strategies and consumer preferences for consistent service experiences, particularly in premium segments where brand identity strongly influences purchase decisions. Multi-brand platforms face operational complexity around vehicle sourcing, maintenance standardization, and customer service consistency, though successful providers achieve differentiation through choice and convenience.

Platform aggregation strategies gain momentum as providers recognize that vehicle diversity drives customer acquisition and retention, with successful multi-brand operators developing sophisticated inventory management and customer matching algorithms. Astara's expansion into Chile with its multi-brand subscription platform demonstrates international scaling opportunities for providers that master operational complexity. The convergence of mobility-as-a-service platforms with subscription offerings creates opportunities for integrated transportation solutions that extend beyond personal vehicles to include public transit, micro-mobility, and ride-sharing services within unified subscription packages.

By End User: Corporate Adoption Accelerates

Private users dominate with 75.95% market share in 2024, though Corporate subscriptions expand at 24.75% CAGR as businesses recognize operational and financial benefits of subscription models over traditional fleet ownership. Corporate adoption accelerates due to simplified expense management, reduced administrative burden, and improved cash flow predictability compared to vehicle ownership or leasing arrangements. KINTO's partnership with office space and parking providers illustrates how subscription services integrate with broader corporate mobility and workspace solutions.

Private user growth reflects changing consumer attitudes toward ownership, particularly among urban millennials and Gen Z consumers who prioritize access over ownership across multiple product categories. Corporate users increasingly value subscription flexibility for seasonal workforce variations, project-based vehicle needs, and employee mobility benefits that traditional fleet arrangements cannot accommodate efficiently. The integration of subscription costs as business expenses provides tax advantages that enhance corporate value propositions, while private users benefit from bundled insurance, maintenance, and roadside assistance that simplify vehicle access and reduce unexpected costs.

By Propulsion Type: EV Subscriptions Address Adoption Barriers

ICE vehicles maintain 82.60% market share in 2024, though EV subscriptions demonstrate exceptional growth at 37.65% CAGR as consumers use subscription models to trial electric vehicles without long-term commitment risks. This growth pattern reflects subscription models' unique value proposition for EV adoption, allowing consumers to experience electric driving while avoiding concerns about technology obsolescence, charging infrastructure limitations, and resale value uncertainty. Toyota's integration of Alphard and Vellfire PHEV models into KINTO subscription services demonstrates OEM strategies to accelerate electrified vehicle adoption through flexible access models.

EV subscription growth benefits from government incentives and corporate sustainability initiatives that favor electric vehicle adoption, with subscription models enabling access to latest EV technologies without ownership depreciation risks. The 37.65% CAGR for EV subscriptions significantly exceeds overall EV market growth rates, indicating that subscription models serve as effective adoption catalysts for consumers hesitant about electric vehicle ownership. Battery leasing integration within EV subscriptions addresses range anxiety and battery replacement concerns while enabling providers to optimize battery lifecycle management and second-life applications that improve overall economics.

Geography Analysis

North America led with 38.25% of global revenue in 2024, leveraging deep credit markets, high smartphone usage, and early-adopter cultures. OEM captives such as BMW Financial Services and Mercedes-Benz Mobility bundle insurance and maintenance into flat-rate offers, resonating with suburban households that juggle multiple vehicles. State-level road-charge pilots and favorable tax treatment for business-use vehicles further entrench the vehicle subscription market in the region. Cross-border opportunities develop as Canadian provinces clarify insurance regulations that recognize subscription contracts distinct from rentals.

Asia-Pacific is the fastest-growing territory with a projected 32.15% CAGR to 2030, propelled by urbanization, EV leadership in China, and digital-payment ubiquity. HSBC notes that Chinese consumers increasingly favor asset-light mobility products as ride-hailing familiarity spills over into longer-term access models. Japan’s KINTO expansion confirms that mature automaker ecosystems can pivot toward services without cannibalizing retail sales. Southeast Asian governments encourage electrified-mobility pilots, positioning subscriptions as test beds for chargers, grid interactions, and fleet-energy management.

Europe maintains a steady upward path anchored by stringent emissions rules and congestion-pricing zones that make flexible access attractive. Germany’s robust used-car export channels help providers manage remarketing, supporting residual-value forecasts essential for profitable pricing. The United Kingdom reviews subscription-specific consumer-protection rules, a move expected to standardize contract transparency and accelerate trust. Integrated mobility passes that combine public transport, micromobility, and car subscriptions gain municipal backing, reflecting policy alignment with decarbonization targets across the bloc.

Competitive Landscape

The car subscription market exhibits moderate concentration with fragmented competitive dynamics as traditional automotive players, technology startups, and mobility service providers compete across different value chain segments. OEM captives leverage brand equity and existing customer relationships to maintain market leadership, while technology-enabled disruptors focus on operational efficiency and customer experience innovation. Market consolidation accelerates as evidenced by Volvo's Care by Volvo discontinuation and FINN's strategic focus on core markets, indicating that sustainable subscription models require significant operational scale and financial resources.

Strategic patterns emerge around platform aggregation, with successful providers developing multi-brand offerings and integrated mobility services that extend beyond basic vehicle access. Technology differentiation focuses on subscription management platforms, predictive analytics, and customer experience optimization, with companies like Loopit raising USD 3.95 million to enhance platform capabilities and market expansion. White-space opportunities exist in corporate fleet subscriptions, integrated mobility-as-a-service platforms, and emerging market expansion where traditional automotive financing remains underdeveloped. BMW's Remote Software Upgrade capabilities demonstrate how connected vehicle technologies enable subscription feature monetization and customer engagement throughout vehicle lifecycles.

Car Subscription Industry Leaders

-

Hyundai Motor Company

-

Hertz Global Holdings

-

Volvo

-

Kinto

-

Free2Move

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: KINTO partnered with Neally and Office Navi to provide integrated vehicle subscription, parking, and office space solutions for corporate customers in Japan, demonstrating subscription service convergence with broader business mobility needs.

- April 2025: Astara launched its Move subscription service in Chile, marking the company's fourth international market and first Latin American expansion with fully digital platform offering customizable subscription terms.

- December 2024: Toyota launched Alphard and Vellfire PHEV models through KINTO subscription service in Japan, enabling corporate customers to claim monthly fees as business expenses while accessing latest electrified vehicle technology.

Global Car Subscription Market Report Scope

| OEM/Captives |

| Mobility Providers |

| Technology Companies |

| 1 to 6 Months |

| 6 to 12 Months |

| More than 12 Months |

| Single Brand (Single-Brand Swap) |

| Multi Brand |

| Private |

| Corporate |

| Internal-Combustion Engine (ICE) |

| Electric Vehicle (EV) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Malaysia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | UAE |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service Provider | OEM/Captives | |

| Mobility Providers | ||

| Technology Companies | ||

| By Subscription Period | 1 to 6 Months | |

| 6 to 12 Months | ||

| More than 12 Months | ||

| By Subscription Type | Single Brand (Single-Brand Swap) | |

| Multi Brand | ||

| By End User | Private | |

| Corporate | ||

| By Propulsion Type | Internal-Combustion Engine (ICE) | |

| Electric Vehicle (EV) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | UAE | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the vehicle subscription market?

The vehicle subscription market size is valued at USD 4.96 billion in 2025 and is projected to reach USD 14.20 billion by 2030.

What CAGR is anticipated for vehicle subscriptions between 2025 and 2030?

The forecast calls for a 23.39% CAGR over the period, reflecting strong consumer demand for access-based mobility.

Which region holds the largest share of vehicle subscription revenue?

North America leads with 38.25% of 2024 revenue due to mature credit systems and early adoption of subscription models.

Why are EV subscriptions growing faster than overall market averages?

EV subscriptions mitigate depreciation risk, give users a chance to test charging infrastructure, and align with corporate sustainability goals, resulting in a 37.65% CAGR outlook.

Page last updated on: