Automotive Data Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

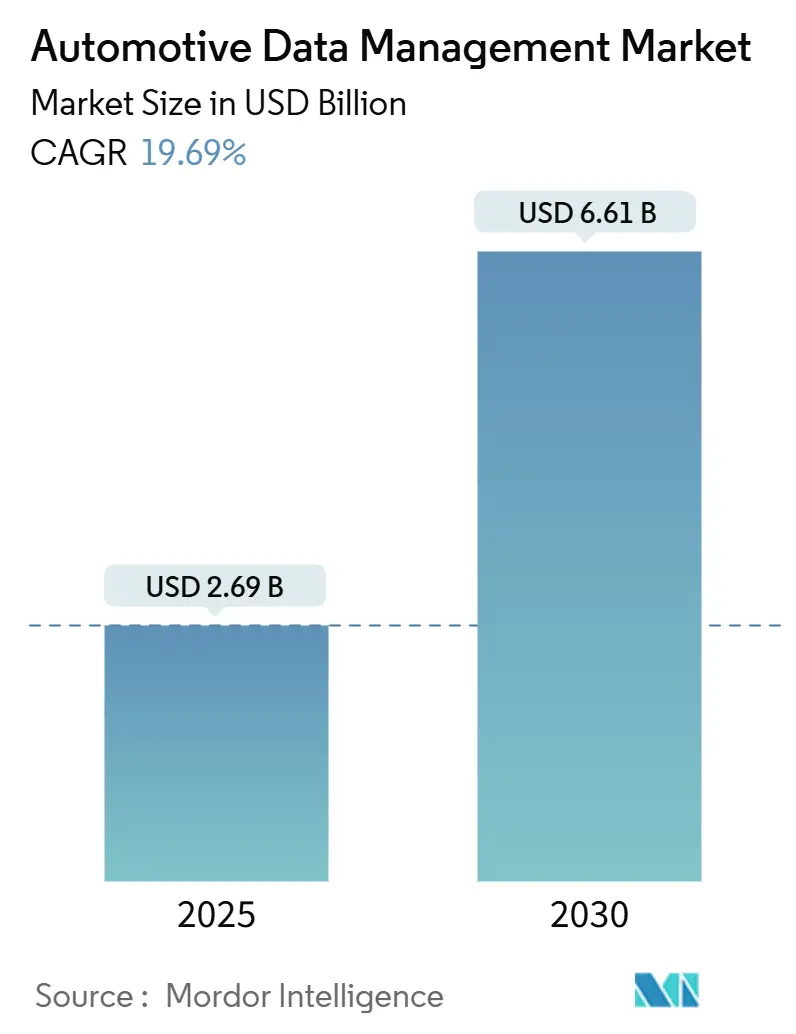

| Market Size (2025) | USD 2.69 Billion |

| Market Size (2030) | USD 6.61 Billion |

| Growth Rate (2025 - 2030) | 19.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Data Management Market Analysis by Mordor Intelligence

The automotive data management market size stood at USD 2.69 billion in 2025 and is projected to reach USD 6.61 billion by 2030, expanding at a 19.69% CAGR. Growth stems from connected- and autonomous-vehicle data surges, wider cloud adoption, and the rapid shift to software-defined architectures. Modern vehicles now generate up to 25 GB of data per hour, and advanced prototypes can exceed 4 TB daily, demanding scalable analytics back-ends and edge intelligence. Cloud deployment dominates because elastic infrastructure cuts infrastructure costs by 40-60%, shortens AI model-training cycles, and supports global over-the-air update strategies. Services revenues rise quickly as OEMs and Tier-1 suppliers outsource implementation complexity, compliance monitoring, and life-cycle optimization. Meanwhile, geopolitical emphasis on digital sovereignty and cybersecurity requirements sustains on-premise and hybrid designs in safety-critical settings.

Key Report Takeaways

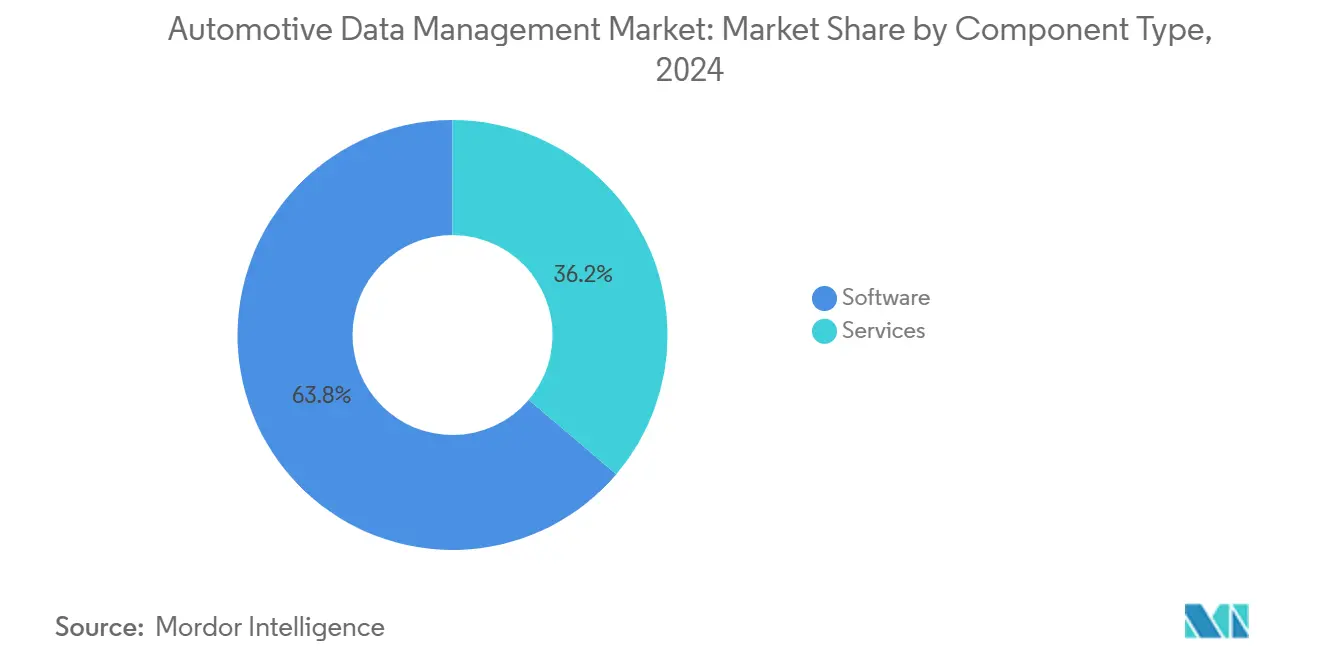

- By component type, software led with 63.78% revenue share in 2024; services are forecasted to expand at a 20.28% CAGR through 2030.

- By vehicle type, non-autonomous vehicles held 68.84% of the automotive data management market share in 2024, while autonomous vehicles are advancing at a 27.54% CAGR through 2030.

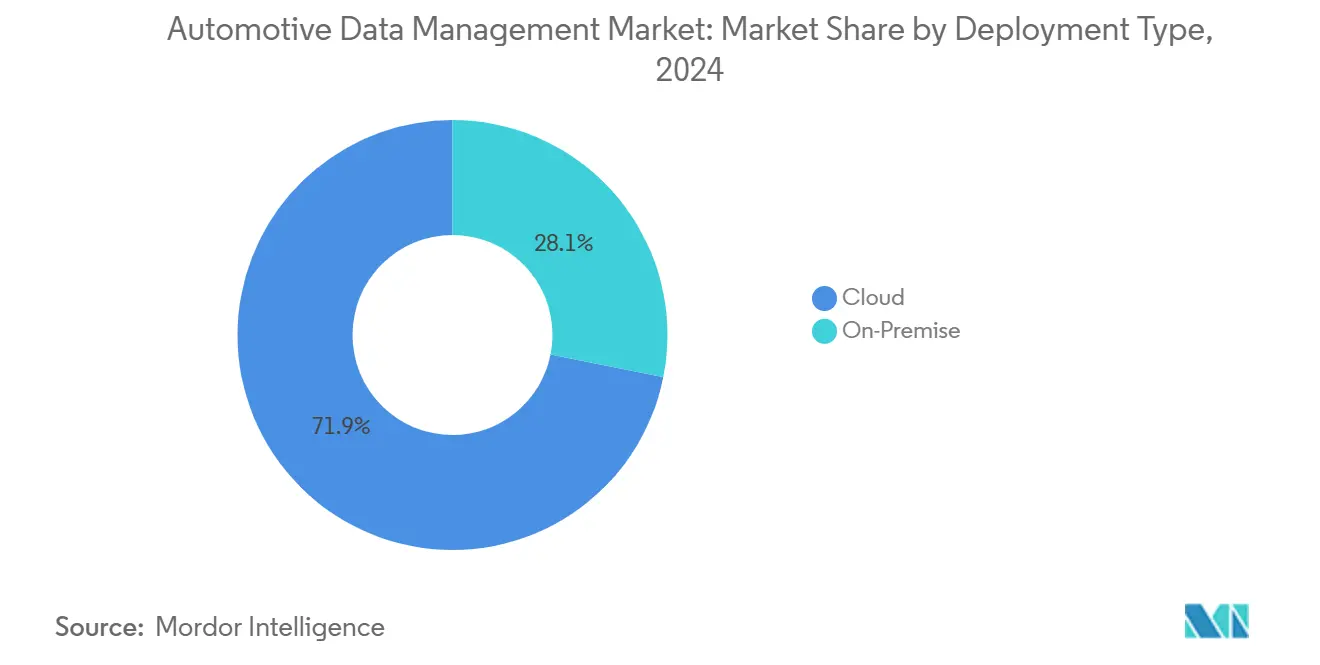

- By deployment type, cloud captured 71.87% revenue of the automotive data management market in 2024, projected to grow at a 26.64% CAGR to 2030.

- By data type, structured data commanded 56.69% of the automotive data management market size in 2024, and unstructured data is progressing at a 29.97% CAGR to 2030.

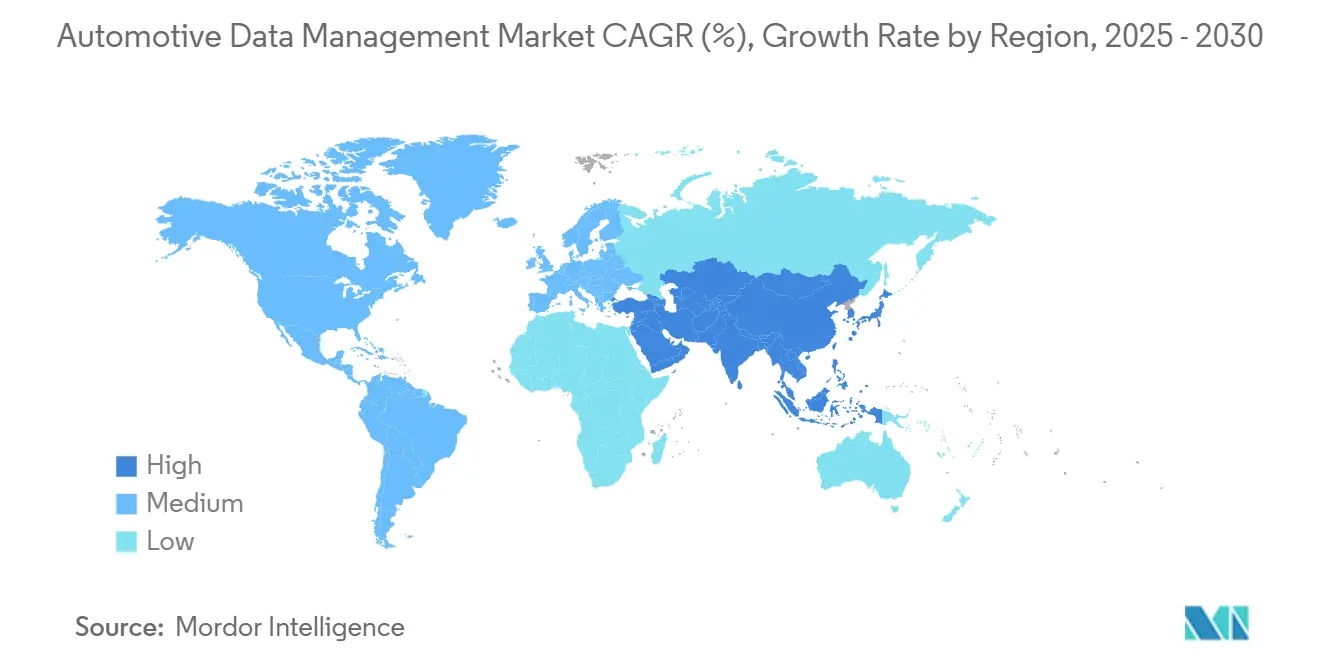

- By geography, North America contributed 38.87% revenue of the automotive data management market in 2024, and Asia-Pacific is expected to register the fastest regional CAGR at 20.13% between 2025 and 2030.

Global Automotive Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected and Autonomous-Vehicle | +1.6% | Global | Short term (≤ 2 years) |

| AI-Driven Closed-Loop Pipelines | +1.4% | North America & EU, APAC core | Medium term (2-4 years) |

| Software-Defined Vehicle Architectures | +1.1% | Global | Medium term (2-4 years) |

| Cloud and Telematics Adoption | +0.9% | Global | Short term (≤ 2 years) |

| Monetization of In-Vehicle Data | +0.7% | North America & EU | Long term (≥ 4 years) |

| Regulatory Mandates | +0.4% | Global, with early gains in EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Connected and Autonomous-Vehicle Data Explosion

Modern Level 3-plus vehicles already stream imaging, LiDAR, radar, and ultrasonic information that can exceed 4 TB per day; BMW’s development fleet channels similar data volumes to cloud clusters for model refinement[1] “BMW Group and DeepSeek AI Announce Strategic Partnership,” BMW Group, bmwgroup.com. Such datasets underpin digital twins that predict component fatigue, battery health, and driver behavior. Tesla, Waymo, and other leaders funnel hundreds of billions of real-world miles into continuous-learning loops that widen performance gaps versus late adopters. The uninterrupted data rise presses OEMs to overhaul network architectures, adopt lossless compression, and implement scalable retention policies. Suppliers seize the opportunity by delivering high-throughput sensors and 800V zonal electrical backbones that simplify data aggregation. Ultimately, the surge positions data governance and analytics maturity as key differentiators across retail, fleet, and robotaxi business models.

AI-Driven Closed-Loop Pipelines Shortening AV Iteration

Artificial-intelligence-enabled feedback loops now compress validation timelines from years to months. Continental’s automated labeling and synthetic-scenario generation clip annotation spend while improving edge-case coverage. Emerging neural-processing units, such as DENSO’s RISC-V-based coprocessors, deliver real-time inference and enable on-vehicle model updates. Fleet telemetry flows into cloud sandboxes overnight, automated test suites verify updates, and secure over-the-air pipelines push refreshed software weekly. The pace benefits safety regulators that need faster proof of compliance and fosters consumer expectations for smartphone-like improvements. Traditional development workflows fracture under this velocity, forcing suppliers to adopt DevOps, digital twins, and virtual homologation.

Software-Defined Vehicle Architectures Standardizing Data Layers

AUTOSAR Adaptive, Ethernet backbones, and standardized event log formats converge to create a common language across electronic control units. Hyundai Motor Group’s 42dot initiative exposes secure APIs that third parties use to build in-vehicle services, simplifying integration and reducing proprietary spaghetti. Standardization lowers switching costs, widens supplier ecosystems, and seeds aftermarket innovation around usage-based insurance, content streaming, and advanced driver assistance. Cloud vendors bundle pre-configured data schemas that shrink integration labor by around 30-50%. Harmonized layers also let regulators audit cybersecurity controls more easily, encouraging earlier approval of advanced autonomy features, especially in Europe and Japan.

Rapid Cloud and Telematics Adoption by OEMs

Cloud infrastructures provide elastic GPU farms, global CDNs, and integrated AI toolchains that speed experimentation. Amazon Web Services hosts HERE Technologies’ billion-dollar migration and Honda’s connected-services backbone[2]“AWS for Automotive,” Amazon Web Services, aws.amazon.com. Microsoft Azure powers Stellantis’ “Mobilisights” data marketplace covering 14 million vehicles, while Google and Oracle court OEMs with specialized digital-twin accelerators. Telematics modules now ship with 5G SA modems that support network-slicing, guaranteeing ultra-reliable low-latency links in autonomous driving lanes. Combined, cloud and telematics form the nervous system for predictive maintenance, remote diagnostics, and subscription-based feature unlocks that boost lifetime revenue per vehicle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Compliance Burden | 1.5% | Global, with early gains in EU, North America | Short term (≤ 2 years) |

| Sensor Data Storage Cost | 1.3% | Global | Medium term (2-4 years) |

| Cloud Latency and Bandwidth Gaps | 1.1% | Rural areas globally, spill-over to suburban | Long term (≥ 4 years) |

| Sustainability Pressure | -0.9% | Global, with early gains in EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Compliance Burden

Regulators intensify scrutiny of connected-vehicle data practices. The U.S. Federal Trade Commission flagged inadequate notice and consent processes in a recent enforcement action, signaling higher penalties for non-compliance[3]“Your Car Is Collecting Data About You,” Federal Trade Commission, ftc.gov. UNECE R155 requires documented threat analyses and mitigation plans, while forthcoming ISO/SAE 21434 audits include supplier chains. OEMs allocate up to 20% of IT budgets to meet multi-jurisdictional rules, deploying zero-trust architectures, certificate-management vaults, and incident-response automation. Privacy-by-design methodologies elongate development cycles, and secure code-signing increases over-the-air update complexity. Smaller suppliers struggle to finance compliance, slowing onboarding into OEM ecosystems.

High Cost of Storing/Processing Unstructured Sensor Data

LiDAR, high-resolution video, and radar outputs created by Level 4 prototypes require petabyte-scale data lakes and GPU clusters. Storage fees can cross USD 50,000 per vehicle each month, and training large-language or perception models incurs triple-digit kilowatt consumption. Compression and smart sampling cut volumes, yet they raise accuracy debates. Edge inference chips reduce data-center loads but add bill-of-materials cost and thermal constraints. Mid-tier OEMs weigh budget trade-offs and may limit pilot fleets, tempering broader deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Software Outpaces as AI Capabilities Mature

Software commanded 63.78% revenue of the automotive data management market in 2024, driven by rising investment in operating-system abstractions, middleware, and AI toolchains. The automotive data management market size for software is projected to climb at an 18.4% CAGR through 2030 as OEM roadmaps prioritize function-on-demand and digital-twin services. Cloud-native microservices modularize data pipelines, boosting reuse and cutting integration labor. Security modules embedded at the kernel layer enhance compliance alignment and speed third-party validation.

Services remain the fastest-growing component, advancing 20.28% annually as vendors provide turnkey ingestion, model-training, and lifecycle-governance offerings. Market incumbents bundle consulting, DevOps, and managed security frameworks, easing adoption for resource-constrained Tier-2 suppliers. Custom analytics and fleet-management subscriptions enlarge recurring revenue. As software complexity balloons, cross-domain orchestration services anchor multicloud and hybrid deployments, ensuring real-time synchronization across manufacturing, in-vehicle, and customer-facing touchpoints.

By Vehicle Type: Autonomous Platforms Accelerate Data Demand

Non-autonomous models delivered 68.84% of the 2024 revenue of the automotive data management market, yet autonomy leads growth. The autonomous segment’s 27.54% CAGR could lift its share significantly by 2030 as Level 3 hands-free systems hit premium lines and geo-fenced robotaxis scale. Each autonomous vehicle pumps terabytes of unstructured sensor data daily, dwarfing connected-car telemetry and stretching back-end systems. Regulators in South Korea and China lay V2X corridors that hasten validations, and subsidy packages lower the total cost of ownership for fleet operators.

Connected but human-driven vehicles continue to adopt over-the-air calibrations, demand-pricing insurance, and predictive maintenance dashboards. These features amplify data richness and weave traditional cars into unified data fabrics shared with autonomous cousins. Consequently, OEMs architect common middleware and analytics engines, enabling gradual migration from driver-assistance to high-automation without forklift upgrades.

By Deployment Type: Cloud Supremacy with Pragmatic Hybrid Edges

Cloud platforms captured 71.87% revenue of the automotive data management market in 2024 and maintain the fastest growth at 26.64% on account of elastic GPU clusters and global content distribution. Over 80% of new analytics workloads are launched in multicloud hubs where pre-trained vision models and managed DevOps pipelines truncate time-to-insight. The automotive data management market size linked to cloud usage is forecast to triple by 2030, propelled by cost advantages and pay-per-use pricing.

On-premise installations persist for latency-sensitive control loops and sovereign data mandates. Manufacturing execution systems, hazardous-environment test rigs, and defense contracts often impose in-country retention. Hybrid patterns dominate as OEMs replicate subsets of cloud runtimes at edge nodes using containerized orchestrators. This architecture assures deterministic response for safety-critical apps while backhauling enriched events to hyperscale analytics for fleet-wide optimization.

By Data Type: Unstructured Formats Unlock AI Monetization

Structured data held a 56.69% share of the automotive data management market in 2024, underpinning production quality, warranty analysis, and CRM workflows. Yet unstructured feeds—video, point-cloud, natural-language, and infotainment logs—post the highest 29.97% CAGR, turning them into prime growth territory. The automotive data management market share for unstructured inputs is rising as AI perception, voice assistants, and cabin monitoring create monetizable insights.

Edge AI chips pre-filter sensor deluges, converting raw pixels to feature vectors that cut uplink bandwidth. Advanced semantic-segmentation condenses LiDAR scans by 90% without safety compromise, curbing storage bills. Structured-unstructured convergence emerges, with unified metadata catalogs enabling cross-querying of CAN logs and camera frames. This blended view powers holistic digital twins that reconstruct physics, behavior, and environment for each asset across its lifetime.

Geography Analysis

North America retained 38.87% of 2024 revenues on account of mature cloud ecosystems, active autonomous-vehicle pilots, and stringent privacy enforcement under FTC guidance. The region’s 16.67% CAGR reflects sustained but moderating expansion as early adopters pivot toward optimizing return on previous digital investments. OEM-hyperscaler alliances deepen, underpinning region-wide 5G slicing and motorway V2X rollouts. Policy incentives like U.S. infrastructure funding speed roadside unit deployments, while Canada’s zero-emission mandates raise data volumes tied to battery analytics and usage-based energy tariffs.

Asia-Pacific clocks the highest 20.13% CAGR, buoyed by China’s annual V2X budget, South Korea’s electric-vehicle penetration, and Japan’s adoption of standardized SDV stacks. The automotive data management market benefits from robust smartphone ecosystems and high mobile-data consumption that normalize connected-service subscriptions. Regional suppliers leverage competitive hardware costs to bundle ADAS sensors with AI co-processors, lowering entry barriers for mid-market brands. Government-backed testbeds in Singapore, Shenzhen, and Seoul fast-track homologation for cross-border platooning, further lifting analytics demand.

Europe sustains a 14.81% CAGR underpinned by GDPR, cybersecurity certification, and circular-economy directives that enforce traceability from raw materials through end-of-life recycling. Cross-industry initiatives integrate battery passports and carbon ledgers into vehicle datasets, augmenting analytics scope. The automotive data management market sees incremental lift from over-the-air software sales that complement tightening emissions standards. Secondary regions—Middle East & Africa, Oceania, and South America—register mid-teen growth as 5G coverage and EV adoption accelerate, though infrastructure disparities and geopolitical uncertainties temper wider uptake.

Competitive Landscape

The automotive data management market exhibits moderate concentration, indicating established platform dominance while leaving room for specialized competitors. Competitive pressure intensifies as cloud giants embed automotive-specific building blocks, digital-twin templates, high-definition-map stores, and embedded fleet-ops consoles into mainstream platforms. Their capital scale lets them slash GPU pricing and waive egress fees, squeezing smaller platform providers.

Traditional suppliers pivot from hardware to value-added analytics. Bosch and Continental embed AI acceleration frameworks that ingest ECU logs in real time, then stream events to multicloud endpoints. DENSO’s partnership with Quadric integrates RISC-V NPUs for on-vehicle L4 perception, enabling micro-batch training and reducing cloud-compute spend. Automaker-controlled ventures, such as Stellantis’ Mobilisights and Hyundai Motor Group’s 42dot, seek to keep monetization in-house, offering API gateways and revenue-sharing models to developers

Start-ups capture niches in predictive-maintenance algorithms, natural-language interfaces, and homomorphic-encryption data vaults that satisfy privacy mandates. VC funding flows to edge-cloud orchestration, with players like ECARX and Axion Ray raising mid-eight-figure rounds. M&A activity rises as incumbents buy specialized sensor-fusion stacks and compliance engines to shorten time-to-market. Competitive differentiation shifts toward breadth of pre-trained models, transparency of governance controls, and ecosystem openness rather than pure compute horsepower.

Automotive Data Management Industry Leaders

Amazon Web Services (AWS)

Microsoft Azure

Bosch Mobility Solutions

IBM

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Force Motors launched Force iPulse, a connected-vehicle platform built with Intangles that melds AI and hybrid analytics for real-time operations.

- June 2025: Targa Telematics partnered with Volvo Cars to harness European fleet data and co-develop connected-mobility solutions.

- May 2025: Snowflake expanded its AI Data Cloud for manufacturing, introducing automotive-specific accelerators.

- March 2025: Tuxera entered connected-car architectures with embedded file-system and flash solutions optimized for zonal computing and EV platforms.

Global Automotive Data Management Market Report Scope

| Software |

| Services |

| Autonomous Vehicles |

| Non-Autonomous Vehicles |

| Cloud |

| On-Premise |

| Structured Data |

| Unstructured Data |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Component Type | Software | |

| Services | ||

| By Vehicle Type | Autonomous Vehicles | |

| Non-Autonomous Vehicles | ||

| By Deployment Type | Cloud | |

| On-Premise | ||

| By Data Type | Structured Data | |

| Unstructured Data | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the automotive data management market expected to grow through 2030?

The market is forecast to expand from USD 2.69 billion in 2025 to USD 6.61 billion by 2030, reflecting a 19.69% CAGR.

Which component segment is expanding the quickest?

Services are advancing at 20.28% annually because OEMs outsource implementation, compliance, and lifecycle optimization tasks.

Why does cloud deployment dominate in automotive data analytics?

Cloud delivers elastic GPU capacity, global over-the-air distribution, and pay-per-use economics that reduce infrastructure costs by up to 60% versus on-premise.

What drives Asia-Pacific’s leading growth rate?

Government V2X investments, high EV adoption, and standardized software-defined vehicle stacks propel the region at a 20.13% CAGR.

Which data type offers the highest growth opportunity?

Unstructured data—from LiDAR, video, and radar—posts a 29.97% CAGR, fueled by advanced perception and AI-analysis demand.

Page last updated on: