Automotive Active Body Panel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.17 Billion |

| Market Size (2030) | USD 3.01 Billion |

| Growth Rate (2025 - 2030) | 6.75% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

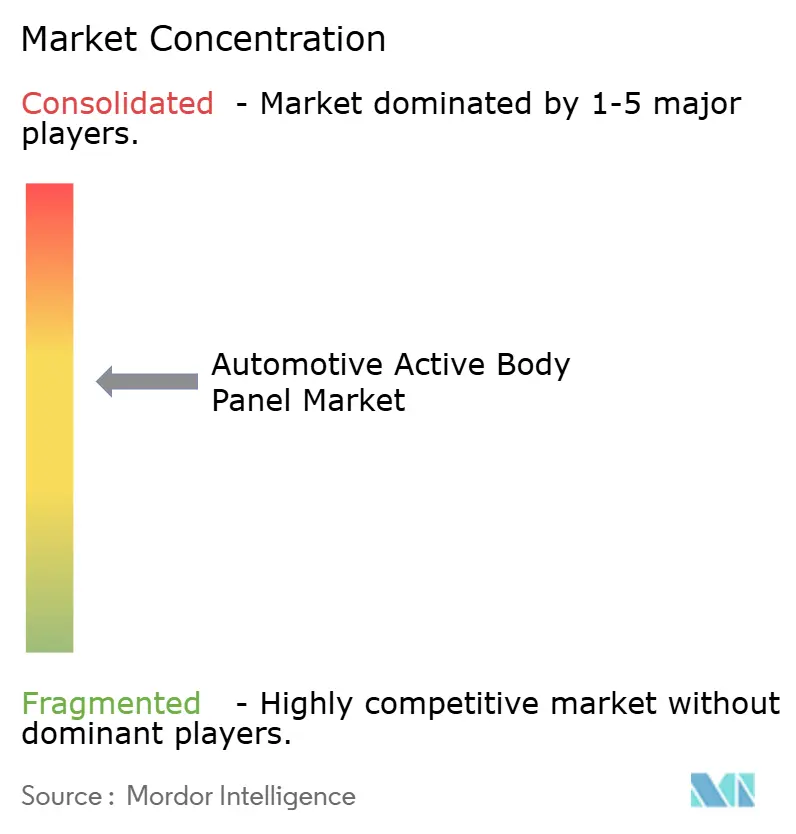

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Active Body Panel Market Analysis by Mordor Intelligence

The Automotive Active Body Panel Market size is estimated at USD 2.17 billion in 2025, and is expected to reach USD 3.01 billion by 2030, at a CAGR of 6.75% during the forecast period (2025-2030). This trajectory is propelled by ever-stricter CO₂ and CAFE standards, the rapid electrification of global vehicle fleets, and significant cost reductions in 48 V electromechanical actuation that transform static outer skins into dynamic, efficiency-enhancing surfaces. Automakers prioritize drag-reducing panels to meet a 58-mpg fleet target in the United States while simultaneously integrating thermal-management features that extend battery range in battery-electric and hybrid-electric vehicles. Asia-Pacific’s technology leadership in actuators and its dominant electric-vehicle output reinforce demand, whereas North America and Europe accelerate adoption through regulatory mandates and smart-city infrastructure upgrades. Competitive intensity is rising as Tier-1 suppliers leverage flexible manufacturing lines that accommodate multiple platforms and derivatives, lowering switching costs for OEMs pursuing lightweight, software-defined exteriors.

Key Report Takeaways

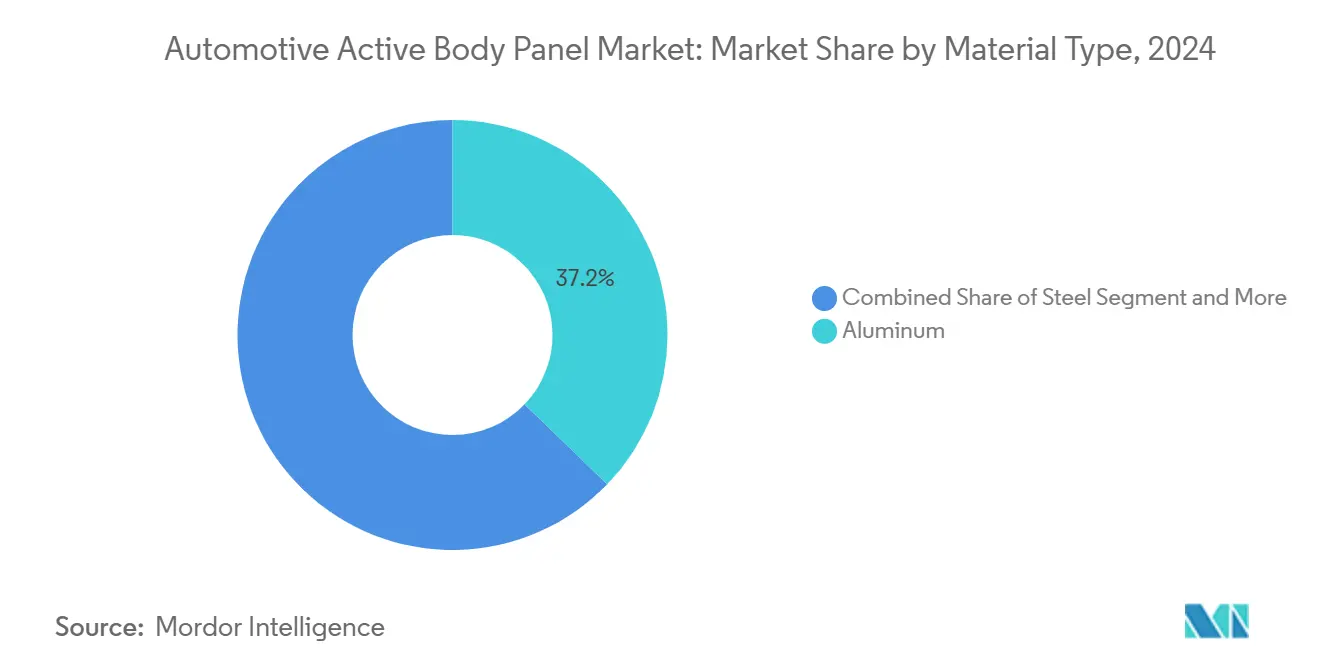

- By material type, aluminum led with a 37.18% share of the automotive active body panel market in 2024, while carbon fiber is projected to achieve a 6.77% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger vehicles accounted for a 67.25% share of the automotive active body panel market size in 2024 and are expected to grow at a 6.79% CAGR during the forecast period (2025-2030).

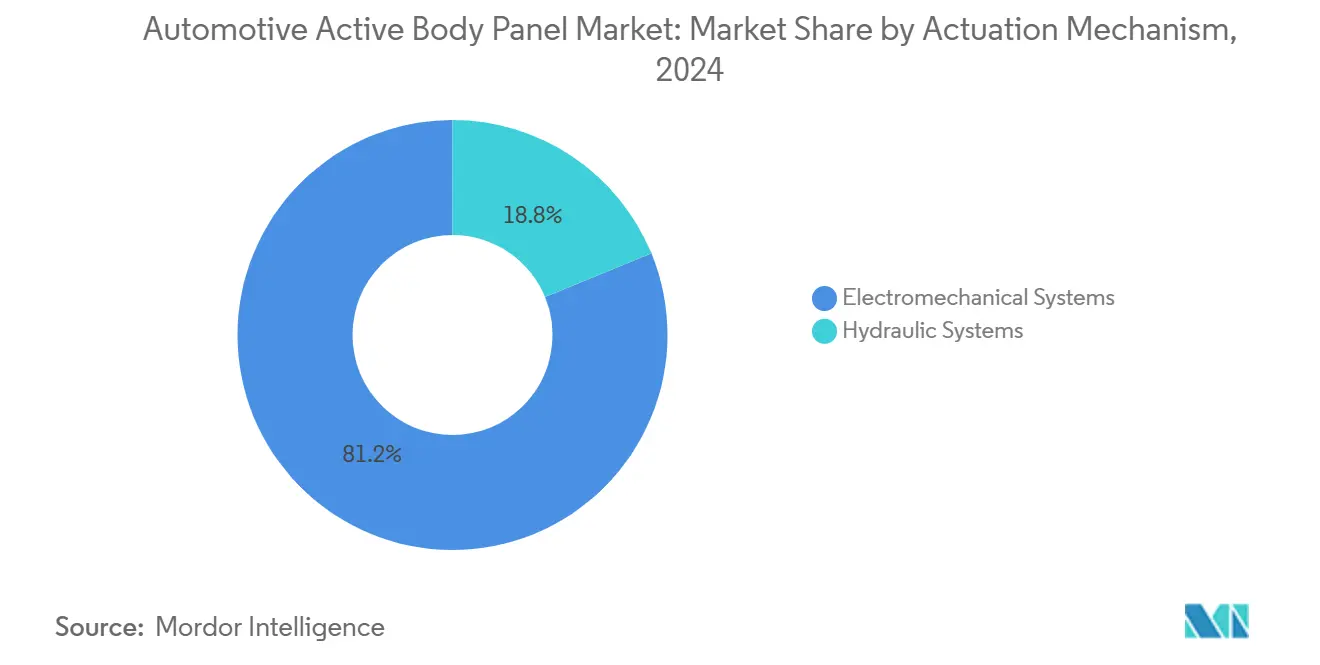

- By actuation mechanism, electromechanical systems captured 81.23% of the automotive active body panel market share in 2024, and the segment is expected to grow at a 6.81% CAGR during the forecast period (2025-2030).

- By end user, OEMs held 87.34% of the automotive active body panel market size in 2024, whereas the aftermarket segment is expected to grow at a 6.83% CAGR during the forecast period (2025-2030).

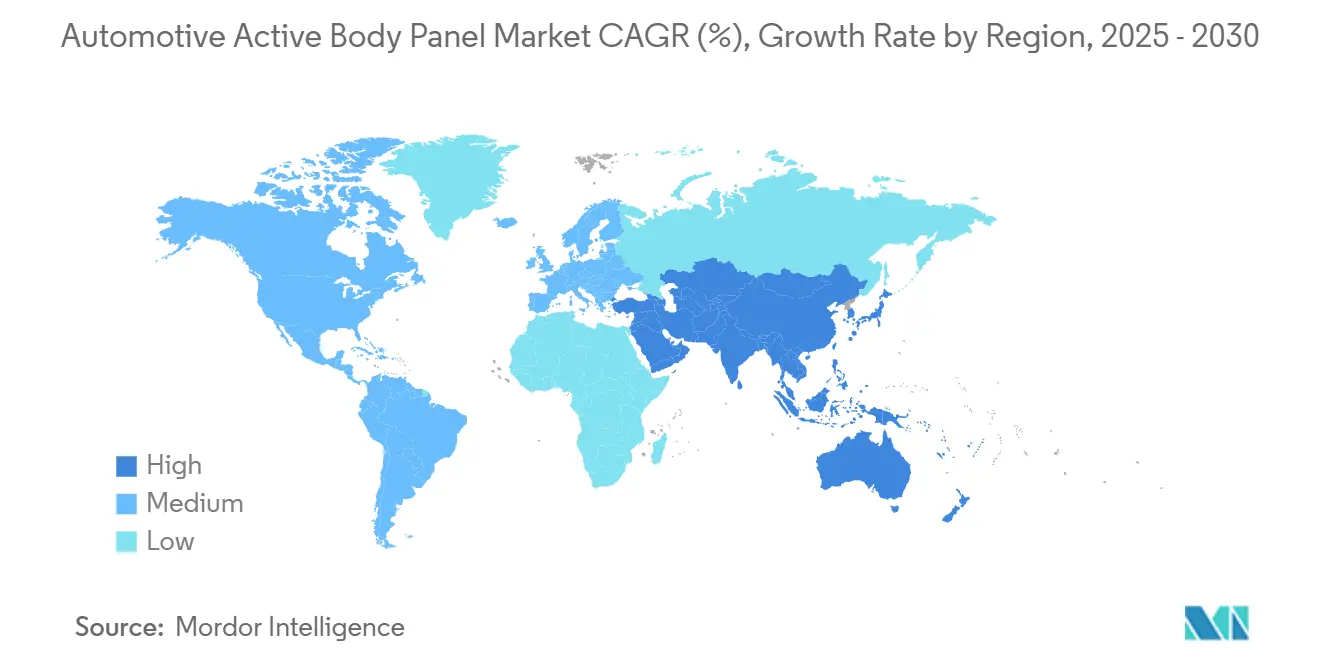

- By geography, Asia-Pacific commanded 34.67% of the automotive active body panel market share in 2024 and is expected to grow at a 6.85% CAGR during the forecast period (2025-2030).

Global Automotive Active Body Panel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV & HEV Growth | +1.5% | Global, spill-over to Asia Pacific core markets | Short term (≤ 2 years) |

| Low-Cost 48V Electromechanical Actuators | +1.3% | Global, with early gains in China, Europe | Short term (≤ 2 years) |

| Tightening CO2/CAFE Regulations Drive OEM | +1.2% | Global, with early gains in EU, North America | Medium term (2-4 years) |

| Integration Of Sensing & Actuation | +1.1% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Vehicle-To-Infrastructure (V2I) Mandates | +0.9% | National, with early gains in smart city regions | Long term (≥ 4 years) |

| Light-Weighting Push | +0.8% | Global, with Asia Pacific manufacturing concentration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid BEV & HEV Growth Amplifies Need For Active Thermal-Management Panels

Battery-electric powertrains generate unique thermal loads spanning battery packs, traction motors, and power electronics. OEMs deploy active body panels such as variable cooling vents to stabilize cell temperatures, safeguarding range retention during fast charging. 48 V architectures simplify power delivery to distributed actuators, while predictive algorithms rely on embedded sensors to modulate airflow in real time. Continental’s biometric exterior concept unveiled at CES 2025 illustrates how active panels can pair temperature sensing with user recognition for anticipatory cooling responses. These advancements foster greater penetration of thermal-management body panels, especially in high-volume crossover and sedan platforms.

Low-Cost 48 V Electromechanical Actuators Reach Mass-Market Price Points

High-density DC-DC converters now down-convert 800 V main packs to 48 V rails in compact footprints, supporting multiple synchronously controlled actuators without breaching SELV limits. Production volumes climbed sharply in 2025 as suppliers added capacity; Harmonic Drive’s line extension alone raised output by a huge amount. AI-driven quality-assurance systems have improved defect captures above four-fifths, compressing launch timelines for variable-geometry body panels. Electromechanical solutions outcompete hydraulic alternatives on weight, packaging, and diagnostic transparency, cementing their substantial share of active-panel actuation.

Tightening CO₂/CAFE Regulations Drive OEM Demand For Drag-Reducing Body Panels

Fleet-wide targets of 58 mpg by 2032 in the United States and the European Union’s updated General Safety Regulation II, which entered force in July 2024, are pushing automakers to capture every feasible aerodynamic gain. Active grille shutters, rear spoilers, and adaptive under-trays offer validated drag reductions by slightly, directly translating into lower emissions and extended BEV range. Computational-fluid-dynamics platforms now permit virtual validation of morphing profiles that meet ISO/SAE 21434 cybersecurity criteria, ensuring energy savings and data integrity. These regulatory levers compress program timelines and elevate the active automotive body panel market as a compliance-critical technology across global nameplates [1]“Corporate Average Fuel Economy Standards for Model Years 2027–2032,” National Highway Traffic Safety Administration, nhtsa.gov .

Integration Of Sensing & Actuation For ADAS-Ready Smart Exteriors

Consolidating cameras, radar, and LiDAR into active surfaces enables vehicles to adapt mechanically and digitally to dynamic driving environments. Zone controllers centralize sensor data, allowing sub-100 ms response times for panel actuation that preserves aerodynamic efficiency while ensuring sensor clarity. AI-enabled perception requires rigorous functional-safety validation under ISO 26262, with cybersecurity safeguards hardening external moving components against remote exploitation. OEM patents involving color-changing skins signal a shift toward exteriors capable of communicating with intent to other road users, thereby broadening the functional palette of the automotive active body panel market [2]“Cybersecurity for Movable Exterior Components,” Society of Automotive Engineers, sae.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -1.1% | Global, with Asia Pacific manufacturing concentration | Short term (≤ 2 years) |

| System Complexity Raises Warranty Costs | -0.9% | Global, with higher impact in premium segments | Medium term (2-4 years) |

| Tier-1 Actuator Supply | -0.8% | Global, with higher impact in Europe and North America | Short term (≤ 2 years) |

| Cyber-Security Certification | -0.7% | EU and North America core, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Aluminum, CFRP) Affects BOM

Fluctuating commodity prices and geopolitical supply risks create uncertainty around bill-of-materials targets. Aluminum production constraints, especially in export-restricted regions, can inflate sourcing costs, while the limited recycled carbon fiber supply restrains broader composite adoption. Automotive suppliers navigating restructuring environments in 2024-2025 highlight the challenge of balancing material inflation against fixed OEM contracts. Regulatory demands for minimum recycled content also raise compliance costs, pressing manufacturers to diversify material portfolios and explore thermoplastic composite pathways for cost stabilization.

System Complexity Raises Warranty Costs & OEM Reluctance

Active body panels incorporate actuators, sensors, controllers, and software layers, making diagnostics and repair more intricate than traditional stamped parts. ISO 26262 functional-safety compliance requirement extends validation cycles, while cybersecurity certification adds further overhead. Dealers face higher training and tooling costs, and OEMs bear exposure to field failures that could trigger costly recalls. Suppliers are automating damping-compound applications and adopting predictive maintenance analytics, but up-front capital expenditures still slow program approvals, particularly in entry-level segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Leads Despite Carbon Fiber's Superior Growth Trajectory

Aluminum accounted for 37.18% of the automotive active body panel market share in 2024, reflecting its favorable cost-to-weight ratio and existing supply infrastructure. Carbon fiber’s 6.77% CAGR underscores premium OEMs’ willingness to pay for extreme lightweighting. Steel remains indispensable for localized reinforcement, while plastics and thermoplastic composites rise in grille shutters and deployable aero devices where complex geometries are essential.

The active automotive body panel market size for composite solutions will climb with fast cycle forming technologies, helping OEMs meet corporate carbon goals without compromising throughput. ART placement and bladder-assisted molding reduce scrap rates, and recycled fiber streams close material loops. Life-cycle assessments highlight reduced embedded carbon versus aluminum when renewable energy powers cure ovens, enhancing the circular economy case.

By Vehicle Type: Passenger Vehicles Drive Adoption Across All Propulsion Types

Passenger vehicles held 67.25% of the automotive active body panel market in 2024, and it registered a robust CAGR of 6.79% through 2030, buoyed by consumer appetite for efficiency features and aesthetic differentiation. Electrified crossovers and sedans increasingly integrate morphing spoilers and cooling shutters, while premium SUVs add active side lips for high-speed stability.

Light commercial fleets are next in line as last-mile operators chase range and fuel savings, especially in regions deploying stringent delivery-zone regulations. Medium and heavy trucks adopt trailer-edge devices validated to cut fuel use up to one-tenth, though longer development cycles temper growth rates relative to the passenger segment.

By Actuation Mechanism: Electromechanical Systems Dominate Through 48 V Architecture Advantages

Electromechanical designs secured 81.23% of the automotive active body panel market share in 2024 and will pace the segment at a 6.81% CAGR to 2030. Compact gearset actuators tied into 48 V backbones streamline integration while maintaining SELV classification. Hydraulic actuation persists in niche heavy-duty applications demanding high force and broad operating-temperature windows.

Ongoing miniaturization and power-density gains enable multi-axis panel movement without sacrificing cargo or cabin volume. AI-based calibration shortens line-side programming, supporting flexible manufacturing approaches capable of handling four platforms and eight derivatives on one line.

By End User: OEMs Lead Integration While Aftermarket Opportunities Emerge

OEMs captured 87.34% of the automotive active body panel market share in 2024 because a fully integrated design is needed to balance structure, aerodynamics, and vehicle electronics. The segment also grows at a robust CAGR of 6.83% through 2030. Tier-1 partners like Magna employ modular tooling that allows rapid platform roll-out with minimal capital duplication, enhancing OEM business cases.

Aftermarket participation is one-fifth but could grow where retrofit cooling shutters help legacy fleets meet emissions zones. Barriers include cybersecurity certification, sealed diagnostic protocols, and the cost of reworking body-control modules. Companies like Chemours show paths forward with low-GWP retrofit thermal kits, although safety-critical functions remain squarely in OEM hands.

Geography Analysis

Asia-Pacific leads the automotive active body panel market, holding 34.67% share and delivering a 6.85% CAGR outlook through 2030. China’s aggressive NEV quotas and investment in smart-city corridors spur early uptake, aided by an abundant actuator-supply base and regional ownership of key aluminum inputs. Japan contributes high-precision gearbox and motor technology, while South Korea’s future-car initiatives showcase morphing skirts and side lips in mass-market EVs.

North America follows, galvanized by CAFE compliance deadlines and well-defined V2I pilots in metropolitan corridors. Substantial Tier-1 expansions, including Aisin’s plant in North Carolina, underpin a stable supply chain for panels and actuators. Early adoption of 48 V subsystems across pickup and SUV platforms provides fertile ground for active aero feature growth, despite trade-policy uncertainty that complicates long-range sourcing commitments.

Europe maintains strong volume and technology leadership due to regulatory foresight. Germany, France, and the Nordics integrate circular-economy mandates that favor thermoplastic composites and recycled fibers. Suppliers with European manufacturing footprints benefit from proximity to OEM design centers, facilitating rapid co-development cycles for software-defined surfaces. The region’s cross-border alignment curtails homologation costs, supporting exports into neighboring markets.

Competitive Landscape

The automotive active body panel market displays moderate concentration and is shaped by a three-tier supply architecture. Tier-1 integrators such as Magna International, Valeo, and Continental AG leverage long-standing OEM relationships and manufacturing scale to win platform contracts. Magna’s active grille shutter line alone ships 3 million units annually, exemplifying volume potential [3]“Software-Defined Vehicle Platform Overview,” Continental AG, continental.com . Valeo’s CES 2025 demonstrations of mini-LED exteriors and panoramic windshield projection reveal a diversification into bright surfaces that merge safety and personalization.

Component specialists provide the underlying actuation muscle. Johnson Electric’s vertical chain from die-casting to PCB assembly delivers cost-controlled 48 V motors, while Harmonic Drive’s capacity elevates supply headroom for precision gears. AI-enabled inspection surpasses the majority of defect detection, compresses validation timelines, and further cements electromechanical technology adoption.

Competitive differentiation is increasingly software-centric. Continental’s zone-controller architecture enables over-the-air recalibration of panel motion profiles, aligning with OEM strategies for software-defined vehicles. Compliance expertise in ISO 26262 and ISO/SAE 21434 serves as a gatekeeper, excluding less experienced entrants from safety-critical programs. Aftermarket entrants confront barriers in secure diagnostics and warranty risk, keeping the primary battleground within OEM-integrated supply contracts.

Automotive Active Body Panel Industry Leaders

Continental AG

Robert Bosch GmbH

Valeo SA

Magna International Inc.

Mahle GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Valeo and Enno Star revealed a mini-LED exterior display at IAA Mobility 2025 that enables crystal-clear signaling and vehicle personalization.

- July 2025: Magna introduced an interior sensing suite combining radar and cameras that detects driver fatigue, passengers, and pets. Global OEM adoption is underway.

- January 2025: Valeo launched Panavision at CES, projecting virtual imagery the width of the windshield and debuting software to assist drivers in roadside emergencies.

Global Automotive Active Body Panel Market Report Scope

| Steel |

| Aluminum |

| Carbon Fiber |

| Plastic |

| Composite Materials |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium & Heavy Commercial Vehicles |

| Electromechanical Systems |

| Hydraulic Systems |

| OEMs |

| Aftermarket Suppliers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Steel | |

| Aluminum | ||

| Carbon Fiber | ||

| Plastic | ||

| Composite Materials | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium & Heavy Commercial Vehicles | ||

| By Actuation Mechanism | Electromechanical Systems | |

| Hydraulic Systems | ||

| By End User | OEMs | |

| Aftermarket Suppliers | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is an automotive active body panel and how does it improve vehicle efficiency?

An automotive active body panel is an exterior surface—such as grille shutters, spoilers, or side lips—that changes shape or position in real time to cut aerodynamic drag, manage heat, or enhance safety, which can reduce energy consumption and extend BEV range.

How large is the global automotive active body panel market size in 2025 and what is its expected growth to 2030?

The segment is valued at USD 2.17 billion in 2025 and is projected to reach USD 3.01 billion by 2030, reflecting a 6.75% CAGR over the forecast period.

Which material is most widely used in active body panels today?

Aluminum holds the leading 37.18% share due to its favorable balance of weight, cost, and existing supply infrastructure, even as carbon-fiber composites post faster growth in premium programs.

Why are 48 V electromechanical actuators favored for active aerodynamic functions?

48 V systems deliver sufficient power within safe voltage limits, are lighter and more compact than hydraulic setups, and integrate seamlessly with modern vehicle electrical architectures, giving them an 82% share of current actuation solutions.

Which region currently leads adoption of active body panels?

Asia-Pacific accounts for 34.67% of global demand, driven by China’s new-energy vehicle quotas, Japan’s precision actuator manufacturing, and South Korea’s future-car initiatives.

What are the main factors restraining faster rollout of active body panels?

Warranty risk from system complexity and raw-material price swings in aluminum and carbon fiber raise OEM costs and extend validation timelines, slowing deployment in price-sensitive vehicle segments.

Page last updated on: