Automotive Safety Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

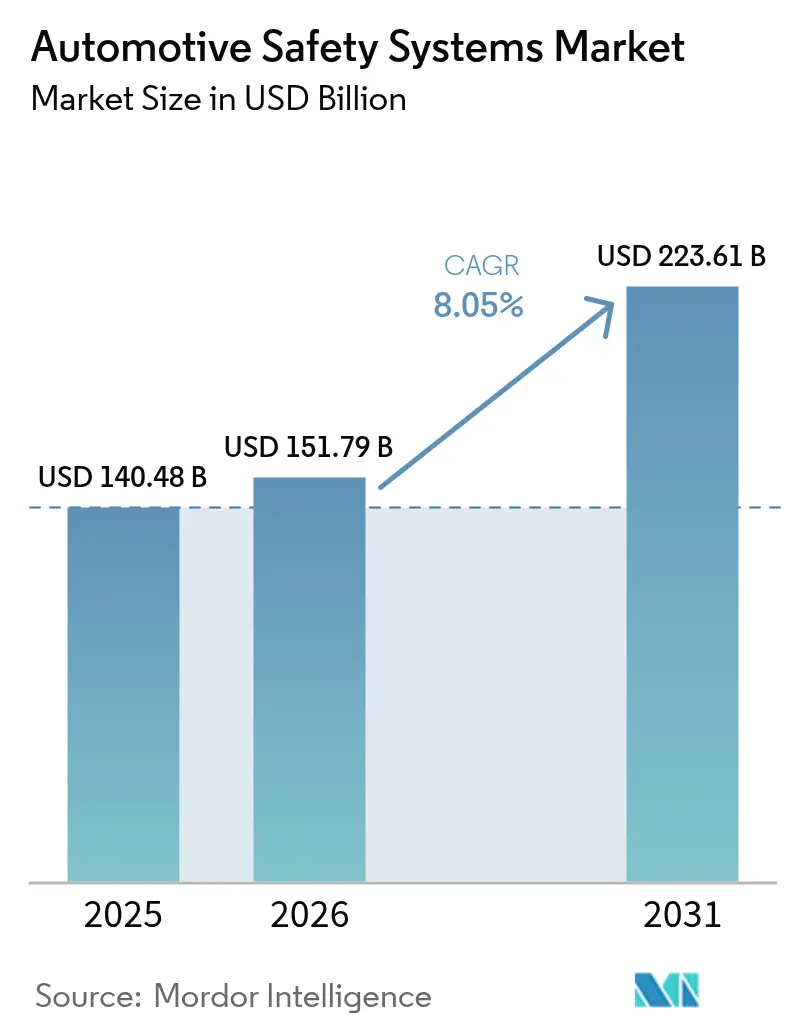

| Market Size (2026) | USD 151.79 Billion |

| Market Size (2031) | USD 223.61 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

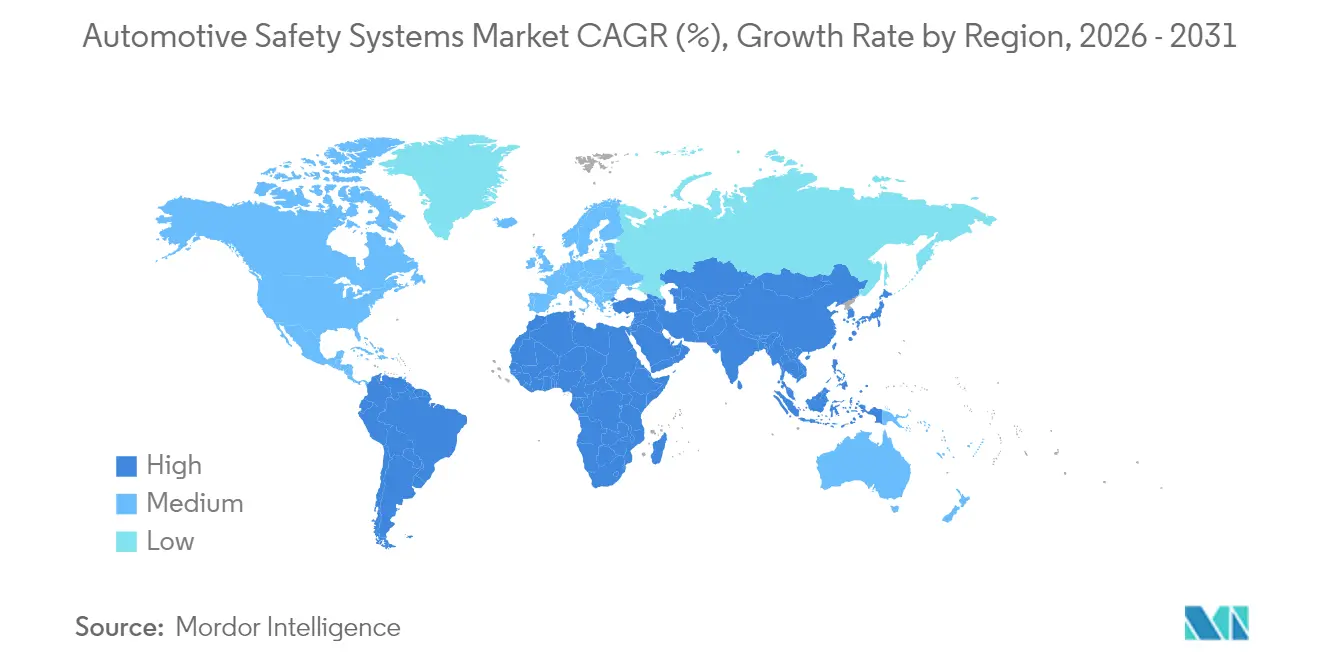

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Safety Systems Market Analysis by Mordor Intelligence

The Automotive Safety Systems market size is expected to grow from USD 140.48 billion in 2025 to USD 151.79 billion in 2026 and is forecast to reach USD 223.61 billion by 2031 at 8.05% CAGR over 2026-2031. Demand reflects simultaneous progress in global safety regulation, rapid sensor price erosion, and the rise of software-defined vehicles that permit over-the-air upgrades. The shift from hardware-only restraint devices toward integrated sensor-plus-software platforms allows vehicles to predict, avoid, and mitigate collisions in real time. Automakers now package active braking, lane keeping, driver monitoring, and cyber-secure update pathways as standard content, especially in markets where star-rating programs influence buying behavior.

Key Report Takeaways

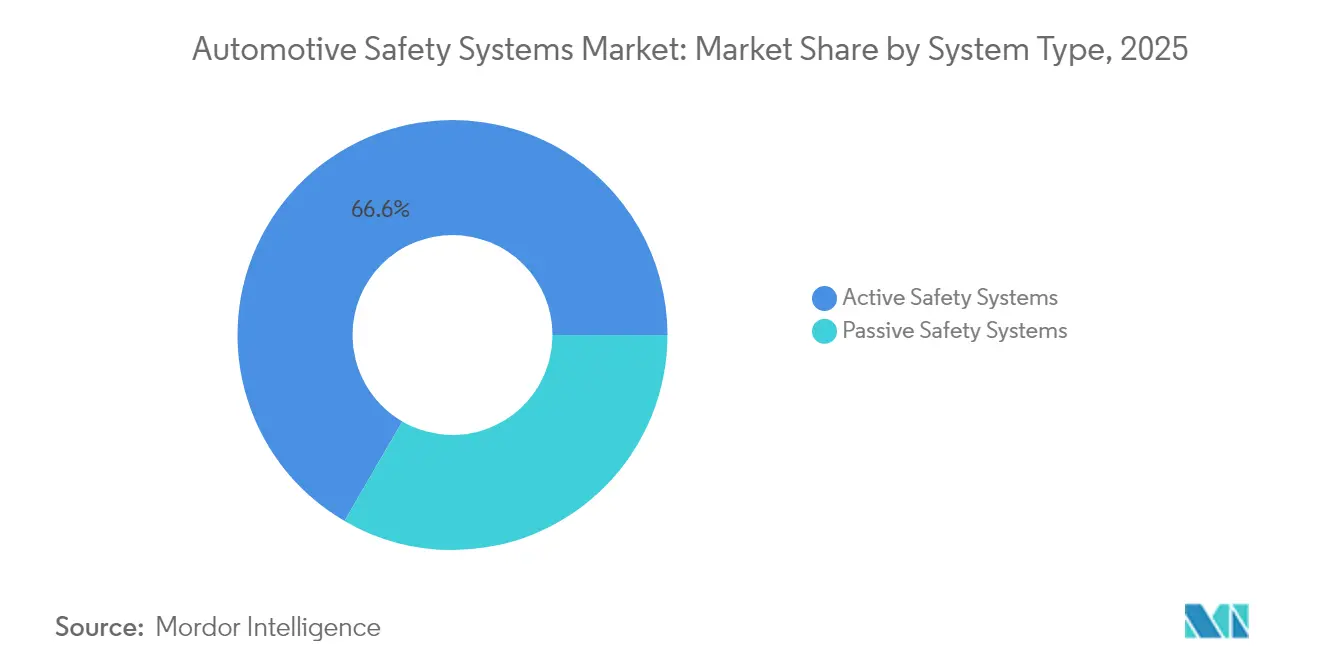

- By system type, Active Safety Systems led with 66.62% of the automotive safety system market share in 2025; in-cabin biometric analytics is projected to expand at an 8.27% CAGR through 2031.

- By technology component, radar commanded 34.08% revenue share in 2025, while LiDAR is on track for an 8.49% CAGR to 2031.

- By end-user, OEM factory-fit solutions represented 83.05% share in 2025; the aftermarket is forecast to grow at an 8.55% CAGR.

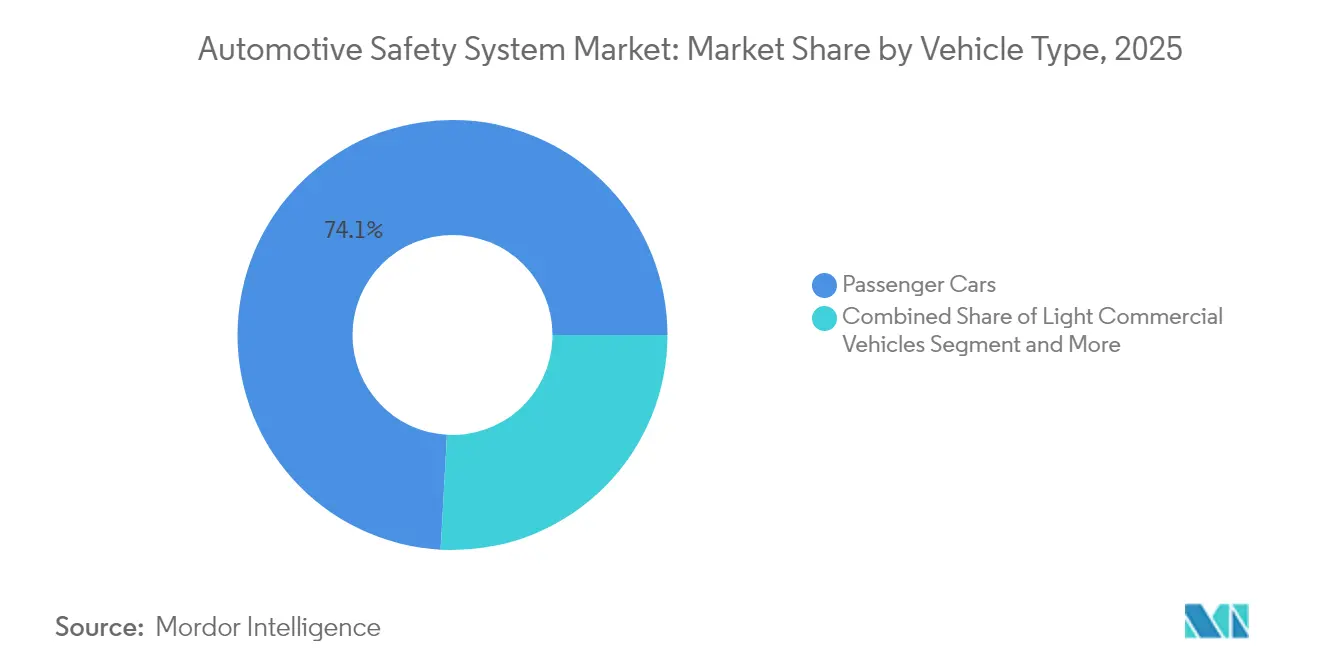

- By vehicle type, passenger cars held 74.12% share in 2025, whereas heavy commercial vehicles are expected to register an 8.16% CAGR through 2031.

- By propulsion, ICE models captured 77.65% share in 2025, while battery-electric vehicles are poised for a 8.98% CAGR to 2031.

- By geography, Asia Pacific accounted for 39.42% revenue in 2025; South America shows the fastest expansion at an 8.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Safety Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Global NCAP and UNECE Safety | +2.1% | Global, with early adoption in EU and China | Short term (≤ 2 years) |

| Rapid Sensor-Cost Deflation | +1.8% | Global, with strongest impact in APAC and North America | Medium term (2-4 years) |

| Boom in Software-Defined Vehicles | +1.5% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Shift Toward Level-2+ Autonomy | +1.3% | North America and EU core markets | Long term (≥ 4 years) |

| Rise of AI-Based in-Cabin Biometric Safety Analytics | +0.9% | Global, with premium segment leadership | Medium term (2-4 years) |

| Bundling of Vehicle-Safety Data into Usage-Based Insurance | +0.7% | North America and EU, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global NCAP & UNECE Safety Mandates

Euro NCAP protocols for 2026 require pedestrian automatic emergency braking and driver monitoring across all model classes, creating a common compliance baseline. China’s Ministry of Industry and Information Technology introduced rules in 2025 that obligate type approval for every software update touching safety functions. The EU General Safety Regulation II, in force since July 2024, obliges intelligent speed assistance and emergency lane keeping on every new vehicle. NHTSA updated its New Car Assessment Program to add blind-spot warning, lane keeping assistance, and pedestrian AEB for 2026 models, signaling a decade-long push for active safety. Global alignment lets manufacturers spread development cost across larger volumes and catalyzes faster diffusion of advanced functions.

Rapid Sensor-Cost Deflation Enabling ADAS Standardisation

Automotive radar prices now fall nearly 18% each year, while processor capability doubles every 18 months, permitting high-performance perception at entry-segment price points. Four-dimensional imaging radar brings centimeter-grade detection accuracy at cost levels close to legacy 3-D units, broadening use beyond adaptive cruise control. Image sensors benefit from smartphone supply chains: 8-megapixel automotive chips with HDR are available below USD 10. NITI Aayog projects semiconductor value per vehicle to double to USD 1,200 by 2030, led by ADAS content. The declining cost curve allows the automotive safety system market to extend Level-1 and Level-2 features to compact cars sold in Asia and Latin America.

Boom in Software-Defined Vehicles (OTA Safety Feature Upgrades)

Centralised compute architectures decouple safety logic from fixed hardware, enabling continual feature growth after sale. HARMAN OTA 12.0 already manages secure updates for more than 40 brands, coordinating high-performance computers and legacy ECUs in the same vehicle domain.[1]“HARMAN Advances OTA 12.0 Platform,” HARMAN, news.harman.com Sibros Deep Updater, certified to ISO 26262 ASIL-D, uses delta files to trim download size, lowering cellular data cost while keeping critical functions current.[2]“Sibros Deep Updater Achieves ASIL-D,” Sibros, sibros.tech UNECE Regulation R156 now requires a software-update management system on every new model, giving cybersecurity parity with the physical safety layer. Subscription pricing for premium AEB algorithms is emerging, creating fresh revenue streams inside the automotive safety system market.

Shift Toward Level-2+ Autonomy in Commercial Vehicles (Fleet TCO Play)

Fleet operators adopt advanced safety packages that cut collision claims by up to 90% and trim yearly accident-related costs by roughly USD 6,000 per heavy truck. The 2024 Work Truck Fleet Safety Study shows that majority of fleets ranking well-maintained vehicles with ADAS as their top priority, and nearly half already equip backup cameras and air-disc brakes. Automated driving systems reduce fatigue-related incidents and let fleets experiment with capacity-as-a-service models that increase asset utilisation. While true driverless operations remain long-term, Level-2+ functionality offers tangible cost benefits that propel the automotive safety system market in commercial segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation and Homologation Cost | -1.2% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Chip-Set Supply Volatility | -0.8% | Global, with acute impact in APAC manufacturing | Short term (≤ 2 years) |

| Cyber-Physical Attack Risk | -0.6% | Global, with highest exposure in connected vehicle markets | Medium term (2-4 years) |

| High-Voltage Electromagnetic Interference and Thermal Loads | -0.4% | Global, concentrated in premium EV segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation & Homologation Cost for Multicountry Compliance

Manufacturers must reconcile China’s C-NCAP 2024 test matrix with Euro NCAP 2026 requirements, often repeating crash and software validation for similar scenarios. TÜV SÜD now runs mandatory penetration testing under EU rules, adding months of cybersecurity reviews before market release. ISO/SAE 21434 demands threat analysis across the full vehicle lifecycle, lengthening development schedules and raising costs for small automakers. These factors slow the spread of cutting-edge features in cost-sensitive markets, restraining part of the automotive safety system market until harmonisation improves.

Chip-Set Supply Volatility Delaying OEM Safety Roll-Outs

Automotive-grade radar and vision chips must withstand extended temperature ranges and meet zero-defect targets, limiting the pool of qualified suppliers. Geopolitical events and natural disasters tighten allocation for key image sensors, while domain-controller processors carry lead times beyond 30 weeks. OEMs adopt dual-sourcing and buffer inventory strategies, yet sporadic shortages still force feature de-contenting on high-volume models. Supply uncertainty particularly disrupts APAC plants that rely on just-in-time logistics, creating a headwind for the automotive safety system market in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Active Safety Systems Cement Leadership

Active Safety Systems generated the largest slice of the automotive safety system market size at 66.62% in 2025. Automated emergency braking, adaptive cruise, lane keeping, and driver monitoring now appear in mid-range trims as Euro NCAP and NHTSA protocols grow stricter. Competitive intensity rises as suppliers integrate radar, camera, and LiDAR data through domain controllers that run machine-learning models in real time. The segment also benefits from fleet demand, with insurers offering premium discounts for trucks equipped with crash-avoidance technology.

In-cabin biometric platforms stand out as the fastest subsegment, advancing at an 8.27% CAGR to 2031. These solutions track driver alertness, heart rate, and even oxygen saturation, issuing proactive warnings before dangerous conditions emerge. As cabin sensors link with active braking controllers, occupants receive a closed-loop safety envelope that anticipates both external and internal threats. Passive safety remains relevant through smart airbags and adaptive seat belts that fit new seat layouts in autonomous vehicles, yet growth stays moderate.

By Technology Component: Radar Dominates as LiDAR Scales

Radar modules accounted for 34.08% of the automotive safety system market in 2025, underpinned by cost-effective 77-GHz chipsets that function reliably in rain, snow, and fog. The move to 4-D imaging radar sharpens angle resolution and permits object classification, narrowing the performance gap with LiDAR at a lower bill of materials. Camera systems continue to leverage smartphone economics, letting OEMs add 360-degree vision for parking and low-speed manoeuvres.

LiDAR registers the quickest expansion at an 8.49% CAGR, supported by solid-state architectures that trim moving parts and cut price per sensor. Level-3 highway-pilot launches in premium sedans rely on forward-facing LiDAR for redundant depth perception and road debris detection, accelerating adoption. Control units merge braking, steering, and perception data into single chips, reducing wiring and weight. Software innovations that apply self-learning algorithms on edge processors differentiate suppliers as the automotive safety system market transitions toward predictive safety.

By End-User: OEM Factory-Fit Dominance Meets Retrofit Demand

OEM factory-fit installations captured 83.05% of the automotive safety system market in 2025 thanks to platform-wide integration of sensors, controllers, and software validated under strict quality gates. Centralised sourcing reduces warranty exposure and unlocks scale economics, allowing automakers to meet regulatory mandates without unplanned cost spikes. Continuous over-the-air improvement further cements the OEM channel as vehicles gain value throughout the service life.

Aftermarket solutions, though smaller, expand at an 8.55% CAGR through 2031. Fleet operators retrofit collision-warning cameras, side radar, and driver monitoring units to older trucks, achieving immediate insurance savings and compliance with tightening safety rules. Suppliers now offer plug-and-play kits that integrate with telematics gateways, easing installation time. Usage-based insurance carriers promote adoption by lowering premiums for vehicles that transmit verified safe-driving metrics, adding momentum to this slice of the automotive safety system industry.

By Vehicle Type: Passenger Cars Remain Core as Trucks Accelerate

Passenger cars controlled 74.12% of the automotive safety system market in 2025, reflecting sheer volume and consumer expectation for high safety scores. Automakers standardise AEB and lane keeping on entry hatchbacks, while premium badges add highway-pilot functions with redundant LiDAR sensing. Interior innovation targets occupant status detection to secure future Euro NCAP stars.

Heavy commercial vehicles represent the quickest-growing class with an 8.16% CAGR to 2031. Fleet economics favour investment in lane centring, adaptive steering, and camera-based blind-spot elimination that together reduce collision frequency by majority. The automotive safety system market size for trucks is further buoyed by driver shortages and hours-of-service restrictions, pushing operators toward partially automated mileage that keeps rigs rolling longer without compromising safety.

By Propulsion: Electrification Introduces New Safety Layers

ICE models still dominate, holding 77.65% share of the automotive safety system market in 2025. The legacy fleet and mature supply chains ensure consistent demand for airbags, seat belts, and cost-optimised ADAS. Hybrid and fuel-cell platforms add battery management and hydrogen leak detection, but account for modest volume today.

Battery-electric vehicles form the fastest-moving propulsion group at a 8.98% CAGR. High-energy packs demand thermal runaway suppression, while chassis layouts with skateboard batteries alter crash kinematics and sensor field-of-view requirements. Hyundai Mobis unveiled a self-extinguishing battery that activates within five minutes of temperature spike, integrating seamlessly with existing airbag controllers. Extra weight from packs also drives adoption of brake-by-wire and regenerative coordination to shorten stopping distance, enriching opportunities across the automotive safety system market.

Geography Analysis

Asia Pacific retained the largest regional position with 39.42% share of the automotive safety system market in 2025. China’s MIIT rules compelling approval for every ADAS software update foster a robust compliance ecosystem that speeds feature rollout. Technology – auto convergence appears in partnerships such as Huawei and Xpeng, which co-develop domain controllers integrating radar, camera, and LiDAR on a common software stack. Japan nurtures AI-driven start-ups that pilot autonomous shuttles for urban centres, while India’s tighter crash regulations boost demand for cost-optimised airbags and AEB in compact cars.

South America posts the highest growth, advancing at an 8.51% CAGR through 2031. Stellantis committed EUR 5.6 billion between 2025 and 2030 to launch more than 40 models from local plants, each aligned with Euro NCAP test protocols. Brazil, Argentina, and neighbouring markets harmonise safety laws, letting global suppliers replicate validated sensor suites without custom tuning. Bio-hybrid powertrains that blend ethanol engines with battery packs open fresh integration tasks for thermal and electrical safety systems.

North America and Europe uphold mature positions with high per-vehicle content and software-defined vehicle regulations. The automotive safety system market share in these regions remains stable, yet value per unit rises as UNECE Regulation 155 enforces full cybersecurity, obliging every safety ECU to meet anti-hacking standards. The Middle East and Africa progress from low baselines, stimulated by infrastructure expansion, yet local climate extremes drive demand for robust sensor housings and dust-proof radar enclosures.

Competitive Landscape

The automotive safety system market features moderate consolidation led by Bosch, Continental, ZF, and Autoliv, each running global manufacturing and software-engineering hubs. Continental’s new Aumovio brand highlights its pivot to software-centric offerings, combining cameras, high-performance controllers, and cloud analytics into a unified package.[4]“Launch of Aumovio,” Continental, continental-press.com ZF merged its Active Safety and Chassis units into a single division, rolling out brake-by-wire on 5 million vehicles and delivering China’s inaugural steer-by-wire system for the Nio ET9. Autoliv collaborates with XPENG AEROHT to create dual-use restraint solutions for both road and low-altitude e-VTOL vehicles.

Semiconductor companies deepen their role. Qualcomm’s acquisition of Autotalks extends its V2X capabilities, embedding direct vehicle-to-infrastructure communication inside the Snapdragon Digital Chassis. Bosch works with Microsoft to infuse generative AI into automated-driving software development pipelines. Volkswagen’s Cariad and Bosch co-develop a Level-3 highway pilot for mass-production vehicles from 2026. Start-ups focused on in-cabin biometrics attract OEM pilots, while Aptiv showcases a modular ADAS stack tailored for commercial fleets that need quick retrofit in regional depots.

Cybersecurity expertise becomes a prerequisite as UN R155 mandates continuous monitoring of attack vectors across the connected vehicle. Suppliers invest in secure gateway architectures and intrusion-detection analytics to maintain homologation. Partnership models extend to cloud providers for safe over-the-air update pipelines, underscoring the convergence between information security and functional safety across the automotive safety system industry.

Automotive Safety Systems Industry Leaders

Continental AG

ZF Friedrichshafen AG

Magna International

Robert Bosch GmbH

Autoliv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qualcomm acquired Autotalks to enhance V2X communications solutions and boost road-safety capabilities, bolstering the Snapdragon Digital Chassis portfolio.

- April 2025: Continental introduced the Aumovio brand focused on software-defined vehicles and autonomous mobility solutions featuring advanced sensors and smart displays.

- January 2025: ZF formed the Chassis Solutions Division by combining Active Safety Technology and Passenger Car Chassis Technology, leading to brake-by-wire deployment on 5 million vehicles.

Global Automotive Safety Systems Market Report Scope

The automotive safety system comprises all the devices, components, sensors, and electronics parts responsible for maintaining vehicle safety standards. Moreover, the report covers a comprehensive breakdown of government regulatory policies across all the regions.

The automotive safety system market is segmented by system type, End-user type, Vehicle Type, and Geography. By System Type, the market is segmented into lane departure warning systems and other onboard safety systems. By end-user type, the market is segmented into OEM and aftermarket.

By Vehicle Type, the market is segmented into passenger cars and commercial vehicles, and by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Africa. For each segment, market sizing and forecast have been done on the basis of value (USD billion).

| Active Safety Systems | Collision-Avoidance (AEB, FCW) |

| Driver Monitoring & HMI Alerts | |

| Chassis Control (ESC, ABS) | |

| Passive Safety Systems | Airbags (Frontal, Side, Curtain, Far-side) |

| Seat-belt & Pretensioners |

| Sensors |

| Radar |

| Camera |

| LiDAR/Ultrasonic |

| Control Units and Domain Controllers |

| Software & Algorithms |

| OEM Factory-Fit |

| Aftermarket / Retrofit |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles & Buses |

| Internal Combustion Engine (ICE) |

| Battery-Electric Vehicles (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By System Type | Active Safety Systems | Collision-Avoidance (AEB, FCW) |

| Driver Monitoring & HMI Alerts | ||

| Chassis Control (ESC, ABS) | ||

| Passive Safety Systems | Airbags (Frontal, Side, Curtain, Far-side) | |

| Seat-belt & Pretensioners | ||

| By Technology Component | Sensors | |

| Radar | ||

| Camera | ||

| LiDAR/Ultrasonic | ||

| Control Units and Domain Controllers | ||

| Software & Algorithms | ||

| By End-User | OEM Factory-Fit | |

| Aftermarket / Retrofit | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles & Buses | ||

| By Propulsion | Internal Combustion Engine (ICE) | |

| Battery-Electric Vehicles (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive safety system market?

The market generated USD 151.79 billion in 2026 and is projected to reach nearly USD 223.61 billion by 2031.

Which system type leads revenue?

Active Safety Systems dominate with 66.62% share in 2025, reflecting regulatory pressure for collision-avoidance functions.

Why is LiDAR gaining momentum despite radar dominance?

LiDAR delivers higher depth accuracy for Level-3 autonomy, leading to an 8.49% CAGR that outpaces other components within the automotive safety system market.

How fast is the aftermarket for safety technology growing?

Retrofit solutions for fleets are expected to rise at an 8.55% CAGR as operators chase insurance savings and regulatory compliance.

Which region shows the strongest growth outlook?

South America leads with an 8.51% CAGR to 2031, supported by major OEM investments and harmonised safety standards.

What role do over-the-air updates play in vehicle safety?

OTA platforms allow automakers to fix vulnerabilities and add new safety features post-sale, aligning with UNECE R156 requirements and expanding recurring revenue opportunities.

Page last updated on: