Market Overview

| Study Period | 2021 - 2031 |

|---|---|

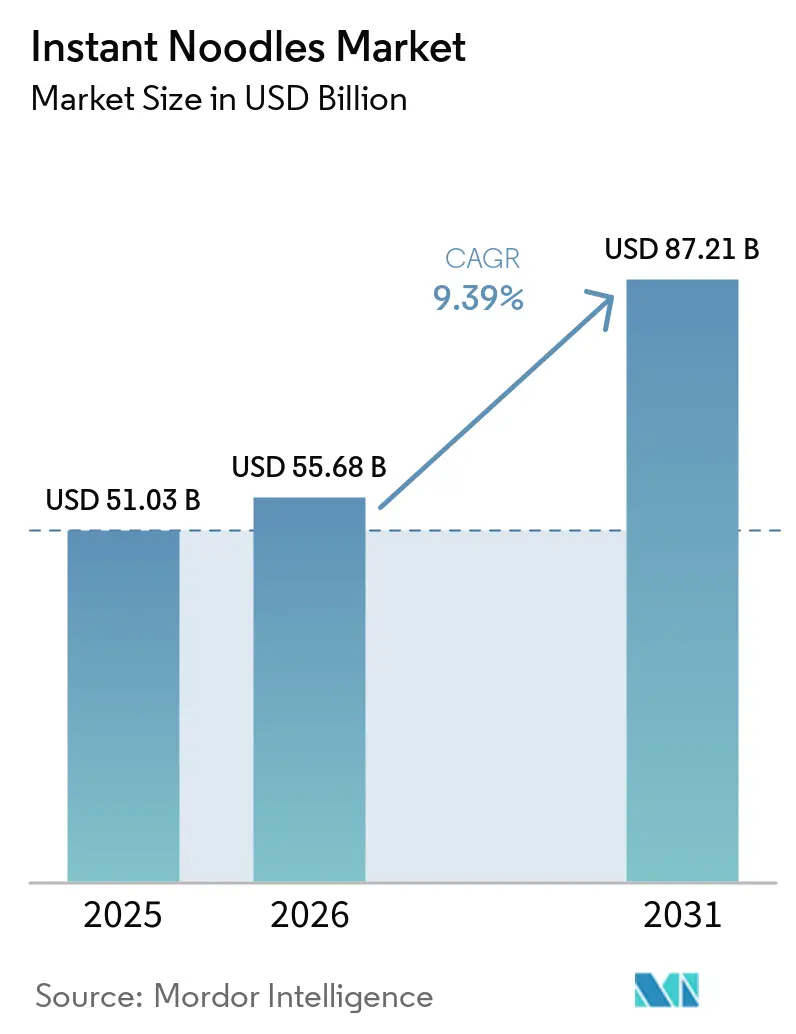

| Market Size (2026) | USD 55.68 Billion |

| Market Size (2031) | USD 87.21 Billion |

| Growth Rate (2026 - 2031) | 9.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Instant Noodles Market Analysis by Mordor Intelligence

The instant noodles market size is expected to grow from USD 51.03 billion in 2025 to USD 55.68 billion in 2026 and reach USD 87.21 billion by 2031, at a CAGR of 9.39% over 2026-2031. This growth within the instant noodles market is primarily driven by the increasing demand for convenient meal options among working households, as these products offer a combination of taste, affordability, and portability. The Asia-Pacific region continues to dominate sales, with premium cup products that use paper-based packaging contributing to higher profit margins for leading brands. Health-focused variants in the instant noodles market, fortified with iron, vitamins, or additional protein, are gaining traction in mainstream grocery stores. Furthermore, the expansion of electronic commerce (e-commerce) platforms and the availability of rapid delivery services are reshaping merchandising strategies. The competitive landscape remains moderately intense, with regional players and multinational companies achieving success by tailoring flavors to local preferences and adopting sustainable packaging solutions.

Key Report Takeaways

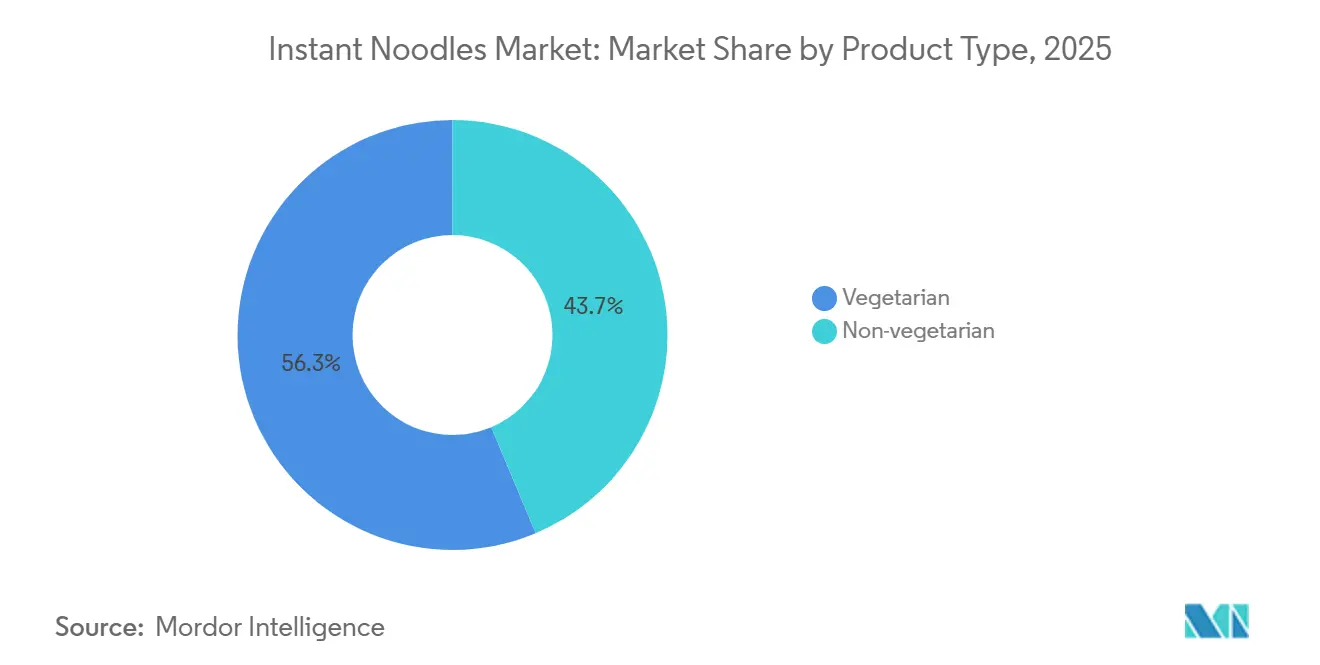

- By product type, non-vegetarian variants led with 43.67% of the instant noodles market share in 2025; vegetarian SKUs are projected to outpace every other cohort at a 9.91% CAGR through 2031.

- By serving size, single-serve packs held 61.82% of the instant noodles market size in 2025, while multi-packs are forecast to expand at a 10.54% CAGR between 2026 and 2031.

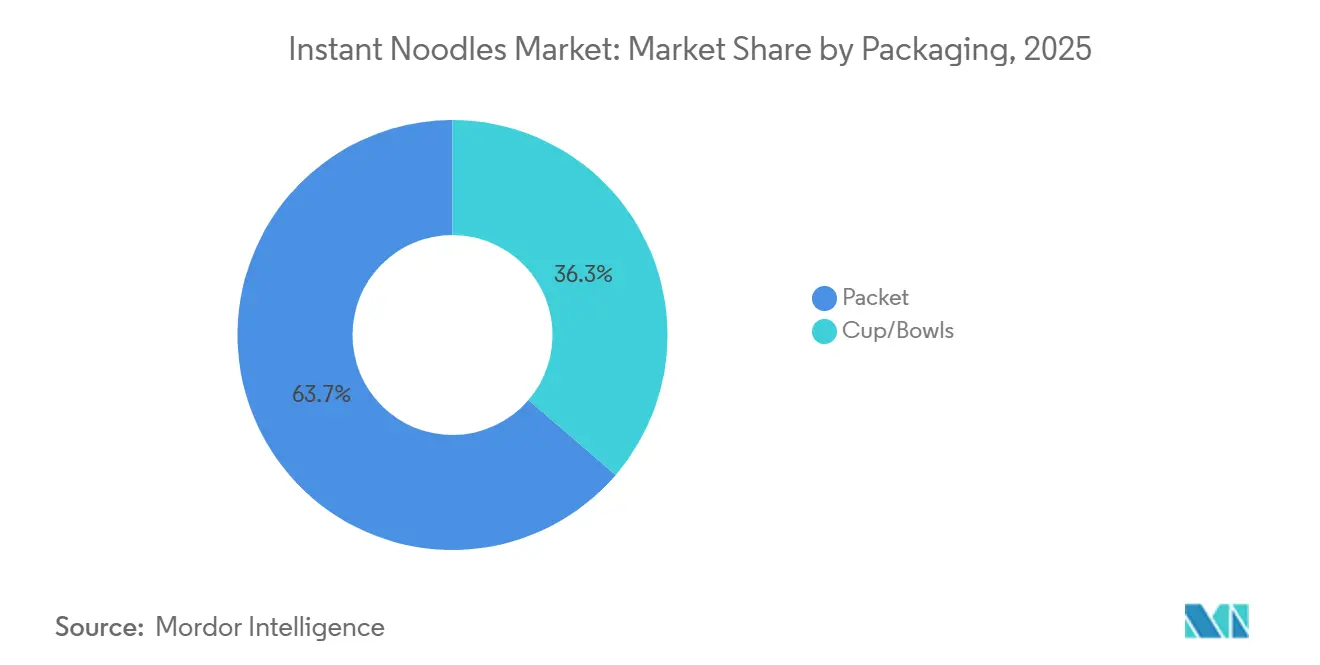

- By packaging, packets accounted for 63.72% of 2025 revenue; cup and bowl formats are expected to register the fastest 10.78% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets captured 42.82% of 2025 sales, yet online retail stores are positioned to grow at an 11.01% CAGR through 2031.

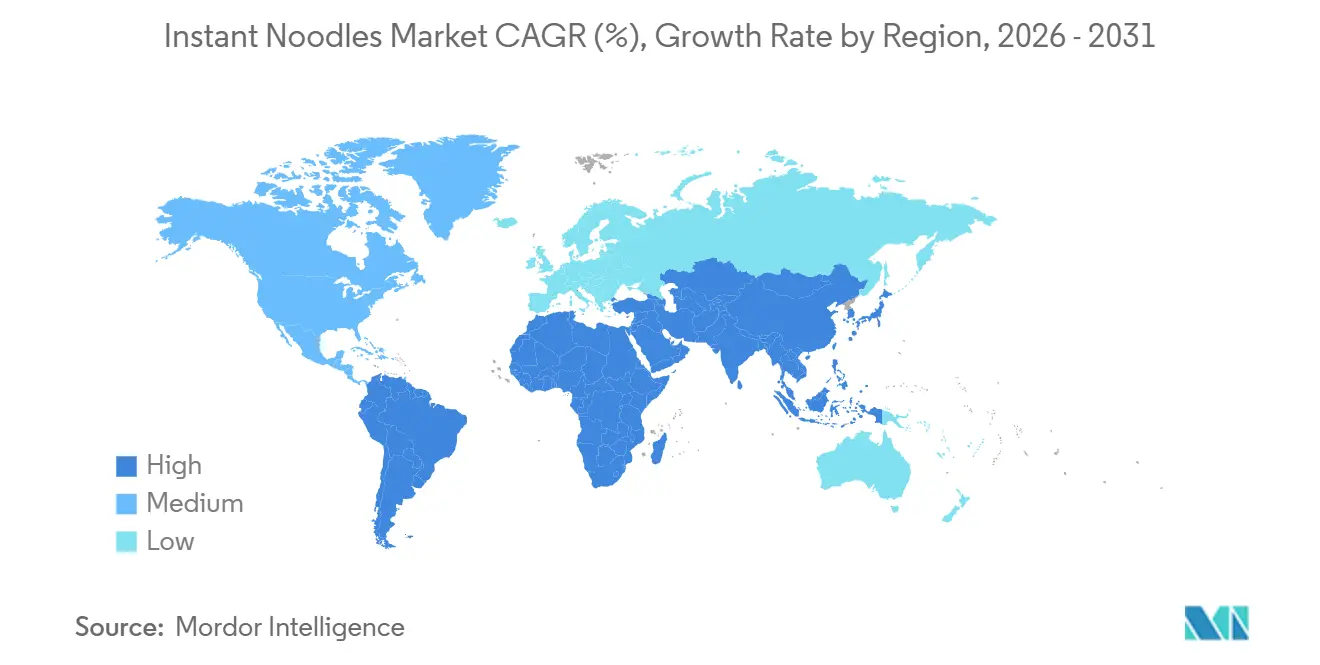

- By geography, Asia-Pacific contributed 74.82% of 2025 value and is on course for an 11.08% CAGR, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Instant Noodles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy lifestyles increase demand for quick, ready-to-eat meals | +2.1% | Global, with highest intensity in Asia-Pacific urban centers and North America | Short term (≤ 2 years) |

| Fortified noodles with vitamins and minerals target nutrition needs | +1.5% | Asia-Pacific (India, Indonesia, Philippines), Sub-Saharan Africa | Medium term (2-4 years) |

| Innovative textures like stir-fried or soup-less noodles attract foodies | +1.3% | North America, Europe, East Asia (Japan, South Korea) | Medium term (2-4 years) |

| Long shelf life supports stocking and emergency use | +0.9% | Global, with elevated demand in disaster-prone regions (Southeast Asia, Caribbean) | Long term (≥ 4 years) |

| Online retail and delivery platforms expand product availability | +2.4% | Asia-Pacific (China, India, Southeast Asia), Latin America | Short term (≤ 2 years) |

| Wide flavor variety attracts diverse taste preferences | +1.2% | Global, with regional flavor innovation hotspots in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient, ready-to-eat food

Urbanization and the increase in dual-income households are supporting growth in the instant noodles market by reducing the time available for meal preparation, making instant noodles a preferred choice for busy consumers. A recent global consumer survey highlights a growing preference for convenience over cost when purchasing packaged foods, indicating a broader lifestyle shift toward quick and easy meal solutions. In markets such as South Korea, convenience store chains have reported significant growth in ramen sales, driven by increased lunch-hour demand as consumers look for affordable alternatives to full-service restaurants amid rising inflation. Single-serve varieties now dominate convenience store offerings. Additionally, specialty ramen outlets are experiencing higher demand for bagged options suited for on-the-go consumption. This trend is also evident in emerging economies, where limited infrastructure and inconsistent access to fresh produce make shelf-stable noodles a reliable and practical food option, requiring only basic preparation with boiling water.

Fortified noodles with vitamins and minerals target nutrition needs

Micronutrient deficiencies continue to be a pressing issue in influencing innovation in the instant noodles market across low- and middle-income countries, prompting governments and manufacturers to take action by adding essential nutrients like iron, vitamin A, and folic acid to staple foods. In 2024, the World Health Organization (WHO) introduced updated fortification guidelines, recommending the inclusion of 30 to 40 milligrams of iron per kilogram of wheat flour in instant noodles to combat anemia rates that exceed 30% in South Asia. Responding to this, Nestlé India's Maggi brand launched iron-fortified variants in 2024, specifically targeting rural households where instant noodles are a primary source of carbohydrates. Research published in peer-reviewed journals in 2024 demonstrated that fortified instant noodles, which provide 15% of the daily iron requirement, improved hemoglobin levels in school-age children by 8% over six months. This finding underscores the potential of such products to address public health challenges. However, the cost of fortification increases production expenses by 3% to 5%, creating barriers for price-sensitive brands that focus more on affordability than on nutritional claims.

Innovative textures like stir-fried or soup-less noodles attract foodies

Texture innovation is expanding the global instant noodles market beyond traditional soup-based formats. Stir-fried yakisoba and dry-tossed variants accounted for 18% of new product launches in Japan during 2024, appealing to younger consumers who associate soup-less noodles with restaurant-quality meals. Between 2019 and 2024, Acecook introduced 68 new instant noodle products in Vietnam, focusing on regional textures such as pho-style rice noodles and bun rieu crab-paste variants that replicate street-food experiences. In the United States, Palmetto Gourmet Foods completed a United States Dollar (USD) 100 million expansion in 2024 to produce high-protein ramen with chewy, restaurant-grade noodles, targeting fitness enthusiasts willing to pay premium prices for 20 grams of protein per serving. These innovations command 15% to 30% price premiums over standard instant noodles but require specialized extrusion equipment and longer production cycles, creating barriers to entry for smaller manufacturers.

Long shelf life supports stocking and emergency use

Products in the instant noodles market, with their ambient shelf life of 12 to 18 months, are an essential part of emergency preparedness kits and government stockpiles. The United States Department of Agriculture (USDA) and the Department of Homeland Security (DHS) recommend including instant noodles in disaster supply kits due to their high caloric content and ease of preparation [1]. In Japan, the Cabinet Office requires local governments to maintain a three-day emergency food reserve, where instant noodles account for approximately 25% of stockpiled meals because they are compatible with portable gas stoves. The increasing frequency of climate-related disasters, as reported by the United Nations (UN), which noted a 40% rise in weather-related emergencies between 2015 and 2024, has further driven the demand for non-perishable foods. This trend ensures consistent demand for instant noodles, even during economic downturns, as households prioritize stocking essential pantry items over discretionary spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health concerns over high sodium content | -1.8% | Global, with regulatory intensity highest in North America, Europe, Singapore | Short term (≤ 2 years) |

| Allergens like gluten and MSG limit consumption for sensitive groups | -0.7% | North America, Europe, Australia | Medium term (2-4 years) |

| Environmental concerns about single-use plastic packaging | -1.2% | Europe, North America, Japan | Short term (≤ 2 years) |

| Counterfeit and unbranded products undermine trusted brands | -0.6% | Southeast Asia, South Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health concerns over high sodium content

A major challenge facing the instant noodles market is that sodium content in instant noodles generally ranges from 1,500 to 2,200 milligrams per serving, which exceeds the National Academies' chronic disease risk reduction intake limit of 2,300 milligrams per day for adults. The United States Food and Drug Administration's Phase II voluntary sodium reduction targets, introduced in 2024, set a maximum limit of 1,370 milligrams per 100 grams for instant noodles. This requires manufacturers to reduce sodium levels by approximately 25 percent from current formulations [2]. In Singapore, the Health Promotion Board has mandated the use of Nutri-Grade labels for instant noodles by mid-2027. Products that exceed sodium thresholds will receive lower grades, which may reduce their shelf visibility and consumer appeal [3]. Reformulating instant noodles to lower sodium content presents technical challenges, as sodium chloride plays a critical role in flavor, texture, and microbial stability. A 2024 white paper by Bell Flavors on clean-label umami systems highlighted kokumi peptides and yeast extracts as partial sodium replacements. However, these alternatives increase production costs by 8 to 12 percent and require extensive consumer acceptance testing.

Allergens like gluten and MSG limit consumption for sensitive groups

Wheat-based instant noodles are not suitable for consumers with celiac disease or gluten sensitivity, a group estimated to comprise 1 to 2 percent of the global population and growing due to improved diagnostic rates. A 2024 cross-national study comparing gluten-free instant noodles in Thailand and Denmark revealed that rice-based formulations achieved a texture comparable to wheat noodles but incurred 15 percent higher production costs due to specialized extrusion processes and longer drying times. Monosodium glutamate, commonly abbreviated as MSG, is a widely used flavor enhancer in many Asian instant noodles but continues to face consumer skepticism despite regulatory approval. According to a 2024 survey, 22 percent of North American consumers actively avoid products labeled with monosodium glutamate. In the same year, Perfect Earth introduced organic gluten-free instant noodles made from brown rice and quinoa, targeting health-conscious consumers willing to pay a premium of 40 to 60 percent. However, distribution remains limited to specialty retailers and e-commerce platforms. Additionally, allergen-free formulations pose manufacturing challenges, as dedicated production lines are required to prevent cross-contamination, which reduces asset utilization for mid-sized manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetarian Variants Gain Momentum

Vegetarian products in the instant noodles market are projected to grow at a compound annual growth rate (CAGR) of 9.91% between 2026 and 2031, surpassing the growth rate of the non-vegetarian segment. Despite this, non-vegetarian products are expected to account for 43.67% of the instant noodles market in 2025. This trend is primarily driven by India's cultural and religious dietary preferences, where over 90% of instant noodle stock-keeping units are formulated without meat or seafood. ITC Foods' Sunfeast Yippee! The brand reported an 8.2% revenue increase in fiscal 2024, attributing this growth to vegetarian masala and curry variants that cater to regional taste preferences.

Non-vegetarian instant noodles, which include chicken, beef, seafood, and pork flavors, continue to dominate in East Asia and Southeast Asia, where meat-based broths are integral to local cuisines. For example, Samyang's Buldak fire-chicken ramen, a spicy non-vegetarian product, achieved 28.7% revenue growth in 2024, supported by viral social media challenges and expanded distribution to over 100 countries. However, increasing awareness of antibiotic use in livestock and concerns about processed meat consumption are encouraging health-conscious consumers to shift toward vegetarian alternatives. This change is particularly noticeable in markets with strong wellness trends, such as North America and Western Europe.

By Serving: Multi-Packs Capture Bulk-Buying Behavior

Multi-packs in the instant noodles market are anticipated to grow at a compound annual growth rate (CAGR) of 10.54% from 2026 to 2031. This growth is attributed to the cost efficiencies provided by hypermarket and e-commerce channels, where unit costs are 20% to 35% lower compared to single-serve formats. Dingdong, a Chinese instant-delivery platform, reported that multi-pack instant noodles generated higher gross merchandise value per transaction than single-serve packs, as consumers often stock up during promotional events. In 2024, Tingyi's Master Kong brand in China introduced 10-pack bundles featuring regional flavor assortments, catering to households that consume instant noodles multiple times per week.

Single-serve packs represented 61.82% of the market in 2025, supported by convenience-store and vending-machine channels, where immediate consumption drives purchasing decisions. CU convenience stores in South Korea reported that 73% of ramen sales in their specialty store format were single-serve bagged noodles, reflecting lunch-hour demand from office workers. Furthermore, Nissin Foods introduced microwaveable paper cups in 2024, allowing single-serve consumption without requiring stovetops, thereby broadening usage occasions to offices, dormitories, and travel settings.

By Packaging: Cup and Bowl Formats Innovate for Convenience

In the instant noodles market, cup and bowl packaging is expected to grow at a compound annual growth rate (CAGR) of 10.78% between 2026 and 2031. This growth is primarily driven by advancements in microwaveable and sustainable materials, which improve convenience while addressing environmental concerns. For example, Nissin Foods USA plans to transition to paper cups with 40% recycled fiber in 2024, eliminating polystyrene and making the cups microwave-compatible. This change allows consumers to add fresh ingredients, such as eggs and vegetables, directly into the cup. Similarly, Unilever's Pot Noodle brand in the United Kingdom tested paper-based packaging in 2023, aiming to attract younger consumers who value sustainability over price.

Furthermore, a study investigated the use of edible polyvinyl-alcohol and sodium-alginate bilayer pouches for seasoning oils. These pouches dissolve in hot water, reducing sachet waste while extending the shelf life of the oil. However, the commercial scalability of this innovation remains uncertain. Packet formats held 63.72% of the market share in 2025, benefiting from lower material costs and compatibility with traditional stovetop preparation methods. Indofood's Indomie brand in Indonesia retained a significant portion of the market by distributing packet noodles to over 150,000 retail outlets. The company utilized vertical integration to effectively manage costs.

By Distribution Channel: Online Retail Disrupts Traditional Channels

Online retail stores are anticipated to grow at a compound annual growth rate (CAGR) of 11.01% from 2026 to 2031, representing the fastest growth rate among distribution channels. This growth is being driven by the increasing adoption of video commerce and 30-minute delivery models, which are significantly influencing consumer purchasing behavior. According to the 2024 Southeast Asia e-Conomy report by Google, Temasek, and Bain, more than 40% of shoppers rely on video content to make purchase decisions. Instant noodles, in particular, have gained from cooking demonstrations and flavor reviews that help reduce the perceived risk of trying new products. Dingdong's Chinese platform reported approximately 13,000 instant-food stock-keeping units (SKUs) in 2023, with private-label instant noodles contributing over 20% of grocery gross merchandise value through its 30-minute delivery service, directly competing with convenience stores.

Supermarkets and hypermarkets accounted for 42.82% of the market in 2025, leveraging promotional pricing strategies and prominent shelf placement to boost sales volumes. The 2024 European grocery report by Savills highlighted that food inflation is encouraging consumers to shift towards discounters and private-label products. Instant noodles have benefited from this trend due to their affordability, making them a popular choice during periods of economic downturn.

Geography Analysis

Asia-Pacific dominated the global instant noodles market, accounting for 74.82 percent of the market share in 2025. The region was characterized by high per capita consumption and expanding middle-class populations, which were key drivers of growth. In 2023, Japan recorded 46 servings per capita, while South Korea exceeded 75 servings per capita, the highest globally. This reflected the positioning of instant noodles as a dietary staple rather than just a convenience food in these countries.

North America and Europe are experiencing slower growth compared to Asia-Pacific, but are witnessing a shift toward premium products. Health-conscious consumers in these regions are increasingly choosing low-sodium, organic, and high-quality instant noodle options. In 2024, Nissin Foods USA transitioned to microwaveable paper cups, eliminating polystyrene and reducing plastic wrap to address environmental concerns, particularly among younger demographics. Additionally, Palmetto Gourmet Foods invested USD 100 million in 2024 to expand its production of high-protein ramen, offering 20 grams of protein per serving and targeting fitness enthusiasts in the United States who are willing to pay a premium for nutritionally enhanced products.

South America, the Middle East, and Africa represent smaller but emerging instant noodles market. Affordability and long shelf life are the primary factors driving adoption in these regions. In Brazil and Argentina, urbanization and rising disposable incomes are contributing to increased demand, although distribution infrastructure remains less developed compared to Asia-Pacific. In Sub-Saharan Africa, counterfeit and unbranded products account for 10 to 15 percent of sales in rural areas, creating challenges for branded players by undermining their pricing power.

Competitive Landscape

The global instant noodles market is moderately fragmented, with strong regional leaders operating alongside multinational corporations. Prominent companies such as Nissin Foods Holdings, Nestlé, Unilever, Tingyi, and Indofood collectively hold a significant instant noodles market share. At the same time, there are opportunities for local brands to grow by offering culturally relevant flavors and adopting competitive pricing strategies. Nissin Foods Holdings has reported steady revenue growth in recent years, while Samyang Foods has gained international traction, driven by the success of its Buldak ramen, which became popular through social media challenges.

Strategies across the instant noodles industry are centered on differentiation through premium product formulations, environmentally friendly packaging, and digital-first distribution models. For example, Nissin’s introduction of microwaveable paper cups made from recycled fiber demonstrates how packaging innovation can strengthen brand positioning while meeting sustainability and regulatory requirements. Additionally, there is considerable growth potential in fortified and allergen-free product varieties, where consumer demand continues to outpace supply. Gluten-free options, often made from alternative bases such as rice or quinoa, command higher price points but are primarily limited to specialty channels due to higher production costs and the need for dedicated facilities to prevent cross-contamination.

Emerging companies like Palmetto Gourmet Foods are capitalizing on health and wellness trends by offering high-protein and gluten-free products targeted at fitness-conscious consumers. These efforts are supported by expansion plans aimed at significantly increasing production capacity in the coming years. Technological advancements across the instant noodles industry, such as blockchain-verified quick response (QR) codes under the Global Standards One (GS1) framework in Hong Kong, are improving transparency and product authentication. However, the high costs associated with these technologies currently limit their application to premium product categories. Meanwhile, the rise of e-commerce platforms in China and the growing adoption of video-commerce models across Southeast Asia are reshaping go-to-market strategies. These developments allow niche brands to bypass traditional retail networks, achieve higher direct-to-consumer margins, and reinvest in innovation and subscription-based offerings.

Instant Noodles Industry Leaders

Nissin Foods Holdings Co., Ltd.

Unilever PLC

Nestlé S.A.

Nongshim Co., Ltd.

PT Indofood CBP Sukses Makmur Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cup Noodles unveiled its newest limited-edition flavor, Cup Noodles Dill Pickle. This flavor melds the sharp zest of dill pickles with the satisfaction of noodles, offering a delightful tangy twist. The product is available on online stores and in stores, including Walmart, Albertsons, and other major retailers.

- March 2025: Wow! Momo entered the high-growth cup noodles market with a variety of Asian and Indian flavors. The company, Wow! Momo Foods has outlined a strategic objective to achieve INR 100 crore in revenue from its newly launched product line, Wow! Noodles, within the next 24 months.

- November 2024: Nissin introduced caffeinated cup noodles in Japan, incorporating key ingredients commonly found in energy drinks, such as caffeine, arginine (an amino acid that supports protein synthesis), and niacin (vitamin B3).

- September 2024: Batchelors introduced a new product to its portfolio, the Super Noodles Chilli and Lime Pot. This latest offering is available at leading United Kingdom retailers, including Sainsbury’s, Farmfoods, B and M, and Home Bargains.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the instant noodles market as the value generated by factory-produced, shelf-stable noodle cakes supplied with seasoning that consumers reconstitute in hot water; packets, cups, and bowls are all included at manufacturer selling price across retail and food-service channels.

Scope Exclusions: Cold or fresh ramen, wet-noodle kits, handmade noodles, and restaurant-prepared servings remain outside this scope.

Segmentation Overview

- By Product Type

- Vegetarian

- Non-vegetarian

- By Serving

- Single-Serve Packs

- Multi Packs

- By Packaging

- Cup/Bowls

- Packet

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Others Distribution Channel

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct semi-structured interviews with noodle makers, ingredient processors, big retailers, and logistics partners across Asia-Pacific, North America, Europe, and key emerging markets. These conversations validate serving-per-capita ratios, ex-factory prices, and uptake of air-dried formats, closing gaps left by desk work.

Desk Research

We begin by mapping demand through public, high-credibility datasets such as World Instant Noodles Association serving counts, FAO cereal utilization tables, UN Comtrade HS-1902 trade flows, and OECD consumer-spend series. Company filings, 10-Ks, investor decks, and national customs records enrich price and channel splits, while news and financial snippets are pulled via Dow Jones Factiva and company intelligence from D&B Hoovers. Peer-reviewed journals and trade associations like the Nutrition Society and the Japan Convenience Food Association help our analysts track health and packaging trends. This list is illustrative. Many additional secondary references support data collection, validation, and research clarification.

Market-Sizing & Forecasting

A top-down model converts verified serving volumes into value through weighted average selling prices adjusted for regional mix, import penetration, and currency. Supplier revenue roll-ups and sampled packet-price-times-volume checks act as bottom-up reasonableness tests. Core variables, including urban convenience index, wheat and palm-oil price curves, disposable-income growth, e-commerce penetration, and annual flavor-launch counts, feed a multivariate regression that projects demand through 2030. Missing splits are interpolated with nearest-neighbor trade ratios that our primary contacts confirm.

Data Validation & Update Cycle

Before release, each model passes variance and anomaly screens. A peer review round follows. Material events trigger mid-cycle refreshes, while regular reports are fully updated every twelve months.

Why Mordor's Instant Noodles Baseline Commands Confidence

Published estimates often diverge because firms choose different product baskets, price ladders, and refresh timings, and we preview those gap drivers here. Our disciplined scope, annual serving audit, and dual-track modeling give decision-makers a transparent baseline tied to clearly documented variables.

Key drivers of variance include some studies folding premium ready meals or dehydrated pasta mixes into instant noodles, others back-casting long-horizon scenarios into the base year, and many applying undisclosed average prices that overstate revenue in lower-price Asian markets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 50.97 B | Mordor Intelligence | |

| USD 64.67 B | Global Consultancy A | Counts gourmet meal kits and sauces, inflating scope |

| USD 83.18 B | Research House B | Uses 2035 forecast scaled backward and broad ASP multipliers |

These comparisons show that Mordor's carefully bounded definition and annually refreshed variables provide users with a balanced, reproducible view they can rely on.

Key Questions Answered in the Report

How large is the instant noodles market in 2026?

The instant noodles market size stands at USD 55.68 billion in 2026 and is projected to reach USD 87.21 billion by 2031.

Which region buys the most instant noodles?

Asia-Pacific commands nearly three-quarters of global sales and is expanding at the fastest regional CAGR of 11.08%.

What packaging trends are shaping product innovation?

Microwave-safe paper cups and mono-material films are replacing polystyrene and multilayer plastics to meet recycled-content mandates.

Why are brands fortifying instant noodles with iron?

Fortification helps tackle anemia rates above 30% in parts of Asia and Africa, and WHO guidelines support adding 30–40 mg of iron per kg of wheat flour.

Page last updated on: