Automotive Repair And Maintenance Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

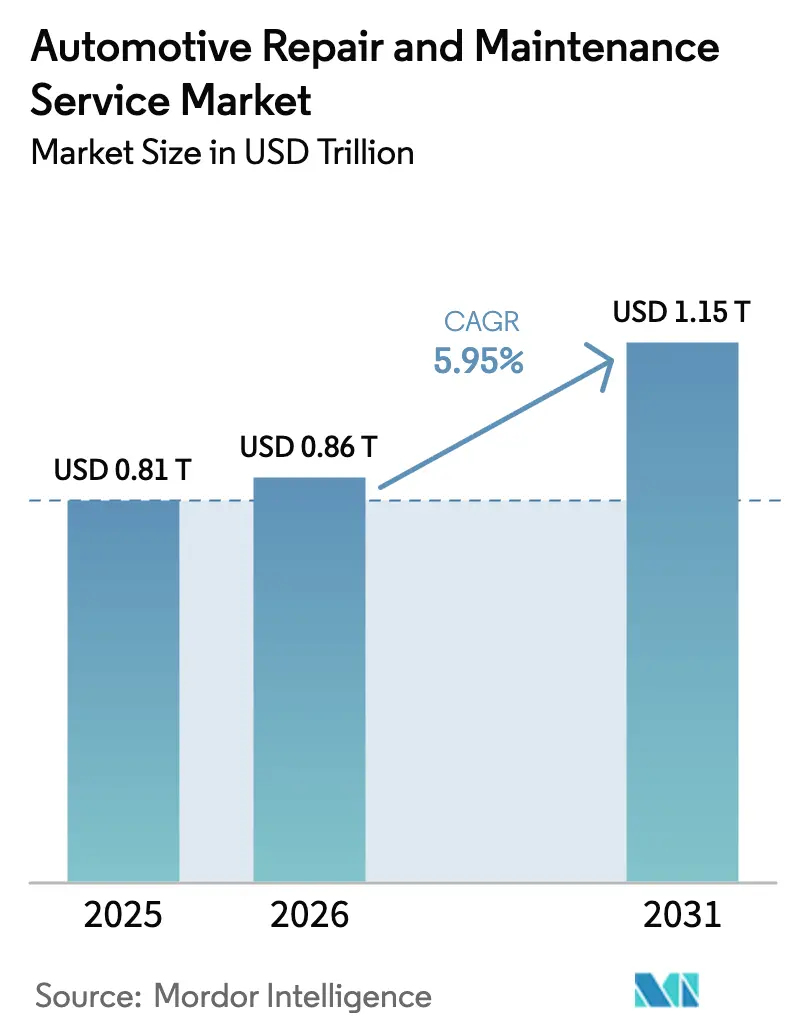

| Market Size (2026) | USD 0.86 Trillion |

| Market Size (2031) | USD 1.15 Trillion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Repair And Maintenance Service Market Analysis by Mordor Intelligence

Automotive Repair And Maintenance Service market size in 2026 is estimated at USD 0.86 trillion, growing from 2025 value of USD 0.81 trillion with 2031 projections showing USD 1.15 trillion, growing at 5.95% CAGR over 2026-2031. Sustained growth is underpinned by record-high average vehicle age, widening adoption of connected-car diagnostics, and expanding on-demand service models that heighten convenience for owners. Fragmented competition fosters technology-led differentiation as artificial intelligence streamlines fault identification, while right-to-repair regulation broadens independent shop access to proprietary data. Technicians remain in short supply, increasing wages and incentivizing automation to protect margins. Meanwhile, electrification moderates routine service frequency but opens battery-specific opportunities, prompting providers to diversify skills and tool investments.

Key Report Takeaways

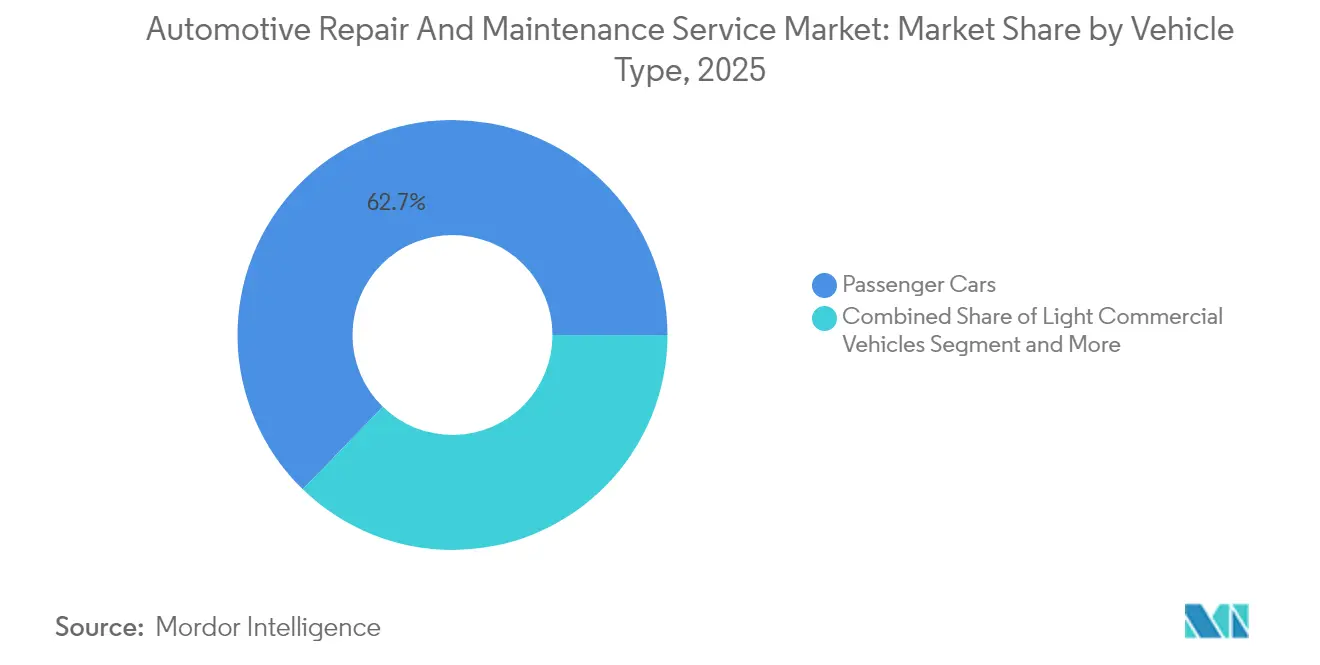

- By vehicle type, passenger cars held 62.74% of the Automotive repair and maintenance service market share in 2025, and the segment is advancing at a 6.03% CAGR during the forecast period (2026-2031).

- By service type, mechanical services accounted for 45.10% of the Automotive repair and maintenance service market share in 2025, while digital and connectivity services posted the fastest 6.12% CAGR during the forecast period (2026-2031).

- By component, tires represented 36.10% of the Automotive repair and maintenance service market share in 2025; batteries led growth at a 6.08% CAGR during the forecast period (2026-2031).

- By service provider, OEM-authorized centers controlled 47.05% of the Automotive repair and maintenance service market share in 2025, yet mobile and on-demand operators expand at a 6.11% CAGR during the forecast period (2026-2031).

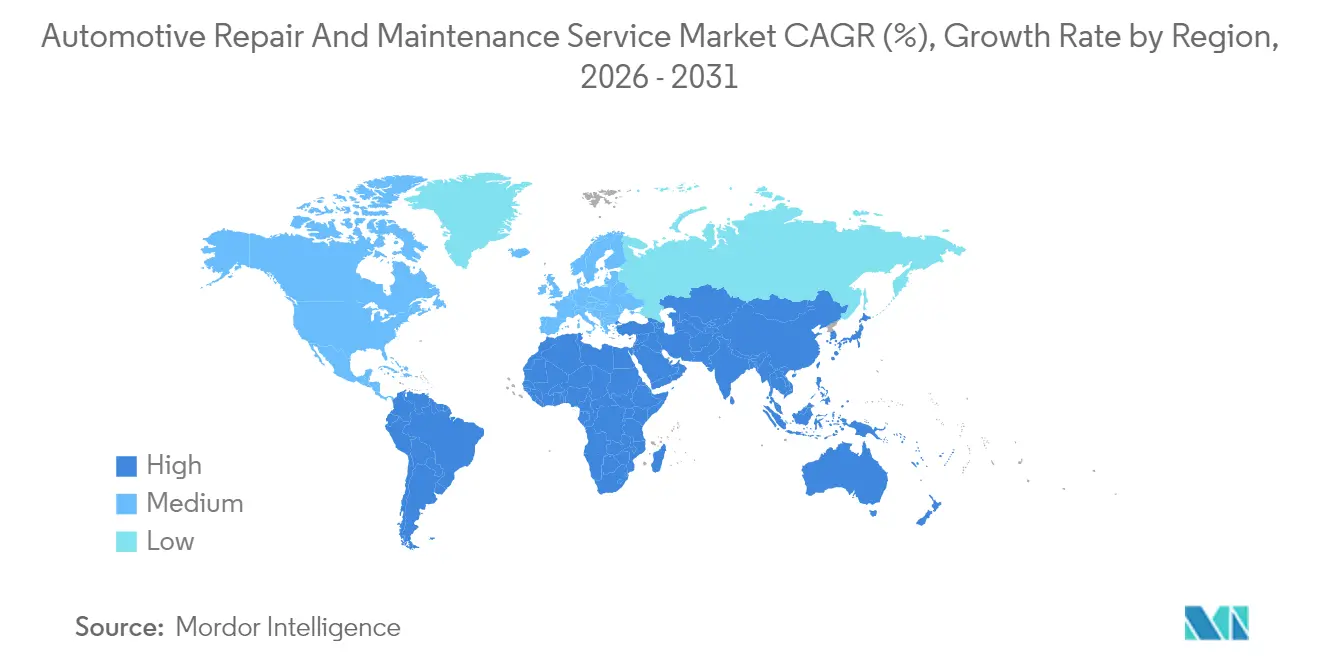

- By geography, North America dominated with a 38.10% of the Automotive repair and maintenance service market share in 2025; Asia Pacific records the top 6.07% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Repair And Maintenance Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Global Vehicle PARC | +2.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Growth Of Connected-Car Diagnostics | +1.8% | North America and EU leading, Asia Pacific following | Medium term (2-4 years) |

| Rapid Expansion Of On-Demand/Mobile Repair Platforms | +1.6% | Urban centers globally, strongest in North America | Short term (≤ 2 years) |

| ADAS Sensor-Calibration Mandates | +0.9% | Global, with regulatory compliance driving adoption | Long term (≥ 4 years) |

| OEM Right-To-Repair Legislation Opening Independent Service Revenue | +0.4% | North America and EU primarily, expanding to Asia Pacific | Medium term (2-4 years) |

| Post-Covid DIY Fatigue Shifting Owners Back To Professional Shops | +0.3% | Global, with regional variations in adoption timing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Global Vehicle PARC Drives Sustained Service Demand

The average United States vehicle age reached 12.8 years in 2025, extending a multi-year upward trend that similarly plays out across Europe [1]“Vehicle Aging Trends, 2025,” U.S. Department of Transportation, transportation.gov. Older vehicles require more frequent component replacements, elevating ticket sizes for providers that can manage complex, intermittent faults. Independent shops gain an edge on cost-sensitive, out-of-warranty owners, while OEM centers must emphasize certified parts and software updates to justify premiums. Higher mileage also amplifies wear-and-tear on consumables such as tires, brakes, and suspensions, locking in predictable service intervals that stabilize cash flow for the Automotive repair and maintenance service market.

Connected-Car Diagnostics Transform Maintenance Paradigms

Modern vehicles stream terabytes of telematics data, enabling predictive dashboards that alert drivers and shops to developing faults days or weeks before failure. AI-powered platforms cut diagnostic time by as much as half, freeing bays for additional revenue work and reducing comebacks that erode reputation [2]“Advancing Telematics and Vehicle Safety,” National Highway Traffic Safety Administration, nhtsa.gov. Early adopters differentiate by offering remote health checks, over-the-air software updates, and proactive parts ordering that minimize downtime. However, data access remains a friction point, prompting legislative efforts to ensure independent providers receive parity with OEM networks.

Right-to-Repair Legislation Opens Independent Service Revenue

Massachusetts’ Data Access Law and the European Union’s updated Type-Approval rules require manufacturers to share diagnostic protocols, expanding competition and lowering ownership costs. Independent garages can program security-coded components and access cloud-based service manuals without hefty subscription fees. Over time, analysts expect greater parts price transparency and faster third-party tool innovation, broadening the addressable customer base for non-dealer outlets across the Automotive repair and maintenance service market.

ADAS Sensor-Calibration Mandates After Collisions

From 2026, more than four-fifths of new passenger cars sold in North America will ship with forward-collision warning or lane-keeping assist systems requiring precise post-repair calibration, creating an additional chargeable step in every collision job [3]“Crash Avoidance Feature Prevalence,” Insurance Institute for Highway Safety, iihs.org . Specialized targets, scan tools, and alignment racks raise capital needs but also strengthen barriers to entry. Multi-location providers invest in centralized calibration centers that service in-house repairs and third-party body shops, adding fresh revenue vertically in the Automotive repair and maintenance service market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower Service Frequency For BEVs | -0.8% | Global, with highest impact in EV-leading markets | Long term (≥ 4 years) |

| Global Shortage Of Certified Technicians | -0.6% | Global, with acute shortages in developed markets | Medium term (2-4 years) |

| Consolidated Insurer Networks | -0.4% | North America primarily, expanding to other regions | Medium term (2-4 years) |

| Counterfeit E-Commerce Parts Eroding Authorized-Parts Margins | -0.3% | Global, with particular impact in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lower Service Frequency for Battery-Electric Vehicles

Battery-electric vehicles have fewer moving parts and no scheduled oil changes, cutting routine visits by around two-fifths compared with internal-combustion cars. Providers offset the drop by offering high-voltage battery health checks, software upgrades, and thermal management services. Yet the shift requires insulated tools, safety training, and dedicated bays that command investment sizable enough to squeeze small independents in the Automotive repair and maintenance service market.

Technician Shortage Drives Wage Inflation and Capacity Constraints

According to Tech Force Foundation data, retirements outpace new entrants, leaving a projected multiple unfilled posts by 2031. Shops raise starting wages and tuition reimbursement but ration bays during peak demand. Some operators deploy augmented-reality headsets that let senior experts guide junior staff remotely, stretching scarce talent while preserving quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Extend Dominance

Passenger cars generated 62.74% of the Automotive repair and maintenance service market share in 2025 and will grow at a 6.03% CAGR through 2031. Aging sedans, SUVs, ADAS retrofits, and software updates create layered revenue beyond traditional oil changes. Light commercial vehicles benefit from e-commerce expansion, prompting fleets to adopt predictive maintenance software that schedules service outside peak delivery windows. Heavy commercial vehicles remain essential for freight and face regulatory emissions checks that mandate periodic aftertreatment service. Two-wheelers capture urban share in Asia Pacific, but their lower average ticket value tempers global impact.

Passenger car complexity drives new calibration work for cameras and radar sensors, raising average repair orders. Subscription-based telematics packages provide remote diagnostic alerts to franchised workshops, increasing visit predictability. Commercial fleets negotiate fixed-price maintenance contracts that smooth revenue recognition for service providers. Across all classes, parts availability remains a differentiator, pushing chains to build regional distribution hubs that minimize downtime.

By Service Type: Mechanical Services Maintain Leadership Amid Digital Growth

Mechanical services held 45.10% of the automotive repair and maintenance market share in 2025, anchored by universal engine, transmission, and suspension care needs. Digital and connectivity services, although starting from a smaller base, are projected to post a 6.12% CAGR to 2031 as over-the-air update requirements multiply. Electrical and electronic repairs are followed closely and powered by growing electrification and infotainment complexity. Exterior and structural repairs maintain a steady demand due to collision rates correlating with vehicle miles traveled.

Hybrid service models emerge, combining physical repairs with software patches delivered remotely or at the bay. Shops invest in multi-protocol interfaces that read vehicular CAN, Ethernet, and LIN networks, ensuring brand coverage. Cybersecurity issues invite additional revenue streams as owners seek firmware checks post software-defined upgrades. Mechanical bay utilization remains high, but the growth of the automotive repair and maintenance industry is increasingly shifting toward diagnostics and digital services.

By Component Type: Tires Remain Essential as Batteries Gain Momentum

Tires accounted for 36.10% of the Automotive repair and maintenance service market size in 2025, reflecting their consumable nature and safety relevance. Ultra-high-performance and seasonal tire adoption lifts unit margins, while fleet managers embrace tire pressure monitoring analytics that optimize replacement intervals. Batteries, spanning 12-volt and high-voltage packs, reach the fastest 6.08% CAGR as electrification boosts demand for diagnostics, cooling system maintenance, and end-of-life recycling logistics.

Brake pads experience slower growth because regenerative braking in EVs reduces friction pad wear, yet ADAS integration demands precise rotor surfaces, sustaining premium machining services. Cabin air filters and wiper blades persist as quick-turn items that drive footfall. Parts distributors expand just-in-time models to support same-day delivery in dense metros, a competitive necessity for urban service providers.

By Service Provider: OEM Centers Lead alongside Rapid Mobile Expansion

OEM-authorized shops held 47.05% of the Automotive repair and maintenance service market share in 2025, buoyed by warranty obligations and brand loyalty. Mobile and on-demand operators, however, accelerate at a 6.11% CAGR by delivering doorstep convenience that resonates with time-pressed consumers. Independent garages maintain relevance through price competitiveness and personalized interactions, while franchise chains scale marketing spend and standardized processes to capture regional mindshare.

Customer-experience platforms allow OEM dealers to offer valet pick-up and drop-off, neutralizing mobile rivals. Hybrid ownership models see dealers partnering with mobile platforms to outsource minor repairs, keeping bays free for heavy work. Investment flows from private equity funnels into multi-location independents that promise roll-up synergies such as bulk parts purchasing and centralized administration.

Geography Analysis

North America commanded 38.10% of the Automotive repair and maintenance service market share in 2025, supported by high vehicle density, an average fleet age above 12 years, and right-to-repair regulations that encourage a diverse provider ecosystem. Suburban commuting patterns and winter road conditions elevate tire and suspension wear, locking in repeat visits. The United States leads regional revenue, with Canada displaying similar characteristics but higher seasonal service peaks. Mexico contributes to growth from expanding manufacturing hubs and a rising middle class.

Asia Pacific delivers the fastest 6.07% CAGR as China, India, and ASEAN nations add millions of first-time car owners annually. Urban congestion increases minor collision frequency, supporting body and painting volume, while government incentives for new-energy vehicles create early demand for EV-specific services. Japan and South Korea showcase advanced telematics integration, setting benchmarks for predictive maintenance adoption across the Automotive repair and maintenance service market.

Europe records steady expansion driven by stringent safety and emissions inspections that guarantee mandatory workshop visits. Premium vehicle concentration in Germany, the United Kingdom, and Scandinavia ups the share of electronic and software updates per repair order. Eastern European markets post above-average growth on the back of rising disposable incomes and improving service infrastructure, though parts availability and counterfeit component risks remain challenges.

Competitive Landscape

The Automotive repair and maintenance service market remains moderately fragmented, yet consolidation accelerates as private equity groups assemble regional multi-shop operations to exploit purchasing leverage and unified technology platforms. OEM dealerships benefit from exclusive access to proprietary diagnostic codes and genuine-part supply chains, but they face margin pressure from labor-rate caps in insurer direct-repair networks. Independent shops leverage community trust and flexible pricing, while mobile startups court digitally savvy drivers with transparent quotes and same-day scheduling apps.

Technology adoption stands out as the key differentiator. Chains roll out cloud-based shop management systems that unify customer records, automate parts ordering, and enable AI-driven repair recommendations. Partnerships emerge between repair networks and software providers to integrate remote diagnostics, accelerating first-time-fix ratios. On the corporate front, TPG’s acquisition of Classic Collision and Driven Brands’ ongoing franchise expansion illustrates a buy-and-build thesis focused on density and operating efficiency.

Labor scarcity pushes operators to rethink workforce models, including apprenticeship pipelines, remote expert assistance, and productivity-tracking wearables. Sustainability also informs strategy, with shops investing in energy-efficient lighting, closed-loop fluid recycling, and certified battery disposal to meet tightening environmental regulations. Competitive intensity now pivots on who can deliver the fastest turnaround, transparent pricing, and consistently high repair quality amid rapidly evolving vehicle technology.

Automotive Repair And Maintenance Service Industry Leaders

LKQ Corporation

Robert Bosch GmbH (Bosch Car Service)

Belron International Limited

TVS Motor Company (myTVS Parts & Accessories)

Mobivia Groupe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Main Street Auto acquired Dennis Quick Auto Service, adding collision repair capabilities and expanding its footprint in the U.S. Northeast.

- August 2024: Steer and AutoOps merged to form an integrated platform offering mobile repairs and traditional shop services.

- June 2024: Crash Champions acquired J&J Auto Body, adding three locations to its network across major metropolitan areas.

Global Automotive Repair And Maintenance Service Market Report Scope

Automotive repair and maintenance services refer to the inspection, diagnosis, and subsequent repair/replacement of parts and components in a vehicle. The automotive service market includes routine services, like oil changes, tire repair, and air conditioning, and non-routine services, like rust-proofing and exterior painting.

The automotive repair and maintenance service market is segmented by vehicle type, service type, component type, service provider, and geography. By vehicle type, the market is segmented into passenger cars, commercial vehicles, and two-wheelers. By service type, the market is segmented into mechanical (tires, lubricants, etc.), exterior and structural (body repair, windows, etc.), and electrical and electronics (electrical wirings, ignition system, etc.). By component type, the market is segmented into tires, seats, batteries, and others (engines, etc.). By service provider, the market is segmented into original equipment manufacturer (OEM) authorized service centers, auto care and repair franchises, and others (local garages, etc.). By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers market size and forecasts for the automotive repair and maintenance market in value (USD) for all the above segments.

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Mechanical Services |

| Exterior & Structural Services |

| Electrical & Electronics Services |

| Digital & Connectivity Services |

| Tires |

| Batteries |

| Seats & Interiors |

| Braking Systems |

| Powertrain & Engine Parts |

| OEM-Authorized Centers |

| Franchise Chains |

| Independent Garages |

| Mobile / On-Demand Operators |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia & New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| By Service Type | Mechanical Services | |

| Exterior & Structural Services | ||

| Electrical & Electronics Services | ||

| Digital & Connectivity Services | ||

| By Component Type | Tires | |

| Batteries | ||

| Seats & Interiors | ||

| Braking Systems | ||

| Powertrain & Engine Parts | ||

| By Service Provider | OEM-Authorized Centers | |

| Franchise Chains | ||

| Independent Garages | ||

| Mobile / On-Demand Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia & New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will the global size of automotive repair and maintenance services be by 2031?

Spending is forecast to reach USD 1.15 trillion in 2031, growing at a 5.95% CAGR from 2026.

Which region is expected to grow fastest in automotive repair and maintenance services by 2031?

Asia Pacific posts the highest 6.07% CAGR, driven by rising vehicle ownership and expanding service networks.

Why do passenger cars generate the highest service revenue?

Passenger cars account for 62.74% of 2025 revenue because their large installed base, aging profiles, and frequent maintenance schedules consistently fill service bays.

How does electric vehicle adoption affect repair and maintenance demand?

Battery-electric models need roughly 40% fewer routine visits, shifting revenue toward specialized battery diagnostics, software updates, and high-voltage safety checks.

What role does connected-car diagnostics play in future service models?

Real-time telematics alerts enable predictive maintenance that cuts diagnostic time by up to 50% and helps shops pre-order parts, improving first-time-fix rates and customer uptime.

Page last updated on: