Market Overview

| Study Period | 2021 - 2031 |

|---|---|

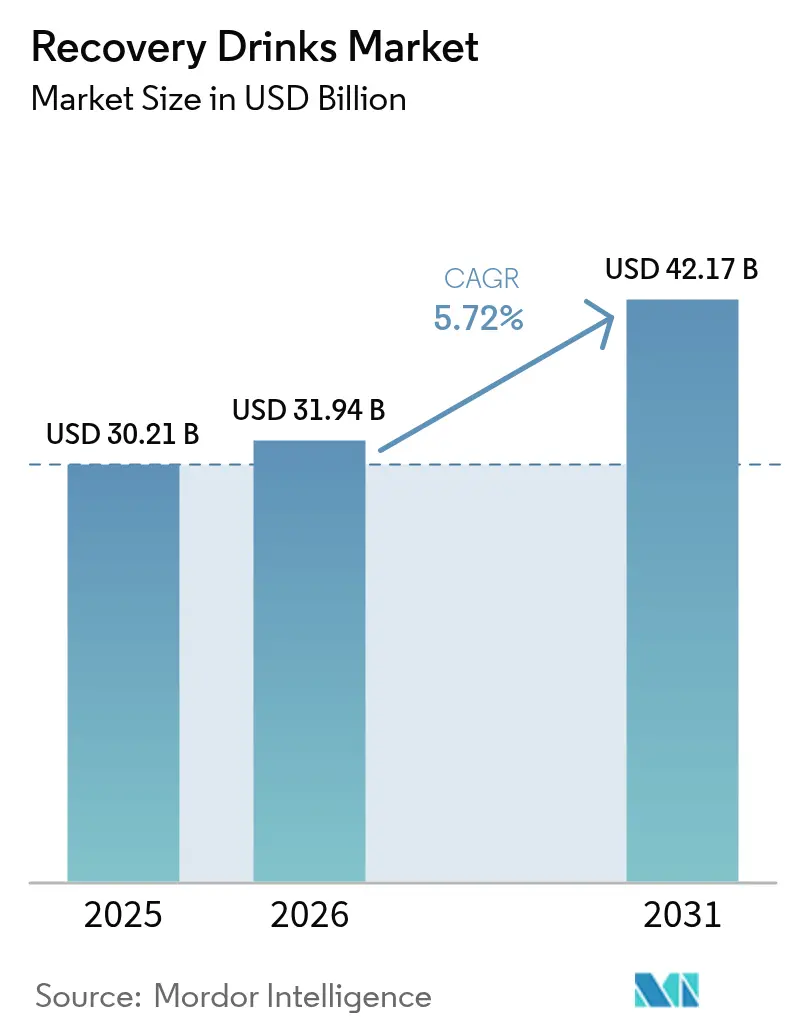

| Market Size (2026) | USD 31.94 Billion |

| Market Size (2031) | USD 42.17 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Recovery Drinks Market Analysis by Mordor Intelligence

The recovery drinks market size is expected to grow from USD 30.21 billion in 2025 to USD 31.94 billion in 2026 and is forecast to reach USD 42.17 billion by 2031 at 5.72% CAGR over 2026-2031. As endurance sports gain popularity and protein-rich diets become mainstream, product portfolios are evolving to meet changing consumer demands. We're seeing a significant shift towards zero-sugar electrolyte blends, ready-to-drink (RTD) beverages packed with 40–50 grams of protein, and formulations designed to support gut health and microbiome balance. Beverage giants are defending their market share by introducing zero-sugar product extensions and adopting sustainable practices, such as using recycled packaging. At the same time, direct-to-consumer brands are disrupting the market by offering personalized formulations at competitive prices, appealing to a growing segment of health-conscious consumers. In the U.S. and Europe, regulatory bodies are enforcing stricter caps on added sugars and closely monitoring health claims made by manufacturers. While these regulations have driven up reformulation costs for many companies, they also present opportunities for innovation, particularly in the development of naturally sweetened, clean-label products that align with consumer preferences for transparency and health benefits. Additionally, the rise of digital commerce and subscription-based models is reshaping the sports nutrition market. Although these models are compressing profit margins, they are simultaneously increasing average order values. Consumers are leveraging these platforms to bundle recovery drinks with complementary sports-nutrition products, creating a more integrated and convenient purchasing experience.

Key Report Takeaways

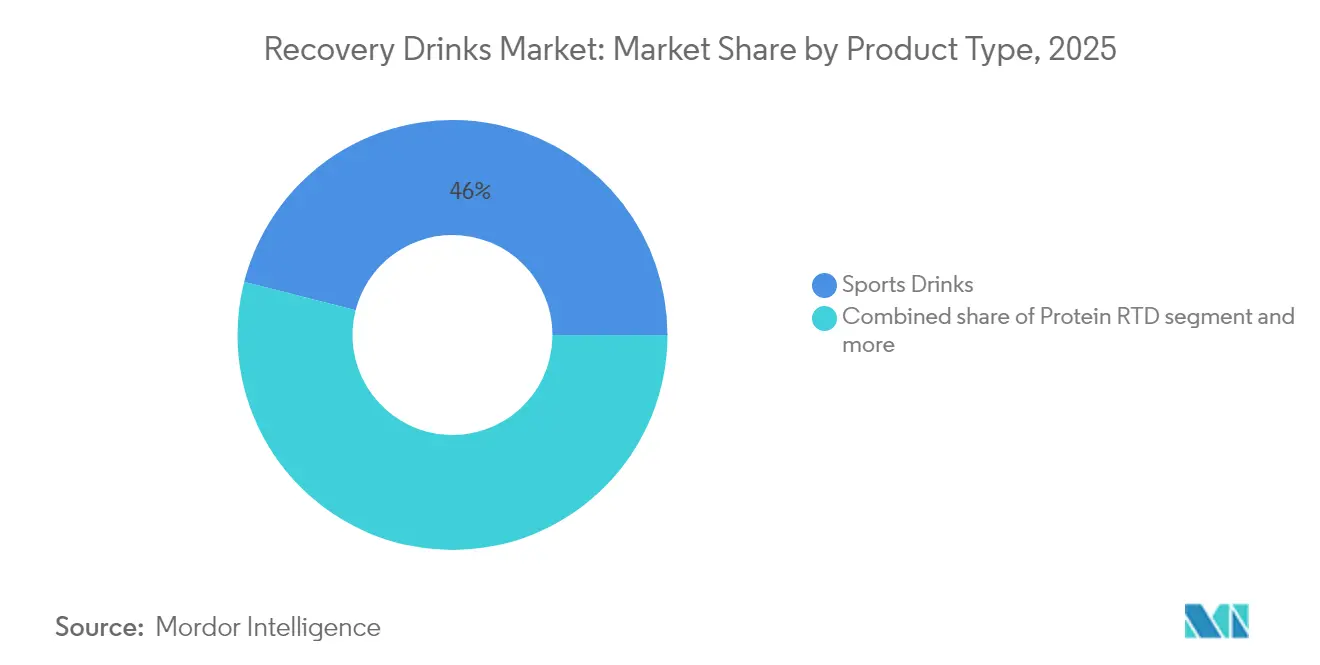

- By product type, Sports Drinks led with a 46.02% share of the recovery drinks market in 2025, whereas Protein RTD is projected to post the fastest 7.12% CAGR through 2031.

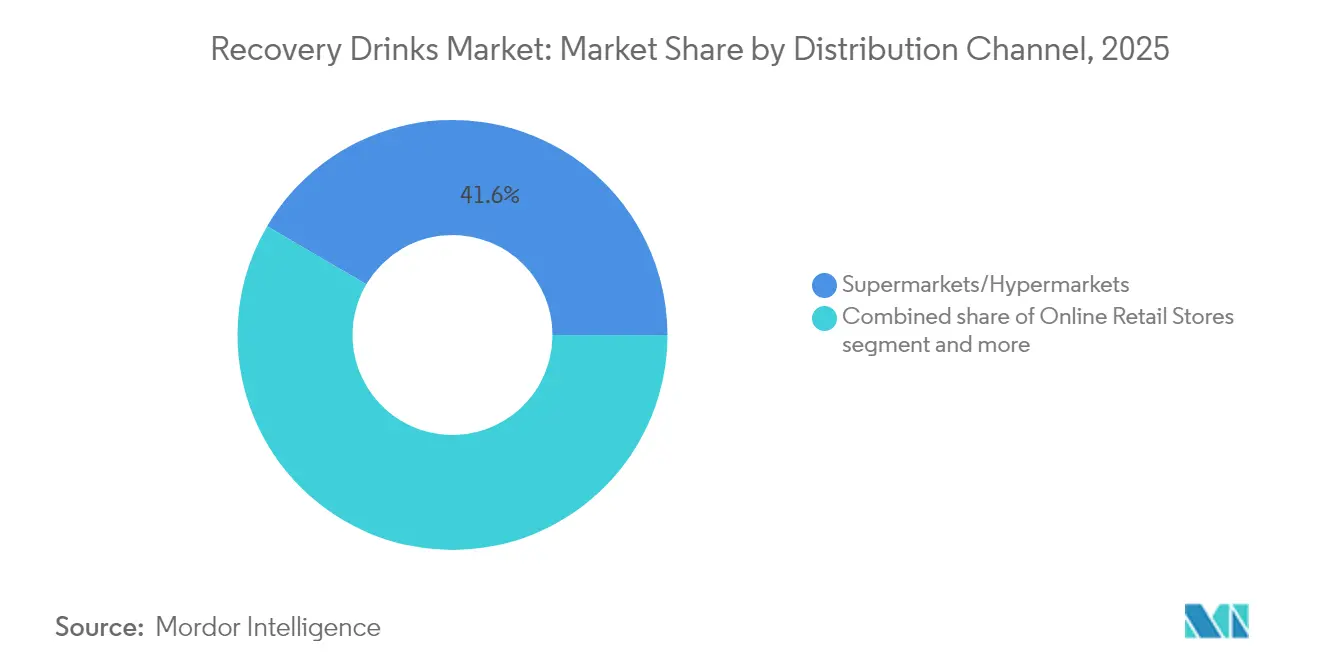

- By distribution channel, Supermarkets and Hypermarkets held 41.55% of the recovery drinks market share in 2025, while Online Retail Stores are poised to expand at a 6.23% CAGR over 2026-2031.

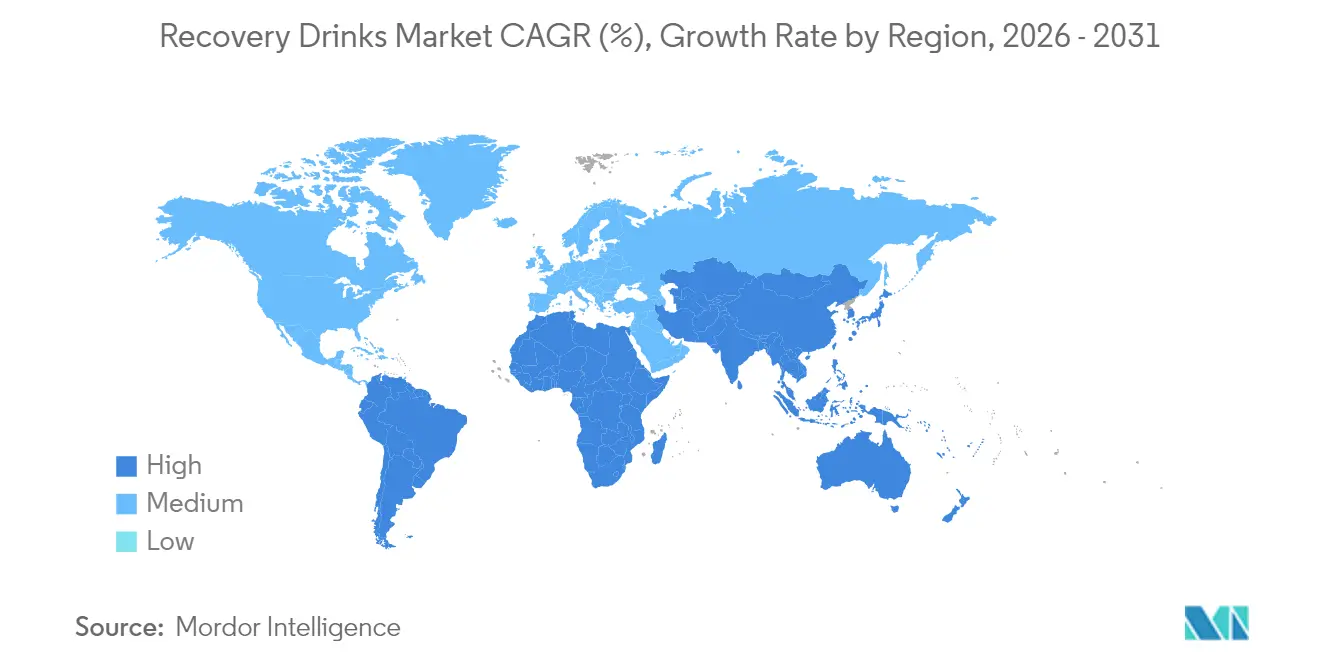

- By geography, North America commanded 38.62% of the recovery drinks market size in 2025, but Asia-Pacific is forecast to grow at an 7.88% CAGR, the quickest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Recovery Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Endurance-sport participation on the rise | +0.9% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Health-conscious consumers are growing | +1.2% | Global, particularly North America, Europe, and affluent APAC metros | Long term (≥ 4 years) |

| E-commerce sales of sports nutrition expanding | +0.8% | Global, led by North America and China; accelerating in India, Southeast Asia | Short term (≤ 2 years) |

| Elite athletes endorse brands | +0.5% | North America and Europe; emerging in Latin America and Middle East | Short term (≤ 2 years) |

| Recovery formulations target the microbiome | +0.7% | North America and Europe; early adoption in Japan, South Korea | Medium term (2-4 years) |

| Research spin-offs for military hydration | +0.4% | North America, with spillover to NATO allies and defense contractors globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Endurance-sport participation on the rise

In 2024, registrations for marathons and triathlons saw a notable uptick, leading to a surge in recovery drink consumption within the crucial 30-minute window post-exercise[1]Source: American College of Sports Medicine, "ACSM Announces Top Fitness Trends for 2025", acsm.org. This growth reflects the increasing awareness among athletes about the importance of timely recovery to enhance performance and reduce fatigue. Supermarkets have begun bundling multipacks of these drinks, specifically targeting recreational runners who adhere to structured recovery routines, thereby catering to a growing segment of health-conscious consumers. Events like the ultra-distance 100-mile trail runs have brought to light the benefits of branched-chain amino acids and sustained-release carbohydrates, highlighting their role in prolonged glycogen replenishment and muscle recovery during extended physical exertion. Meanwhile, free 5 km community runs, drawing in 300,000 participants weekly on a global scale, have helped normalize the use of recovery drinks among casual athletes, fostering a culture of post-exercise nutrition even among non-professional runners. In response to this trend, retailers are now offering smaller bottle sizes that conveniently fit into race bags, simultaneously promoting impulse purchases and meeting the practical needs of athletes during events.

Health-conscious consumers are growing

Seventy-one percent of shoppers prioritize protein content in their selections, while 66% consciously limit their sugar intake. Following the World Health Organization's recommendation to keep free sugars under 10% of total energy, brands are increasingly turning to stevia and monk fruit for their electrolyte solutions, as these natural sweeteners align with consumer demand for healthier alternatives[2]Source: World Health Organization, "WHO calls on countries to reduce sugar intake among adults and children", who.int. New product launches now prominently feature clean labels, spotlighting recognizable ingredients like pea protein, coconut water, and natural colors, which appeal to health-conscious consumers seeking transparency in product formulations. Sales of protein-rich ready-to-drink beverages are surging among adults on GLP-1 receptor agonists, who aim to maintain lean mass even while restricting calories, as these beverages provide a convenient and effective way to meet protein requirements. As regulatory bodies converge on front-of-pack sugar warnings, there's a notable uptick in the adoption of zero-sugar stock-keeping units (SKUs), driven by both consumer preferences and compliance with evolving regulations.

E-commerce sales of sports nutrition expanding

In 2024, online platforms witnessed a robust growth of 15–20%. This surge empowered direct-to-consumer brands to sidestep traditional shelf-space negotiations. These brands now offer tailored product mixes, adjusting to individual workout intensities. Meanwhile, subscribe-and-save models have emerged as a lucrative strategy, ensuring consistent cash flows. They also elevate average order values by bundling items like protein powders with hydration tablets. In response, brick-and-mortar retailers have adopted strategies like click-and-collect and same-day delivery, aiming to capture those post-workout impulse buys. Additionally, social-commerce live streams have revolutionized sales, moving thousands of units in mere minutes by seamlessly merging entertainment with instant purchasing. Online platforms have heightened the visibility of cost-per-gram metrics, intensifying price competition in both protein and electrolyte categories.

Elite athletes endorse brands

In 2024, U.S. college sports policy shifts paved the way for numerous athlete sponsorships, seamlessly integrating recovery-drink brands into the daily narratives of Gen Z. These sponsorships have enabled brands to engage with a younger, health-conscious audience directly, leveraging athletes' influence to build trust and credibility. Lionel Messi exemplifies the athlete-founder model, showcasing how celebrity influence translates to prime shelf space and elevated price tags, further driving consumer interest. Unlike conventional advertisements, the collaborative creation of novel flavors and immediate training content fosters an unmatched authenticity that resonates deeply with consumers seeking relatable and aspirational connections. To mitigate risks, brands are broadening their endorsement portfolios, spanning various sports and regions, ensuring a balanced approach to market exposure. Genuine collaborations with athletes expedite the buying process, as fans increasingly embrace professional-grade recovery routines, inspired by their favorite sports personalities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over sugar content and regulatory focus | -0.6% | Global, with acute pressure in Europe and North America | Short term (≤ 2 years) |

| Private labels intensify price competition | -0.5% | North America and Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Key electrolytes face supply-chain volatility | -0.4% | Global, with dependencies on China and South America for raw materials | Medium term (2-4 years) |

| Backlash against single-use RTD bottles | -0.3% | Europe and North America; growing in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns over sugar content and regulatory focus

In 2024, the FDA updated its "healthy" label criteria, capping added sugars at 2 grams per reference amount[3]Source: Food and Drug Administration, "Use of the 'Healthy' Claim on Food Labeling", fda.gov. This move effectively disqualifies a majority of legacy isotonic drinks, pushing manufacturers to reformulate their products to meet the stricter guidelines. Since 2016, the EFSA has turned down 87.7% of health-claim applications for sports drinks, significantly limiting their ability to market efficacy-related benefits. Reformulating drinks with allulose and stevia demands rigorous sensory trials to sidestep undesirable off-flavors, as these sugar substitutes can impact taste profiles if not carefully balanced. Additionally, varied global regulations lead to fragmented portfolios, forcing brands to manage higher inventory costs due to the need for region-specific formulations. Brands that can't adapt to the new sugar thresholds find themselves losing shelf space to compliant, zero-sugar alternatives, which are increasingly favored by both regulators and health-conscious consumers.

Private labels intensify price competition

Retailer house brands are underpricing leading SKUs by 20–30%, using their scale and reduced marketing expenses to squeeze category margins. These private-label products often appeal to cost-conscious consumers, especially during periods of economic uncertainty. In North America, private-label sports drinks command a 15-20% market share, a figure that tends to surge during economic downturns as consumers prioritize affordability. In response, branded manufacturers are incorporating unique functional ingredients such as adaptogens, probiotics, and nootropics that pose a challenge for private labels to replicate swiftly. These ingredients not only differentiate branded products but also cater to the growing consumer demand for health and wellness benefits. Meanwhile, aluminum and paper cartons are not just eco-friendly choices but also bolster a premium market positioning, appealing to environmentally conscious consumers willing to pay a higher price. However, smaller players, devoid of robust R&D and marketing capabilities, find themselves under pressure to consolidate as they struggle to compete with both private labels and established brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Protein RTD Redefines Recovery

In 2025, sports drinks dominate the global recovery drinks market, holding a 46.02% share. Their stronghold is bolstered by widespread consumer recognition, endorsements from established athletes, and prominent visibility in both convenience and fitness retail channels. Yet, growth in this segment is decelerating, challenged by sugar-reduction mandates and intensifying competition from private-label brands. To navigate these challenges, many are reformulating with natural sweeteners like monk fruit, targeting health-conscious athletes who are now more vigilant about sugar intake. This shift underscores a broader industry trend: a move towards cleaner hydration solutions that still deliver performance benefits.

Protein RTDs are on a rapid ascent, with projections indicating a CAGR of 7.12% through 2031, outstripping all other recovery drink categories. Products such as Fairlife’s Core Power Elite, boasting 50 grams of whey protein per bottle, are becoming favorites among gym enthusiasts, older adults warding off sarcopenia, and bariatric patients in search of nutrient-rich options. Additionally, users of GLP-1 medications, who emphasize preserving lean mass during weight loss, are bolstering the segment's growth. Innovations are emerging, including strains aimed at enhancing amino-acid absorption and cutting-edge microfiltration techniques that maintain flavor while reducing lactose. The introduction of plant-based options, harnessing pea and rice proteins, broadens the segment's appeal, even as there's a continued focus on refining taste and texture.

By Distribution Channel: Online Retail Disrupts Shelf Dynamics

In 2025, supermarkets secured 41.55% of the revenue in the recovery drinks market, leveraging high visibility and impulse purchases to dominate post-workout needs. Their strategic placement of products and promotional campaigns further enhances their appeal to consumers seeking convenient options. To counter the online trend, brick-and-mortar chains are adopting click-and-collect services and same-day delivery, aiming to boost foot traffic and increase basket sizes. These services cater to time-sensitive customers while maintaining the in-store shopping experience. In densely populated regions like Japan and South Korea, convenience stores are utilizing vending machines for quick access, ensuring availability at all hours, and are employing loyalty apps to offer geo-targeted discounts based on workouts tracked by wearables. Specialty gyms and events, despite their niche scale, are acting as premium trial hubs, providing consumers with opportunities to sample high-quality products, thereby swaying broader adoption and influencing purchasing decisions.

Online retail is the fastest-growing channel, boasting a 6.23% CAGR. This growth is driven by platforms like Amazon's Subscribe & Save, which facilitates recurring shipments, and a focus on data-driven personalization that tailors offerings to individual preferences. Brands selling directly to consumers are leveraging insights on consumption to innovate flavors and release limited editions streamed by influencers that quickly sell out, creating a sense of exclusivity and urgency. With social commerce on the rise, brands are feeling the pressure to emphasize functional benefits and sustainable packaging, especially in light of transparent pricing. This trend is particularly evident in China's live-streaming model, which is now making waves in Western markets, showcasing how interactive and engaging formats can drive sales. While traditional retail faces challenges, the expansion through bundled offerings and the convenience of e-commerce is evident, providing consumers with greater flexibility and value.

Geography Analysis

In 2025, North America commanded a significant 38.62% share of the recovery drinks market revenue. This dominance is attributed to the region's deep-rooted gym culture, a vibrant collegiate sports scene, and an early embrace of zero-sugar SKUs, aligning with the FDA's 2-gram sugar guideline. However, the landscape is becoming increasingly competitive. Warehouse clubs and e-commerce behemoths are intensifying the private-label competition, squeezing margins. In response, established brands are pivoting towards ingredient differentiation and forging partnerships with athletes. While Canada grapples with the added costs and slower rollouts due to its bilingual labeling requirements, Mexico faces economic cycles that introduce volume volatility, even as fitness participation rises.

Asia-Pacific is set to lead the global pack with an anticipated 7.88% CAGR through 2031. This growth is fueled by China's robust double-digit expansion in sports nutrition and the burgeoning middle class in India. China's streamlined registration for special foods is facilitating a surge in imports, albeit at the cost of heightened compliance fees for smaller brands. In India, the retail landscape's fragmentation necessitates a hybrid distribution approach, seamlessly integrating e-commerce, modern trade, and traditional kirana stores. Japan is innovatively merging its aging demographic's needs with its established functional drink culture, infusing collagen and probiotics into ready-to-drink (RTD) offerings tailored for seniors. South Korea, riding the K-wellness wave, is shaping regional preferences in flavors and functional ingredients. Europe's landscape is marked by stringent sustainability mandates and the European Food Safety Authority's (EFSA) rigorous claim approvals. While these create formidable entry barriers, brands that navigate them successfully find themselves rewarded with premium shelf positioning. Germany and the UK lead in consumption, but Southern Europe is catching up swiftly, buoyed by a surge in gym memberships. Northern Europe's deposit-return infrastructure is championing recycled-content mandates, leading to a swift shift away from PET. Eastern Europe presents growth opportunities, yet geopolitical currency risks loom large, complicating pricing strategies.

In South America, Brazil's soccer fervor drives the bulk of demand. Yet, inflation and currency devaluation are nudging consumers towards private labels and smaller pack sizes. Both Colombia and Chile are witnessing a surge in gym memberships, but fragmented logistics are hampering swift inventory turnover. Argentina's macroeconomic challenges are stifling investments, compelling brands to either import or co-pack within the region. The Middle East and Africa present a dichotomy of elite opportunities juxtaposed with affordability challenges. The UAE and Saudi Arabia are making significant strides, pouring investments into global sporting events and gym infrastructures, and are quick to embrace premium zero-sugar RTDs. South Africa boasts a well-established retail scene, ensuring steady growth, yet grapples with economic disparities that limit volume. Nigeria, with its expansive population, holds promise for a brighter future, contingent on overcoming hurdles like cold-chain logistics and enhancing purchasing power. Meanwhile, Turkey and Morocco are emerging as pivotal manufacturing hubs, albeit with challenges stemming from currency fluctuations and political uncertainties.

Regulatory Landscape

Regulation is increasingly focused on sugar thresholds, stimulant transparency, and substantiation of functional claims, which is influencing recovery-drink formulation and labeling. In the United States, the FDA updated its "healthy" claim criteria in 2024, capping added sugars at 2 grams per reference amount. This change has pushed legacy isotonic and sports drinks toward reformulation and accelerated zero-sugar SKU rollouts.

In Europe, performance and wellness messaging is constrained by the EU health-claims framework, including the list of permitted claims under Regulation (EU) 432/2012, while food-information rules under Regulation (EU) No 1169/2011 (including an updated version entering into effect in 2025) set labeling compliance requirements across markets. In 2026, policy activity also points to labeling enforcement and consumer information initiatives at the European Commission level, alongside a regulatory classification shift in Canada toward treating sports drinks as foods under the Food and Drugs Act changes, which alters compliance pathways for brands operating across North America.

Competitive Landscape

The recovery drinks market exhibits moderate concentration. PepsiCo and The Coca-Cola Company bolster their market positions with zero-sugar line extensions and the rollout of 100% recycled PET packaging, reflecting their commitment to evolving consumer preferences for healthier and more sustainable options. Abbott Nutrition, drawing on its medical heritage, strategically markets its protein RTDs for clinical recovery, targeting aging consumers who seek functional beverages to support their health and wellness goals. Meanwhile, disruptors like Gainful and Transparent Labs harness subscription models and direct-to-consumer personalization, carving out lucrative niches by offering tailored solutions that cater to individual consumer needs.

Collaborations with defense research units introduce cutting-edge hydration monitoring to civilian athletes, presenting acquisition opportunities and fresh IP avenues for established players. These advancements not only enhance product offerings but also position brands as innovators in the recovery drinks market. Glanbia's breakthrough in stabilizing creatine in RTDs paves the way for a previously overlooked sub-category, addressing a long-standing challenge in the industry and unlocking new growth potential. The M&A landscape is bustling: Celsius Holdings made waves with a USD 1.8 billion acquisition of a female-centric brand, expanding its portfolio to cater to a growing demographic, and Keurig Dr Pepper secured a majority stake in a lifestyle-energy brand, broadening its recovery portfolio to diversify its market presence.

Brands are countering the margin squeeze from private-label pricing by bundling recovery drinks with complementary SKUs in loyalty initiatives. This strategy not only drives consumer retention but also boosts the overall basket value by encouraging repeat purchases and fostering brand loyalty. In today's market, sustainability measures such as recyclable aluminum, paper bottles, and refill pilots have evolved from mere add-ons to vital competitive differentiators. These initiatives reflect a proactive approach by companies to align with the growing consumer emphasis on environmentally friendly practices, which increasingly influence purchasing decisions and brand perception.

Recovery Drinks Industry Leaders

-

PepsiCo Inc.

-

Glanbia PLC

-

The Coca-Cola Company

-

Otsuka Pharmaceuticals

-

SiS(Science in Sport)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product whitespace is emerging for brands that pair hydration with recovery-adjacent benefits, such as protein intake, gut-friendly positioning, and clean-label ingredient decks, while managing sugar and claim risk under tighter regulatory boundaries. PepsiCo has already moved in this direction, introducing Propel Clear Protein and reformulating Muscle Milk to remove artificial ingredients, positioning recovery beverages for daily-use functional occasions for consumers working to hit protein targets, including those using GLP-1 medications.

Formulation approaches are also widening the ready-to-drink space beyond traditional electrolytes, particularly for performance actives that have been harder to translate into RTD formats. KA-EX launched a creatine and EAA RTD using a push-cap approach designed to protect ingredient potency until consumption, which points to routes for bringing higher-value actives into packaged recovery drinks. Ingredient cost and availability remain a practical constraint, with whey protein isolate pricing in the EU reaching around EUR 25,000/mt alongside full-capacity production conditions, increasing the emphasis on alternative proteins (plant-based blends) and on channel strategies that can support premium pricing, including subscription and direct-to-consumer bundles pairing hydration with protein RTDs.

Recent Industry Developments

- July 2026: Science in Sport launched operations in Japan, supported by a dedicated direct-to-consumer platform and a partnership with the running platform RunNet. The initiative places Japan among the priority Asian markets and localizes customer acquisition around endurance communities. It also underscores the growing role of DTC and community partnerships in scaling recovery-drink and sports-nutrition portfolios.

- June 2026: PepsiCo launched Propel Clear Protein and executed a multi-market reformulation across Muscle Milk and related recovery lines, removing artificial ingredients and aligning core SKUs with clean-label standards across North America, Europe, and APAC. The update expands protein-forward recovery formats and broadens multi-channel availability through expanded distribution and direct-to-consumer touchpoints.

- June 2025: The acquisition of Science in Sport plc by Einstein Bidco Limited (advised by bd-capital) was officially completed following court sanctioning. The transaction consolidates ownership and can accelerate international expansion and portfolio investment under a new control structure. It also reflects ongoing deal activity in performance nutrition as brands pursue scale and wider channel reach.

Research Methodology Framework and Report Scope

Segmentation Overview

-

By Type

- Carbohydrate-based

- Protein RTD

- Sport Drinks

- Electrolyte Based Drinks

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Key Questions Answered in the Report

How large is the recovery drinks market in 2026?

The recovery drinks market size is USD 31.94 billion in 2026 with a 5.72% CAGR outlook through 2031.

Which product type is growing fastest?

Protein RTD is the fastest-growing segment, forecast at a 7.12% CAGR to 2031.

Which region offers the highest growth rate?

Asia-Pacific leads with an expected 7.88% CAGR, driven by China’s fitness boom and India’s rising middle class.

How are online channels changing distribution?

E-commerce and subscription models reduce shelf-space dependence, improve personalization, and are projected to grow at 6.23% CAGR through 2031.

What years does this Recovery Drinks Market cover?

The report covers the Recovery Drinks Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Recovery Drinks Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: